koert pretorius roly buys - the competition commission ...€¦ · 4 • provide a broad outline of...

TRANSCRIPT

2

• Koert Pretorius Chief Executive Officer

• Braam Joubert Chief Financial Officer

• Roly Buys Strategy Development Executive

• Schalk Burger SC

INTRODUCTION OF MEDICLINIC

REPRESENTATIVES

3

• To inform the public

• To provide insight on the

interaction between Mediclinic

and various stakeholders in the

private healthcare sector

• To provide regulatory context

PURPOSE OF THE PRESENTATION

4

• Provide a broad outline of

Mediclinic's business

• Setting the scene for further

engagements

• Await outcome of data,

information and profitability

analyses

SCOPE OF THE PRESENTATION

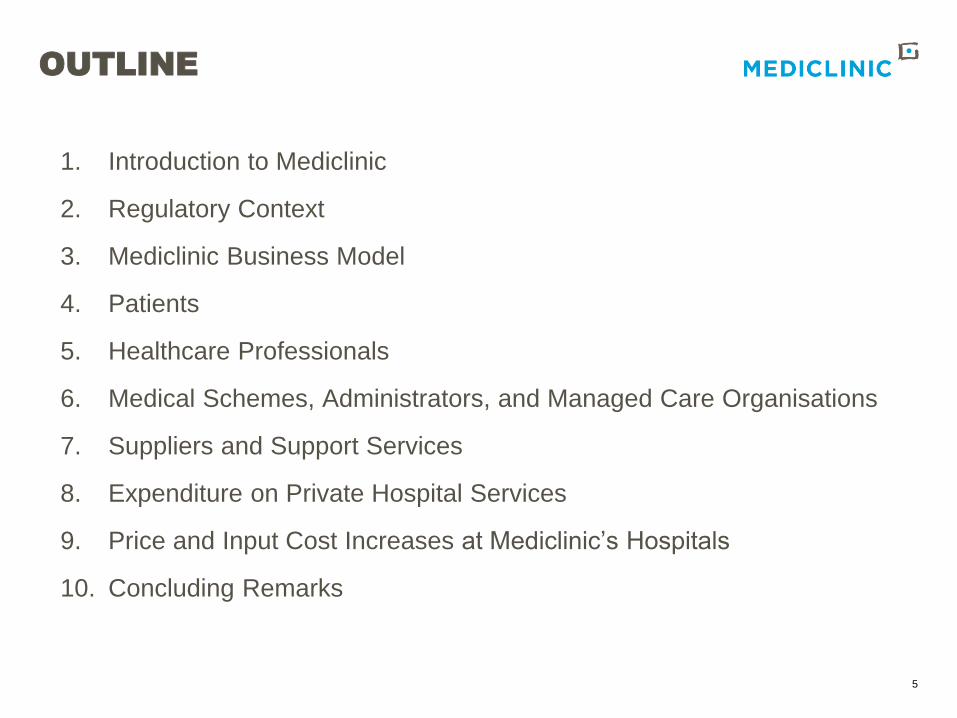

5

1. Introduction to Mediclinic

2. Regulatory Context

3. Mediclinic Business Model

4. Patients

5. Healthcare Professionals

6. Medical Schemes, Administrators, and Managed Care Organisations

7. Suppliers and Support Services

8. Expenditure on Private Hospital Services

9. Price and Input Cost Increases at Mediclinic’s Hospitals

10. Concluding Remarks

OUTLINE

6

INTRODUCTION

TO MEDICLINIC

7

2014

Acquired Hirslanden

Group

(+13 Hospitals)

Acquired Klinik

Stephanshorn

(+85 beds)

Acquired Swissana

Clinic Meggen

(+22 Beds)

Acquisition of controlling

interest in Mediclinic

Middle East

Opening of flagship

hospital, Mediclinic City

Hospital in Dubai

Acquisition of

Al Noor

Acquired 3 clinics with

acquisition of Emaar

clinics

Acquired Clinique La

Colline

(+62 Beds)

SA

CH

Mediclinic listed on

JSE

1986

Acquired Medicor

Group

(+11 Hospitals)

1995

Acquired Hydromed

Group

(+4 Hospitals)

1996

Acquired Hospiplan

Group

(+12 Hospitals)

1998

Acquired Curamed

Group

(+6 Hospitals)

2002

Acquired the

Protector Group

(+4 Hospitals)

2006

UAE

2007 2010 2014

2007 2011 2015/162008 2012

Buyout of GE Healthcare

and Varkey Group stake

in Emirates Healthcare

HOSPITALS

73

CLINICS

35

COUNTRIES

5

2015FY2015

2015

Acquired land to build

Mediclinic Parkview

Hospital

NA

INTRODUCTION TO MEDICLINIC

HISTORY

Source: Company information

8

Notes

1. The National Hospital Network (NHN) is an association of 165 independent private hospitals, day clinics and other facilities

2. As of 31 March 2015

3. As of 30 September 2015

(1)

• The South African private hospital market has three

listed players; Netcare, Life Healthcare and Mediclinic

- Together they account for c. 73% of the private

hospital market

Mediclinic 22%

Netcare28%

Life23%

NHN11%

Independent16%

LISTED PRIVATE HOSPITALS MARKET SHARE

# OF BEDSSA REVENUES

(ZAR MM)(2)

Source: Company information

7,885(2) 12,323

8,647(3) 13,749

9,444(2) 15,738

Source: Company information, National Hospital Network, Broker estimates

SOUTH AFRICA PRIVATE HOSPITAL BED MARKET

SHARE

INTRODUCTION TO MEDICLINIC

MEDICLINIC SOUTHERN AFRICA

9

INTRODUCTION TO MEDICLINIC

GEOGRAPHIC FOOTPRINT

Source: Company information

Namibia

Northern Cape

Western Cape

Eastern Cape

UpingtonMediclinic Upington

KimberlyMediclinic Kimberly

GariepMediclinic Gariep

BloemfonteinMediclinicBloemfontein

WelkomMediclinicWelkom

North West

South Africa

Mediclinic Victoria

PietermartizburgMediclinic Pietermartizburg

Mediclinic Howick

Kwazulu-Natal

NewcastleMediclinic Newcastle

BarbertonMediclinic Barberton

NelspruitMediclinic Nelspruit

Limpopo

TzaneenMediclinic Tzaneen

PolokwaneMediclinic Limpopo

MediclinicLephalale

Pretoria

Gauteng

Mediclinic Hoogland

Mediclinic Emfuleni

Free State

Mediclinic Vereeniging

Mediclinic LegaeBrits

Mediclinic Brits

PotchefstroomMediclinic Potchefstroom

Mediclinic Secunda

Mediclinic Ermelo

Mediclinic Highveld

Mpumalanga

MediclinicThabazimbi

Plettenberg BayMediclinic Plettenberg Bay

OudtshoornMediclinic Klein Karoo

GeorgeMediclinic George

Mediclinic Geneva

HermanusMediclinic Hermanus

WorcesterMediclinic Worcester

StellenboschMediclinic Stellenbosch

StrandMediclinic Strand

VergelegenMediclinic Vergelegen

Paarl Mediclinic Paarl

Peninsula Hospitals• Mediclinic Cape Gate• Mediclinic Cape Town• Mediclinic Constantiaberg• Mediclinic Durbanville• Mediclinic Louis Leipoldt• Mediclinic Milnerton• Mediclinic Panorama

OtjiwarongoMediclinicOtjiwarongo

SwakopmundMediclinicSwakopmund

WindhoekMediclinicWindhoek

Johannesburg Hospitals• Mediclinic Morningside• Mediclinic Sandton• Wits University Donald

Gordon Medical Centre

Pretoria Hospitals• Mediclinic Gynaecological

Hospital• Mediclinic Heart Hospital• Mediclinic Kloof• Mediclinic Medforum• Mediclinic Midstream• Mediclinic Muelmed

Region Number of Hospitals

Western Cape 17

Northern Cape 2

Gauteng 12

Kwazulu-Natal 4

Limpopo 4

North West 2

Free State 3

Namibia 3

Total 52

Mpumalanga 5

SOUTHERN AFRICA GEOGRAPHIC OVERVIEW

10

INTRODUCTION TO MEDICLINIC

OPERATIONAL OVERVIEW

Internal Medicine

26%

General Surgery

17%Obstetrics

and Gynaecology

15%

Orthopaedics13%

Urogenital7%

ENT and Opthalmology

7%

Cardiac and Vascular

7%

Neurology5%

Oral and Maxillofacial

2% Other1%

Source: Company information

SERVICE OFFERING

SPECTRUM OF SERVICES (2014)

SOUTHERN AFRICA OPERATIONAL OVERVIEW

HOSPITALS

52

ADMITTING

DOCTORS

2,451

EMPLOYEES

16,576

BEDS

7,983

DAY CLINICS

2

Source: Company information

INTRODUCTION TO MEDICLINIC

WHAT WE DO

11

• Acute care, specialist orientated, multi-

disciplinary hospital services and

related service offerings

o ER24

o Medical Human Resources (MHR)

o Medical Innovations

• 6 higher education accredited nurse

training centres

Source: Company information

12

REGULATORY

CONTEXT

THE HEALTH MARKET INQUIRY

REGULATORY CONTEXT

13

• The Constitution

• The National Health Act

o OHSC

• Competition Act

• Medical Schemes Act

• Regulatory Authorities

o HPCSA; SANC; SAPC; Competition

Authorities

• Provincial Departments of Health

Licensing Regulations

14

MEDICLINIC

BUSINESS MODEL

15

MEDICLINIC BUSINESS MODEL

PROVIDER ENVIRONMENT

HOSPITAL:

• Infrastructure (Land, Buildings, Equipment)

• Clinical Services (Nursing, Pharmacy)

• Support Services (Technical, Admin, Other)

• Separate Account

DOCTORS:

• Admission of Patients

• Management of Clinical Process

• Separate Account

RADIOLOGISTS, PATHOLOGISTS, AND ALLIED

HEALTHCARE PROFESSIONALS:

• Act on instruction from referring doctor

• Separate Account

Source: Company information

MEDICLINIC BUSINESS MODEL

COMPOSITION OF HOSPITAL ACCOUNT

Fee Income Accommodation (General Ward)

tariff code(price) x quantity (volume) xxx

Accommodation(ICU)

tariff code(price) x quantity (volume) xxx

Total Accommodation XXX

Theatre tariff code(price) x quantity (volume) xxx

Equipment tariff code(price) x quantity (volume) xxx

Total Fee Income XXX

Pharmaceutical Items

Ethicals tariff code(price) x quantity (volume) xxx

Surgicals tariff code(price) x quantity (volume) xxx

Total Pharmacy XXX

TOTAL ACCOUNT (INCL. VAT) XXX

ILLUSTRATIVE EXAMPLE: COMPOSITION OF A TYPICAL HOSPITAL ACCOUNT (INCL. VAT)

16

MEDICLINIC BUSINESS MODEL

COMPOSITION OF HOSPITAL ACCOUNT

9%

18%

73%

Pharmacy 27%Ethicals/Medicines

Surgicals/Medical Devices

Fee Income: Ward, Theatre and Equipment

Source: Company information

OVERVIEW OF A TYPICAL HOSPITAL ACCOUNT

17

MEDICLINIC BUSINESS MODEL

COMPOSITION OF HOSPITAL ACCOUNT

Pharmacy Component

Ethicals/Medicines

Regulated by SEP

(No dispensing fee charged)

Surgicals/Medical Devices

SEP does not apply

Billed at cost (Net Acquisition Price)

Source: Company information

OVERVIEW OF THE PHARMACEUTICAL COMPONENTS

18

19

MEDICLINIC BUSINESS MODEL

INPUT COSTS

• Hospitals are highly labour and capital

intensive facilities

• Capital costs are not directly factored

into the tariff escalation calculations

• Tariffs should be sufficient for:

o the replacement of capital items

and;

o the opportunity cost of the

capital employed

20

MEDICLINIC BUSINESS MODEL

BREAKDOWN OF OPERATING COSTS

Input Weights

Nursing Salaries Between 47% and 51%

Other Salaries (Admin, Pharmacy, Technical) Between 14% and 18%

Repairs and Maintenance Between 4% and 6%

Electricity and Water Between 2% and 4%

Rates and Taxes Between 1% and 2%

Catering, Laundry and Cleaning Between 7% and 9%

Other (ICT, Audit Fees, Insurance, etc) Between 16% and 20%

INPUT COST AS % OF OPERATING COST (EXCL. PHARMACY)

Source: Company information

21

MEDICLINIC BUSINESS MODEL

CAPITAL COSTS

• Specialised building according to

regulations

• Specialised medical equipment,

mainly imported and complying with

European and American patient

safety and quality standards

• Technology innovation

22

PATIENTS

23

• “Patients First @ Mediclinic”

• Value of care delivered through:

o Superior clinical quality;

o Maximising the patient experience;

o Managing cost efficiencies

Source: “The Strategy That Will Fix Health Care”, Michael E. Porter, Thomas H. Lee; Company information

VALUE =Clinical Quality X Patient Satisfaction

Cost per Event

PATIENTS

THE VALUE EQUATION

24

PATIENTS

HOSPITAL COMMUNICATION

Source: Company information

• Website

o Pre-admission form

o Explanation of hospital billing

o Private tariff schedule

o Doctor/hospital search

• Nurse driven pre-admission clinic

• Provide information on medical scheme’s

benefits

• Communicate with medical scheme on

patient’s behalf

• Patient complaint and compliment system

25

STRUCTURE

PROCESS

OUTCOME

• COHSASA Accreditation

• Department of Health Inspections

• National Core Standards

• Organisational Structure

• CURA Clinical Risk Register & Audits

• Best Care…Always! Compliance

• Icnet Surveillance

• Clinical Key Performance Indicators

• Outcome Databases

• HEM System/Legal Reports

PATIENTS

CLINICAL QUALITY INITIATIVES

Source: Company information

26

PATIENTS

CLINICAL QUALITY INITIATIVES

ANTIMICROBIAL UTILISATION INDICATORS – MEDICLINIC SOUTHERN AFRICA (2012- 2015 (YTD))

4,13,3

11,3

3,23,42,5

8,4

3,23,22,4

8,6

2,93,12,2

7,1

2,8

0,0

2,0

4,0

6,0

8,0

10,0

12,0

Catheter Associated UrinaryTract Infections

Central Line-associatedBloodstream Infections

Ventilator AssociatedPneumonia

Surgical Site Infections (per1,000 Theatre Cases)

Rat

e p

er 1

,00

0 D

evic

e D

ays

2012

2013

2014

2015 (YTD)

13%

10%

7%6%

0%

2%

4%

6%

8%

10%

12%

14%

Undesirable Agents Utilised forSurgical Prophylaxis

Pe

rce

nta

ge U

nd

esir

able

P

rop

hyl

axis

(%

)

3,23,0

2,7 2,6

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

Days on Multi-cover (≥4 Antimicrobials) Antimicrobial Utilisation Indicators

Rate

pe

r 1

,00

0 D

ays

(%)

6,7

6,8

7,2 7,2

6,4

6,5

6,6

6,7

6,8

6,9

7,0

7,1

7,2

7,3

Prolonged Treatment per 1,000 Exposures

Ra

te p

er

1,0

00

Ex

po

su

res

DEVICE ASSOCIATED INFECTIONS – MEDICLINIC SOUTHERN AFRICA (2012- 2015 (YTD))

Source: Company information

27

PATIENTS

PATIENT EXPERIENCE

PRESS GANEY – MEDICLINIC SOUTHERN AFRICA (2014- 2016 (JAN))

Source: Company information

10 improvement opportunities

for every hospital: to make the

biggest impact on the patient’s

experience, where it matters

most

24 897 patient voices

heard from the survey’s

inception on 1 September

2014 – 25 January 2016

Average eSurvey

response rate: 21%

MCSA results bench-

marked against more than

1 800 hospitals globally

28

PATIENTS

PATIENT EXPERIENCE

Source: Press Ganey

PRESS GANEY INPATIENT

Survey Section

MCSA Average Mean

Score

Press Ganey Average Mean

Score

Overall 81.7 87.1

Admission 85.5 87.8

Room 77.2 84.3

Meals 77.5 82.5

Nurses 81.5 90.5

Tests and Treatments 82.7 88.1

Visitors and Family 82.0 89.0

Physician 85.5 87.8

Discharge 81.0 85.8

Personal Issues 80.0 87.2

Overall Assessment 84.7 90.4

MEDICLINIC SOUTHERN AFRICA PATIENT SATISFACTION SURVEY SECTION SCORES (2015)

29

MEDICLINIC INITIATIVES

COST PER EVENT

0,7

0,9

1,1

1,3

1,5

2013 2014 2015

Ob

se

rve

d/E

xp

ec

ted

(O

E)

Ra

tio

OE Bed Days OE Pharmacy OE Prosthesis OE Theatre Minutes

EXAMPLE: HOSPITAL ENGAGEMENT WITH A DOCTOR ON COST PER EVENT (INITIAL KNEE REPLACEMENT)

Source: Company information

30

HEALTHCARE

PROFESSIONALS

773,34

591,24

436,37

403

326,44

213,06

174,86

111,47

0 100 200 300 400 500 600 700 800 900

OECD countries

Developing Europe and Central Asia

Developing Latin America and Caribbean

South Africa (2013) adjusted

World

Developing Middle East and North Africa

Developing East Asia and Pacific

Developing Sub-Saharan Africa

31

HEALTHCARE PROFESSIONALS

SHORTAGE OF HEALTHCARE PROFESSIONALS

Source: Econex Presentation, HASA conference 2014

272,06

260,82

197,47

154,42

152,19

142,17

77,60

19,95

0 50 100 150 200 250 300

OECD countries

Developing Europe and Central Asia

Developing Latin America and Caribbean

Developing East Asia and Pacific

World

Developing Middle East and North Africa

South Africa (2013)

Developing Sub-Saharan Africa

DOCTORS (GPS AND SPECIALISTS) PER 100,000 PEOPLE

NUMBER OF TOTAL NURSES PER 100,000 PEOPLE (2010 OR LATEST YEAR AVAILABLE)

32

• Clinical and business independence

o Admit and discharge patients

• Recruitment

• Admission privileges

• Consulting rooms

• Shareholding

HEALTHCARE PROFESSIONALS

RELATIONSHIP WITH SUPPORTING

DOCTORS

Source: Company information

33

MEDICAL SCHEMES,

ADMINISTRATORS AND

MANAGED CARE

ORGANISATIONS

34

• National tariff negotiations

• Robust negotiation process

• Countervailing power through:

o Scheme size

o Comprehensive data

o Network arrangements

• No distinction between PMB and non-PMB

• Information sharing

MEDICAL SCHEMES, ADMINISTRATORS

& MANAGED CARE ORGANISATIONS

Source: Company information

35

SUPPLIERS

AND SUPPORT SERVICES

36

SUPPLIERS AND SUPPORT SERVICES

• Pharmaceutical and medical

equipment suppliers (mainly

imported goods)

• Catering, laundry, cleaning,

security, medical waste

management, etc

Source: Company information

37

EXPENDITURE ON PRIVATE

HOSPITAL SERVICES

38

• Increases in healthcare

expenditure a function of:

1. Price of:

o hospital services

o pharmaceuticals

2. Quantity of medical

services

3. Intensity of the medical

services used

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

Source: Company information

39

2,8%

-0,3%0,9% 0,2%

0,3%

3,0%

4,1%

3,3%

7,7%6,2%

5,8%

6,0%

-2,0%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

2010 2011 2012 2013PE

RC

EN

TA

GE

IN

CR

EA

SE

IN

RE

VE

NU

E

(%)

IntensityPrice Quantity

BREAKDOWN OF MEDICLINIC’S INCREASE IN REVENUE BY SOURCE (2010 - 2013)

Source: Company information

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

0%

20%

40%

60%

80%

100%

120%

140%

Pe

rce

nta

ge

In

cre

as

e in

nu

mb

er

of

ad

mis

sio

ns

INCREASE IN THE NUMBER OF MEDICLINIC ADMISSIONS BY AGE BAND 2002 TO 2013

Source: Company information

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

40

R -

R 5 000

R 10 000

R 15 000

R 20 000

R 25 000

R 30 000

R 35 000

R 40 000

CO

ST

OF

IN

PA

TIE

NT

AD

MIS

SIO

N

THE COST OF A MEDICLINIC INPATIENT ADMISSION BY AGE (2013)

Source: Company information

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

41

7,9%8,7% 9,4% 9,8%

17,7%

20,1%21,4%

22,3%

4,9%5,9%

6,7% 7,3%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

2010 2011 2012 2013Pe

rce

nta

ge

of

Inp

ati

en

t A

dm

iss

ion

s (

%)

Diabetes Hypertension Hyperlipidemia

PERCENTAGE OF INPATIENT ADMISSIONS ADMITTED TO MEDICLINIC WITH DIABETES, HYPERTENSION OR HYPERLIPIDAEMIA (2010-2013)

Source: Company information

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

42

7%

7%8% 8%

5%5%

6% 6%

3%4%

4% 5%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2010 2011 2012 2013

Pe

rce

nta

ge

In

cre

as

e (

%)

2CDL 3 CDL 4 CDL

PERCENTAGE OF MEDICLINIC INPATIENT ADMISSIONS WITH MULTIPLE CHRONIC CONDITIONS (CDL) (2010-2013)

Source: Company information

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

43

R 21 196

R 33 368 R 35 370

R 42 385

R -

R 5 000

R 10 000

R 15 000

R 20 000

R 25 000

R 30 000

R 35 000

R 40 000

R 45 000

No CDL or One CDL Two CDLs Three CDLs Four CDLs

Co

st

pe

r In

pa

tie

nt

Ad

mis

sio

n (

Ra

nd

)

THE COST PER INPATIENT ADMISSION BY THE NUMBER OF CHRONIC CONDITIONS PREVALENT (2013)

Source: Company information

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

44

45

Patient A:

• 50 year old patient

• Normal body mass index

(BMI)

• No underlying chronic

conditions

Expected Account

(Excluding Prosthesis)

Base Cost

Patient B:

• 72 year old patient

• Severely obese

• Diabetes Mellitus

Expected Account

(Excluding Prosthesis)

Additional R7,600

Patient C:

• 85 year old patient

• Morbidly obese

• Diabetes Mellitus

• Hypertension

Expected Account

(Excluding Prosthesis)

Additional

R28,941

HIP REPLACEMENT PROCEDURE (2014)

Source: Company information

EXPENDITURE ON PRIVATE HOSPITAL

SERVICES

DRIVERS OF EXPENDITURE

46

PRICE AND INPUT COST

INCREASES AT

MEDICLINIC’S HOSPITALS

Source: MCSA; “other” refers to For example, security costs, computer costs, insurance and audit fees. 47

• Hospital input cost increases

above CPI

• Nursing salaries are the

largest operating input costs

with high inflation due to the

critical shortage of nurses and

competition for nurses with

the public sector

• Electricity and food show

increases consistently above

CPI

FACTORS DRIVING PRICE INCREASES

HOSPITAL TARIFF INCREASES

Input Weights

Nursing Salaries Between 47% and 51%

Other Salaries (Admin,

Pharmacy, Technical)Between 14% and 18%

Repairs and

MaintenanceBetween 4% and 6%

Electricity and Water Between 2% and 4%

Rates and Taxes Between 1% and 2%

Catering, Laundry and

CleaningBetween 7% and 9%

Other (ICT, Audit Fees,

Insurance, etc.)Between 16% and 20%

INPUT COST AS % OF OPERATING COST

(EXCL. PHARMACY)

48Source: Company Information

FACTORS DRIVING PRICE INCREASES

HOSPITAL TARIFF INCREASES

1,00

1,20

1,40

1,60

1,80

2,00

2,20

2,40

2,60

2,80

2006 2007 2008 2009 2010 2011 2012 2013

Ind

ex

ed

Perc

en

tag

e I

ncre

ase

CPI

Food

Electricity

Weighted nursebasic salaryincreasesMediclinic Tariff

INDEXED INCREASE IN MEDICLINIC’S LARGEST OPERATING INPUT COSTS COMPARED TO THE MEDICLINIC TARIFF INCREASE AND CPI

49

FACTORS DRIVING PRICE INCREASES

CAPITAL EXPENDITURE

Date

BER BCI

(annual rate)

Rand / Euro

exchange rate

(closing rate)

September 2009 -2.86% 10.81

September 2010 -0.28% 9.48

September 2011 6.10% 10.78

September 2012 7.80% 10.69

September 2013 5.00% 13.65

September 2014 8.60% 14.29

Cumulative growth rate (2009 - 2014) 30.06% 32.15%

• Provision for future capital expenditure

o Development cost for new hospitals (R2.5 – R3.5 million per bed)

o Replacement of equipment (2.5% of revenue per annum)

GROWTH IN THE BER BCI AND DEPRECIATION OF THE RAND AGAINST THE EURO

OVER A FIVE YEAR PERIOD

Source: Company Information

50

FACTORS DRIVING PRICE INCREASES

HOSPITAL TARIFF INCREASES

60%

61%

62%

63%

64%

65%

66%

67%

68%

69%

70%

2008 2009 2010 2011 2012 2013

0%

3%

6%

9%

12%

15%

18%

21%

24%

Oc

cu

pa

nc

y R

ate

EB

ITD

AR

/Re

ve

nu

e

Occupancy rate (left axis) EBITDAR/Revenue (right axis)

FIXED COST EFFICIENCY PASSED ON TO MEDICAL SCHEME MEMBERS FROM OPERATIONAL EFFICIENCIES (INCREASING OCCUPANCY)

Source: Company information

51

FACTORS DRIVING PRICE INCREASES

PHARMACEUTICAL COST

• Surgicals/medical devices:

o Prices not regulated

o Prices negotiated with suppliers

o Sold at Net Acquisition Price (at

cost)

• Ethicals/medicines:

o Regulated according to SEP

o No negotiations with suppliers

o SEP does not mean prices in

South Africa are sufficiently

contained

52

FACTORS DRIVING PRICE INCREASES

COMPARATIVE STUDY ON SEP

Product category Weighted average price difference

Anticoagulant -38%

Anaesthetic - parenteral -45%

Haemostatic -61%

IV solution - volume expander -59%

Parenteral nutrition -22%

Surfactant -92%

Product category Weighted average price difference

Anticoagulant -44%

Bone Cement -27%

Cytostatic -48%

IV solution - volume expander -61%

Pain management -59%

Source: Company information

WEIGHTED AVERAGE PRICE DIFFERENTIAL BETWEEN DUBAI AND SOUTH AFRICA (2014)

WEIGHTED AVERAGE PRICE DIFFERENTIAL BETWEEN SWITZERLAND AND SOUTH AFRICA (2014)

Source: Ramjee S, Comparing the cost of hospitalisation across the public and private sectors in South Africa, October 2013 53

Public-sector average cost per admission 8,775

Private-sector average cost per admission 9,284

Ratio of average cost per admission 1.058

FACTORS DRIVING PRICE INCREASES

REASONABLENESS OF PRICE

COMPARISON OF AVERAGE COST PER ADMISSION FOR PRIVATE HOSPITALS 2010 AND PUBLIC HOSPITALS 2010/11

Cost of admission in

private hospital is

only 5.8% higher

than the cost in a

public hospital

54

Private Hospitals

37,6%

Other62,5%

MEDICAL SCHEMES TOTAL BENEFITS PAID 2014

Source: CMS Annual Report 2014/2015; Company information

OVERVIEW OF A TYPICAL HOSPITAL ACCOUNT

15% Discount on Hospital Tariff Equates to:

50% Reduction in Hospital EBITDAR margin

4% Once-off reduction in the contribution rate

(Less than R60 per beneficiary per month on an average premium of R1,410)

9%

18%

73%

Medicines

Medical

Devices

Fee Income:

Ward, Theatre

and Equipment

FACTORS DRIVING PRICE INCREASES

REASONABLENESS OF PRICE

55

• Samples are not comparable

• PPP adjustments are insufficient

• Growth and demographic profile of

medical scheme beneficiaries not

controlled for

• Patient profiles specific to the sample

not controlled for

• Conclusions unsubstantiated due to

flawed analysis

FACTORS DRIVING PRICE INCREASES

OECD/WHO RESPONSE

SOME INITIAL COMMENTS

56

CONCLUDING

REMARKS

Above CPI

Increase

57

• Increases in expenditure by medical

schemes on private hospital services

cannot be benchmarked with reference

to CPI

• Increases in expenditure are driven by

increases in hospital price and

utilisation

• Increases in hospital prices are

marginally above CPI due to above

inflationary increases in significant input

costs

• Increases in utilisation are driven by

amongst others the aging patient

profile, burden of disease and anti-

selection

CONCLUDING REMARKS

Ex

pe

nd

itu

re b

y M

ed

ica

l S

ch

em

es

CP

I

Ho

sp

ital

Pri

ce:

Dri

ven

by I

np

ut

Co

st

Uti

lisati

on

58

CONCLUDING REMARKS

In order to ensure a sustainable

and more efficient private

healthcare market, the focus must

be on:

• Regulatory reform aimed at

ensuring the stability and viability

of the medical scheme risk pool

• Removing barriers to develop

integrated delivery models

• Effective and accessible training

facilities for nurses and doctors

• A more effective public

healthcare sector

QUESTIONS

59