l esson 9 – s ummary methods of evaluating investments the net present value (npv) approach...

TRANSCRIPT

LESSON 9 – SUMMARY

Methods of evaluating Investments

The Net Present Value (NPV) approach Internal Rate of Return (IRR) Profitability Index (PI) Discounted Payback Period (DPP)

Comparison between the approaches

01

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATING INVESTMENT PROJECTS (1/2)

After computing the Cash Flows the next step is the

decision-making process for accepting or rejecting the

project, based on those Cash Flows.

The cash flows represent the money which one must invest

if undertaking the project and the money obtained by it.

Obviously the return has to be enough to allow the recovery

of the capital invested, but also to generate a profitability to

that capital.

Thus, the initial question focuses on the magnitude of that

return, i.e., what should be its size to consider that the

corresponding project is a good one. 02

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATING INVESTMENT PROJECTS (2/2)

This return can be divided in two components:

Risk-free interest rate: if we have a certain capital available to invest, we

could, without any risk, apply it in a secure investment (German

Government bonds) and we would get the interest rate associated with

this type of investment;

Risk premium: the investment in a particular project (business) has of

course a certain degree of risk (we are not sure that the estimated values

will end up happening in the future, in other words, we are not sure that

the cash flows of the project will materialize by the forecasted values).

Thus, the profitability associated with the project should cover

these two components. The greatest difficulty is in defining the

risk premium, since every project has different risk levels (for

example, a project of replacement of an equipment will certainly

have a lower risk than the expansion of the productive capacity

or the creation of a new business area).

03

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATION APPROACHES: NET PRESENT VALUE (1/3)

Let's imagine that in face of the risk of the project we believe that, if the same generates a return of 10%, it represents a good investment, i.e., we wish to undertake it.

Thus, the invested capital will not only have to be recovered but also has to generate an annual return of 10%.

On the other hand we know that the cash flows of the project are distributed over time. To compare or work with them, we have to use them in the same point in time. Usually we discount them all to zero (we have a much better perception of representing 1,000 € today than 1.000 € in five years).

The discount rate should naturally be the 10% that we identified above, i.e., should be the minimum annual return that we demand for our investment, since this rate represents the financial value of time considering jointly the project risk.

04

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATION APPROACHES: NET PRESENT VALUE (2/3)

05

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

Generalizing for any project, the NPV (VAL, in portuguese) is calculated as follows:

Where, I0 Investment undertook today

CFn Cash Flow of period n n Number of years in project lifetime r Discount rate (demanded return)

Decision Rule: If NPV > 0 Undertake the Investment If NPV = 0 Undertake or Re-evaluate the project If NPV < 0 Do not undertake the Investment

31 20 1 2 3

/ ....(1 ) (1 ) (1 ) (1 )

nn

CF CFCF CFVAL NPV I

r r r r

EVALUATION APPROACHES : NET PRESENT VALUE (3/3)

EXAMPLE

Consider that a firm forecasted the following cash flows for an

investment project:

Assuming an annual discount rate of 10%:

1)Compute the NPV.

2)Analyze the outcome and make the decision about undertaking or not

the project.

3)What is the impact on the NPV of a change in the discount rate?

In Excel use the function NPV() .06

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

0 1 2 3 4

Cash Flow

(650) 265 330 365 425

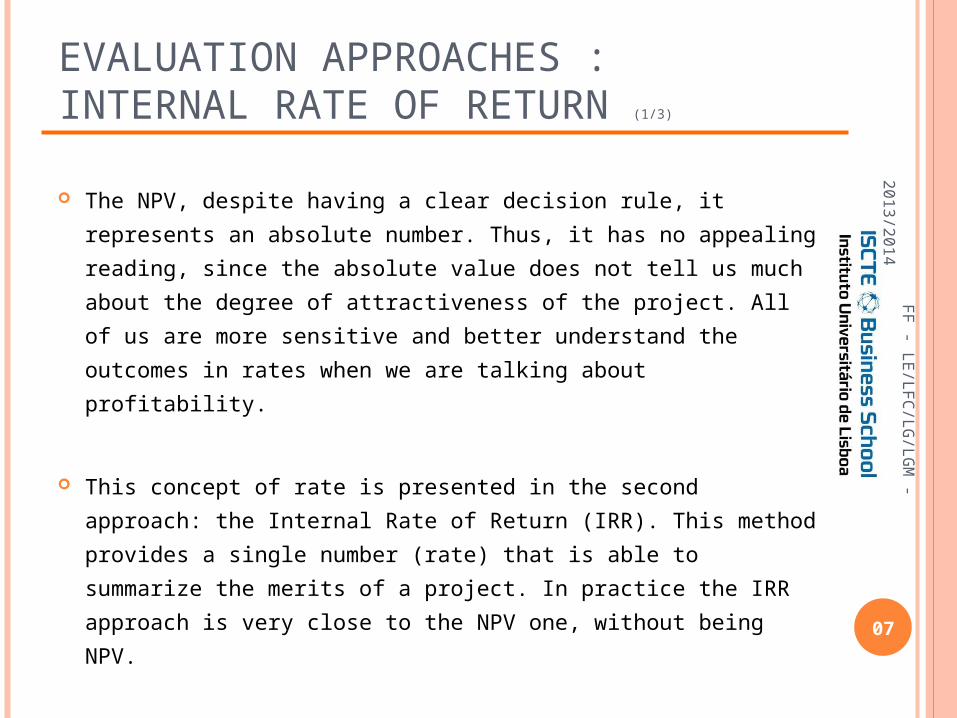

EVALUATION APPROACHES : INTERNAL RATE OF RETURN (1/3)

The NPV, despite having a clear decision rule, it represents an

absolute number. Thus, it has no appealing reading, since the

absolute value does not tell us much about the degree of

attractiveness of the project. All of us are more sensitive and

better understand the outcomes in rates when we are talking

about profitability.

This concept of rate is presented in the second approach: the

Internal Rate of Return (IRR). This method provides a single

number (rate) that is able to summarize the merits of a project.

In practice the IRR approach is very close to the NPV one,

without being NPV.07

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATION APPROACHES : INTERNAL RATE OF RETURN (2/3)

08

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

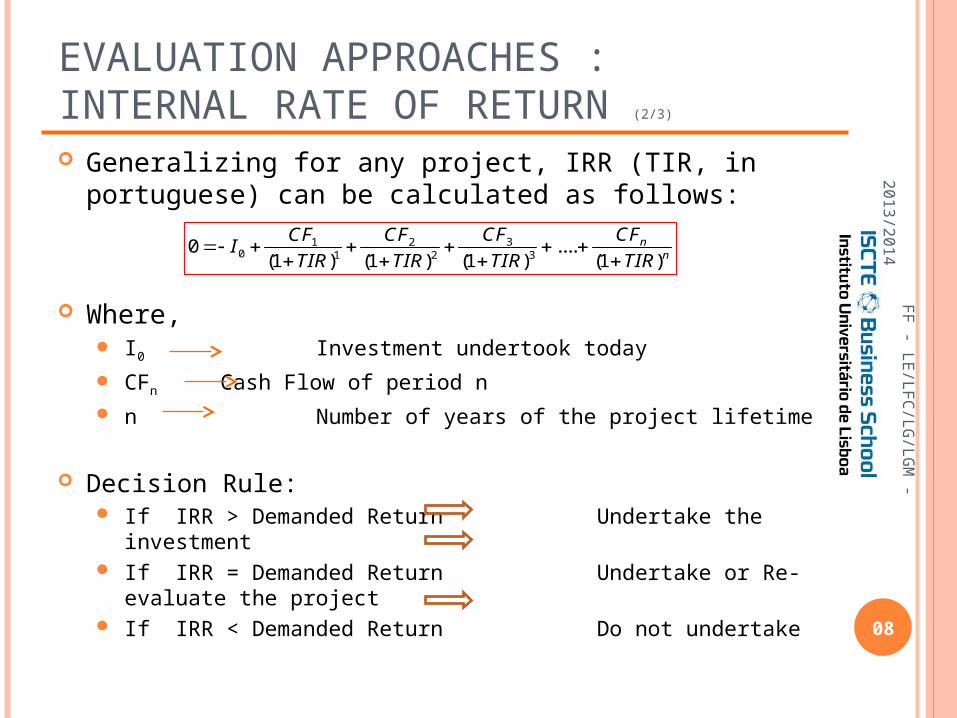

Generalizing for any project, IRR (TIR, in portuguese) can be calculated as follows:

Where, I0 Investment undertook today

CFn Cash Flow of period n n Number of years of the project lifetime

Decision Rule: If IRR > Demanded Return Undertake the

investment If IRR = Demanded Return Undertake or Re-

evaluate the project If IRR < Demanded Return Do not undertake

31 20 1 2 3

0 ....(1 ) (1 ) (1 ) (1 )

nn

CF CFCF CFI

TIR TIR TIR TIR

EVALUATION APPROACHES : INTERNAL RATE OF RETURN (3/3)

EXAMPLE

Consider the information of the previous example and:

1)Compute the IRR.

2)Analyze the outcome and make the decision about undertaking or not

the project.

3)Illustrate graphically the relationship between the NPV and the

discount rate, identifying the IRR.

In Excel use the function IRR() .

09

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATION APPROACHES: PROFITABILITY INDEX (1/3)

The Profitability Index (PI) is essentially a different way of presenting

the information already conveyed by the NPV. Represents the

absolute return, reported to the present moment, per unit of capital

invested.

It is a ratio of the present value of the future cash flows after CAPEX

over the CAPEX.

The reading of the outcome is of: for each money unit invested, it is

possible to get PI units of return. This relationship is established at

the time zero, i.e., at the beginning of the project.10

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATION APPROACHES : PROFITABILITY INDEX (2/3)

11

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

Generalizing for any project, the PI (IRP, in portuguese) can be calculated as follows:

Where, It Investment undertook today

CFt Cash Flow of period t n Number of years of the lifetime of the project r Demanded Return

Decision Rule: If IRP > 1 Undertake the investment If IRP = 1 Undertake or Re-evaluate the project If IRP < 1 Do not undertake

0

0

(1 )

(1 )

nt t

ttn

tt

t

CF I

rIRP

I

r

EVALUATION APPROACHES: PROFITABILITY INDEX (3/3)

EXAMPLE

Still using the same example:

1)Compute the PI.

2)Analyze the outcome and make the decision about undertaking or not

the project.

3)Assuming that on year 3 the firm acquires an equipment by the price

of 25, recalculate the PI.

12

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATION APPROACHES: DISCOUNTED PAYBACK PERIOD (1/3)

The previous approaches value the profitability of the project.

However, in some circumstances, as much or more important as

profitability is the pace of recovery of the investment. Imagine a

project that will be carried out in a context of political, economic or

social instability. In these situations it is important to know how long

it takes to recover the investment.

The DPP is fundamentally a risk indicator and not a profitability

measure.

The procedure to be followed in its calculation is derived from the

sum of the discounted cash flows (opposite to the DPP, the simple

PP does not take into account the time value of money) up to a

value of zero (break-even). 13

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

EVALUATION APPROACHES: DISCOUNTED PAYBACK PERIOD (2/3)

14

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

Generalizing for any project, the DPP (PRI, in portuguese) can be calculated as follows:

Where, CFt Cash Flow of period t r Demanded Return

Decision Rule: If PRI < Lifetime of the project* Undertake the investment If PRI = Lifetime of the project* Undertake or Re-evaluate

the project If PRI < Lifetime of the project* Do not undertake

* or any particular cut-off date

0

0(1 )

PRItt

t

CF

r

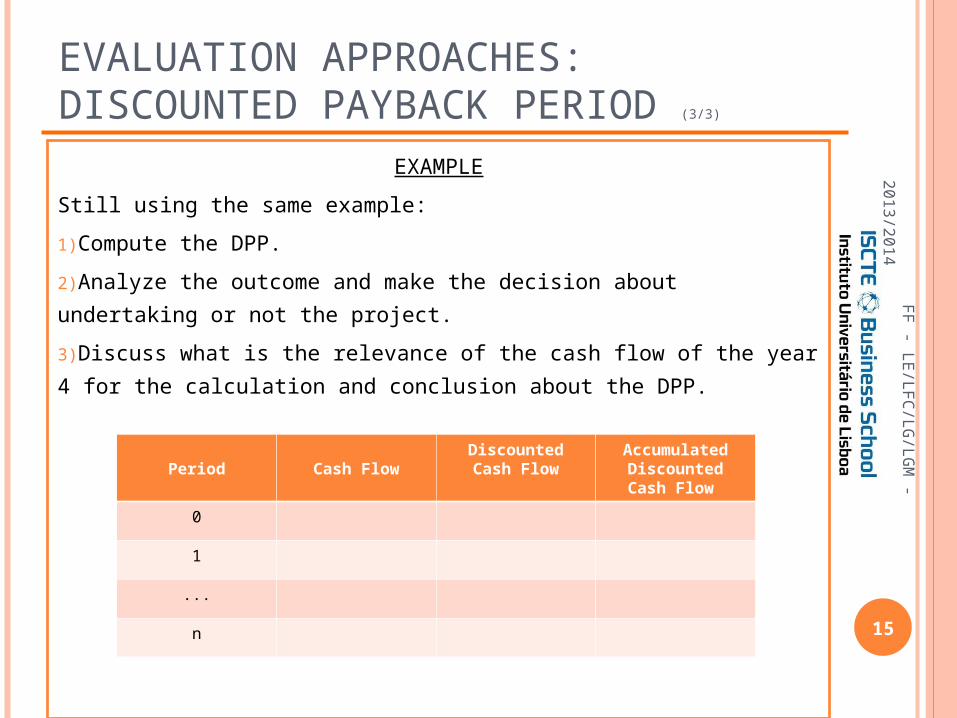

EVALUATION APPROACHES: DISCOUNTED PAYBACK PERIOD (3/3)

EXAMPLE

Still using the same example:

1)Compute the DPP.

2)Analyze the outcome and make the decision about undertaking or not

the project.

3)Discuss what is the relevance of the cash flow of the year 4 for the

calculation and conclusion about the DPP.

15

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

Period Cash FlowDiscountedCash Flow

AccumulatedDiscountedCash Flow

0

1

...

n

COMPARING THE METHODS – A SINGLE PROJECT (1/3)

The NPV is a Cash approach, reflecting the increase in value for the shareholder. Assumes reinvestment of intermediate cash flows at a minimum required rate.

IRR is an annual rate and represents the internal rate of profitability, assuming the reinvestment of project cash flows at the IRR itself.

The PI represents a weight factor for each euro invested in the project.

The DPP is a measure of time and indicates the length of time required for recovery of the investment.

16

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

COMPARING THE METHODS – A SINGLE PROJECT (2/3)

In the presence of a project where there is an initial outflow and later inflows, all methods reach the same conclusion:

Accept the project:NPV > 0 , IRR > r , PI > 1 , DPP < n

Accept/Re-evaluate the project:NPV = 0 , IRR = r , PI = 1 , DPP = n

Reject the project:NPV < 0 , IRR < r , PI < 1 , DPP > n 17

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4

COMPARING THE METHODS – A SINGLE PROJECT (3/3)

In the presence of a project where the cash flows are "abnormal" the method to adopt is of the NPV.

The IRR approach has problems: Does not distinguish between financing or

investing operations. May deliver more than one outcome (Multiple

IRR). In calculating the DPP it is necessary to be

cautious about the fact that the accumulated value of the discounted cash flows may change its sign more than once.

18

FF - LE

/LFC

/LG/LG

M - 2

01

3/2

01

4