last lecture summary analysis of financial statements key financial ratios limitation of financial...

TRANSCRIPT

Last Lecture Summary

• Analysis of Financial Statements• Key Financial Ratios• Limitation of Financial Statements Analysis• Market value added & Economic value added.

TIME VALUE OF MONEY

Learning Objectives:

After going through this lecture, you would be able to have an understanding of the following concepts.

• Main Concepts of FM.• Time Value of Money• Interest Theory and its determinants• Yield curve theory and its dynamics

FM Concepts:

There are certain financial management concepts that should be kept in mind, while making an analysis of a financial decision. The one-liners given here would help you in committing these concepts to your memory.

• A rupee today is worth more than a rupee tomorrow.Time Value of Money & Interest

• A safe rupee is worth more than a risky rupee.- Risk and Return

FM Concepts:

• Don’t compare apples to oranges- Discounting & NPV

• Don’t put all your eggs in one basket.- Portfolio Diversification

• Get insurance because you will break some eggs.- Hedging & Risk Management

Time Value of Money:

• The first concept, time value of money, says that a rupee in your hand today is worth more than the rupee that you are going to get tomorrow or the day after.

• This is because if you have a rupee in hand, you can put it into a bank (invest it) and can earn interest (return) on it, and tomorrow you are going to have more than rupee one, which of course, is more desirable than having just one rupee.

Risk and Return:

• Investors want to earn maximum return on their investment; however, risk is a constraint to this objective. Investors dislike risk-bearing, unless they are adequately compensated for that. Now the risk and return concept states that a safe rupee in your hand is better than a risky rupee which is not in your hand.

Risk and Return:

• This may imply that the investors would be willing to bear risk if they are offered more than a rupee i.e., a certain premium for risk bearing. However, in the absence of this additional compensation, a safe rupee is better than a risky rupee. The details about the concepts of risk and return would be discussed in the middle of the course.

Discounting & Net Present Value (NPV):

The third concept is of discounting and net present value of money. This is a fundamental mathematical concept and students need to practice it to perfection. Whether discounting for an asset or a company, we have to see what cash flow would it generate during its future life and then we bring back those future cash flow to the present, i.e., we discount the future cash flows to obtain their present value.

Discounting & Net Present Value (NPV):

This exercise is done to make comparison of cash flows occurring in different time periods, i.e., comparing apples to apples, rather than oranges. This concept is relentlessly used throughout the course in comparing different investment options in different time periods.

Portfolio Diversification:

The fourth concept is of portfolio diversification i.e. how to select different investment options so as to reduce risk of losing the invested money. For instance if an investor has a million rupees and he invests his total wealth in a single company’s share, he would be exposed to greater risk. If the company goes out of business or faces serious loss, the investor is likely to lose all his investment.

Portfolio Diversification:

However, if that investor puts his total wealth into shares of ten different companies, the chances that all the ten companies would face loss is comparatively lesser and hence the risk for the investor is diversified and reduced. The rule of finance says do not put all your eggs in one basket, because if you drop the basket accidentally, you are likely to lose all the eggs.

Hedging & Risk Management:

Finally, there is this fifth concept of hedging and risk management. Hedging is a strategy of risk management that is employed by investors to reduce or minimize the chances of loss. Insurance is said to be an effective tools used to manage risk.

Hedging & Risk Management:

The concept of hedging and risk management says that whether you put your eggs in one basket or in different baskets, chances are there that you will break your eggs so it is better to get the eggs insured Insurance is the best way to avoid loss so that even if the loss occurs you may get a claim on your damages.

Interest Theory:

Now, let’s discuss the concept of interest in detail, first major & technical area in financial management. Remember, that the basic objective in financial management is to maximize shareholders wealth.

Interest Theory:

• Economic Theory: Interest rate is an equilibrium price, expressed

in percentage terms, at which demand and supply of funds (or capital) meet, i.e., the rate at which the lenders are ready to lend and buyers are ready to buy. But equilibrium price (Interest rate) varies from one market to another.

Interest Theory:

For example, the “price” of capital in the property market is different from the “price” of capital in the cotton market. Markets have different interest rates guided by the supply & demand of funds in that market. Although the interest rates in different markets may differ, however, all the markets in the country and the interest rates prevailing there are interlinked.

Interest Theory:

Now, we come to the factors that determine the interest rates. It is important to understand the factors that make up an interest rate in the present day business environment. In business when we talk about the interest, we usually refer to nominal rate of interest which is determined with the help of following factors.

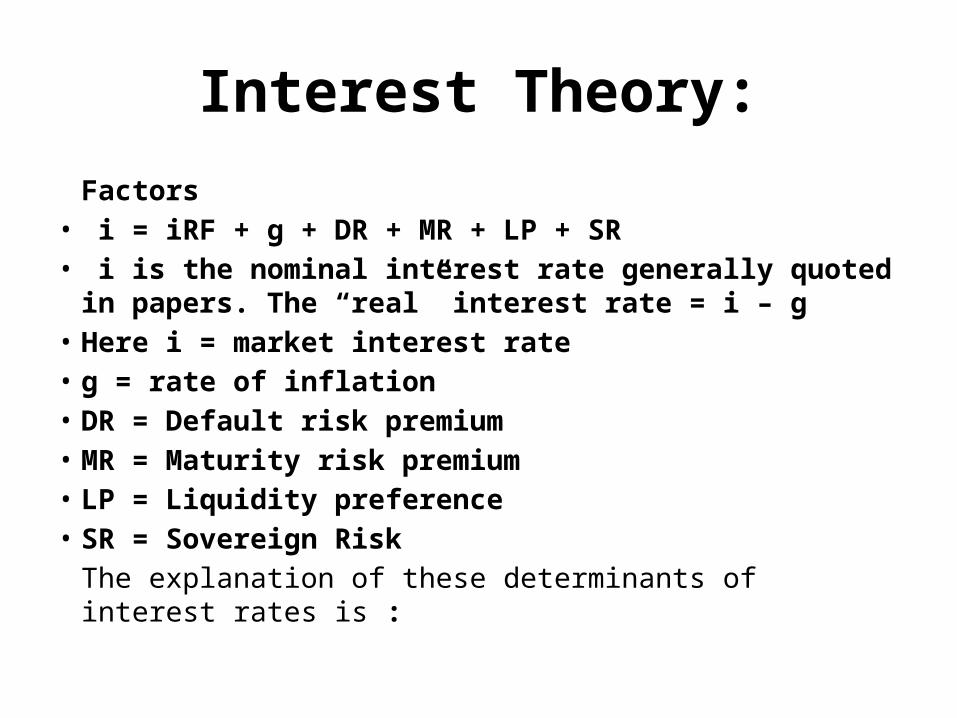

Interest Theory:

Factors• i = iRF + g + DR + MR + LP + SR• i is the nominal interest rate generally quoted in papers. The

“real” interest rate = i – g• Here i = market interest rate• g = rate of inflation• DR = Default risk premium• MR = Maturity risk premium• LP = Liquidity preference• SR = Sovereign Risk

The explanation of these determinants of interest rates is :

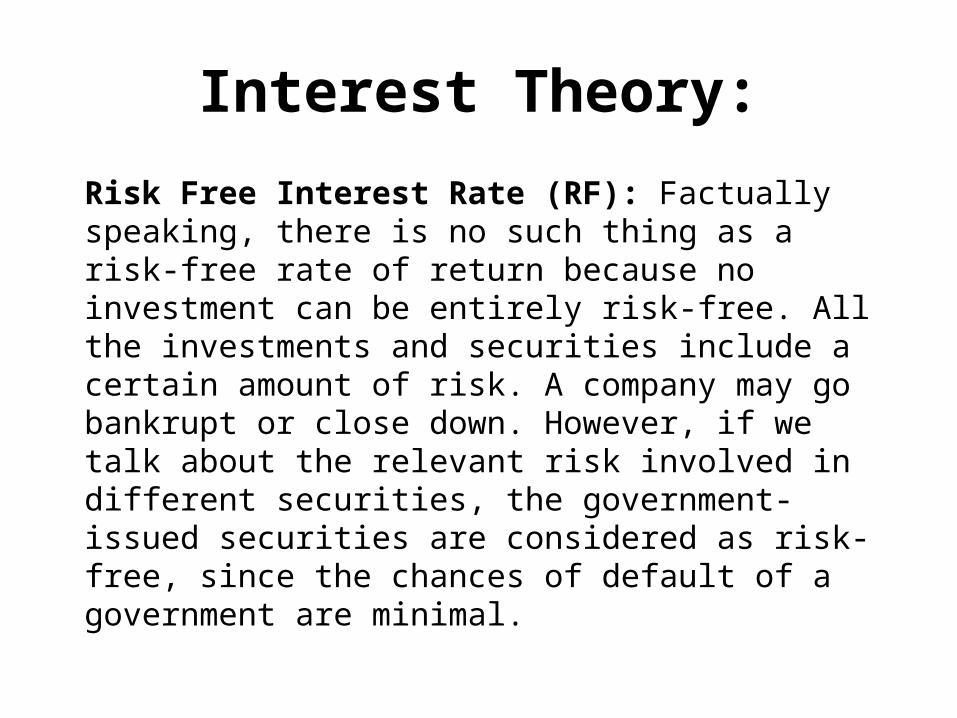

Interest Theory:

Risk Free Interest Rate (RF): Factually speaking, there is no such thing as a risk-free rate of return because no investment can be entirely risk-free. All the investments and securities include a certain amount of risk. A company may go bankrupt or close down. However, if we talk about the relevant risk involved in different securities, the government-issued securities are considered as risk-free, since the chances of default of a government are minimal.

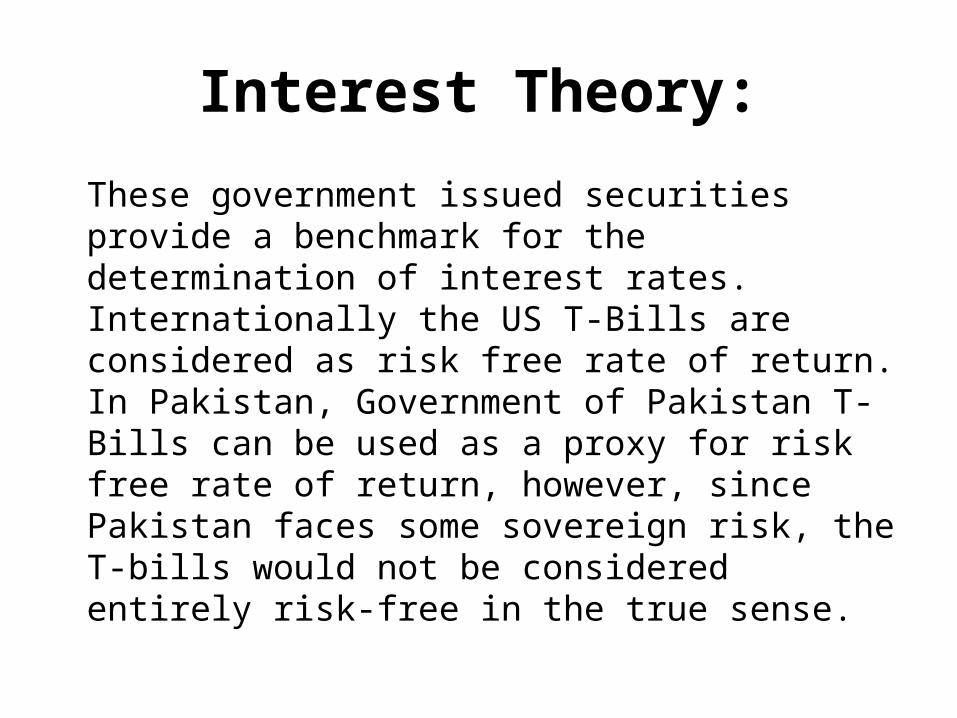

Interest Theory:

These government issued securities provide a benchmark for the determination of interest rates. Internationally the US T-Bills are considered as risk free rate of return. In Pakistan, Government of Pakistan T-Bills can be used as a proxy for risk free rate of return, however, since Pakistan faces some sovereign risk, the T-bills would not be considered entirely risk-free in the true sense.

Interest Theory:

Inflation (g):The expected average inflation over the life of the investment or security is usually inculcated in the nominal interest rate by the issuer of security to cover the inflation risk. For instance, consider a bond with a maturity of 5 years.

Interest Theory:

If the inflation rate in Pakistan is 8 % and the bond is also offering 8% percent interest rate, the investors would not be willing to invest in the bond since the gains from the interest rate would be exactly offset by the inflation rate which is actually eroding the wealth of the investor. To secure the investor against inflation the issuers, while quoting nominal interest rates, add the rate of inflation to the real interest rate.

Interest Theory:

Default Risk Premium (DR):Default risk refers to the risk that the company might go bankrupt or close down & bonds, orshares issued by the company may collapse. Default Risk Premium is charged by the investor, as compensation, against the risk that the company might goes bankrupt. Companies may also default on interest payments, something not very unusual in the corporate world.

Interest Theory:

In USA, rating agencies like Moody’s and S&P grade securities (debt and equity instruments) according to their financial health and thus identify those companies which have a good ability to pay off their principal lending and interest charges and those which might default on the payments.

Interest Theory:

The rating from best to worst is: AAA, AA, A, BBB, BB, B, CCC, CC, C. In Pakistan, Pakistan Credit Rating Agency (PACRA) and Vital Information Services (VIS) are actively conducting analysis of corporate securities and grading them.

Interest Theory:

Maturity Risk Premium (MR):The maturity risk premium is linked to the life of that security. For example, if you purchase the long term Federal Investment Bonds issued by the government of Pakistan, you are assuming certain risk, because changes in the rates of inflation or interest rates would depreciate the value of your investment.

Interest Theory:

These changes are more likely in the long term and less likely in the short term. Maturity Risk Premium is linked to life of the investment. The longer the maturity period, the higher the maturity risk premium.

Interest Theory:

Sovereign Risk Premium (SR): Sovereign Risk refers to the risk of government default on debt because of political or economic turmoil, war, prolonged budget and trade deficits. This risk is also linked to foreign exchange (F/x), depreciation, and devaluation.

Interest Theory:

Now-a-days the individuals as well as institutions are investing billions of rupees globally. If a bank wants to invest in Pakistan, it will have to take view of Pakistan’s political, economic, and financial environment..

Interest Theory:

If the bank sees some risk involved it would be willing to lend at a higher interest rate. The interest rate would be high since the bank would add sovereign risk premium to the interest rate. Here it may be clarified that Pakistan is not considered as risky as many other countries of Africa and South America

Interest Theory:

Liquidity Preference (LP):Investor psychology is such that they prefer easily encashable securities. Moreover, they charge the borrower for forgoing their liquidity. A higher liquidity preference would always push the interest rates upwards.

Yield Curve Theory:

Term Structure and Yield Curve:Interest rates for any security vary across time horizon. The supply & demand for funds vary depending on how long the funds are required. Normally, short term interest rates are lower than long term rates, or we can say that the interest rates depend on their term structure. Based on the maturity, the securities can be classified into three categories, although, these classes have been loosely defined.

Yield Curve Theory:

• Short Term: Short term means for the period of one year or less.

• Medium Term: For the period of any where between one year to five years.

• Long Term: Any where between 15 years to 20 years some people say that medium term is from 5 year to ten years and long term from 10 years to 20 years and plus.

Nominal or upward sloping yield curve:

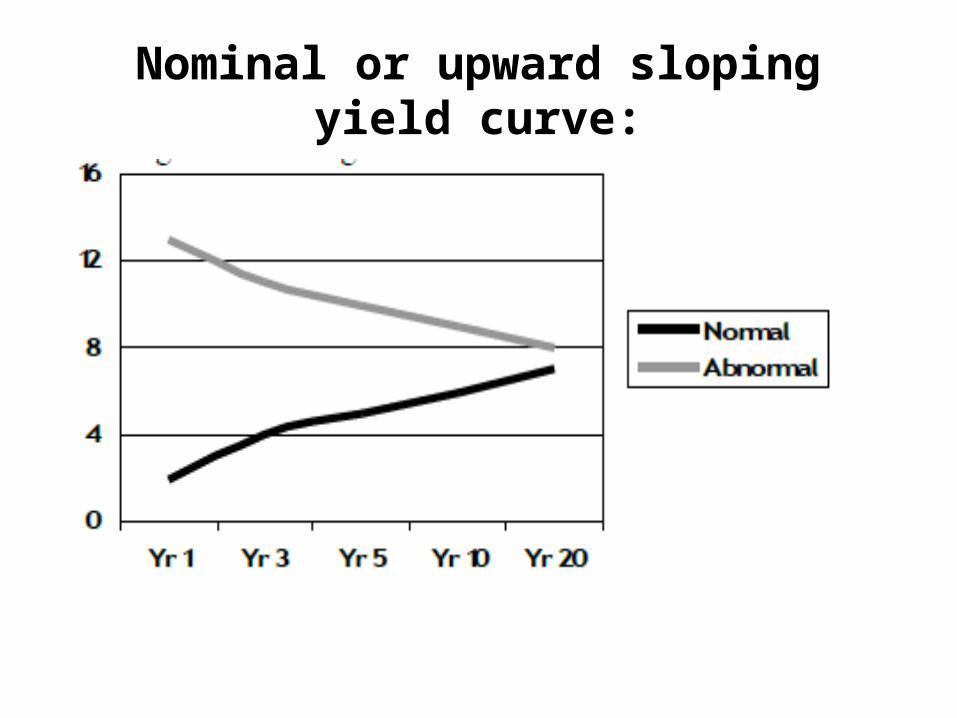

The supply & demand of funds or capital varies depending upon how long funds are required. For example, today the supply and demand for short term money might be different from supply and demand of the long term money. In another words, the number of borrowers to take loan for one week may be different from the borrowers of loan for one year.

Nominal or upward sloping yield curve:

Short term interest may be different than the long term interest; normally, short term interest rates are lower than long term than interest rates because investors think that inflation is going to increase. This phenomenon results in nominal or upward sloping yield curve.

Nominal or upward sloping yield curve:

Abnormal or downward sloping yield curve:Sometimes, the reverse is true. This is known as the Abnormal (or Downward Sloping) Yield Curve. It is the case where the short term raters are higher than long term interest tares. You can also have a mixed or Humped Back Curve.

Nominal or upward sloping yield curve: