kopernik global investors call... · please consider all risks carefully before investing. the...

TRANSCRIPT

Kopernik Global Investors1Q 2019 Conference Call

Presented by:David B. Iben, CFACIO & Lead Portfolio Manager

The information presented herein is proprietary to Kopernik Global Investors, LLC. This material is approved for a presentation to authorized individuals only and, accordingly, thismaterial is not to be reproduced in whole or in part or used for any purpose except as authorized by Kopernik Global Investors, LLC.

Please consider all risks carefully before investing. The investment strategies managed by Kopernik are subject to certain risks such as market, investment style, interest rate,deflation, and illiquidity risk. Investments in small and mid-capitalization companies also involve greater risk and portfolio price volatility than investments in larger capitalizationstocks. Investing in non-U.S. markets, including emerging and frontier markets, involves certain additional risks, including potential currency fluctuations and controls, restrictionson foreign investments, less governmental supervision and regulation, less liquidity, less disclosure, and the potential for market volatility, expropriation, confiscatory taxation, andsocial, economic and political instability. Investments in energy and natural resources companies are especially affected by developments in the commodities markets, the supplyof and demand for specific resources, raw materials, products and services, the price of oil and gas, exploration and production spending, government regulation, economicconditions, international political developments, energy conservation efforts and the success of exploration projects. There can be no assurances that investment objectives willbe achieved.

Kopernik Global Investors, LLC is an investment adviser registered under the Investment Advisers Act of 1940, as amended.

This document, as of April 2019 is descriptive of how the Kopernik team manages the investment strategies offered by Kopernik. There is no guarantee that any strategy’sinvestment performance objectives will be achieved. This profile is not legally binding on Kopernik Global Investors, LLC or its affiliates.

© 2019 Kopernik Global Investors, LLC | Two Harbour Place | 302 Knights Run Avenue Suite 1225 | Tampa, Florida 33602 | 813.314.6100 | www.kopernikglobal.com

Important Information

2

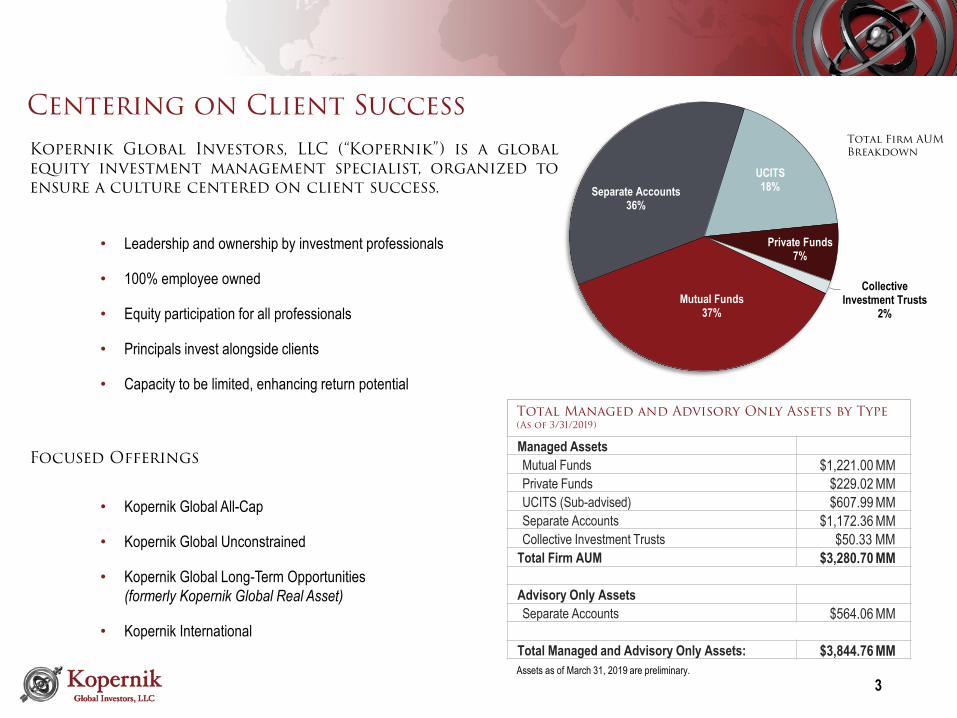

Mutual Funds37%

Separate Accounts36%

UCITS18%

Private Funds7%

Collective Investment Trusts

2%

• Leadership and ownership by investment professionals

• 100% employee owned

• Equity participation for all professionals

• Principals invest alongside clients

• Capacity to be limited, enhancing return potential

3

Total Managed and Advisory Only Assets by Type (As of 3/31/2019)

• Kopernik Global All-Cap

• Kopernik Global Unconstrained

• Kopernik Global Long-Term Opportunities (formerly Kopernik Global Real Asset)

• Kopernik International

Centering on Client Success

Managed AssetsMutual Funds $1,221.00 MMPrivate Funds $229.02 MMUCITS (Sub-advised) $607.99 MMSeparate Accounts $1,172.36 MMCollective Investment Trusts $50.33 MM

Total Firm AUM $3,280.70 MM

Advisory Only AssetsSeparate Accounts $564.06 MM

Total Managed and Advisory Only Assets: $3,844.76 MM

Kopernik Global Investors, LLC (“Kopernik”) is a globalequity investment management specialist, organized toensure a culture centered on client success.

Focused Offerings

Assets as of March 31, 2019 are preliminary.

Total Firm AUM Breakdown

Like our namesake, we are dedicated to reasoning over convention and to clients’ needs above convenience.

Our Investment Beliefs

Independent thought

Long-term global perspective

Limited capacity

Value as a prerequisite

Bottom-up fundamental analysis

Industry-tailored valuations

Group vetting

Mikolaj Kopernik, better known by the Latin spelling, Nicolaus Copernicus, proposed the heliocentric model of the universe in the early 1500s. Whatinterests us is the fact that he trusted his own observations instead of accepting what “everyone” thought to be true. He faced scorn for his “novel andincomprehensible” theses. Though primarily an astronomer, Kopernik set forth a version of the “quantity theory of money,” a principal concept ineconomics to the present day. He also formulated a version of Gresham’s Law, predating Gresham.

As independent thinkers, Kopernik Global Investors honors Mikolaj Kopernik in the contemporary investment world. We believe that accomplishedinvestors who trust their own analyses and instincts can generate significant excess returns as a result of market inefficiencies driven by erroneousprofessional and academic theories and practices.

4

Achieving Value through Independent Thought

5

Q1 in a Nutshell

“The job of the Federal Reserve is to take away the punch bowl just as the party gets going”

William McChesney Martin9th Chairman of the Federal Reserve

6

The Return of Monetary Profligacy

7

• Mnuchin to convene U.S. 'Plunge Protection Team’

• Fed Chairman Powell reverses course says interest rate hikes are not likely anytime soon

• Get Used to the “Powell Put”

• The Fed committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September

• The ECB took investors mostly by surprise in its decision to announce a new round of stimulus

• Kuroda brushes aside that BOJ has run out of tools to ease monetary policy - "There has been no change to our stance of buying large amounts of government bonds," Kuroda said

• China’s Credit Growth Surges Back - Aggregate financing was 2.86 trillion yuan ($426 billion) last month, compared with about 700 billion yuan in February - the People’s Bank of China

8

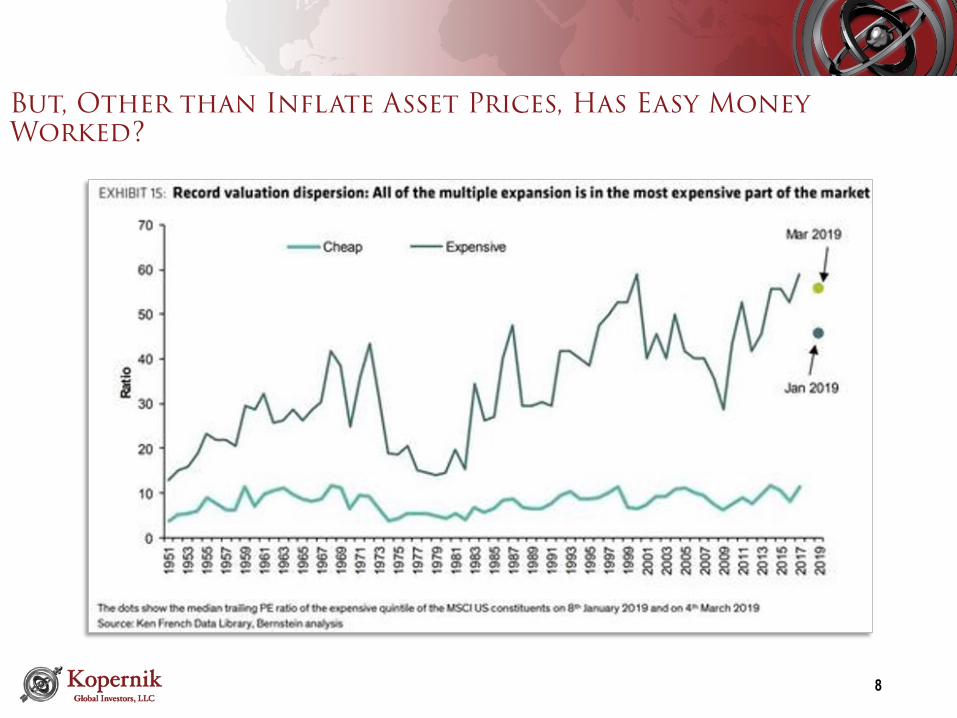

But, Other than Inflate Asset Prices, Has Easy Money Worked?

9

We are told that QE workedWe are told that MMT portends Nirvana;

This seems like an excellent time to employ Independent Thought.

10

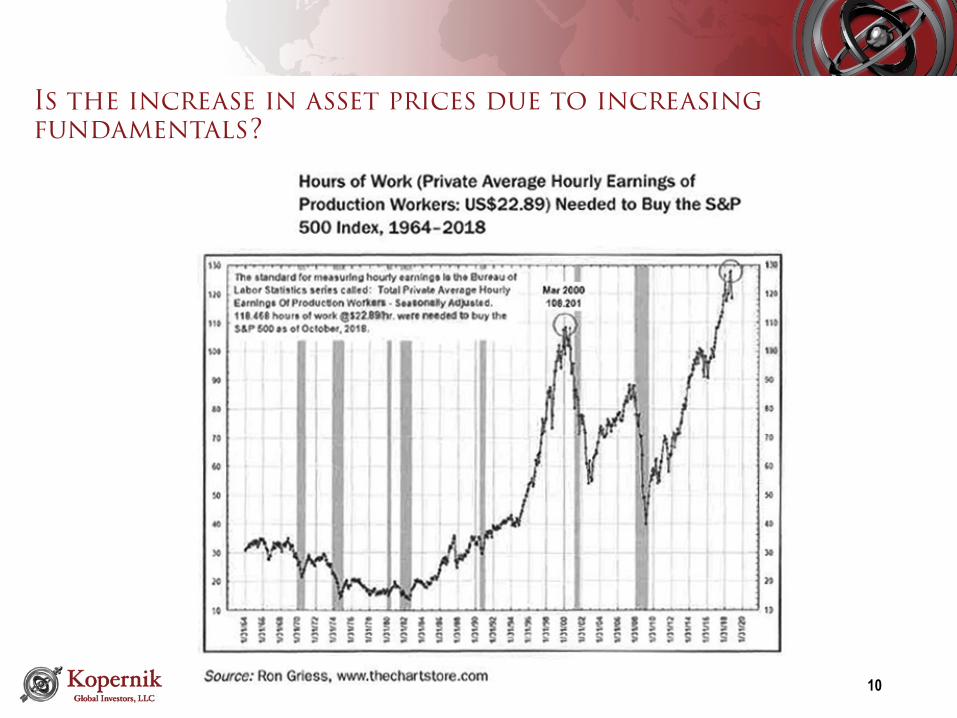

Is the increase in asset prices due to increasing fundamentals?

11

Prices and fundamentals are Diverging

12

Synchronized Global Economic Slowdown

13

Inequality back to 1929 levels

14

Student Loan Troubles

15

16

Source: Bloomberg.com

Auto Loan at GFC Delinquency Levels

17

Potentially a larger problem

18

Sovereign Debt has Become a Major Problem

affecting QE driven economies such as the U.S., Japan, and China

19

Source: BLS

Inflationary Symptoms are important areas

And what about asset inflation?

Stocks?Bonds?

Real Estate?

20

No Inflation?

Is it a coincidence that the Federal Reserve was founded just over 100

years ago?

21

Policy of consumption, rather than production

22

Since 1999, write-offs and write-downs for the companies in the S&P 500 totaled $220.92 per share,more than $1.84 trillion! Cumulative operating earnings totaled $1,616 per share, or $13.5 trillion, so theshave was 13.6% of S&P defined operating earnings.

S&P 500 SAI Accounting Adjustments 2018 Dollar Adjustment Per Share Adjustment

Write-offs and Write-downs ($195 B) ($23.55)

Pensions ($70 B) ($8.35)

Amortization of Intangibles $30 B $3.53

Total ($235 B) ($28.37)

Source: Semper Augustus, 13D Global Strategy & Research - Feb 28 2019

Do Lax Monetary Standards Lead to Lax Accounting Standards?

23

Does mindless monetary standards lead to mindless investments?

24

Does careless monetary standards lead to careless investment?

25

Does ill advised monetary policy lead to mal-investment?

26

Is it a coincidence that the flows into assets roughly match the amount printed by the Fed?

27

How much higher can the U.S. Markets go?

28

Investment Strategy

Inquiring Minds Want to Know!

We Believe that this will be a Stock-Pickers Market; A Thinking Person’s Market!

• Is It Possible For Bureaucrats to Conjure Wealth Out of Thin Air?

• Can Governments Borrow Their Way to Prosperity?

• Is the Best Way to Invest Sans Analysis? Really?

• Does a Government’s Weak Financial Position Truly Justify Lower Rates of Interest?

• Is Supply No Longer a Determinant of Price; Only Demand Matters Now?

• Are Good Stories Really More Valuable than Good Economics?

29

“Hit em where they ain’t” – Wee Willie Keeler

30

Where they Ain’t is outside of the United States

31

Source: Ed Yardeni, www.yardeni.com

Which is a great opportunity, because that’s where the growth & the Production is (especially in EM)

32

Notice the diverging productivity trends

33Source: Bloomberg.com

$-

$50

$100

$150

$200

$250

Jul-13 Jul-14 Jul-15 Jul-16 Jul-17 Jul-18

Emerging Markets vs NASDAQ vs Gold Miners vs RTSI IndexJuly 2013 – April 2019

iShares MSCI Emerging Markets Indx (EEM US) VanEck Vectors Gold Miners ETF (GDX US) NASDAQ Composite Index (CCMP Index) Russian Trading System Cash Index (RTSI Index)

In their rush to buy FAANG, they left a lot of resources behind.

34

Commodities are arguably the cheapest ever

35

$95

$97

$99

$101

$103

$105

$107

$109

$111

$113

Dec-18 Jan-19 Feb-19 Mar-19

Gold vs Copper vs Silver Jan 2019 – April 2019

Gold Copper Silver

Source: Bloomberg.com

They especially don’t like precious metals

36

Source: Bloomberg.com

(20)

(10)

-

10

20

30

40

Dec-18 Jan-19 Feb-19 Mar-19

Uranium vs Crude Oil vs Natural GasJan 2019 – April 2019

Uranium (UXA1) Crude Oil (CLA) Natural Gas (NGA)

They don’t like clean energy anymore

37

Security Changes in Global All-Cap Rep Account12/1/18 - 2/28/19

New Net Added to Net Reduced Eliminated

Astarta Holding NV Centrais Eletricas Brasileiras China Yurun Food Group Ltd

Draegerwerk AG & Co KGaA China Mobile Ltd Diebold Nixdorf Inc

Hankook Tire Worldwide Co Ltd General Electric Co Goldcorp Inc

Hemas Holdings PLC Mitsubishi Corp Kinross Gold Corp

Northern Dynasty Minerals Ltd West Japan Railway Co Korea Electric Power Corp

Range Resources Corp Wheaton Precious Metals Corp

Turquoise Hill Resources Ltd

They don’t like volatility!

38

Security Changes in International Rep Account12/1/18 - 2/28/19

New Net Added to Net Reduced Eliminated

Turquoise Hill Resources Ltd Centrais Eletricas Brasileiras Kinross Gold Corp

China Mobile Ltd Korea Electric Power Corp

LUKOIL PJSC

“It’s not enough to be different – you also need to be correct. The problem is thatextraordinary performance comes only from correct nonconsensual forecasts, butnonconsensual forecasts are hard to make, hard to make correctly, and hard to act on. ”

- Howard Marks

Characteristics above are based on the holdings of a model portfolio as of March 31, 2019 and are calculated using data from Bloomberg. Harmonic weighted average is a method of calculating an average value that lessensthe impact of large outliers. The MSCI All Country World Index is a broad-based securities market index that captures over two thousand primarily large- and mid-cap companies across 23 developed and 24 emerging marketcountries. The MSCI All Country World ex U.S. Index is a broad-based securities market index that captures over two thousand primarily large- and mid-cap companies across 22 developed and 24 emerging market countries.The MSCI All Country World Index and the MSCI All Country World ex U.S. Index are different from the strategy in a number of material respects, including being much more diversified among companies and countries,having less exposure to emerging market and small-cap companies, having no exposure to frontier markets and having no ability to invest in fixed income or derivative securities.

39

As of March 31, 2019

1.59

0.66

2.24

0.62

Trailing P/B Ratio(Price to Book)

Global All-Cap

MSCI ACWI

International

MSCI ACWI ex USA

$70,735

$15,005

$152,257

$12,578

Weighted Average Market Cap ($USD, Millions)

MSCI ACWI

MSCI ACWI ex USA

G

I

1.84

0.68

2.40

0.64

Trailing P/TBV Ratio(Price to Tangible Book Value)

Global All-Cap

MSCI ACWI

International

MSCI ACWI ex USA

$8,441

$3,757

$10,166

$1,472

Median Market Cap ($USD, Millions)

G

MSCI ACWI

International

MSCI ACWI ex USA

1.49

0.97

1.89

1.07

Trailing EV/S Ratio(Enterprise Value to Sale)

Global All-Cap

MSCI ACWI

International

MSCI ACWI ex USA

14.64

7.65

16.76

10.07

Trailing P/E Ratio(Price to Earnings)

Global All-Cap

MSCI ACWI

International

MSCI ACWI ex USA

9.03

4.11

10.70

4.57

Trailing P/CF Ratio(Price to Cash Flow)

Global All-Cap

MSCI ACWI

International

MSCI ACWI ex USA

3.27

2.32

2.53

2.31

Yield TTM(Trailing Twelve Months)

Global All-Cap

MSCI ACWI

International

MSCI ACWI ex USA

And they sure don’t like Value!

40

0

5

10

15

20

25

30

Comm.Services

Cons.Disc.

Cons.Staples

Energy Financials HealthCare

Industrials Info.Tech.

Materials RealEstate

Utilities

0

10

20

30

40

50

60

Canada Emerging Markets Europe Japan Pacific ex Japan US

Portfolio Region Weights*

Portfolio Sector Weights* Top Ten HoldingsName Country Port Weight %

Cameco Corp Canada 4.50Newcrest Mining Ltd Australia 4.50KT Corp South Korea 4.25Range Resources Corp United States 4.00Gazprom PJSC Russia 4.00Turquoise Hill Resources Ltd Canada 3.75RusHydro PJSC Russia 3.25Electricite de France SA France 3.00Centerra Gold Inc Canada 3.00Golden Agri-Resources Ltd Singapore 3.00

Global All-Cap – Model Portfolio Characteristics (as of 3/31/2019)

*Does not include Options, which were approximately 1.00% of the portfolio as of March 31, 2019.**Small-Cap = less than $2 billion, Mid-Cap = $2 billion - $10 billion, Large-Cap = greater than $10 billionPortfolio weights and characteristics above are based on the holdings of a model portfolio as of March 31, 2019. Portfolio characteristics, sector and country designations are calculated using data from Bloomberg. The MSCIAll Country World Index is a broad-based securities market index that captures over two thousand primarily large- and mid-cap companies across 23 developed and 24 emerging market countries. The MSCI All Country WorldIndex is different from the strategy in a number of material respects, including being much more diversified among companies and countries, having less exposure to emerging market and small-cap companies, having noexposure to frontier markets and having no ability to invest in fixed income or derivative securities.

Portfolio % MSCI ACWI %Large-Cap** 27.5 90.0Mid-Cap** 33.9 9.9Small-Cap** 31.4 0.1

Developed Markets 56.5 88.3Emerging Markets 37.3 11.7

U.S. 5.8 55.0Non U.S. 88.0 45.0

Portfolio Characteristics

Excludes non-equity securities

41

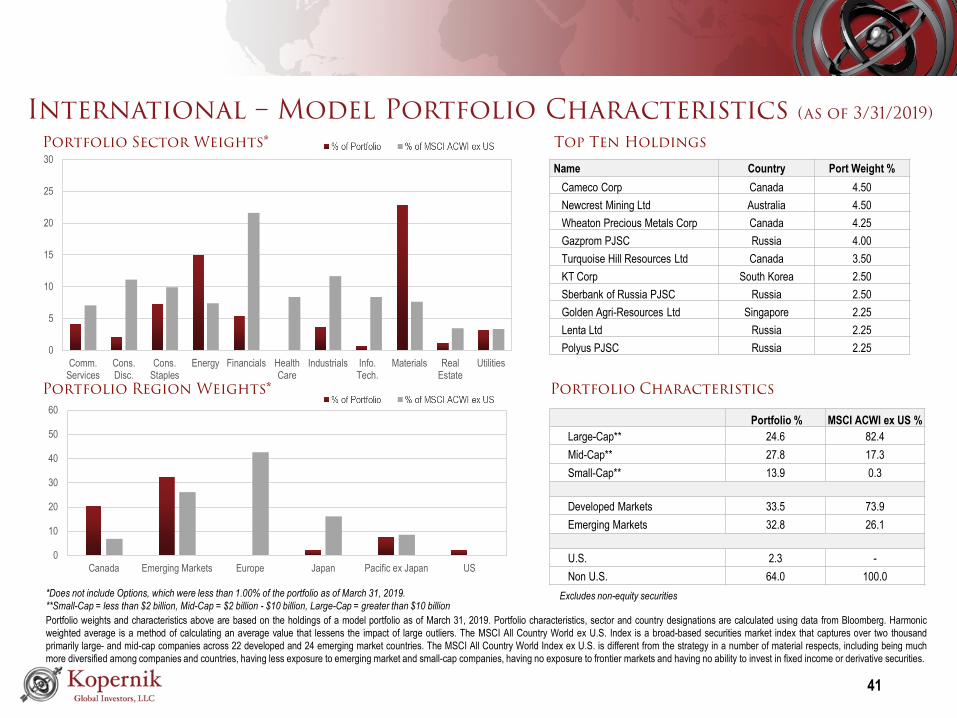

0

5

10

15

20

25

30

Comm.Services

Cons.Disc.

Cons.Staples

Energy Financials HealthCare

Industrials Info.Tech.

Materials RealEstate

Utilities

0

10

20

30

40

50

60

Canada Emerging Markets Europe Japan Pacific ex Japan US

Portfolio Region Weights*

Portfolio Sector Weights* Top Ten HoldingsName Country Port Weight %

Cameco Corp Canada 4.50Newcrest Mining Ltd Australia 4.50Wheaton Precious Metals Corp Canada 4.25Gazprom PJSC Russia 4.00Turquoise Hill Resources Ltd Canada 3.50KT Corp South Korea 2.50Sberbank of Russia PJSC Russia 2.50Golden Agri-Resources Ltd Singapore 2.25Lenta Ltd Russia 2.25Polyus PJSC Russia 2.25

International – Model Portfolio Characteristics (as of 3/31/2019)

*Does not include Options, which were less than 1.00% of the portfolio as of March 31, 2019.**Small-Cap = less than $2 billion, Mid-Cap = $2 billion - $10 billion, Large-Cap = greater than $10 billionPortfolio weights and characteristics above are based on the holdings of a model portfolio as of March 31, 2019. Portfolio characteristics, sector and country designations are calculated using data from Bloomberg. Harmonicweighted average is a method of calculating an average value that lessens the impact of large outliers. The MSCI All Country World ex U.S. Index is a broad-based securities market index that captures over two thousandprimarily large- and mid-cap companies across 22 developed and 24 emerging market countries. The MSCI All Country World Index ex U.S. is different from the strategy in a number of material respects, including being muchmore diversified among companies and countries, having less exposure to emerging market and small-cap companies, having no exposure to frontier markets and having no ability to invest in fixed income or derivative securities.

Portfolio % MSCI ACWI ex US %Large-Cap** 24.6 82.4Mid-Cap** 27.8 17.3Small-Cap** 13.9 0.3

Developed Markets 33.5 73.9Emerging Markets 32.8 26.1

U.S. 2.3 -Non U.S. 64.0 100.0

Portfolio Characteristics

Excludes non-equity securities

This “Return on patience” should prove unusually high

Potential UpsideYear 50.0% 100.0% 150.0%

1 50.0% 100.0% 150.0%

Inte

rnal

Rate

of R

etur

n

2 22.5% 41.2% 58.1%

3 14.5% 26.0% 35.7%

4 10.7% 18.9% 25.7%

5 8.5% 14.9% 20.1%

6 7.0% 12.3% 16.5%

7 6.0% 10.4% 14.0%

8 5.2% 9.1% 12.1%

9 4.6% 8.0% 10.7%

10 4.1% 7.2% 9.6%

The “Return on Patience” Appears Exceptionally High!

“Why is it that it takes a real bear market to get analysts interested in the value approach?”

-Benjamin Graham

“In the short run, the market is a voting machine but in the longrun, it is a weighing machine.”

-Benjamin Graham

“Patient opportunism – waiting for bargains – is often your best strategy”

–Howard Marks

“I think the record shows the advantage of a peculiar mind-set –not seeking action for its own sake, but instead combiningextreme patience with extreme decisiveness”

-Charlie Munger

“Patience can produce uncommon profits” -Philip L. Carret

“The big profits go to the intelligent, careful and patient investor,not to the reckless and overeager speculator”

-J. Paul Getty"[There] is the need for patience if big profits are to be made frominvestment. Put another way, it is often easier to tell what willhappen to the price of a stock than how much time will elapsebefore it happens"

-Phil Fisher

THANK YOU

Q&A Session