leadingage 2015 - repositioning skilled nursing

TRANSCRIPT

Repositioning Skilled Nursing: Opportunity and Challenge

Joe Wagman, Chairman – Wagman Construction, Inc.Susan Brecht, President – Brecht Associates

Rick Barger, EVP, Treasurer – Diakon Lutheran Social MinistriesRebecca Townsend, Chief Strategy Officer – Covenant Health Network

Session Overview

• Joe Wagman - Background

• Susan Brecht - Market Trends

• Rick Barger – Diakon’s Response

• Rebecca Townsend - Strategic Issues

• Discussion

Background

• Repositioning/Reconsidering

o 2014 LeadingAge session

o Cost of care rising• ICD – 10 (administrative costs and coding errors)

• Staff shortages

• EMR

• Regulatory reporting

Background

• Repositioning/Reconsidering

o Competition increasing

• For-Profits (Medicare)

• Hospitals

• Other CCRCs

• Home Health & Hospice

Background

• Repositioning

o Private pay declining

o Sales of stand alones

o New SNF’s less common

o ‘Small House’ phases

o Remodels – buying time

o Segregating STC

Background

• Alternative ideas

o Exit? – Resident expectations

o Central facilities for system or affiliation?

o STC separate business line from LTC – physically separate STC from LTC re quality measures?

o Outsource STC and LTC?

Nursing Homes: Changing World

Susan Brecht

Nursing Homes: Changing World

• High demand for renovating or rebuilding nursing homes

• Average nursing home is 45 years old

• Capital available through HUD, REITs, commercial banks, private equity investors

• Just under 30% owned by single-site providers

• There is and will be increasing competition from traditional providers and hospitals

Changes May Include

• Overall upgrade of common spaces, hallways, room décor• Conversion to more private rooms• Converting or developing dedicated post-acute/sub-acute units• Dedicated short term rehab sections with all private rooms and high

level amenitieso Flat screen TVo Upgraded furnishingso Separate diningo Separate entranceo High-quality rehab facilities

• New homes average 725 SF per bed total size 2x size of existing facilities

Prominence of For-Profits

• Nearly 75% of investment grade nursing homes are owned by for-profit entities

• For-profits may be ahead of the game because of ready access to capital through a wide variety of funding sources, and ability to act quickly to access those sources

• REITs have played active role in acquisition of nursing home portfolios

The Green House™

• Now 12 years old• Serves 10-12 people in

single story design that looks like real home

• Current 183 homes across 139 organizations

• 60% are willing to pay more• 73% willing to drive further• Other models include small

houses and neighborhood design

http://thegreenhouseproject.org/green-house-model

Mainstreet – Next Generation

• Based in Carmel, IN

• Has built 25 new projects in 5 states

• Has another 50 projects in 11 states under development

• Typically 75-100 licensed SNF units + 30 assisted living units

• Focuses primarily on transitional care

• Do not take long term care patients

• Average length of stay 20 days

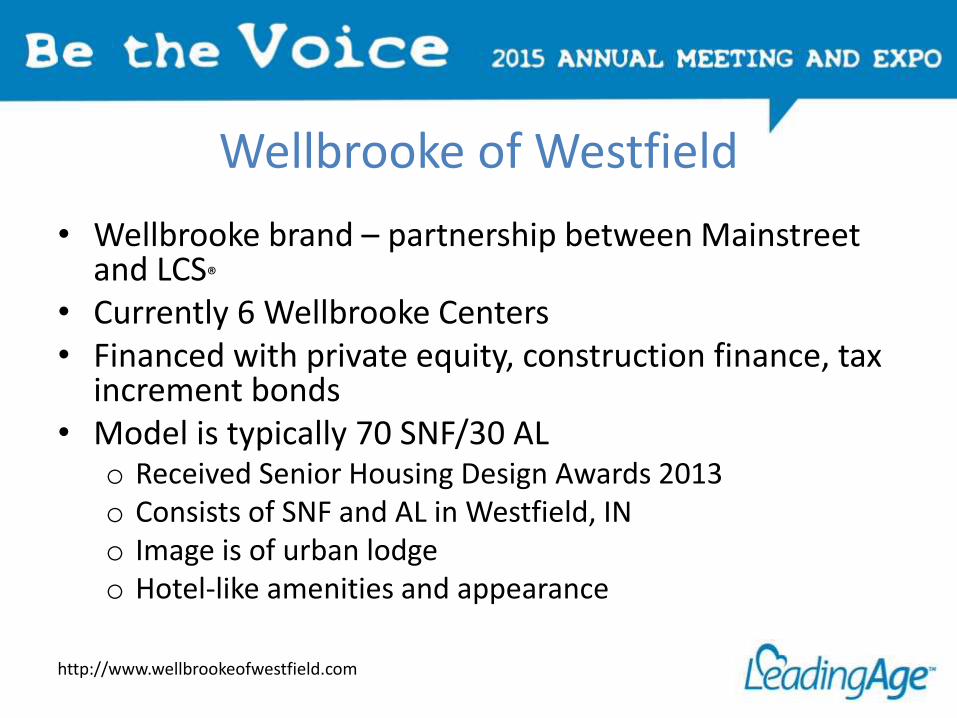

Wellbrooke of Westfield

• Wellbrooke brand – partnership between Mainstreet and LCS®

• Currently 6 Wellbrooke Centers• Financed with private equity, construction finance, tax

increment bonds• Model is typically 70 SNF/30 AL

o Received Senior Housing Design Awards 2013o Consists of SNF and AL in Westfield, INo Image is of urban lodgeo Hotel-like amenities and appearance

http://www.wellbrookeofwestfield.com

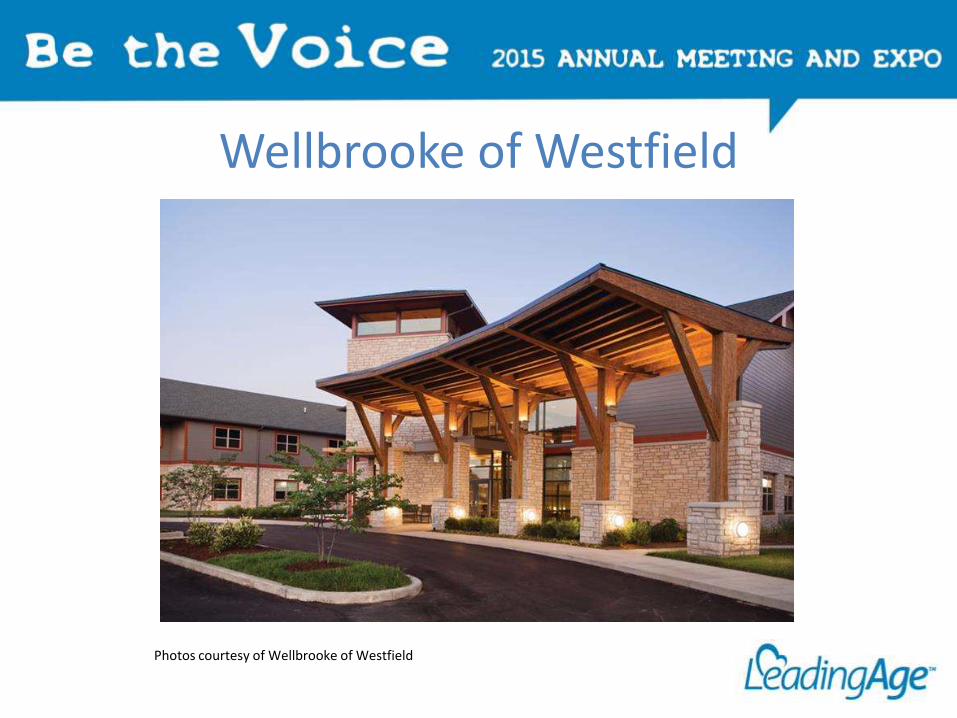

Wellbrooke of Westfield

Photos courtesy of Wellbrooke of Westfield

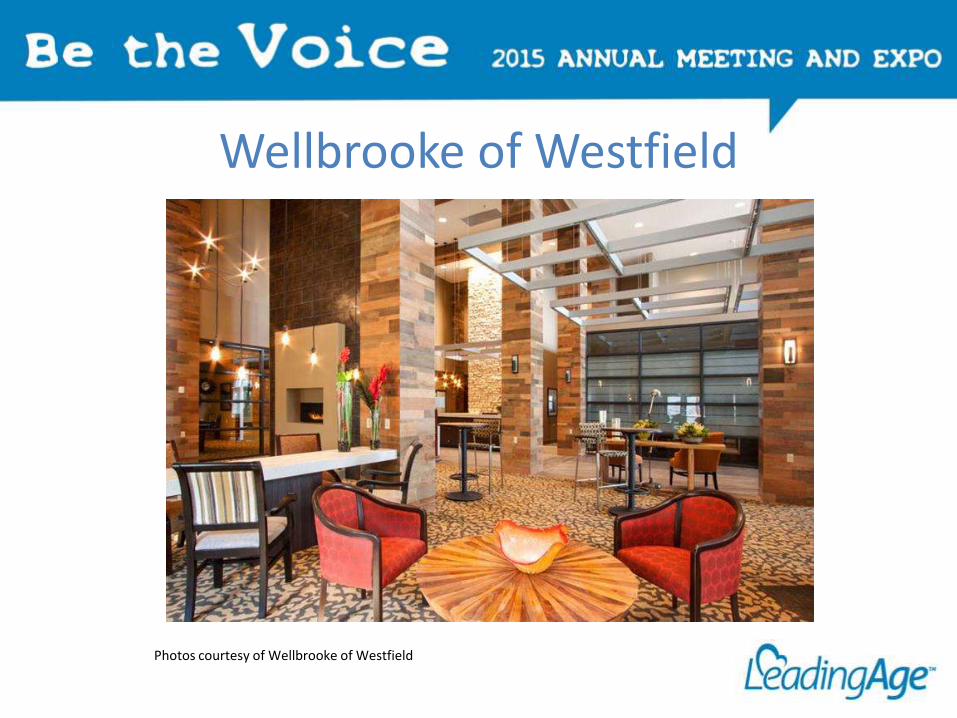

Wellbrooke of Westfield

Photos courtesy of Wellbrooke of Westfield

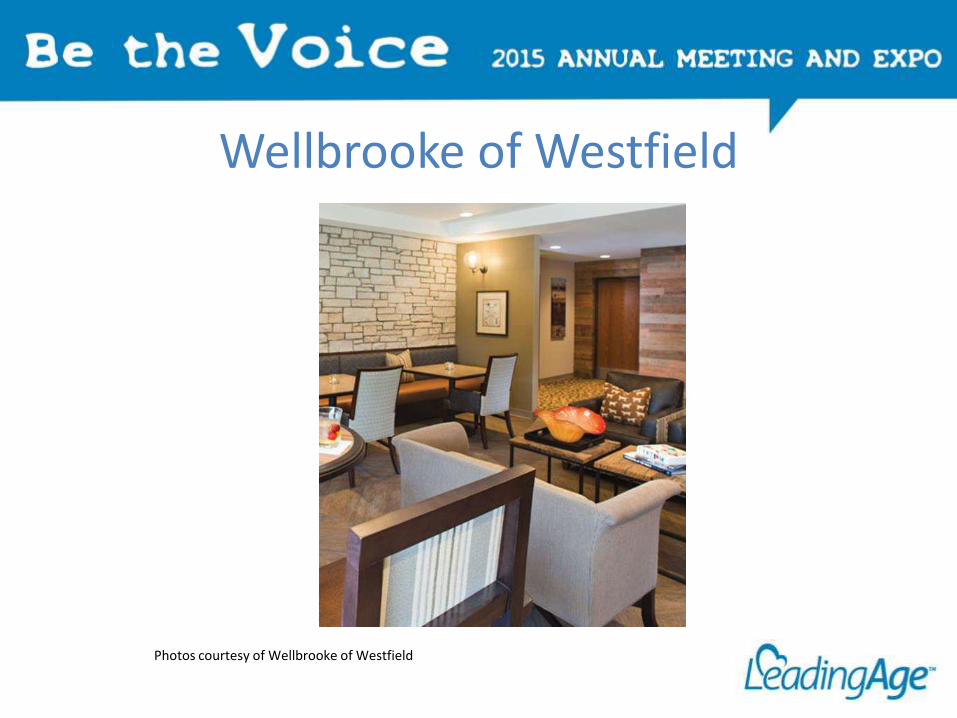

Wellbrooke of Westfield

Photos courtesy of Wellbrooke of Westfield

Genesis Powerback Rehabilitation Centers

• Short-term rehab concept – about 124 private rooms• Currently 10 PowerBack Centers• “1-2-4 Promise” assessed within 1 hour meets therapist within 2 hours See doctor within 4 hours.

• Length of stay 14-16 days• Patient education after discharge and follow-up• Powerback Rehabilitation card• Emphasis is on client being in control

http://www.powerbackrehabilitation.com

Survey of Providers

• We conducted a survey of providers including most of you here today

• Survey addressed:o Short term rehab vs. long term care

o Source of admissions

o Changes in size of SNF

o Remodeling/renovation

o ACOs

• We received 72 responses

Short Term Rehab

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

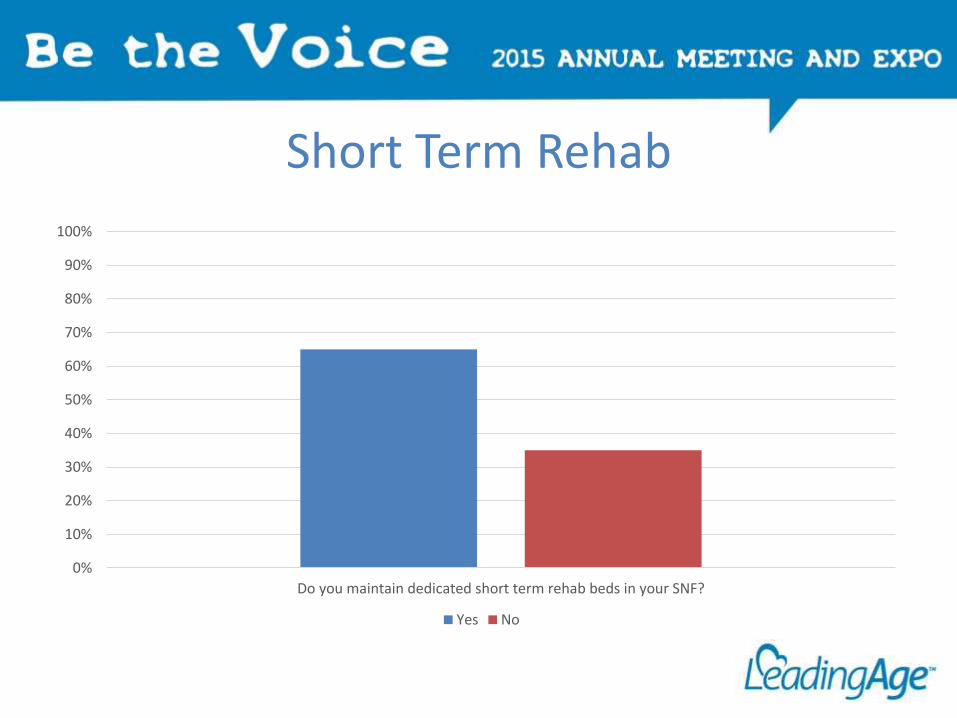

Do you maintain dedicated short term rehab beds in your SNF?

Yes No

Short Term Rehab

• 77% say short term rehab admissions have increased in the last three years

• Only 23% say they have more SNF beds than they need

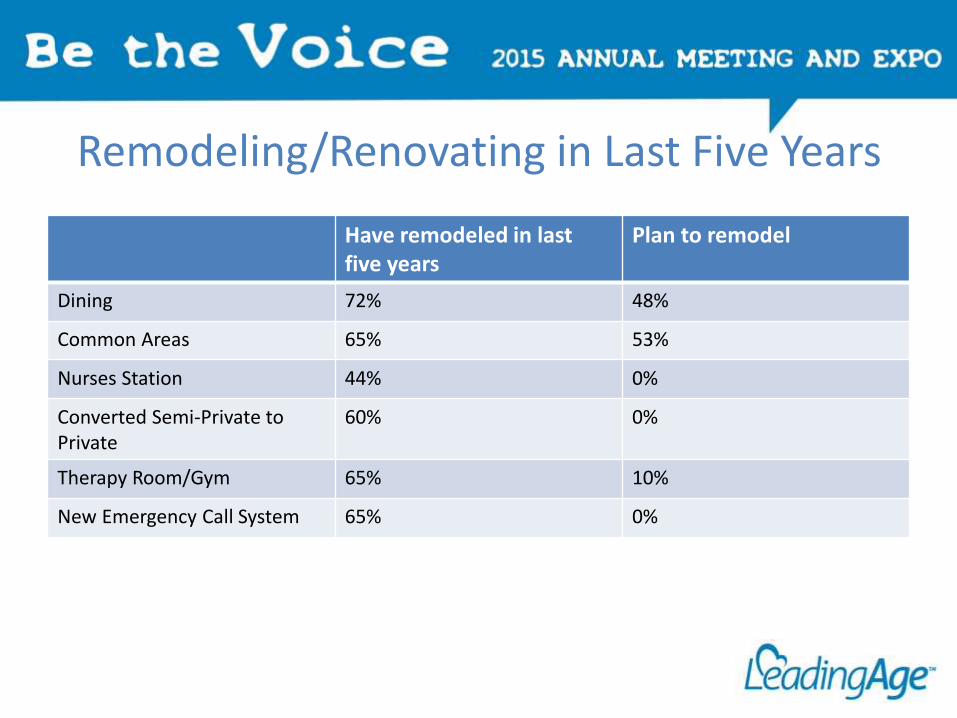

Remodeling/Renovating in Last Five Years

Have remodeled in last five years

Plan to remodel

Dining 72% 48%

Common Areas 65% 53%

Nurses Station 44% 0%

Converted Semi-Private to Private

60% 0%

Therapy Room/Gym 65% 10%

New Emergency Call System 65% 0%

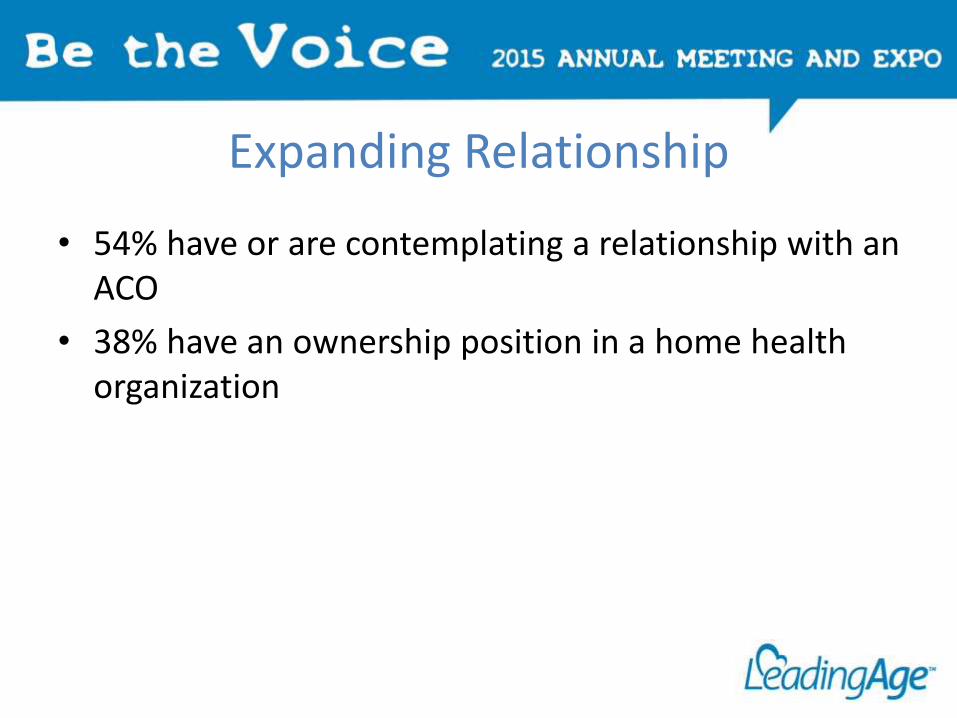

Expanding Relationship

• 54% have or are contemplating a relationship with an ACO

• 38% have an ownership position in a home health organization

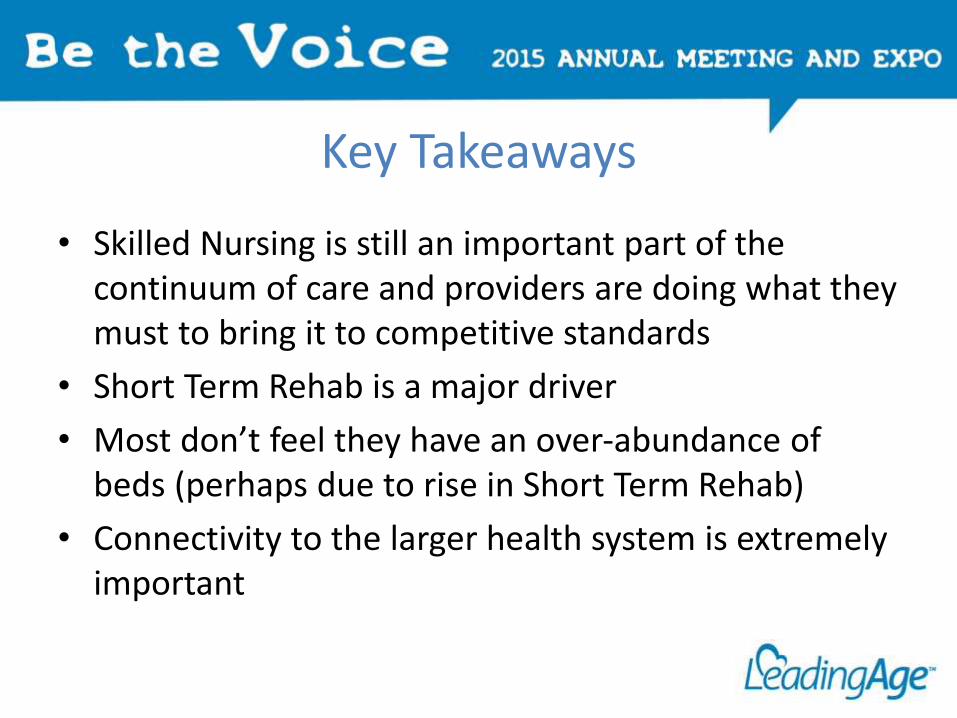

Key Takeaways

• Skilled Nursing is still an important part of the continuum of care and providers are doing what they must to bring it to competitive standards

• Short Term Rehab is a major driver

• Most don’t feel they have an over-abundance of beds (perhaps due to rise in Short Term Rehab)

• Connectivity to the larger health system is extremely important

Diakon’s Response to the Changing SNF Environment

Rick Barger

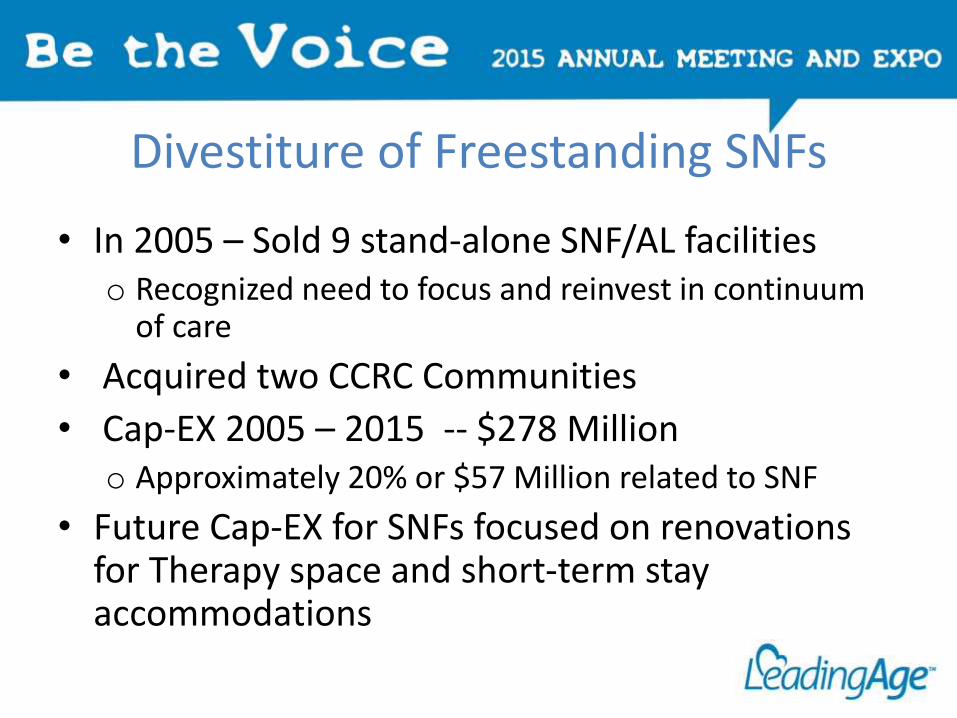

Divestiture of Freestanding SNFs

• In 2005 – Sold 9 stand-alone SNF/AL facilitieso Recognized need to focus and reinvest in continuum

of care

• Acquired two CCRC Communities

• Cap-EX 2005 – 2015 -- $278 Milliono Approximately 20% or $57 Million related to SNF

• Future Cap-EX for SNFs focused on renovations for Therapy space and short-term stay accommodations

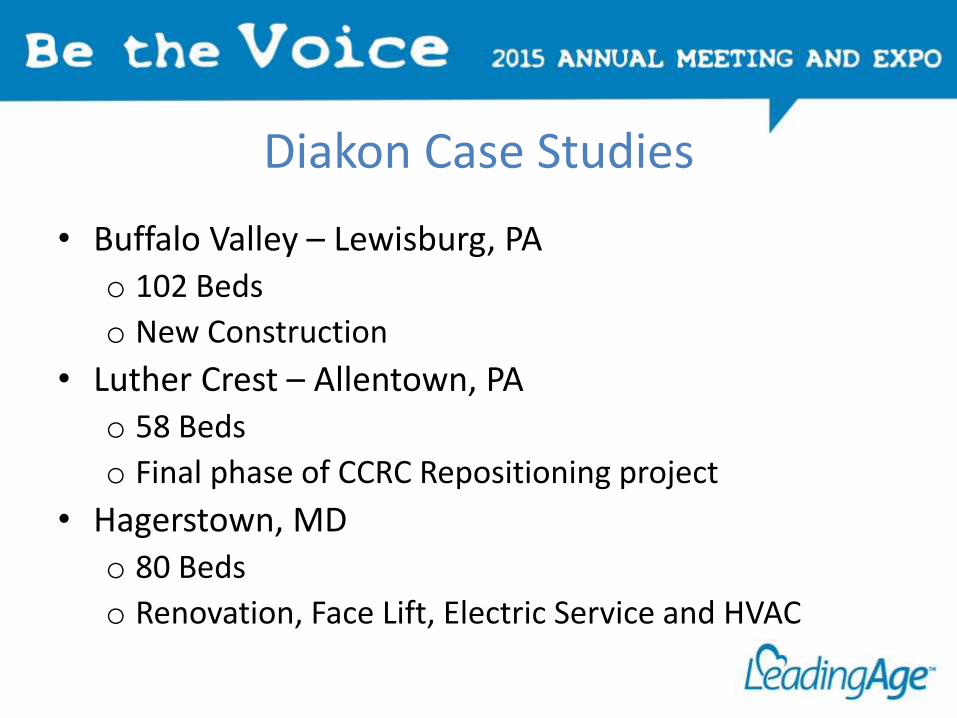

Diakon Case Studies

• Buffalo Valley – Lewisburg, PAo 102 Beds

o New Construction

• Luther Crest – Allentown, PAo 58 Beds

o Final phase of CCRC Repositioning project

• Hagerstown, MDo 80 Beds

o Renovation, Face Lift, Electric Service and HVAC

Diakon Case Studies

• Reason we chose to build new vs. renovate

• Challenges of renovating while continuing operations

• Before and after challenges and results

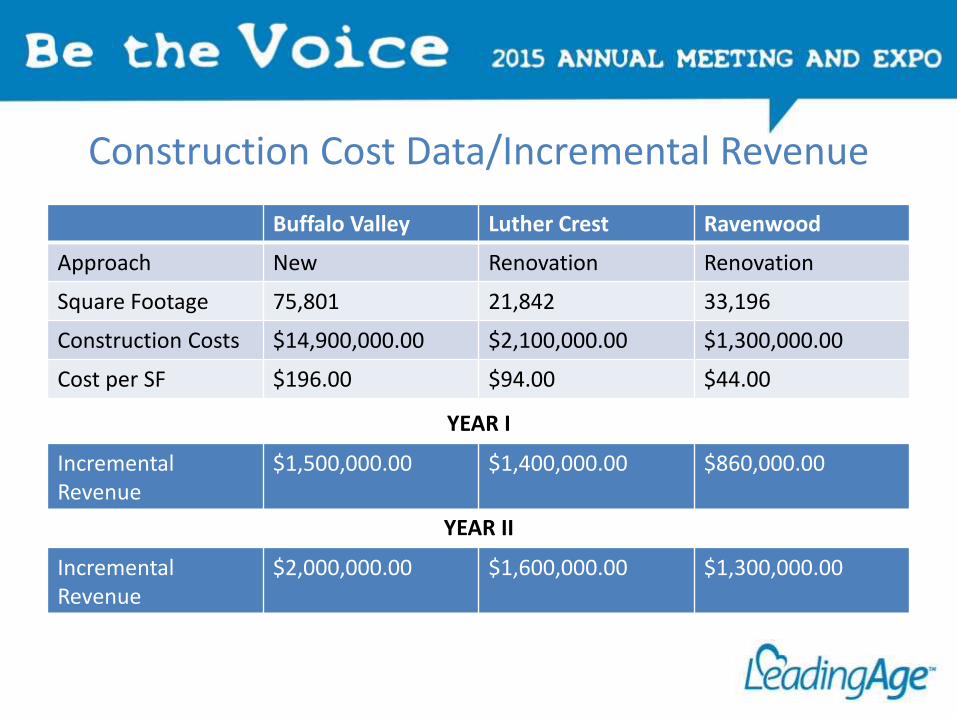

Construction Cost Data/Incremental Revenue

Buffalo Valley Luther Crest Ravenwood

Approach New Renovation Renovation

Square Footage 75,801 21,842 33,196

Construction Costs $14,900,000.00 $2,100,000.00 $1,300,000.00

Cost per SF $196.00 $94.00 $44.00

Incremental Revenue

$1,500,000.00 $1,400,000.00 $860,000.00

YEAR I

Incremental Revenue

$2,000,000.00 $1,600,000.00 $1,300,000.00

YEAR II

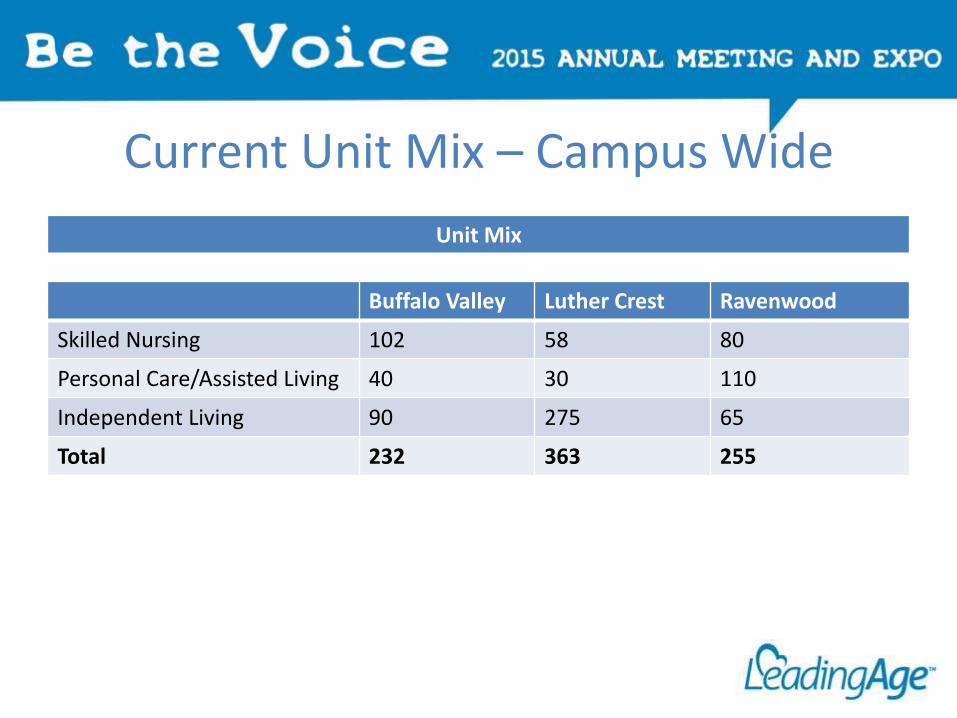

Current Unit Mix – Campus Wide

Unit Mix

Buffalo Valley Luther Crest Ravenwood

Skilled Nursing 102 58 80

Personal Care/Assisted Living 40 30 110

Independent Living 90 275 65

Total 232 363 255

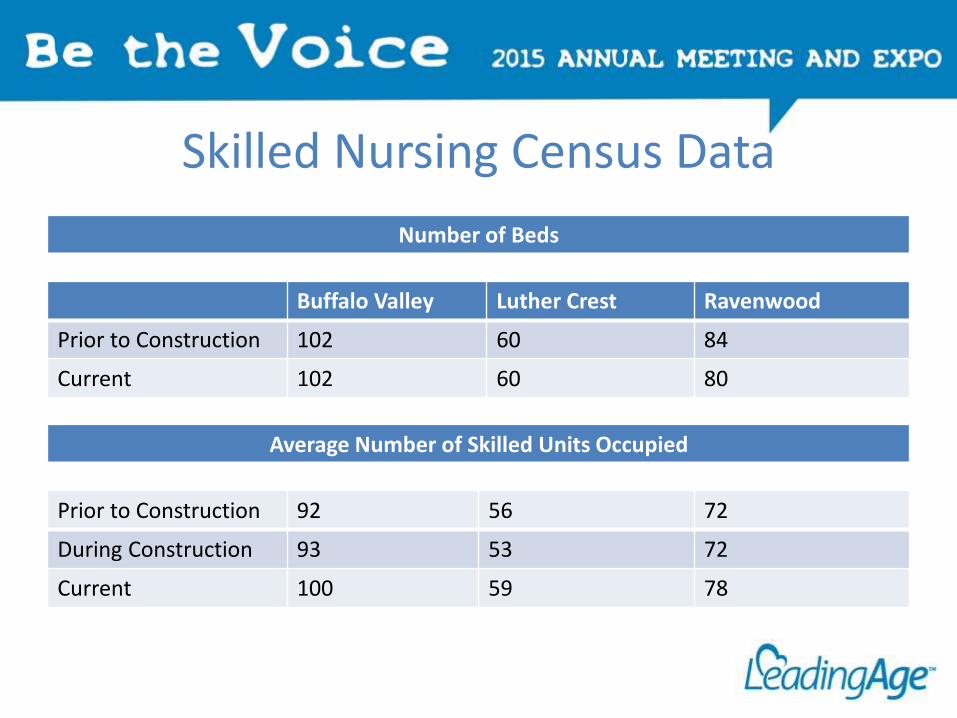

Skilled Nursing Census Data

Number of Beds

Buffalo Valley Luther Crest Ravenwood

Prior to Construction 102 60 84

Current 102 60 80

Average Number of Skilled Units Occupied

Prior to Construction 92 56 72

During Construction 93 53 72

Current 100 59 78

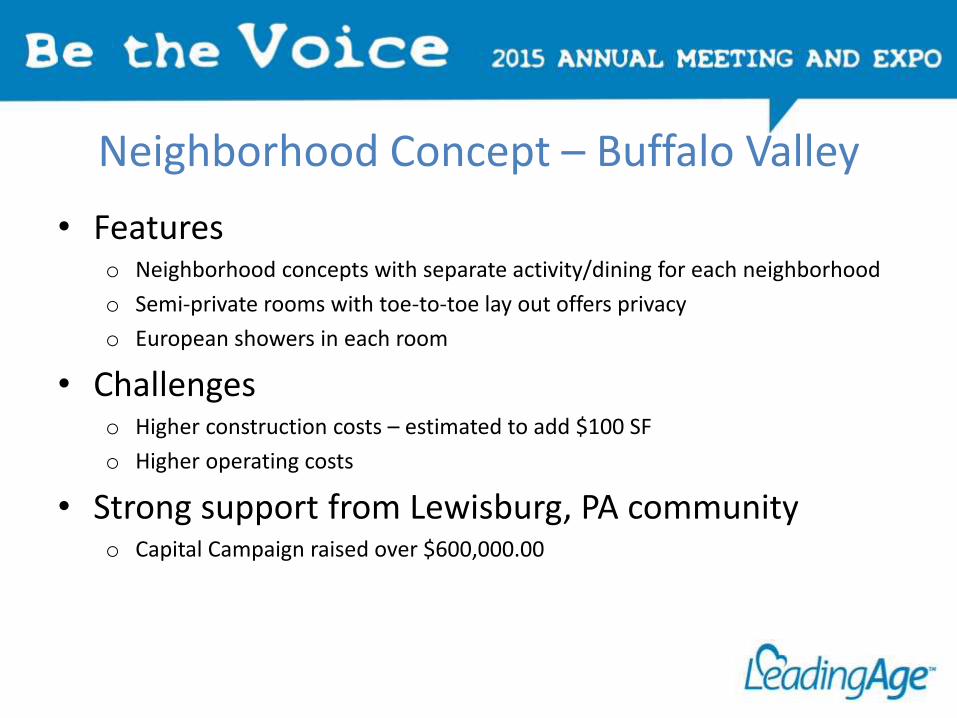

Neighborhood Concept – Buffalo Valley

• Featureso Neighborhood concepts with separate activity/dining for each neighborhood

o Semi-private rooms with toe-to-toe lay out offers privacy

o European showers in each room

• Challengeso Higher construction costs – estimated to add $100 SF

o Higher operating costs

• Strong support from Lewisburg, PA communityo Capital Campaign raised over $600,000.00

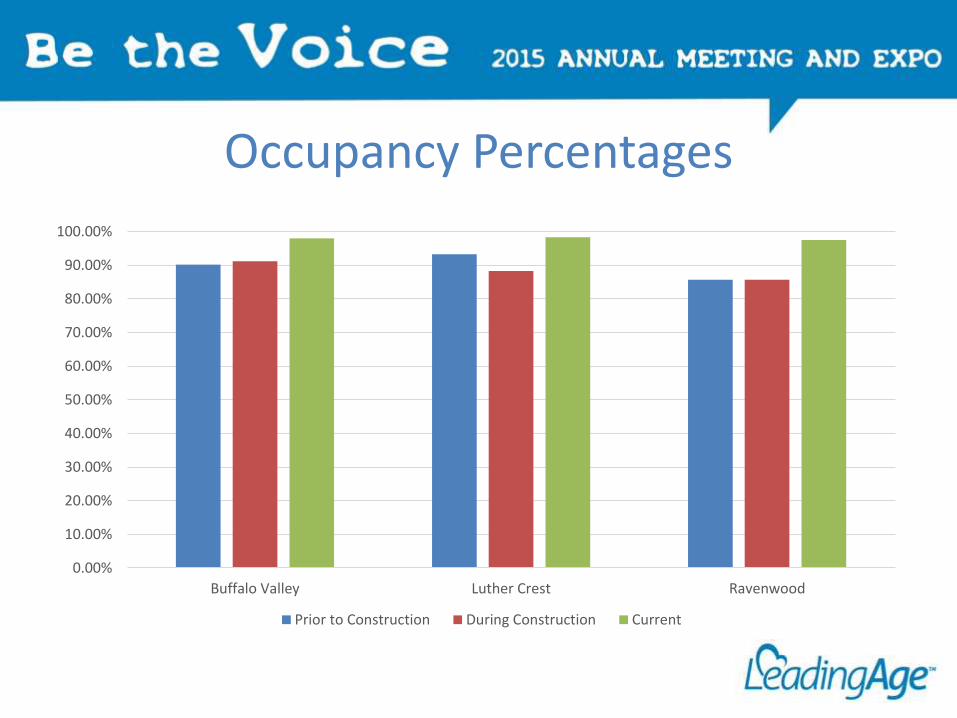

Occupancy Percentages

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Buffalo Valley Luther Crest Ravenwood

Prior to Construction During Construction Current

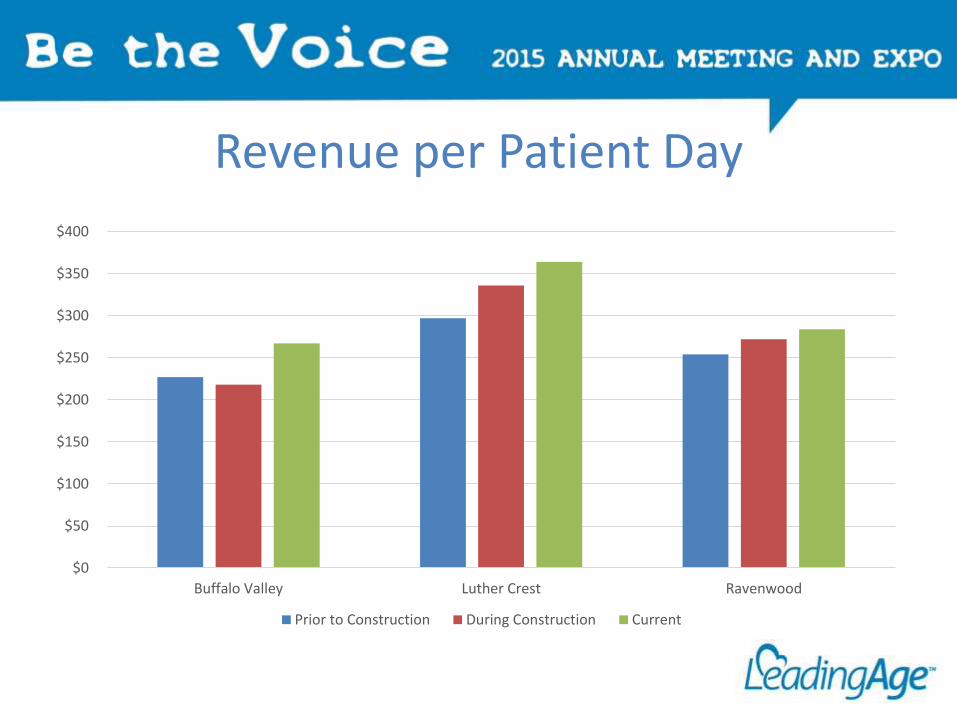

Revenue per Patient Day

$0

$50

$100

$150

$200

$250

$300

$350

$400

Buffalo Valley Luther Crest Ravenwood

Prior to Construction During Construction Current

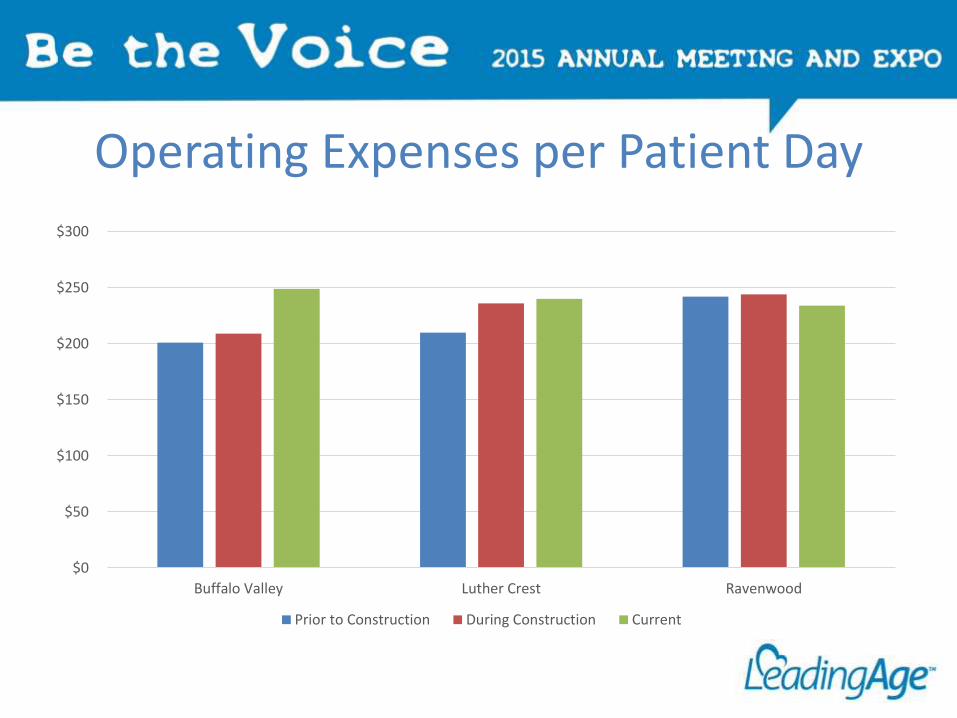

Operating Expenses per Patient Day

$0

$50

$100

$150

$200

$250

$300

Buffalo Valley Luther Crest Ravenwood

Prior to Construction During Construction Current

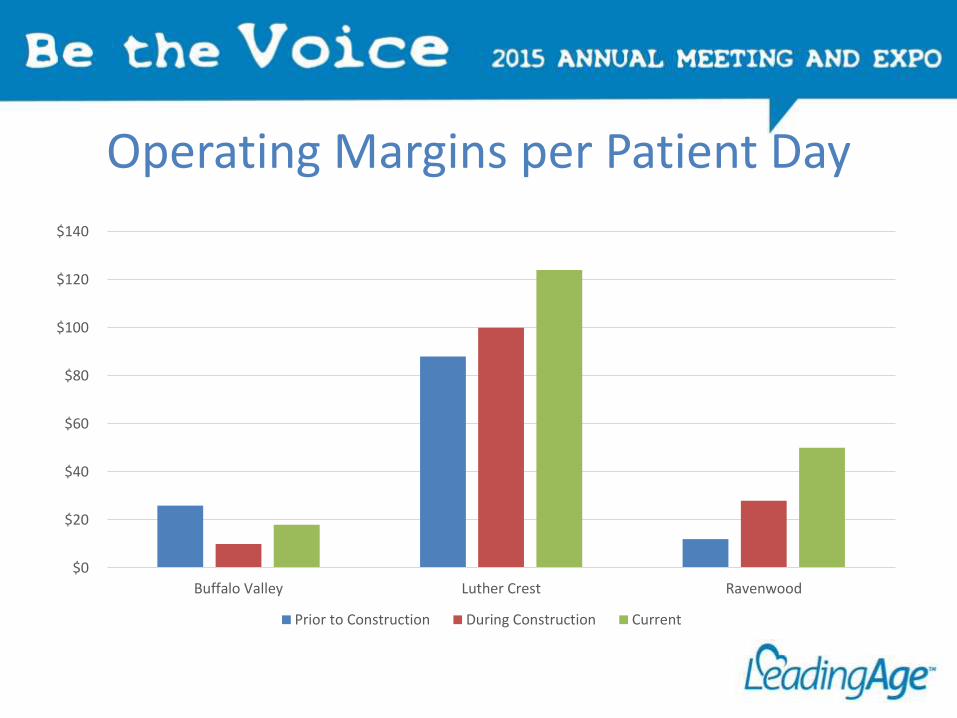

Operating Margins per Patient Day

$0

$20

$40

$60

$80

$100

$120

$140

Buffalo Valley Luther Crest Ravenwood

Prior to Construction During Construction Current

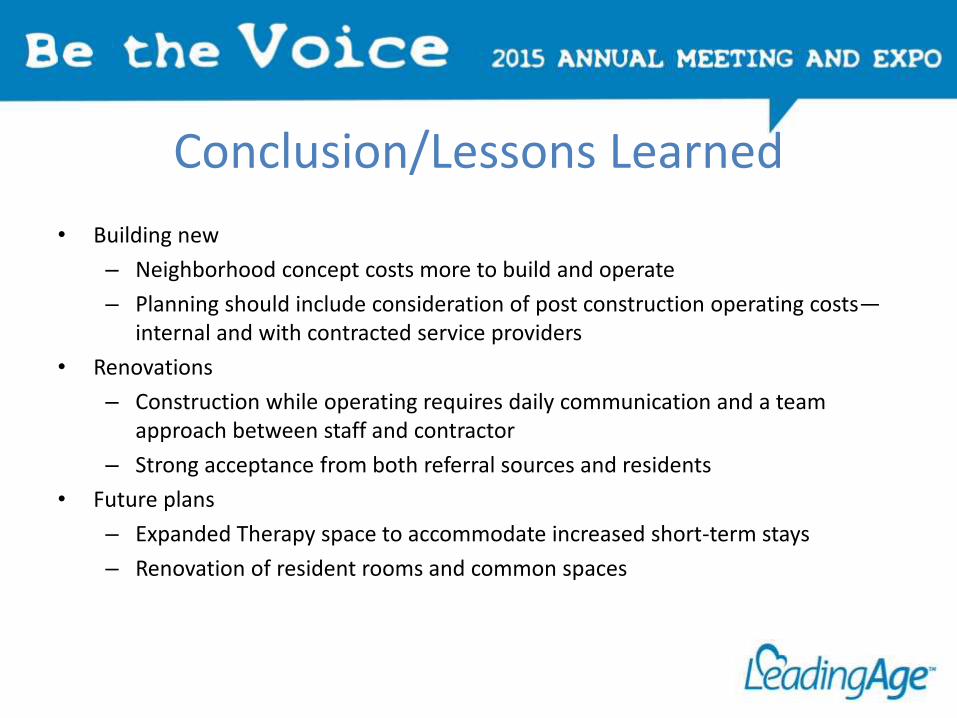

Conclusion/Lessons Learned

• Building new

– Neighborhood concept costs more to build and operate

– Planning should include consideration of post construction operating costs—internal and with contracted service providers

• Renovations

– Construction while operating requires daily communication and a team approach between staff and contractor

– Strong acceptance from both referral sources and residents

• Future plans

– Expanded Therapy space to accommodate increased short-term stays

– Renovation of resident rooms and common spaces

SNF Related Strategies Arising out of ACO Dynamics

Rebecca Townsend

Impact of Change in Health Care Reform on Continuum of Care Models

• The “sea of change” is the issue of sharing risk as systems are now expected to manage their populations healtho Accountable Care Organizations

o Bundled Payment Models

o Medicare Advantage

o Medicaid Managed Care

o Acute Care Systems• Readmission Penalties

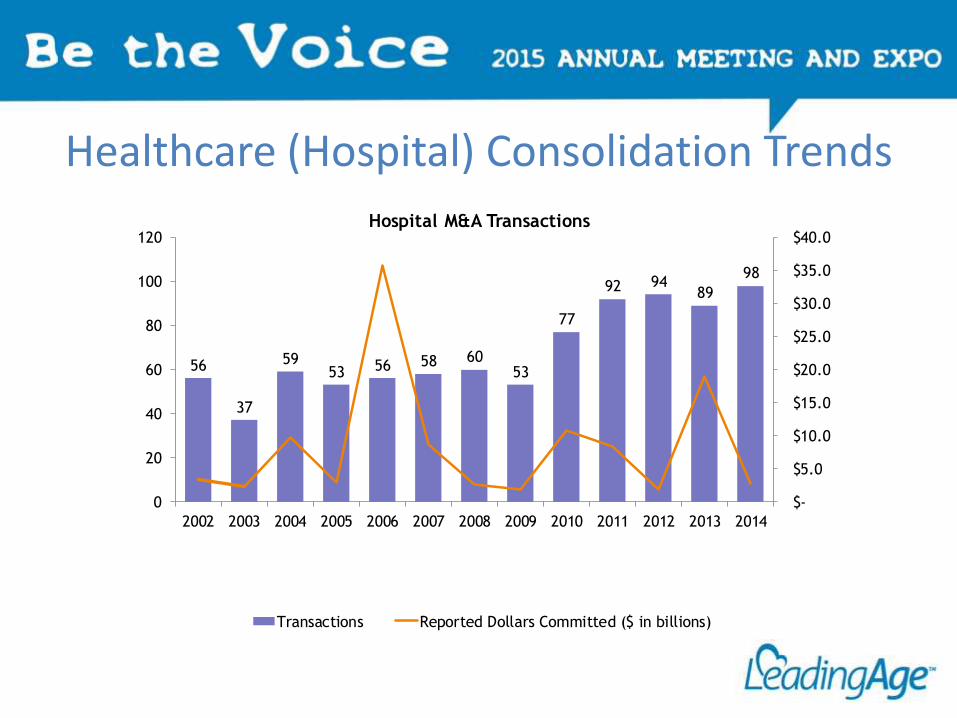

Healthcare (Hospital) Consolidation Trends

56

37

5953 56 58 60

53

77

92 9489

98

$-

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

0

20

40

60

80

100

120

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hospital M&A Transactions

Transactions Reported Dollars Committed ($ in billions)

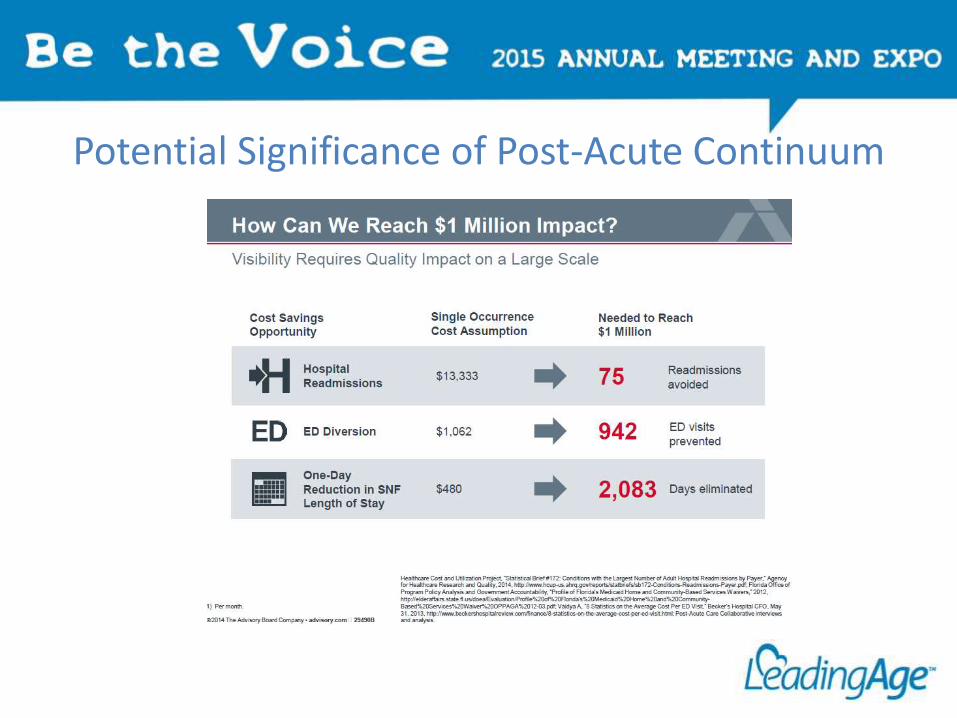

Potential Significance of Post-Acute Continuum

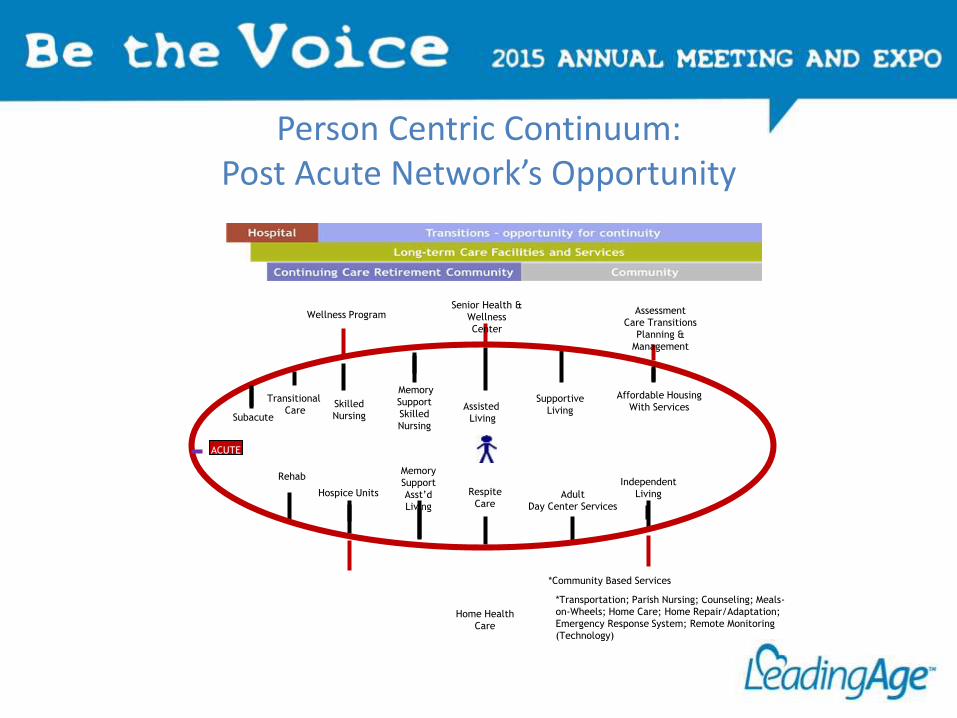

Person Centric Continuum:Post Acute Network’s Opportunity

Subacute

Rehab

Memory

Support

Skilled

Nursing

Respite

Care

Assisted

Living

Supportive

Living

Senior Health &

Wellness

Center

*Community Based Services

Wellness Program Assessment

Care Transitions

Planning &

Management

Independent

LivingAdult

Day Center Services

Memory

Support

Asst’d

Living

Home Health

Care

Skilled

Nursing

Hospice Units

ACUTE

Transitional

Care

*Transportation; Parish Nursing; Counseling; Meals-

on-Wheels; Home Care; Home Repair/Adaptation;

Emergency Response System; Remote Monitoring

(Technology)

Affordable Housing

With Services

Strategies to Assure Relevance

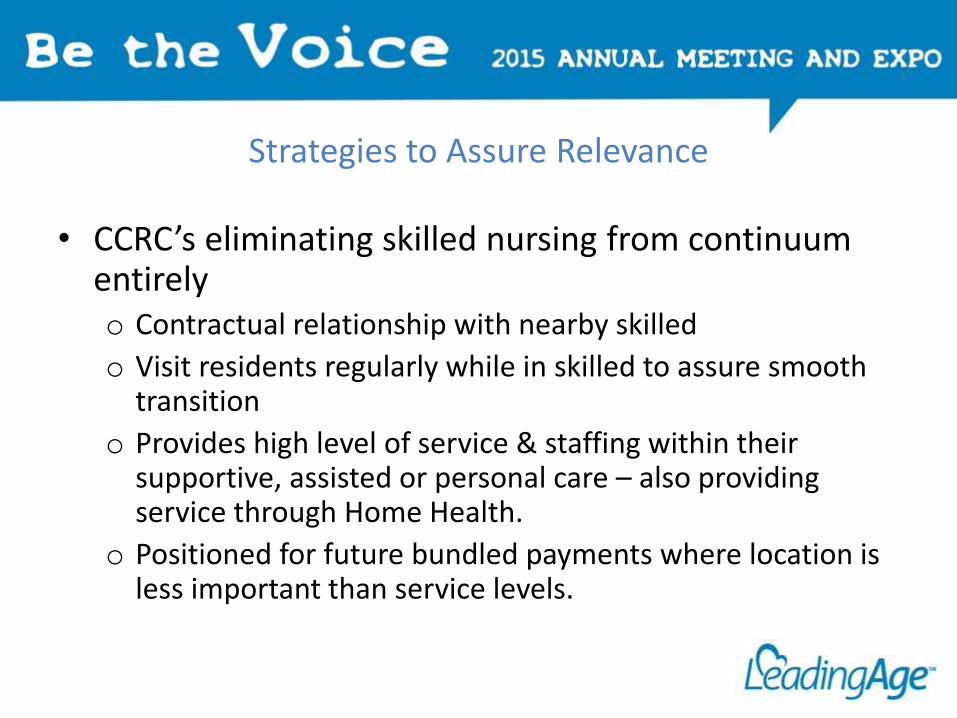

• CCRC’s eliminating skilled nursing from continuum entirelyo Contractual relationship with nearby skilled

o Visit residents regularly while in skilled to assure smooth transition

o Provides high level of service & staffing within their supportive, assisted or personal care – also providing service through Home Health.

o Positioned for future bundled payments where location is less important than service levels.

Strategies to Assure Relevance

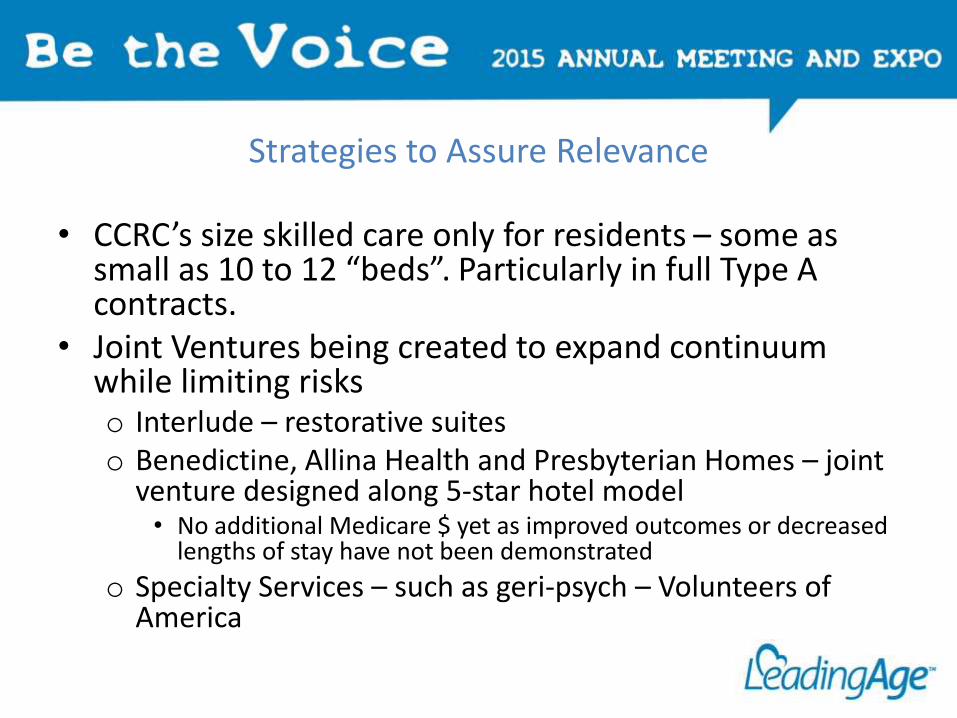

• CCRC’s size skilled care only for residents – some as small as 10 to 12 “beds”. Particularly in full Type A contracts.

• Joint Ventures being created to expand continuum while limiting riskso Interlude – restorative suiteso Benedictine, Allina Health and Presbyterian Homes – joint

venture designed along 5-star hotel model• No additional Medicare $ yet as improved outcomes or decreased

lengths of stay have not been demonstrated

o Specialty Services – such as geri-psych – Volunteers of America

Strategies to Assure Relevance

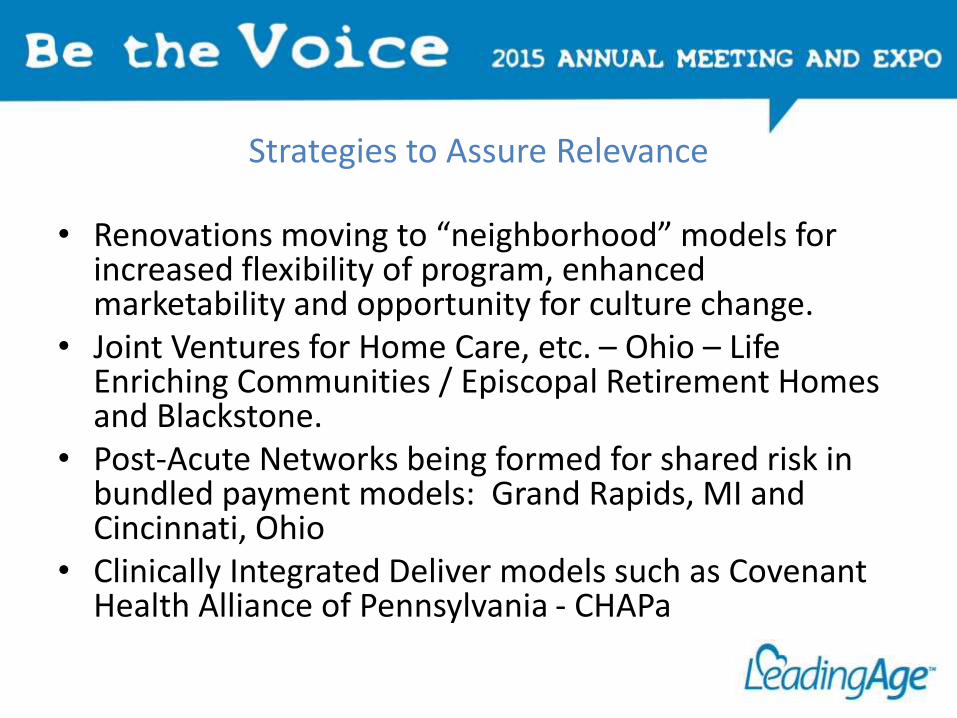

• Renovations moving to “neighborhood” models for increased flexibility of program, enhanced marketability and opportunity for culture change.

• Joint Ventures for Home Care, etc. – Ohio – Life Enriching Communities / Episcopal Retirement Homes and Blackstone.

• Post-Acute Networks being formed for shared risk in bundled payment models: Grand Rapids, MI and Cincinnati, Ohio

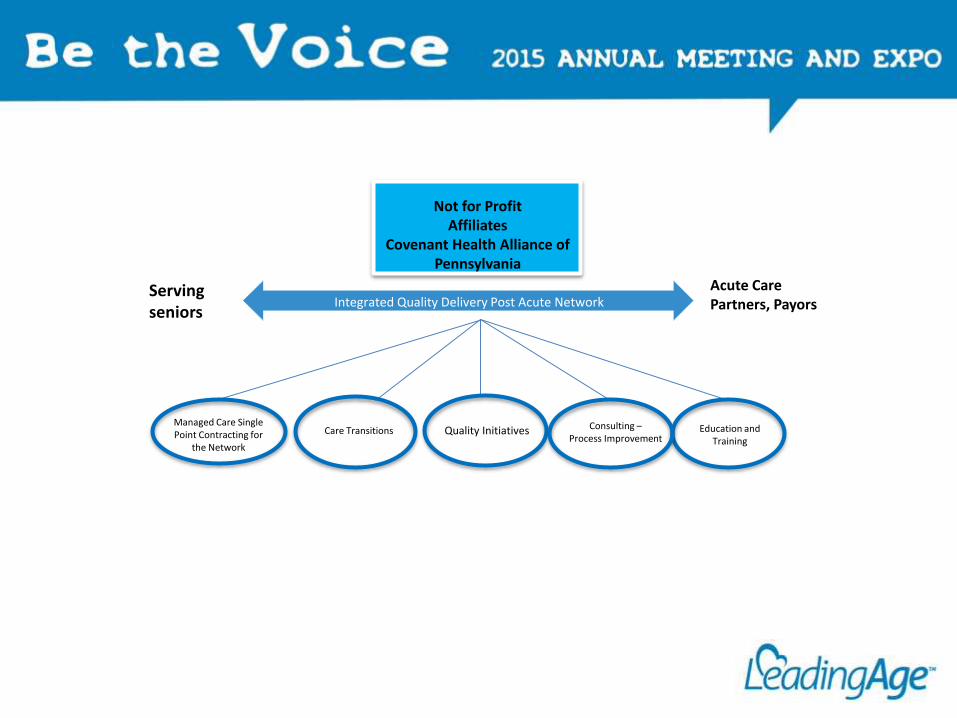

• Clinically Integrated Deliver models such as Covenant Health Alliance of Pennsylvania - CHAPa

Not for ProfitAffiliates

Covenant Health Alliance of Pennsylvania

Integrated Quality Delivery Post Acute Network Serving seniors

Acute Care Partners, Payors

Managed Care Single Point Contracting for

the Network

Care Transitions Quality Initiatives Consulting –Process Improvement

Education and Training

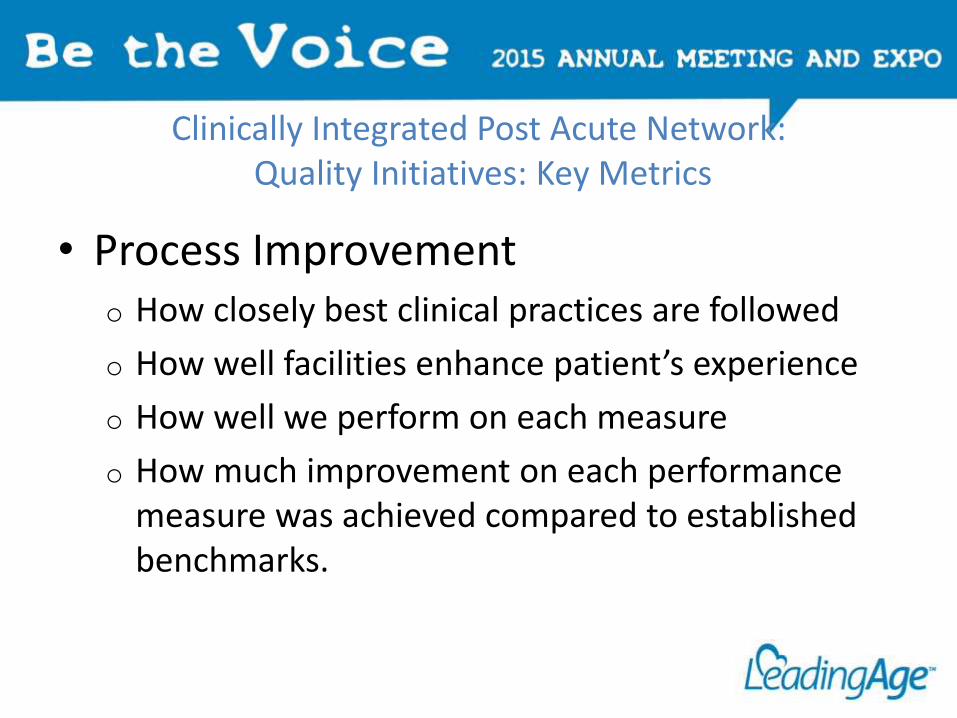

Clinically Integrated Post Acute Network:Quality Initiatives: Key Metrics

• Process Improvemento How closely best clinical practices are followed

o How well facilities enhance patient’s experience

o How well we perform on each measure

o How much improvement on each performance measure was achieved compared to established benchmarks.

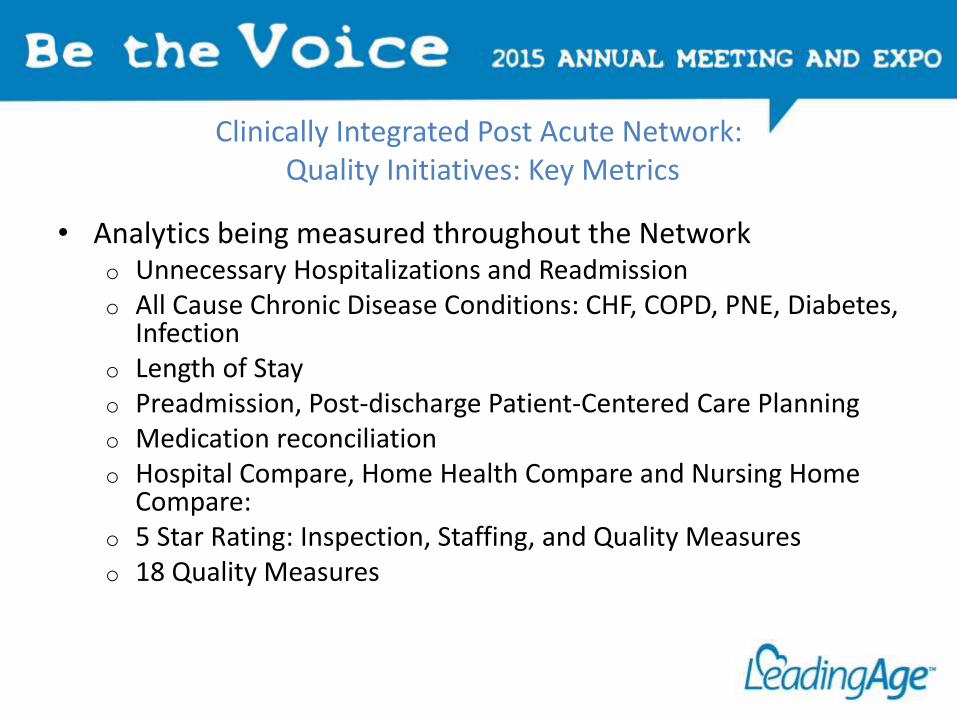

Clinically Integrated Post Acute Network:Quality Initiatives: Key Metrics

• Analytics being measured throughout the Networko Unnecessary Hospitalizations and Readmissiono All Cause Chronic Disease Conditions: CHF, COPD, PNE, Diabetes,

Infectiono Length of Stayo Preadmission, Post-discharge Patient-Centered Care Planningo Medication reconciliationo Hospital Compare, Home Health Compare and Nursing Home

Compare:o 5 Star Rating: Inspection, Staffing, and Quality Measures o 18 Quality Measures

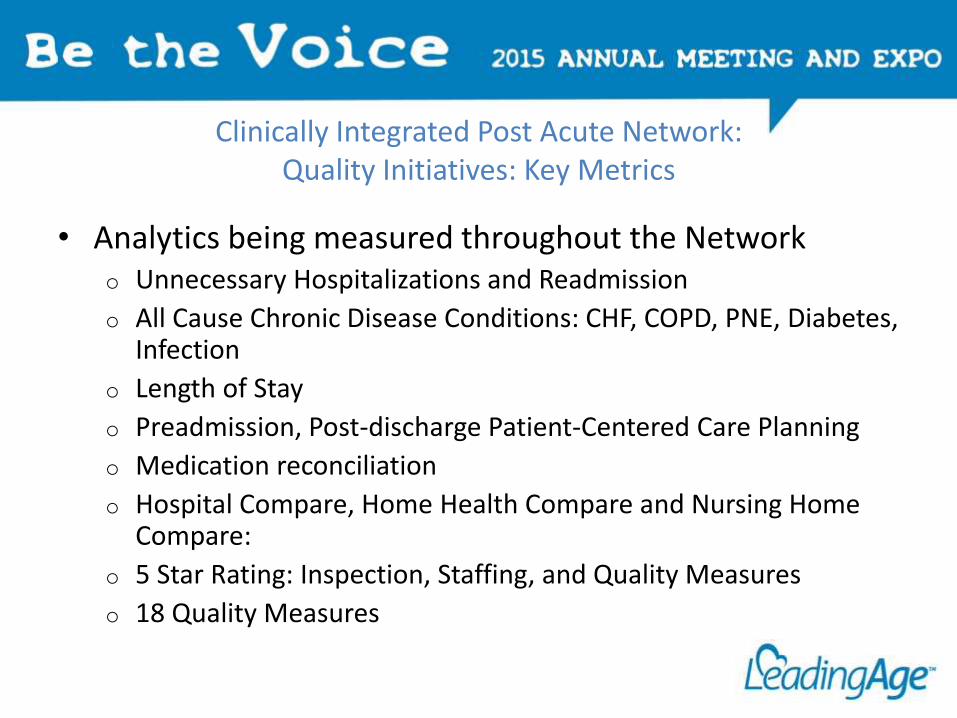

Clinically Integrated Post Acute Network: Quality Initiatives: Key Metrics

• Analytics being measured throughout the Networko Unnecessary Hospitalizations and Readmission

o All Cause Chronic Disease Conditions: CHF, COPD, PNE, Diabetes, Infection

o Length of Stay

o Preadmission, Post-discharge Patient-Centered Care Planning

o Medication reconciliation

o Hospital Compare, Home Health Compare and Nursing Home Compare:

o 5 Star Rating: Inspection, Staffing, and Quality Measures

o 18 Quality Measures

Clinically Integrated Post-Acute Health Network Additional Advantages

• Provides a single point of entry into continuum of serviceso Match need with capacity (skills and occupancy)o Match need regardless of location

• Skilled Nursing• Home Health• Hospice• Palliative• Home Care• Other

o Provide feedback regarding plan and outcomes

• Environment for study – UTI example, Pharmacy study, increase acuity, pay for performance

• Resident Satisfaction measures• Enhanced Informatics –role in support of collection, analysis and consolidation of

data.• Quality review ongoing for all members and business partners – process

improvement resources readily available when necessary.

As the landscape is changing…Opportunity

• Bundled Payment models offer opportunity to determine models of care and support with improved outcomes and reduced costs. Continuum providers are best suited to consider this model however risk concerns require mitigation. Perhaps a network or joint venture.

• Hospital systems and payors are just now beginning to acknowledge the significant role which senior service providers, particularly not for profit, can play for their health populations.

• Strategic repositioning of the continuum is essential – includes capital improvements, technology, message of measureable outcomes and redefinition of quality care.

Discussion