lca_presentation_example

TRANSCRIPT

LABCORP A PREMIER HEALTHCARE SERVICES

COMPANY Associate Regional Manager of Business

Development Opportunity for Tony Fanelli PLEASE NOTE: EXAMPLE OF RECENT PRESENTATION. IT WILL PROVIDE

YOU WITH MY UNDERSTANDING OF THE CLINICAL DIAGNOTICS AND

HEALTHCARE ARENAS. THE JOB WAS CANCELLED BY LCA.

“The task of the leader is to get his people from where

they are to where they have not been.”

-Henry Kissinger

The Patient Comes First: Commitment to the “Voice of the Customer”

“A customer is the most important visitor on our premises; he is not dependent on us. We are dependent on him. He is not an interruption to our work. He is the purpose of it. He is not an outsider in our business. He is part of it. We are not doing him a favor by serving him. He is doing us a favor by giving us the opportunity to do so.”

- Mahatma Gandhi

2

Health Care Continuum, LabCorp & Personalized Medicine Personalized Medicine Is…

Personalized medicine is a multi-faceted approach to patient care that not only improves our ability to diagnose and treat disease, but offers the potential to detect disease at an earlier stage, when it is easier to treat effectively. Health Information Technology is a key enabler and potential accelerator of the successful adoption of personalized medicine. The full implementation of personalized medicine encompasses the 7 phases of the Health Care Continuum denoted below:

Risk Assessment: Genetic testing to reveal predisposition to disease

Prevention: Behavior/Lifestyle/Treatment intervention to prevent disease

Detection: Early detection of disease at the molecular level

Diagnosis: Accurate disease diagnosis enabling individualized treatment strategy

Treatment: Improved outcomes through targeted treatments and reduced side effects

Management: Active monitoring of treatment response and disease progression

Integration of Information:

Seamless and rapid flow of digital information, including genomic, clinical outcome, and claims data

3

LabCorp: A Premier Healthcare Services Company

• Attractive Market

• Strong Financial Fundamentals

• Superior Execution

• Clear Mission

• Five Pillar Strategy

4

Attractive Market: Lab Testing Is A Valuable Service

• Small component of total cost that influences 70-80% of physician decisions: 2-3% of total spend of $2.8 Trillion

• 10% of spend, moving toward personalized medicine as companion diagnostics improve efficacy and safety

• Screening, early detection and monitoring reduce downstream costs

• Decision support tools guide providers to better patient outcomes

5

Attractive Market: Lab Testing Growth Drivers • Aging population

• Industry consolidation

• Healthcare Reform and Value-Based Care

• Key managed care relationships

• Population Health Analytics & HIT adaptation

• Alternative Delivery Models & Care Delivery Systems

• Escalating opiate, substance and alcohol abuse among teens, adults, and special populations

• Advances in genomics & personalized medicine

• Pharmacogenomics / companion diagnostics

• Cost pressures will reward lower cost and more efficient providers

6

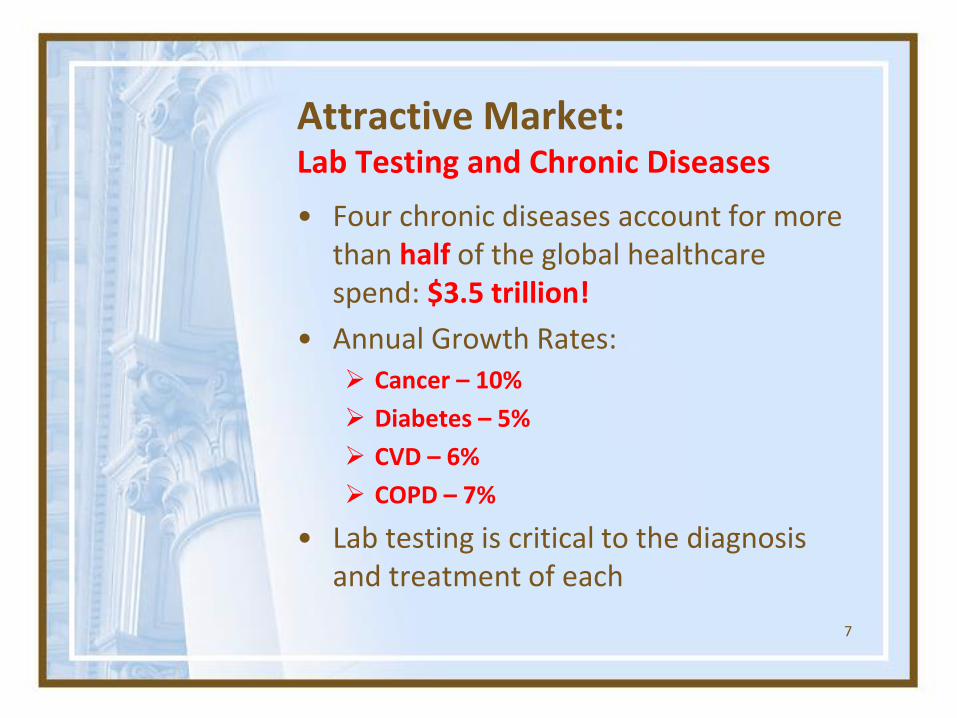

Attractive Market: Lab Testing and Chronic Diseases

• Four chronic diseases account for more than half of the global healthcare spend: $3.5 trillion!

• Annual Growth Rates: Cancer – 10%

Diabetes – 5%

CVD – 6%

COPD – 7%

• Lab testing is critical to the diagnosis and treatment of each

7

Attractive Market: Lab Testing International Opportunities • Manageable capital outlay – capital light model

• 2010 global healthcare spend of ~ $4.0 trillion, ex U.S.

Est. $160 billion global diagnostics market, ex U.S.

Chronic conditions growing at ~ 20% annually

• Growing middle class in large Asian and Latin American populations

• Will look at opportunities in countries with the following characteristics:

Large self – pay segment

20%+ of population mid to upper class

Majority of population concentrated in a small number of cities

Diagnostic segment ~ 4% of healthcare spend

Physician community aware of, and educated in, complex diagnostics

Infrastructure – airports and roads

8

Attractive Market: Lab Testing & Opportunity to Take Share

• $60 billion US lab market

• Approximately 5,700 independent labs

• Less efficient, higher cost competitors

• Full service, “one stop shop”

• Contract clinical trials partnerships

• $30.25 billion opportunity in hospital affiliated labs, $6.6 billion in Quest, and $12 billion in Independents!

9

Attractive Market: LabCorp’s Diversified Payor & Test Mix

• No customer > 11% of revenue

• Limited government exposure with about 17% of revenue in Medicare and Medicaid

• About 21% in Managed Care Fee – For - Service

• With recent acquisitions, esoteric testing comprises over 41% of revenue – not including Covance

• Core business ~ 63% of revenue

10

Mission Statement

We Will Be a Trusted Knowledge Partner for Stakeholders, Leading to Growth in Our Business and Continued Creation of Shareholder Value

We Will Achieve This Mission by Continuing to Execute Our Five Pillar Strategy

11

Five Pillar Strategy: Pillar One - Capital Deployment Deploy Capital to Investments That Enhance Our Footprint and Return Capital to Shareholders:

• Acquisitions: Genzyme Genetics, Orchid Cellmark, MEDTOX Scientific, and Covance

• Approximately $2.9 billion of share repurchase since 2009

• Future accretive acquisitions

Future Capital Deployment Strategy:

• Target Leverage Ratio of ~ 2.5 to 1 (Debt/EBITDA) over time

• Acquisitions

• Share Repurchase

12

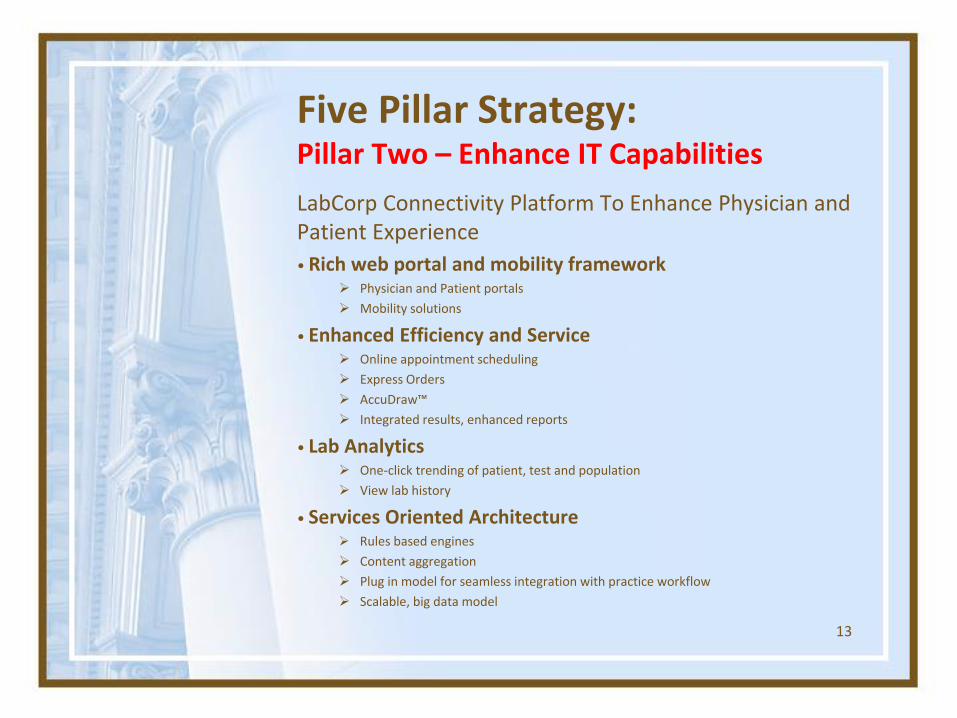

Five Pillar Strategy: Pillar Two – Enhance IT Capabilities

LabCorp Connectivity Platform To Enhance Physician and Patient Experience

• Rich web portal and mobility framework Physician and Patient portals

Mobility solutions

• Enhanced Efficiency and Service Online appointment scheduling

Express Orders

AccuDraw™

Integrated results, enhanced reports

• Lab Analytics One-click trending of patient, test and population

View lab history

• Services Oriented Architecture Rules based engines

Content aggregation

Plug in model for seamless integration with practice workflow

Scalable, big data model

13

Five Pillar Strategy: Pillar Two – Enhance IT Capabilities

Patient Portal

• Patients receive lab results as easily as checking email

• Provides greater patient intimacy

• Over 400,000 patients have signed up for this innovative service

• 2014 enhancements will focus on adding content to assist patients in understanding results

14

Five Pillar Strategy: Pillar Three – Improve Efficiency

Focus On Efficiency to Offer the Most Compelling Value in Laboratory Services

• Comprehensive review of cost structure

• Standardization Lab platforms, instruments and processes

Billing system

• Supply chain optimization

• Automation of pre-analytics

• Facility rationalization

• Propel splitting and sorting robotics

15

Five Pillar Strategy: Pillar Four – Scientific Innovation At Appropriate Pricing

LabCorp – Laboratory Corporation of America • Core Testing

• Specialty Testing Groups Cellmark FORENSICS

Colorado COAGULATION

Dianon PATHOLOGY

Endocrine SCIENCES

Integrated GENETICS

Integrated ONCOLOGY

MedTox LABORATORIES

LabCorp DNA IDENTITY

Litholink

Monogram BIOSCIENCES

National GENETICS INSTITUTE

ViroMed LABORATORIES

LabCorp CLINICAL TRIALS

16

Five Pillar Strategy: Pillar Four – Scientific Innovation at Appropriate Pricing Companion diagnostics and personalized medicine

• IL-28B

• BRAF V600E metastatic melanoma (Zelboraf)

• Vysis ALK Break Apart FISH probe (XALKORI)

• K-RAS

• HLA-B* 5701, HLA by NGS

• EGFR Mutation Analysis

• HCV GenoSure NS3/4a

• PhenoSense, PhenoSense GT

• HERmark

• SNP Microarray-Oncology

• CYP 450 2C19

• BRCA 1/2 Sequencing

• Intelligen NGS Therapeutic Panel, NGS Universal Carrier Screening, NGS Gene Panels

• 4th Generation HIV test

• HistoPlus: Lung Cancer

• GeneSeq: Cardiomyopathy NGS panels

• Thiopurine metabolites, expanded Inflammatory Bowel Disease (IBD) offerings

• SNP Microarray-Oncology

• NanoString Prosigna Breast Cancer Prognostic Gene Signature Assay

Women’s health

• ROMA

• Nuswab STD testing on a single swab

• Expanded Vaginosis and Candida testing

• Expanded options for HPV DNA testing

• Age-based guideline testing initiative for HPV

• Non-Invasive Prenatal Screening

17

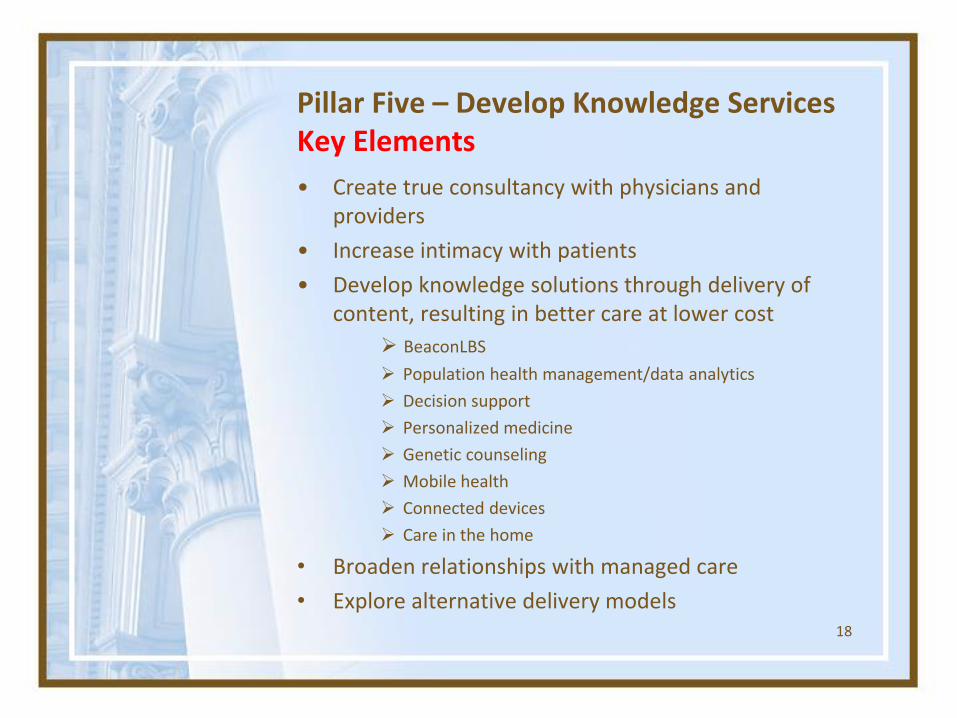

Pillar Five – Develop Knowledge Services Key Elements

• Create true consultancy with physicians and providers

• Increase intimacy with patients

• Develop knowledge solutions through delivery of content, resulting in better care at lower cost

BeaconLBS

Population health management/data analytics

Decision support

Personalized medicine

Genetic counseling

Mobile health

Connected devices

Care in the home

• Broaden relationships with managed care

• Explore alternative delivery models

18

Integrated Delivery Network: The Ultimate Delivery Model Objectives of Integrated Delivery Networks • Quality Improvement and Cost Reduction:

• Reducing administrative/overhead costs

• Sharing risk

• Eliminating cost-shifting

• Outcomes management and continuous quality improvement

• Reducing inappropriate and unnecessary resource use

• Efficient use of capital and technology

• Consumer Responsiveness:

• Seamless continuum of care from “Womb to Tomb”

• Focus on health of enrollees

• Expand footprint and increase access to providers and services

• Community Benefit:

• Improvement of community health status

• Addressing the prevention of social issues which affect community health – HIV, substance abuse, high infant mortality, child abuse, clinical trials

19

Current Trends of Integrated Delivery Networks • Purchasing PCPs to capture patients in order to increase revenue and utilization of primary

and ancillary service lines.

• Shortage of primary care physicians leading to increased care from PAs and NPs.

• PCMH accreditations and Health Home Case Management Programs to address the “frequent flyers” or patients that drain the system of scarce and costly resources.

• Implementing technology like Medication Therapy Management and other Population Health Analytics tools to proactively manage high-risk patients and to reduce hospital stay and readmissions.

• Re-entering the health insurance market ; heightened relationships with MCOs.

• Adopting and implementing EMR systems per the ARRA of 2009. Also upgrading HIS/LIS to achieve a plug-in model for seamless integration with practice workflow and future HIT and Telemedicine applications.

• Interfacing EHRs with RHIOs / SHINS per the ARRA of 2009 to facilitate a secure electronic exchange of clinical information among providers. Goal is to achieve true Connected Communities of Health Interoperability.

• Migrating specialists to the EMR.

• Incentivized to provide personalized medicine and evidence-based preventive medicine across the Health Care Continuum.

• Patient Protection and Affordable Care Act to have a positive impact on PCP patient access in 2014 with a focus on the rural Medicaid populations. However, higher annual deductibles and co-payments will cause hospitals to intensify efforts to collect directly from patients.

• Shifting non-critical care patients from inpatient beds and EDs to outpatient and home care.

20

Integrated Delivery Networks: My View From The Inside

• Seeking products or services that will make their network best of breed and emulated throughout the region.

• Seamless network for the treatment of pain management, addiction medicine, agonist therapy, inpatient / outpatient care, and primary and behavioral health care integration initiatives.

• PCP as the hub of all relevant activity and responsible for the coordination of value-based care.

• Pursuing strategic partnerships to mutually penetrate new markets, increase revenue and transform patient care through the adaptation of cutting-edge technologies.

• Looking for ease of use in terms of time and hassle saved as well as the highest quality and most compelling value.

• A “Patient First” approach through community focus groups and commitment to the “Voice of the Customer.”

• Direct to consumer marketing to expand footprint and provide the convenience of one-stop-shopping throughout the network’s continuum of health care services and providers.

• Offers a wide range of Health Resources for the community from wellness programs to support groups to clinical trials in order to increase patient access and engagement.

• Shared service and purchase service agreements within and out of network to increase efficiencies and reduce redundancies and costs.

• Taking a proactive approach to HealthCare Reform; preparing for new Part D requirements, ICD-10 conversions, and future CMS metrics and policies.

• Ongoing FTE reductions are adversely affecting patient care.

21

Integrated Delivery Networks: My View From The Inside, Cont.

IDN Business Development Strategies:

Partnerships = Pull Through

• Utilize the following process to develop the pipeline:

• PROSPECT & ENGAGE: Identify prospects, diagram organizational chart, qualify prospects and secure appointments

• DIFFERENTIATE & ENTICE: Differentiate, develop right needs and inspire emotion

• BUILD VALUE: Permeate account, present solution and gain technical win or added value

• CONFIRM & CLOSE: Sell decision makers and influencers, prove capabilities and secure the contract

• MAKE REFERENCEABLE: Deliver value, make reference able and discover new needs. Leverage current relationships.

• Right of First Negotiation

• Positioning-Based Selling

• Consultative Resource / Added-Value Approach

• Utilize the following strategies to expand footprint:

• Shared Service Agreements

• Purchase Service Agreements

• Contract Pathology Services

• Infrastructure Agreements

• Capacity Rationalization

• Logistics Service Agreements

• PSC Service Agreements

• Phlebotomy Services

• STAT Service Agreements

• Joint Outreach Ventures

• Test/Department/Lab Take-downs

• Lab Management Agreements

• Consultative Services

• LIS/HIS/EMR Interfaces

• GPO & MCO RFP Negotiation/Implementation/ Compliance

• Leverage hospital relationships

• Programs outlined on pgs. 20,21

22

• Academic Institutions / Teaching Hospitals / School Districts

• Addiction Medicine Providers

• Accountable Care Organizations (ACO)

• Add – On or Upsells From Client Base

• Ambulatory Surgery Centers

• Behavioral Health Providers

• Cancer Management Providers

• Centers of Excellence

• Clinics and Rural Health Groups

• Clinical Trials

• Coalitions

• Complimentary Medicine

• Concierge Medicine

• Co – Occurring Disorders (MH and CD)

• Commercial and Capitated Health Plans / Private Pay Markets

• Community Outreach Partnerships & Fundraisers

• Consultative and Contract Services

• Competitor Accounts

• Corporations / EAPs

• Criminal Justice Systems

• Departments of Mental Health – County & State

• Disease Management Organizations (DMO)

• Dual – Diagnosis (Alcohol / Substance Abuse)

• Enroll America

• Government Agencies – State & Federal

• Government & Privately Funded Initiatives

• Health Home Case Management Programs

• Health Insurance Exchanges

• Health Information Exchanges / Regional and State

• Holistic Medicine Providers

• Health Systems

• Hospices

• Hospital Emergency Departments

• Hospitals – National / Regional Agreements

• Hospitals – Rural

• Hospitals - Specialty

23

Alternate Delivery Models, CDOs & Targets: Changes in Healthcare “Center of Gravity”

Alternate Delivery Models, CDOs & Targets: Cultivate Prospects to Build a Robust Pipeline

• Integrated Delivery Networks (IDN)

• Independent Physician Associations (IPA)

• Managed Behavioral Health Organizations (MBHO)

• Management Services Organizations (MSO)

• Medicaid Providers and Populations

• Medical Tourism

• Mega – Physician Practices

• Mental Illness & Companion Medical Issues

• Military Populations and Organizations

• Mobile, Telehealth & Home Care

• New Delivery Models Under Healthcare Reform

• Non – Traditional Opportunities

• Pain Management Providers

• Patient-Centered Specialty Practice Recognition (PCSP)

• Partners in Healthcare

• Physical Medicine, Rehabilitation and Orthopedic Providers

• Patient-Centered Medical Homes (PCMH)

• Physician Hospital Organizations

• Physician Specialists & Pathology

• Pilot Programs

• Primary Care Physicians

• Retail Clinics

• Rural Health Networks

• Special Populations

• Self – Funded Health Organizations

• Third Party Administrators

• Wellness Providers

• Managed care collaborations with and ownership of all of the above

24

Integrated Delivery Networks: Partnerships = Pull Through Over the years, I have partnered with numerous IDNs.

• BayCare Health System

• Lee Memorial Health System

• HCA Healthcare

• IASIS Healthcare

• USF Health

• VA Sunshine Health

• Florida Rural Health Association

• Community Health Systems

• Tampa General Health

• Sarasota Memorial Healthcare System

• Lee Memorial Healthcare System

• NCH Healthcare System

• Orlando Health

• Florida Hospital Healthcare System

• Ocala Health

• Shands Healthcare

• Central Florida Health Alliance

• Health First

• University Community Health

• Rochester Health

• Catholic Health

• Kaleida Health

25

Managed Care Organizations: Broaden Relationships With Managed Care Managed Care Experience • Aetna

• Amerigroup

• AvMed

• Beech Street

• Blue Cross Blue Shield

• Choice Managed Care (Workers’ Comp)

• Cigna

• Commercial

• CorVel (Workers’ Comp)

• Coventry Health Care

• Empire – NYS Employees

• Fidelis

• First Health (Workers’ Comp & Medical)

• First Service Administrators

• Focus (Workers’ Comp)

• Freedom Health

• Health First

• Health Options

• Health Choice

• Healthy Kids Florida

• Health Now

Managed Care Experience • Hernando County Government

• Hillsborough County Government

• Humana

• Independent Health

• Magellan

• Manatee Health Network*

• Medicaid

• Medicare

• Memorial Employee Health Plans*

• Pasco County Government*

• Pinellas County Schools*

• Rockport (Workers’ Comp)

• TRICARE

• UnitedHealthcare

• Univera

• WellCare

• Wellpoint

• NUMEROUS OTHERS

*denotes plans that I negotiated . The other

plans I have experience with, helped to set-up, implement

& manage compliance / leakage issues

26

Health Care Reform = Opportunity Increased Access, Parity, Integration and Prevention

Health Reform Basics • The American Recovery & Reinvestment Act of 2009

• The Affordable Care Act of 2010

• Mental Health Parity and Addiction Equity Act of 2008

• Primary and Behavioral Health Care Integration

• Grants

• Health Homes

• Patient-Centered Medical Homes

• Eligibility & Enrollment – Medicaid and ACA Health Insurance Exchanges

• National Prevention Strategy

• Preventive Task Force

• Community Transformation Grants

• Prevention and Public Health Fund

• Prevention Services Covered Under the ACA

• Medicare Preventive Services Coverage

• Medicaid Preventive Services Financing

• Employer Wellness Programs

27

Leadership That Gets Results: Proactive Solutions • My Value To LabCorp:

Track Record & Experience

• Leadership:

Unite, Lead and Deliver

• Leadership Tools & Strategies:

The Path To Success

• Growth & Retention Tools:

Continuously Expand Footprint

• IDN Business Development Strategies:

Partnerships = Pull Through

• Personal Mission Statement

The Voice Of The Customer

28

My Value to LabCorp Track Record & Experience • Over 28 years of progressive experience in physician, hospital,

GPO, and IDN arenas with 20 years served in positions of leadership

• Alignment of goals, strengths and cultures • P & L and territory management acumen • Ability to build and motivate diverse, high-performance teams • Proven producer and winner • Superb networking and business development skills • IT and connectivity solutions acumen • Unsurpassed work ethic and integrity • Extremely loyal and dedicated • Cross-functional leadership • Industry insight and technical knowledge • Leadership Tools • Growth and Retention Tools • Business Development Strategies • Proactive approach to Health Care Reform • Commitment to the “Voice of the Customer” • Excel in rapidly evolving systems and priorities

29

Leadership: Unite, Lead and Deliver • Embrace role as a COACH with a passion – provides an

honest, open and encouraging environment that fosters communication and creativity

• Proactively builds bench-strength

• Liaison between clients, sales and operations

• Provide tools for success

• Cross-functional ingenuity

• Hands-on management style – work in the “trenches” with my team

• Never more than one step from the customer

• Leads by example

• Visionary and out-of-the-box strategist

• Team player and persuading conductor

• Bottom-line and big picture oriented

• Always one step ahead of the challenge and two steps ahead of the competition!

30

The Eleven Critical Qualities of Leadership: My Daily Mission!

1. Unwavering Courage

2. Self-Control

3. A keen sense of justice

4. Definiteness of decision

5. Definiteness of plans

6. The habit of doing more than paid for

7. A pleasing personality

8. Sympathy and understanding

9. Mastery of detail

10. Willingness to assume full responsibility

11. Cooperation

31

Leadership Tools & Strategies: The Path To Success • Liaison between sales and operations per the “Voice of the

Customer”

• Customer and associate satisfaction surveys

• Continuous cross-functional process improvements to differentiate brand and eliminate silos

• Team Sales Approach Model

• Weekly conference calls and quarterly meetings

• Provide tools for success

• Business unit recognition programs

• Field Work Contact Review Form

• Proactive bench-strength pipeline

• Personal Development Program

• Mentoring Partnerships - utilize your stars

• Team-building and development – Rembrandt Advantage and Myers-Briggs Type Indicators

• Active role in industry-related organizations – AACC, CLMA

• ACOUNTABILITY! URGENCY! EVOLUTION!

32

Growth and Retention Tools: Continuously Expand Footprint • Territory Management Reports • Sales Force Automation • Microsoft Excel/Access Upsell Report • Internal Account Manager “Mining” Program • Internal Account Manager support efforts • Attrition, leakage and variance reports • Targeted fee increases • Competitor “Spiff” incentive programs • Account-specific pipeline strategies • Brainstorm for non-traditional opportunities • Rent PSC space in large targets • Strategic account stability plans • Accordion Sales Presentation Tool • Adopt-A-Customer Program • Direct to consumer marketing and branding • Population growth-targeted PSCs • Maximize under-performing PSC volumes • Centralized CEUs and other added value programs • Evaluate local market production schedules • Always be in the center of health care delivery! • Keep your competitors on the defensive!

33

IDN Business Development Strategies:

Partnerships = Pull Through

• Utilize the following process to develop the pipeline:

PROSPECT & ENGAGE: Identify prospects, diagram organizational chart, qualify prospects and secure appointments

DIFFERENTIATE & ENTICE: Differentiate, develop right needs and inspire emotion

BUILD VALUE: Permeate account, present solution and gain technical win or added value

CONFIRM & CLOSE: Sell decision makers and influencers, prove capabilities and secure the contract

MAKE REFERENCEABLE: Deliver value, make reference able and discover new needs. Leverage current relationships.

• Right of First Negotiation

• Positioning-Based Selling

• Consultative Resource / Added-Value Approach

• Utilize the following strategies to expand footprint:

Shared Service Agreements

Purchase Service Agreements

Contract Pathology Services

Infrastructure Agreements

Capacity Rationalization

Logistics Service Agreements

PSC Service Agreements

Phlebotomy Services

STAT Service Agreements

Joint Outreach Ventures

Test/Department/Lab Take-downs

Lab Management Agreements

Consultative Services

LIS/HIS/EMR Interfaces

GPO & MCO RFP Negotiation/Implementation/ Compliance

Leverage hospital relationships

Programs outlined on pgs. 20,21

34

Personal Mission Statement: The Voice Of The Customer I am a highly sought-after sales leader in the clinical laboratory diagnostics and healthcare services fields. I have over 28 years combined experience with Abbott Diagnostics, SmithKline Beecham Clinical Laboratories/Quest Diagnostics, University Community Health, Florida Drug Screens LLC, and Niagara Falls Memorial Medical Center. Twenty of my twenty-eight years have been served in positions of leadership. As a strategic leader, I direct teams to optimal performance and exceptional profits in the hospital, physician, IDN and GPO arenas. Currently, I am an Electronic Health Records Specialist with Niagara Falls Memorial Medical Center (NFMMC), gaining valuable experience while I conduct my career campaign. NFMMC is part of a 33 hospital integrated delivery network in Western New York that includes Rochester Health, Catholic Health, and Kaleida Health.

As a leader, I act as a liaison between sales and operations to deliver cutting-edge solutions per the “Voice of the Customer” – both internal and external. The patient comes first. It is my passion to provide each and every customer with services and products of uncompromising quality – error free, on time, every time. In addition, I collaborate with strategic partnerships to mutually penetrate new markets and deliver the most innovative technologies that enhance patient care and provide value to my customers. Combined with my strong hospital operations and cross-functional skills, I have the unique ability to proactively relate to every provider, contact and department within an IDN, maximizing each opportunity while nurturing mutually beneficial, long-term business relationships.

35

Personal Mission Statement: The Voice Of The Customer – Cont. My goals and strengths are completely aligned with Laboratory Corporation of America’s (LCA) Five Pillar Strategy. I am an advocate of personalized medicine, companion diagnostics, population health management, and connected communities of health interoperability. As the industry leader and a premier healthcare services company, LCA is well positioned through enhanced IT and connectivity solutions with over 41 percent of revenue generated from esoteric testing through its Core Testing and Integrated Specialty Testing Groups. I am confident that LCA will enhance its footprint as a trusted partner to stakeholders, providing knowledge to optimize decision making, improve health outcomes, reduce treatment costs, and continue to revolutionize healthcare. These are the core reasons that I am seeking career opportunities with LCA.

Poised for advanced challenges, I look forward to contributing to LCA’s success through my outstanding leadership. I am seeking progressive challenges and responsibilities that will enable me to proactively utilize my vast wealth of knowledge and experience. Most importantly, I want to be a driving force that will enable LCA to execute its Mission through its Five Pillar Strategy.

Dedicated, self-driven, focused, and results oriented; always one step ahead of the challenge and two steps ahead of the competition!!!

Anthony E. Fanelli

36

Key Points Summary: Why LabCorp? • Industry leader and critical position in health care

delivery system • Alignment of goals, strengths and cultures • Mission & Five Pillar Strategy • Leadership in personalized medicine & companion

diagnostics • Clinical Trials leadership and partnerships • Commitment to the “Voice of the Customer” • IT and connectivity solutions • Limited government exposure • Managed care contracts • Economies of scale – most efficient provider • Proactive approach to Health Care Reform • Well positioned to gain share • Superb career opportunity!

37

Key Points Summary: My Value to LabCorp • Over 28 years of industry experience

• Proven producer and winner

• Versatile leader and team player

• P & L and territory management expertise

• IT and connectivity proficiency

• Cross-functional leadership acumen

• Leadership Tools

• Growth & Retention Tools

• IDN Business Development Strategies

• Proactive approach to Health Care Reform

• Commitment to the “Voice of the Customer”

38