lafarge africa plc n131.65 billion rights issue africa... · lekki-ikoyi bridge, lagos nigeria...

TRANSCRIPT

Lekki-Ikoyi Bridge, Lagos Nigeria

Lafarge Africa PlcN131.65 Billion Rights Issue

Facts Behind the Offer

November 30, 2017

The information in this presentation is given in confidence and may not be reproduced or redistributed to any other persons

This document has been prepared solely for use at the Facts Behind the Offer held in connection with the Lafarge Africa PLC

(“Lafarge Africa” or the “Company”) Rights Issue Programme. The information contained in this document has not been

independently verified and no representation or warranty, express or implied, is made as to, and no reliance should be placed

on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. The information set out

herein may be subject to updating, revision, verification and amendment and such information may change materially. Chapel

Hill Denham Advisory Limited (“Chapel Hill”), and Standard Chartered Capital & Advisory Nigeria Limited (“Standard

Chartered”), are not under any obligation to update the information contained in this presentation and any opinions expressed in

it are subject to change without notice. Chapel Hill, Standard Chartered or any of their respective affiliates, advisers or

representatives shall not have any liability whatsoever (in negligence or otherwise) for any loss whatsoever arising from any use

of this document or its contents, or otherwise in connection with this presentation

Any decision to purchase or subscribe for securities in connection with the Right Issuance should be made solely on the basis of

your own investigations with respect to Lafarge Africa and the Rights Issuance

None of the professional parties herein stated nor any of their representatives make any representation or warranty, expressed

or implied, as to the accuracy or completeness of any information contained in this document

Only those particular representation and warranties, if any, which may be made in a definitive written agreement, when, as and if

executed, and subject to such limitation and restrictions as may be specified therein, will have any legal effect

Any market analysis and estimates presented in this document represent the subjective views of Chapel Hill, and Standard

Chartered or the source reference if any

Disclaimer

2

Outline

3

Section Page

1. Company Overview 5

2. Nigerian Cement Industry Overview 11

3. Financial Overview 15

4. Business Outlook 21

5. Transaction Summary 24

6. Appendix 28

Company Overview

REVENUE CONTRIBUTION (FY’16)

Snapshot of Lafarge Africa

LISTING INFORMATION

► Listed on The Nigerian Stock Exchange in 1979

► 9th largest company on The NSE by market

capitalisation

► Market capitalization of N307 billion1

PRODUCTION INFORMATION

14.1 MTPA2

TOTAL

CAPACITY

OPERATIONS

3 COUNTRIES

(NIGERIA, SOUTH AFRICA, GHANA)

21

QUARRIES

PRODUCTS

► Cement

► Ready-Mix

► Aggregates

► Fly Ash

9th

70%

NIGERIA

30%

SOUTH

AFRICA

SELECT AWARDS

► Most innovative in manufacturing (2017,

2016), BusinessDay

► Best Company in Stakeholder Engagement

and Most Outstanding Company of the

Decade (2016), SERA

► Best Company in Sustainability Reporting

(2015), SERA

Revenue

(FY’16)

Revenue CAGR

(FY’12 – FY’16)

PAT

(FY’16)

Earnings per

share (FY’16)

Total assets

(FY’16)

Return on equity

(FY’16)

Sources: Lafarge Africa, NSE, Bloomberg

1. As at 20 October 2017

2. Excludes aggregates, RMC, Fly Ash

6

CEMENT

PLANTS

N220bn 24.7% N3.15N16.9bn N503bn 6.8%

6

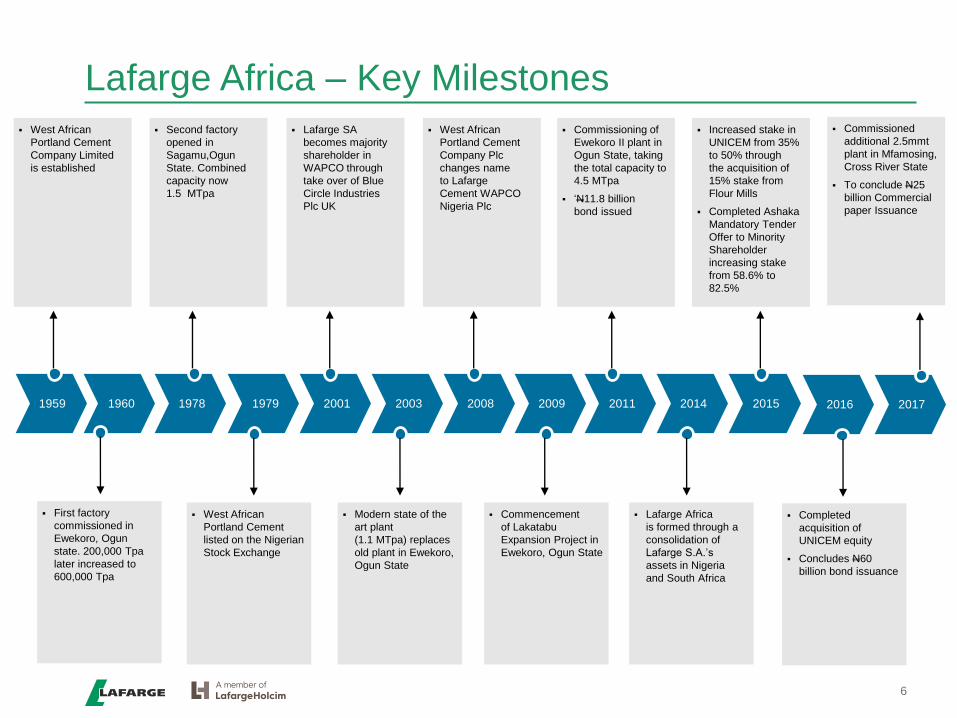

Lafarge Africa – Key Milestones

6

Increased stake in

UNICEM from 35%

to 50% through

the acquisition of

15% stake from

Flour Mills

Completed Ashaka

Mandatory Tender

Offer to Minority

Shareholder

increasing stake

from 58.6% to

82.5%

Commissioning of

Ewekoro II plant in

Ogun State, taking

the total capacity to

4.5 MTpa

‘N11.8 billion

bond issued

West African

Portland Cement

Company Plc

changes name

to Lafarge

Cement WAPCO

Nigeria Plc

Lafarge SA

becomes majority

shareholder in

WAPCO through

take over of Blue

Circle Industries

Plc UK

Second factory

opened in

Sagamu,Ogun

State. Combined

capacity now

1.5 MTpa

West African

Portland Cement

Company Limited

is established

1959 1960 1978 1979 2001 2003 2008 2009 2011 2014 2015

Lafarge Africa

is formed through a

consolidation of

Lafarge S.A.’s

assets in Nigeria

and South Africa

Commencement

of Lakatabu

Expansion Project in

Ewekoro, Ogun State

Modern state of the

art plant

(1.1 MTpa) replaces

old plant in Ewekoro,

Ogun State

West African

Portland Cement

listed on the Nigerian

Stock Exchange

First factory

commissioned in

Ewekoro, Ogun

state. 200,000 Tpa

later increased to

600,000 Tpa

2016

Completed

acquisition of

UNICEM equity

Concludes N60

billion bond issuance

Commissioned

additional 2.5mmt

plant in Mfamosing,

Cross River State

To conclude N25

billion Commercial

paper Issuance

2017

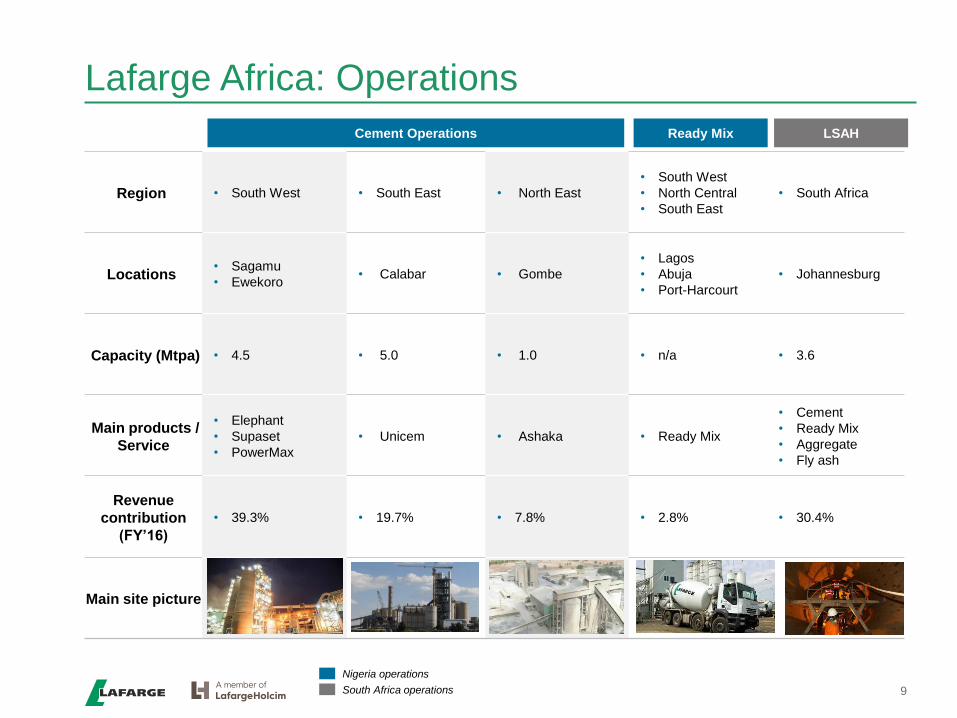

Lafarge Africa: Operations

Cement Operations

Region • South West • South East • North East

• South West

• North Central

• South East

• South Africa

Locations• Sagamu

• Ewekoro• Calabar • Gombe

• Lagos

• Abuja

• Port-Harcourt

• Johannesburg

Capacity (Mtpa) • 4.5 • 5.0 • 1.0 • n/a • 3.6

Main products /

Service

• Elephant

• Supaset

• PowerMax

• Unicem • Ashaka • Ready Mix

• Cement

• Ready Mix

• Aggregate

• Fly ash

Revenue

contribution

(FY’16)

• 39.3% • 19.7% • 7.8% • 2.8% • 30.4%

Main site picture

Ready Mix LSAH

Nigeria operations

South Africa operations 9

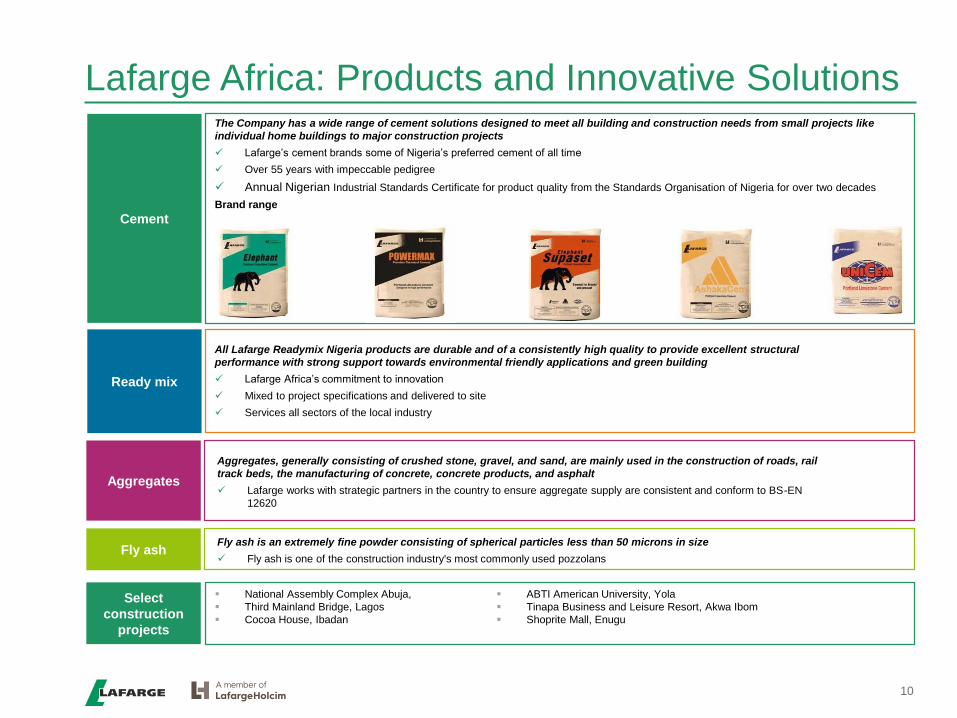

Lafarge Africa: Products and Innovative Solutions

Ready mix

All Lafarge Readymix Nigeria products are durable and of a consistently high quality to provide excellent structural

performance with strong support towards environmental friendly applications and green building

Lafarge Africa’s commitment to innovation

Mixed to project specifications and delivered to site

Services all sectors of the local industry

Aggregates

Aggregates, generally consisting of crushed stone, gravel, and sand, are mainly used in the construction of roads, rail

track beds, the manufacturing of concrete, concrete products, and asphalt

Lafarge works with strategic partners in the country to ensure aggregate supply are consistent and conform to BS-EN

12620

Fly ashFly ash is an extremely fine powder consisting of spherical particles less than 50 microns in size

Fly ash is one of the construction industry's most commonly used pozzolans

Cement

The Company has a wide range of cement solutions designed to meet all building and construction needs from small projects like

individual home buildings to major construction projects

Lafarge’s cement brands some of Nigeria’s preferred cement of all time

Over 55 years with impeccable pedigree

Annual Nigerian Industrial Standards Certificate for product quality from the Standards Organisation of Nigeria for over two decades

Brand range

10

Select

construction

projects

National Assembly Complex Abuja,

Third Mainland Bridge, Lagos

Cocoa House, Ibadan

ABTI American University, Yola

Tinapa Business and Leisure Resort, Akwa Ibom

Shoprite Mall, Enugu

Nigerian Cement Industry Overview

10

Nigeria as a key investment destination

US$457bn1

Nigeria’s 2016 GDP

18 yearsMedian age in Nigeria

77% of population

under

35 years

c.187mnNigeria’s population

Rural : urban mix

expected to shift from

52:48 in 2015 to

48:52 in 2021

2.5%Population growth to reach

212mn by 2021

One of Africa’s largest

economies

Economic recovery

expected in 2017, following

2016 recession; c.1%

growth expected in 2017

600%Nigeria’s middle class

growth from 2000 to

2014

Middle class

households expected

to grow from 4.1mn

to 11.7mn by 2030

Household

spending

expected to

grow by

US$26bn from 2015 –

2020

Sources: World Bank, EIU, AFDB Economic Outlook, National Bureau of Statistics, Standard Bank Research, McKinsey & Company, International Monetary Fund1 World Bank – Constant 2010 US$

11Cities with population

over 1 million people

Favourable Demography

and Economic Reforms

continue to position

Nigeria as a key

investment destination

Demography to drive

household demand

Urbanization and middle class

Young population

Support from key policy

reforms:

ERGP

Fiscal discipline

World Bank Housing Finance

Development Program

Improving Financial Stability

Improved currency liquidity

Successful Eurobond and

Diaspora Bond issuances

I&E Window for foreign

portfolio investors

Recovery of Stock Exchange

Agriculture, 22.97%

Industries, 23.31%

Services, 53.73%

A diversified economy with large

growth scope for industrials

US$2,178GDP Per Capita

Macro-economics at a glance

11

Strong fundamental in the

Long RunStrong improvement in

2017

Recovery expected in

2018-2019

• Population growth at

+2,6%p.a. (+5% for urban)

• Nominal GDP at +5% p.a.

(assumption oil price from

45-71$/bbl)

• Major housing gap (still

growing)

• Infrastructure gap (roads,

power, rail, …)

• Exit from recession but

mainly from Oil and Agric

sector. Construction and

Manufacturing still lagging

• Stabilization of FX rate but

strong Naira liquidity

squeeze

• In 2018-2019, recovery is

expected with real GDP

growth bouncing back

• IMF anticipate +1,9% in

2018 and 2019

• World Bank forecast +2,5%

Nigeria: medium-term macroeconomic outlook September 2017

TAC ECONOMICS - www.taceconomics.com

19

Macroeconomic outlook

In this chapter, we focus on the current economic situation and outlook taking into

consideration (1) the massive negative shock from much lower oil prices and (2) the

adjustment policy implemented so far, in particular since the 2016 currency depreciation

and subsequent economic recession.

1. Review of past episodes of lower oil prices

Nigerian GDP growth is closely related to the dynamics global oil prices. In order to assess

the macroeconomic outlook in the aftermaths of the oil price shock in 2014, past episodes

of oil price downfalls and their impact in terms of economic performances and of policies’

changes are reviewed. Indeed, several variables play a significant role in economic

recovery.

Exhibit 18

GDP and oil prices

Exhibit 19

GDP growth and oil prices

Source: TAC ECONOMICS

Box: Summary of Macroeconomic Adjustments for Past Oil Shocks in Nigeria

1982 Oil Crisis Oil price fell when President S. Shagari was in his third year of Presidency. He

was then ousted in a military coup in 1983 and President M. Buhari formed a

government. Within a year, his rule felt due to a coup and General I.B.

Babangida assumed Presidency from 1985 to 1993.

Meanwhile, the economy registered high inflation and unemployment level;

low foreign exchange reserves could barely cover one month of imports. It was

only as late as 1986 that IMF’s structural adjustment programs were

implemented and the economy slowly bounced back as oil prices too rose.

1999 Oil Crisis In 1999, O. Obasanjo came to power as the first democratically elected

President after the 6 years of General S. Abacha’s rule, considered one of the

most corrupt rulers of Nigerian history. The economy started to improve slowly

Nigerian Cement Industry: Demand

12

Main Drivers of

Cement Demand

in Nigeria:

Increasing urban

population (~50%)

growing twice as fast as

total population (~5%

p.a.)

Major housing gap of

17M houses still

increasing

$3,000bn of investment

required in infrastructure

Housing Deficit - Nigerian housing stock

per capita (units/1000)

-3

2

7

12

17

22

27

32

37

42

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Housing stock per capita Ideal

Infrastructure stock (%)

0%

20%

40%

60%

80%

100%

Nig

eri

a

Bra

zil

India

Chin

a

So

uth

Afr

ica

Indo

nesia

Po

lan

d

State of Infrastructure Benchmark

Source: National Planning CommissionSource: Chapel Hill Denham Research

Cement consumption per capita (kg) in 2015

125 150 180 210

430

600

970

400

560

0

200

400

600

800

1,000

1,200

Nigeria Senegal Algeria Libya GlobalAverage

Source: Global Cement Magazine, 2015

% of Construction in GDP

2010 2011 2012 2013 2014 2015

Non-construction Construction

Nigerian Cement Industry: Overview

13

GDP vs Cement

Growth

• Strong boom in

cement

consumption

between 2005-2013

(CAGR 9,7%)

• Cement market

stabilized around

21mt between

2013-2016

• Cement growth in

Nigeria at an avg

premium to GDP

growth of +2,5%

Source: Lafarge Africa Estimates Source: IMF, TAC, Economics Intelligence Unit, Lafarge Africa Estimates

Cement supply multiplied by 5 in 10 years

14

Cement nominal capacity (mn tonnes)

Source: BMI Research

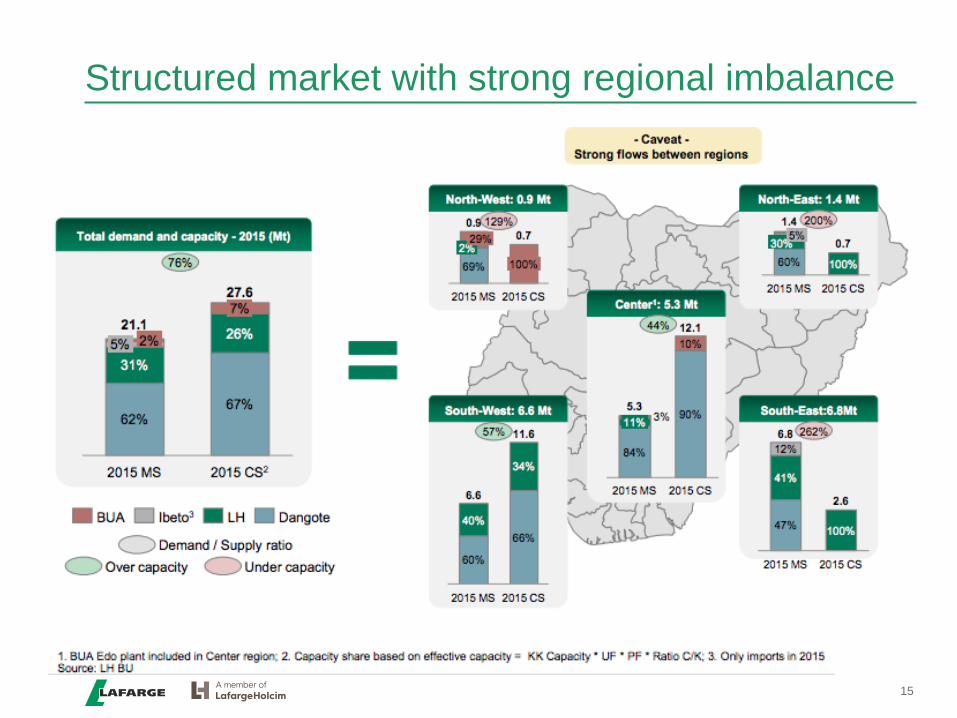

Structured market with strong regional imbalance

15

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

55.000

60.000

60

80

100

120

140

160

180

200

220

240

260

280

300

jan-14avr-14 jui-14 oct-14 jan-15avr-15 jui-15 oct-15 jan-16avr-16 jui-16 oct-16 jan-17avr-17 jui-17

LHCem

entN

etP

rice(N

GN/t)

LHCementNetPrice(CHF/t)

LHNetPrice(USD)@CBNRate LHNetPrice(USD)@AvgRate LHNetPrice(NGN)

Rational price changes and at the right level

16

BUA Sokoto 2

announcement

BUA Edo

Launch

Financial Overview

2016 Performance: Perfect Storm (1/2)

18

CAGR: 25.7% CAGR: 5.6%

Revenue (N’bn) and y-o-y growth Gross Profit (N’bn) and GP Margin

Source: Lafarge Africa PLC Audited Financials

88

206

261 267

220

41%

134%

27%

2%

-18%

-40%

0%

40%

80%

120%

160%

-

50

100

150

200

250

300

2012 2013 2014 2015 2016

Revenue % Growth

33

67

83 83

41

37%33%

32%

31%

19%

0%

40%

-

10

20

30

40

50

60

70

80

90

2012 2013 2014 2015 2016

Gross Profit Margin

EBITDA (N’bn) and EBITDA Margin PBT (N’bn) and PBT Margin

21

64

40

29

(23)

24%

31%

15% 11%

-10%

-40%

0%

40%

(40)

(20)

-

20

40

60

80

2012 2013 2014 2015 2016

PBT PBT Margin

32

56

69 68

26

36%

27%27% 25%

12%

0%

40%

-

10

20

30

40

50

60

70

80

2012 2013 2014 2015 2016

EBITA EBITA Margin

2016 Performance: Perfect Storm (2/2)

19Source: Lafarge Africa PLC Audited Financials

Total Debt (N’bn) Net Debt (N’bn)

Total Assets (N’bn) Shareholders Funds (N’bn)

37 28

121

148

128

2012 2013 2014 2015 2016

28

(6)

101

132

102

2012 2013 2014 2015 2016

152

298

416

452

502

2012 2013 2014 2015 2016

68

171 176 176

249

2012 2013 2014 2015 2016

Turnaround Plan in Nigeria to deliver our ambitions

20

Pricing

Key Indicators

Commercial

Performance

Industrial

Performance

Fuel

Flexibility

FX impact on

Cost

Re-

organisation

Turnaround Enablers

Impact

compared to

Q3 LY

+N16,3 Bn

Market share

sustained

~98% reliability

Stable industrial operations with all running kilns at

optimal levels, in spite of disruption in August in

Mfamosing

Strong contribution from coal, pet-coke and

alternative fuels

SAP implementation, Go live in Q1 2018

South West plants operations optimised

Reduced exposure to FX in our cost, mainly thanks to

higher reliance on coal & AF

N2,5 Bn

15%

improvement

in exposure

On track

Price adjustments in Q1 and April 2017 sustained

Product portfolio optimization on track

Route to market initiatives and Logistics Performance

improvement plan

Impact YTD

+N66 Bn

Market

share

improvement

N6,1 Bn

12,6%

improvement

in exposure

Unaudited Quarter 3 & 9 Months Results 2017

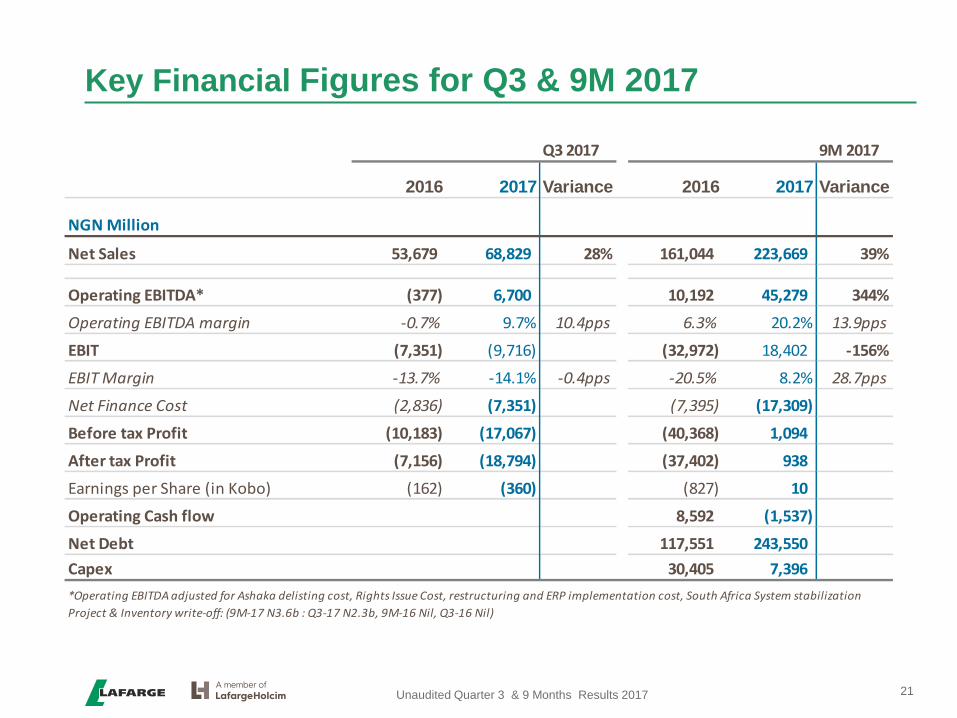

Key Financial Figures for Q3 & 9M 2017

21Unaudited Quarter 3 & 9 Months Results 2017

Q3 2017 9M 2017

2016 2017 Variance 2016 2017 Variance

NGN Million

Net Sales 53,679 68,829 28% 161,044 223,669 39%

Operating EBITDA* (377) 6,700 10,192 45,279 344%

Operating EBITDA margin -0.7% 9.7% 10.4pps 6.3% 20.2% 13.9pps

EBIT (7,351) (9,716) (32,972) 18,402 -156%

EBIT Margin -13.7% -14.1% -0.4pps -20.5% 8.2% 28.7pps

Net Finance Cost (2,836) (7,351) (7,395) (17,309)

Before tax Profit (10,183) (17,067) (40,368) 1,094

After tax Profit (7,156) (18,794) (37,402) 938

Earnings per Share (in Kobo) (162) (360) (827) 10

Operating Cash flow 8,592 (1,537)

Net Debt 117,551 243,550

Capex 30,405 7,396

*Operating EBITDA adjusted for Ashaka delisting cost, Rights Issue Cost, restructuring and ERP implementation cost, South Africa System stabilization

Project & Inventory write-off: (9M-17 N3.6b : Q3-17 N2.3b, 9M-16 Nil, Q3-16 Nil)

Nigeria Operations – Strong operational performance

22

Lafarge Africa Staff

Unaudited Quarter 3 & 9 Months Results 2017

Q3 2017 9M 2017

2016 2017 Variance 2016 2017 Variance

Cement (kt) 1,015 936 -7.8% 4,093 3,401 -16.9%

ReadyMix (km3) 41 41 0.0% 144 143 -0.7%

NGN Million

Net Sales 30,703 44,191 44% 107,406 155,611 45%

Operating EBITDA* (1,440) 12,198 8,619 49,873 479%

Operating EBITDA margin -4.7% 27.6% 32.3pps 8.0% 32.0%

EBIT (6,911) (2,331) (32,023) 26,779

EBIT Margin -22.5% -5.3% 17.2pps -29.8% 17.2%

Net Finance Cost** (2,697) (6,902) (6,660) (16,132)

Before tax Profit (9,608) (9,233) (38,683) 10,647

After tax Profit (7,276) (13,780) (36,796) 6,847

**S,G&A** inclusive of ERP Implementation cost, Ashaka delisting, Rights Issue and other resturcturing costs

**Net finance cost driven by finance charges on the shareholder loans & other borrowings

*Operating EBITDA adjusted for Ashaka delisting cost, Rights Issue Cost, restructuring and ERP implementation cost: (9M-17 N2.7b : Q3-17 N1.4b, 9M-16

Nil, Q3-16 Nil)

SG& A expenses higher than LY, due to SAP implementation cost & training of users across the business

Nigeria Operating EBITDA* 9M 2017 vs. LY

23

In N’ B

*Operating EBITDA adjusted for Ashaka delisting cost, Rights Issue Cost, restructuring and ERP implementation cost

Unaudited Quarter 3 & 9 Months Results 2017

8,6

49,9

-6,3

66,3

-17,1

-5,0 6,11,6 -4,3

OpEBITDA9M 2016

Volume Price Inflation andFX

Distribution Energy RawMaterials &

Others

Fixed costs OpEBITDA9M 2017

South Africa Operations

24

Lafarge Africa Staff

SA operations adversely impacted by:

Operational challenges at our Lichtenburg plant

On-going stabilization of SAP system implemented in January

Unaudited Quarter 3 & 9 Months Results 2017

Q3 2017 9M 2017

2016 2017 Variance 2016 2017 Variance

NGN Million

Net Sales 22,977 24,638 7% 53,638 68,058 27%

Operating EBITDA* 1,064 (5,498) 1,573 (4,593)

Operating EBITDA margin 4.6% -22.3% -26.9pps 2.9% -6.7% -9.7pps

EBIT (441) (7,385) (950) (8,377)

EBIT Margin -1.9% -30.0% -28.1pps -1.8% -12.3% -10.5pps

Net Finance Cost** (138) (449) (735) (1,176)

Before tax Profit (576) (7,834) (1,684) (9,553)

After tax Profit 120 (5,015) (606) (5,910)

*Operating EBITDA adjusted for ERP Stabilization project cost & inventory write-off: (9M-17 N0.88b : Q3-17 N0.88b, 9M-16 Nil, Q3-16 Nil)

Operating EBITDA to Net Income

25Unaudited Quarter 3 & 9 Months Results 2017

Q3 2017 9M 2017

NGN Million 2016 2017 Variance 2016 2017 Variance

Operating EBITDA* (377) 6,700 10,192 45,279

Depreciation & Amortisation (4,642) (4,802) (12,288) (16,174) -

One-Offs Adjustment - (2,280) - (3,614)

Current Operating income (5,019) (383) (2,096) 25,491 -

Net other operating income /(expenses) (2,332) (9,333) (30,876) (7,089) -

EBIT (7,351) (9,716) (32,972) 18,402

Net finance costs (2,836) (7,351) (7,395) (17,309) -

Share of net income from associates 3 - - -

Profit before Tax (10,183) (17,067) (40,368) 1,094 -

Income tax 3,027 (1,728) 2,965 (156) -

Profit after Tax (7,156) (18,794) (37,402) 938 -*Operating EBITDA adjusted for Ashaka delisting cost, Rights Issue Cost, restructuring and ERP implementation cost, South Africa System

stabilization Project & Inventory write-off: (9M-17 N3.6b : Q3-17 N2.3b, 9M-16 Nil, Q3-16 Nil)

Net Financial Debt Dec 2016 to September 2017

26

Net Debt (N’B)

South Africa debt included in Net debt position

Net debt position in Nigeria is N227 Billion (Net borrowing is largely 220mUSD converted from Quasiequity to loan)

Nigeria position is expected to improve to <N200 Billion by year-end after the Right Issue

Unaudited Quarter 3 & 9 Months Results 2017

**

* Excl Quasi Equity Instrument

Business Outlook

Cement market demand in Nigeria is expected to recover slightly in Q4 2017, to close theyear -14% to -12%, lower than LY :

Overall market rebound expected in Q1 2018

Sizeable infrastructure investments are foreseen to be initiated and executed from Q1 2018

Current low consumption per capita

Industrial & operational performance expected to remain stable in Nigeria

Stable pricing environment in Nigeria for Q4 2017 and Volume trend to reflect seasonality effect

On-going Logistic and Industrial Performance Improvement plan to deliver

Target EBITDA margin in mid-30s is expected to be achieved

Cement market in South Africa is expected to close the year lower, however:

Industrial stabilization team in place to ensure plant is operational

Cost containment programs in place

SAP stabilization process in place, with learning points established for other entities

Financial restructuring to be completed by year-end

Rights issue of N131,7 billion at a price of 42,5N/share to be concluded by Year-End

Commercial Paper of N25 billion to be completed beginning of November

Net Debt position for Nigeria to improve, to close the year at < N200 Billion

Expansion plans on track

Ashaka power plant on track to be delivered in Q4 2018

Outlook

28

Lafarge Africa: Key Investment Highlights

29

• The only vertically-integrated Cement Company in Nigeria

• Growing Aggregates & Concrete penetration

• Diversified Cement Product Line

Vertical Integration

• Strong track record of profitability with an annual CAGR of

33.5% from N8.5 billion in 2011 to N28.6 billion in 2015.

• Strong H1 2017 recovery with N19.7 billion net income from

operating loss in 2016 given the impact of naira devaluation

Consistent Profitability

Business reorganization to produce cost and revenue

synergies, driven by:

Optimising route to market,

Supplier Rationalisation,

Fixed-Cost Dilution from Mfamosing 2, etc.

Cost and Revenue Synergies

Regional diversification strengthening competitive position

and mitigating country-specific cycles

Regional Diversification

Leverages on the expertise of the Lafarge Holcim Group,

the Global Industry Leader, with access to:

World-Class R&D facilities (Lyon, France)

Global Best Practices, and

Wide product portfolio/knowledge

Access to Group Expertise

Resilient demand drivers for Building Materials including

the N117bn Marshall Plan for the North East, and FGN

infrastructure budgetary spend

Strong Industry Demand Drivers

Strong presence in Africa’s two largest economies –

Nigeria and South Africa

Strong Presence in Africa

Lafarge Africa is rated by two leading credit rating agencies:

A+ by Global Credit Ratings Co,

A+ by Agusto a& Co

Strong Credit Ratings

Rights Issue –Transaction Summary

Right Issue terms

31

Offering structure• Listing of new ordinary shares on the Nigerian Stock Exchange

• Issuer is Lafarge Africa Plc.

Offering size • N131,65bn through an offering of 3,098 million new ordinary shares

Subscription price • N42,5 per new shares - discount of 17,5% to closing price of 22nd Sept. 2017

Subscription ratio • Subscription ratio of 5 rights for every 9 shares held as at November 1, 2017

Use of proceeds

• Any convertible loan; shareholder loan or any other loan facility is due from the

company are authorized to apply for any shares subscribed for.

• The rights issue is being undertaken to de-leverage Lafarge Africa’s balance sheet,

finance working capital and the expansion of operations

Key dates• Qualification Date: November 1, 2017

• Rights trading and subscription period : November 24, 2017 to December 15, 2017

Issuing Houses• Lead Issuing House : Chapel Hill Denham Advisory Ltd

• Joint Issuing House : Standard Chartered Capital & Advisory Nigeria Ltd

Rights Issue Impact on Lafarge Africa

32

Rights Issue Impact

• Debt restructuring through the

rights issue reduces the impact

FX volatility has on Lafarge

Africa’s earnings

• Greater headroom to raise

additional capital to further

capitalize on the emerging

opportunities in Africa.

• Cashflow preservation-

reduction in interest expense

• Short term liquidity support

through financing working

capital

Deleveraged Balance Sheet

Headroom for Additional

Capital

Cashflow Preservation

Improved Liquidity

Lafarge Africa – Trading Performance

High

(N)Low (N) VWAP (N)

Share price

volatility

30 day 58 48.58 50.8054 2.35%

60 day 63 48.54 53.0098 2.10%

90 day 63 48.54 55.0245 2.62%

120 day 63 48.54 54.6579 2.48%

6 month 63 46.00 53.2889 2.54%

1 year 63 34.50 49.0804 2.82%

Market cap (N

billion) 307.469

RI Size (N billion) 131.7

RI size as % of

Market Cap 42.83%

Key statistics (as at 17 October 2017)

Description #

Share Price (N) 56.00

Shares outstanding ( billion) 5.49

Market cap (N ‘billions) 307.469

P/E 4.37

P/BV (2016) 3.99

Free float liquidity 35.76%

VWAP analysis

The volume

weighted average

price provides a

sense of trading

momentum on the

stock

The recent trading

performance of

Lafarge on the NSE

will be a core

benchmark for

shareholders

considering

participation in the

Rights Issue

30

35

40

45

50

55

60

65

0

20,000

40,000

60,000

80,000

100,000

120,000

Sep-16 Nov-16 Jan-17 Mar-17 May-17 Jul-17 Sep-17

Volume Traded Price 30 day VWAP 60 day VWAP

90 day VWAP 120 day VWAP 6 month VWAP 1 year VWAP

Lafarge Africa – Shareholder Options

5 for 9 rights issue

Investor holding 9 shares receives 5 rights

Sells the 5 rights

on the NSE to a

new investor No action taken

Accepts and

Subscribes to 5

new shares at the

rights price

New investor

subscribes for 5

new shares at

rights price

Unsubscribed

shares allotted to

shareholders who

applied for

additional rights

Issuer allots 5 new shares

• Subscription Ratio: Existing

shareholders receive subscription

rights based on their shareholding.

5 for 9 means shareholder receives

5 rights for every 9 shares they

own

• Oversubscription: When existing

shareholders apply for additional

rights above and beyond all the

shares available in the issue

• Partial subscription: When a

shareholder takes up some but not

all of their provisional rights

allocation

• Renunciation: When a shareholder

does not take up their rights

• Trade in Rights: When a

shareholder trades their right to

another investor

Shareholder

earns premium

on rights traded

LafargeHolcim

Group1

Ownership Structure Before & After Rights Issue

73% 27%

Subsidiary

Division

35

Lafarge Africa Plc

1Related entities before Ashaka Scheme of Arrangements ( Court Order Meeting October 23rd, 2017)2 Ownership will depend on subscription during the rights issue

Before Rights Issue

Minority

Shareholders

After Rights Issue

Egyptian

Cement

Holding BV.

100%

100%

100%86.51% 100%100%

LafargeHolcim

Group2

Minority

Shareholders

100%

72.4%

35%

Lafarge

ReadyMix

Nigeria Ltd

AshakaCem Atlas

Lafarge

South Africa

Holding

South

African

Operations

West

Operations

Nigeria

Cement

Holding BV.

UniCem

East & West

Operations

Lafarge

ReadyMix

Nigeria Ltd

AshakaCem

Lafarge

South Africa

Holding

72.4%

South

African

Operations

100% 100% 100%

Lafarge Africa Plc

CBI Ghana CBI Ghana35%

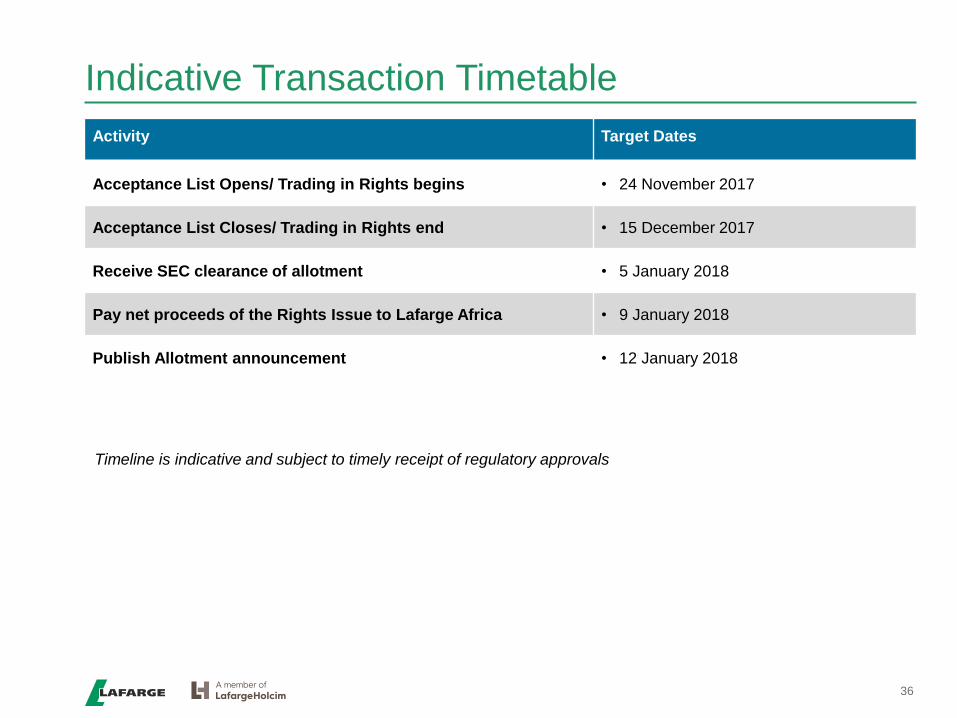

Indicative Transaction Timetable

36

Activity Target Dates

Acceptance List Opens/ Trading in Rights begins • 24 November 2017

Acceptance List Closes/ Trading in Rights end • 15 December 2017

Receive SEC clearance of allotment • 5 January 2018

Pay net proceeds of the Rights Issue to Lafarge Africa • 9 January 2018

Publish Allotment announcement • 12 January 2018

Timeline is indicative and subject to timely receipt of regulatory approvals

Thank You

Appendix

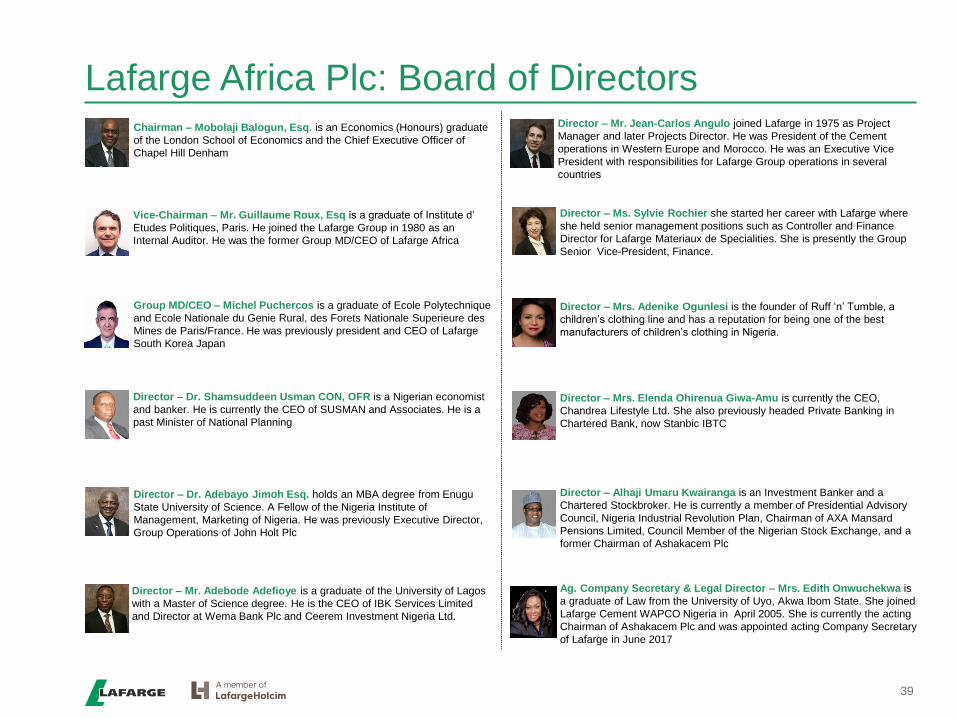

Lafarge Africa Plc: Board of DirectorsChairman – Mobolaji Balogun, Esq. is an Economics (Honours) graduate

of the London School of Economics and the Chief Executive Officer of

Chapel Hill Denham

Vice-Chairman – Mr. Guillaume Roux, Esq is a graduate of Institute d’

Etudes Politiques, Paris. He joined the Lafarge Group in 1980 as an

Internal Auditor. He was the former Group MD/CEO of Lafarge Africa

Director – Dr. Adebayo Jimoh Esq. holds an MBA degree from Enugu

State University of Science. A Fellow of the Nigeria Institute of

Management, Marketing of Nigeria. He was previously Executive Director,

Group Operations of John Holt Plc

Director – Ms. Sylvie Rochier she started her career with Lafarge where

she held senior management positions such as Controller and Finance

Director for Lafarge Materiaux de Specialities. She is presently the Group

Senior Vice-President, Finance.

Director – Mr. Jean-Carlos Angulo joined Lafarge in 1975 as Project

Manager and later Projects Director. He was President of the Cement

operations in Western Europe and Morocco. He was an Executive Vice

President with responsibilities for Lafarge Group operations in several

countries

Director – Mr. Adebode Adefioye is a graduate of the University of Lagos

with a Master of Science degree. He is the CEO of IBK Services Limited

and Director at Wema Bank Plc and Ceerem Investment Nigeria Ltd.

Director – Dr. Shamsuddeen Usman CON, OFR is a Nigerian economist

and banker. He is currently the CEO of SUSMAN and Associates. He is a

past Minister of National Planning

Director – Mrs. Adenike Ogunlesi is the founder of Ruff ‘n’ Tumble, a

children’s clothing line and has a reputation for being one of the best

manufacturers of children’s clothing in Nigeria.

Director – Mrs. Elenda Ohirenua Giwa-Amu is currently the CEO,

Chandrea Lifestyle Ltd. She also previously headed Private Banking in

Chartered Bank, now Stanbic IBTC

Director – Alhaji Umaru Kwairanga is an Investment Banker and a

Chartered Stockbroker. He is currently a member of Presidential Advisory

Council, Nigeria Industrial Revolution Plan, Chairman of AXA Mansard

Pensions Limited, Council Member of the Nigerian Stock Exchange, and a

former Chairman of Ashakacem Plc

Group MD/CEO – Michel Puchercos is a graduate of Ecole Polytechnique

and Ecole Nationale du Genie Rural, des Forets Nationale Superieure des

Mines de Paris/France. He was previously president and CEO of Lafarge

South Korea Japan

Ag. Company Secretary & Legal Director – Mrs. Edith Onwuchekwa is

a graduate of Law from the University of Uyo, Akwa Ibom State. She joined

Lafarge Cement WAPCO Nigeria in April 2005. She is currently the acting

Chairman of Ashakacem Plc and was appointed acting Company Secretary

of Lafarge in June 2017

39

Lafarge Africa Plc: Key Management

40

Bruno is a Mechanical Engineer graduate, a safety professional

and an alumnus of London Business School.

He joined Lafarge in the Middle East and Africa Regional office

in Cairo and held various senior management positions in

Egypt, France, Malawi, and NigeriaBruno Hounkpati

Logistics Director

Bruno holds a Business Engineering degree from Universite

Catholique de Louvain-la-Neuve in Belgium, and completed his

Master’s in Business Administration at Georgetown University,

specialising in Financial Risks Management

Mr. Bayet joined Lafarge in 2013 as a director in AshakaCem

Plc and added the role of Chief Financial Officer in September

2014

Bruno Bayet

Chief Financial Officer

Abdel-Ileh holds MBA from Georgetown University, Washington

D.C. and a post graduate degree in Financial Risks

Management with honours

He started his career as a Project Engineer with Lafarge in

1998 and has held various key positions in operations including

Production Manager and Plant Manager. In 2012, he became

the H&S Director, a role he held until 2015 when he was

appointed Director of Concrete Operations for Lafarge Morocco

Abdel-lleh Chouar

Industrial Director –

Cement

Michel Pucheros was appointed on 16th March 2016

He was the past MD at Bamburi Cement from September 2005 to 2009 and then appointed President and

CEO of Lafarge South Korea Japan OperationsMichel Puchercos

Group MD/CEO

He has over 35 years work experience spanning several

countries and several industries.

He joined Lafarge India and later moved into East Africa on

Technical Partnership support covering countries like Kenya,

Tanzania and Malawi.

Vipul joined Unicem in 2006 and worked as Marketing &

Technical Assistance capacity on the Excom of the BU, before

the eventual merger in 2015. He was appointed Acting

Marketing Director in May 2016

Vipul Agrawal

Marketing Director

He holds a Master of Business Administration from Heriot-Watt

University, Edinburgh and a Bachelor of Arts in Economics

from the University of Essex, Colchester.

Lolu joined Lafarge as the CFO for Lafarge WAPCO. Lolu Alade-Akinyemi

Procurement Director

She holds several degrees including M.Sc (Sociology) and

Masters in Business Administration

She joined Lafarge in December 2010 and prior to this was

General Manger, HRFidelia Osime

Organization and Human

Resource Director

She holds a Bachelor of Accounting degree from London

Guildhall and a Masters of Business Administration from the

Open University, Milton Keynes, UK

She was appointed as Director of Communications, Public

Affairs & Sustainable Development, Lafarge Africa Plc in

October 2016

Folashade Ambrose

Medebem

Communications, Public

Affairs & Sustainable

Development Director

Marlene has a BA, International Business and Marketing from

NEGOCIA ACI (Academie Commerciale Internationale) in Paris

as well as a General Management Progam from Harvard

Business School

She joined the organisation in January 2016 as Sales Director,

Key Accounts & IHB Precast Segment

Marlene Kiniffo-Zounon

Sales Director

41

Rabiu is a graduate of Accounting from Bayero University Kano

as well as General Management Program from Harvard

Business School

He joined Lafarge Nigeria in June 2014 as the Energy and

Power Director, and is currently the Managing Director Ashaka

Cem

Rabiu Umar

Managing Director,

Ashaka

Raymond joined LafargeHolcim Group Qatar- the Qatar

Readymix Group, as the Company Manager of both the quarry

company and the trading / transport company. Raymond was

then promoted to the role of Industrial Manager for the

aggregates business in South Africa.

Prior to this, he worked for Hanson Aggregates (now part of the

Heidelberg Cement Group) for 17 years in a range of line

management roles

Raymond Chambers

Head of Aggregates &

Concrete

Lafarge Africa Plc: Key Management (cont’d)

Edith is a graduate of Law 1997 (LLB)

She is a member of the Institute of Chartered Secretaries and

Administrators UK

She joined Lafarge WAPCO in 2005 and later became

Company Secretary/Legal Adviser of the Company in 2008

In 2011 moved to the Regional office in Cairo, Egypt as Legal

Counsel Sub-Saharan Africa and currently Lafarge Africa

General Counsel/Public Affairs Director

Edith Onwuchekwa

Legal & Public Affairs

Director

Helmut holds an Executive MBA (2006) from California State

University

He started his professional career as a military infantry officer

in Austria which included a number of command and staff

positions at home as well as overseas. Mr Korak resigned from

the armed forces in 2001 and became a diplomat appointed to

the Organization for Security and Co-operation in Europe

He joined Lafarge Africa in July 2016

Helmut Korak

Country Security

Manager

Graeme has a Mechanical Engineering degree from University

of Birmingham and an MBA from Manchester Business School.

He has over twenty years industrial experience in the power,

sugar and cement business. The last thirteen of these have

been spent in Asia and Africa in Cement.

In Lafarge, he has held manufacturing roles in plant line

management, head office and regional coordination.

Graeme Bride

Health and Safety

Director

42

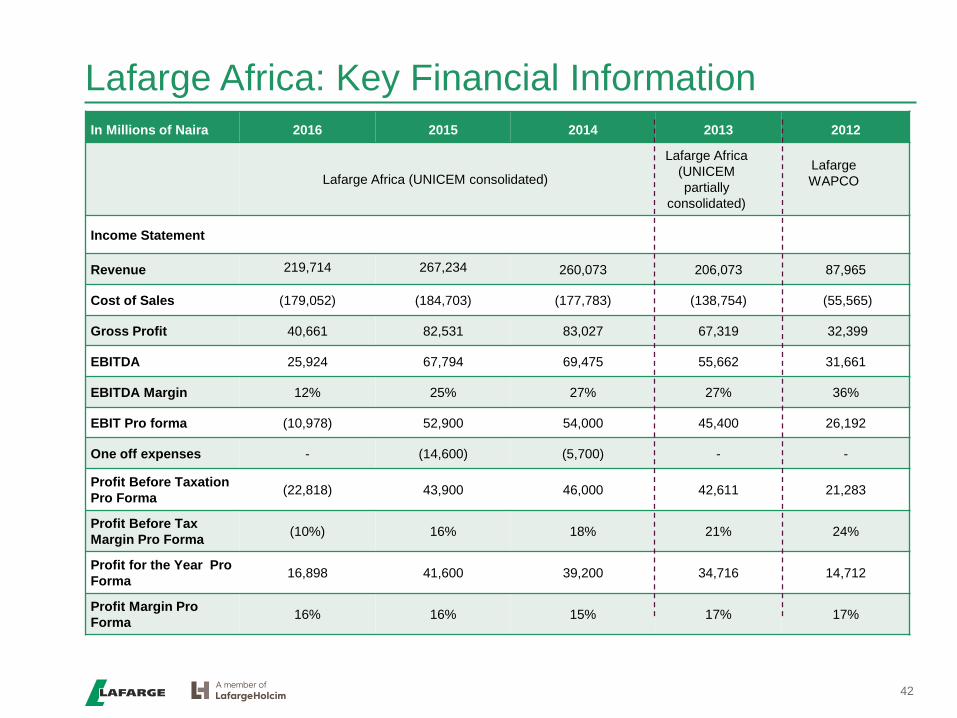

Lafarge Africa: Key Financial Information

In Millions of Naira 2016 2015 2014 2013 2012

Lafarge Africa (UNICEM consolidated)

Lafarge Africa

(UNICEM

partially

consolidated)

Lafarge

WAPCO

Income Statement

Revenue 219,714 267,234 260,073 206,073 87,965

Cost of Sales (179,052) (184,703) (177,783) (138,754) (55,565)

Gross Profit 40,661 82,531 83,027 67,319 32,399

EBITDA 25,924 67,794 69,475 55,662 31,661

EBITDA Margin 12% 25% 27% 27% 36%

EBIT Pro forma (10,978) 52,900 54,000 45,400 26,192

One off expenses - (14,600) (5,700) - -

Profit Before Taxation

Pro Forma(22,818) 43,900 46,000 42,611 21,283

Profit Before Tax

Margin Pro Forma(10%) 16% 18% 21% 24%

Profit for the Year Pro

Forma16,898 41,600 39,200 34,716 14,712

Profit Margin Pro

Forma16% 16% 15% 17% 17%

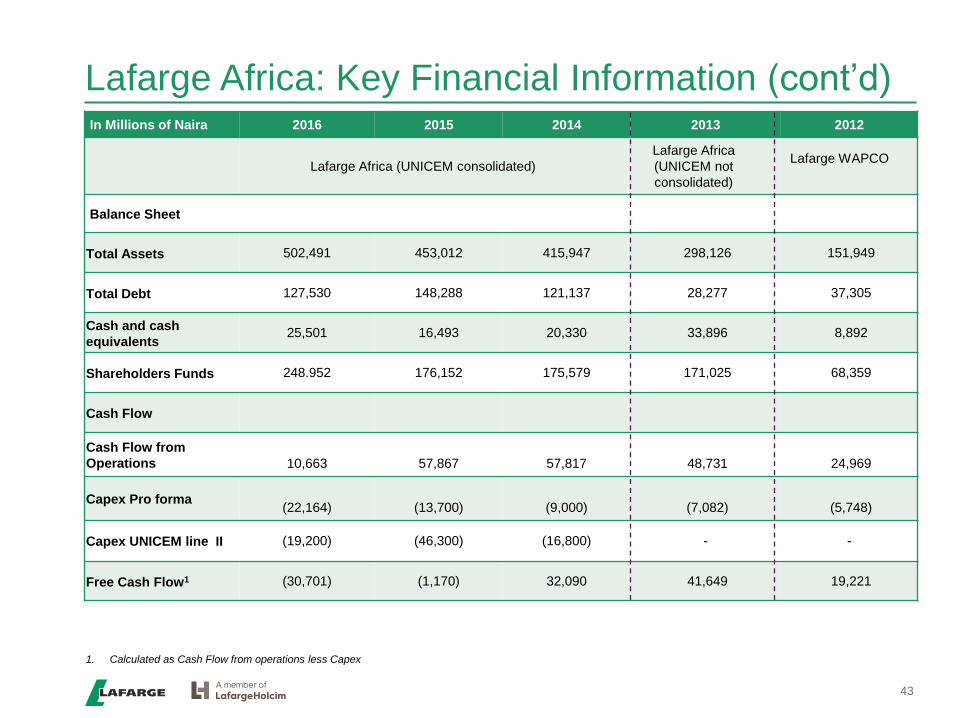

Lafarge Africa: Key Financial Information (cont’d)

43

In Millions of Naira 2016 2015 2014 2013 2012

Lafarge Africa (UNICEM consolidated)

Lafarge Africa

(UNICEM not

consolidated)

Lafarge WAPCO

Balance Sheet

Total Assets 502,491 453,012 415,947 298,126 151,949

Total Debt 127,530 148,288 121,137 28,277 37,305

Cash and cash

equivalents25,501 16,493 20,330 33,896 8,892

Shareholders Funds 248.952 176,152 175,579 171,025 68,359

Cash Flow

Cash Flow from

Operations 10,663 57,867 57,817 48,731 24,969

Capex Pro forma(22,164) (13,700) (9,000) (7,082) (5,748)

Capex UNICEM line II (19,200) (46,300) (16,800) - -

Free Cash Flow1 (30,701) (1,170) 32,090 41,649 19,221

1. Calculated as Cash Flow from operations less Capex

Contact Us

44

Kemi Awodein

Email:

Mobile: + 234 802 242 7729

Michelle Akinrinade

Email:

Mobile: +234 802 242 7750

Yemisi Deji - Bejide

Email:

Mobile: +234 802 3188 781

Yetunde Falore

Email:

Mobile: +234 703 480 9132

Wole Adeleke

Email: [email protected]

Mobile: + 234 802 3641894

Damilola Oni

Email: [email protected]

Mobile: +234 701 583 4293

27B Gerrard Road

Ikoyi

Lagos

Telephone: +234 1 271 3990

1st Floor, 45 Saka Tinubu Street

P.O. Box 74520

Victoria Island

Lagos

Telephone: +234 1 279 9563/4

142 Ahmadu Bello Way

Victoria Island

Lagos

Telephone: +234 1 236 8374