lanxess – energizing chemistry · 2018-04-26 · global lubricant precursors production (bu add)...

TRANSCRIPT

LANXESS – Energizing Chemistry

Business Profile 2018

Investor Relations, March 2018

2

The information included in this presentation is being provided for informational purposes only and does not constitute an offer to sell, or a solicitation of an offer to purchase, securities of LANXESS AG. No public market exists for the securities of LANXESS AG in the United States. This presentation contains certain forward-looking statements, including assumptions, opinions, expectations and views of the company or cited from third party sources. Various known and unknown risks, uncertainties and other factors could cause the actual results, financial position, development or performance of LANXESS AG to differ materially from the estimations expressed or implied herein. LANXESS AG does not guarantee that the assumptions underlying such forward-looking statements are free from errors nor does it accept any responsibility for the future accuracy of the opinions expressed in this presentation or the actual occurrence of the forecast developments. No representation or warranty (expressed or implied) is made as to, and no reliance should be placed on, any information, estimates, targets and opinions, contained herein, and no liability whatsoever is accepted as to any errors, omissions or misstatements contained herein, and accordingly, no representative of LANXESS AG or any of its affiliated companies or any of such person's officers, directors or employees accept any liability whatsoever arising directly or indirectly from the use of this document.

Safe harbor statement

3

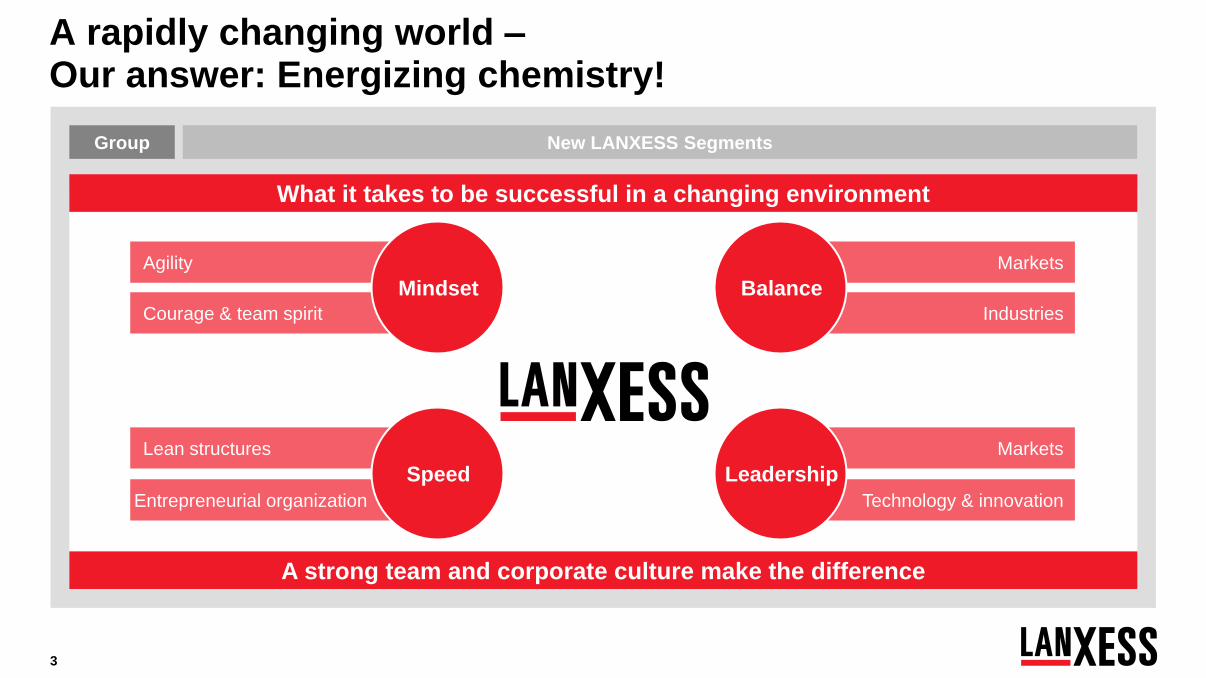

A rapidly changing world – Our answer: Energizing chemistry!

What it takes to be successful in a changing environment

A strong team and corporate culture make the difference

Markets

Industries

Balance

Markets

Technology & innovation

Leadership

Lean structures

Entrepreneurial organization

Speed

Courage & team spirit

Agility

Mindset

Group New LANXESS Segments

4

Our journey: Shaping New LANXESS – a story in three chapters

REPAIR

Realigning our business

IMPROVE

Strengthening our platform

ACCELERATE

Leveraging our strengths

2014 2017 ~2021

Group New LANXESS Segments

5

Phase 1 & 2 cost

improvements

become visible

All BUs with improved

organic return profile

Growth is picking up

Restructuring and change of strategy yields first positive results

LANXESS transformation starts to become visible

SGO

AII HPM

IPG

LEA

LPT

MPP

ADD

Key 2016 points

Substantial room for improvement left

EB

ITD

A C

AG

R 2

011-1

6

ROCE 2016

Chapter 3

Chapter 2

Chapter 1

Repair

Group New LANXESS Segments

6

Chemtura integration: €100 m of synergies by 2020

~€30 m

Corporate /

country costs

~€20 m

Marketing and sales

~€50 m

Production and

procurement set-up Organizational streamlining

Leveraging new regional strengths

Topline synergies provide additional comfort

€100 m synergy

breakdown:

Chapter 3

Chapter 2

Improve

Chapter 1

Group New LANXESS Segments

7

Organic investments will improve company ROCE

€100 m Debottleneckings, BU AII

€60 m Debottleneckings, BU

SGO, custom manufacturing

€60 m Greenfield, BU IPG

€50-100 m Debottleneckings, BU HPM,

global compounding hubs

€50 m Debottleneckings in remaining

BUs in Performance Chemicals

€50-100 m Investments in Specialty

Additives

Target: Increase ROCE to former levels

0

5

10

15

20

2011 2013 Q12017

% ROCE

~€400 m capex until 2020 at

ROCE of ~20%

Group New LANXESS Segments

Chapter 3

Chapter 2

Improve

Chapter 1

8

Chapter 2 proceeds with visible measures

Chapter 2

started

Restructuring of

chrome chemicals

activities (BU LEA)

Consolidation of

global lubricant

precursors production

(BU ADD)

Divestiture of non-

core chlorine

dioxide business

(BU MPP)

Acquisition of

Solvay’s U.S.

phosphorus additives

business (BU ADD)

Focused execution ongoing

Group New LANXESS Segments

9

Advanced Intermediates Specialty Additives

Performance Chemicals Engineering Materials

Growth capex: €100 m BU AII / €60 m Saltigo

Agro bounce back

New Saltigo Products in 2019

Improvement of Organometallics

performance

Portfolio & mix improvements:

Chemours integration /

Chlorine Dioxide divestment

Leather chemicals restructuring

BU IPG capacity expansion

BU HPM: Balanced capacity model with all

polyamide 6 used in compounds by 2020

Expansion of Urethane Systems business

in Europe

Chemtura integration and realization of

€100 m synergies

Lubricant additive price adjustment

& optimizing production set-up

Confirmation of 20% EBITDA margin target

LANXESS Value Drivers: Working towards our 2021 targets

Portfolio

improvement Strategy &

value chain

Chemtura

integration

& synergies

Organic

growth

Group New LANXESS Segments

10

Regionally balanced platform with no pronounced

dependencies

Diversified industrial platform mitigates impact from

any individual industry’s volatility

Market positions in every business at least among

leading players to keep or improve profitability level

Chapter 3: More balanced and stronger platform along three key dimensions

Regional platform Industrial platform Market positions

Chapter 3 will establish an even stronger platform Solid

growth

Chapter 3

Accelerate

Chapter 2

Chapter 1

Group New LANXESS Segments

Balancing the ground for further growth

11

LANXESS’ target 2021 – Leading, balanced and strongly cash generative

EBITDA pre

margin (group, Ø through

the cycle)

14-18%

Cash con-

version >60%

Underlying growth: Sustainable >GDP growth targeted

Cash conversion: (EBITDA pre – capex) / EBITDA pre

EBITDA

margin

volatility LOW

2-3%pts

Strategic and financial goals

Stable specialty chemical company with sound

cash generation and balanced portfolio

Increased footprint in growing regions

(North America and Asia)

Leading positions in core and attractive mid-

sized markets

Low dependency on individual markets, thus

less cyclical

Solid investment grade rating and significantly

reduced net financial debt

Group New LANXESS Segments

12

New LANXESS - A better end market exposure

LANXESS in 2015 New LANXESS ~2018

End market split by sales End market split by sales excl. ARLANXEO

More diversified and resilient

Automotive**

Chemicals

Agro

chemicals Consumer

Construction

E&E

Other*

* Including General Industry, Pharma, Tire; ** Including relevant parts of lubricants

Group New LANXESS Segments

13

Progressing very focused with clear priorities regarding capital allocation

Degree of specialization (driven

by technology and service)

Market

size

mid-sized bulk, commodity niches

New

LANXESS

in the

future

LANXESS

in 2014

New

LANXESS

in 2017

Organic growth (brown fields)

Portfolio

management

Dividend

Deleveraging

Deleveraging

Integration

(Chemtura)

Organic growth (brown fields)

Dividend

Portfolio

management

thereafter Until 2018

Integration & deleveraging Focused organic and external growth

Priorities Priorities

Group New LANXESS Segments

LANXESS – Energizing Chemistry

Advanced

Intermediates

Engineering

Materials

Performance

Chemicals

* Reporting structure since closing of Chemtura acquisition on 21 April 2017; ** ARLANXEO to be reported as discontinued operations from 1 April 2018 (with a restatement of 2017

and 2018 YTD figures) and reported as associate using the equity method from 1 April 2019

Specialty

Additives

Building a global

and resilient

intermediates

player

Creating a major

global additives

business

Building a

specialty division

Building an

integrated

engineering

plastics player

Leading position

in production and

marketing of

synthetic rubber

New LANXESS – a well diversified portfolio*

Europe No. 1-2 Top 3 position No. 1-4 in niches Leading position

ARLANXEO** joint venture

Globally No. 1-3

ARLANXEO**

Mark

et

positio

n

Group New LANXESS Segments and ARLANXEO

15

FY 2017: LANXESS delivers

0

2.000

4.000

6.000

8.000

10.000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

11,0%

9,2%

12,9% 13,1% 13,4%

8,9% 10,1%

11,2%

12,9%

13,3%

6%

8%

10%

12%

14%

0

200

400

600

800

1.000

1.200

1.400

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0

150

300

450

600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

[€ m] [€ m] [€ m]

All references to EBITDA are pre exceptionals; 1 Net of capitalized borrowing cost, projects financed by customers and finance lease

Sales 2008-2017

Sales by Region 2017

EBITDA (margin) 2008-2017

Sales by Segment 2017 EBITDA by Segment 2017

CAPEX1 2008-2017

Europe w/o

Germany

28%

Germany

15% Asia

28%

North America 19%

ARLANXEO

Performance

Chemicals

Advanced

Intermediates

ARLANXEO

Performance

Chemicals

Advanced

Intermediates

LatAm

9% Engineering

Materials Engineering

Materials

Group New LANXESS Segments and ARLANXEO

Specialty

Additives Specialty

Additives

16

EBITDA [€ million]

LANXESS – successful transformation and profitable growth

All references to EBITDA are pre exceptionals; 2012 restated due to IAS 19 (revised)

447 581 675 719 722

465

918 1.146 1.223

735 808 885 995

1.290

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Growth Crisis Transformation Repair Improve

Group New LANXESS Segments and ARLANXEO

17

FY 2017: Strong operational development in all regions in addition to portfolio effect of Chemtura acquisition

* Currency and portfolio adjusted

Group New LANXESS Segments and ARLANXEO

+14%

+15%

+21%

+32%

Regional development of sales

[€ million]

Operational

development*

EMEA (excl. Germany)

North America

Germany

Asia/Pacific

FY 2016 FY 2017

9,664

7,699 2,698

1,489

1,859

2,720

898

+40%

+22%

+8%

+11%

+11%

+11%

LatAm

EMEA (excl. Germany)

28 North

America

19

FY 2017 sales by region

[%]

2,039

1,292

1,326

2,254

788

LatAm

9

Asia/Pacific

28

Germany

16

18

KPIs are improving again

1 Pre exceptionals; 2 Net of exceptional charges and income, amortization of intangible assets and attributable tax effects as well as non-recurring

earnings effects of the U.S. tax reform

Group New LANXESS Segments and ARLANXEO

2013

735

1,731

2.4x

91%

1.73

…

…

…

…

…

… 2012

1,223

1,483

1.2x

64%

6.44

EBITDA1

Net financial debt

Net fin. debt / EBITDA1

Gearing

EPS pre [in €]

2

In € m

447

1,135

2.5x

101%

2004 2016

995

269

0.3x

7%

2.69

2011

1,146

1,515

1.3x

73%

2010

918

913

1.0x

52%

2017

1,290

2,252

1.8x

66%

4.14

808

1,336

1.7x

62%

2.22

2014

885

1,211

1.4x

52%

2.03

2015

19

The Advanced Intermediates segment comprises our businesses in intermediates and fine chemicals

Advanced Industrial Intermediates Saltigo

One of the world’s leading manufacturers of high-

quality industrial intermediates such as benzene-

and toluene-derivatives, amines, polyols, and

inorganics

Competitiveness through an integrated production

network with resilient businesses in the agro and

chemical industries

A leading supplier in the custom synthesis market,

providing state of the art technologies and services

to the agrochemicals and specialty chemicals

industries

Growth driven by strong foothold in agrochemical

industry

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

20

0

500

1.000

1.500

2.000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sales 2008-20171

Sales by BU 2017

13,0%

11,3%

16,6% 15,8%

16,2%

15,2%

16,7%

18,6% 18,7% 17,0%

8%

11%

13%

16%

18%

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

EBITDA (margin) 2008-20171

0

25

50

75

100

125

150

175

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Capex2 2008-20171

Advanced Intermediates – Intermediates form a very cost efficient production platform

[€ m] [€ m] [€ m]

All references to EBITDA are pre exceptionals; 1 Operating segments; pro forma restatements with new BU structure as of Jan 1st

2016; 2 Net of capitalized borrowing cost, projects financed by customers and finance lease

Characteristics

SGO

AII

Leading market positions and process technologies

Efficient and strong production platform

Highly diversified end markets

Attractive cash generation through technology leadership and efficient business

set-up

Growth slightly above GDP

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

21

Specialty Additives: World class player in several highly attractive additives niches

The portfolio of Rhein Chemie consists of:

customized active ingredient compounds

processing aids for the rubber, plastics and

colorants industries

specialty chemicals

The additives business unit comprises a broad

portfolio of:

phosphorus and brominated flame retardants

lubricant products

plastisizers and bromine performance products

Additives Rhein Chemie

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

22

0

500

1.000

1.500

2.000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sales 2008-20171

Sales by BU 2017

18,0%

16,6%

8%

11%

13%

16%

18%

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

EBITDA (margin) 2008-20171

0

25

50

75

100

125

150

175

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Capex2 2008-20171

Specialty Additives offers a higher than average profitability

[€ m] [€ m] [€ m]

Characteristics

ADD

RCH

Leading market positions and backward integrated bromine chain

Knowledge and technical service intensive products

Tailor-made, high value added solutions for highly diversified customer base

Global production footprint and sales platform

Growth above GDP

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

All references to EBITDA are pre exceptionals as of 21 April 2017 Chemtura’s additives business was consolidated; 1 Operating segments; pro forma restatements

with new BU structure as of Jan 1st 2016; 2 Net of capitalized borrowing cost, projects financed by customers and finance lease

23

Wide range of microbial

control products for

construction and paints,

beverages, industrial use

and wood protection

Performance Chemicals: Production of application-focused chemicals for a wide range of industries

A leading global supplier

of inorganic pigments for

the coloring of

construction materials,

coatings, plastics and for

technical applications

Supplier with a complete

range of products for

leather processing

(tanning agents,

preservatives, finishing

auxiliaries, dye products)

One of the leading global

producers of ion ex-

change resins, adsor-

bers, functional polymers

and reverse osmosis

membranes for the

treatment and purification

of water and other liquids

Material Protection Prod. Inorganic Pigments Leather Liquid Purification Technol.

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

24

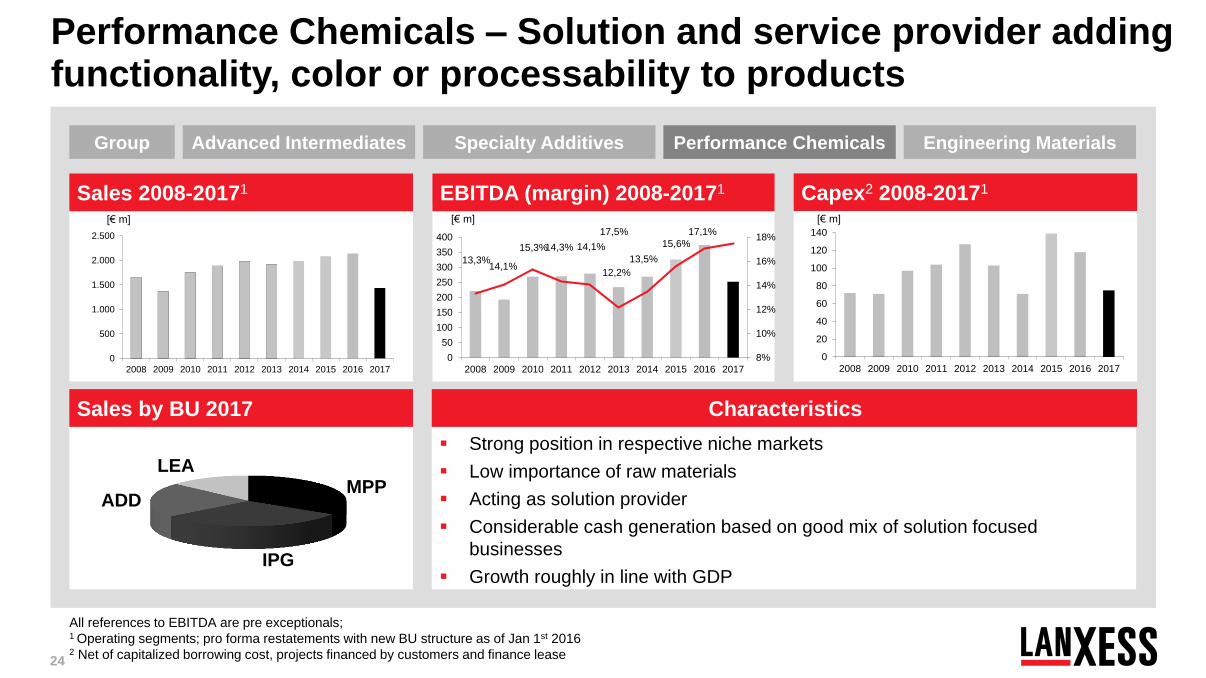

0

500

1.000

1.500

2.000

2.500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sales 2008-20171

Sales by BU 2017

EBITDA (margin) 2008-20171

Strong position in respective niche markets

Low importance of raw materials

Acting as solution provider

Considerable cash generation based on good mix of solution focused

businesses

Growth roughly in line with GDP

Characteristics

0

20

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Capex2 2008-20171

Performance Chemicals – Solution and service provider adding functionality, color or processability to products

[€ m] [€ m] [€ m]

All references to EBITDA are pre exceptionals; 1 Operating segments; pro forma restatements with new BU structure as of Jan 1st 2016 2 Net of capitalized borrowing cost, projects financed by customers and finance lease

MPP

IPG

ADD

LEA

13,3% 14,1%

15,3% 14,3% 14,1%

12,2%

13,5%

15,6%

17,1% 17,5%

8%

10%

12%

14%

16%

18%

0

50

100

150

200

250

300

350

400

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

25

Engineering Materials: Innovative plastic solutions for challenging industrial and automotive applications

One of the leading providers of a wide range of

engineering plastic compounds for the automotive,

electrical & electronic and other industries, benefiting

from the trend of replacing metal in structural

automotive parts

Globally market and technology leading position for

cast elastomer systems. Products are highly

customer specific offering abrasion resistance with

various degrees of hardness

High Performance Materials Urethane Systems

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

26

0

400

800

1.200

2015 2016 2017

Sales 2015-2017

Sales by BU 2017

10,2%

15,1% 16,0%

6%

8%

10%

12%

14%

16%

18%

0

50

100

150

200

250

2015 2016 2017

EBITDA (margin) 2015-2017

Customer and market proximity; backward integrated into strategic raw materials

Global production network

Among leading providers of engineering plastics

Focus on high-tech compounds to meet global trend in lightweight constructions

Growth for engineering plastics in automotive applications²

0

10

20

30

40

50

60

70

80

2015 2016 2017

Capex1 2015-2017

High Performance Materials: Leading supplier of light-weight solutions with integrated engineering capability

[€ m] [€ m] [€ m]

All references to EBITDA are pre exceptionals; 1 Net of capitalized borrowing cost, projects financed by customers and finance lease; 2 Source: AMI Plastics,

IHS Chemicals, LMC Automotive, PCI Nylon, Plastics Europe, LANXESS volume estimates / demand growth through substitution (from metal to plastics in cars)

HPM

URE

Characteristics

Group Advanced Intermediates Specialty Additives Performance Chemicals Engineering Materials

27

A leading global supplier of synthetic rubbers for a

wide range of technical applications (e.g. seals,

hoses, profiles, cable sheathing, special films and

adhesives)

A leading manufacturer of high quality synthetic

rubbers which are primarily used in inner liners,

treads and sidewalls of modern, fuel-efficient tires

as well as non-tire applications

ARLANXEO

High Performance Elastomers Tire & Specialty Rubbers

Group Advanced Intermediates Performance Chemicals High Perf. Materials ARLANXEO

28

0

500

1.000

1.500

2.000

2.500

3.000

3.500

2015 2016 2017

Sales 2015-2017

Sales by BU 2017

13,7% 13,8% 11,9%

6%

9%

12%

15%

18%

0

150

300

450

2015 2016 2017

EBITDA (margin) 2015-2017

Leading market positions with strong and diversified portfolio

Global production network

Broadest synthetic rubber platform with competitive advantage for future

development

Growth slightly above GDP

0

20

40

60

80

100

120

140

160

2015 2016 2017

Capex1 2015-2017

ARLANXEO: Newly formed joint venture for synthetic rubber between Saudi Aramco and LANXESS

[€ m] [€ m] [€ m]

All references to EBITDA are pre exceptionals; 1 Net of capitalized borrowing cost, projects financed by customers and finance lease; As of Q2 2016 the BUs

TSR and HPE formed ARLANXEO; They were reported in the Performance Polymer segment before

TSR

HPE

Characteristics

Group Advanced Intermediates Performance Chemicals High Perf. Materials ARLANXEO

29

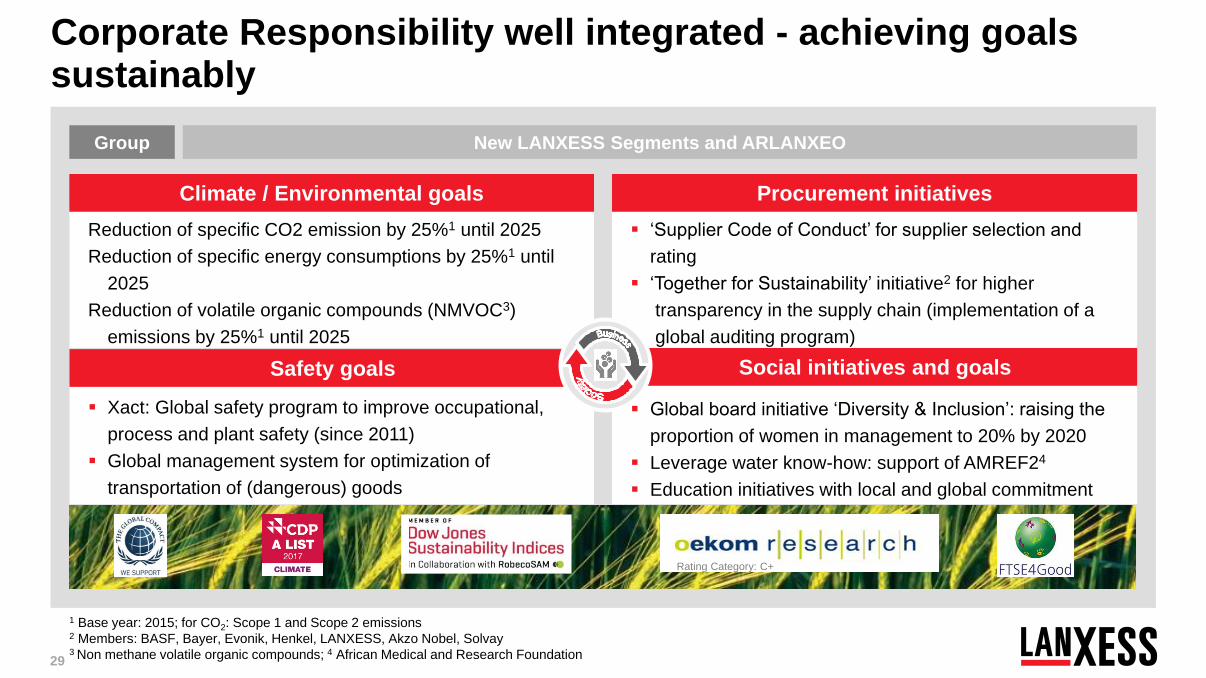

Xact: Global safety program to improve occupational,

process and plant safety (since 2011)

Global management system for optimization of

transportation of (dangerous) goods

Safety goals

Reduction of specific CO2 emission by 25%1 until 2025

Reduction of specific energy consumptions by 25%1 until

2025

Reduction of volatile organic compounds (NMVOC3)

emissions by 25%1 until 2025

‘Supplier Code of Conduct’ for supplier selection and

rating

‘Together for Sustainability’ initiative2 for higher

transparency in the supply chain (implementation of a

global auditing program)

Corporate Responsibility well integrated - achieving goals sustainably

Climate / Environmental goals Procurement initiatives

Rating Category: C+

Global board initiative ‘Diversity & Inclusion’: raising the

proportion of women in management to 20% by 2020

Leverage water know-how: support of AMREF24

Education initiatives with local and global commitment

1 Base year: 2015; for CO2: Scope 1 and Scope 2 emissions 2 Members: BASF, Bayer, Evonik, Henkel, LANXESS, Akzo Nobel, Solvay 3 Non methane volatile organic compounds; 4 African Medical and Research Foundation

Group New LANXESS Segments and ARLANXEO

Social initiatives and goals

30

AII Advanced Industrial Intermediates

SGO Saltigo

IPG Inorganic Pigments

LEA Leather

MPP Material Protection Products

LPT Liquid Purification Technologies

Abbreviations

HPM High Performance Materials

URE Urethane Systems

Engineering Materials

Performance Chemicals

Advanced Intermediates

TSR Tire & Specialty Rubbers

HPE High Performance Elastomers

ARLANXEO*

ADD Additives

RCH Rhein Chemie

Specialty Additives

* ARLANXEO will be accounted for as discontinued operations from April 1, 2018 onwards

31

Head of Treasury & Investor Relations

Tel. : +49-221 8885 9611

Fax. : +49-221 8885 5400

Mobile : +49-175 30 49611

Email : [email protected]

Assistant to Oliver Stratmann

Tel. : +49-221 8885 9834

Fax. : +49-221 8885 4944

Mobile : +49-151 74613059

Email : [email protected]

Institutional Investors / Analysts / AGM

Tel. : +49-221 8885 1035

Mobile : +49-151 7461 2789

Email : [email protected]

Head of Investor Relations

Tel. : +49-221 8885 3494

Mobile : +49-175 30 23494

Email : [email protected]

Visit the IR website

Institutional Investors / Analysts

Tel. : +49-221 8885 7344

Mobile : +49-151 7461 2913

Email : [email protected]

Institutional Investors / Analysts

Tel. : +49-221 8885 5249

Mobile : +49-151 7461 2969

Email : [email protected]

Private Investors / AGM

Tel. : +49-221 8885 1989 Mobile : +49-151 7461 2615 Email : [email protected]

Contact details Investor Relations

Oliver Stratmann Katharina Forster

Andre Simon

Annika Klaus

Janna Günther

Jens Ussler

Thorsten Zimmermann