lbbw fixed income conference 2015.€¦ · bmw group automotive: balanced sales ... business lines...

TRANSCRIPT

LBBW FIXED INCOME CONFERENCE 2015.

Stuttgart, September 29, 2015

BERND DASER,INVESTOR RELATIONS.

AGENDA.

1 OPERATING PERFORMANCE 2015

2 FUTURE GROWTH

3 FUNDING THE GROWTH: BMW GROUP TREASURY ACTIVITIES

4 SUMMARY

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 3

BMW GROUP POSTS SOLID FIRST HALF-YEAR RESULTS.

Profit before tax - BMW Group

H1-2015: € 4,851 mn H1-2014: € 4,813 mn +0.8

PBT margin: 10.8% PBT margin: 12.6% -1.8 pp

EBIT - Automobiles

H1-2015: € 3,613 mn H1-2014: € 3,741 mn -3.4

EBIT margin: 8.9% EBIT margin: 10.7% -1.8 pp

Revenues - BMW Group Change in %

H1-2015: € 44,852 mn H1-2014: €38,140 mn +17.6

Deliveries to Customers (in units) - Automobiles

H1-2015: 1,099,748 H1-2014: 1,020,211 +7.8

Revenues - Automobiles

H1-2015: € 40,543 mn H1-2014: € 35,063 mn +15.6

Free Cash Flow - Automobiles

H1-2015: € 2,557 mn H1-2014: € 1,002 mn .

EBT - Financial Services

H1-2015: € 1,055 mn H1-2014: € 905 mn +16.6

2014 numbers adjusted

9.0 8.8

8.1 7.9 7.8

6.76.4 6.4

1.4

-0.6

8.0

11.8

10.8

9.4

9.6

8.9

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013 2014 H1-2015

in %

*) 2012 figures have been adjusted in accordance with the revised version of IAS 19, see note 7 on page 106 of the annual report 2012.

Target

corridor

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 4

EBIT MARGIN DEVELOPMENT AUTOMOTIVE SEGMENT.TARGET PROFITABILITY OF 8-10%.

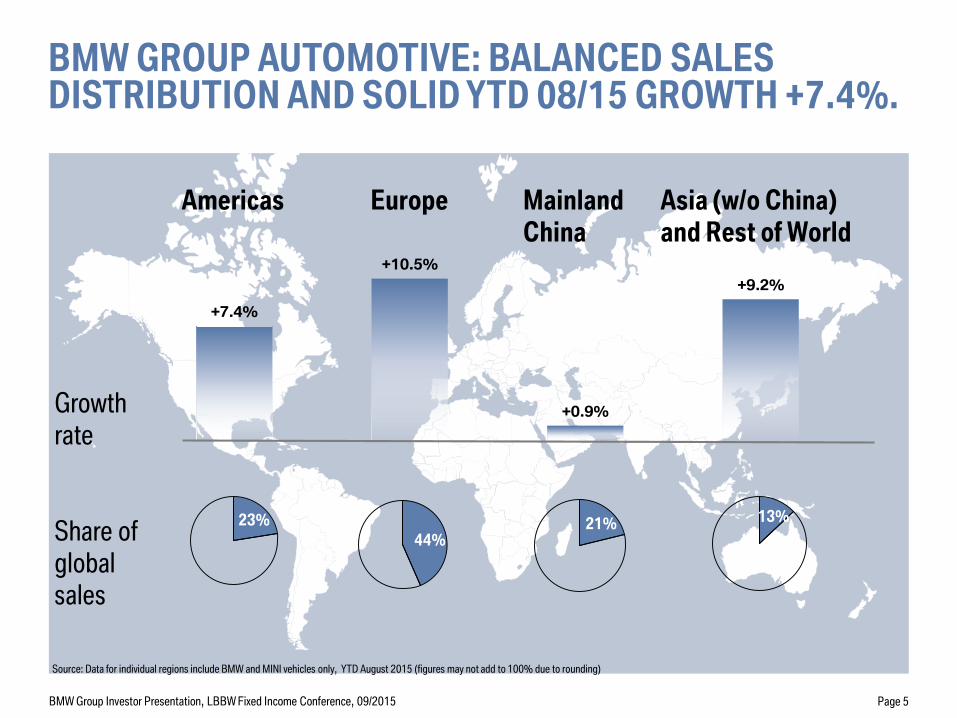

+7.4%

+10.5%

+0.9%

+9.2%

BMW GROUP AUTOMOTIVE: BALANCED SALES DISTRIBUTION AND SOLID YTD 08/15 GROWTH +7.4%.

Share of

global

sales

Source: Data for individual regions include BMW and MINI vehicles only, YTD August 2015 (figures may not add to 100% due to rounding)

Growth

rate

Mainland

China

Asia (w/o China)

and Rest of World

Americas Europe

23%

44%21% 13%

Page 5BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

BMW GROUP FINANCIAL SERVICES IS AN INTEGRAL PART OF THE AUTOMOTIVE VALUE CHAIN .

Global Presence June 2015

Global Operations in 54 Countries

Business Lines (Portfolio Size Q2/2015)

BankingInsurance

Multi Make

Financing

Commercial FinanceRetail Finance

€ 15.6 bn

€ 7.9 bn

€ 9.3 bn

€ 74.0 bn

3.0 mn Contracts

Fleet

Business

€ 10.2 bn

Page 6BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

29%

25%16%

30%

~4.1 Million Serviced Retail Contracts

EU Bank

EMEA

Americas

Asia, Pacific

13.6%

17.8% 17.8%19.2% 19.5%

17.1% 17.2% 17.4%

20.9%

24.7% 24.1%

20.0% 20.7%22.5%

20.8%23.9%

20.9%

17.2% 18.3%

19.1%

22.5%24.0%

25.2%27.2%

27.6%

24.3%24.1%

21.1% 19.7%

21.5%

20.9%

21.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 H1-2015

Financing Leasing

34.5% 35.0%36.1%

38.3%

42.0%41.1%

42.4%

48.5%

44.6%

49.0%

41.1%

48.2%

* The penetration rate dropped significantly due to the consolidation of BMW Group Financial Services China as of January 1st, 2011.

*

40.4%

44.0%

41.7%

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 7

PENETRATION RATE RETAIL BUSINESS.

45.1%

DEVELOPMENT OF CREDIT LOSS RATIO.

0.54%

0.46%

0.41%

0.37%

0.41%

0.46%

0.59%

0.84%

0.67%

0.49%0.48%

0.46%0.50%

0.34%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 H1-2015

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 8

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 9

RESIDUAL VALUE DEVELOPMENT IN THE USA.

Source: Manheim Used Vehicle Index, mix and mileage adjusted.

70

75

80

85

90

95

100

105

110

115

120

Jan

-06

Ap

r-0

6

Ju

l-0

6

Oct

-06

Jan

-07

Ap

r-0

7

Ju

l-0

7

Oct

-07

Jan

-08

Ap

r-0

8

Ju

l-0

8

Oct

-08

Jan

-09

Ap

r-0

9

Ju

l-0

9

Oct

-09

Jan

-10

Ap

r-1

0

Ju

l-1

0

Oct

-10

Jan

-11

Ap

r-1

1

Ju

l-1

1

Oct

-11

Jan

-12

Ap

r-1

2

Ju

l-1

2

Oct

-12

Jan

-13

Ap

r-1

3

Jul

-13

Oct

-13

Jan

-14

Ap

r-1

4

Ju

l-1

4

Oct

-14

Jan

-15

Ap

r-1

5

Ju

l-1

5

BMW brand used car index (through August 2015)

OUTLOOK 2015 – POSITIVE BUSINESS DEVELOPMENT DESPITE CHALLENGES.

BMW Group

Solid increase of BMW Group EBT compared to previous year.

Automotive Segment

Solid increase in vehicle deliveries and significant increase of revenues

compared to previous year.

EBIT margin in target range of 8-10%.

Financial Services Segment

Return on equity of at least 18%, on par with previous year.

Motorcycle Segment

Solid rise in deliveries compared to previous year.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 10

AGENDA.

1 OPERATING PERFORMANCE 2015

2 FUTURE GROWTH

3 FUNDING THE GROWTH: BMW GROUP TREASURY ACTIVITIES

4 SUMMARY

CONNECTED CARS

NEW PRODUCTSE-MOBILITY

INNOVATIVE SERVICES

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 12

INNOVATIONS AND NEW PRODUCTS DRIVE FURTHER GROWTH.

Q1 Q2 Q3 Q4

= M Models

1 Series 5-door & 3-door LCI

X5 xDrive40e

X12 series Gran Tourer

X5 M

X6 M

7 Series6 Series & M6 Convertible LCI*

6 Series & M6Coupé LCI*

6 Series & M6Gran Coupé LCI*

MINI Clubman2 Series Convertible

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 13

PRODUCT ROADMAP 2015.

3 Series derivatives LCI

MINI John Cooper Works

*6 Series vehicles shown here

Luxury

Compact/

Small

Lower

Medium

Upper

Medium

Page 14

NEW PRODUCT 2015. BMW 7 SERIES.

Launch 10/2015

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

WE ARE TRANSFERRING BMW i TECHNOLOGY TO OUR CORE BRAND VEHICLES – NEW PHEV MODELS.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

BMW 3 Series eDrive

~183 kW / 245 hp / >400Nm

~2.1 ltr/100km / ~ 50 gCO2/km

0-100 km/ h < 7.0 s

~ 35 km purely electric driving

Market launch: 2016.

BMW Concept Active Tourer eDrive

>140 kW / 190 hp / >250 Nm

~2.1 ltr/100km / ~ 50 gCO2/km

0-100 km/ h < 8.0 s

~ 35 km purely electric driving

Market launch: tbd.

BMW X5 xDrive40e

230kW / 313 hp / 450Nm

3.3 – 3.4 ltr/100km / 77 -78 g CO2/km

0-100 km/h 6.8 s

up to 31km purely electric driving

Market launch: Autumn 2015.

Page 15

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 16

INNOVATIVE TECHNOLOGIES AND SERVICES TO MEET CHANGING CUSTOMER DEMANDS.

Vehicle automation New BMW ConnectedDrive Store Touch Command

Connected Mobility iDrive Controller Fully automated parking

DRIVE NOW IS EXPANDING – BMW i3 JOINS THE FLEET.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 17

AGENDA.

1 OPERATING PERFORMANCE 2015

2 FUTURE GROWTH

3 FUNDING THE GROWTH: BMW GROUP TREASURY ACTIVITIES

4 SUMMARY

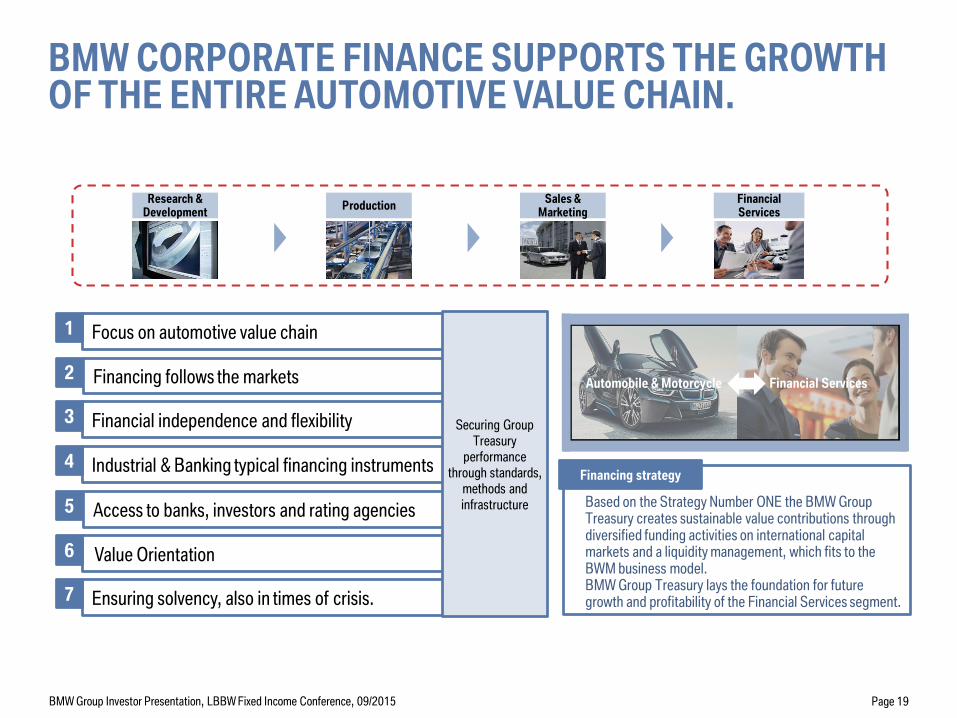

BMW CORPORATE FINANCE SUPPORTS THE GROWTH OF THE ENTIRE AUTOMOTIVE VALUE CHAIN.

Focus on automotive value chain

Financing follows the markets

Financial independence and flexibility

Industrial & Banking typical financing instruments

Access to banks, investors and rating agencies

Value Orientation

Ensuring solvency, also in times of crisis.

1

2

3

4

5

6

7

Automobile & Motorcycle Financial Services

Based on the Strategy Number ONE the BMW Group Treasury creates sustainable value contributions through diversified funding activities on international capital markets and a liquidity management, which fits to the BWM business model. BMW Group Treasury lays the foundation for future growth and profitability of the Financial Services segment.

Financing strategy

Securing Group

Treasury

performance

through standards,

methods and

infrastructure

Research & Development

ProductionSales &

MarketingFinancial Services

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 19

Page 20

InvestorsBanks

Group Treasury

„one face to the

market“

Rating

Agencies

ACCESS TO BANKS, INVESTORS AND RATING AGENCIES AS SUCCESS FACTORS.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

Page 21

BMW GROUP TREASURY OPERATING ENVIRONMENT.

Internal Drivers External Trends

Growing funding needs as a result

of growing automotive and

financial services business

Business growth in new marketsLow interest rates and high

liquidity

High volatility of emerging

markets’ economies and FX rates

Risk

ManagementFunding

Liquidity

Management

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

Funding Instruments Financial Debt as of 30.06.2015 (€ 82.4 bn*)

CP

<1yr 1yr 2yrs 3yrs 4yrs 5yrs 7yrs 10yrs+

(EMTN) PPs Bonds

Customers deposits

Banks loans

Fed

FundsBCD’s

Bank-typical instrumentsIndustry-typical

instruments

ABS ABCP

DIVERSIFIED FUNDING MIX WITH A COMBINATION OF INDUSTRY AND BANK TYPICAL FINANCING INSTRUMENTS.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 22

3.4%8.3%

9.9%

5.9%

0.9%

14.3%

7.2%

49.5%

0.5%

*Adjusted, excl. FX and interest rate derivatives

EMTN/bonds/

SSDs

Commercial Paper

ABS

Fed funds

Brokered CD‘s

Customer deposits

Structured

FinanceOther

Bank loans

SSDs*

1-4%Privat-

platzierungen*8-12%

Öffentliche

Anleihen*42-51%

Projekt-

bezogene Finanzierung

1-4%

Kredite

4-7%

Einlagen

7-13%

Brokered CDs

3-5%

ABS

12-16%

Commercial

Paper5-10%

SSDs*

1-4%

Anleihen/

Privat-platzierungen*

43-47%

Projekt-

bezogene Finanzierung

3-5%Kredite

6-7%

Einlagen

13-17%

Brokered CDs

6-8%

ABS

12-16%

Commercial

Paper6-10%

THE DEBT STRUCTURE ENSURES FLEXIBILITY IN LINE WITH THE GROWTH OF THE COMPANY.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 23

The Financial Debt Structure is driven by:

Diversification

Maturities

Independency

Company Growth

Funding is done worldwide to optimize refinancing costs and to establish a broad investor base.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 24

USA

USD Commercial Paper

USD US PP

USD ABS

Euro Capital Markets

EUR Commercial Paper

French Commercial Paper

EUR (EMTN) PPs

EUR Benchmark Bonds

USD Eurodollar

AUD Euroaussie

NOK (EMTN) Bonds

SEK (EMTN) Bonds

EUR ABS

Great Britain

GBP (EMTN) PPs

GBP Bonds

GBP ABS

Switzerland

CHF (EMTN) PPs

CHF Bonds

CHF ABS

Japan

JPY (EMTN) PPs

JPY Euro-Yen

JPY ABS

JPY Schuldschein

Australia

AUD (EMTN) PP

AUD ABS

AUD (AMTN) Bonds

Hong Kong

RMB (EMTN) PP

HKD (EMTN) PP

South Africa

ZAR ABS

ZAR Domestic Bonds

Canada

CAD ABS

CAD (EMTN) PPs

CAD Domestic Bonds

Mexico

MXN (EMTN) PP India

INR Domestic Bond

South Korea

KRW Domestic Bond

USD ABS

Mainland China

RMB ABS

BROAD INVESTOR BASE.

Brazil

BRL ABS

Page 25

Financing of Financial Services

Business free of liquidity risk

Verfügbarkeit der Konzernliquidität

über Kapitalsammelstellen (TCs).

Nutzen von Skalleneffekten.

Access to central bank liquidity

Maturity Profile

Treasury Center

Network

Central Bank

AccessInvestor Access

Strong free cash flow generation

Free Cash FlowLiquidity Reserve

Group Liquidity > 10 bn. EUR.

Availability of group liquidity thru

treasury centers. Using economic of

scale

Direct access to investors

BMW GROUP LIQUIDITY IS ENSURED, ALSO IN CASE OF A CRISIS.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

BMW GROUP WITH BEST RATING AMONG EUROPEAN AUTOMOTIVE MANUFACTURERS.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 26

Standard & Poor's Moody's

Short-term Rating A-1 P-1

Long-term Rating A+ A2

Outlook Stable Positive

Page 27

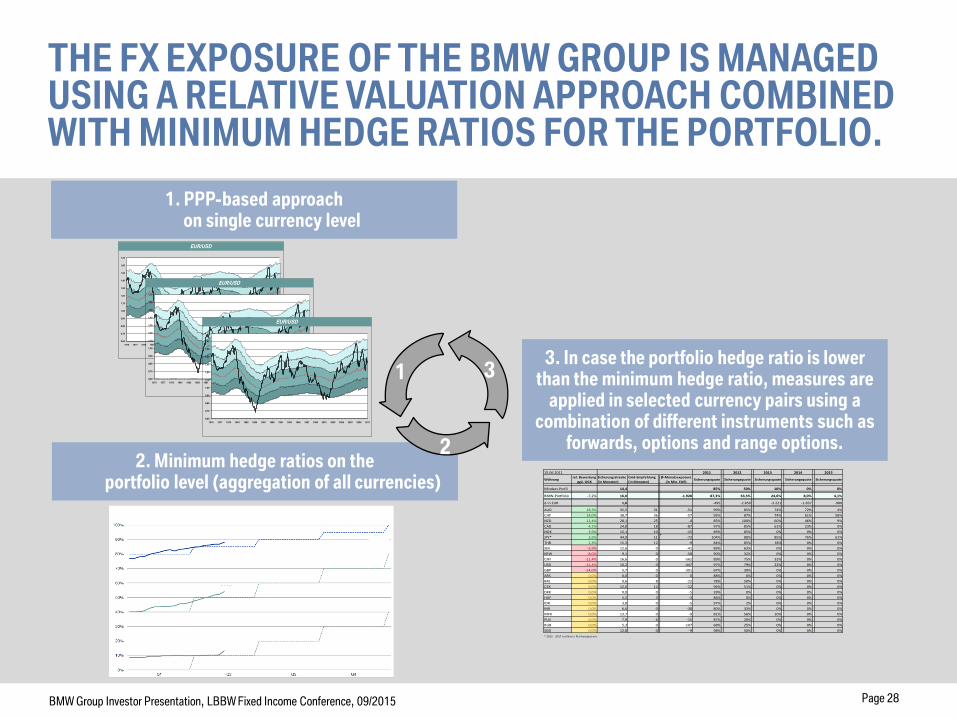

BMW GROUP TREASURY SUPPORTS THE AUTOMOTIVE VALUE CHAIN ALSO THROUGH FINANCIAL RISK MANAGEMENT.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

Interest Risk Currency Commodities

BMW Group’s financial risk management increases planning reliability, reduces earnings risks

and allows to take advantage of market opportunities.

1. PPP-based approach on single currency level

2. Minimum hedge ratios on the portfolio level (aggregation of all currencies)

3. In case the portfolio hedge ratio is lower than the minimum hedge ratio, measures are

applied in selected currency pairs using a combination of different instruments such as

forwards, options and range options.

1 3

2

0,60

0,70

0,80

0,90

1,00

1,10

1,20

1,30

1,40

1,50

1,60

1,70

1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

EUR/USD

0,60

0,70

0,80

0,90

1,00

1,10

1,20

1,30

1,40

1,50

1,60

1,70

1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

EUR/USD

0,60

0,70

0,80

0,90

1,00

1,10

1,20

1,30

1,40

1,50

1,60

1,70

1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

EUR/USD

THE FX EXPOSURE OF THE BMW GROUP IS MANAGED USING A RELATIVE VALUATION APPROACH COMBINED WITH MINIMUM HEDGE RATIOS FOR THE PORTFOLIO.

Währungrel. Bewertung

ggü. GGK

Sicherungsstrecke

(in Monaten)

Grid-Empfehlung

(in Monaten)

Ø-Monatsexposure

(in Mio. EUR)Sicherungsquote Sicherungsquote Sicherungsquote Sicherungsquote Sicherungsquote

Mindest-Profil 14,4 85% 50% 10% 0% 0%

BMW-Portfolio -7,2% 16,0 -1.928 87,3% 63,5% 24,6% 8,0% 4,1%

Δ in EUR 1,6 -495 -2.850 -3.221 -1.837 -980

AUD 18,3% 35,5 31 -51 99% 85% 74% 72% 4%

CHF 14,0% 38,7 36 -57 95% 87% 74% 61% 58%

NZD 12,4% 28,1 25 -4 85% 100% 60% 46% 9%

CAD 4,1% 24,8 18 -87 97% 85% 61% 23% 0%

NOK 3,9% 15,1 10 -15 89% 85% 0% 0% 0%

JPY* 2,6% 44,9 11 -72 104% 88% 85% 76% 61%

THB 2,3% 15,3 12 -9 84% 85% 18% 0% 0%

SEK -5,9% 12,6 0 -41 89% 63% 0% 0% 0%

KRW -8,0% 9,1 0 -58 90% 32% 0% 0% 0%

CNY -11,4% 16,6 0 -562 89% 75% 32% 0% 0%

USD -11,4% 16,2 0 -447 97% 79% 22% 0% 0%

GBP -14,0% 5,7 0 -301 67% 30% 0% 0% 0%

ARS 0,0% 0,0 0 0 88% 0% 0% 0% 0%

BRL 0,0% 9,6 8 -22 78% 50% 0% 0% 0%

CZK 0,0% 12,0 12 -12 96% 51% 0% 0% 0%

DKK 0,0% 0,0 0 -5 39% 0% 0% 0% 0%

HUF 0,0% 5,5 3 -3 86% 0% 0% 0% 0%

IDR 0,0% 3,8 0 -5 97% 2% 0% 0% 0%

INR 0,0% 6,6 0 -30 80% 33% 0% 0% 0%

MYR 0,0% 13,7 0 -9 81% 56% 10% 0% 0%

PLN 0,0% 7,9 6 -15 87% 20% 0% 0% 0%

RUB 0,0% 5,3 0 -107 68% 25% 0% 0% 0%

SGD 0,0% 12,8 0 -9 98% 50% 0% 0% 0%

* 2012 - 2017 auf Bas is Ris ikoexposure

201515.06.2011 2011 2012 2013 2014

Page 28BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015

AGENDA.

1 OPERATING PERFORMANCE 2015

2 FUTURE GROWTH

3 FUNDING THE GROWTH: BMW GROUP TREASURY ACTIVITIES

4 SUMMARY

SUMMARY.

GOOD FIRST HALF OF THE FINANCIAL YEAR 2015.

GUIDANCE CONFIRMED.

BMW GROUP IS WELL PREPARED FOR THE FUTURE.

BMW GROUP TREASURY MANAGES GROWING FUNDING

NEEDS AND IS WELL POSITIONED IN A VOLATILE MARKET

ENVIRONMENT.

BMW Group Investor Presentation, LBBW Fixed Income Conference, 09/2015 Page 30