kpmg forum. issue 4/2015€¦ · kpmg forum. a polish-english quarterly where experts . from kpmg...

TRANSCRIPT

nr 4 | 2015

ISSN 2299/6206

KPMG FORUMA Polish-English quarterly where experts

from KPMG in Poland share their professional expertise in audit, taxation,

as well as strategic, operational and legal advisory services.

kpmg.com/pl/KPMGForum

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Editorial office: KPMG Sp. z o.o. ul. Inflancka 4A 00-189 Warszawa tel. +48 22 528 11 00 fax +48 22 528 10 09

Editor in Chief: Magdalena MaruszczakSupervising editor: Monika Muracka Design studio: KPMG Sp. z o.o.

kpmg.pl

2 KPMG FORUM

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Experts contributing to the issue 4/2015 ................................................................................................................................ 5

The amended Accounting Act (further referred to as the ‘Act’) brings simplifications to small undertakings – Wiktoria Chowaniec ................................................................................................................................................................. 6

Investments, or enterprise development with grant funding support – Nina Perret ............................................................ 8

Calculation of the revenue allocation key by the taxpayers conducting business in the Special Economic Zones – Oskar Wala ...............................................................................................................................................................................12

Development strategies selected by listed companies in Poland vs. their share price returns – Tomasz Wiśniewski, Jacek Komór, Jakub Matusiak ................................................................................................................14

The traditional finance function seeks a transformation! – Violetta Małek ...........................................................................19

Electronic Proceedings by Writ of Payment (‘EPU’) – The Consequences of Taking a Shortcut – Tomasz Kamiński ......... 24

Major Amendments to the Copyright Law – Justyna Szymaszek ......................................................................................... 27

Precautionary Measures in Litigation Involving Corporate – Rafał Krzyżak ......................................................................... 30

Reports by KPMG .................................................................................................................................................................... 32

TABLE OF CONTENTS

3KPMG FORUM

4 KPMG FORUM

Warszawaul. Inflancka 4A00-189 WarszawaT: +48 22 528 11 00F: +48 22 528 10 09E: [email protected]

Krakówal. Armii Krajowej 1830-150 KrakówT: +48 12 424 94 00F: +48 12 424 94 01E: [email protected]

Poznańul. Roosevelta 1860-829 PoznańT: +48 61 845 46 00F: +48 61 845 46 01E: [email protected]

Wrocławul. Bema 250-265 WrocławT: +48 71 370 49 00F: +48 71 370 49 01E: [email protected]

Gdańskal. Zwycięstwa 13a 80-219 Gdańsk T: +48 58 772 95 00F: +48 58 772 95 01E: [email protected]

Katowiceul. Francuska 3440-028 KatowiceT: +48 32 778 88 00F: +48 32 778 88 10E: [email protected]

Łódźal. Piłsudskiego 2290-051 ŁódźT: +48 42 232 77 00F: +48 42 232 77 01E: [email protected]

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Printed on recycled material Cyclus Print

KPMG offices in Poland

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

5KPMG FORUM

Experts contributing to the issue 4/2015

Justyna Szymaszek

Rafał Krzyżak

Oskar Wala

Wiktoria Chowaniec

Nina Perret

Tomasz Kamiński

Jacek Komór

Violetta Małek

Jakub Matusiak

Tomasz Wiśniewski

kpmg.plkpmg.com/pl/KPMGForum

Znajdź nas:youtube.com/kpmgpoland

facebook.com/kpmgpolandtwitter.com/kpmgpoland

linkedin.com/company/kpmg_polandinstagram.com/kpmgpoland

pinterest.com/kpmgpolandkpmg.com/pl/app

itunes.com/apps/KPMGThoughtLeadershipitunes.com/apps/KPMGGlobalTax

itunes.com/apps/KPMGPolandCareer

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The amended Accounting Act (further referred to as the ‘Act’)

brings simplifications to small undertakings

The Accounting Act amendmentThe smaller enterprises will welcome with a sense of relief the amendments to the Act adopted by the Polish House of Representatives (Sejm) on 23 July 2015 for the purpose of reducing the administrative burden for small undertakings. The amendments constitute transposition into Polish law of certain requirements imposed by the European Union: the amendment the Act implements the provisions of the Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 (further referred to as the ‘Directive’) on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings.

The main beneficiaries of the amended provisions of the Act will be the entities which fulfil the criteria of a small undertaking. Pursuant to the new regulations, a small undertaking is defined as one which both in the financial year for which it has prepared financial statements and

Financial statements provide snapshots of an undertaking that enable assessment of its operational results, financial condition and the trends prevailing in its business. The obligatory preparation of financial statements at completion of every financial year is one of the milestones in the timetable of the corporate financial and accounting function. The entities subject to the Act prepare their annual financial accounts in accordance with specific uniform rules, which ensures comparability of data for a broad range of interested users. It should be stressed that the largely same rules have been incumbent equally

The amendment to the Act adopted by Sejm in July 2015 provides for specific reporting simplifications available

to small undertakings. Having obtained a decision of the approving authority for preparation of financial

statements with the use of specific simplifications, authorised entities will be able to take advantage

of the new simpler solutions. The changes implement solutions which adjust Polish regulations to the

requirements of European Union law.

Keep up to date at kpmg.com/pl/audyt

Follow changes in International Financial Reporting Standards (IFRS), Polish accounting rules, including the Accounting Act, and National Accounting Standards at kpmg.com/pl/BiuletynRachunkowosci.

on large non-public companies, with broad market outreach and a substantial number of diverse transactions, and on smaller business entities. However, many of the enterprises required to comply with the provisions of the Act are relatively small undertakings, with a homogeneous business profile, limited market impact, small number of users and small employment. These are often family-owned businesses, lacking any extensive reporting base, for which preparation of the expanded version of financial statements calls for a substantial investment of time.

6 KPMG FORUM Audit

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

in the preceding year reported data which do not exceed minimum two of the following values:

1. total assets on the balance sheet, at the end of a financial year, of not more than PLN 17 million;

2. net revenue from the sale of goods and products, in a financial year, of not more than PLN 34 million;

3. average annual employment not greater than 50 full-time job equivalents.

The definition of a small undertaking is primarily addressed to joint-stock companies, limited liability companies and limited joint stock partnerships. Other beneficiaries of those simplifications will include natural persons, civil law partnerships of natural persons, registered general partnerships of natural persons and partner companies required to comply with the Act. Worth underscoring is that the condition precedent here is the approving authority’s decision relating to preparation of financial statements incorporating the legally authorised simplifications.

Simplifications in the amended ActThe legislators primarily provided the possibility of preparing simplified balance sheets, income statements and supplementary information, with reduced scope of disclosures. In addition, small undertakings will be able to opt out of preparation of the statement of changes in equity and the statement of cash flows.

Whenever pursuant to the Act an entity was required to report on its operations, but satisfies the criteria of a small undertaking, the amended regulation allows for a solution in which such a report would not need

to be prepared. It should be borne in mind that information on purchase of own shares will still need to be disclosed in the supplementary information.

In turn, the relief for the undertakings which in the past year did not exceed two of the three indicators described as relating to small undertakings will include the possibilities (which do not arise from the Directive) of recognition lease agreements in accordance with the rules laid down in the tax law and of obtaining waiver to calculation of deferred income tax assets and allowances. Until now, those two simplifications were accessible only to entities whose financial statements were not subject to mandatory examination by the auditor. Additionally, the small undertakings will benefit from the possibility of seeking exemption from the provisions setting out the rules of recognition, valuation methods, scope of disclosure and the manner of presentation of financial instruments.

The amended regulation will be applicable for the first time in respect of the reporting periods commencing on 1 January 2016 or later. However, the legislators allowed for the possibility of early application

of the new solutions, this in respect of the financial years ended after the date of entry of the amended Act into force.

We need to also note that the definition of a small undertaking excludes public-interest entities and public finance sector entities. Hence, those entities, regardless of their revenues, will not be able to take advantage of the simplifications discussed here in preparation of their financial statements.

Practical information for the usersFinancial statements are prepared firstly for their users. In the case of smaller undertakings, the number of report recipients is often limited, which is why it seems reasonable that the relevant financial information be as simple as possible and easy to prepare. The changes which the amended Act introduces will be available to a larger number of entities, and are ultimately intended to contribute to reduction of the costs associated with accounting.

Wiktoria Chowaniec-Gojny

Chartered accountant, ACCA, Senior Manager of General Audit Department of KPMG in Poland

• auditing stand-alone and consolidated financial statements prepared in accordance with Polish and international accounting standards

• her experience includes audits of domestic and international enterprises, including Warsaw Stock Exchange listed companies, as well as provision of training in the methodology of audit and International Financial Reporting Standards

• her sector specific experience encompasses: petrochemicals, refining, steel and automotive industry

• with KPMG since 2003

7KPMG FORUMAudit

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Investments, or enterprise development with grant funding support

This September, the 2014-2020 Programming Period’s initial calls for proposals for co-financing company

investments are being accepted. There is new public co-financing available, among others, for acquisition

of fixed assets, lands and buildings. Enterprises will be able to take advantage of two new support mechanisms

available for enterprise expansion.

I. Support of investments in enterprise R&D infrastructureThe first support mechanism is available to enterprises under the sub-measure 2.1, 'Support of investments in corporate R&D infrastructure', of the Smart Growth Operational Programme, i.e. co-financing of investments in research and development centres (‘R&D’). Enterprises can file applications for this co-financing between 1 September do 31 October 2015.

Who can apply for the support?The competition is addressed to the SME sector and large enterprises. These can apply for support of projects involving new and further development of enterprise R&D infrastructure through investments in, among others, machinery, equipment and technologies, which enable activity in research and development, in other words, in new and further development of products or services.

What is the scale of the available co-financing?The minimum value of eligible project costs stands at PLN 2 million. The competition budget amounts to PLN 460 million, of which PLN 44,749,197.00 is earmarked for projects located in the Mazovia Province and PLN 415,250,803.00 for projects located in voivodeships other than the Mazovia Province.

The maximum co-financing rate for experimental development works stands at: 45% of eligible costs in the

Keep up to date at kpmg.com/pl/podatki Are you interested in Tax issues?Visit: kpmg.com/pl/globaltaxapp kpmg.com/pl/ppt kpmg.com/pl/taxalerts kpmg.com/pl/frontiersintax abcplatnika.pl taxownik.pl

8 KPMG FORUM Tax

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

case of micro- and small enterprises, 35% in the case of medium enterprises and 25% in the case of large enterprises.

The maximum support for infrastructure ranges between 10% and 70% of eligible project costs (depending on project location and enterprise size). The rate of the support will be consistent with the adopted map of regional aid (see Chart 1). The micro- and small enterprises are entitled to additional 20% increase while the medium enterprises to additional 10% increase in the co-financing.

What can be co-financed?Within the sub-measure 2.1 of the Smart Growth Operational Programme, the support is available for coverage of the following costs:

a) acquisition of developed and undeveloped real estate (including the right of perpetual usufruct);

b) leasing instalment payments for developed and undeveloped real estate incurred and made by the user until the project completion date, up to their initial value at the leasing agreement date, conditional on the leasing agreement covering a period of minimum 5 years following the anticipated project completion date, a in the case of micro-,

small and medium enterprises – a period of minimum 3 years;

c) acquisition or construction of fixed assets other than those specified under point a), including the cost of their installation and commissioning;

d) procurement of construction works and building materials;

e) procurement of intangible assets in the form of patents, licenses, know-how and other intellectual property rights;

f) instalment payments for the initial value of fixed assets other than those specified under point d) incurred and made by the user on account of a leasing agreement leading to the transfer of ownership of those fixed assets onto their user, excluding sale and lease-back transactions; and

g) procurement of technical knowledge as well as advisory and equivalent services used for project purposes;

h) as part of de minimis aid, applications can include the cost of procurement of materials and products used directly for project implementation.

II. Research to marketThe second mechanism making available co-financing for investments is provided under the sub-measure 3.2.1, Support for implementation of results of R&D works – 'Research to market'. Applications for co-financing are being accepted between 31 August and 28 October 2015.

Who can apply for o support?The competition is addressed to micro-, small and medium enterprises.

Source: Proprietary analysis by KPMG in Poland based on §§ 3 and 5 of the Council of Ministers Regulation of 30 June 2014 on the establishment of the map of

regional aid for the years 2014-2020 (Journal of Laws, item 878)

Chart 1:

Map of regional aid

Warsaw: until 31 December 2017: 15% from 1 January 2018: 10%

The support rate will be increased by 20 percentage points for the micro- andsmall enterprises and by 10 percentage points for the medium enterprises.

9KPMG FORUMTax

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

What types of projects will be co-financed?The co-financing available within the sub-measure 3.2.1 is designated for investment projects involving implementation of R&D work results and aimed at market launch of new or significantly improved products or services.

The co-financing is available for:

• experimental development works;

• advisory services required for implementation of R&D work results;

• capital expenditures directly related to commercialisation of R&D results.

Development of design documentation is also deemed a project component.

What is the amount of the available co-financing?The competition budget for the year 2015 amounts to PLN 500 million. The minimum value of eligible project costs stands at PLN 10 million. The maximum project co-financing amount is PLN 20 million, and includes funding for:

a) development works, with:

• PLN 1 million as the maximum value of eligible costs; and

• PLN 450,000 as the maximum co-financing; and

b) the advisory component, with:

• PLN 1 million as the maximum value of eligible costs; and,

• PLN 500,000 as the maximum co-financing.

The maximum rate of regional investment aid will be consistent with the map of regional aid adopted for the years 2014-2020 (see Chart 1).

The maximum support rate for development works stands at:

• 35% of eligible costs for medium enterprises; and

• 45% of eligible costs for micro-enterprises and small enterprises.

The maximum co-financing for the advisory component stands at 50% of eligible project costs.

What can be co-financed?Within the research component, the eligible costs are those of experimental development works, which include, e.g.:

a) staff costs: researchers, technicians and other support staff, to the extent they are used in a given research project;

b) costs of the research conducted on a contract basis;

c) operating costs, including costs of materials, supplies and similar products.

Within the advisory component, the eligible costs are those of advisory services required in implementation of R&D works, as provided by external consultants.

Within the investment component, the eligible project costs include, among others:

10 KPMG FORUM Tax

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

a) acquisition of the right of perpetual usufruct to land and of ownership rights to real estate, excluding residential housing units;

b) procurement or construction of fixed assets other than those specified under point a);

c) procurement of construction works and building materials;

d) procurement of intangible assets in the form of patents, licenses, know-how and other intellectual property rights; and

e) repayment of principal instalments of developed and undeveloped real estate.

Nina Perret

Tax Expert in the Grants and Incentives Team of the Tax Advisory Department, KPMG in Poland

• specialising in grants and incentives advisory

• holder of a PhD degree in Economics, the Warsaw School of Economics

• a former member of the Board (Research Council) and the Secretary General of the Association of Polish Economists (in the years 2012-2014)

• her experience in working with the EU Structural Funds spans over more than seven years and has included, among others: the Ministry of Economy’s Expert for the Innovative Economy Operational Programme since 2011; membership of the Project Evaluation Committee operating within the framework of the Innovative Economy Operational Programme at the Polish Agency for Enterprise Development and the Ministry of Economy; and participation in the development of the Smart Growth Operational Programme 2014-2020 and the Eastern Poland Operational Programme 2014-2020

• her state aid practice experience includes, among others: acquisition of grants from the EU Structural Funds, domestic funds and other sources which support research and development and capital investment projects; reconciliation of grant application projects; preparation of state aid related research and opinions; provision of grants and incentives advisory

• conducted numerous company addressed conferences, training courses and seminars within her area of expertise

• her sector specific experience encompasses: ICT technologies, pharmaceuticals, biotechnology and chemicals

• with KPMG in Poland since March 2015

SummaryBoth the mechanisms offering investment project co-financing discussed in this article provide development support for R&D activity in the corporate sector. It should be borne in mind that R&D is also understood as product or service development or enhancement in an enterprise. Given this, the type of investment an enterprise requires and the public funds to be utilised for the purpose are worth considering carefully.

11KPMG FORUMTax

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Calculation of the revenue allocation key by the

taxpayers conducting business in the Special

Economic ZonesIn accordance to the Act on Corporate Income Tax, income from business

activity conducted in a Special Economic Zone (‘SEZ’) on the basis of a permit to operate in an SEZ is exempted from corporate income

tax. Calculation of SEZ generated income calls for recognition of SEZ generated revenue together with the tax deductible costs.

After adjustment of the SEZ generated revenue for the related tax deductible costs we obtain SEZ generated income,

which benefits from income tax exemption.

It is often the case that taxpayers conducting business activity in Special Economic Zones (‘SEZs’) also operate non-SEZ business activities, which do not benefit from income tax exemption and are subject to taxation under general rules. Under such circumstances, the taxpayer needs to separate revenue and tax deductible costs arising from SEZ related business activity, which generates income exempted from corporate income tax, from the income being subject to tax. Applied to specific revenue and

costs this classification exercise may involve uncertainties, nonetheless it should be as simple as recognition of each specific revenue and cost item as falling into either one or the other category.

The situation complicates, however, in the case of tax deductible costs, a category of a general nature termed the common costs. In addition to costs which can be assigned to specific revenue, the business activity of SEZ entities also includes common costs, such as

12 KPMG FORUM Tax

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

general and administrative expenses, which cannot be unequivocally assigned only to SEZ on non-SEZ business activity. Pursuant to the Act on Corporate Income Tax, such costs should be assigned in part to SEZ incurred costs and in part to non-SEZ costs. Calculation of the ratio of that assignment, referred to as the revenue allocation key, is required for the purpose. For instance, if the non-SEZ revenue represents 30% while the SEZ generated revenue constitutes 70% of the taxpayer’s total revenue, then 30% of the common costs should be allocated to the non-SEZ tax deductible costs while 70% to the SEZ incurred costs respectively.

Calculation of the revenue allocation key in the case of a company merger In practice, there may be doubts about the way in which to calculate the revenue allocation key in the event a taxpayer conducting business operations in an SEZ merges with a non-SEZ company in the course of a fiscal year. An opinion on the matter was presented by the District Administrative Court in Gliwice in its ruling of 15 July 2015 (ref. no. I SA/Gl 82/15).

The ruling was passed in response to one taxpayer’s request for individual interpretation. An SEZ company (the acquiring one) was required to settle for purposes of its annual tax return the taxable revenue and costs of a non-SEZ company (the acquired one) generated and incurred prior to the merger date, thus treating them as own revenue/costs relating to their non-SEZ business activity. As a result, the merger had a direct impact on the tax base subject to CIT posted by the SEZ company.

The possible revenue allocation key calculation methods in the case of a company mergerThe doubts the SEZ company voiced related to the question whether revenue of the acquired company generated prior to the merger should figure in the revenue allocation key calculation. The tax authorities concluded that it should not. In the tax authorities’ opinion, that revenue could be in no way associated with the common costs incurred by the SEZ company.

The District Administrative Court (‘DAC’) in Gliwice disagreed with that position of the tax authorities. The DAC stated that for purposes of calculation of the revenue allocation key the SEZ company should also account for the value of the acquired company’s revenue generated before the merger date. Hence, this revenue amount impacted the tax settlement amount due from the SEZ company in respect of the year in which the merger took place. In other words, there was no basis for the claim that this revenue should not affect the

value of the revenue allocation key for that specific year.

The position taken by the DAC benefits the SEZ company, because inclusion of this additional non-SEZ revenue amount in the revenue allocation key calculation changes the ratio applied in settlement of the common costs, with the effect that a larger part of the common costs can be allocated to the non-SEZ activity, and the tax deductible costs associated with the non-SEZ activity increases. As a result, the tax base subject to CIT will be reduced.

In conclusion, we can state that, as a rule, the Gliwice DAC presented an interpretation of the corporate income tax provisions favourable to the taxpayers, nonetheless the disputes between taxpayers and tax authorities indicate that the regulation of the matter is not sufficiently clear. In effect, related problems may continue to arise.

Oskar Wala

Tax Expert in the Tax and Court Proceedings Team of the Tax Advisory Department, KPMG in Poland

• specialising in tax and in court and administrative proceedings

• his responsibilities cover process strategy advisory and general tax advisory

• he participates in business restructuring projects and tax reviews

• his experience includes, inter alia, business restructuring advisory

• his sector specific experience encompasses power industry and real estate

• with KPMG in Poland since 2007

13KPMG FORUMTax

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Development strategies selected by listed companies in Poland

vs. their share price returns Every company usually has at its disposal a number of different pathways to achieve

its business objectives. The three primary development strategies include organic growth, growth through mergers and acquisitions and growth through alliances. Selection of the appropriate growth path is often a key dilemma for the corporate

management, since it ultimately impacts, among others, the risk, transparency, flexibility and speed of the investment project implementation. How do the individual

growth strategies differ? Which aspects should be taken into consideration when choosing between them? Which growth path is the most effective one?

Does it pay off to pursue more than one strategy at the same time?

KPMG in Poland has analysed the impact of the development strategies chosen by companies on changes in their market valuations as a measure of effectiveness of the respective strategies. For that purpose KPMG examined a total of 50 companies listed on the Warsaw Stock Exchange over the period between 1 January 2013 and 30 April 2015. The research demonstrated that though selection of the relevant development strategy always calls for consideration of the individual case, several interdependencies exist between the development paths chosen by the listed companies in Poland and the growth of their stock market value.

Three primary development strategiesAchievement of corporate business objectives normally involves gaining access to new resources and

Opening of a new location

Launch of a new product

Procurement of assets

Merger of ‘equals’

Acquisition of smaller companies

Gaining of new customers or markets

Expansion of production capacities

Strategic alliance

Contracts with external entities

Joint venture concerning assets (as a buyer or seller)

Development strategies

Organic growth

Growth through M&As

Growth through alliances

Source: Analysis conducted by KPMG in Poland

Chart 1:

Examples of the respective development strategies

Keep up to date at kpmg.com/pl/UslugiDoradcze Download KPMG publications about your industry from blibliotekakpmg.pl

14 KPMG FORUM Advisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

competences. At that stage, the company management essentially needs to decide on the manner in which they should be secured. The required assets can be either developed internally or obtained externally, through procurement or borrowing. As a result, we typically differentiate between three basic development strategies: organic growth, growth through acquisitions and growth through alliances.

As can be demonstrated through numerous examples observed on the Polish market, spectacular company’s growth can be achieved by adopting each of the three aforementioned paths of development. Yet, when considered at the individual level, the respective strategies may yield markedly different results, among others, due to many differences in their characteristics.

Factors Organic growth Alliances Mergers and acquisitions

Cost of implementation

• relatively high financial outlays

• expenses spread over time

• costs shared between the partners

• possibility to use resources on license fee or contract basis

• high financial outlays

• expenditures highly concentrated over a short period of time

Business development

speed

• frequent necessity to build 'from scratch'

• gradual, 'step by step' business development

• usually preceded by analysis and negotiations between the parties

• immediate access to the partner's resources

• multiple stage process preceding the transaction

• quantum-leap in business development after transaction closing

Risk

• large capital expenditures

• full responsibility for the uncertain future cash flows from development

• risk shared with the partner

• ability to terminate contract or licensing agreement

• very high up-front costs

• full responsibility for the uncertain future cash flows

• valuation and synergy assessment risks

Transparency• full access to investment

project data

• information asymmetry between the company and the resource borrower or partner

• complete information on the acquisition target not available

Flexibility• possibility to opt out of

a project after its launch

• relative easiness in both opting out of the alliance and returning to it

• lack of the possibility of opting out of an investment project once it is launched

Source: Analysis conducted by KPMG in Poland

Table 1:

Differences between the respective strategies of development

Profiles of the respective development strategiesInformed selection of the most appropriate development path would not be possible without a thorough analysis of the differences in the respective

15KPMG FORUMAdvisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

strategies’ characteristic features. The three aforementioned growth paths will typically have divergent impact on the cost and speed of investment project implementation as well as its relative risk, transparency and flexibility. Table 1 provides an illustrative listing of the essential differences between the respective strategies of development.

How to choose the appropriate strategy The selection of the most appropriate development strategy by a given company depends, among others, on the resources and competences it holds, the pace at which it plans to achieve its business objectives, its competitive environment, its size and its access to financing sources.

In the case of companies with a unique product as well as those focused on their core business, for which internal resources are extremely valuable, organic growth is typically the most popular form of development. This strategy is often also appropriate for highly reputable companies, in the case of which a potential merger or collaborative partnership could impact their image in a detrimental way. Moreover, organic growth may represent the only viable development option for companies which do not have adequate funds to pursue an acquisition or are too small to attract a strategic partner.

Development through alliances is, as a rule, the solution for companies using highly marketable resources, which can conceivably obtain significant savings due to licensing or contractual arrangement. In turn, finding a strategic partner could be the right choice for those in need of sector-specific know-how or desired resources of a potential ally.

On the other hand, merger or acquisition of another entity is a good solution when a company is looking for a rapid and marked increase in the scale of its

operations. The solution is particularly useful when a potential acquisition target or merger partner has a strong market position or a recognisable brand. This particular strategy is, however, advisable only if a relatively easy integration with the other company is possible. Otherwise, the merged entities may prove difficult to control.

In practice, every company should consider the matter of choosing its development strategy on an individual basis, which is why companies frequently pursue more than one strategy at the same time.

KPMG research methodologyKPMG in Poland has studied the impact of the development strategies chosen by selected companies on the changes in their market valuations, as reflective of the effectiveness of those respective strategies. For that purpose KPMG examined a total of 50 Warsaw Stock Exchange (‘WSE’) listed companies over the period from 1 January 2013 to 30 April 2015.

The development paths pursued by the companies in the period under examination were determined on the basis of current reports of the companies and other publically available information. Specifically, only substantial internal investment projects, such as opening of new outlets or new product launches, were deemed demonstrative of organic growth.

Effectiveness of the respective growth strategiesAnalysis of average share returns of selected Polish companies in the period under consideration yielded the following conclusions:

• share price of the companies that followed the organic growth strategy rose by an average of around 20%, i.e. by 18 percentage points more than the companies which did not conduct any substantial internal investment projects;

Development strategy

Sha

re p

rice

retu

rn

Organic growth

0%

5%

10%

15%

20%

25%

20.2%

1.9%

Mergers and acquisitions

0%

5%

10%

15%

20%

25%

12.1%

15.2%

Alliances

0%

5%

10%

15%

20%

25%22.0%

8.0%

Source: Analysis conducted by KPMG in Poland based on publically available information

Chart 2:

Selection of the respective growth strategies as compared to average share price growth in 50 selected WSE listed companies between 1 January 2013 and 30 April 2015

16 KPMG FORUM Advisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• market capitalisation of the companies engaging in alliances rose at a faster rate than market value of the entities which did not follow that strategy, i.e. by 22% and 8% respectively; and

• share price of the companies which did not acquire any entities grew by an average of 15%, i.e. by 3 percentage points more than the companies pursuing growth through mergers and acquisitions.

The results presented above can be justified by the fact that every effective merger and/or acquisition process carries with it many practical problems, such as difficulties with proper pricing analysis, assessment of synergies, errors in the due diligence process, differences in corporate cultures or errors in the integration process. Equally, a merger or an acquisition can be an attractive ‘shortcut’ as it can potentially speed up achievement of business objectives, which can then translate into their excessive usage.

According to the data published by DealWatch, only around 580 M&A deals had been finalised in Poland in the period under examination, hence the aforementioned results should be interpreted with caution. On the other hand, as established through KPMG’s international survey published in a report entitled 'A new dawn: good deals in challenging times', only one out of three M&A transactions delivers growth in a company’s value.

Number of implemented strategies and market returnsIt should be borne in mind that not every company pursues a single dominant development strategy. A significant number of companies, particularly among the larger WSE listed entities, follow a number of different growth paths at the same time.

KPMG in Poland has studied interdependencies between share price return rates and the number of development strategies implemented by the same companies. It turned out that the companies that followed three parallel growth paths in the period under examination achieved an average market capitalisation growth of circa 22% as compared to 3% achieved by those which did not pursue any strategy. Moreover, in general, the greater the number of pursued development strategies the higher the average share price return. Yet, it is also worth noting that only in the case of the companies which pursued all three strategies discussed here, the average market capitalisation growth exceeded the WIG index yield, in the period under review, a return investors would expect from the company managers.

The outcomes cited above can be explained, among others, by greater openness of some companies to the pursuit of various growth paths, and thus of not limiting themselves to continual employment of their one preferred development path. Companies should work out their own effective system for assessment of their strategy selection decision-making process and always consider the outcome of objective economic calculation before embarking on an investment project.

Research conclusions The three primary development paths available to every company include: organic growth, growth through mergers and acquisitions, and growth through alliances. Effectiveness of the respective growth paths can, however, differ vastly in specific cases, among others, due to differences in company characteristics, which ultimately impact investment project implementation cost, risk, transparency, flexibility and speed.

Sha

re p

rice

retu

rn

Number of strategies

0%

5%

10%

15%

20%

25% WIG (Warsaw Stock Exchange Index)

19.0%

22.2%

15.0%

11.5%

2.5%

3 2 1 0

Source: Analysis conducted by KPMG in Poland based on publically available information

Chart 3:

Number of implemented growth strategies compared to average share price growth rate in selected 50 companies listed on the WSE between 1 January 2013 and 30 April 2015

17KPMG FORUMAdvisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Jacek Komór

Executive in Valuation Team in Deal Advisory Group, KPMG in Poland

• specialises in business valuations for transaction, regulatory and financial reporting purposes

• he is responsible for carrying out business valuations, valuations of intangible assets, purchase price allocations as well as development and review of financial models for companies of various sectors

• his tasks include, among others: building financial models, valuation of companies with income, market and asset-based approach, review of impairment models, market research as well as preparation of lists of comparable transactions and comparable companies for valuation purposes

• with KPMG in Poland since 2013

Tomasz Wiśniewski

Partner, Head of Valuation Team in Deal Advisory Group, KPMG in Poland

• specialises in advisory services relating to business valuations prepared for transaction, financial reporting and regulatory purposes (including mergers, demergers and squeeze-outs)

• he conducts pricing analyses of trademarks for the purposes of licensing processes (including those conducted in conjunction with alliances)

• he has extensive experience in issuing opinions on the financial terms of transactions (Fairness Opinions)

• with his team, he performs analyses of project feasibility studies as well as develops and verifies financial models

• he heads the KPMG Valuation Services in the CEE region and participates in the work of the European Valuation Group and the Global Valuation Committee of KPMG

• with KPMG in Poland since 1994

Jakub Matusiak

Analyst in Valuation Team in Deal Advisory Group, KPMG in Poland

• takes part in projects involving business valuations, valuations of intangible assets, purchase price allocations, development and verification of financial models for companies of various sectors

• he also engages in reviews of impairment models, market research, calculation of discount rates and preparation of lists of comparable market transactions and listed companies for valuation purposes

• with KPMG in Poland since 2014

Analysis of the interdependencies between the development strategies chosen by the Warsaw Stock Exchange listed companies and their average share price returns in the period under consideration suggests that parallel implementation of diverse development strategies is normally conducive to company value growth.

Given the above, companies should be open to adopt various growth strategies rather than limiting themselves to continual employment of their one preferred development path. A decision to select specific strategy should result from an objective economic calculation. Specifically, companies should exercise great caution when considering implementation of an M&A strategy, as it potentially represents the most trouble prone form of corporate development, particularly when a company fails to plan it properly or to execute it in a professional manner. Frequently, M&A transactions are for them one-off investment opportunities, which on average deliver some company value growth in merely one out of three cases.

The experience of KPMG indicates that the common characteristics of all successful acquisitions include very good understanding of the acquired company’s value and a realistic assessment of the achievable synergies. That is why at selection of the pertinent development path and assessment of a potential acquisition target, a company is well advised to retain a professional firm that specialises in business valuations, which will apply best practices and can be relied on to provide independent and objective analysis. Such a course of action can increase the chances of selecting the correct growth path and achieving the expected shareholder earnings.

18 KPMG FORUM Advisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

In April 2015, KPMG in Poland conducted a survey among 120 CFOs. Its goal was to define the current trends in finance function performance. In the survey we asked respondents to assess the effectiveness of finance teams, indicate their strengths and weaknesses, identify critical skills in key financial processes, assess whether and how the role of the finance function in supporting business strategy evolves, and to identify the biggest challenges and ways to overcome possible

Global leaders, in an attempt to meet modern business expectations, are working hard to continuously strengthen the importance of finance function, improve overall performance and increase the role of finance in creating the company value. Their focus is shifting from the traditional finance function (internally focused services, finance function in silos, CFO as a scorekeeper, processes in specific business units, incompatible systems and data models, decentralized processing) towards building business partnership. This transformation requires a modern CFO to build an modern approach to managing a team of financial business partners. What kind of challenges is a modern CFO facing now and what is the recipe for success in such a fast-changing business world?

The traditional finance function seeks a transformation!

problems in redefining finance functions performance and assess whether changes in the perception of the finance role are visible. A report – Business partnership of the intelligent finance function – was prepared based on the survey responses and presents the main CFOs insights, their ambitions and the strengths of their finance teams. However, it also points out the areas for improvement, weaknesses and barriers the overcoming of which will lead to a path of transformation – a path of success.

Observations and ambitions of CFOs Continuously facing pressures both internal and external naturally influences positive changes in a finance team, and continuous improvements bring teams closer to global standards and best practices – from improvement of productivity and operational effectiveness to building business partnership and providing full support for the process of building a company’s value.

19KPMG FORUMAdvisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Table 1 shows the key and current trends in Poland concerning the finance function performance.

The talent management investments planned for the next few years are intended to support the transformation into intelligent finance function that supports business.Building an intelligent finance function, using its strengths and eliminating weaknesses, in an organisation of the future goes beyond the current traditional understanding of responsibilities such as financial reporting and control, rather it seeks to actively support the management of a business – reliably, quickly and completely describing in financial reports the real situation of a business, thus increasing the awareness of strategic decisions.

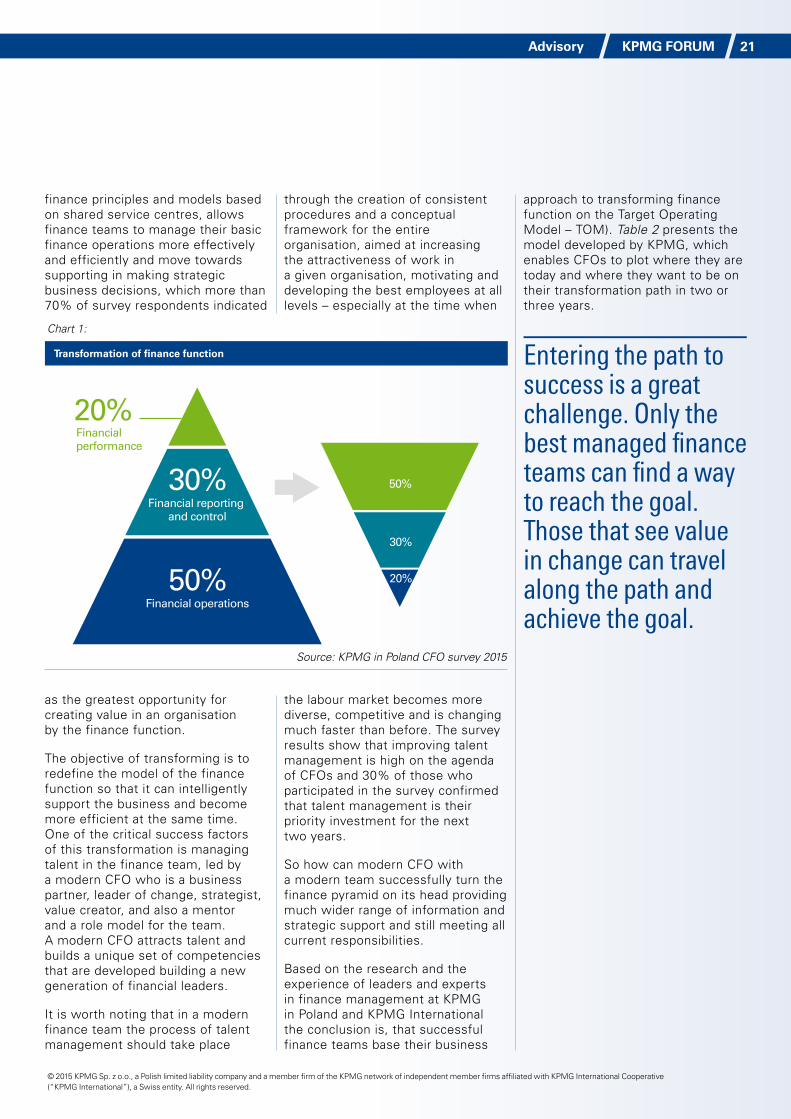

Intelligent transformation of the finance functionTraditional finance teams still spend most of their time and attention to ‘the basics' – transaction processing and accounting – and less time to the strategic, value-adding finance activities. The intelligent transformation of a finance function, including the deployment of lean

Source: KPMG in Poland CFO survey 2015

Table 1:

Current trends in Poland concerning the finance function

Top strengths Biggest weaknesses

About 60% of survey respondents are satisfied with finance function performance, and they highlighted accounting and statutory reporting as the strongest points, as well as

banking and treasury activities.

Talent management and the increasing technical knowledge of

staff were highlighted as the biggest weaknesses, and almost 30% of

respondents indicated this area also as the most difficult to improve.

The lean finance principles

45% respondents appreciate the importance of implementing lean finance in their organisation, and a similar proportion believe that their organisation is

implementing it effectively.

Managing talent

Although difficult to master, talent management is rated as the most important factor for creating value and the sustainable competitiveness of finance teams – almost 70% of respondents think that it is also an important factor for ensuring

effective support for business decisions in an organisation.

Planning, budgeting and forecasting

The biggest challenge in today's business environment is to anticipate the future and how to reflect it most reliably in financial forecast – almost 30% of CFOs

claimed that these processes require improvement in their organisation.

From decentralized to centralized

Most finance function in mature economies are moving towards a centralised operating model, for example shared service centres and outsourcing; however,

only 22% of surveyed CFOs believe their use is important.

Finance and risk alignment

70% of CFOs indicate that building awareness about finance and risk is important for improving the alignment of finance and risk activities, which is

reflected in the fact that companies that apply weight to the integration of these two activities achieve greater effectiveness in making faster and more balanced

in terms of risk business decisions.

Upcoming changes and investments

Almost 50% of CFOs plan to increase investment in the development of systems and tools for finance and accounting, while a similar proportion plan such investments in talent management. The aim is to support the transformation into intelligent finance function that supports business

20 KPMG FORUM Advisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

finance principles and models based on shared service centres, allows finance teams to manage their basic finance operations more effectively and efficiently and move towards supporting in making strategic business decisions, which more than 70% of survey respondents indicated

as the greatest opportunity for creating value in an organisation by the finance function.

The objective of transforming is to redefine the model of the finance function so that it can intelligently support the business and become more efficient at the same time. One of the critical success factors of this transformation is managing talent in the finance team, led by a modern CFO who is a business partner, leader of change, strategist, value creator, and also a mentor and a role model for the team. A modern CFO attracts talent and builds a unique set of competencies that are developed building a new generation of financial leaders.

It is worth noting that in a modern finance team the process of talent management should take place

through the creation of consistent procedures and a conceptual framework for the entire organisation, aimed at increasing the attractiveness of work in a given organisation, motivating and developing the best employees at all levels – especially at the time when

the labour market becomes more diverse, competitive and is changing much faster than before. The survey results show that improving talent management is high on the agenda of CFOs and 30% of those who participated in the survey confirmed that talent management is their priority investment for the next two years.

So how can modern CFO with a modern team successfully turn the finance pyramid on its head providing much wider range of information and strategic support and still meeting all current responsibilities.

Based on the research and the experience of leaders and experts in finance management at KPMG in Poland and KPMG International the conclusion is, that successful finance teams base their business

approach to transforming finance function on the Target Operating Model – TOM). Table 2 presents the model developed by KPMG, which enables CFOs to plot where they are today and where they want to be on their transformation path in two or three years.

Entering the path to success is a great challenge. Only the best managed finance teams can find a way to reach the goal. Those that see value in change can travel along the path and achieve the goal.

Financial operations

Financial reporting and control

Financial performance

50%

30%

20%

50%

30%

20%

Source: KPMG in Poland CFO survey 2015

Chart 1:

Transformation of finance function

21KPMG FORUMAdvisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Entirely internally focused

Finance function in silos

Scorekeeper

Business unit (BU) specific

Incompatible systems and data models

Value driver

Integrated finance function

Business partner

Standarized and optimized

Central data model / systems

Strategic sourcing / SSCs

optimized

Multiple agendas, cost centre mentality

Autonomous finance functions, e.g. objective setting at BU level

Diligent caretaking

Disaggregated processes and responsibilities, multiple G/Ls

Multiple data models, tools / applications and G/Ls

All processes are internal and decentralized

Finance vision agreed and aligned with the business

BU finance reporting directly into local mgmt / dotted line to center

Reactive ad hoc analysis

Low degree of standardization and automation (divisions / geographies)

Standard consolidation layer

Some centralization for low value, high volume transactions

Focus on value managment

Business acumen and financial knowledge

Strong alignment with central finance (hard dotted line)

Recommendation for common methods, processes and reference data

Standard systems, interface layer and recommended data models

Sourcing (central or external) of finance support tasks (i.e. finance systems)

Finance is a business partner of management and the board

Central guidance for BU implementation

Insightful analysis and comment

Standardized processes for low value, high volume transactions

Standard data models, tools / applications, on multiple ocurrences

Majority of finance processing are sourced (central or external)

Key influencer of stakeholders

Integrated finance community

Constructive challenge

Standardized processes for financial management

Standard tools and applications, on single ocurrence

All financial processes in optimum locations

Decentralized processing

Traditional finance function Modern finance function

Processes

Services

Technology

People

Location

Organization

Table 2:

Target Operating Model developed by KPMG

Source: KPMG in Poland CFO survey 2015

Defining a clear finance vision and strategy and designing the fit-for-purpose structure of the Target Operating Model (hereinafter: ‘TOM’) that will deliver the vision should be the first step in a finance function’s transformation program. A fully-fledged program that addresses all aspects of TOM is not always needed. CFOs can choose how far and fast they want to move the finance function, based on an assessment of prioritized requirements and their expected benefits.

In this way, a TOM shows up what competencies are missing in a finance function to be identified,

and which ones should be developed and improved, and to what extent, in order to enter the path of success and become a leader in the modern financial team management, which will be a team of partners intelligently supporting the business.

In the report by KPMG in Poland – Business partnership of the intelligent finance function – key solutions and tools are presented that when implemented will contribute to the success of intelligent finance function and their organisations.

22 KPMG FORUM Advisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Violetta Małek

Director of the Advisory Services Department at KPMG in Poland

• specialising in the optimisation of processes, transformation of financial departments and the creation, implementation and management of shared services centres

• experienced in projects to optimise business (implementing the value management philosophy), financial (lean finance), manufacturing (lean manufacturing), sales and operational processes

• Violetta participates in the creation, implementation and management of shared services centres

• she has over 20 years of experience in managing the finances and the performance of companies, advising on creating and implementing cost optimisation programmes and value creation programmes, carrying out restructuring and transformation processes, including complex implementations of IT solutions, as well as the implementation of such as competence centres (including EMEA SSC, CEE) and payroll services and change management

• prior to joining KPMG she worked in management positions (finance director, CEO, board member)

• her sector experience includes: manufacturing, cosmetics, logistics, transport, business services, technology and telecommunications

• Violetta is a graduate of: WUT Business School (a program shared with the London Business School, HEC in Paris and the Norwegian School of Economics in Bergen, EMBA), College of Management and Marketing in Warsaw (Financial Management, MA), University of Lodz, Faculty of Economics (Organisation and Management, Bachelor) and Warwick Business School (Business Administration Program)

• with KPMG in Poland since 2015

The priorities of a modern CFO building a team of business partnersThe awareness of and interest in the implementation of the concept of intelligent financial solutions is constantly growing. Among the many important issues contained in the TOM model, five key aspects can be highlighted for the increasingly important role of finance function and their ability to generate even more value for a business.

The building of modern organisational models using the lean finance

principles, shared service centres and outsourcing, implementing innovative techniques and analytical tools to carry out reliable forecasts, a strategic approach to talent management in an organisation and an alignment of financial and risk activities are the priorities of modern CFOs building teams of business partners.

23KPMG FORUMAdvisory

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Electronic Proceedings by Writ of Payment (‘EPU’)

– The Consequences of Taking a Shortcut

Simplified civil procedures give creditors a relatively easy means of enforcing their

claims. However, the simplified procedures may at times prove fatal to the debtor,

especially where the creditor exercises it rights in bad faith.

by means of entering it into an ICT system. Pursuant to Article 50532 §1 of the Code of Civil Procedure1, a suit lodged by the plaintiff is not accompanied by evidence. What makes these proceedings so popular is the simplicity and speed of action taken by the plaintiff in litigation.

Fictitious Delivery and Its ResultsThe aspiration to accelerate and simplify proceedings under the EPU implies that the plaintiff is not required to submit evidence together with the lodged suit. In issuing an order for payment, which includes the amount of the claims, the reasons of substance as well as the place of residence or seat of the defendant, the court does not rely on evidence but only on statements of the plaintiff2. Consequently, if there are formal grounds to issue an order for payment (the court only considers whether this is the appropriate procedure for the issuance of an order for payment and does not examine the merits of the claim), the order asserting the plaintiff’s claims is issued and sent to the address

What Is the EPU?In the current legal system, creditors may (and sometimes must) enforce their claims in civil proceedings under special procedures such as simplified, payment order, or writ of payment proceedings. These include simplified and accelerated fact-finding proceedings. However, such advantages are occasionally achieved at the expense of weakening the position of the defendant in the proceedings. Particularly important are electronic proceedings by writ of payment (‘EPU’) introduced in amending legislation of 2009. These proceedings are unique among others in the way that documents are lodged and served. A suit is brought

1 Code of Civil Procedure – Act of 17 November 1964 (Journal of Laws No. 43, item 296).2 Cf. decision of the Appeal Court of Lublin of 9 April 2014, case no. SA I ACa 844/13.

24 KPMG FORUM Legal

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

provided by the plaintiff. The order becomes legally valid unless the defendant raises an objection with the court. Therefore, the key issue is the proper delivery of the order for payment to the defendant to ensure that the defendant can effectively defend its rights.

Article 139 of the Code of Civil Procedure is crucial. It provides that a letter sent to the address of the defendant specified in the suit is deemed to be served even if the addressee fails to collect it after being notified twice.

However, these provisions also apply to the EPU, even though in the absence of evidence the court does not know how the plaintiff has determined the actual place of residence of the defendant. Furthermore, the same applies to the first delivery of documents in the case3. The address provided by the plaintiff may be incorrect and, in the extreme case, an order for payment may be issued without the defendant being aware of the proceedings. In that case, the defendant will only learn about the claims having been asserted when the bailiff collects the debt. So much trust put in the statements of the plaintiff is supposed to be counterbalanced by procedural instruments designed to improve the position of the defendant in the proceedings.

General Instruments Improving the Position of the DebtorOne such instrument is the objection: if correctly raised by the defendant, it

nullifies the order in its entirety. The defendant need not provide reasons for the objection: by simply expressing the intention to have the order nullified, the court is obliged to refer the case to be examined under the general jurisdiction (i.e. not under the electronic procedure). This instrument is available to the defendant, provided of course that the notice of suit is served.

Another instrument which protects the interests of the defendant under the EPU is the sanction. According to Article 50532 § 3 of the Code of Civil Procedure, the court may fine the plaintiff, its representative or proxy if the provided address of the defendant is incorrect due to wilful action or negligence. The regulations do not specify the amount of the fine; consequently, pursuant to Article 163 of the Code of Civil Procedure, the fine may be up to PLN 5 thousand. However, this is a follow-up measure which offers no protection of the defendant against unfair process on part of the plaintiff.

It would seem that the current legal system does not offer sufficient protection against actions of a creditor acting in bad faith who provides the incorrect address of the defendant to obtain a legally valid order for payment under the EPU. The bailiff will collect the asserted claims at the request of the creditor after a declaration of enforceability is issued (it is issued automatically under the EPU pursuant to Article 782 § 2 of the Code of Civil Procedure).

Suspension and Discontinuation of EnforcementThe question is: what is the position of the debtor when the actions of

the creditor eventually come to its attention? Pursuant to Article 805 § 1 of the Code of Civil Procedure, the debtor should be served a notice of enforcement when enforcement is first undertaken. In practice, this could be when the debtor first learns about the proceedings pending against it. The notice should quote the content of the enforcement writ, or a transcript of the writ should be attached to the notice.

An order for payment is declared enforceable by raising a relevant flag in the ICT system. Consequently, the request for enforcement should be accompanied by a document from the ICT system which allows the enforcement authority to verify the writ (in fact, it is a print-out of the enforcement writ: the order for payment and the declaration of its enforceability). Article 8203 § 1 of the Code of Civil Procedure is of key importance to the debtor as it provides that the bailiff must suspend enforcement if the document shows a different address of the debtor that the address determined during the enforcement. However, this depends on the debtor, who must file a request for suspension.

The fact that an order has been issued in proceedings where the plaintiff provided the incorrect address of the defendant will always be clear from the print-out from the ICT system. This follows from the Regulation which specifies the contents of the document. According to Article 2 of the Regulation4, if an enforcement writ is served to the defendant pursuant to Article 139 § 1 of the Code of Civil Procedure (where the defendant is notified twice), the original delivery address becomes clear whenever the enforcement writ is available. If the bailiff is obliged to attach the writ to the enforcement notice, the debtor at each time has the remedy necessary to suspend the enforcement and to have the order

3 Cf. decision of the Appeal Court of Rzeszów of 6 December 2012, case no. I ACa 379/12.4 Regulation of the Minister of Justice of 28 December concerning court actions relating to the issuance of declarations of enforceability of court decisions

issued under electronic proceedings for writ of payment.

25KPMG FORUMLegal

Keep up to date at kpmglegal.pl

Follow changes in Polish and European legislation, as well as the most significant judicial decisions of domestic and European institutions at kpmglegal.pl/legal-newsletter

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

nullified. If the bailiff is unwilling to suspend the enforcement, the debtor should lodge a complaint against the bailiff with the court responsible for the bailiff.

Enforcement begins when the debtor is served a request for enforcement or a print-out from the ICT system. Thus, the debtor first learns about the declaration of enforceability of the order issued in its case. This means that the declaration of enforceability may be appealed against, which could lead to discontinuation of the suspended enforcement.

It is of utmost importance that in addition to filing a request for the suspension of enforcement the debtor also approaches the court which has processed its case under the electronic procedure. Since the order for payment has never been properly served to the debtor, it is possible to have the time limit for raising an objection against the order reinstated. The case reference number is available in the document accompanying the enforcement notice; in the absence of any requirement to provide substantive grounds for an objection against an order for payment, the case number

is the only piece of information that the debtor needs in order to raise an objection. According to Article 169 of the Code of Civil Procedure, a request for reinstating the time limit should be substantiated (by means of providing the actual address) and the action whose time limit is to be reinstated should be undertaken (an objection against the order should be raised).

SummaryThe introduction of the EPU is part of the development of increasingly accelerated means of enforcing financial claims. Considering the average duration of court proceedings, this seems to be the right choice. However, one should consider the risks related to the acceleration and simplification of proceedings. The risks inherent in the EPU procedure can be mitigated, provided that the debtor takes immediate action and resorts to professional legal counsel due to the complexity of the legal system.

Tomasz Kamiński

Legal Counsel with the law firm D.Dobkowski sp.k. affiliated with KPMG in Poland

• graduate of the Department of Law and Administration, University of Warsaw; the School of European and English Law (University of Cambridge/University of Warsaw); the Postgraduate Course in Taxation and Tax Law (University of Warsaw)

• Legal Counsel since 2010 (Regional Chamber of Legal Counsels, Warsaw)

• he specialises in corporate M&As and restructuring, and in energy law including renewable energy sources

• he has extensive experience in designing optimised investment methods and in the implementation of complex restructuring transactions

• he works with the law firm D.Dobkowski sp.k. affiliated with KPMG in Poland since 2004

26 KPMG FORUM Legal

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Major Amendments to the Copyright Law

The Constitutional Tribunal Reduces Damages for Copyright InfringementThe Constitutional Tribunal in case no. SK 32/14 reviewed a constitutional complaint concerning provisions of the Copyright Law governing claims for damages available in the event of culpable copyright infringement. Article 79.1.3(b) of the Copyright Law stipulated that the rightsholder whose rights had been infringed (culpably) may request the person who had infringed such rights to repair the damage by payment of triple the

amount of respective remuneration that would have been due as of the time of claiming it in exchange for the rightsholder’s consent for the use of the work.

In its judgment of 23 June 2015, the Constitutional Tribunal declared that this provision of the Act was unconstitutional to the extent of damages for culpable copyright infringement. The Constitutional Tribunal decided among others that this was in breach of Article 64.1-2 of the Constitution (protection of property). The relevant provision of the Copyright Law became null and void on 1 July 2015 (date of publication in the Journal of Laws).

The decision of the Constitutional Tribunal may pave the way for

The Copyright and Neighbouring Rights Act has been significantly amended in the last few months (Act of 4 February 1994 – Copyright and Neighbouring Rights Law, consolidated text Journal of Laws of 2006, No. 90, item 631, as amended, hereinafter the ‘Copyright Law’). The amendments include mainly the amount of damages for infringement of copyright, the extension of certain terms of protection, and the fair use. The latter amendment is particularly relevant to media monitoring providers who will now be unable to use press clippings without the consent of the authors. The amendment of the amount of claims for damages is relevant to companies whose intellectual property is at the risk of illegal use.

reopening litigation closed with legally valid judgments granting damages equal to three times the amount of remuneration due for the use of the work under the aforementioned provision. Pursuant to Article 407 § 2 of the Code of Civil Procedure, a request to reopen proceedings should be lodged within 3 months of the effective date of the decision of the Constitutional Tribunal. However, a case cannot be reopened more than five years after the court decision became legally valid (Article 408 of the Code of Civil Procedure).

In the case in question, the Constitutional Tribunal did not examine the constitutionality of claims for damages also available under Article 79.1.3(b) of the Copyright Law in the event

27KPMG FORUMLegal

© 2015 KPMG Sp. z o.o., a Polish limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

of non-culpable copyright infringement (damages equal to double the amount of the remuneration that would have been due in exchange for the rightsholder’s consent for the use of the work); hence, the provision is still in force.

Small Amendment of the Copyright LawThe amendment of the Copyright Law known as a 'small amendment' took effect on 1 August 2015 (Act of 15 May 2015 amending the Copyright and Neighbouring Rights Act, Journal of Laws of 2015, item. 994). The amendment implements EU legislation into Polish law (Directive on the term of protection of copyright and certain related rights).