learnings from an advanced market - korean experiments - marketing insight by jin kook kim jenny i...

TRANSCRIPT

Learnings from an Advanced Market

- Korean Experiments -

Marketing Insight

by Jin Kook Kim Jenny I Jin Jang

ContentsI. Overview of the Korean Market

II. Research Design

III. Key Findings

IV. Conclusions and Implications

3/32

Introduction Overview of Korean Telecommunication Market

Why is Korea the Test Bed of Mobile Convergence?

Mobile Convergence Initiatives in the Korean Market

4/32

Overview of Korean Telecommunication Market

• The first country to adopt CDMA • Three domestic service providers (SK Telecom, KTF, LG Telecom)• Three major handset manufacturers (Samsung, LG, Pantech) • Handset purchase price: average 292 euros * • Mobile service charge: average 28.5 euros a month * • Communication expenses higher than: ‘education’, ‘medical care’

*Source: The 4th Syndicated Telecom Research by Marketing Insight (Sep. 2006)

• Low-end products/ Non camera phones• Prepaid billing system• Charge for receiving calls• Imported phones

Korea has almost No Market for:

Overview ofthe Korean market

5/32

19992000200120022003200420052006

MusicPhoneCamera

phone(Built-in)

Telematics(Phone)Mobile-

BankingS-DMB(phone)

T-DMB

HSDPA

Wibro

World’s first launch

Mobile Convergence Initiatives in the Korean Market

Overview ofthe Korean market

3.5 Generation

6/32

How Do Korean Consumers UseMobile Convergence Service?

1 Music CameraTelematic

s

Banking DMB HSDPA

Game2 3 4

5 6 7

Overview ofthe Korean market

7/32

MobileConvergence

- Government - Business- Media- Consumers

Necessity of new revenue streams for carriers

Obsessive atmosphere

What Makes Korea a Test Bed?

Overview ofthe Korean market

Solid IT infrastructure

Focus on premium handsets

8/32

Difference S-DMB T-DMBLaunched in May 2005 Dec. 2005

Governed by

Ministry of Information &

Communications

Ministry of Culture & Tourism

Law Telecommunicatio

nsBroadcasting

Operated byMobile service

providerBroadcasting

Corp.

Focus onSatellite

broadcastingTerrestrial

broadcastingProfit source

Subscription feeBased on

advertising

Price €11 Free

Further development of mobile convergence involves issues of diplomacy among various parties rather than technology.

Key Issue for theConvergence Market

Overview ofthe Korean market

9/32

Research Design

Study Purpose

Research Methodology

10/32

Study Content

Ongoing convergences in the Korean market11

Consumer responses to convergence22

Prospects for mobile convergence33

44 Prospects for Fixed-Mobile Convergence (FMC)

Research Design

11/32

UniverseUniverse

StudyFrequency

StudyFrequency

More than 100,000 mobile phone usersSample SizeSample Size

SamplingFrame

SamplingFrame

MajorContents

MajorContents

Overview of Syndicated Telecom Research (by Marketing Insight)

Mobile phone users aged 14-64

Conducted bi-annually since March 2005 (March and September)

Panel of Marketing Insight (0.6 million panelists) Members of major Internet portal sites

U&A Mobile Convergence CPQ (Consumer Perceived Quality)

Research Methodology

E-mail surveyData

CollectionData

Collection

Research Design

12/32

Buyer within6 months

RespondentsData

CollectionTime of purchase

4th

Wave4th

WaveAug 30 - Sep 15

2006100,901 21,015

Mar-Aug2006

3rd

Wave3rd

WaveMar 7 - 25

2006100,000 17,477*

Sep.2005-Feb.2006

2nd

Wave2nd

WaveSep 6 - 20

2005110,455 24,704

Mar-Aug 2005

1st

Wave1st

WaveMar 10 - Apr 4

2005100,779 24,212

Sep 2004 - Feb 2005

*Demand was temporarily low due to a mobile handset subsidy policy

Primary target is those who bought a handset within past 6 months.

Research MethodologyResearch Design

13/32

Mobile Convergence Market & Trends

Pricing

Prospect for FMC

Key Findings

14/32

Owner-ship

Use rate(Owners

)

Satisfaction rate among

users

Feature

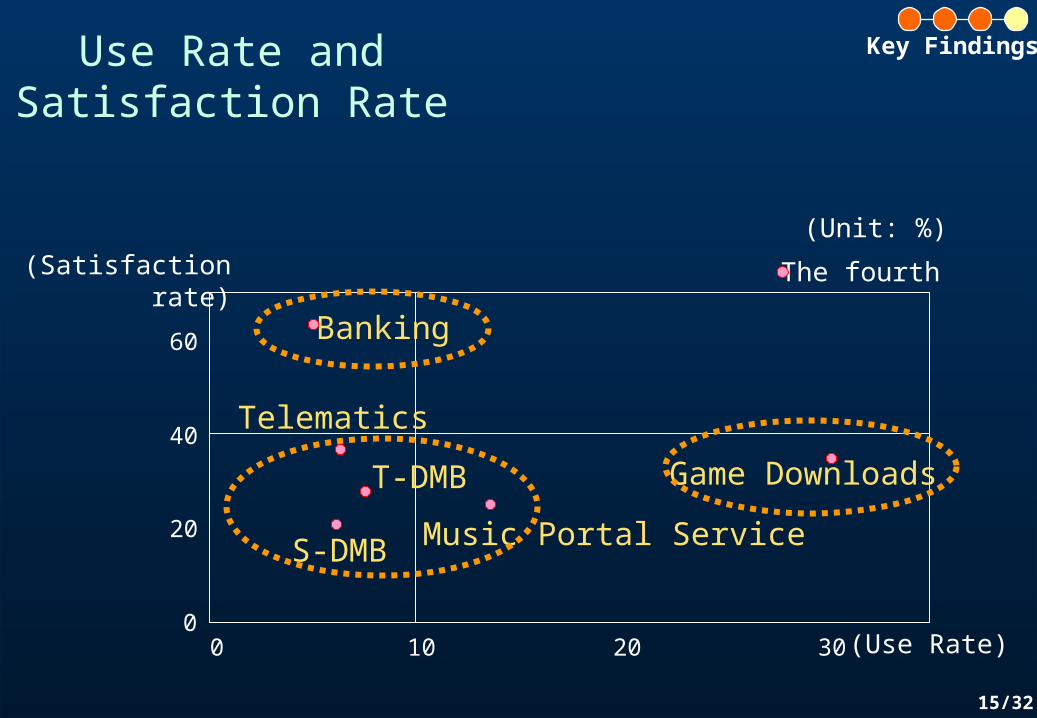

Camera 98 94 (95) 42 Music playback 89 62 (70) 50 Telematics 28 6 (23) 36 Banking 27 5 (19) 63 S-DMB 8 6 (75) 21 T-DMB 9 8 (80) 28 HSDPA 0.4 0.2 (57) - Wibro - - -

Service

Game download service

- 30 35

Music portal service - 14 25

(Base: Buyer within past 6 months, Unit: %)

Penetration, Use Rate andSatisfaction Rate

Key Findings

15/32

Telematics

Banking

T-DMB

S-DMB Music Portal Service

Game Downloads

(Use Rate)

(Satisfactionrate)

(Unit: %)

The fourth

0

20

40

60

0 10 20 30

Use Rate andSatisfaction Rate

Key Findings

16/32

Telematics

Banking

T-DMBS-DMB

Music Portal Service

Game Downloads

(Use Rate)

(Satisfactionrate)

(Unit: %)

The fourth The third

0

20

40

60

0 10 20 30

Changes in Consumers’Responses to Convergence

Key Findings

17/32

Reasons for Dissatisfaction withConvergence Service

S-DMBS-DMB

%Dis-satisfied Price*

Major reasons for dissatisfaction

*Monthly fee (as of Sep. 2006)

Price Content Quality Convenience

51%€11

T-DMBT-DMB Free 48%

MusicMusic €4 37%

GameGame 19%**

TelematicsTelematics€8-15 15%

BankingBanking €0.7 8%

** Charged per download: data + call charge

Key Findings

18/32

Use (intention) rate

Use rate (a)Intention rate (b)

Gap (b-a)

Banking 5 37 32

T-DMB 8 34 26

Telematics 6 24 18

S-DMB 6 11 5

Music portal 14 14 0.4

Wibro - 32 -

HSDPA - 26 -

Market potential based on a comparison of current use andfuture use intention (Unit: %)

Prospects for theConvergence Market

Key Findings

19/32

0

20

40

60

0 10 20 30 40

Telematics

Banking

T-DMB

S-DMBMusic portal

(Use/Intention Rate)

(Satisfactionrate)

(Unit: %)

Prospects for theConvergence Market

The fourthThe third Intention

HSDPA Wibro

Key Findings

20/32

Current price(monthly fee)

as of Sep. 2006

Price willing to pay

Current users

Intenders

Telematics 8 - 15 2.0 2.3 Banking 0.7 0.7 1.5 S-DMB 11 3.9 4.7 T-DMB Free 2.1 2.4 Music portal 4 2.0 2.1 HSDPA 10 - 42 - 5.7 Wibro 13 - 25 - 4.8

(Unit: Euro)

<<<<<

Intenders are willing to pay slightly more than current users.

Acceptable price for users is estimated to be €2, much lower than the current price.

Price Acceptance for EachConvergence Service

<

<

<<

=

Key Findings

21/32

0

2

4

6

8

10

12

14

16

0 10 20 30 40

Telematics

BankingT-DMB

S-DMB

Music portal

(Intention Rate, %)

(Price, €)(Base: Intenders)

Willing to pay Current price

Price Acceptance for EachConvergence Service

Intention Rate & Acceptable Price

Key Findings

HSDPA Wibro

22/32

E-mail 71Shopping 61

Messenger 55Blog/mini home page 51

On-line cafe/club 47Video service 45

......

(Unit: % MA)

Communication-centered + shopping

Entertainment-centered + e-mail

(Unit: % MA)

Music portal service 17E-mail 14

Video service 10Broadcasting service 8

Traffic information 8...

...

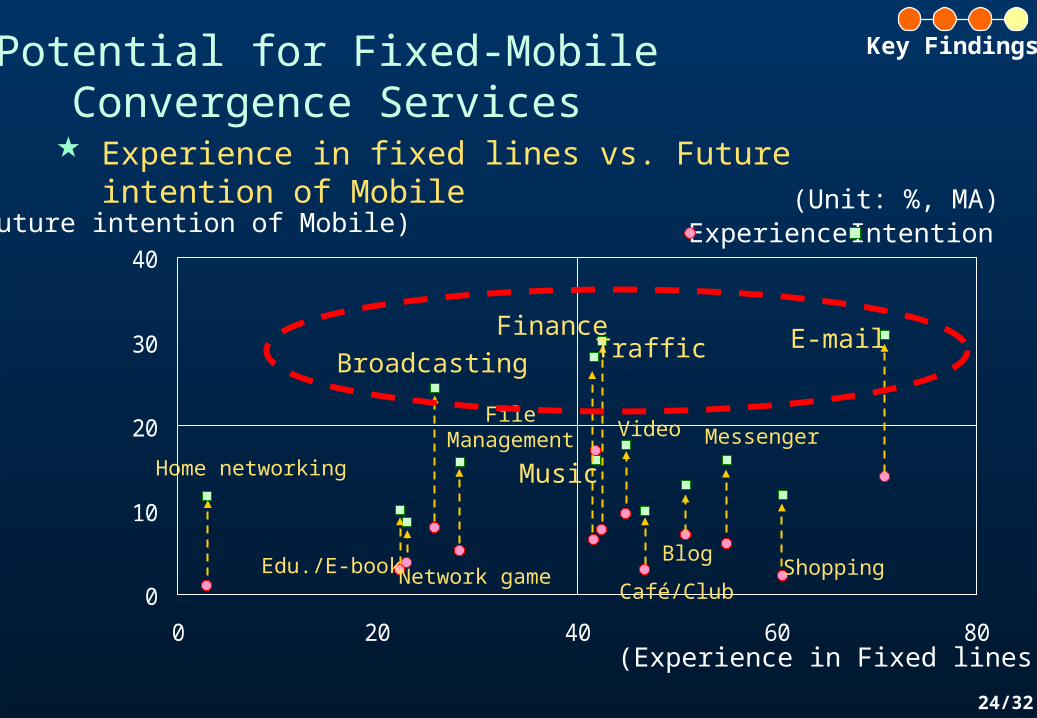

Experience in fixed lines

Experience of mobile

Experience of Fixed-MobileConvergence Services

Key Findings

23/32

ExperienceFuture

Intention of mobilePC

Mobile

E-mail 71 14 31Traffic information 43 8 30

Financial service 42 6 28GPS service - 5 28

Broadcasting service

26 8 24

Video service 45 10 18Music portal

service42 17 16

......

......

Practical serviceon a real time base

Entertainmentservice

Intention of future use of mobile

(Unit: % MA)

Potential for Fixed-MobileConvergence Services

<

Highest experience but low intention

Key Findings

24/32

0

10

20

30

40

0 20 40 60 80(Experience in Fixed lines)

(Future intention of Mobile)(Unit: %, MA)

Experience Intention

Potential for Fixed-MobileConvergence Services

Shopping

Messenger

Blog

Café/Club

Video

TrafficFinance

FileManagement

Broadcasting

Home networking

Edu./E-book Network game

Music

Experience in fixed lines vs. Future intention of Mobile

Key Findings

25/32

Conclusions

Implications

Conclusions and Implications

26/32

CameraCameraMost common feature in convergence

- But does not generate much revenue

MusicMusic Low growth potential- Low satisfaction & intention rates

- Difficult to make profit by increasing the use rate

GameGame Declining use rate- Need to develop fun games while on the move

Conclusions- Prospects for each

convergence service-

Conclusions andImplications

27/32

Tele-maticsTele-

maticsOn a steady rise with its own product value

- Needs to compete with low-end navigation products

BankingBankingMost promising convergence service

- Failure of initial price strategy: too low to make profits- Issue of chip integration will be a turning point

DMBDMBComplex issues among parties Uncertain market - The solution for above issues involves agreement between interested parties

Conclusions- Prospects for each

convergence service-

Conclusions andImplications

28/32

Pricing

1. Maximum affordable cost (median): €342. Current monthly cost (median): €28.53. New product intenders: approx. 30% - they are willing to pay approx. €5 (equivalent to €34 -

€28.5)4. Acceptable price for existing service: €2

Implications- Marketing Tips for

Mobile Convergence-

Several hypotheses were derived:

Conclusions andImplications

29/32

Product

Promising products:“Practical, NOT heavily content-dependent”

Banking service: High growth potential Telematics: Practical but limited in serviceMusic portal service: Not practical and too content-

dependent

Implications- Marketing Tips for

Mobile Convergence-

Conclusions andImplications

30/32

PromotionEvent-centered convergence services: sport or entertainment events

Eg. WBC event

DistributionDiversity of distribution channels

Eg. Selling of mobile handsets at banks for mobile banking

Implications-Marketing Tips for

Mobile Convergence-

Conclusions andImplications

31/32

The future of mobile convergence is uncertain. The success and failure of mobile convergence is hard to

predict. Numerous unexpected variables that may affect the success

or failure of mobile convergence lead us to uncertainty.

Epilogue

T-DMB: Promising!

S-DMB: Not promising!

What’s

happening?

32/32

From a conversation with a CMO of a mobile service company…

Q. Any success yet?

A. None yet.

Q. Will there be one?

Q. What are you doing?

A. Not sure

A. We’re trying!

Epilogue

MobileConvergence

MobileConvergence

33/32

Marketing Insight