larsenandtoubro-130914065740-phpapp01

TRANSCRIPT

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 1/64

PRESENTED BY :

• ROHIT VERMA 111268

• SHUBHI JAIN 111338

• SHUBHAM DWIVEDEE 111339

• ANKIT SAHA 1113401

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 2/64

2

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 3/64

3

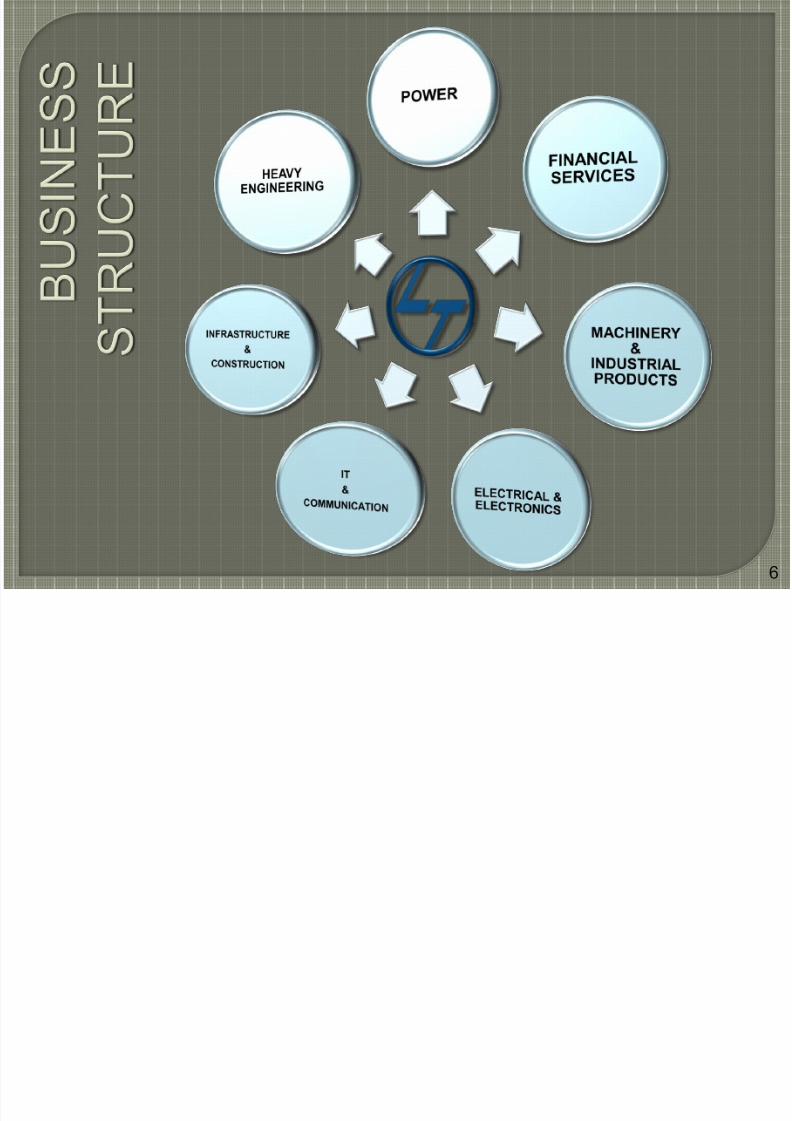

Larsen & Toubro Limited (L&T) is amongst one of the India’s largest technology,

engineering construction and manufacturing conglomerate.

• L&T is considered to be the "bellwether of India's engineering sector“, and wasrecognized as the company of the year in 2010.

• L&T’s business structure has a dominant presence in India's infrastructure,power, hydrocarbon, machinery, shipbuilding and railwaysectors.

• L&T has an international presence. The company's businesses are supported by

a wide marketing and distribution network, and have established a reputation forstrong customer support.

• With more than a seven decades of dedicated customer-focused service andcontinuous quest for world class quality have established them as the leader of theE&C sector in India.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 4/64

4

The evolution of L&T into the country's largest engineering and constructionorganization is among the most remarkable success stories in Indian industry.

• L&T was founded in Bombay (Mumbai) in 1938 by two Danish engineers,Henning Holck-Larsen and Soren Kristian Toubro. Both of them were strongly

committed to developing India's engineering capabilities to meet thedemands of industry.

• In the year 1950, L&T became a Public Company with a paid-up capital of Rs.2million and a sales turnover of Rs.10.9 million that year. And now, In 2012 the company generated a total revenue of US $13.5 billion.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 5/64

5

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 6/64

6

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 7/647

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 8/648

RATIO ANALYSIS

LIQUIDITYRATIOS

LEVERAGERATIOS

TURNOVERRATIOS

PROFITABILITYRATIOS

VALUATIONRATIOS

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 9/64

Current Ratio

Quick Ratio

Can they meettheir currentobligations??

9

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 10/64

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2006 2007 2008 2009 2010 2011

CR

CR

It is a measure of the firm’s short term solvency i.e., it indicates the availabilityof current assets in rupees for every one rupee of current liability. It representsa margin of safety for the creditors of the firm.

CR

(times)

YEAR

1.10 2006

1.03 2007

0.92 2008

1.18 2009

1.02 2010

1.02 2011 10

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 11/64

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

2006 2007 2008 2009 2010 2011

QR

QR

Quick Ratio a.k.a. Acid-Test Ratio establishes relationship between quickassets and current liabilities, where quick assets refer to those assets whichcan be converted into cash immediately or reasonably soon without loss ofvalue.

QR

(times)

YEAR

0.79 2006

0.71 2007

0.61 2008

0.86 2009

0.69 2010

0.60 2011 11

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 12/6412

Liquidity refers to the readiness of assets to be converted to cash. They givea general idea of the firm's ability to pay its short-term debts.

Ideally the current ratio should be greater than 1.5. Though there can beexceptions, some good companies can have less than 1 or even a negativecurrent ratio when they receive money faster from their customers than theyhave to pay to their vendors.

So, we can say that L&T will not be able to meet its current obligations as long

as they do not use their inventories efficiently as its inventories form a large partof their current assets.

ANALYSIS: (LIQUDITY RATIOS)

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 13/64

Financial

LeverageRatios

• Debt Ratio• Debt-Equity Ratio

• Debt-Asset Ratio

CoverageRatios

• Interest CoverageRatio

13

What debt-equity mix dothey prefer ??

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 14/64

DR

(times)

YEAR

15.88 2006

17.91 2007

22.63 200825.67 2009

23.53 2010

19.33 2011 1414

0.00

5.00

10.00

15.00

20.00

25.00

30.00

2006 2007 2008 2009 2010 2011

DR

DR

It tells us about the proportion of the interest-bearing debt in the capitalstructure of the firm. Total debt will include short & long-term borrowings fromfinancial institutions, debentures/bonds, deferred payment arrangements , bankborrowings, public deposits, etc.

DEBT RATIO

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 15/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 16/64

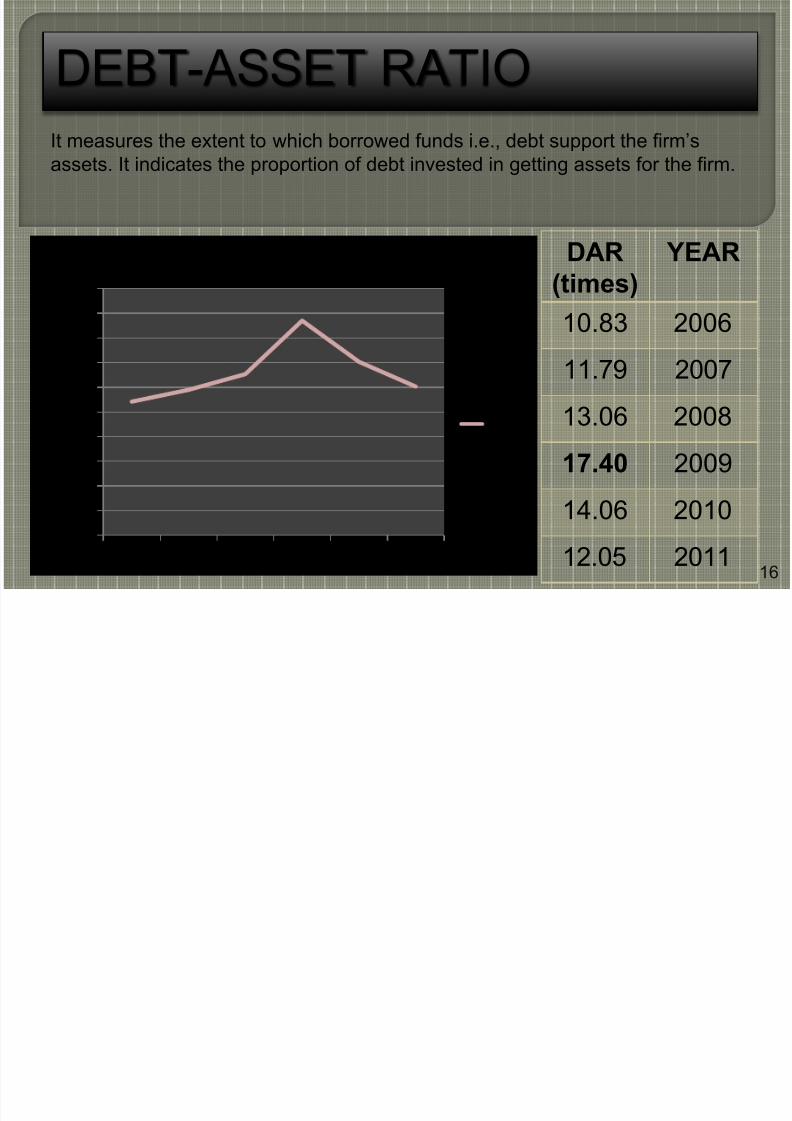

DAR

(times)

YEAR

10.83 2006

11.79 2007

13.06 2008

17.40 2009

14.06 2010

12.05 2011 16

0.00

2.00

4.00

6.00

8.0010.00

12.00

14.00

16.00

18.00

20.00

2006 2007 2008 2009 2010 2011

DAR

DAR

DEBT-ASSET RATIO

It measures the extent to which borrowed funds i.e., debt support the firm’sassets. It indicates the proportion of debt invested in getting assets for the firm.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 17/64

17

ANALYSIS: (FINANCIAL LEVERAGES)

Financial leverage indicates the reliability of a business on its debts in order tooperate.

Lower value of debt ratio is favorable and a higher value indicates that higherportion of company's assets are claimed by it creditors which means higher riskin operation.

In case debt ratio is less than 0.5.This indicates that company’s assets are

financed through equity and less of debt, lower values of debt-to-equity ratio are

favorable indicating less risk. Thus, the company is less riskier.

L&T has low proportion of debt in its capital structure and thus the assetssupported by them and cost of debt against a rupee of equity show a similartrend.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 18/64

ICR

(times)

YEAR

12.47 2006

24.29 2007

28.63 200812.94 2009

13.47 2010

10.90 2011 18

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2006 2007 2008 2009 2010 2011

ICR

ICR

INTEREST COVERAGE

RATIOICR a.k.a. times-interest-earned is used to test the firm’s debt servicing

capacity. It shows the number of times the interest charges are covered byfunds that are ordinarily available for their payment.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 19/64

19

ANALYSIS: (COVERAGE RATIOS)

The higher the coverage ratios the less a company is burdened by debt. If acompany has no debt or the loan interest is being paid by interest income frominvestments or other activities the ratio is zero which of course is excellent.

A negative ratio tells us that the company cannot even pay its interest on loansfrom its operating income, stay far away from such companies.

In case of L&T the ratios are comparatively moderate.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 20/64

Inventory Turnover Ratio

Debtors Turnover Ratio

Average Collection Period Asset Turnover Ratios

• Days of Inventory Holding

• Total Assets Turnover Ratio20

What do theturnoversdepict??

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 21/64

ITR

(times)

YEAR

6.80 2006

5.99 2007

5.88 20085.92 2009

4.84 2010

3.54 2011 21

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.008.00

2006 2007 2008 2009 2010 2011

ITR

ITR

INVENTORY TURNOVER

RATIOIt indicates the efficiency of the firm in producing and selling its product. Itshows how rapidly the inventory is turning into receivables through sales.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 22/64

DIH

(days)

YEAR

53 2006

60 2007

61 200861 2009

74 2010

102 2011 22

0.00

10.00

20.00

30.0040.00

50.00

60.00

70.00

80.00

2006 2007 2008 2009 2010 2011

DIH

DIH

Days of Inventory Holding

It gives us an idea of the stock management of the company.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 23/64

DTR

(times)

YEAR

2.98 2006

2.61 2007

1.96 20081.11 2009

1.05 2010

0.93 2011 23

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2006 2007 2008 2009 2010 2011

DTR

DTR

DEBTORS TURNOVER

RATIOThe debtors turnover ratio is the is the relationship between net sales andaverage debtors. It is also called account receivable turnover ratio because wedebtor and bill receivables' total is used for calculation.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 24/64

ACP

(months)

YEAR

4.02 2006

4.59 2007

6.11 200810.84 2009

11.38 2010

12.91 2011 24

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2006 2007 2008 2009 2010 2011

ACP

ACP

AVERAGE COLLECTION

PERIODThe average collection period is the ratio of the number of days in a period andthe inventory turnover ratio.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 25/64

ATR

(times)

YEAR

1.12 2006

0.85 2007

0.55 20080.40 2009

0.31 2010

0.25 2011 25

0.00

0.20

0.40

0.60

0.80

1.00

1.20

2006 2007 2008 2009 2010 2011

ATR

ATR

ASSET TURNOVER RATIO

The asset turnover ratio is the measure of the ability of a company or a firm touse its assets efficiently in order to generate sales.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 26/64

26

ANALYSIS: (TURNOVER RATIOS)

A low turnover implies poor sales and, therefore, excess inventory. A highratio implies either strong sales or ineffective buying. From the year 2006 to2008 the ratio is high but for the latter part the ratio is low.

Debtors turnover indicates the velocity of debt collection of a firm.Lower debtor turnover ratio is bad because it means, slowly, money isbeing collected and liquidity position will become weak.

Companies with low profit margins tend to have high asset turnover, whilethose with high profit margins have low asset turnover. Thus, the companyhas high profit margins.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 27/64

• Gross Profit Margin Ratio• Net Profit Margin Ratio• Expenses Ratio

ProfitMarginRatios

• Return on Investment

• Return on Equity• Earnings per Share• Dividend per Share• Dividend-Payout Ratio

Rate ofReturnRatios

• Operating Expenses Ratio

27

How are theprofitsshaping up?

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 28/64

GPM

(%)

YEAR

9.20 2006

11.15 2007

12.56 200813.56 2009

15.76 2010

13.13 2011 28

0.00

2.00

4.00

6.008.00

10.00

12.00

14.00

16.00

18.00

2006 2007 2008 2009 2010 2011

GPM

GPM

GROSS PROFIT MARGIN

RATIOThe gross profit margin reflects the efficiency with which managementproduces each unit of product. It implies how cost efficiently a firm can produceits goods.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 29/64

NPM

(%)

YEAR

6.73 2006

7.80 2007

8.59 200810.13 2009

11.70 2010

8.93 2011 29

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2006 2007 2008 2009 2010 2011

NPM

NPM

NET PROFIT MARGIN RATIO

It establishes a relationship between net profit and sales and indicates the firmsefficiency in manufacturing, administering and selling its products.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 30/64

OER

(%)

YEAR

90.44 2006

89.98 2007

91.21 200887.88 2009

85.57 2010

87.70 201130

82.0083.0084.0085.0086.00

87.0088.0089.0090.0091.0092.00

2006 2007 2008 2009 2010 2011

OER

OER

OPERATING EXPENSES

RATIOIt indicates the operating expenses incurred by the company in its productionand working.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 31/64

31

ANALYSIS: (PROFIT MARGIN RATIOS)

Since the profitability ratios are high, it indicates that the company has anefficient management.

It also indicates that the cost of goods sold remains constant and there is anincrease in the proportionate volume of higher margin items.

The company has increasing profits till the year 2010 after which there is aslight depreciation which can be a result of the global economic slowdown.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 32/64

32

ROI

ROTA RONA

Return on Investment

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 33/64

ROTA

(%)

YEAR

7.54 2006

7.95 2007

7.92 20089.24 2009

9.04 2010

6.66 2011 33

0.00

2.00

4.00

6.00

8.00

10.00

2006 2007 2008 2009 2010 2011

ROTA

ROTA

Return on Total Assets

ROTA tells us about the how effectively the investment in the firm i.e., pool offunds supplied by shareholders and lenders is being used in terms of totalassets.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 34/64

RONA

(%)

YEAR

76.73 2006

79.97 2007

74.53 200884.62 2009

79.67 2010

59.56 2011 34

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

2006 2007 2008 2009 2010 2011

RONA

RONA

Return on Net Assets

RONA tells us about the how effectively the investment in the firm i.e., pool offunds supplied by shareholders and lenders is being used in terms of netassets.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 35/64

ROE

(%)

YEAR

22.04 2006

24.47 2007

22.81 200828.00 2009

23.92 2010

18.13 2011 35

0.00

5.00

10.00

15.00

20.00

25.00

30.00

2006 2007 2008 2009 2010 2011

ROE

ROE

Return on Equity

ROE indicates how well the firm has used the resources of owners. It iscalculated to see the profitability of owner’s investment in the firm.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 36/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 37/64

EPS

(Rs.)

YEAR

7.36 2006

4.95 2007

7.43 20085.94 2009

7.27 2010

6.50 2011 37

0.00

1.00

2.00

3.004.00

5.00

6.00

7.008.00

2006 2007 2008 2009 2010 2011

EPS

EPS

Earnings Per Share

This is the amount of income that the common stockholders are entitled toreceive (per share of stock owned). This income may be paid out in theform of dividends, retained and reinvested by the company, or acombination of both.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 38/64

DPS

(Rs.)

YEAR

1.17 2006

0.66 2007

0.63 20080.57 2009

0.64 2010

0.65 2011 38

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2006 2007 2008 2009 2010 2011

DPS

DPS

Dividend Per Share

Dividend per share (DPS) is the total dividends paid out over an entire year(including interim dividends but not including special dividends) divided bythe number of outstanding ordinary shares issued.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 39/64

DPR YEAR

0.16 2006

0.13 2007

0.09 2008

0.10 2009

0.09 2010

0.19 2011 39

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.180.20

2006 2007 2008 2009 2010 2011

DPR

DPR

Dividend-Payout Ratio

The percentage of earnings paid to shareholders in dividends.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 40/64

40

ANALYSIS: (EPS, DPS, D/P)

Having a growing in the dividend per share can be a sign that thecompany's management believes that the growth can be sustained.

More mature companies tend to have a higher payout ratio. A stabledividend payout ratio indicates a solid dividend policy by the company's

board of directors. Thus, the company is stable.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 41/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 42/64

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2006 2007 2008 2009 2010 2011

PER

PER

PER

(times)

YEAR

4.54 2006

4.09 2007

4.39 20083.57 2009

4.18 2010

5.51 2011 42

The P/E ratio reflects the price currently being paid by the marketfor each rupee of currently reported EPS. It is widely used by thesecurity analysts to analyze the firm’s performance as expected by the

investors.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 43/64

43

ANALYSIS: (VALUATION RATIOS)

Valuation ratio measures different ways of looking at the relative value of acompany's stock.

A high P/E ratio may signify that the company is overvalued, which means thateventually market forces will drive the price down.

On the other hand, a high P/E could indicate great earning power and thepossibility that profitability will increase over time, justifying the higher price.Thus, the company has high earning power.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 44/64

44

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 45/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 46/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 47/64

47

YEAR 2006 2007 2008 2009 2010 2011

Net Worth 100 124.88 207.59 270.98 398.54 475.59

Borrowings 100 142.94 246.56 451.03 467.87 492.66

Current Liabilities

&

Provisions

100 134.56 197.35 256.02 321.25 419.86

Deferred Tax Liability 100 97.66 116.46 207.43 185.55 262.04

Total Liabilities 100 131.35 204.38 280.70 360.38 442.89

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 48/64

48

YEAR 2006 2007 2008 2009 2010 2011

Sales 100 118.54 166.33 232.65 252.95 293.39

EBDITA 100 138.76 215.74 330.43 418.04 433.48

EBDTA 100 144.65 226.36 331.48 420.74 428.03

EBT 100 144.92 229.95 336.89 426.13 420.56

PAT 100 138.62 214.84 344.17 432.50 391.19

EPS 100 67.26 101.01 80.77 98.71 88.31

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 49/64

49

FINDINGS:

Index analysis of a company's financial statements is important to be able todetermine whether a company is growing or shrinking.

The positive inter-annual trends in the income statement components, bothincome and expense, have lifted the company's profit margins.

In the case of L&T, it experienced a major increase in sales for the periodreviewed and was also able to control the expense side of its business. That'sa sign of a very efficient management.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 50/64

50

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 51/64

51

Financial statement analysis displays all items as percentages of acommon base figure.

This type of financial statement allows for easy analysis betweencompanies or between time periods of a company.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 52/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 53/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 54/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 55/64

55

FINDINGS:

Formatting financial statements in this way reduces the bias that can occur whenanalyzing companies of differing sizes.

It also allows for the analysis of a company over various time periods, revealing,for example, what percentage of sales is cost of goods sold and how that valuehas changed over time.

In this case, the sales had been considerably good till 2010 and then from theyear 2010 to 2011 the income or the earnings of the company decreased.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 56/64

56

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 57/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 58/64

58

• In spite of L&T’s global presence, it is not verypopular in the international market.

• The customer service staff still needs training

specially in the delivery and help desk areas, that

threaten inviting new clients.• Sectoral growth is constrained due to low

unemployment levels and competition for staff.

• There are some gaps in range for certain sectors

like global delivery management, processes andsystems, that somehow have management issues.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 59/64

59

• Demand of its services in Middle East, Europe andSouth-East Asia.

• L&T is good at converting adversities into

opportunities and continue it’s march of progress .

• The end-users respond positively to new ideas, sothere exists a great possibility that L&T could

extend to overseas broadly.

• Mainframe management capabilities will give

opportunity to L&T-Ites to go for largeinfrastructure deals and hosting biz.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 60/64

60

• Legislation could make an impact over L&T’sbusiness proceedings.

• In spite of being among the most dominant

conglomerate in the country, L&T may be

vulnerable to reactive attack by its majorcompetitors.

• Lack of infrastructure in rural areas could

constrain investment.

• The high volume/low cost market is intenselycompetitive.

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 61/64

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 62/64

62

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 63/64

63

• Wikipedia• www.larsentoubro.com

• www.moneycontrol.com • www.cnbc.com • Financial Management by I M Pandey

8/13/2019 larsenandtoubro-130914065740-phpapp01

http://slidepdf.com/reader/full/larsenandtoubro-130914065740-phpapp01 64/64

so much for bearing us for the past 20 minutes..