knox county retirement and pension board .... for the voluntary 457 and merp plans, participants may...

TRANSCRIPT

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OTHER POST EMPLOYMENT BENEFIT AND RETIREMENT TRUST FUNDS OF

KNOX COUNTY, TENNESSEE

Knoxville, Tennessee

FINANCIAL STATEMENTS

June 30, 2017 and 2016

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OTHER POST EMPLOYMENT BENEFIT AND RETIREMENT TRUST FUNDS OF KNOX COUNTY, TENNESSEE

TABLE OF CONTENTS

Page

Number INTRODUCTORY SECTION

Roster of Board Members, Officials and Others .................................................................................................... i-ii

FINANCIAL SECTION

Independent Auditor’s Report .............................................................................................................................. 1-2

Management Discussion and Analysis ................................................................................................................ 3-8

Basic Financial Statements:

Statements of Fiduciary Net Position ............................................................................................................. 9-10

Statements of Changes in Fiduciary Net Position ........................................................................................ 11-12

Notes to the Financial Statements ............................................................................................................... 13-45

REQUIRED SUPPLEMENTARY INFORMATION SECTION

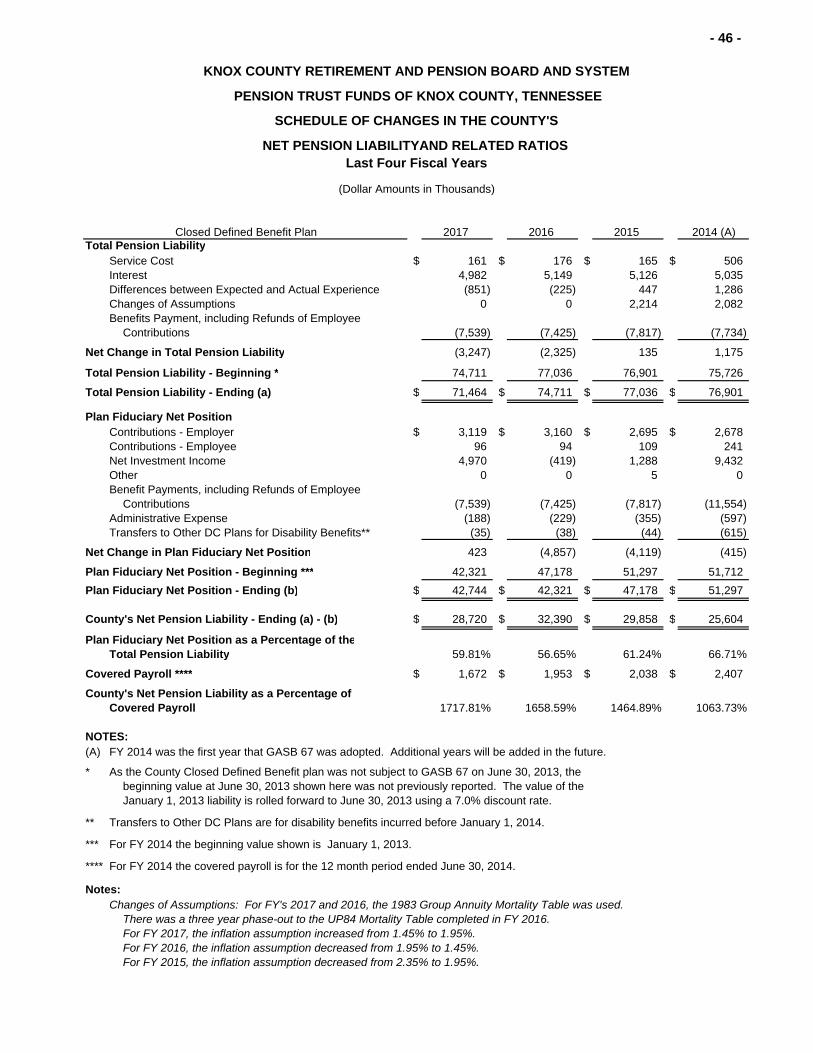

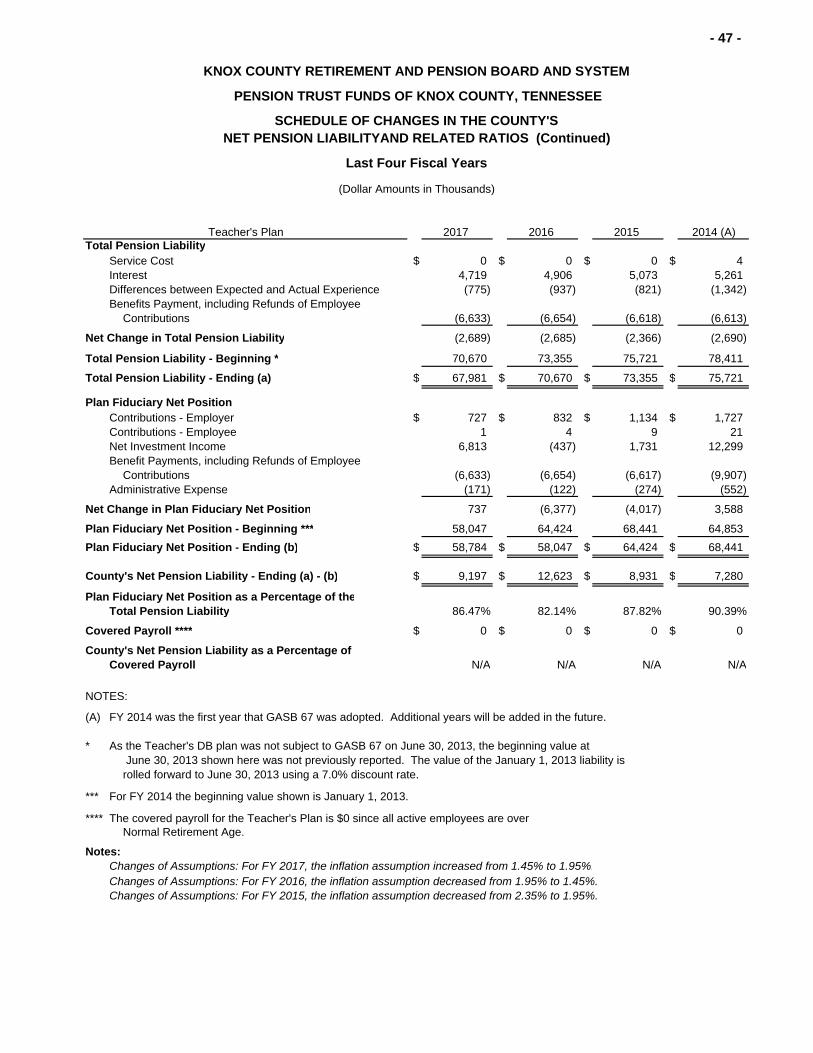

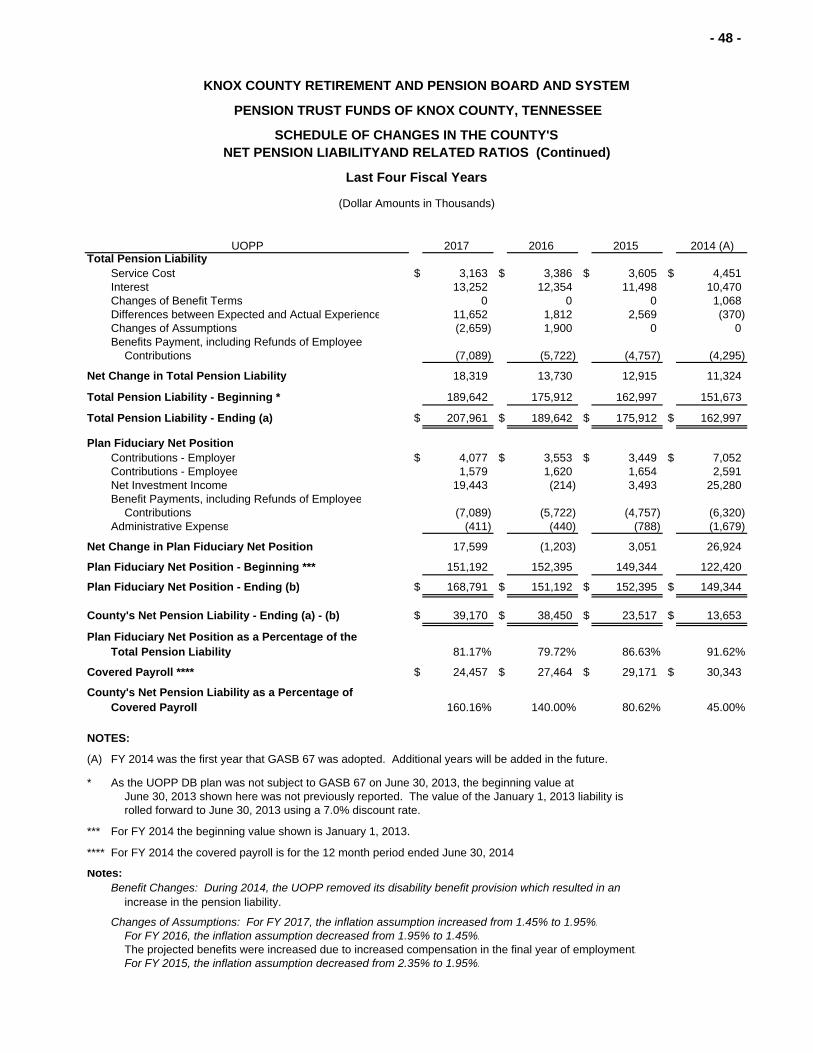

Schedule of Changes in County’s Net Pension Liability and Related Ratios .................................................. 46-48

Schedule of County’s Pension Contributions .................................................................................................. 49-51

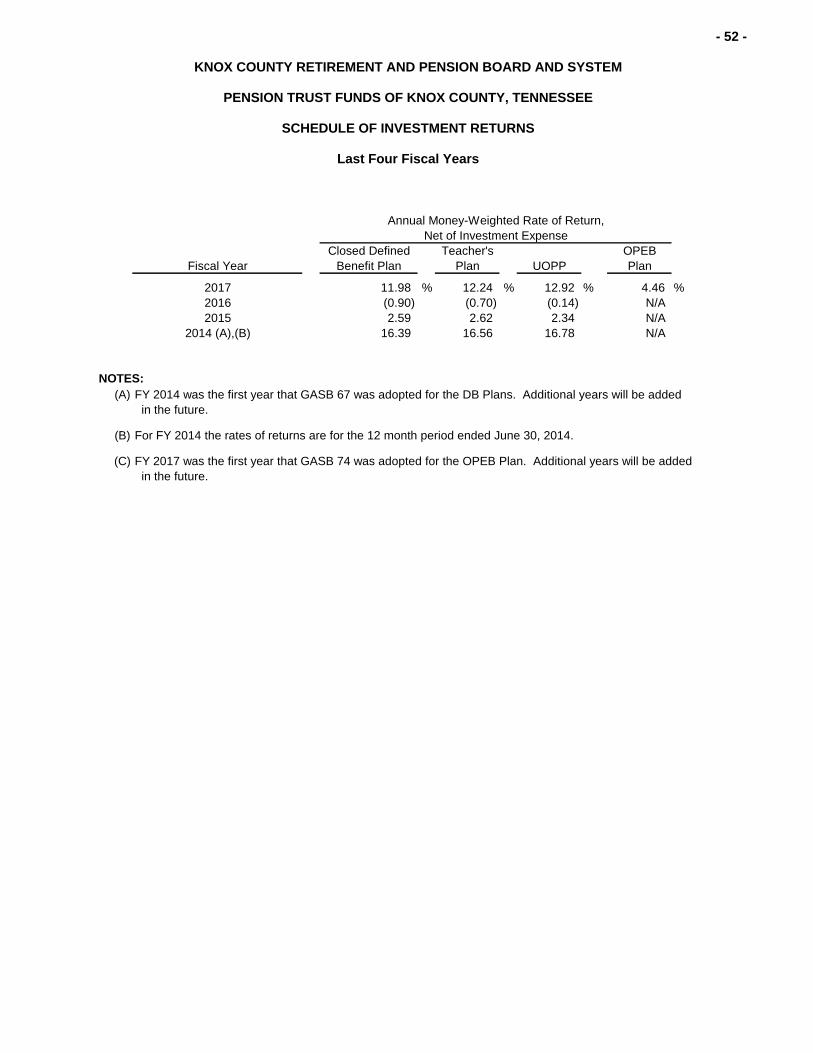

Schedule of Investment Returns .......................................................................................................................... 52

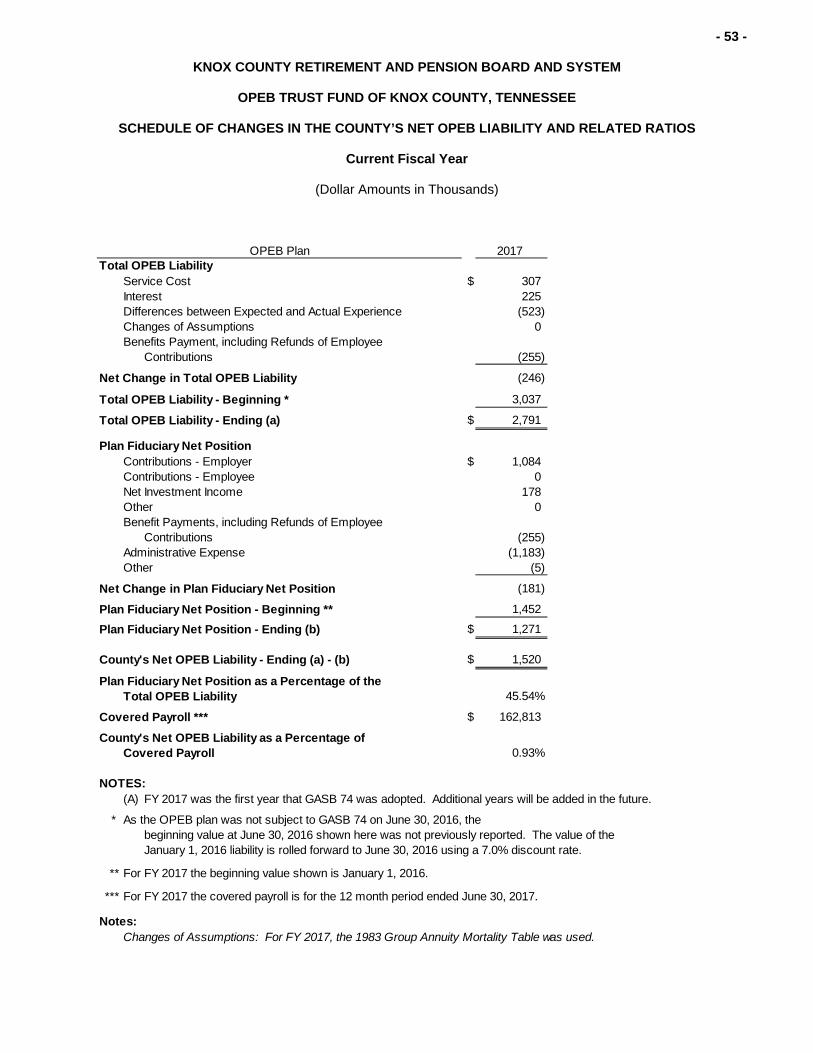

Schedule of Changes in the County’s Net OPEB Liability and Related Ratios…………………………………... .. 53

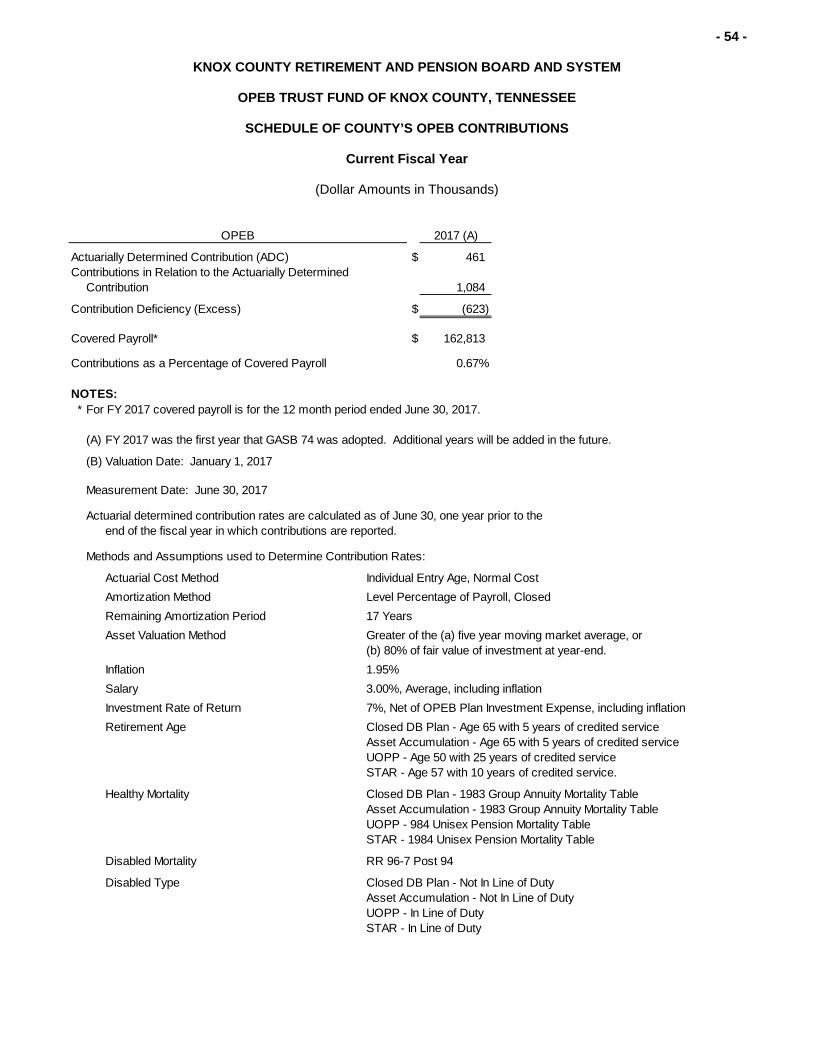

Schedule of County’s OPEB Contributions .......................................................................................................... 54

INTERNAL CONTROL AND COMPLIANCE SECTION

Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ................................................................................... 55-56

Schedule of Findings and Responses .................................................................................................................. 57

Schedule of Prior Year Findings ........................................................................................................................... 58

CORRECTIVE ACTION PLAN

Corrective Action Plan .......................................................................................................................................... 59

INTRODUCTORY SECTION

- i -

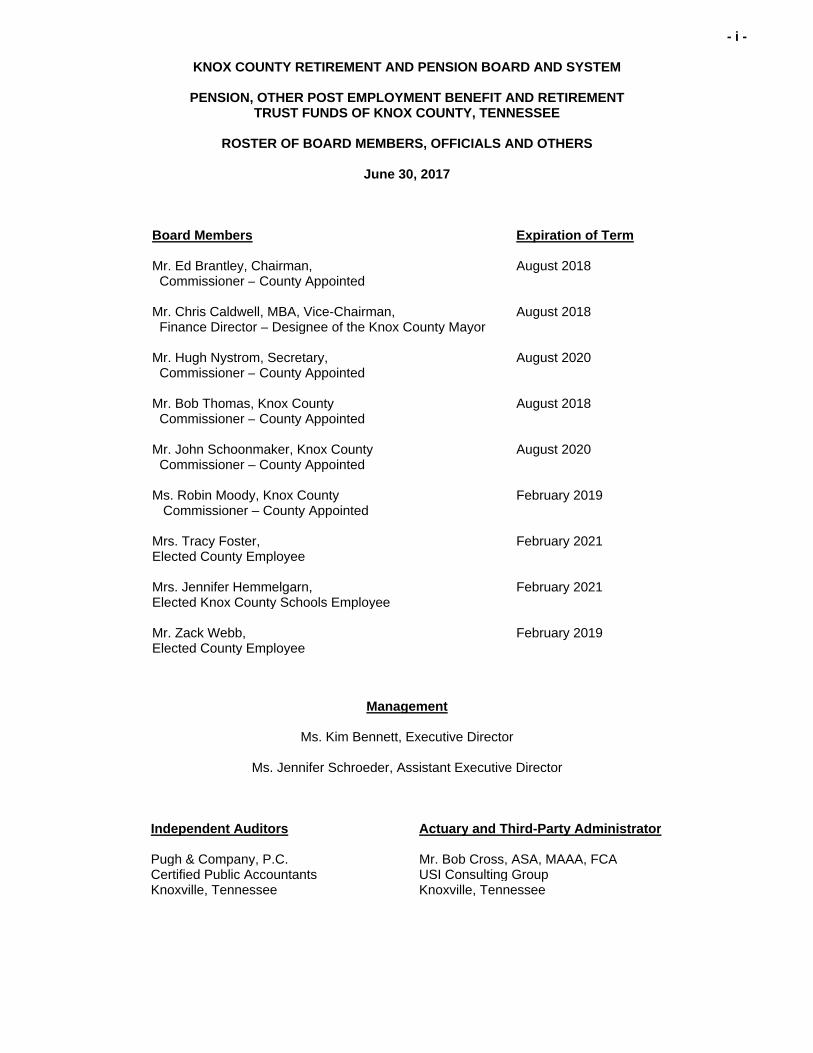

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OTHER POST EMPLOYMENT BENEFIT AND RETIREMENT TRUST FUNDS OF KNOX COUNTY, TENNESSEE

ROSTER OF BOARD MEMBERS, OFFICIALS AND OTHERS

June 30, 2017

Board Members Expiration of Term Mr. Ed Brantley, Chairman, Commissioner – County Appointed

August 2018

Mr. Chris Caldwell, MBA, Vice-Chairman, Finance Director – Designee of the Knox County Mayor

August 2018

Mr. Hugh Nystrom, Secretary, Commissioner – County Appointed

August 2020

Mr. Bob Thomas, Knox County Commissioner – County Appointed

August 2018

Mr. John Schoonmaker, Knox County Commissioner – County Appointed Ms. Robin Moody, Knox County Commissioner – County Appointed Mrs. Tracy Foster, Elected County Employee Mrs. Jennifer Hemmelgarn, Elected Knox County Schools Employee

August 2020 February 2019 February 2021 February 2021

Mr. Zack Webb, Elected County Employee

February 2019

Management

Ms. Kim Bennett, Executive Director

Ms. Jennifer Schroeder, Assistant Executive Director

Independent Auditors Actuary and Third-Party Administrator Pugh & Company, P.C. Mr. Bob Cross, ASA, MAAA, FCA Certified Public Accountants USI Consulting GroupKnoxville, Tennessee Knoxville, Tennessee

- ii -

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OTHER POST EMPLOYMENT BENEFIT AND RETIREMENT TRUST FUNDS OF KNOX COUNTY, TENNESSEE

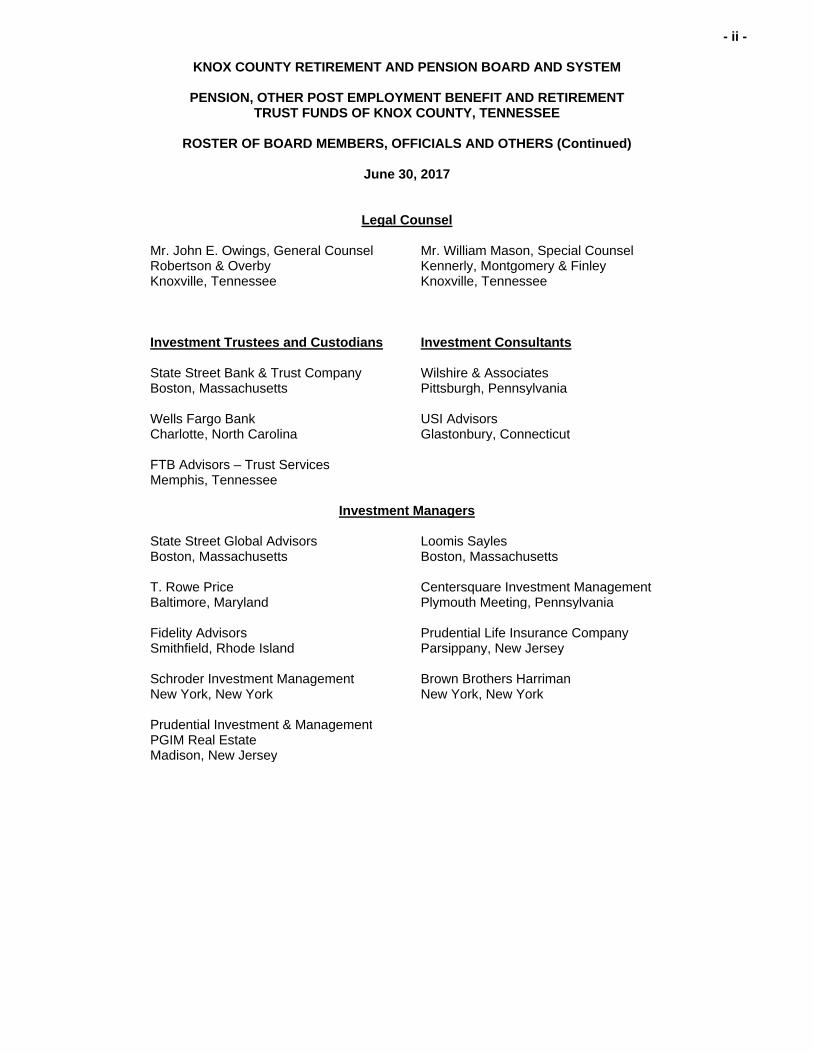

ROSTER OF BOARD MEMBERS, OFFICIALS AND OTHERS (Continued)

June 30, 2017

Legal Counsel Mr. John E. Owings, General Counsel Robertson & Overby Knoxville, Tennessee

Mr. William Mason, Special Counsel Kennerly, Montgomery & Finley Knoxville, Tennessee

Investment Trustees and Custodians Investment Consultants State Street Bank & Trust Company Boston, Massachusetts

Wilshire & Associates Pittsburgh, Pennsylvania

Wells Fargo Bank Charlotte, North Carolina

USI Advisors Glastonbury, Connecticut

FTB Advisors – Trust Services Memphis, Tennessee

Investment Managers

State Street Global Advisors Boston, Massachusetts

Loomis Sayles Boston, Massachusetts

T. Rowe Price Baltimore, Maryland

Centersquare Investment Management Plymouth Meeting, Pennsylvania

Fidelity Advisors Smithfield, Rhode Island

Prudential Life Insurance Company Parsippany, New Jersey

Schroder Investment Management New York, New York

Brown Brothers Harriman New York, New York

Prudential Investment & Management

PGIM Real Estate Madison, New Jersey

FINANCIAL SECTION

- 1 -

TSCPA

Members of the Tennessee Society Of Certified Public Accountants

RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms.

Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International.

KNOXVILLE OFFICE: OAK RIDGE OFFICE:

315 NORTH CEDAR BLUFF ROAD – SUITE 200 800 OAK RIDGE TURNPIKE – SUITE A404

KNOXVILLE, TENNESSEE 37923 OAK RIDGE, TENNESSEE 37830

TELEPHONE 865-769-0660 TELEPHONE 865-769-1657

PUGH & COMPANY, P.C.

www.pughcpas.com

INDEPENDENT AUDITOR’S REPORT Members of the Knox County Retirement and Pension Board and System Knoxville, Tennessee Report on the Financial Statements

We have audited the accompanying financial statements of the Knox County Retirement and Pension Board and System (the “System”) pension trust funds of Knox County, Tennessee, which comprise the statements of fiduciary net position as of June 30, 2017 and 2016, and the related statements of changes in fiduciary net position and related notes to the financial statements for the years then ended. Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal controls. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion.

- 2 -

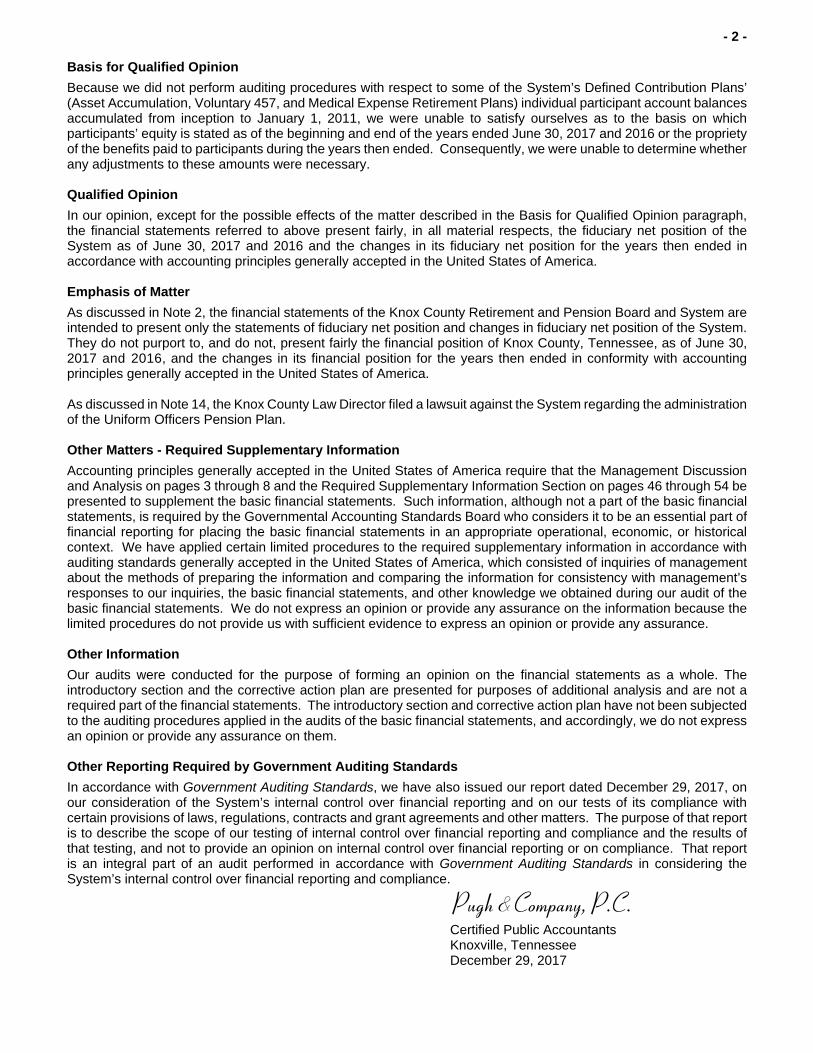

Basis for Qualified Opinion

Because we did not perform auditing procedures with respect to some of the System’s Defined Contribution Plans’ (Asset Accumulation, Voluntary 457, and Medical Expense Retirement Plans) individual participant account balances accumulated from inception to January 1, 2011, we were unable to satisfy ourselves as to the basis on which participants’ equity is stated as of the beginning and end of the years ended June 30, 2017 and 2016 or the propriety of the benefits paid to participants during the years then ended. Consequently, we were unable to determine whether any adjustments to these amounts were necessary. Qualified Opinion

In our opinion, except for the possible effects of the matter described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the fiduciary net position of the System as of June 30, 2017 and 2016 and the changes in its fiduciary net position for the years then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter

As discussed in Note 2, the financial statements of the Knox County Retirement and Pension Board and System are intended to present only the statements of fiduciary net position and changes in fiduciary net position of the System. They do not purport to, and do not, present fairly the financial position of Knox County, Tennessee, as of June 30, 2017 and 2016, and the changes in its financial position for the years then ended in conformity with accounting principles generally accepted in the United States of America. As discussed in Note 14, the Knox County Law Director filed a lawsuit against the System regarding the administration of the Uniform Officers Pension Plan. Other Matters - Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the Management Discussion and Analysis on pages 3 through 8 and the Required Supplementary Information Section on pages 46 through 54 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information

Our audits were conducted for the purpose of forming an opinion on the financial statements as a whole. The introductory section and the corrective action plan are presented for purposes of additional analysis and are not a required part of the financial statements. The introductory section and corrective action plan have not been subjected to the auditing procedures applied in the audits of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on them. Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated December 29, 2017, on our consideration of the System’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the System’s internal control over financial reporting and compliance.

Pugh &Company, P.C. Certified Public Accountants Knoxville, Tennessee December 29, 2017

- 3 -

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OTHER POST EMPLOYMENT BENEFIT AND RETIREMENT TRUST FUNDS OF KNOX COUNTY, TENNESSEE

MANAGEMENT DISCUSSION AND ANALYSIS

For the Years Ended June 30, 2017, 2016 and 2015

The accompanying financial statements of the Knox County Retirement and Pension Board and System (the “Retirement Board” and “System”) reflect the Defined Benefit (“DB Plans”), Other Post Employment Benefit (“OPEB Plan”) and Defined Contribution (“DC Plans”) Plans' investment of assets, contributions, investment results, payments of benefits and the operational expenses for the years ended June 30, 2017 and 2016. The measurement focus is to show the value and period change in the fiduciary net position restricted for pension, OPEB and retirement benefits for the employees and participants. The financial statements are prepared on the accrual basis of accounting in accordance with the Government Accounting Standards Board (GASB) pronouncements. The Plans are managed by the Knox County Retirement and Pension Board (the “Board”) and its Executive Director. The Plans cover eligible employees of Knox County, Tennessee (“County”), Knox County Board of Education (“BOE”) and certain affiliated entities. The Knox County BOE employees covered are not eligible to participate in the Tennessee Consolidated Retirement System (TCRS) Plan which covers primarily certified teachers and administrators. The U.S. national averages for defined benefit plans are from the annual report of the Funding of State and Local Pensions as published by the Center for State and Local Government Excellence as of June 2017 and 2016. Financial Highlights The System’s fiduciary net position restricted for pension, OPEB and retirement benefits as of June 30, 2017, June 30, 2016 and June 30, 2015, were $606.6 million, $546.0 million and $558.6 million, respectively. The total fiduciary net position is available to meet the System’s ongoing obligations to current Knox County and Knox County BOE employees, plan participants, retirees and their beneficiaries. The System’s fiduciary net position increased $61 million or 11.2% during the year ended June 30, 2017 due mainly to positive financial markets. For the year ended June 30, 2017, net investment gain was $66.6 million, contributions were $35.1 million and benefits paid were $38.5 million. The System’s fiduciary net position decreased $12.6 million or (2.2)% during the year ended June 30, 2016 due mainly to negative financial markets. For the year ended June 30, 2016, net investment income (loss) was $(2.8) million, contributions were $31.9 million and benefits paid were $40.2 million. The System’s fiduciary net position decreased $0.9 million or less than 1% during the year ended June 30, 2015 due mainly to benefits payments being approximately equal to investment income and contributions for the year. For the year ended June 30, 2015, net investment income was $16.1 million, contributions were $30.1 million and benefits paid were $45.7 million. Additions to total net plan position for the year-end June 30, 2017 included employer contributions of $20.1 million, employee contributions of $13.9 million, and employee rollover contributions of $1.1 million for a total of $35.1 million. Additions to total net plan position for the year-end June 30, 2016 included employer contributions of $18.6 million, employee contributions of $12.6 million, and employee rollover contributions of $713,456 for a total of $31.9 million. Additions to total net plan position for the year-end June 30, 2015 included employer contributions of $17.8 million, employee contributions of $12.1 million, and employee rollover contributions of $148,831 for a total of $30.1 million.

- 4 -

Financial Highlights (Continued) Deductions from fiduciary net position for the year-end June 30, 2017 were $41.9 million, a decrease of $500 thousand from the year-end June 30, 2016 due to decrease in benefits paid in 2017. Administrative expenses and transfers to other plans were up $1.1 million during the year ended June 30, 2017. Deductions from fiduciary net position for the year-end June 30, 2016 were $42.4 million, a decrease of $5.5 million from the year ended June 30, 2015 due to a decrease in benefits paid in 2016. Administrative expenses and transfers to other plans remained flat during the year ended June 30, 2016. Deductions from fiduciary net position for the year-end June 30, 2015 were $47.9 million, an increase of $25.9 million from the six-month period ended June 30, 2014 due to an increase in benefits paid in 2015. Administrative expenses increased $1.0 million in 2014 to $1.6 million during the year ended June 30, 2015. These increases were due to the comparisons of an annual twelve-month period in 2015 to a six-month period in 2014. Overview of the Financial Statements The following discussion and analysis is intended to serve as an introduction to the System’s financial statements which follow. The financial statements report information about the System using full accrual accounting methods, and reporting investments at fair value as required by the GASB and include the following:

Management Discussion and Analysis

Statements of Fiduciary Net Position

Statements of Changes in Fiduciary Net Position

Notes to the Financial Statements

Required Supplementary Information

Internal Control and Compliance Section Management’s Discussion and Analysis (MD&A) serves as the introduction to the basic financial statements and represents management’s analysis of the System’s financial condition and performance. Summary financial data and other key indicators used in the System’s operations of the Plans and other management information were used for this analysis. The Statements of Fiduciary Net Position are a snapshot of account balances at period, or year-end. They indicate the assets available for future payments to retirees and any current liabilities. The Statements of Changes in Fiduciary Net Position show the additions and deductions from the System’s assets over the current period/year. Notes to the financial statements provide additional information which is essential for a full understanding of the data provided in the basic financial statements. Required Supplementary Information (RSI) provides additional information and details about the System’s progress in the County’s net pension liabilities, funding its future obligations, history of County contributions and investment returns of the defined benefit plans. Also, RSI provides the funded status and contributions of the OPEB – Employee Disability Plan. The Internal Control and Compliance Section include the independent auditor’s report on the System’s internal controls and compliance in accordance with Government Auditing Standards.

- 5 -

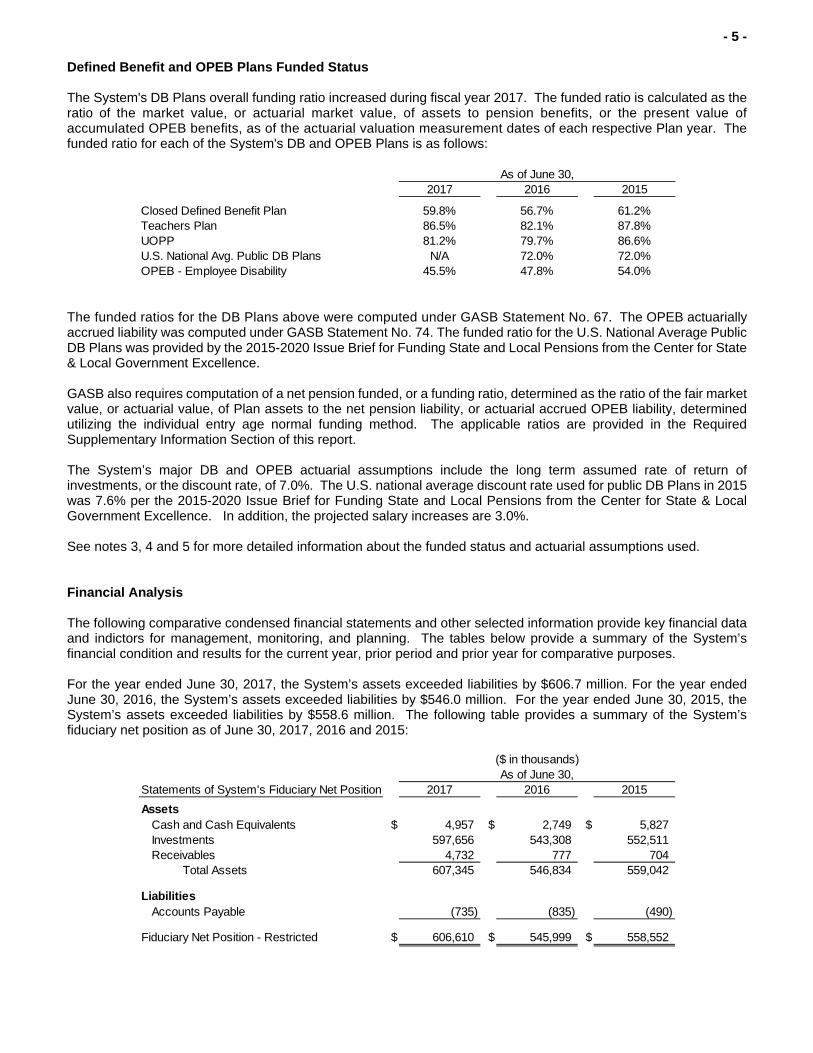

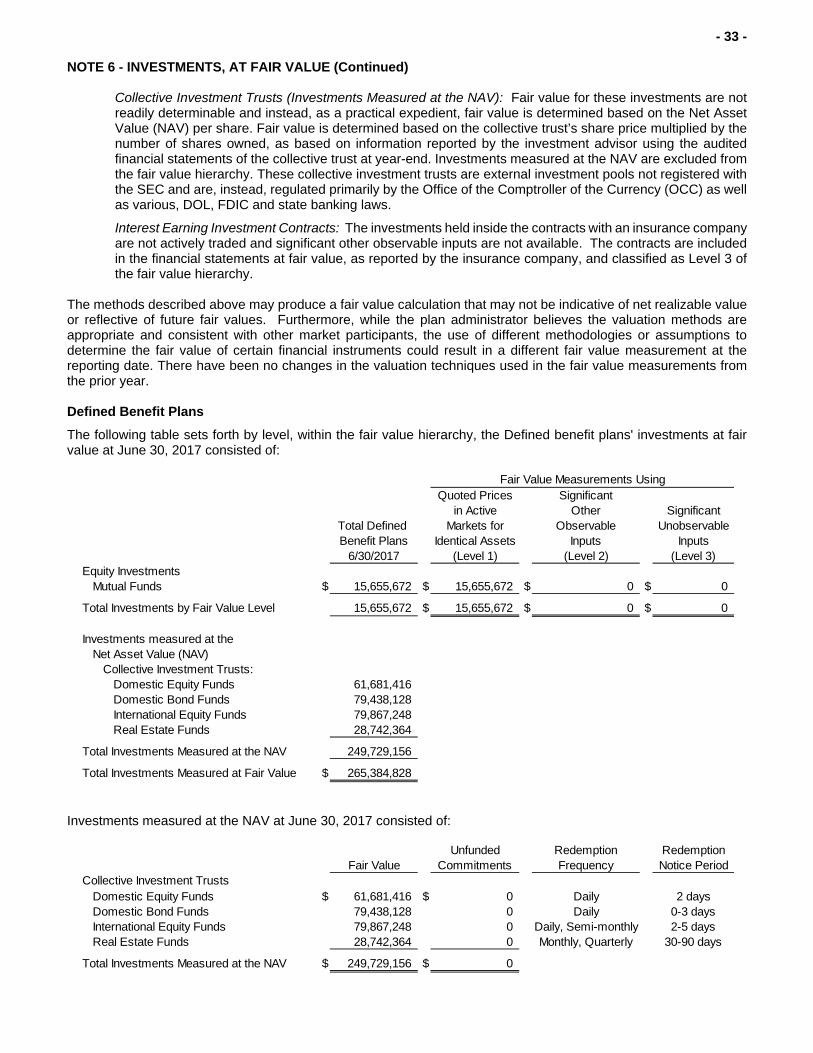

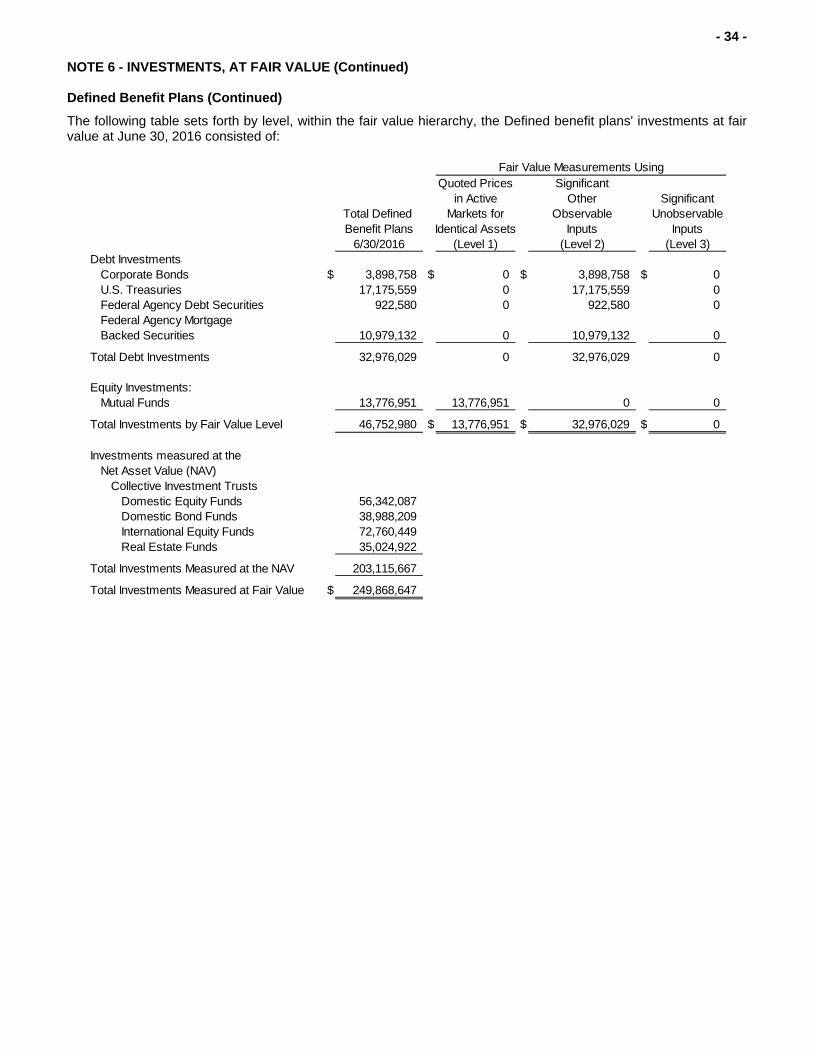

Defined Benefit and OPEB Plans Funded Status The System's DB Plans overall funding ratio increased during fiscal year 2017. The funded ratio is calculated as the ratio of the market value, or actuarial market value, of assets to pension benefits, or the present value of accumulated OPEB benefits, as of the actuarial valuation measurement dates of each respective Plan year. The funded ratio for each of the System's DB and OPEB Plans is as follows:

2017 2016 2015

Closed Defined Benefit Plan 59.8% 56.7% 61.2%Teachers Plan 86.5% 82.1% 87.8%UOPP 81.2% 79.7% 86.6%U.S. National Avg. Public DB Plans N/A 72.0% 72.0%OPEB - Employee Disability 45.5% 47.8% 54.0%

As of June 30,

The funded ratios for the DB Plans above were computed under GASB Statement No. 67. The OPEB actuarially accrued liability was computed under GASB Statement No. 74. The funded ratio for the U.S. National Average Public DB Plans was provided by the 2015-2020 Issue Brief for Funding State and Local Pensions from the Center for State & Local Government Excellence. GASB also requires computation of a net pension funded, or a funding ratio, determined as the ratio of the fair market value, or actuarial value, of Plan assets to the net pension liability, or actuarial accrued OPEB liability, determined utilizing the individual entry age normal funding method. The applicable ratios are provided in the Required Supplementary Information Section of this report. The System’s major DB and OPEB actuarial assumptions include the long term assumed rate of return of investments, or the discount rate, of 7.0%. The U.S. national average discount rate used for public DB Plans in 2015 was 7.6% per the 2015-2020 Issue Brief for Funding State and Local Pensions from the Center for State & Local Government Excellence. In addition, the projected salary increases are 3.0%. See notes 3, 4 and 5 for more detailed information about the funded status and actuarial assumptions used. Financial Analysis The following comparative condensed financial statements and other selected information provide key financial data and indictors for management, monitoring, and planning. The tables below provide a summary of the System’s financial condition and results for the current year, prior period and prior year for comparative purposes. For the year ended June 30, 2017, the System’s assets exceeded liabilities by $606.7 million. For the year ended June 30, 2016, the System’s assets exceeded liabilities by $546.0 million. For the year ended June 30, 2015, the System’s assets exceeded liabilities by $558.6 million. The following table provides a summary of the System’s fiduciary net position as of June 30, 2017, 2016 and 2015:

Statements of System's Fiduciary Net Position 2017 2016 2015

AssetsCash and Cash Equivalents $ 4,957 $ 2,749 $ 5,827Investments 597,656 543,308 552,511Receivables 4,732 777 704

Total Assets 607,345 546,834 559,042

LiabilitiesAccounts Payable (735) (835) (490)

Fiduciary Net Position - Restricted $ 606,610 $ 545,999 $ 558,552

($ in thousands)As of June 30,

- 6 -

Financial Analysis (Continued) The following table provides a summary of the changes in fiduciary net position for the years ended June 30, 2017, 2016 and 2015 :

Statements of Changes in System's Fiduciary Net Position 2017 2016 2015

AdditionsNet Investment Income (Loss) $ 66,635 $ (2,777) $ 16,145Interest on Notes Receivable 85 0 0Participant's Contributions 13,886 12,603 12,090Employer Contributions 20,078 18,626 17,896Rollover Contributions 1,094 713 149Transfers In from Other Plans 736 694 617Other 0 0 5

Total Additions 102,514 29,859 46,902

DeductionsBenefits Paid 39,198 40,151 45,657Administrative Expenses 1,970 1,565 1,605Transfers to Other Plans 735 694 617

Total Deductions 41,903 42,410 47,879

Change in Fiduciary Net Position $ 60,611 $ (12,551) $ (977)

For the Years Ended June 30,($ in thousands)

County Employer Contributions The County’s employer contributions increased by $1.5 million during the year ended June 30, 2017, of which $0.3 million was for the DB plans and $1.2 million was for the DC plans. These increases were attributed mainly to normal plan activity. The County’s employer matching contribution percentages did not change for any of the DC Plans during the year ended June 30, 2017. The County’s employer contributions increased by $0.7 million during the year ended June 30, 2016, of which $0.3 million was for the DB plans and $0.4 million was for the DC plans. These increases were attributed mainly to normal plan activity. The County’s employer matching contribution percentages did not change for any of the DC Plans during the year ended June 30, 2016. The County’s employer contributions increased by $10.8 million during the year ended June 30, 2015, of which $4.8 million was for the DB plans. Knox County increased its employer contributions to the Closed Defined Benefit Plan by $2.5 million, the Teacher’s Plan by $1.1 million and the UOPP by $1.1 million for the year ended June 30, 2015 when compared to the six-month period ended June 30, 2014. The increases in the DB employer contributions were due to the comparison of an annual period to a six-month period. The employer matching contribution percentage for the Medical Expense Retirement Plan (MERP) increased to a 50% match with a maximum match of $208 per participant during the year ended June 30, 2015. All other DC employer matching contribution percentages did not change during the year ended June 30, 2015.

- 7 -

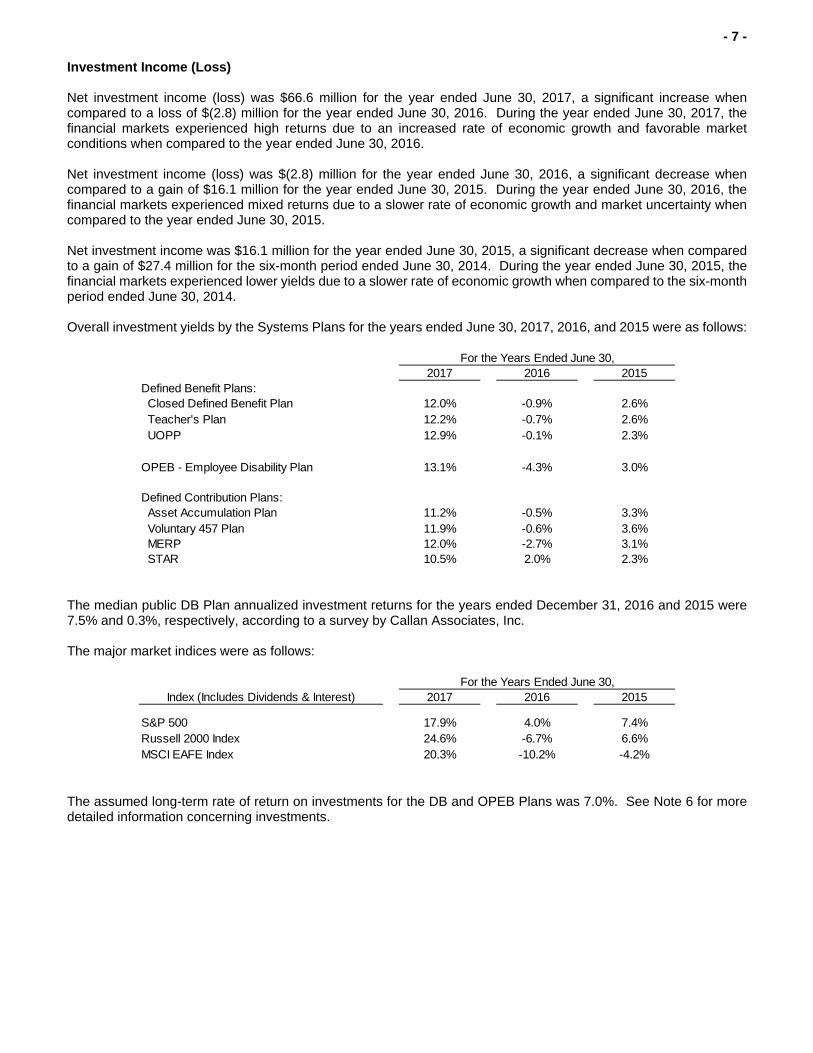

Investment Income (Loss) Net investment income (loss) was $66.6 million for the year ended June 30, 2017, a significant increase when compared to a loss of $(2.8) million for the year ended June 30, 2016. During the year ended June 30, 2017, the financial markets experienced high returns due to an increased rate of economic growth and favorable market conditions when compared to the year ended June 30, 2016. Net investment income (loss) was $(2.8) million for the year ended June 30, 2016, a significant decrease when compared to a gain of $16.1 million for the year ended June 30, 2015. During the year ended June 30, 2016, the financial markets experienced mixed returns due to a slower rate of economic growth and market uncertainty when compared to the year ended June 30, 2015. Net investment income was $16.1 million for the year ended June 30, 2015, a significant decrease when compared to a gain of $27.4 million for the six-month period ended June 30, 2014. During the year ended June 30, 2015, the financial markets experienced lower yields due to a slower rate of economic growth when compared to the six-month period ended June 30, 2014. Overall investment yields by the Systems Plans for the years ended June 30, 2017, 2016, and 2015 were as follows:

2017 2016 2015Defined Benefit Plans: Closed Defined Benefit Plan 12.0% -0.9% 2.6% Teacher's Plan 12.2% -0.7% 2.6% UOPP 12.9% -0.1% 2.3%

OPEB - Employee Disability Plan 13.1% -4.3% 3.0%

Defined Contribution Plans: Asset Accumulation Plan 11.2% -0.5% 3.3% Voluntary 457 Plan 11.9% -0.6% 3.6% MERP 12.0% -2.7% 3.1% STAR 10.5% 2.0% 2.3%

For the Years Ended June 30,

The median public DB Plan annualized investment returns for the years ended December 31, 2016 and 2015 were 7.5% and 0.3%, respectively, according to a survey by Callan Associates, Inc. The major market indices were as follows:

2017 2016 2015

S&P 500 17.9% 4.0% 7.4%Russell 2000 Index 24.6% -6.7% 6.6%MSCI EAFE Index 20.3% -10.2% -4.2%

Index (Includes Dividends & Interest)For the Years Ended June 30,

The assumed long-term rate of return on investments for the DB and OPEB Plans was 7.0%. See Note 6 for more detailed information concerning investments.

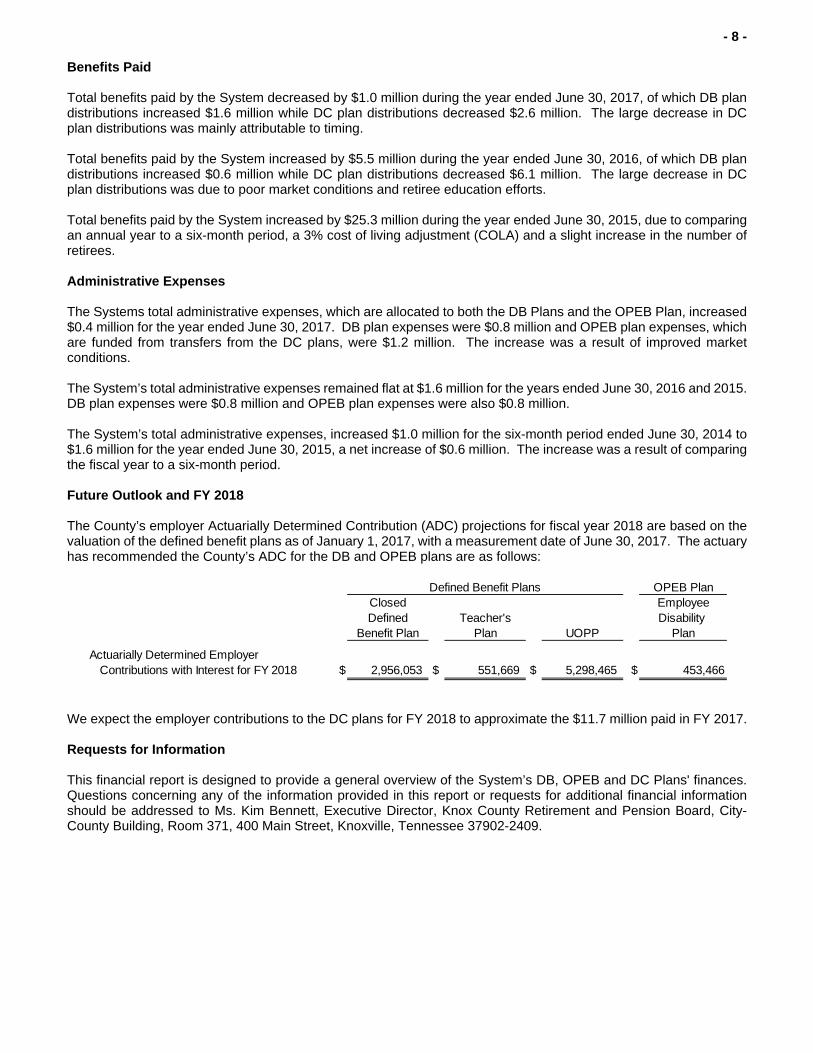

- 8 -

Benefits Paid Total benefits paid by the System decreased by $1.0 million during the year ended June 30, 2017, of which DB plan distributions increased $1.6 million while DC plan distributions decreased $2.6 million. The large decrease in DC plan distributions was mainly attributable to timing. Total benefits paid by the System increased by $5.5 million during the year ended June 30, 2016, of which DB plan distributions increased $0.6 million while DC plan distributions decreased $6.1 million. The large decrease in DC plan distributions was due to poor market conditions and retiree education efforts. Total benefits paid by the System increased by $25.3 million during the year ended June 30, 2015, due to comparing an annual year to a six-month period, a 3% cost of living adjustment (COLA) and a slight increase in the number of retirees. Administrative Expenses The Systems total administrative expenses, which are allocated to both the DB Plans and the OPEB Plan, increased $0.4 million for the year ended June 30, 2017. DB plan expenses were $0.8 million and OPEB plan expenses, which are funded from transfers from the DC plans, were $1.2 million. The increase was a result of improved market conditions. The System’s total administrative expenses remained flat at $1.6 million for the years ended June 30, 2016 and 2015. DB plan expenses were $0.8 million and OPEB plan expenses were also $0.8 million. The System’s total administrative expenses, increased $1.0 million for the six-month period ended June 30, 2014 to $1.6 million for the year ended June 30, 2015, a net increase of $0.6 million. The increase was a result of comparing the fiscal year to a six-month period. Future Outlook and FY 2018 The County’s employer Actuarially Determined Contribution (ADC) projections for fiscal year 2018 are based on the valuation of the defined benefit plans as of January 1, 2017, with a measurement date of June 30, 2017. The actuary has recommended the County’s ADC for the DB and OPEB plans are as follows:

OPEB PlanClosed EmployeeDefined Teacher's Disability

Benefit Plan Plan UOPP Plan

Actuarially Determined EmployerContributions with Interest for FY 2018 $ 2,956,053 $ 551,669 $ 5,298,465 $ 453,466

Defined Benefit Plans

We expect the employer contributions to the DC plans for FY 2018 to approximate the $11.7 million paid in FY 2017. Requests for Information This financial report is designed to provide a general overview of the System’s DB, OPEB and DC Plans' finances. Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to Ms. Kim Bennett, Executive Director, Knox County Retirement and Pension Board, City-County Building, Room 371, 400 Main Street, Knoxville, Tennessee 37902-2409.

OPEB PlanClosed Uniformed Total Medical Sheriff's Total Total Defined Officers Defined Employee Asset Expense Accumulation DefinedBenefit Teacher's Pension Benefit Disability Accumulation Voluntary Retirement Retirement Contribution

Plan Plan Plan Plans Plan Plan 457 Plan Plan Plan Plans TotalASSETS

Cash and Cash Equivalents $ 687,713 $ 945,462 $ 3,109,002 $ 4,742,177 $ 0 $ 152,407 $ 0 $ 0 $ 62,603 $ 215,010 $ 4,957,187

Investments, at Fair ValueMutual Funds 2,230,647 3,067,790 10,357,235 15,655,672 874,981 227,378,245 15,593,838 4,065,421 1,666,787 248,704,291 265,234,944Interest-Earning Investment Contracts 0 0 0 0 268,651 50,028,533 2,412,569 385,992 615,583 53,442,677 53,711,328Collective Investment Trusts 39,675,667 54,565,602 155,487,887 249,729,156 82,707 8,582,760 694,216 1,254,331 53,748 10,585,055 260,396,918

Total Investments at Fair Value 41,906,314 57,633,392 165,845,122 265,384,828 1,226,339 285,989,538 18,700,623 5,705,744 2,336,118 312,732,023 579,343,190

Investments, at Contract ValueGuaranteed Investment Contract 0 0 0 0 0 17,022,236 1,290,142 0 0 18,312,378 18,312,378

Total Investments 41,906,314 57,633,392 165,845,122 265,384,828 1,226,339 303,011,774 19,990,765 5,705,744 2,336,118 331,044,401 597,655,568

ReceivablesParticipant's Contributions 2,624 0 58,099 60,723 0 240,503 129,724 10,160 18,322 398,709 459,432Employer Contributions 0 0 108 108 0 308,406 0 0 36,643 345,049 345,157Accrued Interest and Dividends 829 1,140 3,755 5,724 0 31,161 0 0 0 31,161 36,885Receivable from Other Plans 0 0 0 0 202,803 0 0 0 0 0 202,803Receivable for Investments Sold 210,500 289,500 0 500,000 0 0 0 0 0 0 500,000Notes Receivable from Participants 0 0 0 0 0 3,187,274 0 0 0 3,187,274 3,187,274

Total Receivables 213,953 290,640 61,962 566,555 202,803 3,767,344 129,724 10,160 54,965 3,962,193 4,731,551

Total Assets 42,807,980 58,869,494 169,016,086 270,693,560 1,429,142 306,931,525 20,120,489 5,715,904 2,453,686 335,221,604 607,344,306

LIABILITIES

Accounts Payable - Administrative Expenses (63,757) (84,716) (224,777) (373,250) (158,586) 0 0 0 0 0 (531,836)Accounts Payable - to Other Plans 0 0 0 0 0 (140,199) 0 0 (62,603) (202,802) (202,802)

Total Liabilities (63,757) (84,716) (224,777) (373,250) (158,586) (140,199) 0 0 (62,603) (202,802) (734,638)

NET POSITION - RESTRICTED FOR PENSION, OPEB, AND

RETIREMENT BENEFITS $ 42,744,223 $ 58,784,778 $ 168,791,309 $ 270,320,310 $ 1,270,556 $ 306,791,326 $ 20,120,489 $ 5,715,904 $ 2,391,083 $ 335,018,802 $ 606,609,668

Defined Benefit Plans Defined Contribution Plans

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OPEB, AND RETIREMENTTRUST FUNDS OF KNOX COUNTY, TENNESSEE

STATEMENTS OF FIDUCIARY NET POSITION

June 30, 2017

-9

-

The accompanying notes are an integral part of these financial statements.

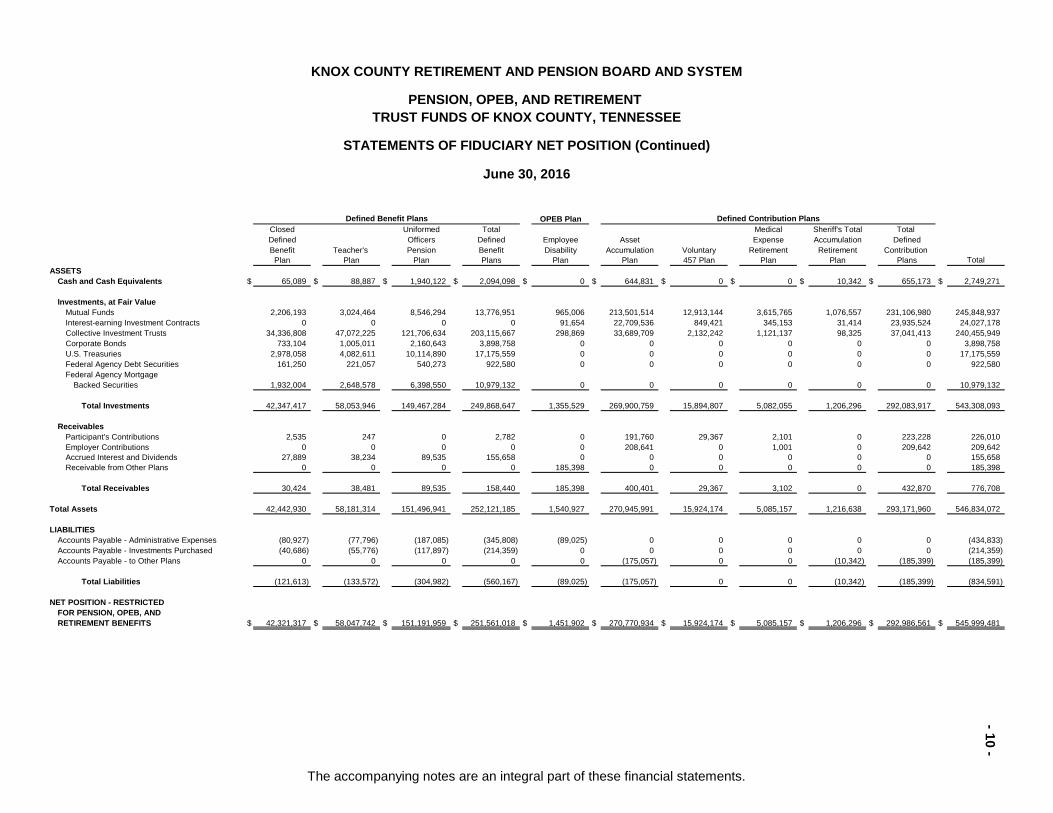

OPEB PlanClosed Uniformed Total Medical Sheriff's Total Total Defined Officers Defined Employee Asset Expense Accumulation DefinedBenefit Teacher's Pension Benefit Disability Accumulation Voluntary Retirement Retirement Contribution

Plan Plan Plan Plans Plan Plan 457 Plan Plan Plan Plans TotalASSETS

Cash and Cash Equivalents $ 65,089 $ 88,887 $ 1,940,122 $ 2,094,098 $ 0 $ 644,831 $ 0 $ 0 $ 10,342 $ 655,173 $ 2,749,271

Investments, at Fair ValueMutual Funds 2,206,193 3,024,464 8,546,294 13,776,951 965,006 213,501,514 12,913,144 3,615,765 1,076,557 231,106,980 245,848,937Interest-earning Investment Contracts 0 0 0 0 91,654 22,709,536 849,421 345,153 31,414 23,935,524 24,027,178Collective Investment Trusts 34,336,808 47,072,225 121,706,634 203,115,667 298,869 33,689,709 2,132,242 1,121,137 98,325 37,041,413 240,455,949Corporate Bonds 733,104 1,005,011 2,160,643 3,898,758 0 0 0 0 0 0 3,898,758U.S. Treasuries 2,978,058 4,082,611 10,114,890 17,175,559 0 0 0 0 0 0 17,175,559Federal Agency Debt Securities 161,250 221,057 540,273 922,580 0 0 0 0 0 0 922,580Federal Agency Mortgage Backed Securities 1,932,004 2,648,578 6,398,550 10,979,132 0 0 0 0 0 0 10,979,132

Total Investments 42,347,417 58,053,946 149,467,284 249,868,647 1,355,529 269,900,759 15,894,807 5,082,055 1,206,296 292,083,917 543,308,093

ReceivablesParticipant's Contributions 2,535 247 0 2,782 0 191,760 29,367 2,101 0 223,228 226,010Employer Contributions 0 0 0 0 0 208,641 0 1,001 0 209,642 209,642Accrued Interest and Dividends 27,889 38,234 89,535 155,658 0 0 0 0 0 0 155,658Receivable from Other Plans 0 0 0 0 185,398 0 0 0 0 0 185,398

Total Receivables 30,424 38,481 89,535 158,440 185,398 400,401 29,367 3,102 0 432,870 776,708

Total Assets 42,442,930 58,181,314 151,496,941 252,121,185 1,540,927 270,945,991 15,924,174 5,085,157 1,216,638 293,171,960 546,834,072

LIABILITIESAccounts Payable - Administrative Expenses (80,927) (77,796) (187,085) (345,808) (89,025) 0 0 0 0 0 (434,833)Accounts Payable - Investments Purchased (40,686) (55,776) (117,897) (214,359) 0 0 0 0 0 0 (214,359)Accounts Payable - to Other Plans 0 0 0 0 0 (175,057) 0 0 (10,342) (185,399) (185,399)

Total Liabilities (121,613) (133,572) (304,982) (560,167) (89,025) (175,057) 0 0 (10,342) (185,399) (834,591)

NET POSITION - RESTRICTED FOR PENSION, OPEB, AND

RETIREMENT BENEFITS $ 42,321,317 $ 58,047,742 $ 151,191,959 $ 251,561,018 $ 1,451,902 $ 270,770,934 $ 15,924,174 $ 5,085,157 $ 1,206,296 $ 292,986,561 $ 545,999,481

Defined Benefit Plans Defined Contribution Plans

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

STATEMENTS OF FIDUCIARY NET POSITION (Continued)

June 30, 2016

PENSION, OPEB, AND RETIREMENT TRUST FUNDS OF KNOX COUNTY, TENNESSEE

-1

0 -

The accompanying notes are an integral part of these financial statements.

OPEB PlanClosed Uniformed Total Medical Sheriff's Total Total Defined Officers Defined Employee Asset Expense Accumulation DefinedBenefit Teacher's Pension Benefit Disability Accumulation Voluntary Retirement Retirement Contribution

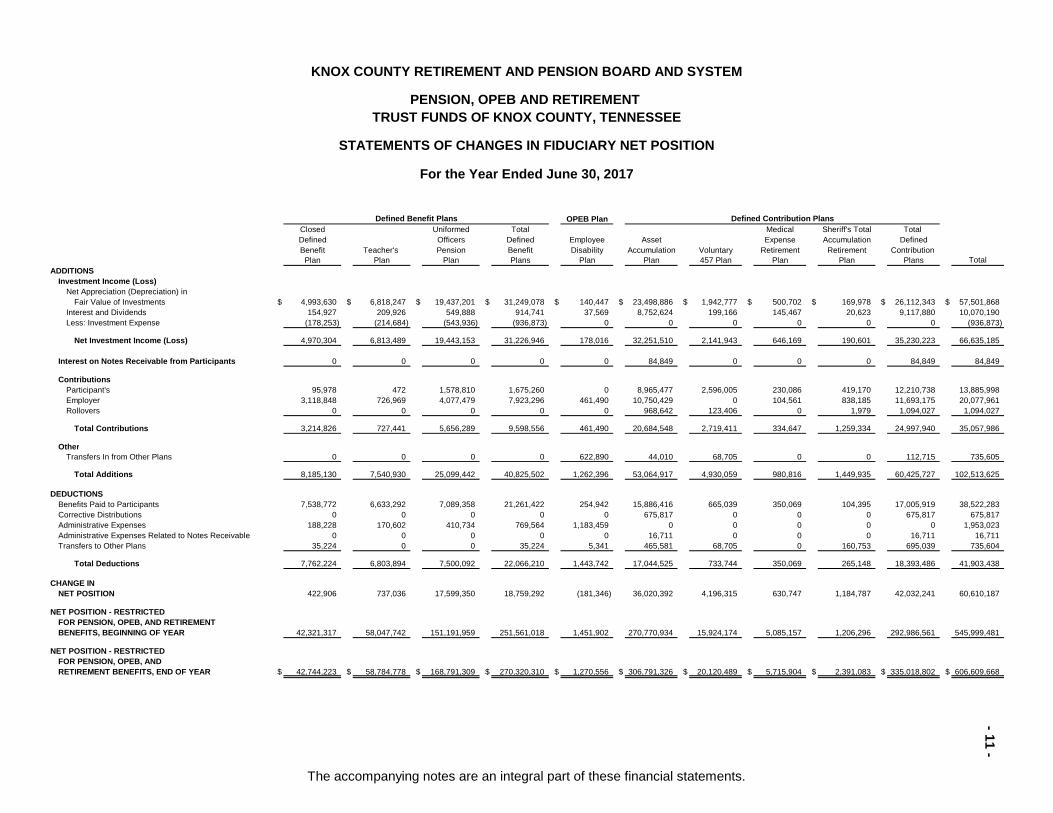

Plan Plan Plan Plans Plan Plan 457 Plan Plan Plan Plans TotalADDITIONS

Investment Income (Loss)Net Appreciation (Depreciation) in Fair Value of Investments $ 4,993,630 $ 6,818,247 $ 19,437,201 $ 31,249,078 $ 140,447 $ 23,498,886 $ 1,942,777 $ 500,702 $ 169,978 $ 26,112,343 $ 57,501,868Interest and Dividends 154,927 209,926 549,888 914,741 37,569 8,752,624 199,166 145,467 20,623 9,117,880 10,070,190Less: Investment Expense (178,253) (214,684) (543,936) (936,873) 0 0 0 0 0 0 (936,873)

Net Investment Income (Loss) 4,970,304 6,813,489 19,443,153 31,226,946 178,016 32,251,510 2,141,943 646,169 190,601 35,230,223 66,635,185

Interest on Notes Receivable from Participants 0 0 0 0 0 84,849 0 0 0 84,849 84,849

ContributionsParticipant's 95,978 472 1,578,810 1,675,260 0 8,965,477 2,596,005 230,086 419,170 12,210,738 13,885,998Employer 3,118,848 726,969 4,077,479 7,923,296 461,490 10,750,429 0 104,561 838,185 11,693,175 20,077,961Rollovers 0 0 0 0 0 968,642 123,406 0 1,979 1,094,027 1,094,027

Total Contributions 3,214,826 727,441 5,656,289 9,598,556 461,490 20,684,548 2,719,411 334,647 1,259,334 24,997,940 35,057,986

OtherTransfers In from Other Plans 0 0 0 0 622,890 44,010 68,705 0 0 112,715 735,605

Total Additions 8,185,130 7,540,930 25,099,442 40,825,502 1,262,396 53,064,917 4,930,059 980,816 1,449,935 60,425,727 102,513,625

DEDUCTIONSBenefits Paid to Participants 7,538,772 6,633,292 7,089,358 21,261,422 254,942 15,886,416 665,039 350,069 104,395 17,005,919 38,522,283Corrective Distributions 0 0 0 0 0 675,817 0 0 0 675,817 675,817Administrative Expenses 188,228 170,602 410,734 769,564 1,183,459 0 0 0 0 0 1,953,023Administrative Expenses Related to Notes Receivable 0 0 0 0 0 16,711 0 0 0 16,711 16,711Transfers to Other Plans 35,224 0 0 35,224 5,341 465,581 68,705 0 160,753 695,039 735,604

Total Deductions 7,762,224 6,803,894 7,500,092 22,066,210 1,443,742 17,044,525 733,744 350,069 265,148 18,393,486 41,903,438

CHANGE INNET POSITION 422,906 737,036 17,599,350 18,759,292 (181,346) 36,020,392 4,196,315 630,747 1,184,787 42,032,241 60,610,187

NET POSITION - RESTRICTED FOR PENSION, OPEB, AND RETIREMENT BENEFITS, BEGINNING OF YEAR 42,321,317 58,047,742 151,191,959 251,561,018 1,451,902 270,770,934 15,924,174 5,085,157 1,206,296 292,986,561 545,999,481

NET POSITION - RESTRICTED FOR PENSION, OPEB, AND RETIREMENT BENEFITS, END OF YEAR $ 42,744,223 $ 58,784,778 $ 168,791,309 $ 270,320,310 $ 1,270,556 $ 306,791,326 $ 20,120,489 $ 5,715,904 $ 2,391,083 $ 335,018,802 $ 606,609,668

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OPEB AND RETIREMENT TRUST FUNDS OF KNOX COUNTY, TENNESSEE

Defined Benefit Plans Defined Contribution Plans

STATEMENTS OF CHANGES IN FIDUCIARY NET POSITION

For the Year Ended June 30, 2017

-1

1 -

The accompanying notes are an integral part of these financial statements.

OPEB PlanClosed Uniformed Total Medical Sheriff's Total Total Defined Officers Defined Employee Asset Expense Accumulation DefinedBenefit Teacher's Pension Benefit Disability Accumulation Voluntary Retirement Retirement Contribution

Plan Plan Plan Plans Plan Plan 457 Plan Plan Plan Plans TotalADDITIONS

Investment Income (Loss)Net Appreciation (Depreciation) in Fair Value of Investments $ (439,916) $ (483,914) $ (535,422) $ (1,459,252) $ (122,075) $ (4,436,701) $ (265,205) $ (221,795) $ 13,889 $ (4,909,812) $ (6,491,139)Interest and Dividends 286,433 387,093 975,508 1,649,034 61,327 3,000,424 167,034 83,283 11,484 3,262,225 4,972,586Less: Investment Expense (265,586) (339,930) (653,632) (1,259,148) 0 0 0 0 0 0 (1,259,148)

Net Investment Income (Loss) (419,069) (436,751) (213,546) (1,069,366) (60,748) (1,436,277) (98,171) (138,512) 25,373 (1,647,587) (2,777,701)

ContributionsParticipant's 93,544 3,718 1,619,506 1,716,768 0 8,305,970 2,094,590 220,302 265,285 10,886,147 12,602,915Employer 3,160,060 832,401 3,553,311 7,545,772 530,426 9,914,030 0 105,251 530,579 10,549,860 18,626,058Rollovers 0 0 0 0 0 432,597 278,581 0 2,278 713,456 713,456

Total Contributions 3,253,604 836,119 5,172,817 9,262,540 530,426 18,652,597 2,373,171 325,553 798,142 22,149,463 31,942,429

OtherTransfers In from Other Plans 0 0 0 0 653,097 40,988 0 0 0 40,988 694,085

Total Additions 2,834,535 399,368 4,959,271 8,193,174 1,122,775 17,257,308 2,275,000 187,041 823,515 20,542,864 29,858,813

DEDUCTIONSBenefits Paid to Participants 7,424,676 6,654,509 5,722,723 19,801,908 141,788 18,798,198 874,085 501,993 32,865 20,207,141 40,150,837Administrative Expenses 228,654 121,781 439,588 790,023 774,388 1,000 0 0 0 1,000 1,565,411Transfers to Other Plans 38,696 0 0 38,696 2,291 559,242 0 2,963 90,893 653,098 694,085

Total Deductions 7,692,026 6,776,290 6,162,311 20,630,627 918,467 19,358,440 874,085 504,956 123,758 20,861,239 42,410,333

CHANGE INNET POSITION (4,857,491) (6,376,922) (1,203,040) (12,437,453) 204,308 (2,101,132) 1,400,915 (317,915) 699,757 (318,375) (12,551,520)

NET POSITION - RESTRICTED FOR PENSION, OPEB, AND RETIREMENT BENEFITS, BEGINNING

OF PERIOD 47,178,808 64,424,664 152,394,999 263,998,471 1,247,594 272,872,066 14,523,259 5,403,072 506,539 293,304,936 558,551,001

NET POSITION - RESTRICTED FOR PENSION, OPEB, AND RETIREMENT BENEFITS, END

OF PERIOD $ 42,321,317 $ 58,047,742 $ 151,191,959 $ 251,561,018 $ 1,451,902 $ 270,770,934 $ 15,924,174 $ 5,085,157 $ 1,206,296 $ 292,986,561 $ 545,999,481

Defined Benefit Plans Defined Contribution Plans

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OPEB, AND RETIREMENTTRUST FUNDS OF KNOX COUNTY, TENNESSEE

STATEMENTS OF CHANGES IN FIDUCIARY NET POSITION (Continued)

For the Year Ended June 30, 2016

-1

2 -

The accompanying notes are an integral part of these financial statements.

- 13 -

KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM

PENSION, OTHER POST EMPLOYMENT BENEFIT AND RETIREMENT TRUST FUNDS OF KNOX COUNTY, TENNESSEE

NOTES TO THE FINANCIAL STATEMENT

For the Years Ended June 30, 2017 and 2016

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS Administration - The Knox County Retirement and Pension Board and System (“Retirement Board” and “System”) was created by Tennessee General Assembly, House Bill No. 866, Chapter 246, Private Acts 1967-68, as amended. The powers of the Retirement Board are governed by the Knox County Charter, Article VII, as amended. The Retirement Board is governed by nine members who include the (a) County Mayor, or his designee, (b) four members of the Knox County Commission and (c) four current employees of Knox County Government and the Board of Education who are participating members of the System and elected by the current employees. Elected Board members serve staggered four-year terms and the County Mayor and four County Commission members serve concurrently with their terms as elected County Officials. The Retirement Board employs an executive director who is responsible for administering Knox County’s single employer pension, OPEB, and retirement plans. The System uses USI Consulting Group, Inc. as the actuary for its defined benefit plans and OPEB employee disability plan and as third-party administrator to help in administering the defined contribution plans. As of January 1, 2017, the Board appointed First Tennessee Bank Advisors as Plan Trustee for the defined contribution plans and the Employee Disability Plan. Prior to this appointment, Countybank Trust Services served in this role. Wells Fargo Bank is the investment custodian of the defined contribution plans and the OPEB - Employee Disability Plan. State Street Bank & Trust Company is the Plan Trustee and Investment Custodian for the Defined Benefit Plans. The Retirement Board has also hired several different investment advisors to manage its investment portfolio for its defined benefit plans. The following brief descriptions of the System's Plans are provided for general information only. Participants should refer to the various Plan documents for more complete information. Employee Retirement and Income Security Act of 1974 (ERISA) - According to the Employee Retirement Income Security Act of 1974 (ERISA), the System operates governmental pension, OPEB and retirement plans and is not subject to the statutory provisions of ERISA. Eligibility - The System covers employees of Knox County Government, Knox County Board of Education classified education employees (not certified), the Knoxville-Knox County Public Building Authority, and various other related entities. Employees (participants) can become participants immediately upon employment and must be scheduled to work a minimum of 18.5 hours or more per week to be eligible to enroll and continue to participate in the various Plans. Eligibility for the Knox County Sheriff’s Office employees who participate in the UOPP defined benefit plan or the STAR defined contribution plan is limited to full time employees who work a minimum of 40 hours or more per week. Plans - The System operates eight single-employer pension and retirement plans which consist of three defined benefit, one OPEB and four defined contribution plans which includes the following:

Defined Benefit Plans: This includes the Closed Defined Benefit Plan (closed to new participants as of September 30, 1991), Teacher's Plan (assumed from the former City of Knoxville Board of Education July 1, 1987 and closed to new participants as of July 1, 1977), the Uniformed Officers Pension Plan (UOPP, closed to new Sheriff’s Department Officers employed on or after January 1, 2014). Effective June 30, 2014, the Plans were amended to change the plans’ year end from December 31 to June 30.

- 14 -

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued)

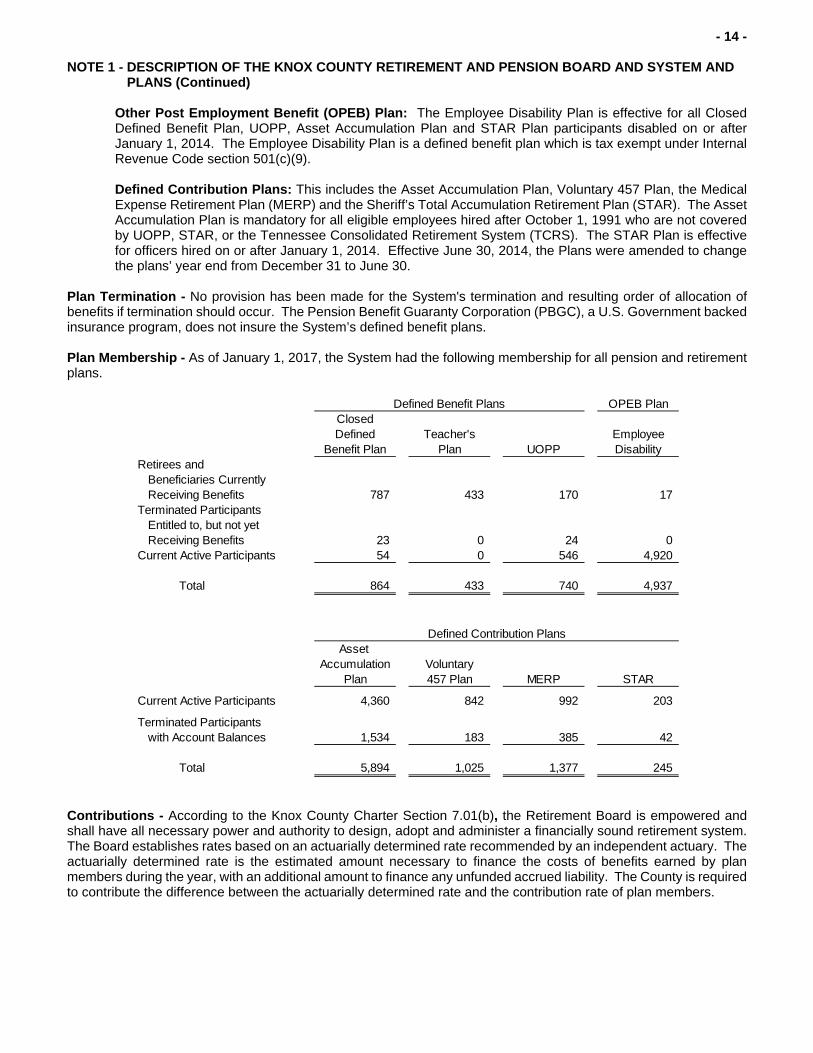

Other Post Employment Benefit (OPEB) Plan: The Employee Disability Plan is effective for all Closed Defined Benefit Plan, UOPP, Asset Accumulation Plan and STAR Plan participants disabled on or after January 1, 2014. The Employee Disability Plan is a defined benefit plan which is tax exempt under Internal Revenue Code section 501(c)(9).

Defined Contribution Plans: This includes the Asset Accumulation Plan, Voluntary 457 Plan, the Medical Expense Retirement Plan (MERP) and the Sheriff’s Total Accumulation Retirement Plan (STAR). The Asset Accumulation Plan is mandatory for all eligible employees hired after October 1, 1991 who are not covered by UOPP, STAR, or the Tennessee Consolidated Retirement System (TCRS). The STAR Plan is effective for officers hired on or after January 1, 2014. Effective June 30, 2014, the Plans were amended to change the plans’ year end from December 31 to June 30.

Plan Termination - No provision has been made for the System's termination and resulting order of allocation of benefits if termination should occur. The Pension Benefit Guaranty Corporation (PBGC), a U.S. Government backed insurance program, does not insure the System’s defined benefit plans. Plan Membership - As of January 1, 2017, the System had the following membership for all pension and retirement plans.

OPEB PlanClosedDefined Teacher's Employee

Benefit Plan Plan UOPP DisabilityRetirees and

Beneficiaries Currently Receiving Benefits 787 433 170 17

Terminated Participants Entitled to, but not yet Receiving Benefits 23 0 24 0

Current Active Participants 54 0 546 4,920

Total 864 433 740 4,937

Defined Benefit Plans

Asset Accumulation Voluntary

Plan 457 Plan MERP STAR

Current Active Participants 4,360 842 992 203

Terminated Participantswith Account Balances 1,534 183 385 42

Total 5,894 1,025 1,377 245

Defined Contribution Plans

Contributions - According to the Knox County Charter Section 7.01(b), the Retirement Board is empowered and shall have all necessary power and authority to design, adopt and administer a financially sound retirement system. The Board establishes rates based on an actuarially determined rate recommended by an independent actuary. The actuarially determined rate is the estimated amount necessary to finance the costs of benefits earned by plan members during the year, with an additional amount to finance any unfunded accrued liability. The County is required to contribute the difference between the actuarially determined rate and the contribution rate of plan members.

- 15 -

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Contributions (Defined Benefit and OPEB Plans) - The System operates one OPEB and three different single-employer defined benefit plans which are contributory plans that require the employer (Knox County and the Knox County Board of Education) to make contributions determined by annual actuarial valuations, as stated above. In addition, participants are required to make employee contributions to the defined benefit plans of varying percentages and are remitted to the trusts on a per pay period basis. For the years ended June 30, 2017 and 2016, the County’s average contribution rate as a percentage of covered payroll was as follows:

OPEB PlanClosedDefined Teacher's Employee

Fiscal Year Benefit Plan Plan UOPP Disability Plan 2017 186.55 % N/A 16.67 % 0.93 %2016 161.80 N/A 12.94 0.76

Defined Benefit PlansContribution as a Percentage of Covered Payroll

Contributions (Defined Contribution Plans) - Participants’ contributions of 6% to the Asset Accumulation Plan are mandatory and employees may voluntarily make qualified retirement contributions to the Voluntary 457 and MERP defined contribution Plans. Employee contributions are deducted pre-tax from the participants and remitted to the trusts on a per pay period basis for federal income tax purposes under Section 401(a) and 457(b) of the Internal Revenue Code. Employer matching contributions are also remitted to the trusts on a per pay period basis. Participants may also rollover amounts representing distributions from other qualified defined benefit or defined contribution plans. Participants may elect to make tax-deferred contributions to the 457 Plan subject to annual IRS limitations. For the Voluntary 457 and MERP Plans, participants may change their contribution percentage monthly and participants may stop deferring with any payroll. The Asset Accumulation and Voluntary 457 defined contribution plans allow participants to direct employee and employer contributions in a variety of mutual funds, common collective trusts and guaranteed investment contracts. Participants may change their investment options at their discretion. For the MERP the Retirement Board has selected one investment “mix” option for participants. The one MERP investment option consists of 10% conservative, 45% moderate, and 45% ultra-aggressive investment styles. The contributions for each participant are accounted for separately as to employer and participant contributions. The Sheriff’s Total Accumulation Retirement Plan (STAR) is reserved for officers of Knox County Sheriff’s Officers hired or re-hired on or after January 1, 2014. Participants’ contributions of 6% are mandatory. Employee contributions are deducted pre-tax from the participants on a per pay period basis for federal income tax purposes under Section 401(a) and 457(b) of the Internal Revenue Code. Participants may also rollover amounts representing distributions from other qualified defined benefit or defined contribution plans. Participant Accounts (Defined Contribution Plans) - Each participant's account is credited with the participant's contribution, the employer's contributions and an allocation of plan earnings. The benefit to which a participant is entitled is the benefit which can be provided from the participant's vested account. Notes Receivable from Participants (Defined Contribution Plans) - Participants in the Asset Accumulation and STAR plans may borrow from their fund accounts if they are actively employed, paid on a 12-month payroll cycle, fully vested in their accounts (STAR participants do not have to be fully vested in the Employer Supplemental Contribution Account) and have a minimum balance of $20,000. Employees from the following groups are excluded from borrowing from their fund accounts - Knox County Schools and Charter Schools. The minimum amount a participant may borrow is $5,000 up to a maximum equal to the lesser of $50,000 or 25% of their vested balance. Loan terms may not exceed five years and only one loan is permitted at any time. The loan interest rate is set at 4% per year (as of September 1, 2016). Principal and interest is paid ratably through payroll deductions.

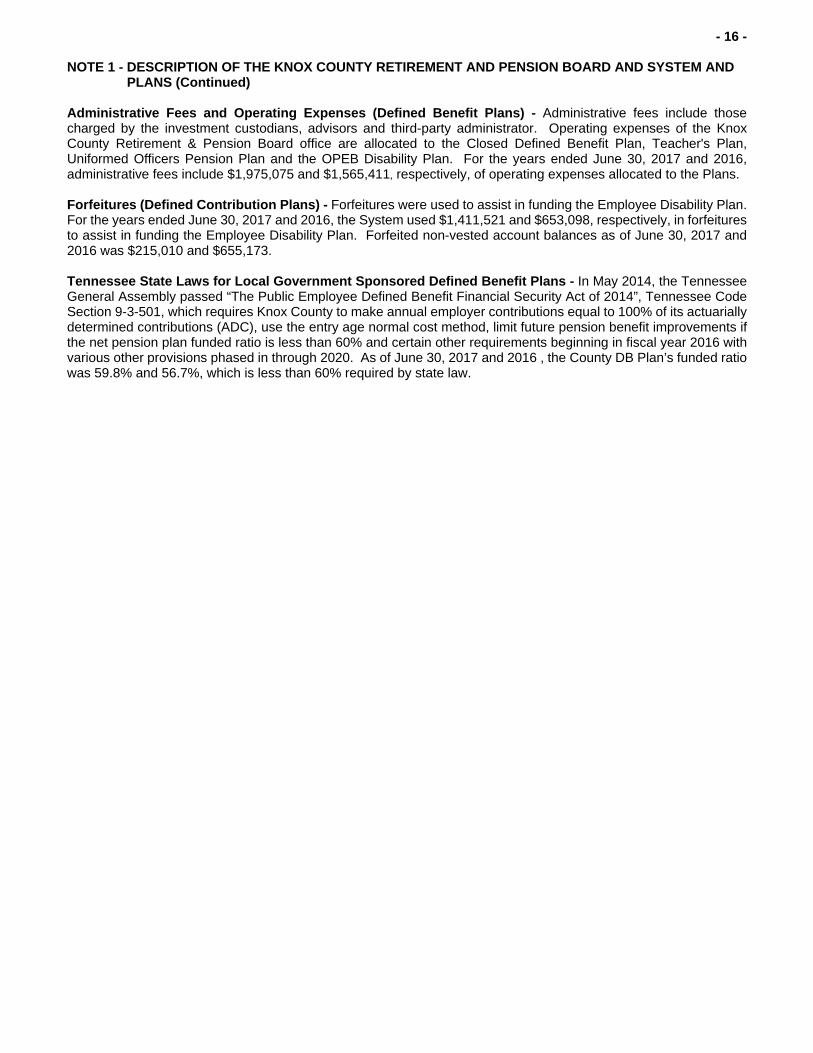

- 16 -

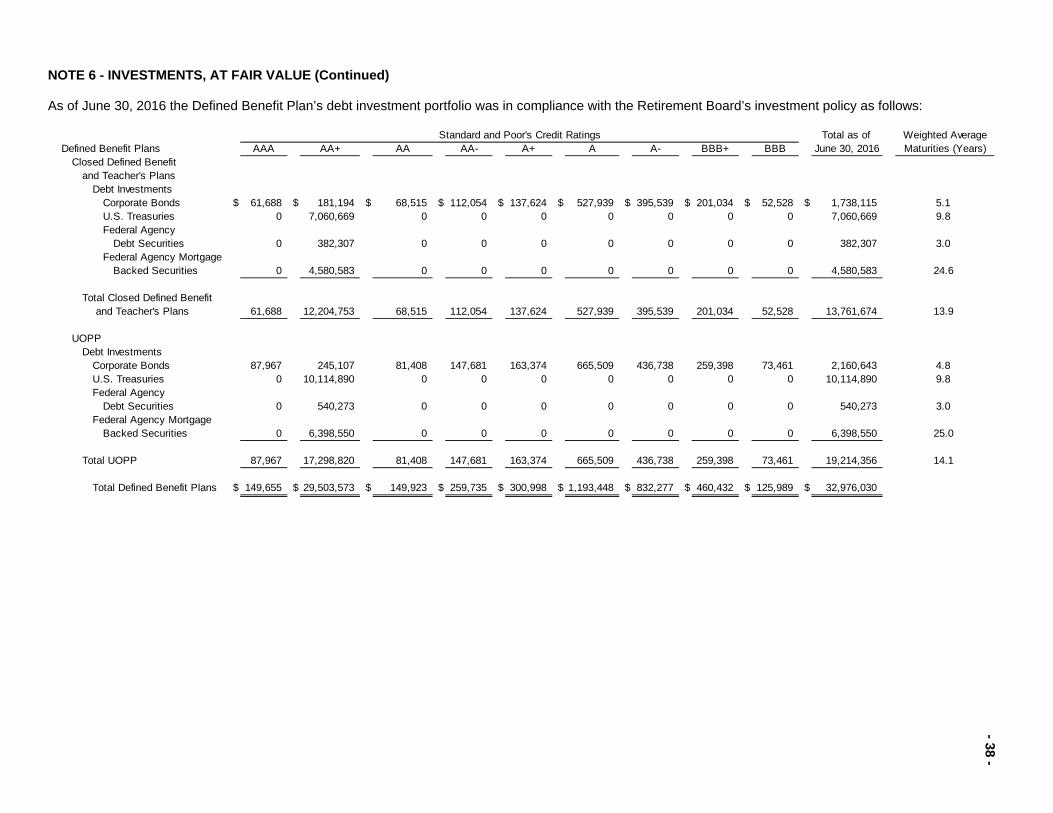

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Administrative Fees and Operating Expenses (Defined Benefit Plans) - Administrative fees include those charged by the investment custodians, advisors and third-party administrator. Operating expenses of the Knox County Retirement & Pension Board office are allocated to the Closed Defined Benefit Plan, Teacher's Plan, Uniformed Officers Pension Plan and the OPEB Disability Plan. For the years ended June 30, 2017 and 2016, administrative fees include $1,975,075 and $1,565,411, respectively, of operating expenses allocated to the Plans. Forfeitures (Defined Contribution Plans) - Forfeitures were used to assist in funding the Employee Disability Plan. For the years ended June 30, 2017 and 2016, the System used $1,411,521 and $653,098, respectively, in forfeitures to assist in funding the Employee Disability Plan. Forfeited non-vested account balances as of June 30, 2017 and 2016 was $215,010 and $655,173. Tennessee State Laws for Local Government Sponsored Defined Benefit Plans - In May 2014, the Tennessee General Assembly passed “The Public Employee Defined Benefit Financial Security Act of 2014”, Tennessee Code Section 9-3-501, which requires Knox County to make annual employer contributions equal to 100% of its actuarially determined contributions (ADC), use the entry age normal cost method, limit future pension benefit improvements if the net pension plan funded ratio is less than 60% and certain other requirements beginning in fiscal year 2016 with various other provisions phased in through 2020. As of June 30, 2017 and 2016 , the County DB Plan’s funded ratio was 59.8% and 56.7%, which is less than 60% required by state law.

- 17 -

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of Defined Benefit Plans

Closed Defined Benefit Plan Teacher's Plan UOPP

Effective and Closed Plan was established July 1, 1968 Plan was previously a City of Plan was established July 1, 2007 Dates: and was closed to new participants Knoxville Board of Education and was closed to new participants

on September 30, 1991. which was assumed by Knox on December 31, 2013.County as of July 1, 1987.

Employees Covered: Employees of Knox County and Former City of Knoxville Board of Officers regularly employed by the the Knox County Board of Education teachers who were in Knox County Sheriff's Office and Education (non-teachers) who the Plan as of June 30,1987 and who do not participate in the were hired before the plan was regularly employed by the Knox Closed Defined Benefit or Asset closed on September 30, 1991 County Board of Education. Accumulation Plans.and did not choose to convert to the Asset Accumulation Plan.

Employees Excluded: Employees of Knox County who Employees of Knox County who Employees of Knox County who participate in one of the other two participate in one of the other two participate in closed DB Plansdefined benefit plans, or who defined benefit plans, or who or who participate in the Asset participate in the Asset participate in the Asset Accumulation Plan. Accumulation Plan. Accumulation Plan. Also, Knox

County Board of Education teachers and administrators who are participants in the Tennessee Consolidated Retirement System(TCRS).

Employee 5% of Annual Compensation 3% of base earnings ($4,800 6% of annual compensation, no Contributions: annually) with 5% for amounts in employee contributions after a

excess of base earnings. participant has completed 30 years of credited service.

Vesting: 100% after completing five years 100% after completing ten years 100% after completing five years of of credited service. of credited service. credited service.

Normal Retirement Minimum of age 65, with five years of Minimum of age 62, with ten years Minimum of age 50, with 25 years of Age & Required credited service. For elected officials, of credited service. credited service.

Creditable Service: age 55 with five years of credited service.

Normal Retirement Years of credited service times the One-twelfth of credited service Monthly benefit equal to 2.5% of Benefit Formula: greater of (a) 1.75% of average multiplied by the sum of (a) .75% average monthly compensation

monthly compensation or, (b) $30. times average base earnings and multiplied by years of credited(b) 1.50% times average excess service up to 30 years.earnings.

Normal Form of Life Annuity Life Annuity Life annuity for un-marriedBenefit: participants. A 50% joint and

survivor annuity for married participants.

- 18 -

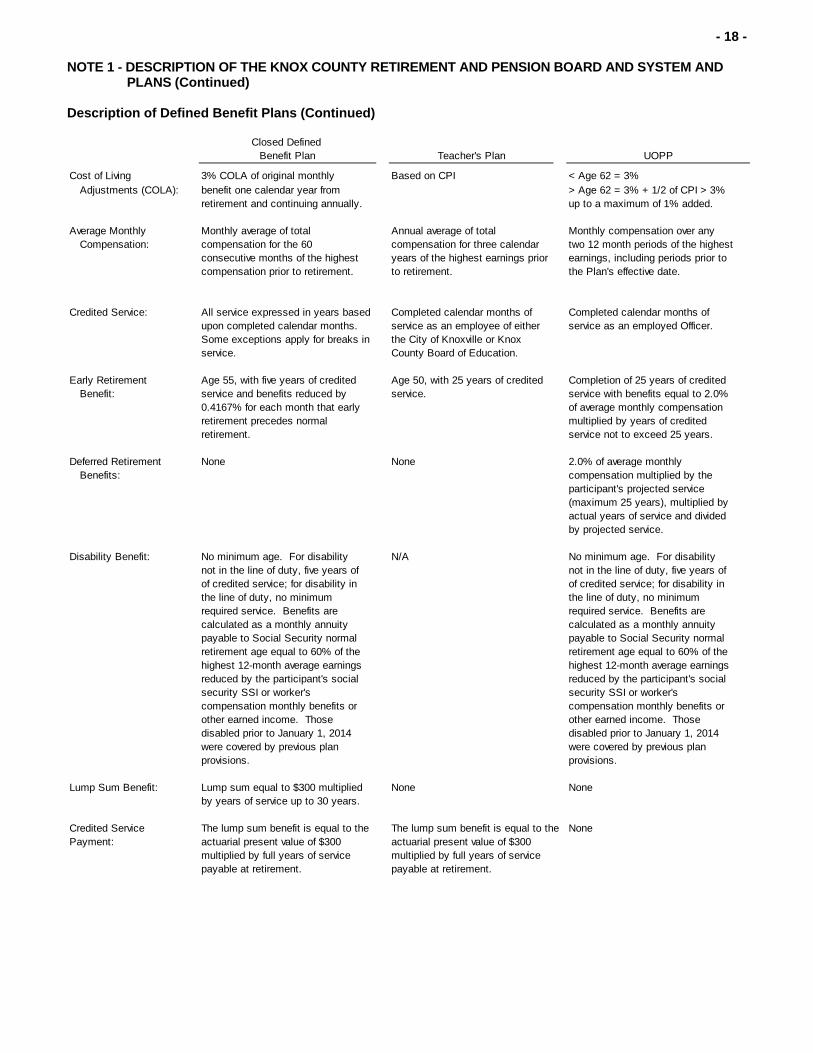

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of Defined Benefit Plans (Continued)

Closed Defined Benefit Plan Teacher's Plan UOPP

Cost of Living 3% COLA of original monthly Based on CPI < Age 62 = 3%

Adjustments (COLA): benefit one calendar year from > Age 62 = 3% + 1/2 of CPI > 3% retirement and continuing annually. up to a maximum of 1% added.

Average Monthly Monthly average of total Annual average of total Monthly compensation over any

Compensation: compensation for the 60 compensation for three calendar two 12 month periods of the highest consecutive months of the highest years of the highest earnings prior earnings, including periods prior tocompensation prior to retirement. to retirement. the Plan's effective date.

Credited Service: All service expressed in years based Completed calendar months of Completed calendar months of upon completed calendar months. service as an employee of either service as an employed Officer.Some exceptions apply for breaks in the City of Knoxville or Knox service. County Board of Education.

Early Retirement Age 55, with five years of credited Age 50, with 25 years of credited Completion of 25 years of creditedBenefit: service and benefits reduced by service. service with benefits equal to 2.0%

0.4167% for each month that early of average monthly compensation retirement precedes normal multiplied by years of credited retirement. service not to exceed 25 years.

Deferred Retirement None None 2.0% of average monthly Benefits: compensation multiplied by the

participant's projected service (maximum 25 years), multiplied byactual years of service and divided by projected service.

Disability Benefit: No minimum age. For disability N/A No minimum age. For disabilitynot in the line of duty, five years of not in the line of duty, five years ofof credited service; for disability in of credited service; for disability in the line of duty, no minimum the line of duty, no minimumrequired service. Benefits are required service. Benefits arecalculated as a monthly annuity calculated as a monthly annuitypayable to Social Security normal payable to Social Security normalretirement age equal to 60% of the retirement age equal to 60% of thehighest 12-month average earnings highest 12-month average earningsreduced by the participant's social reduced by the participant's social security SSI or worker's security SSI or worker's compensation monthly benefits or compensation monthly benefits or other earned income. Those other earned income. Those disabled prior to January 1, 2014 disabled prior to January 1, 2014were covered by previous plan were covered by previous plan provisions. provisions.

Lump Sum Benefit: Lump sum equal to $300 multiplied None Noneby years of service up to 30 years.

Credited Service The lump sum benefit is equal to the The lump sum benefit is equal to the NonePayment: actuarial present value of $300 actuarial present value of $300

multiplied by full years of service multiplied by full years of servicepayable at retirement. payable at retirement.

- 19 -

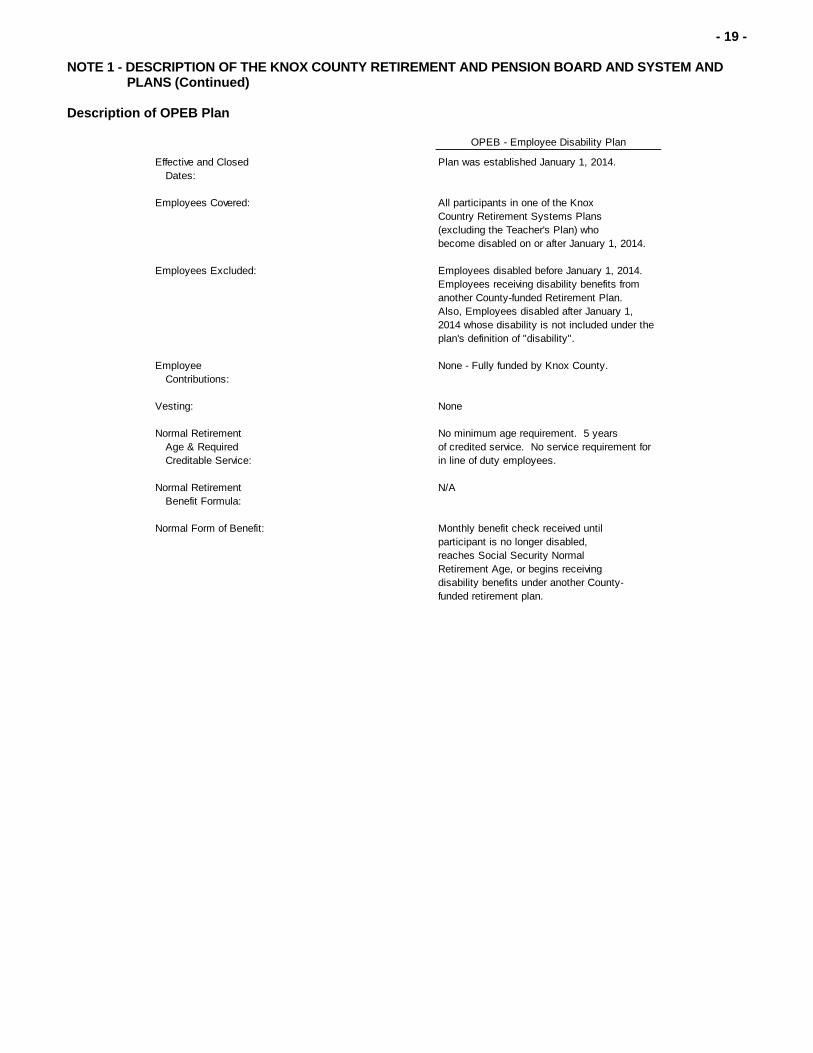

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of OPEB Plan

OPEB - Employee Disability Plan

Effective and Closed Plan was established January 1, 2014.Dates:

Employees Covered: All participants in one of the Knox Country Retirement Systems Plans(excluding the Teacher's Plan) who become disabled on or after January 1, 2014.

Employees Excluded: Employees disabled before January 1, 2014.Employees receiving disability benefits fromanother County-funded Retirement Plan. Also, Employees disabled after January 1, 2014 whose disability is not included under the plan's definition of "disability".

Employee None - Fully funded by Knox County.Contributions:

Vesting: None

Normal Retirement No minimum age requirement. 5 years Age & Required of credited service. No service requirement for

Creditable Service: in line of duty employees.

Normal Retirement N/ABenefit Formula:

Normal Form of Benefit: Monthly benefit check received until participant is no longer disabled, reaches Social Security Normal Retirement Age, or begins receivingdisability benefits under another County-funded retirement plan.

- 20 -

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of OPEB Plan (Continued)

OPEB - Employee Disability Plan

Cost of Living None

Adjustments (COLA):

Average Monthly Monthly average of total Compensation: compensation for the 12

consecutive months of the highest compensation prior to disability.

Credited Service: Completed calendar months of service as an employee of either Knox County or the Knox CountyBoard of Education.

Early Retirement Benefit: N/A

Deferred Retirement 2.0% of pre-disability compensationBenefits: contributed for STAR or Asset

Accumulation participants annually.

Disability Benefit: No minimum age. For disabilitynot in the line of duty, five years ofof credited service; for disability in the line of duty, no minimumrequired service. Benefits arecalculated as a monthly annuitypayable to Social Security normalretirement age equal to 60% of thehighest 12-month average earningsreduced by the participant's social security SSI or worker's compensation monthly benefits or other earned income.

- 21 -

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of Defined Contribution Plans

Asset Accumulation Plan Voluntary 457 Plan

Eligibility and Employees of Knox County and Employees of Knox County and Participation: the Knox County Board of the Knox County Board of

Education (non-teachers) who Education (non-teachers) who are were hired after the Defined Benefit participating in the Asset Plan was closed on September 30, Accumulation or the Closed 1991. Former participants of the Defined Benefit Plans.Closed Defined Plan had the option to transfer to the Asset AccumulationPlan.

Employees Excluded: Employees of Knox County who Employees of Knox County whoparticipate in one of the other three participate certain TCRS plans and certifieddefined benefit plans. Certified teachers of the Knox County Board of teachers and administrators of the Education.Knox County Board of Education covered by TCRS.

Employee Contributions: 6% of Annual Compensation Voluntary(Mandatory)

Employer Matching 6% of Annual Compensation Less than five years of service 0%, Contributions: more than five but less than 10 up

to 2%, more than 10 but less than 15 up to 4%, and more than 15 years up to 6%. Closed DB participants are up to 3%. Matching employer contributions are credited to the participant's Asset Accumulation Plan account.Participants in the UOPP, STAR and TCRSplans are not eligible for employer match.

Vesting of Employer 20% per year after completing one Immediate 100% vesting.Matching Contributions: year of service with 100% after

completing five years of creditedservice.

Normal Retirement Age 55, with five years of credited Based on retirement eligibility of Age & Required service. other plans.Creditable Service:

- 22 -

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of Defined Contribution Plans (Continued)

MERP STAR Plan

Eligibility and Employees of Knox County and Officer's of Knox County Sheriff'sParticipation: the Knox County Board of Office, as classified by the Merit Board

Education (non-teachers) who are as either a law enforcement or participating in the Asset correctional officer, hired or re-hired onAccumulation or the Closed or after January 1, 2014.Defined Benefit Plans.

Employees Excluded: Employees of Knox County who Employees not considered "Officers"participate in the TCRS, UOPP and by the plan. Officer's hired in priorSTAR Plans, Certified teachers years participating in the Assetof the Knox County Board of Education Accumulation Plan or the Uniformedcovered by TCRS. Officer's Pension Plan.

Employee Contributions: Voluntary 6% of Annual Compensation(Mandatory)

Employer Matching 50% of employee contributions up Base contribution of 10% andContributions: to annual maximum of $208. Supplemental contribution of 2% up

to 30 years. After 30 years base contribution decreases to 6% and there is no the supplemental contribution.

Vesting of Employer Immediate 100% vesting. The base contribution is 100% vestedMatching Contributions: after 10 years of service and the

supplemental contributions is 100% vested after 15 years. 100% vesting will occur in both after 10 years of service and the participant is at least 57 years of age.

Normal Retirement Based on retirement eligibility of Age 57, with 10 years of credited Age & Required other plans. service.Creditable Service:

- 23 -

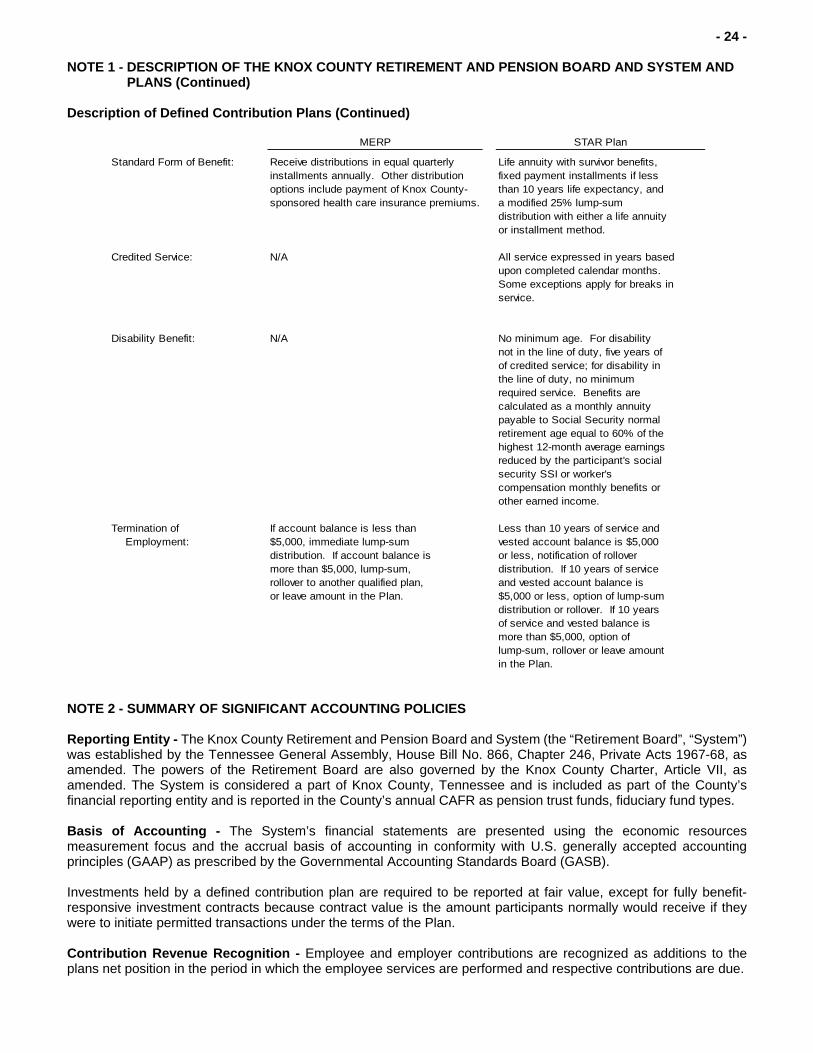

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of Defined Contribution Plans (Continued)

Asset Accumulation Plan Voluntary 457 Plan

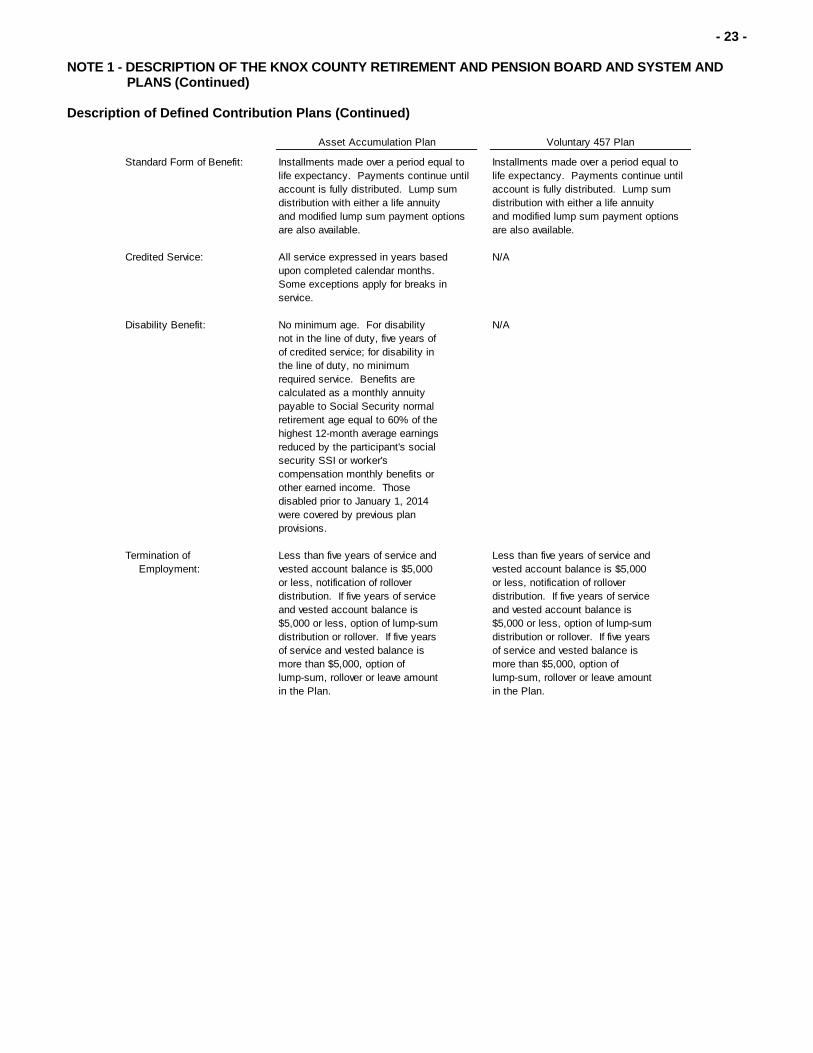

Standard Form of Benefit: Installments made over a period equal to Installments made over a period equal to life expectancy. Payments continue until life expectancy. Payments continue until

account is fully distributed. Lump sum account is fully distributed. Lump sum distribution with either a life annuity distribution with either a life annuity and modified lump sum payment options and modified lump sum payment optionsare also available. are also available.

Credited Service: All service expressed in years based N/Aupon completed calendar months.Some exceptions apply for breaks inservice.

Disability Benefit: No minimum age. For disability N/Anot in the line of duty, five years ofof credited service; for disability in the line of duty, no minimumrequired service. Benefits arecalculated as a monthly annuitypayable to Social Security normalretirement age equal to 60% of thehighest 12-month average earningsreduced by the participant's social security SSI or worker's compensation monthly benefits or other earned income. Those disabled prior to January 1, 2014were covered by previous plan provisions.

Termination of Less than five years of service and Less than five years of service and Employment: vested account balance is $5,000 vested account balance is $5,000

or less, notification of rollover or less, notification of rolloverdistribution. If five years of service distribution. If five years of service and vested account balance is and vested account balance is $5,000 or less, option of lump-sum $5,000 or less, option of lump-sum distribution or rollover. If five years distribution or rollover. If five years of service and vested balance is of service and vested balance is more than $5,000, option of more than $5,000, option of lump-sum, rollover or leave amount lump-sum, rollover or leave amount in the Plan. in the Plan.

- 24 -

NOTE 1 - DESCRIPTION OF THE KNOX COUNTY RETIREMENT AND PENSION BOARD AND SYSTEM AND PLANS (Continued) Description of Defined Contribution Plans (Continued)

MERP STAR Plan

Standard Form of Benefit: Receive distributions in equal quarterly Life annuity with survivor benefits, installments annually. Other distribution fixed payment installments if less

options include payment of Knox County- than 10 years life expectancy, and sponsored health care insurance premiums. a modified 25% lump-sum

distribution with either a life annuity or installment method.

Credited Service: N/A All service expressed in years basedupon completed calendar months.Some exceptions apply for breaks inservice.

Disability Benefit: N/A No minimum age. For disabilitynot in the line of duty, five years ofof credited service; for disability in the line of duty, no minimumrequired service. Benefits arecalculated as a monthly annuitypayable to Social Security normalretirement age equal to 60% of thehighest 12-month average earningsreduced by the participant's social security SSI or worker's compensation monthly benefits or other earned income.

Termination of If account balance is less than Less than 10 years of service and Employment: $5,000, immediate lump-sum vested account balance is $5,000

distribution. If account balance is or less, notification of rollovermore than $5,000, lump-sum, distribution. If 10 years of service rollover to another qualified plan, and vested account balance is or leave amount in the Plan. $5,000 or less, option of lump-sum

distribution or rollover. If 10 years of service and vested balance is more than $5,000, option of lump-sum, rollover or leave amount in the Plan.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Reporting Entity - The Knox County Retirement and Pension Board and System (the “Retirement Board”, “System”) was established by the Tennessee General Assembly, House Bill No. 866, Chapter 246, Private Acts 1967-68, as amended. The powers of the Retirement Board are also governed by the Knox County Charter, Article VII, as amended. The System is considered a part of Knox County, Tennessee and is included as part of the County’s financial reporting entity and is reported in the County’s annual CAFR as pension trust funds, fiduciary fund types. Basis of Accounting - The System’s financial statements are presented using the economic resources measurement focus and the accrual basis of accounting in conformity with U.S. generally accepted accounting principles (GAAP) as prescribed by the Governmental Accounting Standards Board (GASB). Investments held by a defined contribution plan are required to be reported at fair value, except for fully benefit-responsive investment contracts because contract value is the amount participants normally would receive if they were to initiate permitted transactions under the terms of the Plan. Contribution Revenue Recognition - Employee and employer contributions are recognized as additions to the plans net position in the period in which the employee services are performed and respective contributions are due.

- 25 -

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Cash and Cash Equivalents - Cash and cash equivalents consist of highly liquid investments, including cash held on a temporary basis by the investment trustee and custodian and money market funds. Substantially all cash and cash equivalents are uninsured and uncollateralized; carrying values approximate fair value. Investment Valuation and Income Recognition - Investments, except for the guaranteed investment contract, are stated at fair value. Securities traded on a national or international exchange are valued at the last reported sales price at current exchange rates. Net increases (decreases) in fair value of investments reflect the change in market values from the preceding year-end to the current year-end (including investments bought, sold and held during the year). The guaranteed investment contract is valued at contract value. See Note 7, Guaranteed Investment Contract, for additional information. Purchases and sales of securities are recorded on a trade-date basis. Interest and dividend income is recorded on the accrual basis. Dividends are recorded on the ex-dividend date. A description of the valuation methodologies used to measure investments at fair value are further described in Note 6. Investment Policy - The Retirement Board has investment policies in regards to allocation of investment assets in the defined benefit plans and OPEB plan and may be amended by the Board. It is the policy of the Board to pursue an investment strategy that reduces risk through the prudent diversification of the investment portfolio across a broad selection of investment classes. The Board’s investment policies are further described in Note 6. Benefits Paid - Benefit payments to participants are recorded as incurred according to the plan provisions. Net Fiduciary Position - Net fiduciary position comprises results from investment income (loss), contributions, benefits paid and administrative expenses. Net fiduciary position is classified as follows: restricted for pension, OPEB and retirement benefits. Pension Liabilities and Actuarial Present Value of OPEB Liabilities (Defined Benefit and OPEB Plans) - Pension liabilities, and actuarial accrued OPEB liabilities are those future periodic payments that are attributable under the Plan's provisions to the service employees have rendered. Pension and OPEB liabilities include benefits expected to be paid to (a) retired or terminated employees or their beneficiaries, (b) beneficiaries of employees who have died, and (c) present employees or their beneficiaries. Benefits payable under all circumstances - retirement, death, disability, and termination of employment - are included, to the extent they are deemed attributable to employee service rendered to the valuation date. The pension liabilities and the actuarial present value of OPEB liabilities is determined by an actuary from USI Consulting Group and is that amount which results from applying actuarial assumptions to adjust the pension and OPEB liabilities to reflect the time value of money (through discounts for interest) and the probability of payment (by means of decrements such as for death, disability, withdrawal or retirement) between the valuation date and the expected date of payment. Net Position Flow Assumption - The System's fiduciary net position is restricted for pension, OPEB and retirement benefits. In order to calculate the amounts to report as restricted - net position and unrestricted - net position in the financial statements, a flow assumption must be made about the order in which the resources are considered to be applied. When both restricted and unrestricted resources are available for use, it is the System’s policy to consider restricted - net position to have been depleted before unrestricted - net position is applied. As of June 30, 2017 and 2016, the System did not have any unrestricted net position. Expenses - Operating expenses of the System, such as salaries, benefits, occupancy costs, and fees charged by the investment custodians, advisors, actuary and third-party administrator are allocated to the defined benefit plans and OPEB plan. Investment fees related to the defined contribution plans participants' accounts are included in net appreciation (depreciation) of fair value of investments. Use of Estimates - The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the statement of plan net position date, and reported amounts of additions and deductions during the reporting period. Significant estimates include fair value of investments and all actuarial calculations. Accordingly, actual results may differ from those estimates.

- 26 -

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Governmental Accounting Standard Board (GASB) Pronouncements

GASB Statement No. 72 - During the year ended June 30, 2016, the System adopted GASB Statement No. 72, Fair Value Measurement and Application, required for fiscal periods beginning after June 15, 2015. The accompanying financial statements, notes and required supplementary information have been updated to incorporate the changes under GASB Statement No. 72. GASB Statement No. 74 - During the year ended June 30, 2017, the System adopted GASB Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, required for fiscal periods beginning after June 15, 2016. The accompanying financial statements, notes and required supplementary information have been updated to incorporate the changes under GASB Statement No. 74.