kzn cc bpo report - 1

TRANSCRIPT

0

�������������������� �������������

�������� ��������������������

�����������

�� ���������

���������������� � ������������������������������������� �������

1

CONTENTS

Executive Summary .................................................................................................. 4

Key Numbers ............................................................................................................ 5

About Durban and KwaZulu-Natal ............................................................................ 6

1. Introduction........................................................................................................... 8

2. Global Market and Trends ..................................................................................... 9

2.1. Market Size .................................................................................................... 9

2.2. Trends ............................................................................................................ 9

2.3. Major Competitors........................................................................................ 11

2.4. Generic Success Factors................................................................................ 15

3. South African Profile........................................................................................... 17

3.1. Trends in the South African Market .............................................................. 17

3.2. Regional Profile............................................................................................ 18

4. Durban and KwaZulu-Natal Sector Performance Analysis................................... 20

4.1. Sector Profile................................................................................................ 20

4.2. Operations .................................................................................................... 26

4.3. Human Resources ......................................................................................... 30

5. Durban and KwaZulu-Natal Environmental Profile and Trends .......................... 38

5.1. Introduction .................................................................................................. 38

5.2. Economic Development................................................................................ 39

5.3. Telecommunications and Information Technology........................................ 41

5.4. Labour and Skills.......................................................................................... 42

5.5. Infrastructure ................................................................................................ 45

5.6. Location ....................................................................................................... 46

Appendix A: Methodology ...................................................................................... 49

Appendix B: Population Statistics ........................................................................... 50

Appendix C: Business Indicators ............................................................................. 52

Appendix D: Call Centre/BPO Operations in KwaZulu-Natal.................................. 60

Appendix E: Exchange Rates................................................................................... 62

Appendix F: Contact Details.................................................................................... 63

List of Sources ........................................................................................................ 64

2

LIST OF FIGURES

Figure 1: Split of South African call centres according to location........................... 18

Figure 2: Medium and large call centre versus pocket call centres ........................... 20

Figure 3: Year of establishment ............................................................................... 21

Figure 4: Industry of operation ................................................................................ 22

Figure 5: Average firm outsourced versus captive orientation.................................. 23

Figure 6: Average firm international versus domestic orientation by turnover.......... 23

Figure 7: Functions performed................................................................................. 24

Figure 8: Use of language........................................................................................ 25

Figure 9: Inbound versus outbound calls.................................................................. 26

Figure 10: International versus domestic calls ......................................................... 27

Figure 11: Communication channels utilised ........................................................... 28

Figure 12: Frequency of client satisfaction measurement ......................................... 29

Figure 13: Employment race profile ........................................................................ 31

Figure 14: Employment gender profile .................................................................... 31

Figure 15: Attrition by employee category............................................................... 32

Figure 16: Average tenure by employee category .................................................... 33

Figure 17: Frequency of performance appraisals...................................................... 34

Figure 18: Hours of training per annum by employee category ................................ 34

Figure 19: Recruitment source................................................................................. 35

Figure 20: Agent recruitment requirements.............................................................. 36

Figure 21: Supervisor/team leader recruitment requirements ................................... 36

Figure 22: Manager Recruitment requirements ........................................................ 37

Figure 23: Economic development performance ...................................................... 39

Figure 24: Telecommunications and information technology performance .............. 41

Figure 25: Labour and skills performance................................................................ 43

Figure 26: Infrastructure performance ..................................................................... 45

Figure 27: Location performance............................................................................. 46

3

LIST OF TABLES

Table 1: Economic classification of call centre/BPO host countries ......................... 11

Table 2: Comparative rankings for international business indices ............................ 12

Table 3: Contact centre and BPO international investment environment comparison 13

Table 4: Country sector profile ................................................................................ 14

Table 5: Sector operational profile........................................................................... 15

Table 6: South African provincial comparison......................................................... 19

Table 7: Location of call centre operations .............................................................. 22

Table 8: Average working hours per month for staff................................................ 26

Table 9: Voice and data costs .................................................................................. 42

Table 10: Agent salaries in Rands............................................................................ 43

Table 11: Average office rental costs in Rands per m2 ............................................. 46

4

EXECUTIVE SUMMARY

Both Durban and KwaZulu-Natal have a well-established and yet rapidly growing call

centre industry. KwaZulu-Natal has a Gross Geographic Product (GGP) of US$

12,364 billion and is placed as the province with the second largest economy in South

Africa. Of the total 3.1 million people living in Durban itself, 943,538 speak English

as a first language while 23% have completed their secondary schooling or have a

tertiary qualification.

There are 67 call centre operations in KwaZulu-Natal employing a total of 7,573

people and serving a variety of sectors, the most prevalent of which are financial

services, ICT & telecommunications, retail and insurance. In total, 20% of call centre

capacity is orientated towards outsourcing. Further to this the amount of experience

and skills in these sectors can be considered to be substantial given that the average

number of years since establishment is 12 years. The growth projections for the

industry are also very promising. It is anticipated that the total number of operations

will increase to 83 over the next two years.

The average number of seats per KwaZulu-Natal operation is 120 and the median

number of calls handled per month is 53,006. A full 37% of all calls are international

in either origin or destination, highlighting the mix of offshore and domestic focus

that exists within the industry. A strong service culture can be considered to be

present, with an average 93% customer retention since establishment reported. This is

generally supported by factors such as strong employee performance management

practices at all levels and a low average external voluntary agent attrition rates of just

7%. In addition the average ratio of agent to supervisors is 6.1:1 and the ratio of

supervisors to managers is 6.5:1.

Contributory factors which have supported the establishment and growth of the

regional call centre industry include the comparatively low cost of rental space and

agents. A grade office space is available at an average monthly rental of R61.36

(£5.34) per m2, while the average cost of an agent per hour is R30.76 (£2.67).

Additional factors which have played a role in the development of the industry’s

offshore provision of services include the region’s strong cultural affinity to the UK

and similar English speaking markets, and time zone compatibility with Europe.

5

KEY NUMBERS

South Africa Sector Overview

Gross domestic Product (GDP) $160 billion Profile

Population 45 million Average percentage of

outsourcing 20%

Purchasing Power Parity (PPP)

(International Dollars) 10 960 Average seats per call centre 119.9

Estimated number of call centre

employees 79 000

Average employment per call

centre 128.3

Durban / KwaZulu-Natal Overview Projected employment growth

over next two years 91%

Gross Geographic Product (GGP)

for KwaZulu-Natal $12 billion

Average years since

establishment of operation 12

Population of KwaZulu-Natal 9.6 million Major international market UK

Population of Durban 2.81 million Operations

Unemployment in KZN 26.5% Primary language of service

provision English

People with tertiary qualifications

in KZN 6.9% Modal days of operation 365

English home language speakers

in KwaZulu-Natal 1 285 011 Median calls handled per month 53,006

Number of call centres 67 International calls as % of total

calls 37.1%

Number of seats 8 034 Voice telecoms cost per month R 236 216

Number of call centre employees 7 572 Average client retention since

establishment 92.6%

Agent cost per hour R 30.76 (£2.67) Human Resources

Projected salary increase for

agents in 2006 6%

Hours worked per month by

agents 167.2

International call cost per minute R 0.40 Agent external voluntary

attrition rate 6.9%

National call cost per minute R 0.44 Agents per team leader/

supervisor 6.1

Cost of 2 Mb line per month R 121 600 Team leaders/ supervisors per

manager 6.5

Monthly cost of A grade office

space per m2

R 61.36

(£ 5.34)

6

ABOUT DURBAN AND KWAZULU-NATAL

Welcome to the first report on the

Durban / KwaZulu-Natal call centre

environment. It is with great pleasure

that I share with you the depth of

experience and wealth of potential that this independently researched report

highlights.

My new appointment here at KZNonSOURCE is indicative of the focus and

commitment that the city has to the development of the region as a contact centre

service hub, to productively use the human capital that has developed alongside the

region’s world-class manufacturing, tourism, commercial and financial services

sectors.

Tasked primarily with attracting potential investors and clients to the city and the

region, KZNonSOURCE is confident that multinational company leaders will

recognise the benefits of the Durban operating environment, as have other global

companies who make the city their home, such as Unilever, Grindrod and Bell

Equipment.

This trend is also being observed in nationally operating corporates, who are

increasingly recognising the value proposition of Durban and KwaZulu-Natal and

migrating their operations to the region. Examples include Africa’s largest mobile

phone operator, MTN; the national mobile phone operator, Cell C; as well as the

financial services provider, Nedbank.

Our organisation is supported in its role by associated bodies such as the Durban

Investment Promotion Agency and Trade and Investment KwaZulu-Natal. However,

it is the close relationship and commitment to excellence and service delivery

exhibited by local and provincial government and city management that makes me

most confident of the local industry’s future. Indeed, I believe that the outsourcing

7

and internationally-focussed contact centre work emerging in the city is the beginning

of an influx of such opportunities, as international companies recognise the high

calibre of Durban’s service providers and personnel over and above the general

benefits of the South African operating environment and position.

The South African Contact Centre Community (SACCCOM) is an umbrella body for

the national industry that is tasked with highlighting the attractiveness of South Africa

as a call centre locale, particularly to the culturally-similar markets of the UK and

USA. Under their auspices, KZNonSOURCE is positioned to sell potential investors

who are considering South Africa on the particular benefits of our beautiful and

thriving UniCity.

Of course, my confidence in the development of Durban and KwaZulu-Natal is also

due to the amount of energy and resources that KZNonSOURCE has motivated to be

used on the development and support of the local industry, such as the development of

the Skills Development Academy, which has been implemented to ensure that we are

able to meet the increasing demand for trained operators, managers and supervisors.

I look forward to sharing our vision and strategy with you as we develop, and

introducing introduce investors and interested parties to the benefits of our city.

William Goldstone

Chief Executive Officer, KZNonSOURCE

8

1. INTRODUCTION

In recent years South Africa has become recognised as a key offshore contender for

call centre and business process outsourcing business. The purpose of this report is to

explore and define Durban and KwaZulu-Natal’s sector through the establishment of

baseline data for key indicators on the industry.

Within the broader goal of understanding and driving industry decision-making, the

aims of the research include:

• The identification of key strategic advantages that will promote Durban and

KwaZulu-Natal as a captive or outsourced operations destination to

international investors

• The provision of comparable measures across regions and sectors that will

allow local industry stakeholders to gauge industry trends and internal

performance

• The provision of factual and comprehensive insight into the industry for use

by local government in making development support decisions and developing

strategy.

To achieve these aims the report explores the global market and trends that are

shaping it before considering the positioning of South Africa relative to its major

competitors. The report then moves on to an analysis of Durban and KwaZulu-Natal

within South Africa, along with the profile and performance of the local sector.

Lastly, the report evaluates the performance of KwaZulu-Natal according to a set of

key investment drivers.

9

2. GLOBAL MARKET AND TRENDS

2.1. Market Size

A single figure for the total global market size of call centres and business process

outsourcing is not a practicable measure, although the aspects that can be quantified

offer insight into the likely size.

If one considers the global balance of payments figures for 2001, the total market for

all offshore service exports was estimated at $32 billion, mostly supplied by Ireland,

India, Canada and Israel. This figure however includes all service exports and is

limited to those countries that actually capture offshore service exports as an industry

classification. Within the 2003 figures for the USA, most noticeable was the increase

in the categories of computer and data processing services and accounting, auditing

and bookkeeping (UNCTAD, 2004). This represents a figure of US $1,8 billion per

annum. Research by Deloitte found that the world’s 100 largest financial institutions

expect to shift base cost to the value of $350 billion to international locations by 2008

(Gentle, 2003).

While the global figure cannot be calculated from these numbers alone, the figures do

suggest the market is both substantial and growing.

2.2. Trends

The global trends that are shaping the industry can be divided into those that motivate

companies to outsource and those that influence development in potential host nations

as nearshore and offshore destinations.

2.2.1. Trends Motivating Outsourcing

The triggers for considering outsourcing are brought about primarily under four

broad circumstances, in addition to the cost and profitability considerations, which are

taken for granted (Bousfield, 2003). Briefly, these include:

10

Mergers and acquisitions and the resulting rationalisation of operations

• Industry-wide changes such as deregulation

• Company-wide continuous improvement and process re-engineering

• Expansion and the resulting need to rationalise disperse localities and

resources.

2.2.2. Trends Influencing Development in Outsourcing Host Nations

In terms of trends amongst host nations, while there are a great number of trends to

incorporate, there are seven fundamental areas of change and development that

provide the most impetus and direction for the call centre and business process

outsourcing (BPO) industry, whether serving captive or outsourced markets (c.f

UNCTAD, 2004, AT Kearney, 2004, Merchants, 2005). These trends include:

• Intelligent networks and modern ICT capabilities that have facilitated the

match between a demand for cost savings and the availability of lower cost

host countries

• The quest by companies for new sources of cheap personnel and requisite

skills, that has in many cases been met by the proactive support of

governments when it comes to training and skills development

• The presence and promotion of existing skill sets and service potential have

frequently motivated location choice, following which foreign direct

investment (FDI) has been forthcoming from multi-national companies

• Agglomeration has resulted in the more established host countries gaining skill

and advanced services

• ‘Single-point service’ offering requirements by client firms have stimulated

consolidation and the increasing prominence of multi-national outsourcing

service providers

• Protection of intellectual property (IP) is gaining increasing prominence as

companies that outsource are looking to shift increasingly more sensitive and

demanding services to international locations based on capabilities and cost

savings

11

• Trends that could limit growth in locations, particularly those such as India

where growth has been extremely rapid, include demand for skilled and

experienced agents outstripping supply, and growing concerns regarding the

loss of mid to higher level white collar job functions in countries such as the

US.

2.3. Major Competitors

2.3.1. Defining South Africa’s Competitors

The global market can be distinguished by individual countries who are engaged in

contact centre and BPO activities on a scale that elicits either marked economic

changes, political pre-eminence, or both.

While these countries can be grouped according to geographic and economic zones,

for the purposes of analysis they have been subjectively grouped according to

economic value classification by virtue of their perceived ability to easily the required

levels of customer empathy and associated identification with the customer and

quality of service.

Table 1: Economic classification of call centre/BPO host countries

Mid to high-end value chain economies Ireland, South Africa, Israel, Philippines1

UK, Canada, Singapore, USA

Mass-market low value economies India

China

Source: Catalyst, 2005, unless otherwise indicated

While there are currently a large number of countries marketing themselves as

outsourcing destinations, for the purposes of this study the focus will be on countries

perceived to be English speaking competitors. To this end, Ireland can be identified as

a developed country which has become a benchmark in the global outsourcing trend,

as well as Israel, the Philippines and India which are perceived to be direct developing

economy competitors in terms of service provision in English.

1 The placement of the Philippines as a mid-to high-end value chain economy by B&M Analysts is by

virtue of its close cultural similarities with the USA (The Department of Trade and Industry, 2004).

12

2.3.2. Comparative Rankings for International Business Indices

In terms of South Africa’s position in the global call centre and business process

outsourcing market, international business indices find South Africa to hold a

consistently reliable position amidst the variable performances of competitor nations.

This deduction derives from the basket of indices presented in Table 2, where South

Africa is fairly consistently placed in the midst of the four competitors despite the

generally inconsistent ranking of the competitors themselves from one measure to the

next.

For each index, the first figure given (between 1 and 5) is limited to South Africa and

the four chosen comparators, and represents a performance ranking of only these

countries in relation to each other. The second figure represents the ranking of each

country in the overall index, with (n) denoting the number of countries included in the

total measure. Additional detail and explanations of these indices may be found in

Appendix E.

Table 2: Comparative rankings for international business indices

South Africa

Ireland India Israel Philip-pines

Business Competitiveness Indicator (n=103)2

3 (25)

2 (22)

4 (30)

1 (21)

5 (70)

Growth Competitiveness Index (n=103)3

3 (41)

2 (30)

3 (55)

1 (19)

5 (76)

AT Kearney Offshore Attractiveness Index (n=24)4

3 (17)

4 (23)

1 (1)

5 (24)

2 (6)

TI Corruption Perception Index (n=146)5

3 (44)

1 (17)

4 (90)

2 (26)

5 (102)

Moody’s Ratings6

4 (Baa1)

1 (Aaa)

5 (Baa3)

2 (A2)

3 (B)

2.3.3. Operating Environment Comparison

The socio-economic and infrastructural environment more specific to the

attractiveness of the call centre industry is also important in that it impacts greatly on

2 Source: World Economic Forum: Global Competitiveness Report 2004 3 Source: World Economic Forum: Global Competitiveness Report 2004 4 Source: AT Kearney: Offshore Location Attractiveness Index 2004 5 Source: Transparency International: Corruption Perception Index 2004 6 Source: Moody’s Investor Services 2005

13

the approach to foreign direct investment, marketing and support of the call centre and

BPO industry.

South Africa once again performs in a fairly stable position in terms of the various

measures presented in Table 23. Two factors in particular which differentiate South

Africa when compared to lesser developed economies are the strong intellectual

property (IP) protection laws, of which the favourable Software Piracy rankings are

indicative, and the reasonably high standard of living, of which the Purchasing Power

Parity (PPP) is indicative.

The same method of ranking and presentation of ratings has been used as in Table 2

above. Additional detail on these indices may also be found in Appendix E.

Table 3: Contact centre and BPO international investment environment comparison

South Africa

Ireland India Israel Philip-pines

Standard Corporate Sector Taxation

2 (30%)

1 (12.5%)

5 (41%)

4 (36%)

3 (32%)

Purchasing Power Parity (PPP) (International Dollars) PPP ranking (n= 208)7

3 (10,960)

1 (33,170)

4 (3,100)

2 (23,510)

5 (1,170)

Unemployment 4 (31.2%)

1 (2%)

Not available

2 (10.5%)

3 (10.7%)

Network Readiness Index (n=104)8

3 (34)

2 (22)

4 (39)

1 (18)

5 (67)

Software Piracy Rankings (n=103)9

2 (37%)

3 (38%)

5 (74%)

1 (33%)

4 (71%)

2.3.4. National Call Centre and BPO Sector Comparison

For ease of reference, the sector comparison across the five countries has been broken

down into sections dealing with sector profile (including size, markets served and

functions performed) and operational profile (including costs and staffing measures

such as attrition).

If call centres are considered separately from the more broadly defined concept of

7 World Bank (2005) 8 World Economic Forum (2004-2005) 9 Business Software Alliance (2005)

14

BPO, South Africa can be considered to have the second largest sector by

employment. While this is somewhat surprising given the late entry of South Africa

into the offshore outsourcing market, this may be explained by the well developed

domestic banking and telecommunication markets, both of which are defined as being

the top markets served by the South African call centre sector.

Table 4: Country sector profile

South Africa10

Ireland11 India12 Israel13 Philip-pines14

Estimated number of call centres (total)

535 110 Not available

500 200

Estimated number of call centre employees

79,000 28,000 403,00015 11,000 32,000

Most prevalent outsource country serviced

UK USA UK

USA UK

USA Europe

USA Malaysia Australia

Singapore Top sectors serviced

Financial services

Telecoms Medical

Telecoms IT

Telecoms E-commerce

IT Healthcare Insurance Travel & tourism

Telesales IT

HR Legal

services Financial services

Outsourcing bureaus Telecoms

Media Utilities Retail

Wholesale

Primary activities Customer service Account handling Technical support

Customer service Sales

Provide info

Customer Services

Provide info

Sales Customer

service Provide

info

Telesales Customer

service Technical support

Collections

Table 5 quantifies the operational competitiveness position of South Africa. Agent

salary costs, while higher than those in India and the Philippines, can be considered to

be considerably lower than those of Israel and Ireland. Similarly, the average rate of

attrition in South Africa is far lower than that of any of the comparators. This

10 Mitial Research (2003) 11 TOSCA (2004) 12 Scope Marketing and Information Systems (2001) 13 Catalyst (2005) 14 ACA Research (2003) 15 Employment refers to both ITES and call centre industries

15

indirectly implies that the relative annual investment in training and recruitment at a

South African call centre can be considered to be lower than that of the other

countries.

Table 5: Sector operational profile

South Africa

Ireland India Israel Philip-pines

Cost per seat / hour (USD) 13.84 7.00 19.00 4.39 Agent salaries / month (USD) 693 2, 670 141 800 236

Average agent tenure (months) 14.7%16 24 36 19

Average rate of attrition 6% 30% 22% 30% 15% Sources: As per Table 4 above

2.4. Generic Success Factors

Although a number of trends in the global contact centre market have been

highlighted, there appear to be four specific factors contributing to the success of

countries as outsourcing locations.

2.4.1. Government interventions

These tend to be structured around both short term inhibitors to growth as well as

future threats. For example, many countries have recognised the need for a large

labour pool who speak fluent English, have technical or computer skills, and are thus

addressing this from primary school to college-level educational institutions (AT

Kearney, 2004). Concurrent to this, governments are ensuring that skills training is

available to agents who are currently in or entering the industry to ensure that there is

no significant lag likely to the locality’s of competitive advantage.

2.4.2. Incentives to Encourage MNCs and FDI

Host countries are united in the favourable investment environments that they have

created for foreign direct investment and multi-national companies. While some (such

as Ireland) have placed no provisos on this investment in terms of either ownership or

16 Merchants (2005) figure for Africa

16

local participation, others (such as the Philippines) have insisted on skills transfer to

the local population (Tosca, 2004; ACA Research, 2003).

2.4.3. Co-operation and Consolidation

Successful outsourcing host nations have recognised their own areas of skill and

weakness, and marketed themselves accordingly. In some cased this has led to

agreements with those nations who have the skills that they lack in order to become

single-point service suppliers to their clients. For example, India makes use of

Singapore for IP-sensitive operations in recognition of its weak legislated intellectual

property protection (AT Kearney, 2004).

2.4.4. Cost versus Non-cost Based Positioning

While host countries recognise that cost will always be a motivating factor in

offshoring decisions, the industry has developed a level of sophistication where

differentiation and sustainability are measured in terms of quality and end-user

satisfaction measures, as opposed to simple cost calculations. This allows for focussed

development efforts and competition that takes into account all aspects of service

delivery. This has led to the type of positioning illustrated in Table 1.

17

3. SOUTH AFRICAN PROFILE

3.1. Trends in the South African Market

The London-based consultancy Control Risks Group is quoted as saying that South

Africa has a positive business environment with low political and security risk. It also

praises government policy and business governance, and claims that South Africa is

setting the trend for Africa (Financial Times Business, 2005).

This sentiment is reflected in the country’s strong investment rating, as well as

evidence of foreign direct investment into the country in a broad spectrum of

categories. The orientation towards global outsourcing is set to further grow as South

Africa is increasingly becoming more attractive as a ‘tier 2’ destination to countries

such as the United Kingdom as a result of unmet demand in ‘tier 1’ countries such as

India andChina.. This represents a direction of growth for the national industry in

addition to the one presented in Table 1, namely that of a mid- to high-end value

economy.

This is particularly encouraging in light of the fact that almost half of the opportunity

is anticipated to fall within the financial services and insurance sectors, and the

international indices discussed above reflect South Africa as strong within these areas

and still improving.

While South Africa offers a 30% to 40% cost saving over countries such as the United

Kingdom, it is still more costly than India and China, which could be an inhibiting

factor to industry growth. Despite this however South Africa is also increasingly

recognised as being able to differentiate itself on the basis of quality as opposed to

just cost when compared to destinations such as India and China.

18

3.2. Regional Profile

The South African Call Centre Community (SACCCOM) is an umbrella organisation

that has been established to promote the South African industry as a whole. To date,

however, the majority of marketing, promotion and development of the industry has

been undertaken by the individual organisations representing Gauteng

(ContactinGauteng), the Western Cape (CallingtheCape) and KwaZulu-Natal

(KZNonSOURCE).

Turning to the relative concentration of South Africa’s call centre industry, research

undertaken in 2002 indicated that the industry was clustered largely into three regions,

namely those mentioned above. Further to this it was estimated that 10.1% of the

industry was located in KwaZulu-Natal (Mitial Research, 2002).

All other (Including PE)

11%

Gauteng (JHB & Pretoria)

63%KwaZulu-Natal

(Durban & other)10%

Western Cape (Cape Town)

16%

Figure 1: Split of South African call centres according to location

Although the relative distribution is unlikely to have changed since 2002, the actual

number of call centres can be expected to be significantly out of date and are hence is

not supplied. Primary research undertaken for this report however identified a more

realistic figure which is presented in the next section.

19

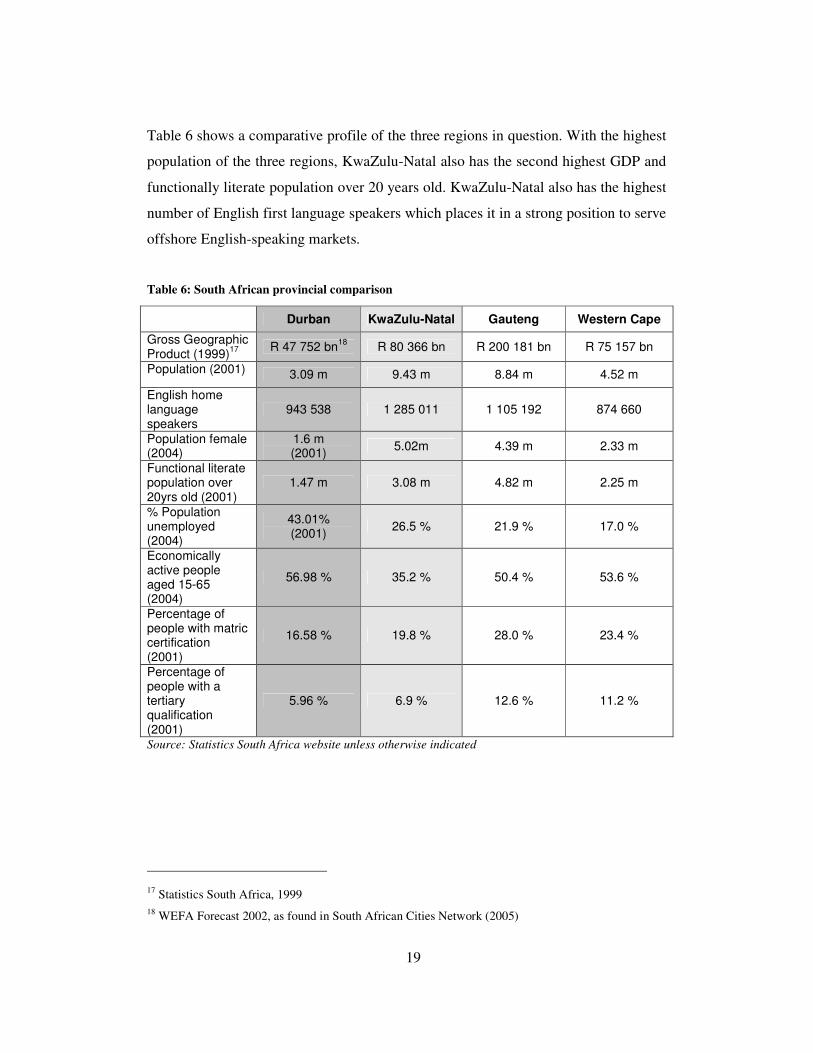

Table 6 shows a comparative profile of the three regions in question. With the highest

population of the three regions, KwaZulu-Natal also has the second highest GDP and

functionally literate population over 20 years old. KwaZulu-Natal also has the highest

number of English first language speakers which places it in a strong position to serve

offshore English-speaking markets.

Table 6: South African provincial comparison

Durban KwaZulu-Natal Gauteng Western Cape

Gross Geographic Product (1999)17 R 47 752 bn18 R 80 366 bn R 200 181 bn R 75 157 bn

Population (2001) 3.09 m 9.43 m 8.84 m 4.52 m

English home language speakers

943 538 1 285 011 1 105 192 874 660

Population female (2004)

1.6 m (2001) 5.02m 4.39 m 2.33 m

Functional literate population over 20yrs old (2001)

1.47 m 3.08 m 4.82 m 2.25 m

% Population unemployed (2004)

43.01% (2001) 26.5 % 21.9 % 17.0 %

Economically active people aged 15-65 (2004)

56.98 % 35.2 % 50.4 % 53.6 %

Percentage of people with matric certification (2001)

16.58 % 19.8 % 28.0 % 23.4 %

Percentage of people with a tertiary qualification (2001)

5.96 % 6.9 % 12.6 % 11.2 %

Source: Statistics South Africa website unless otherwise indicated

17 Statistics South Africa, 1999 18 WEFA Forecast 2002, as found in South African Cities Network (2005)

20

4. DURBAN AND KWAZULU-NATAL SECTOR PERFORMANCE

ANALYSIS

4.1. Sector Profile

4.1.1. Size and Growth

A total of 67 call centres were identified to be operating in KwaZulu-Natal. The

average employment amongst the sample survey participants of 119.9 implies that the

total employment within the sector is approximately 7,572. The average number of

seats per contact centre was slightly higher at 128.3, indicating that the total number

of seats is approximately 8,034. A full 71.4% of the call centres have more than 20

seats and can therefore be classed as medium or large call centres.

Pocket call centres28.6%

Medium & large call centres

71.4%

Figure 2: Medium and large call centre versus pocket call centres

The projected growth in turnover over the next year amongst the sample of firms

surveyed was 28.0%. In addition to this the average growth in employment and

number of seats is expected to increase by 54.7% and 65.8% respectively over the

course of the next two years. The increase of seats in tandem with employment is

21

essential in ensuring that there is enough capacity to deal with growth in the size of

the industry, however it is also evident that surplus seat capacity will remain.

Most of the surveyed operations are fairly new, with a substantial number (47.6%) of

them having been established in the past 5 years and 19.0% in the past two years. This

suggests that the industry is firstly fairly well established, but that it is also growing

very rapidly through the establishment of a number of Greenfield operations.

0

5

10

15

20

25

30

35

40

45

50

2000 - 2005 1995 - 1999 1990 - 1994 1985 - 1989 - 1984

Year of establishment

Per

cent

age

Figure 3: Year of establishment

Given that the number of call centre operations grew by 23.5% from 2003 to 2005, it

is reasonable to estimate that similar growth in Greenfield operations should be

expected from 2005 to 2007. A conservative estimate of total growth through to 2007

would therefore result in sector employment and seats reaching approximately 14,000

and 16,000 respectively, and the total number of contact centre operations increasing

to 83.

22

4.1.2. Location of Operations

Most of the call centre operations are located in the Durban CBD (44.8%), while the

remaining 55.2% are scattered around Pinetown/Westville (17.9%), Umhlanga/ Mt

Edgecombe (19.4%); Pietermaritzburg (7.5%). A further 10.4% are found in areas

other than those specified.

Table 7: Location of call centre operations

Durban CBD Pietermaritz-

burg

Umhlanga/

Mt Edgecombe

Pinetown/

Westville

Other

44.8% 7.5% 19.4% 17.9% 10.4%

4.1.3. Market and Orientation

The industry of operation and the number of companies operating in a particular

industry are given in Figure 4 below. The findings show that most of the companies

are operating in the financial, retail, ICT & telecommunications, and insurance

industries.

0 5 10 15 20 25 30 35 40

Financial Services

ICT & Telecommunications

Retail

Insurance

Government

Medical

Pharmaceuticals

Publishing

Security

Tourism

Vehicle Fleets

Manufacturing

Legal

Petrochemicals

Tobacco

Education

Gaming

Indu

stry

of o

pera

tion

Percentage

Figure 4: Industry of operation

23

Figure 5 highlights that the industry has a 20% outsourcing orientation on average,

meaning that on average 20% of turnover is derived from outsourcing work.

However it should be noted that the outsourcing orientation of individual firms varies

greatly from just 1% to 100%, but that 18.1% of the operations operate exclusively as

outsourcers. Amongst the firms that offer outsourcing services to one extent or

another the average number of clients served is 21.4.

Captive80.0%

Outsourced20.0%

Figure 5: Average firm outsourced versus captive orientation

Domestic96.3%

International3.7%

Figure 6: Average firm international versus domestic orientation by turnover

24

Figure 6 shows that the sector has a strong domestic focus at present when evaluated

by the un-weighted average turnover generated from offshore services, with 96.3% of

turnover on average being derived from domestic clients. The international markets

served include the UK, the Benelux states, Botswana, Italy, Mauritius, Namibia,

Swaziland and Zimbabwe, although the most significant foreign market by far is the

UK.

4.1.4. Operating Profile

Companies serve various functions as indicated in Figure 13. The most prominent

functions are customer services (90.9%), e-mails (72.2%), sales (68.2) and data

capture (45.5%). As illustrated in Figure 7, some functions are performed by few

companies, indicating a diverse set of competencies within the region.

0 10 20 30 40 50 60 70 80 90 100

Customer services

E-mails

Sales

Data capture

Correspondence management

Technical support

Credit Collection

Credit Card administration

Data Cleansing

Insurance/medical/other policy administration

Appointment setting

Securities administration

Financial accounting

Monitors alarm signals

Conducting surveys

Planning

New business processing

Ope

ratio

n

Percentage

Figure 7: Functions performed

Languages were rated to evaluate which languages are mostly used when serving

clients. In this regard it was established that all operations use English as their

primary medium of communication, highlighting a clear proficiency in the use of

English. However, it was also established that strong competencies exist in additional

25

domestic languages. Figure 8 illustrates that in addition to English numerous call

centres serve their clients in Afrikaans, IsiZulu and IsiXhosa.

Limited foreign language skills are apparent, thus restricting the ability to service

clients outside of those whose communication medium is English.

0 10 20 30 40 50 60 70 80 90 100

English

Afrikaans

IsiZulu

IsiXhosa

Sesotho

Portuguese

Italian

French

Hungarian

Use

of l

angu

age

Percentage

Figure 8: Use of language

An analysis of the number of days worked per annum highlights that although the

average number of days for call centres is 311.6, the mode of the sample is 365 days,

with 20% of firms comprising the mode.

Further to the above, while a staggered shift system is generally the norm, 18.2% of

the sample can be considered to operate on a 24/7 basis. The hourly utilisation during

weekdays is only 54.4% (typically 08:00 to 17:00) indicating a large excess in

available capacity.

On average, managers work 171.5 hours per month, while supervisors and agents

work 170.9 and 167.2 hours respectively. South African legislation is fairly flexible

regarding working hours and overtime and restrictions on working hours and overtime

does not apply in cases where staff receive more than R89,000 a year or R7,417 per

month.

26

Table 8: Average working hours per month for staff

Category Agents Supervisors Managers Hours 167.2 170.9 171.5

4.2. Operations

4.2.1. Call Volumes and Costs

The median number of calls handled by a single call centre is 53,006 per month,

although the maximum number is considerably higher than the median as a result of a

small number of large call centre handling extremely large call volumes.

At an aggregate level, 60.2% of all individual calls are outbound while 39.8% are

inbound. The significance of the measurement of total calls as opposed to the median

or average for firms is evident in the domestic versus international call volume

comparison (Figure 10). The measurement of offshore versus domestic turnover

presented in Figure 6 reflected a very low offshore orientation of the sector as it was

an un-weighted average of the orientation of each surveyed firms. Figure 10,

however, captures more the significant scale of those firms that are operating

internationally.

Outbound60.2%

Inbound39.8%

Figure 9: Inbound versus outbound calls

27

Domestic62.9%

International37.1%

Figure 10: International versus domestic calls

Lastly, the average expenditure on voice telecommunications per month is R 236,216,

while the average spend on data services is R 35,335. Specific call and data costs

available to firms are covered in more detail in the next section.

4.2.2. Call handling Statistics

Both call resolution and call abandonment are commonly used as international

performance metrics. On average, firms have a 76.9% first call resolution

performance. This is an interesting measure and one that needs to be considered in

conjunction with the function performed by a call centre and the context within which

it is being used by management. For example, certain query types may by their very

nature necessitate a resolution post the first call but may still be logged as an inability

to resolve on a first call basis. Abandonment rates clearly differ significantly between

the international and domestic markets served. Interestingly, abandonment rates

amongst the KwaZulu-Natal based firms when serving the domestic market average

4.0%, considerably higher than the 1.9% that they report for their international

markets. In this regard it is important to take note that the domestic average is brought

down considerably by the inclusion of call centres operating in, and making use of,

cellular network services.

28

The average time to an operator excluding IVR or voice recognition is 24.4 seconds.

While this measure is once again strongly influenced by factors as basic as available

seats, staffing levels, the market served and type of queries handles amongst others, it

is indicative of a general service-orientated culture in the sector.

Also relating to the handling of calls is the continuity of and reliability of operations.

In this regard 95.5% of the respondents indicated that they use a hot backup system

and at each of the firms with hot backup systems backups take place daily or more

frequently.

The average percentage downtime per company is 1.9% of total operational time, with

individual company percentage downtime varying from 0% to 10%. Problems that

result in downtime primarily relate to power failures and server problems.

4.2.3. Communication Channels

Figure 11 represents the communication channels from the most used to the least

used. It is clear that there is high penetration and hence a suggested competency in the

sector for all the areas explored. Interestingly, however, no firms have adopted speech

recognition technology to date.

0 10 20 30 40 50 60 70 80 90 100

Voice

Fax

SMS

Internet

Postal mail

Face-to-face

IVR

WAP/GPRS

Com

mun

icat

ion

chan

nel

Percentage

Figure 11: Communication channels utilised

29

4.2.4. Customer Satisfaction

There are varying performances in regard to the customer retention indicator. Half of

the companies have managed to retain 75-80% of the customers, while the other half

retained 98-100% of their customers since establishment. In a highly competitive

environment, it is important for companies to measure their client’s satisfaction in

order to enhance their customer retention and as such it is encouraging to note that the

average customer retention rate since establishment for the sector is 92.6%.

Although companies conduct surveys according to their need for information on

certain issues that are essential to their competitiveness, it is important for companies

to have ongoing assessments. This is particularly true in the services sector, where the

needs of clients have to be constantly monitored and catered for if companies want to

retain their customers. Companies that do not conduct client satisfaction

measurements are likely to remain complacent. The same applies to companies that

do not have ongoing monitoring systems, as they are likely to adopt retroactive rather

than proactive approaches in their dealings with challenges presented by their market.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Weekly ormore often

Monthly Quarterly Bi-annually Annually Less thanannually

Never

Frequency

Per

cent

age

Figure 12: Frequency of client satisfaction measurement

30

In this regard, it is evident that strong customer retention performance is supported by

strong client satisfaction measurement practices. The timing of measurement varies

considerably amongst the sample, with 9.1% of firms undertaking it as frequently as

weekly. What is extremely encouraging though is that 86.3% do undertake client

satisfaction performance measurements in one form or another on a systematic basis.

4.3. Human Resources

4.3.1. Employment Profile

The sector is clearly a large employer of Previously Disadvantaged Individuals

(PDIs)19, and it is encouraging to note that the majority of companies (81.8%) are

working towards achieving employment equity profiles more representative of that of

the demographic profile of the province through formal employment equity plans20 .

Asians currently constitute 55% of all agents working in this sector, as illustrated in

Figure 13. This is followed by Blacks (28,1%), Coloureds (10.7%) and Whites

(6.1%).

At the supervisory level, Asians still remains dominant (46.1%), whilst Blacks

constitutes 16.9%, Coloureds, 16.3% and Whites, 15.2% of employees working as

supervisors/team leaders. A majority of managers in this sector are however White

(42.6%) and Asian (38.9%) with Coloureds and Blacks constituting 5.6% and 13.0%

of the total respectively.

The number of women agents (70.9%) employed in this sector is more than twice that

of males (29.1%). Interestingly though, despite the high number of women at the level

of agents, this number declines significantly as one moves up the hierarchy. For

instance, at the supervisory/team leader category women constitute 26.9% of the total,

with males constituting 73.1%.

19 PDI’s refer to those individuals of population groups that were discriminated against prior to

democracy in 1994 20 Employment equity refers to the practice of realigning employee race, gender and disability profiles

to be representative of the country’s corresponding demographic profile

31

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Employee Category

Per

cent

age

Coloured 10.7 16.3 5.6

White 6.1 15.2 42.6

Asian 55.0 46.1 38.9

Black 28.1 16.9 13.0

Agents Supervisors Managers

Figure 13: Employment race profile

The situation at the management level also reflects an unexpected imbalance in

gender representation, although favouring women this time. 63% of managers are

women, while 37% are male.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Employee Category

Per

cent

age

Female 70.9 26.9 63.0

Male 29.1 73.1 37.0

Agents Supervisors Managers

Figure 14: Employment gender profile

32

The survey also revealed that there are an insignificant proportion of disabled persons

employed in the sector, at only 0.3% at an agent level and none at either a supervisory

or management level.

Of additional interest is that the average age of agents is 27.1 years and that 59% of

employees are from areas that could be classified as ‘previously disadvantaged’21.

4.3.2. Attrition and Tenure

As can be expected, staff attrition is the highest among agents at an average of 15.3%

per annum for 2004/2005. It is however important to distinguish between the three

different types of attrition, namely forced, external and voluntary, and internal and

voluntary. Figure 15 shows that only 7.5% of attrition is external and voluntary.

Both supervisor and management attrition can be considered negligible at just 8.0%

and 0.5% in total respectively.

0

2

4

6

8

10

12

14

16

18

Employee category

Per

cent

age

Forced attrition per annum 0.9 0.0 0.0

External & voluntary attrition perannum

7.5 2.4 0.2

Internal & voluntary attrition perannum

6.9 5.6 0.3

Agents Team leaders/supervisors Managers

Figure 15: Attrition by employee category

21 Previously disadvantaged areas are those formal and informal settlements that suffered socially and

economically under pre-democratic governance in South Africa, and are thus earmarked for upliftment

33

As can be expected from the low attrition rates presented above, average tenure

periods are high. The average length of tenure for an agent is 62.8 months, although it

is important to note that there is significant variance within the sample of firms. Given

that these measures are indicative of job satisfaction, and hence commitment to a

firm, this variance can be largely attributed to varying company cultures and

management practices.

0

10

20

30

40

50

60

70

80

90

Employee category

Mon

ths

Average tenure (months) 62.8 80.6 82.6

Agents Team leaders/supervisors Managers

Figure 16: Average tenure by employee category

4.3.3. Training and performance management

The data indicates that 60-70% of companies have performance-related compensation

for all employment categories (agents, supervisors and managers), which further

correlates with frequent performance appraisals. For example, 59.1% of agents and

52.4% of supervisors receive performance appraisals on a monthly or more frequent

basis.

A clear focus on productivity and service delivery therefore also exists, which is

reinforced by the average ratio of 6.1 agents per supervisor/team leader and 6.4

managers per supervisor/team leader.

A breakdown of hours spent on training indicates that agents receive an average of

65.2 hours of training per annum, while supervisors receive 75.7 hours and managers

34

receive 55.9 hours. There is a definite practical orientation to the agent-level training

as the average number of seats dedicated to training amongst the surveyed population

of call centres is 6.5.

0

5

10

15

20

25

30

35

40

45

50

Frequency

Per

cent

age

Agents 22.7 36.4 18.2 9.1 9.1 4.5

Supervisors 4.8 47.6 19.0 14.3 9.5 4.8

Weekly or more often Monthly Quarterly Bi-annually Annually

Less frequent or never

Figure 17: Frequency of performance appraisals

0

10

20

30

40

50

60

70

80

Agents Team leaders/supervisors Managers

Employee category

Hou

rs o

f tra

inin

g pe

r an

num

Figure 18: Hours of training per annum by employee category

35

It was estimated that the average cost to train an employee to competency is slightly

over R19,000, although this will differ considerably depending on the job

requirements and minimum skill and experience requirements when recruiting.

4.3.4. Recruitment

Figure 19 shows that employees are most commonly sourced via direct recruitment

and that where this is not the case recruitment agencies are used. No firms make use

of training providers, whilst very few have taken advantage of the SETA’s learnership

programme at this point (this may be attributed to the fact that the first set of students

who have been through the learnership programme have only recently graduated).

An analysis of the minimum educational levels of agents in Figure 20 indicates that

most of the firms (66.7%) require agents to pass Grade 12. This requirement does

however differ significantly from one firm to the next, with some firms requiring a

qualification as high as a post-matric diploma to be considered for an agent position.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Agents Team leaders/supervisors Managers

Employee Category

Per

cent

age

SETA learnersDirect employmentRecruitment agency

Figure 19: Recruitment source

36

Grade 1012%

Grade 1256%

Call centre certificate3%

Diploma3%

Degree0%

In-house training26%

Figure 20: Agent recruitment requirements

Figure 21 shows that while Grade 12 remains the predominant requirement at a

supervisor level, the importance of formal certificates and diploma qualifications

increases considerably. At a management level this remains the case, with Grade 12

constituting the minimum requirement 45% of the time, although at this level a degree

becomes a minimum requirement 22% of the time.

Grade 106%

Grade 1249%

Call centre certificate6%

Diploma11%

Degree11%

In-house training17%

Figure 21: Supervisor/team leader recruitment requirements

37

These finding suggest two things. The first is that career progression within the

industry even with very limited formal training is possible, and secondly that there is

a need for in-house training and learnership-type programmes to ensure that the

supervisors and managers are adequately equipped to deal with the challenges that

face them.

Grade 100%

Grade 1245%

Call centre certificate11%

Diploma11%

Degree22%

In-house training11%

Figure 22: Manager Recruitment requirements

38

5. DURBAN AND KWAZULU-NATAL ENVIRONMENTAL PROFILE AND

TRENDS

5.1. Introduction

An environmental profile and trends analysis was undertaken to unpack how Durban

and KwaZulu-Natal perform as call centre investment and operating locations. The

process used for this analysis incorporated the following:

Step 1: Identification of key investment drivers: Surveys and interviews with UK-

based executives of multi-national call centre and outsourcing operations as

well as interviews with South African-based senior mangers and executives of

multi-national call centres that have already invested in South Africa.

Step 2: Evaluation of investment performance: Executives and senior managers from

five major Durban-based call centre operations were interviewed and asked to

provide ratings of the performance of their operating environment for each of

the investment drivers identified.

The first step of the process yielded a total of 22 investment drivers which were

classified into the following categories:

• Telecommunications and information technology

• Labour and skills

• Infrastructure

• Investment support and economic environment

• Geographic location

The sections that follow outline the environmental ratings while also providing insight

into the factors which are presently or will in the future influence the ratings.

For each driver 1 represents ‘very poor’ performances, 5 ‘moderate’ performance and

10 ‘excellent performance’.

39

5.2. Economic Development

Economic development

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Pol

itica

l &ec

onom

icst

abili

ty

Ince

ntiv

es

Dev

elop

men

tag

ency

sup

port

Pre

senc

e of

an

esta

blis

hed

call

cent

re in

dust

ry

Figure 23: Economic development performance

5.2.1. Political and Economic Stability

International ratings agency Standard & Poor's has recently raised South Africa's

long-term credit rating from A to A+ in response to the country's improved economic

stability and reduced vulnerability to external shocks. The new rating places the

country three levels above the entry-level investment grade rating and above that of

Mexico and on a par with that of Poland and Thailand. More specifically, Standard &

Poor’s was quoted as follows: “The ratings on South Africa are supported by the

sovereign's prudent macroeconomic policies, a moderate debt burden, and strong and

stable political institutions” (SouthAfrica.info, 2005).

5.2.2. Presence of an Established Call Centre Industry

With 67 call centre operations and an average age of 12 years it is surprising to note

the fairly low rating for this criterion. With a conservative projected employment

40

growth rate of roughly 100% over the next two years this is again an indicator that can

be expected to see some change in future.

5.2.3. Development Agency Support and Incentives

There are two main investment agencies providing support to this sector. The first is

the Durban Investment Promotion Agency (DIPA) whose stated purpose is to

“facilitate sustainable investment in Durban for the benefit of all”.

In addition to the above, the province also has a specific focus on trade and

investment promotion via Trade and Investment KwaZulu-Natal (TIKZN). TIKZN is

tasked with stimulating trade and actively seeking both foreign and local direct

investment.

The primary vehicle for both of these entities to engage with the industry is

KZNonSOURCE, a specialised call centre association formed for the province in

2004. The first permanent CEO of KZNonSOURCE was appointed in July 2005 and,

with the strong support of both provincial and City governments, the scope and depth

of support to the industry provided by KZNonSOURCE can be expected to increase

significantly.

The present focus of KZNonSOURCE is four-fold:

• Skills development: A major programme is underway to establish a Skills

Development Academy (SDA) in Durban. The SDA is expected to produce

1,000 learners a year with qualifications and training aimed at agents,

supervisors and managers.

• Incentives: At present the Department of Trade and Industry (DTI) offers a set

of incentives that are generally linked to depreciation of assets. Opportunities

for sector specific incentives at a provincial or municipal level are being

explored.

41

• Marketing: Durban and KwaZulu-Natal are actively promoted as an

investment location both locally and internationally.

• Client liaison: Establishing and building relationship with existing operations

in the industry plays an important part in the institutionalisation and success of

joint industry initiatives.

5.3. Telecommunications and Information Technology

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Suitability of technologies Availability of serviceproviders

Availability of IT Skills

Figure 24: Telecommunications and information technology performance

5.3.1. Telecommunication Trends and Costs

South Africa’s telecoms industry has begun a deregulation process that will offer end-

users more competitive services. While the historical monopoly, Telkom, can be

considered to have built a national infrastructure that is rated as one of global

standing, the deregulation process can be expected to yield significant benefit to the

call centre industry.

42

The deregulation process has taken on multiple fronts. The most significant of these

has been the licensing of a Second Network Operator (SNO) and the liberalisation

allowing Value Added Network Service providers (VANS) to provide VOIP in

addition to carrying data.

At the time of this research the SNO had been licensed but had yet to make public any

service offerings. Once up and running however the service and price offerings are

expected to improve the competitiveness landscape for firms.

As of 1 February 2005 VANS have also been able to offer VOIP solutions to

corporate clients. This has generally resulted in more competitive long distance call

costs. The major competitors in this field include DataPro, Internet Solutions, Storm,

Telkom and UUNet. A survey of voice and data service providers revealed that the

lowest international call rate was R0.402 per minute while the lowest cost of a 2 Mb

leased line between Durban and London was R121,600 per month.

Table 9: Voice and data costs

International National Local 2 Mb leased line

(Durban-London)

Lowest

available cost

R0.402

per minute

R0.44

per minute

R0.307

per minute

R121,600

per month

5.4. Labour and Skills

5.4.1. Agent and Supervisor Availability and Skills

The inter-regional analysis showed that there are 841,000 unemployed people in

KwaZulu-Natal and that the total number of people with a tertiary qualification is 348,

744. The establishment of the Skills Development Academy by KZNonSOURCE

should contribute significantly to the skill level and skill pool of available candidates.

43

Labour & skills

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Ava

ilabi

lity

ofag

ents

Ava

ilabi

lity

ofsu

perv

isor

s

Ski

ll le

vel o

fav

aila

ble

agen

ts

Ski

ll le

vel o

fav

aila

ble

supe

rvis

ors

Com

petit

ive

labo

ur c

osts

Dom

estic

lang

uage

ski

lls

Fore

ign

lang

uage

ski

lls

Cul

tura

l aff

inity

to c

lient

mar

ket

Att

ritio

n &

sta

fftu

rnov

er

Figure 25: Labour and skills performance

5.4.2. Labour Costs

Labour costs in Durban are generally viewed to be more competitive than those of

either Cape Town or Johannesburg. Table 10, which is indicative of national salaries

for agents handling inbound calls at the time of placement, however suggests that at a

provincial level average agent salaries in KwaZulu-Natal are lower than those in

Gauteng, but that there is not much of a differentiation between KwaZulu-Natal and

the Western Cape. Differences that do exist seem to be specific to the level at which

the agent is being employed rather than an overall cost advantage in either location.

Table 10: Agent salaries in Rands22

Average Lower 25% Middle 50% Top 25%

Gauteng23 6,419 4,009 – 4,821 4,821 – 6,039 6,039 – 9,389

Western Cape 5,070 3,502 – 4,415 4,415 – 5,227 5,227 – 8,120

KwaZulu-Natal 5,140 3,553 – 4,263 4,263 – 5,887 5,887 – 7,866

Source: Kelly salary survey 2004

22 Salary figures represent basic remuneration and exclude fringe benefits and bonuses such as a 13th

cheque. 23 Un-weighted average of central and north Johannesburg, East Rand, West Rand and Pretoria rates

44

Supplementary primary research indicates that the average agent in KwaZulu-Natal

earns R30.70 per hour (£2.67) or approximately R5,157 per month based on a 168

hour month, although the entry level wage can potentially be as low as R23.00 (£2.00)

or approximately R3,864 per month. The average rate is therefore 70.2% cheaper than

that of an agent in Ireland. The lowest paying sectors are generally considered to be

those of leisure, media and retail, while the highest paying are considered to be those

of cellular telecommunications and electricity.

Average supervisor costs are in the region of R10,067 per month while entry level

costs are R4,800. By comparison, managers earn on average R20,000 per month but

can cost as little as R15,000 per month.

Increases for agents in the coming year are expected to average 6.0%, while increases

for supervisors and managers are expected to increase by 6.5%.

5.4.3. Cultural Affinity to Client Market and Language Skills

Cultural affinity to market needs to be separated into affinity to domestic market and

affinity to foreign market. In relation to cultural affinity to domestic market KwaZulu-

Natal is well placed. 80.9% of the population speak IsiZulu as a home language, while

13.6% speak English, 2.3% speak IsiXhosa and 1.3% Afrikaans. Collectively this

means that 63% of South Africa’s population could be served in their home language

and by agents who share their culture with ease. Further to this, home language

speakers for each of the other official languages are also available.

Historically, South Africa can be considered to have fairly strong cultural ties with the

UK, and Durban benefits from having Leeds (in the UK) as its sister city. Further to

this, the developed state of the economy, especially when compared to countries such

has India, allows for agents to far better relate to UK and US based customers.

Outside of the connection to English speaking (i.e. typically the UK and US) markets,

however, the extent of cultural affinity to offshore market is somewhat weaker.

5.4.4. Staff attrition and Turnover

The findings from the previous section highlight that the average agent attrition rate

inclusive of forced and voluntary attrition is 11.6%, while the average tenure of

45

agents is 62.8 months. This rate compares extremely favourably to the performance of

the comparator countries of Ireland, India, Israel or the Philippines.

5.5. Infrastructure

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Availability and cost of premises Local public transport

Figure 26: Infrastructure performance

5.5.1. Cost and Suitability of Premises

In terms of physical locations, South Africa has first-world office space in business

parks in all regions, as well as urban renewal incentives for CBD locations in many

cases. Comparative costs for both Grade A and Grade B office space in the three

major metropolitan areas where call centres tend to be clustered are illustrated in

Table 11.

Grade A office space in Durban at R 61.36 (£5.34) per m2 compares very favourably

to the cost of office space locations internationally.

46

Table 11: Average office rental costs in Rands per m2 24

Durban

& Environs Johannesburg

& environs Cape Town & Environs

Grade A 61.36 57.62 62.46

Grade B 47.58 50.02 48.58 Source: SAPOA (2004/5)

5.5.2. Local Public Transport

South Africa has a developed road system and international airports in all major

centres. Local public transport is perceived to be a problem however in that

commuters must rely on privately-operated minibus taxis due to the limited routes of

the municipal bus services.

5.6. Location

Geographic location

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Tim

e zo

neco

mpa

tibili

tyw

ith m

arke

t

Pro

xim

ity to

dom

estic

clie

nts

Acc

essa

bilit

y by

air

Cul

tura

l aff

inity

to e

x-pa

tin

vest

ors

&m

anag

emen

t

Qua

lity

of li

fe

Ple

asan

ten

viro

nmen

t to

visi

t

Figure 27: Location performance

24 Based on an un-weighted basket of rentals for each metropolitan area.

47

5.6.1. Time Zone Compatibility with Markets

South Africa has a maximum time difference of two hours with Europe, which makes

it well placed to compete with the United Kingdom’s current near-shoring operations.

In addition, potential also exists for potential operations to use their excess capacity to

service the USA market on the basis of a ‘follow the sun’ strategy.

5.6.2. Proximity to Domestic Clients

Durban has the second highest GDP and second highest population of all cities in

South Africa. A number of national and regional headquarters are consequently based

in the city. Examples of these include Unilever and Spar.

5.6.3. Accessibility by Air

Flight times between Durban International Airport and Johannesburg International

Airport are 1 hour, while flight times to and from Cape Town International Airport

are approximately 2 hours 5 minutes. At present no direct flights between Europe are

in place, although International flight times between London/Frankfurt and

Johannesburg are around 10 hours 40 minutes.

5.2.5. Cultural Affinity to Ex-pat Investors and Management, Quality of Life and

Pleasantness of Environment to Visit

Cultural affinity to ex-pats is difficult to define and quantify without a specific

cultural group as a reference point. However, despite the average rating provided for

this measure, the following should be noted:

• Language: South Africa can be considered to have fairly strong cultural lies

with the UK as well as other European countries from which emigrants have

historically been received. Although there are eleven official languages,

English has been the language of business since 1994. There are 943,538

English first-language speakers in Durban (35% of the total population) and

1,285,011 in KwaZulu-Natal. The English spoken is similar to that of the

United Kingdom and the USA which eases communication.

48

• Weather: The climate of the region is typified by warm, humid summers with

high rainfalls, and mild dry winters, meaning that the weather does not impede

business activities, and residents can enjoy an outdoor lifestyle year-round.

The average temperature in January is 22.70C and 12.60C in July, while

rainfall averages 137mm in January and 12mm in July. Durban enjoys an

average of 320 days of sunshine per year.

• Developed state of economy: The World Bank PPP index ranks the country

74th out of 208 countries. This highlights that even were an ex-pat to earn an

equivalent South African salary they would more likely enjoy a lifestyle

according to which they are accustomed than if they were based in India

(145th), or the Philippines (126th).

KwaZulu-Natal is also accustomed to hosting tourists, receiving an estimated 13.8

million domestic tourists and 1.2 million foreign tourists during 2003. 21% of the

foreign tourists were from the UK, while 12% were from Germany and 11% from the

US and Canada. 62% of all foreign visitors were on holiday while 22% were on

business. Further to this, Durban is accustomed to hosting major international events

such as the annual Tourism Indaba, at the city’s world-class International Conference

Centre (ICC).

49

APPENDIX A: METHODOLOGY

The research methodology employed was based on the stated objective of gaining

accurate and informed measures from relevant industry sources, so that the insight

derived was credible, and could be used with confidence for strategic development. It

is recognised that due to anticipated industry growth, this information will require

updating at regular intervals, but provides both the current position and key baseline

data for further studies.

Step 1 Identify the information required and formulate the research objectives

Step 2 Confirm the appropriateness of the research design methodologies

Step 3 Secondary research data collection

Step 4 Primary research data collection

Step 5 Design of the questionnaires

Step 6 Administer the surveys

Step 7 Collate and analyse the data and information gathered

Step 8 Report preparation

50