korea western power co., ltd. rating review presentation to standard & poor’s 26 july 2007

TRANSCRIPT

Korea Western Power Co., Ltd.Korea Western Power Co., Ltd.

Rating Review Presentation toRating Review Presentation toStandard & Poor’sStandard & Poor’s

26 July 2007 26 July 2007

2Rating Review Presentation to Standard & Poor’s

Company OverviewCompany Overview

OperationsOperations

Financial ManagementFinancial Management

Concluding Remarks Concluding Remarks

Table of Contents

3Rating Review Presentation to Standard & Poor’s

Introduction to KOWEPO

1. Applied FX rate : KRW 920/USD 2. 1H 2007 financial figures are provisional figures

Inception Inception Inception Inception Spun off from KEPCO in April 2, 2001 Spun off from KEPCO in April 2, 2001

OwnershipOwnershipOwnershipOwnership 100% owned by KEPCO (54% owned by Korean Government) 100% owned by KEPCO (54% owned by Korean Government)

Generation Generation CapacityCapacity

Generation Generation CapacityCapacity 9,585.3 MW (Operation: 8,380.1 MW, Under Construction: 1,205.2 MW) 9,585.3 MW (Operation: 8,380.1 MW, Under Construction: 1,205.2 MW)

Total AssetsTotal AssetsTotal AssetsTotal Assets 1H 2007 : KRW 3,720 bn (USD 4.1 bn)

FY2006 : KRW 3,708 bn (USD 4.0 bn)

1H 2007 : KRW 3,720 bn (USD 4.1 bn)

FY2006 : KRW 3,708 bn (USD 4.0 bn)

Total Total RevenueRevenue

Total Total RevenueRevenue

1H 2007 : KRW 1,535 bn (USD 1.7 bn)

FY2006 : KRW 2,424 bn (USD 2.6 bn)

1H 2007 : KRW 1,535 bn (USD 1.7 bn)

FY2006 : KRW 2,424 bn (USD 2.6 bn)

Net IncomeNet IncomeNet IncomeNet Income 1H 2007 : KRW 118 bn (USD 128.8 mn)

FY2006 : KRW 160 bn (USD 173.9 mn)

1H 2007 : KRW 118 bn (USD 128.8 mn)

FY2006 : KRW 160 bn (USD 173.9 mn)

Credit Credit RatingsRatings

Credit Credit RatingsRatings S&P : A- (stable) / Moody’s : A1 (stable) S&P : A- (stable) / Moody’s : A1 (stable)

4Rating Review Presentation to Standard & Poor’s

Operation Overview

Note: T/P denotes “Thermal Power Plant”, C/C denotes “Combined Cycle”, P/S denotes “Pumped Storage”

Base load, intermediate load, and peak load account for 42%, 17% and 41% respectively in terms of generation capacity in operation

Over 85% of capacity is located in or near the Seoul and Gyeonggi metropolitan areas

– Seoul and Gyeonggi metropolitan areas comprise approximately 40% of total national demand

Generation Capacity by Type of Plant(1H 2007)

1,400MW

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Base Load Intermediate Load Peak Load

In Operation Under Construction

Taean T/P(3,500 MW)

Pyeongtaek T/P(1,400 MW)

4,180MW4,000MW

Taean T/P (500 MW)

Seoincheon C/C

(1,800 MW)

Samrangjin P/S (600 MW)

CheongsongP/S (600 MW)

PyeongtaekC/C (480 MW)

Location of Plant Complex

TaeanPyeongtaek

Gunsan(under construction)

Cheongsong

CoalLNGBC OilPumped Storage

Seoincheon

Samrangjin

Seoul Metropolitan Area

GunsanC/C (700 MW)

5Rating Review Presentation to Standard & Poor’s

Power Plant Facilities in Operation

Plant TypeFuel Type

Number of Units

Unit Capacity

(MW)

Total Capacity

(MW)Year of Establishment

Taean

(Chungnam)

Thermal Bituminous 7 500 3,500#1:’95.6, #2:’95.12, #3:’97.3, #4:’97.8

#5:’01.10, #6:’02.5, #7:’07.2

Solar - 1 0.1 0.1 ’05.8

Pyeongtaek

(Gyeonggi)

Thermal BC Oil 4 350 1,400 #1:’80.4, #2:’80.6, #3:’83.5, #4:’83.8

Combined

CycleLNG

4

1

80

160

320

160

GT:’92.6

ST:’94.6

Seoincheon

(Incheon)

Combined

CycleLNG

8

8

150

75

1,200

600

GT:’92.6

ST:’92.11

Samrangjin

(Gyeongnam)

Pumped

Storage- 2 300 600 #1:’85.11, #2:’85.12

Cheongsong

(Gyeongbuk)

Pumped

Storage- 2 300 600 #1:’06.9, #2:’06.12

Total 37 8,380.1

KOWEPO operates 37 generation units with total generation capacity of 8,380.1MW in 5 different sites

6Rating Review Presentation to Standard & Poor’s

Strategy – Develop Growth Engine

Plant TypeGeneration

capacity (MW)

Expected completion of Construction

Remarks

Under Construction

Taean #8 Thermal 500 Aug 2007 -

Gunsan Combined Cycle 700 Nov 2009 -

New Plants

Taean IGCC (Integrated Gasification

Combined Cycle)300 Sep 2015 -

Equity Investments

Garorim Tidal Power 480 Dec 2012

Consortium with Posco E&C, Daewoo E&C, Lotte E&C

Project financing KOWEPO to be in charge of operation and

maintenance

Godeok Combined Cycle 700 June 2011

Consortium with SK E&C, SK E&S Project financing KOWEPO to be in charge of operation and

maintenance

Yangju Combined Cycle 1,400 Dec 2013

Consortium with Daelim Industry Project financing KOWEPO to be in charge of operation and

maintenance

KOWEPO plans to maintain its leading market position and superior operating performance promoting growth with new plant constructions

7Rating Review Presentation to Standard & Poor’s

Strategy – Diversify Revenue Sources

Plant TypeGeneration

capacity (MW)

Remarks

New Business

Community Energy System

- 923Gcal/h

Plan to use Seoincheon C/C’s stream and waste heat Consortium with Lotte E&C, Incheon City Gas and Kenertec Expected to begin providing heat from Jan 2008

Overseas Project

Laos Hydro Power 372

Consortium with SK E&C / Project financing BOOT (Build, Own, Operate, Transfer) MOU agreement between the government of Laos and domestic consortium KOWEPO to be in charge of operation and maintenance

IndonesiaThermal Power

400

Consortium with Hanwha and Koresia / Project financing BOOT (Build, Own, Operate, Transfer) MOU agreement between the government of Sumatra and Koresia KOWEPO to be in charge of operation and maintenance

New/Renewable Energy

Samrangjin Solar Power 3,000kW Expected to complete construction in Dec. 2008

TaeanSmall Hydro

Power2,200kW Expected to complete construction in Sep. 2007

KOWEPO will diversify its revenue sources by investing in new business, overseas project, and new/renewable energy

8Rating Review Presentation to Standard & Poor’s

Company OverviewCompany Overview

OperationsOperations

Financial ManagementFinancial Management

Concluding Remarks Concluding Remarks

Table of Contents

9Rating Review Presentation to Standard & Poor’s

KOWEPO8,38012.6%

KOSEP7,19810.8%

KOMIPO8,50112.7%

KOSPO7,75111.6%

EWP9,00113.5%

KHNP18,25227.4%

Others7,59011.4%

KOWEPO’s Market Position

Sales Volume Market Share (1H 2007)Generation Capacity Market Share (1H 2007)

Total Generation Capacity66,673 MW

Total Electricity Sales183,259 GWh

(MW) (GWh) Others4,8762.6%

KHNP67,56636.9%

EWP21,56611.8%

KOSPO24,79313.5%

KOMIPO19,91610.9%

KOSEP21,31211.6%

KOWEPO23,22912.7%

10Rating Review Presentation to Standard & Poor’s

Operational Efficiency

Thermal efficiency and utilization rate have been relatively stable over the years.

In the 1H 2007, the utilization rate has substantially increased due to the completion of Taean #7 and the increased utilization rate of Pyeongtaek power plant

Utilization Rate Thermal Efficiency

40.8

41.4 41.341.1

40.8

40.240.5

40.8

40.3

37.0

38.0

39.0

40.0

41.0

42.0

2003 2004 2005 2006 2007

(%)

Full year 1H

59.7

60.7

59.6

64.9

59.259.1 59.3

57.6

58.6

52.0

54.0

56.0

58.0

60.0

62.0

64.0

66.0

2003 2004 2005 2006 2007

(%)

Full year 1H

11Rating Review Presentation to Standard & Poor’s

Long-Term Supply Contracts

Bituminous

Supplier Country Contract Amount (1,000 ton/year)

Terms

Xstrata Australia 1,100 ‘01.04 ~ ‘09.12Ensham Australia 500 ‘04.01 ~ ‘08.12Peabody Australia 240 ‘05.01 ~ ‘07.12Centennial Australia 500 ‘04.07 ~ ‘10.06BHP-Billiton Australia 500 ‘95.01 ~ ‘07.12Resouce Pacific Australia 250 ‘07.01 ~ ‘09.12Flame Australia 500 ‘07.01 ~ ‘09.12ECM Australia 375 ‘07.01 ~ ‘09.12

Australia - Sub-total 3,965 (47%) SCIEGC China 1,000 ‘99.04 ~ ‘07.07CCIEC China 500 ‘96.01 ~ ‘07.07SHENHUA China 960 ‘01.07 ~ ‘09.06Minmetals China 180 ‘06.04 ~ ‘09.03China - Sub-total 2,640 (31%) Indominco Indonesia 500 ‘03.10 ~ ‘09.12

ABK Indonesia 500 ‘04.10 ~ ‘07.12

Tanito Harum Indonesia 200 ‘05.01 ~ ‘07.12

Peabody Indonesia 325 ‘06.04 ~ ‘09.03

ECM Indonesia 300 ‘06.04 ~ ‘09.03

Indonesia - Sub-total 1,825 (22%) 8,430 (100%)

Fuel Oil Type Supplier Contract amount TermsB.C oil (Sulfa 2.5%) SK Corp. 279,000 ㎘ ‘07.07 ~ 12Kerosene for boiler SK Incheon Oil 3,511 ㎘ ‘07.07 ~ 12

LNG Supplier Contract amount (1,000 ton/year)

Terms

LNG KOGAS 1,490 ‘07 – ‘26 (20year)

KOWEPO enters into long-term supply contracts to:

– Control the costs of bituminous coal, oil and LNG amid the rising prices

– Assure an adequate supply of the raw materials for a smooth operation

Bituminous Coal Contracts

12Rating Review Presentation to Standard & Poor’s

Company OverviewCompany Overview

OperationsOperations

Financial ManagementFinancial Management

Concluding Remarks Concluding Remarks

Table of Contents

13Rating Review Presentation to Standard & Poor’s

Capital Structure (1H 2007)

Capital Structure

2,976

3,262

3,708 3,720

1,351

3,038

2,3692,3022,198

2,0601,988

1,406

1,064916

1,050

0

1,000

2,000

3,000

4,000

2003 2004 2005 2006 1H 2007(K

RW

bill

ion

)

Total assets

Total shareholders' equity

Total Liability

AssetsAssetsAssetsAssets KRW 3,720 billion

– Fixed Assets/Total Assets Ratio : 89.4%

KRW 3,720 billion – Fixed Assets/Total Assets

Ratio : 89.4%

LiabilityLiabilityLiabilityLiability KRW 1,351 billion

– Liability-to-Equity Ratio : 57.0%

KRW 1,351 billion– Liability-to-Equity Ratio :

57.0%

ShareholdeShareholders’ Equityrs’ Equity

ShareholdeShareholders’ Equityrs’ Equity

KRW 2,369 billion– Stake is wholly owned by

KEPCO

KRW 2,369 billion– Stake is wholly owned by

KEPCO

RevenueRevenueRevenueRevenue KRW 1,535 billion KRW 1,535 billion

EBITEBITEBITEBIT KRW 177 billion

– Net Income : KRW 118 billion

KRW 177 billion – Net Income : KRW 118

billion

14Rating Review Presentation to Standard & Poor’s

Financial Performance

Sales revenue shows a stable growth rate since 2004 EBIT continues to remain stable since 2004 but in the second half of 2006, EBIT declined due to

temporary price cut in CP of base load facilities EBIT is expected to improve going forward due to the CBP market improvement and operation

of Taean #7 and 8

EBITRevenue

2,057.72,227.0

2,424.1

1,534.8

2,134.4

1,235.01,101.3

997.81,058.1

0

500

1,000

1,500

2,000

2,500

3,000

2003 2004 2005 2006 2007

(KR

W b

illio

n)

Full year 1H

260.8 255.7226.4

177.3

428.9

179.9160.9

139.7

213.7

0

100

200

300

400

500

2003 2004 2005 2006 2007

(KR

W b

illio

n)

Full year 1H

15Rating Review Presentation to Standard & Poor’s

Healthy Coverage and Leverage Ratio

Coverage ratios have been stable and relatively strong due to KOWEPO’s proactive debt restructuring efforts

KOWEPO has acquired the right to use connecting line to transmission facilities of KEPCO in 2007, in which KOWEPO is making installment payments to KEPCO for the usage of the facilities. However, it is fully compensated by capacity payment. Therefore, any increase in leverage ratio from this does not mean KOWEPO’s financial status deteriorates

LeverageCoverage

7.0

5.7

8.3

5.7

6.8

1.1 1.3 1.5

2.21.6

0

3

6

9

2003 2004 2005 2006 1H 2007

(Tim

es)

EBIT/Gross interest expense Debt/EBITDA

39.3

31.933.7

43.641.7

29.430.4

25.224.228.2

0

10

20

30

40

50

2003 2004 2005 2006 1H 2007

(%)

Debt/equity Debt/capital

16Rating Review Presentation to Standard & Poor’s

Peer Comparison (FY2006)

Revenue

2,424.1

2,069.8

2,508.5

3,308.3

2,575.4

0

500

1,000

1,500

2,000

2,500

3,000

3,500

KOWEPO KOSEP KOMI PO KOSPO EWP

(KR

W b

illio

n)

EBIT Net Income

EBIT Margin ROE Leverage

226.4

148.2

201.6

283.0

94.7

0

50

100

150

200

250

300

KOWEPO KOSEP KOMI PO KOSPO EWP

(KR

W b

illio

n)

159.6

77.8

168.6

207.7

45.7

0

50

100

150

200

250

KOWEPO KOSEP KOMI PO KOSPO EWP

(KR

W b

illio

n)

9.3

7.2

8.08.6

3.7

0

2

4

6

8

10

KOWEPO KOSEP KOMIPO KOSPO EWP

(%)

7.1

3.9

7.1

9.0

1.8

0

2

4

6

8

10

KOWEPO KOSEP KOMIPO KOSPO EWP

(%)

43.6

79.1

30.1 31.9

57.5

30.4

44.2

23.1 24.2

36.5

0

20

40

60

80

100

KOWEPO KOSEP KOMIPO KOSPO EWP

(%)

Debt/Equity Debt/Capital

17Rating Review Presentation to Standard & Poor’s

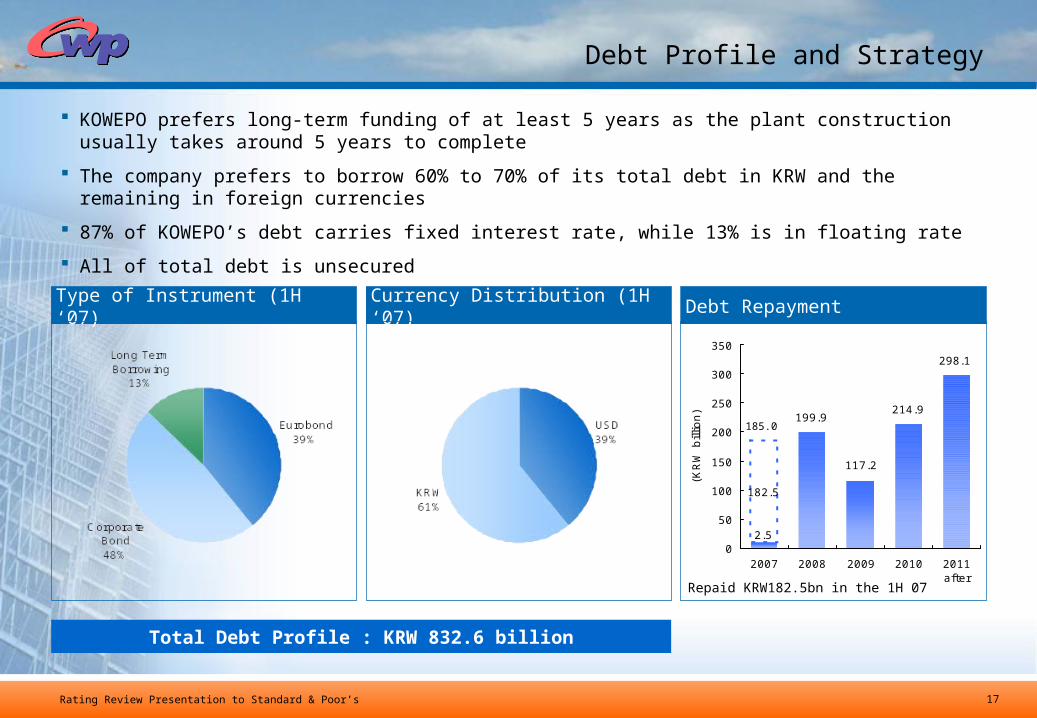

Debt Profile and Strategy

KOWEPO prefers long-term funding of at least 5 years as the plant construction usually takes around 5 years to complete

The company prefers to borrow 60% to 70% of its total debt in KRW and the remaining in foreign currencies

87% of KOWEPO’s debt carries fixed interest rate, while 13% is in floating rate

All of total debt is unsecured

Type of Instrument (1H ‘07) Currency Distribution (1H ‘07) Debt Repayment

199.9

117.2

214.9

298.1

2.5

182.5

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011after

(KR

W b

illio

n)

Total Debt Profile : KRW 832.6 billion

Repaid KRW182.5bn in the 1H 07

185.0

18Rating Review Presentation to Standard & Poor’s

Company OverviewCompany Overview

OperationsOperations

Financial ManagementFinancial Management

Concluding Remarks Concluding Remarks

Table of Contents

19Rating Review Presentation to Standard & Poor’s

Concluding Remarks

Improving economic fundamentals with structural improvements in South Korea and eased political tensions from North Korea

Healthy operating environment provided by favourable industry conditions

Continued supportive regulatory frame work and the expected well-paced, gradual approach in industry restructuring

Maintains one of the leading positions in terms of Management Appraisal of Gencos by KEPCO.

Strong financial performance and debt servicing ability supported by stable, recurring revenue and cash flow

Robust capital structure and strong financial flexibility to support the capex plan