kt proprietaryidate conference 20021 elements contributing to korea’s leadership in broadband...

TRANSCRIPT

KT Proprietary IDATE Conference 2002 1

Elements Contributing to Elements Contributing to

Korea’s Leadership in Korea’s Leadership in BroadbandBroadband

November 21, 2002November 21, 2002

Hansuk KimHansuk KimVP/Head, Management Research Lab, KTVP/Head, Management Research Lab, KT

President, Pacific Telecommunications CouncilPresident, Pacific Telecommunications Council

The Value Networking Company

KT Proprietary IDATE Conference 2002 2

AgendaAgenda

Korean Broadband OverviewKorean Broadband Overview

Lessons LearnedLessons Learned

Future ChallengesFuture Challenges

KT Proprietary IDATE Conference 2002 3

AgendaAgenda

Korean Broadband Korean Broadband OverviewOverview

Lessons LearnedLessons Learned

Future ChallengesFuture Challenges

KT Proprietary IDATE Conference 2002 4

Korean Broadband SubscribersKorean Broadband Subscribers

MillioMillionn

1010

88

66

44

Dec. Dec. ‘98‘98

KTKT

HanaroHanaro

ThrunetThrunetOtherOther

ss

Dec. Dec. ‘99‘99

Dec. Dec. ‘00‘00

Dec. Dec. ‘01‘01

Sep. Sep. ‘02‘02

22

Market shareMarket share(Sept. (Sept. 20022002))

KT: 45.3%

Hanaro: 28.7%

Thrunet: 13.0%

Others: 13.0%

KT Proprietary IDATE Conference 2002 5

Driving KT’s Revenue GrowthDriving KT’s Revenue Growth

Subscriber & EBITDA MarginSubscriber & EBITDA Margin

-13%

1.7M

5M

52%

3.8M

39%

2000 2001 2002 E

Number of Subscribers

Broadband Revenue Growth Broadband Revenue Growth

( Non-consolidated, KRW trillion )( Non-consolidated, KRW trillion )

0.250.5

1.6

2002E 2000 1H 2001 2001

1.1

CAGR 111%

CAGR 111%

KT Proprietary IDATE Conference 2002 6

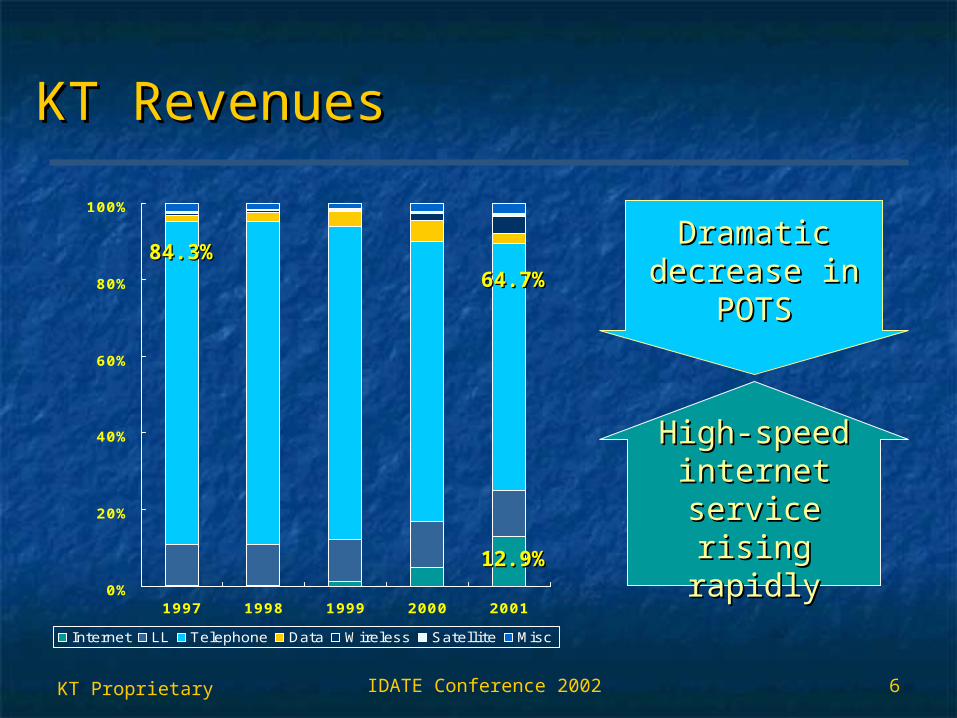

KT RevenuesKT Revenues

0%

20%

40%

60%

80%

100%

1997 1998 1999 2000 2001

Internet LL Telephone Data Wireless Satellite Misc

12.912.9%%

64.764.7%%

84.384.3%%

High-speed High-speed internet internet

service rising service rising rapidlyrapidly

Dramatic Dramatic decrease in decrease in

POTSPOTS

KT Proprietary IDATE Conference 2002 7

Technology EmployedTechnology Employed

June 2001June 2001

September September 20022002

DSLDSLCableCable

LANLANBWLL/BWLL/

SatelliteSatellite

53.853.8%%

34.534.5%%

11.611.6%%

0.1%0.1%

First service by cable First service by cable modemmodem

DSL dominant now DSL dominant now June 2000June 2000

60.260.2%%

39.339.3%%

DSLDSLCableCable

KT Proprietary IDATE Conference 2002 8

DSL Network Coverage (KT)DSL Network Coverage (KT)

• Direct installation Direct installation without qualitywithout quality

degradation degradation

• Direct installation Direct installation with some qualitywith some quality

degradation degradation

78%

Quality guarantee through optical fiber

3Km

4Km

2Km Network CoverageNetwork Coverage

2Mbps2Mbpsguaranteeguarantee

93% 86% 78% 39%

5%(100%) 17%(95%) 36%(78%)42%

KT Proprietary IDATE Conference 2002 9

Home Internet AccessHome Internet Access

Dramatic Dramatic increase in increase in the Internet the Internet connectivity connectivity and usageand usage

PC OwnershipPC Ownership

46.0%46.0%

15.2%15.2%

0.0%0.0%

48.9%48.9%

0%0%

25%25%

50%50%

75%75%

100%100%

’’99.699.6 ’’99.1299.12 ’’00.600.6 ’’00.1200.12 ’’01.601.6 ’’01.1201.12

Internet UsageInternet Usage

High-speed High-speed InternetInternet

Source: KT Panel Survey, Management Research Lab, 2002

65.9%65.9%

53.1%53.1%

KT Proprietary IDATE Conference 2002 10

Internet UsageInternet Usage

On-line stock tradingOn-line stock trading 54% KSE 79% KOSDAQ

On-line stock tradingOn-line stock trading 54% KSE 79% KOSDAQ

Internet broadcastingInternet broadcasting 74% of Korean Internet population

access audio/video content

Internet broadcastingInternet broadcasting 74% of Korean Internet population

access audio/video content

On-line gamesOn-line games 54% penetration of Korean

Internet users

On-line gamesOn-line games 54% penetration of Korean

Internet users

Source: Nielsen NetRatings, as of 2002

16.316.3

10.8

10.0

9.8

8.3

7.9

0 5 10 15 20

KoreaKorea

Canada

US

Hong Kong

Germany

Japan

Hours per Hours per weekweek

KT Proprietary IDATE Conference 2002 11

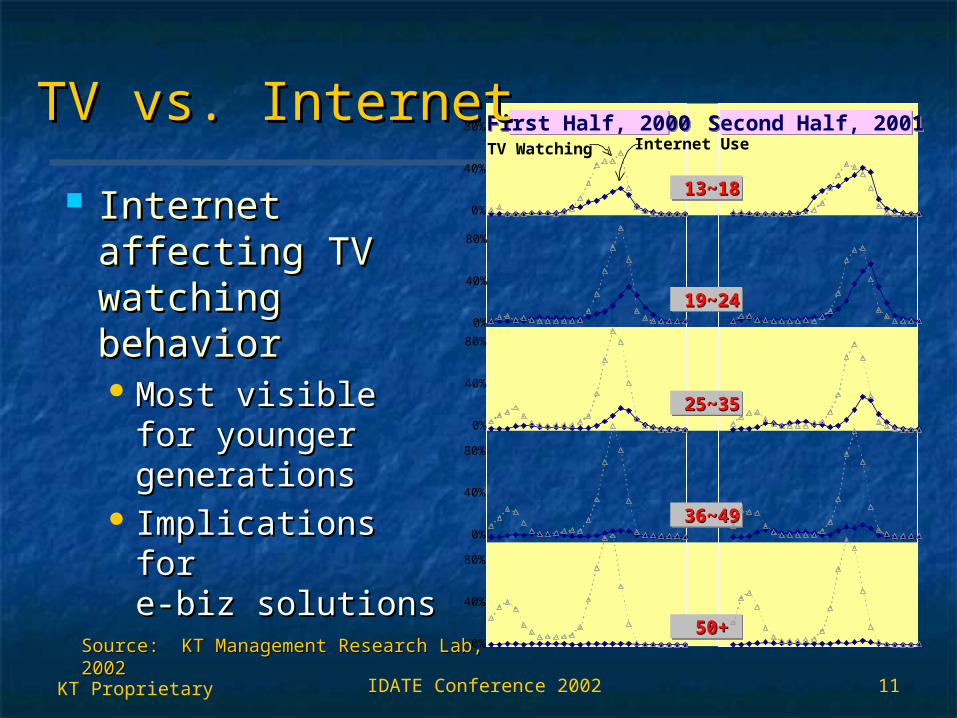

Internet Internet affecting TV affecting TV watching watching behaviorbehavior Most visible for Most visible for

younger younger generationsgenerations

Implications forImplications fore-biz solutionse-biz solutions

Source: KT Management Research Lab, 2002Source: KT Management Research Lab, 2002

First Half, 2000First Half, 2000 Second Half, 2001Second Half, 2001

13~1813~18 13~1813~18

19~2419~24 19~2419~24

25~3525~35 25~3525~35

36~4936~49 36~4936~49

50+50+ 50+50+

80%

40%

0%

80%

40%

0%

80%

40%

0%

80%

40%

0%

80%

40%

0%

TV Watching Internet Use

TV vs. InternetTV vs. Internet

KT Proprietary IDATE Conference 2002 12

AgendaAgenda

Korean Broadband OverviewKorean Broadband Overview

Lessons LearnedLessons Learned

Future ChallengesFuture Challenges

KT Proprietary IDATE Conference 2002 13

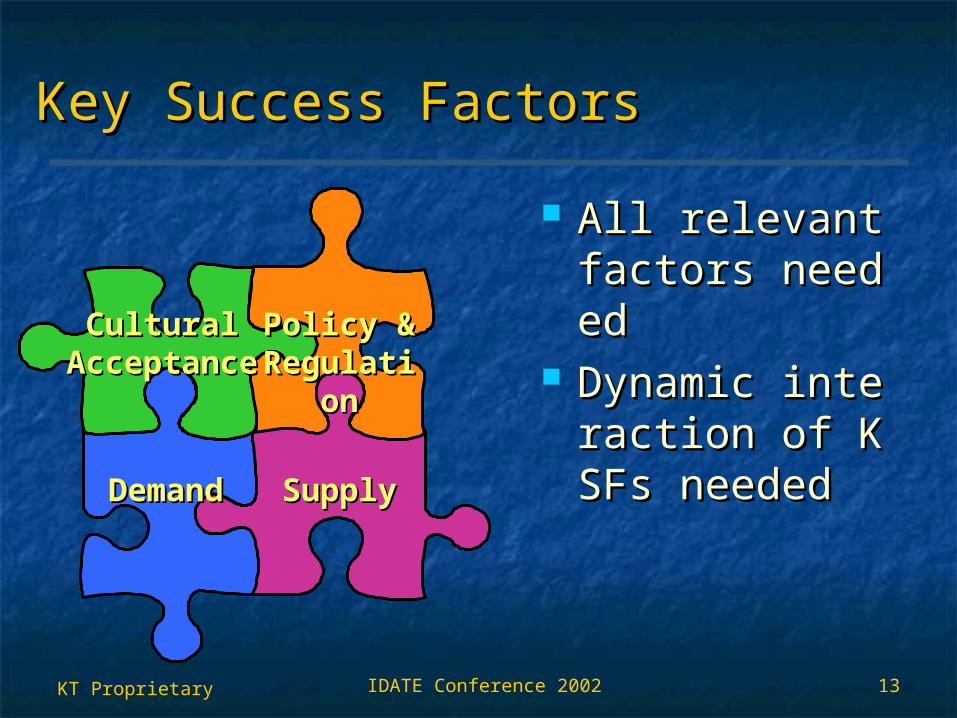

Key Success FactorsKey Success Factors

All relevant factoAll relevant factors neededrs needed

Dynamic interactDynamic interaction of KSFs neeion of KSFs neededded

Policy & Policy & RegulatiRegulati

onon

SupplySupply

CulturalCulturalAcceptancAcceptanc

ee

DemandDemand

KT Proprietary IDATE Conference 2002 14

KSF: Cultural AcceptanceKSF: Cultural Acceptance

““Digital or die”Digital or die” Historical lessons Historical lessons

driving national driving national consensus for consensus for digitalization digitalization

Socially competitiveSocially competitive Peer pressurePeer pressure

““Hurry” psychologyHurry” psychology

Cultural Cultural AcceptaAccepta

ncence

KT Proprietary IDATE Conference 2002 15

KSF: Policy and RegulationKSF: Policy and Regulation

Gov’t projects/initiativesGov’t projects/initiatives Early adopter roleEarly adopter role Public promotion Public promotion

Pro-competitionPro-competition Liberalization, forbearanceLiberalization, forbearance Facility-based competitionFacility-based competition

Effective incentivesEffective incentives Internet PCInternet PC Cyber Building CertificatesCyber Building Certificates

Policy & Policy & RegulatiRegulati

onon

KT Proprietary IDATE Conference 2002 16

KSF: DemandKSF: Demand

Enthusiastic adoption of Enthusiastic adoption of new servicesnew services Affluent, savvy, young Affluent, savvy, young

usersusers Many killer applicationsMany killer applications

Online games, stock Online games, stock tradingtrading

Extensive IT in educationExtensive IT in education Wholesale demandWholesale demand

PC cafes as aggregatorsPC cafes as aggregators .Com ventures.Com ventures

DemandDemand

KT Proprietary IDATE Conference 2002 17

KSF: SupplyKSF: Supply

Need for SurvivalNeed for Survival Facility-based competitionFacility-based competition Aggressive pricingAggressive pricing

Geographical AdvantagesGeographical Advantages Dense population/networkDense population/network Extensive legacy networkExtensive legacy network

Dropping network costsDropping network costs Quantity procurementQuantity procurement

SupplSupplyy

KT Proprietary IDATE Conference 2002 18

LessonsLessons

All factors are requiredAll factors are requiredPolicyPolicy: Align incentives of all key players,: Align incentives of all key players, Need to assume early adopter Need to assume early adopter rolesroles

DemandDemand: Attractive services/apps: Attractive services/appsSupplySupply: Facility based and fair competition: Facility based and fair competition

Timing and coordination is crucialTiming and coordination is crucialNeed to reach critical mass as fast as possibleNeed to reach critical mass as fast as possibleSequence less importantSequence less important

KT Proprietary IDATE Conference 2002 19

AgendaAgenda

Korean Broadband OverviewKorean Broadband Overview

Lessons LearnedLessons Learned

Future ChallengesFuture Challenges

KT Proprietary IDATE Conference 2002 20

Potential Broadband MarketPotential Broadband Market

Residential Broadband MarketResidential Broadband Market(Sub. in Mn) (Sub. in Mn)

1.73.9

5.0

8.3

0.3

12.0

9.5

7.8

4.0

2%

28%

54%

71%63%

1999 2000 2001 2002E 2005E

Business Broadband MarketBusiness Broadband Market

3.5 Mn Laptop/PDA Users

3 Mn SME/SOHO Users

Wireless LANWireless LAN

Multi-ADSLMulti-ADSL

KT KT subsub

ss

TotalTotalsubssubs

HH HH PenetratPenetrat

ionion

KT Proprietary IDATE Conference 2002 21

WLAN for BroadbandWLAN for Broadband

Rising Penetration RateRising Penetration Rate W-LAN ARPU EnhancementW-LAN ARPU Enhancement

00

2020

4040

6060

8080

Broadband Broadband ARPUARPU

Broadband + Broadband + W-LANW-LANARPUARPU

Broadband Broadband Broadband + W-LANBroadband + W-LAN

3030 3030

1313

(% per households and businesses )(% per households and businesses ) (KRW Thousand)(KRW Thousand)

27%

47%59%

67%69%

0%

25%

50%

75%

100%

2000 2002E 2004E2003E2001 2005E

70%

KT Proprietary IDATE Conference 2002 22

Broadband for SMEsBroadband for SMEs

Multi-ADSL SubscribersMulti-ADSL Subscribers B2B Solution SubscribersB2B Solution Subscribers Up to 16 Computers with 1 ADSL LineUp to 16 Computers with 1 ADSL Line

Higher ARPU: W53,000~W196,000 Higher ARPU: W53,000~W196,000 (W70,000 average) (W70,000 average)

110,000

89,000

73,000

Dec. 2001 Mar. 2002 May. 2002

For 3 million SMEs in KoreaFor 3 million SMEs in Korea

Provide tailored solutionsProvide tailored solutions

67,000

7,328

2,516

Dec. 2001 Mar. 2002 Aug. 2002

KT Proprietary IDATE Conference 2002 23

Broadbanding Challenges Broadbanding Challenges

- xDSL (VDSL)- xDSL (VDSL)

- IP- IP

- Metro Ethernet- Metro Ethernet

- IDC- IDC

e-portale-portale-portale-portal Wire & WirelessWire & WirelessIntegrationIntegration

Wire & WirelessWire & WirelessIntegrationIntegration

““Value networking Value networking company”company”

Total integrated Total integrated ServiceService

Broadband ServiceBroadband ServiceBroadband ServiceBroadband Service

- B2B solution platform- B2B solution platform

- Billplaza- Billplaza

- e-market portal- e-market portal

- 2.5G - 2.5G 3G 3G

- IP & Broadband- IP & Broadband

- Home Networking (HDS)- Home Networking (HDS)

- Fixed-Wireless Integration (WLAN)- Fixed-Wireless Integration (WLAN)

KT Proprietary IDATE Conference 2002 24

Value Networking ChallengesValue Networking Challenges

• Local cyber communityLocal cyber community

Cyber Dream TownCyber Dream Town

Home Networking

Mobile Networking

Office Networking

NESPOTNESPOT BizmekaBizmeka

• Home gateway/STBHome gateway/STB

Home Digital ServiceHome Digital Service

• B2B solutions portalB2B solutions portal

• VOD, entertainmentVOD, entertainment

Home Media ServiceHome Media Service

• Hot-spot WLANHot-spot WLAN

Xroshot serviceXroshot service• Unified MessagingUnified Messaging

enTUMenTUM• Hosting, IDCHosting, IDC

Metro Ethernet, IP-VPNMetro Ethernet, IP-VPN

KT Proprietary IDATE Conference 2002 25

Further ChallengesFurther Challenges

Business issuesBusiness issuesMature domestic market, M&A inevitableMature domestic market, M&A inevitableLegacy network poses evolution challengesLegacy network poses evolution challengesAdding value to broader-band networksAdding value to broader-band networks

Policy and regulatory issuesPolicy and regulatory issuesOverhauling traditional regulatory Overhauling traditional regulatory frameworkframework

Promotion of convergent servicesPromotion of convergent servicesOvercoming digital divideOvercoming digital divide

KT Proprietary IDATE Conference 2002 26

The Value Networking Company

Thank youThank you

The Value Networking CompanyThe Value Networking Company