kupiec & martin state and local tax webinar (as much as we can say in 60 minutes!) november 16,...

TRANSCRIPT

KUPIEC & MARTIN STATE AND LOCAL TAX WEBINAR(As much as we can say in 60 minutes!)

November 16, 2010

David J. Kupiec Natalie M. MartinKupiec & Martin, LLC Kupiec & Martin, [email protected] [email protected]

Welcome and Introductions

• Presenters• David Kupiec, Partner – Kupiec & Martin• Natalie Martin, Partner – Kupiec & Martin

• Administrative details – website and telephone • Participation welcome!• Let’s get started…

2

Webinar Overview

• Our purpose (and hopefully yours)• 4 recent presentations• Illinois election results – what does it mean?• What’s next?

3

4 Recent Presentations

• Is this Bad Sourcing and Allocation or Just Inconsistency? (Taxpayers’ Federation of Illinois Annual State and Local Tax Conference, September 23, 2010)

• Recent Developments in State and Local Tax – 2010: Legislative Developments (Illinois Bar Association State Tax & Local Tax Section Annual Fall Seminar, September 30, 2010)

• Current Issues and Opportunities in State Tax Controversy (Chicago Tax Club, October 27, 2010)

• Where Do We Go From Here? Differing Perspectives on How the Economy Affects State and Local Tax Issues (Chicago Bar Association, November 4, 2010)

4

Sales Factor

• Starting Point – 3 factor• National shift to single sales factor• All sales or gross receipts• Traditional sourcing – TPP– Services/intangible – cost of performance– throwback

5

Sales Factor- Emerging Trends

• Market approach• MTC• Gross v. Net Receipts• Throwout• Impact of inconsistency among states

6

Sales Factor – Illinois’ New Focus

• Audits/Auditor Interpretation and Discretion• Statutory Changes• Regulatory Changes• Case Law• Alternative Apportionment

7

Sales Factor – Recent Changes in Other States

• Texas and Michigan – MTC• Wisconsin – cost of performance• Oklahoma – market sourcing• Washington – market sourcing• New Jersey – throwout• Maine – throwout• California - numerous

8

Illinois 2010 Legislative Recap

• More than 10,000 Bills Introduced During the 2010 Legislative Session

• Illinois General Assembly Session Ended May 31, 2010 Without Passing a Balanced Budget

• Estimated Budget Shortfall Approx. $14 plus Billion (Deficit for Fiscal Years 2011 & 2012)

• Governor Proposed Income Tax Rate Increase & Business Items to Address Budget Shortfall

9

2009 Proposed Senate Bill 2252 – Not Passed

• 2 Year Temporary Income Tax Rate Increase (2010 and 2011)

• Individual Income Tax Rate Would Increase From 3% to 4.5% and Earned Income Tax Credit Would Increase from 5% to 10% of the Federal Tax Credit

• Corporate Income Tax Rate Would Increase From 4.8% to 7.2% (Personal Property Tax Replacement Tax Combined Rate of 9.7%)

• Status – Illinois House Voted Against (May 31, 2009)

10

2009 Proposed House Bill 0174 (“750”) – Not Passed

• Individual Income Tax Rate Would Increase From 3% to 5% on July 1, 2009

• Corporate Income Tax Rate Would Increase From 4.8% to 5% (Personal Property Tax Replacement Tax Combined Rate of 7.5%)

• Increase Property Tax Credit on Income Taxes From 5% to 10% and Earned Income Tax Credit From 5% to 15% of the Federal tax credit

• Expand Sales Tax Base - 39 Additional Services• Status – Illinois Senate Passed 31-27 (May 30, 2009)

11

Proposed Expanded Sales Tax Base(39 Potential Services)

• Other warehousing and storage• Travel agent services• Carpet and upholstery cleaning services• Dating services• Dry cleaning and laundry (except coin operated)• Consumer goods rental• Health clubs, tanning parlors, reducing salons• Linen supply• Interior design services• Other business services, including copy shops• Bowling Centers• Coin operated video games and pinball machines• Membership fees in private clubs• Admission to spectator sports (excluding horse tracks)• Admission to cultural events• Billiard Parlors• Scenic and sightseeing transportation• Taxi and Limousine services• Unscheduled chartered passenger air transportation• Motion pictures theaters, except drive-in theaters

• Pet grooming• Landscaping services (including lawn care)• Income from intrastate transportation of persons• Mini-storage• Household goods storage• Cold storage• Marina Service (docking, storage, cleaning, repair)• Marina towing service (including tugboats)• Gift and package wrapping service• Laundry and dry cleaning services, coin operated• Other services to buildings and dwellings• Water softening and conditioning• Internet Service Providers• Short term auto rental• Information Service• Amusement park admission and rides• Circuses and fairs – admission and games• Cable and other program distribution• Rental of video tapes for home viewing

12

• PA 96-1012 (SB3658) - Back to School State Sales Tax Holiday

• PA 96-0888 (SB1578) – Small Business Job Creation Tax Credit Act

• PA 96 – 1435 (SB0377)- Tax Amnesty Program • PA 96-1388 (SB0459) – Use Tax Reporting/Amnesty• PA 96-0905 (SB3089) – EDGE Credit Automotive

Manufacturers• PA 96- 0937 (SB3655) – R&D Credit Extension

13

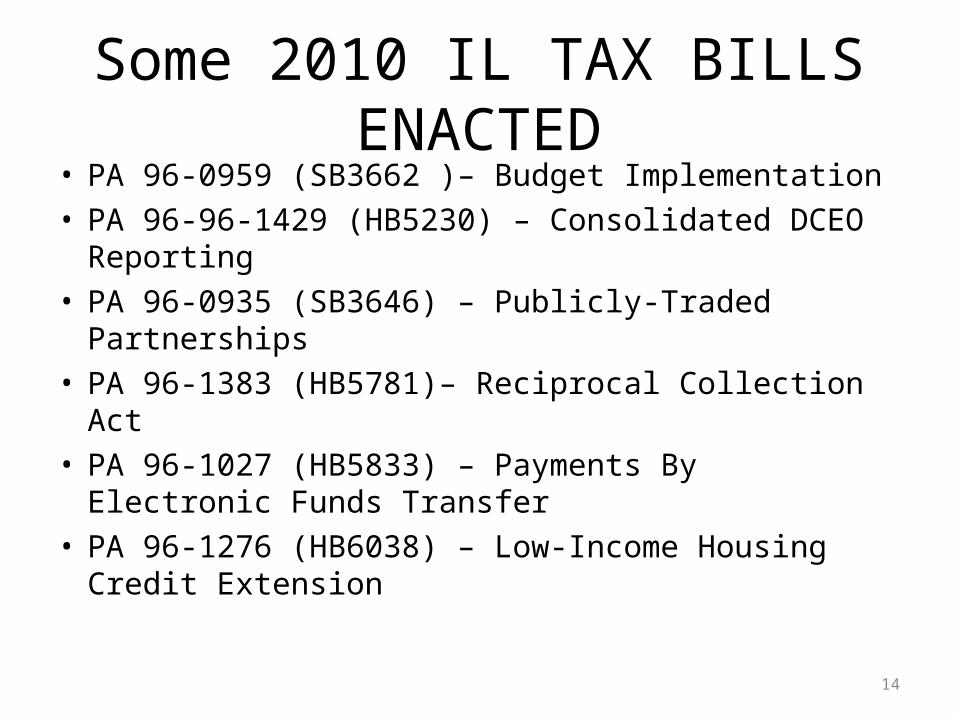

Some 2010 IL TAX BILLS ENACTED

• PA 96-0959 (SB3662 )– Budget Implementation• PA 96-96-1429 (HB5230) – Consolidated DCEO

Reporting• PA 96-0935 (SB3646) – Publicly-Traded Partnerships• PA 96-1383 (HB5781)– Reciprocal Collection Act• PA 96-1027 (HB5833) – Payments By Electronic

Funds Transfer• PA 96-1276 (HB6038) – Low-Income Housing Credit

Extension

14

Some 2010 IL TAX BILLS ENACTED

State Tax Controversy – The Current Economy

Taxpayer Issues:

• Tax Returns and Related Issues• Tax Planning• Tax Departments/Changes• Changes in business and operations• Dispute Resolutions – various methods• Disclosure and Reporting Requirements

15

State Tax Controversy – The Current Economy

State and Local Governments:

• It’s about the money!• Current auditors – hiring and retiring• Less resources in other areas• Complex audit issues• Legislative changes to enhance revenues

16

State Tax Controversy – The Current Economy

17

Legislation:

• It works!• Technical in nature• Expanding and extending tax benefits• Lobbying• Be proactive!

State Tax Controversy – The Current Economy

18

Refunds/Offsets:

• Currently, no refunds/offsets in Illinois• Less money in refund fund (statutory change)• States’ fiscal condition• Options going forward

State Tax Controversy – The Current Economy

19

Outlook for the future:

• Net loss carryforwards• Unitary groupings• Audit cycles• Litigation• Next “loophole closures”• Improving economy!

• Transactions

– Dispositions– Acquisitions– Restructurings– Mergers– Bankruptcy

20

The Future – Upcoming Activities

The Future – How to React

• Know your business and how it might change• Amend or Enact Laws• Promulgate Regulations• Alternative Apportionment• Settlements• Letter Rulings– General Information Letters– Private Letter Rulings

21

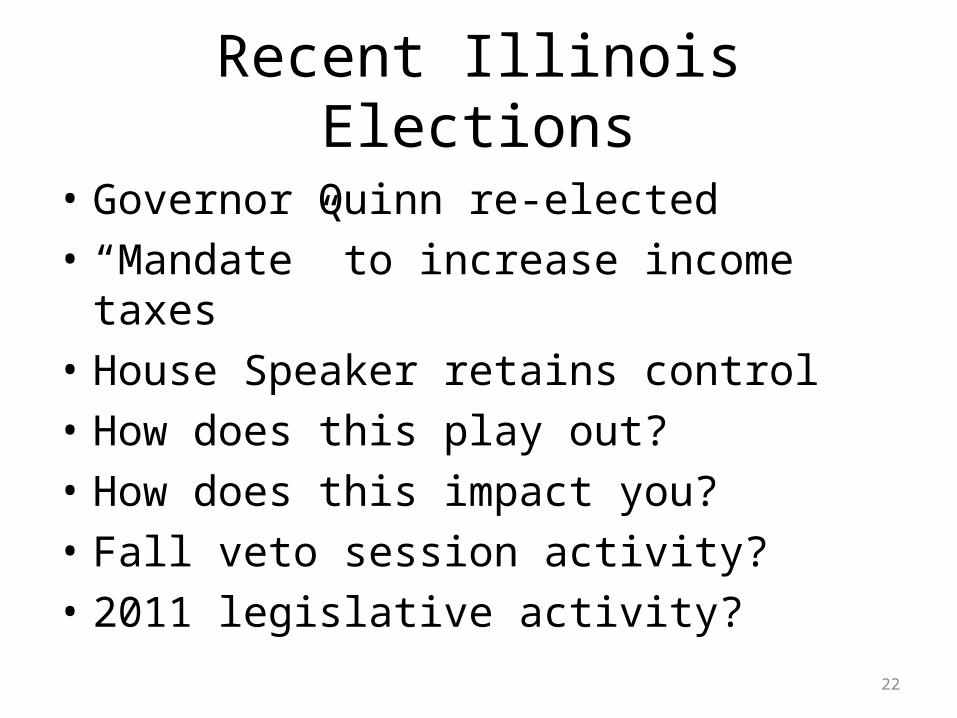

Recent Illinois Elections

• Governor Quinn re-elected • “Mandate” to increase income taxes• House Speaker retains control• How does this play out?• How does this impact you?• Fall veto session activity?• 2011 legislative activity?

22

What’s Next? • Potential Illinois Income Tax rate increase

– How much– Who it impacts– Opportunities– Expanded credits

• Potential Illinois Sales Tax Base Expansion– How much– Who it impacts– Opportunities– Expanded credits/exemptions

23

Conclusion

• 4 recent presentations – Take Aways• Illinois election results – what does it mean?• What’s next?

24

Questions?Contact Us

• David J. Kupiec(312) [email protected]

• Natalie M. Martin(312) [email protected]

• www.kupiecandmartin.com25

Circular 230 Disclosure

• CIRCULAR 230 DISCLOSURE - To comply with Treasury Department regulations, we inform you that, unless otherwise expressly indicated, any tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (1) avoiding penalties that may be imposed under the Internal Revenue Code or any other applicable tax law, or (2) promoting, marketing or recommending to another party any transaction, arrangement or other matter.

26