lease accounting changes and equipment leasing

TRANSCRIPT

Lease Accounting Changes and Equipment Leasing

Tony Plesner

CFO/CAO

Intralinks

John Kirk

Managing Director

Lease Portfolio Recovery Services, LLC

Disclaimer

3

This product is intended to serve solely as an aid. Due to the constantly changing nature of the subject of the materials, this product is not appropriate to serve as the sole resource for any accounting opinion or return position, and must be supplemented for such purposes with other current authoritative materials. The information in this manual has been carefully compiled from sources believed to be reliable, but its accuracy is not guaranteed. In addition, Lease Portfolio Recovery Services LLC and Tony Plesner are not engaged in rendering legal, accounting or other professional services and will not be held liable for any actions or suits based on these slides or comments made during any presentation. If legal advice or other expert assistance is required, seek the services of a competent professional.

Professional Biographies – Tony Plesner

Tony Plesner

CFO/CAO

IntraLinks

Mr. Plesner has served as IntraLinks’ Chief Financial Officer and Chief

Administrative Officer since April 2005.

Prior to joining IntraLinks, he founded and operated snapSolutions, a consulting

group which provided strategic and operational financial support services to a

variety of content management and distribution organizations. He has also served

as Chief Operating Officer and Chief Financial Officer of The NewsMarket, an

online broadcast video news distribution service.

In addition, he has held the positions of President and Chief Operating Officer

of 24/7 Media, Inc., a provider of digital marketing services and solutions, and

Senior Vice President, Finance/Business Development at Medscape, Inc., a

provider of health information via the Internet.

Anthony also serves on the board of directors of Bluefly, Inc., a leading online

retailer of designer brands and fashion trends.

Professional Biographies – John Kirk

John Kirk

Managing Director

LPRS, LLC

Mr. Kirk works with clients to develop and implement equipment lease cost and

risk mitigation strategies. With 20 years of experience in growing analysis-based

firms and practices, Mr. Kirk is a pioneer in developing a data analysis-driven

approach to equipment finance program design, management and performance

measurement. Mr. Kirk has improved the equipment finance portfolio performance

of firms such as the American Red Cross, IntraLinks, Alvarez and Marsal,

PETsMART, Horizon Blue Cross Blue Shield, Anadarko and many others.

Prior to co-founding Lease Portfolio Recovery Services, Mr. Kirk spent three

years at Alvarez & Marsal as a Senior Director. Mr. Kirk was managing partner of

the Boston-based lease analysis and advisory firm American River Partners for 6

years prior to arranging for the ARP practice to become a business unit of Alvarez

and Marsal in 2008.

Mr. Kirk earned a bachelor's degree in English from Dartmouth College in

Hanover, New Hampshire, and a master's degree in management from the

Kellogg Graduate School of Management at Northwestern University in Evanston,

Illinois, where he focused on management, marketing and finance. Mr. Kirk is

active in the Association of Finance Professionals and has presented at various

Treasury Management Association events in the U.S.

Professional Biographies – Jonathan Nykvist

Mr. Nykvist assists clients in improving the performance of their technology equipment finance arrangements. His primary areas of concentration are analyzing and evaluating the historical performance of finance portfolios, and leveraging this data to provide services, including vendor selection, lease contract negotiation, asset and lease management process improvement, as well as lease buyout and restructuring.

With more than twelve years of experience in the equipment finance business, Mr. Nykvist has reviewed, advised and financed transactions for numerous Fortune 500 organizations. Some of Mr. Nykvist's notable analysis and advisory assignments include: PETsMART, Inc., Horizon Blue Cross Blue Shield, National Leisure Group, American Red Cross, Jefferies Broadview and Boston Scientific.

Prior to co-founding LPRS, Mr. Nykvist was a Director at the global services firm Alvarez & Marsal and was partner with Boston-based lease analysis and advisory firm American River Partners for nine years. American River Partners became a business unit of Alvarez & Marsal in 2008.

Mr. Nykvist earned an MBA from the Olin School of Business at Babson College in Wellesley, Massachusetts and a bachelor's degree in economics from Colby College in Waterville, Maine.

Jonathan Nykvist

Senior Director

LPRS, LLC

The New Lease Accounting Standards

Basics of Equipment Leasing

Proposed Accounting Changes

Emerging Transition Best Practices

IntraLinks Leasing Experience

87

Equipment Leasing Companies (Lessors) can be highly profitable businesses but go-to-market with attractive rates

How can Lessors make 10-20% per dollar invested in equipment when they offer low finance rates?

Lessors predict lessee behavior and manage relationship to maximize profitability:

Beginning of Lease: End of Lease:

- Interim Rents - Extension Rents

- Deposits - Renewals

- Prepaid Fees - Equipment Resale

Economic Substance - Equipment Leases are Different

89

Case Study: Online Media Conglomerate

Portfolio Analysis /

Equipment Lease

Buyout

Client Context

A fast growing Internet Portal expanded through acquisition and organically, financed data center and

office equipment through several leasing companies including a particularly large portfolio with an

independent leasing company. Due to the companies rapid growth and uneven financial performance the

leases and equipment were both not well tracked and frequently restructured by mutual agreement with

the leasing company to reduce short term cash requirements. The client was merged with another large

multinational and decided to buy out the leases to eliminate extension payments.

LPRS Role

LPRS experts assisted with the buyout of the overall portfolio with several lessors. Analysis showed that

the program was costly - with one lessor the client had spent more than $70 million for $43 million worth

of equipment. LPRS leveraged analysis to reduce the cost of the lease portfolio buyout.

Key Outcomes

More than $1 million immediate savings on the buyout transactions.

Online Media

Conglomerate

Proposed Lease Accounting Changes

Converged Exposure Drafts by FASB and IASB

Exposure Drafts August 2010

Proposed significant changes

Over 700 comment letters

FASB and IASB began re-deliberations February 2011

12

Redeliberations

6 months, 4 public roundtables, 15 preparer workshops

Significant changes to both lessee and lessor accounting compared to exposure draft (ED)

Lessee accounting – Retained basic model, eliminated many of the complexities

Lessor accounting – Completely different model

The Big News FASB and IASB will issue a second exposure draft

for comment

13

Second Exposure Draft

FASB and IASB expect to complete

redeliberations in Q3 2011

Expect to see new exposure draft by year-end

Comment period yet to be determined

Expect final standard by mid to late 2012

Effective date?

14

Some Key differences No more operating leases Leases on Balance Sheet

FAS 13: Operating Lease – Off the balance sheet FAS 13: Capital Lease – On balance sheet

New Standard in ED: All leases on balance sheet

• Committed Rents

• Inception Costs

• Renewal Options – If “significant economic incentive”

• “Short-term” leases not capitalized, but lessee can elect

The New Standards

55

Scope

Proposed model will apply to all leases, except:

Leases of intangible assets

Leases to explore for or use non-regenerative

resources, such as minerals, oil, natural gas,

etc.

Leases of biological assets

Distinct service components in contracts

containing a lease

Investment property measured at fair value

Contracts which represent the purchase or sale

of the underlying asset

Many of these

arrangements

would otherwise

meet the

definition of a

lease

21

Short-term leases have significantly different accounting.

Scope

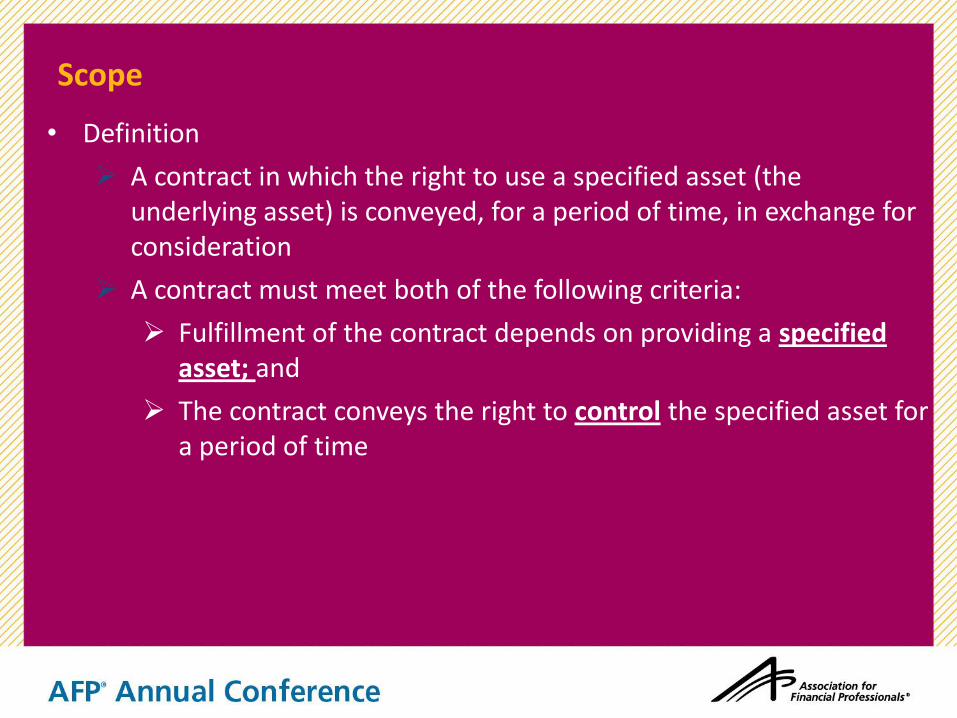

• Definition

A contract in which the right to use a specified asset (the underlying asset) is conveyed, for a period of time, in exchange for consideration

A contract must meet both of the following criteria:

Fulfillment of the contract depends on providing a specified asset; and

The contract conveys the right to control the specified asset for a period of time

22

Scope

Two key factors:

Specified asset

Control

23

Scope – Control

The boards will provide indicators of control in the final standard, including: • Physical access

• Customization

• Controlling benefits

Revised concept of control may result in arrangements currently classified as leases NOT qualifying as leases under new standard • Power purchase contracts

• Take or pay contracts

26

Highlights - Short-Term Lease

Definition: A lease that, at the date of commencement of the lease, has a maximum possible term of 12 months or less – including any options to renew

Lessee may elect an alternative accounting policy and not capitalize • Policy election is made at the asset class level

Accounting would be essentially the same as current operating

lease accounting

Significant change from exposure draft • Would have required capitalizing short-term leases, but did

not require PV calculation

30

Highlights - Initial Recognition Recognize a liability representing the obligation to pay rent

• Present value of lease payments

Recognize an asset representing the right to use the leased asset

• Same as liability to make lease payments

• Initial direct costs incurred by the lessee

31

Highlights - Lease Term

Non-cancellable term plus options to extend or terminate when

there is significant economic incentive

Significant change from exposure draft • Would have required probability assessment of exercising renewal options

• Would have resulted in more renewal periods being included in lease term

• Analysts and other financial statement users do not like this change

32

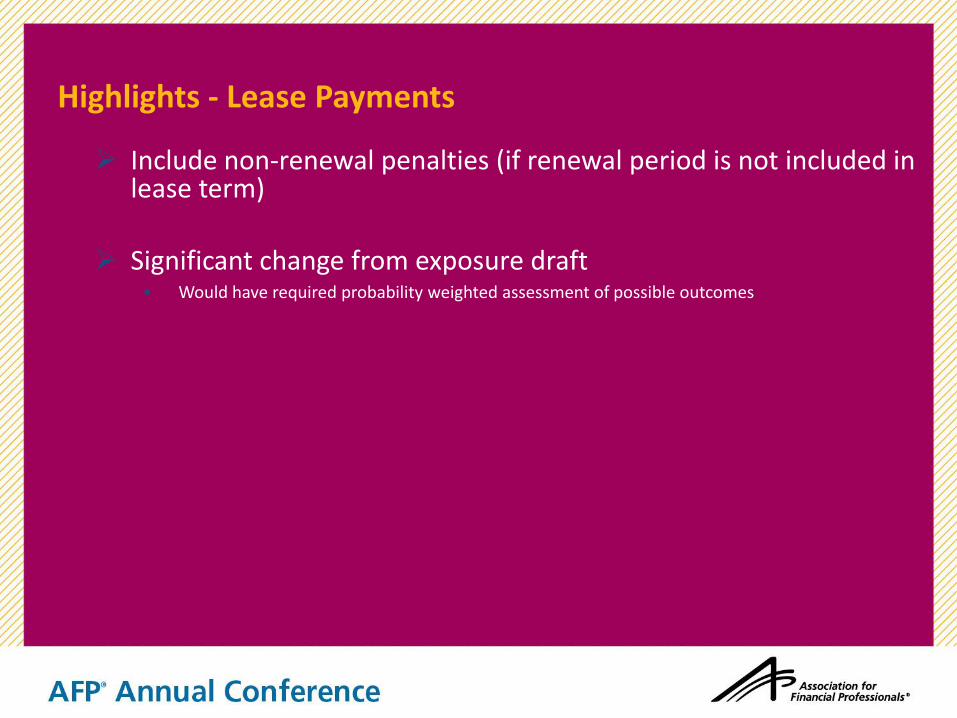

Highlights - Lease Payments

Include non-renewal penalties (if renewal period is not included in lease term)

Significant change from exposure draft • Would have required probability weighted assessment of possible outcomes

34

Highlights - Right to Use Asset

Initial Direct Costs May Include Does Not Include

Commissions

Legal fees

Evaluation of lessee’s financial condition

Negotiating terms

Preparing and processing documents

Closing

Other direct and incremental costs

attributable to negotiating and arranging the

lease

General overhead, rent, depreciation,

occupancy

Unsuccessful origination efforts

Idle time

Advertising / soliciting potential lessees

Servicing existing leases

Other ancillary activities

37

• Costs that are directly attributable to negotiating and arranging a lease that would not have

otherwise been incurred

Highlights – Cash Flow Statement

36

• Lease payments to be split between principal and interest for the purpose of presentation in the statement of cash flows

Highlights – Pre-term payments to be addressed

36

An onerous lease contract with lease payments made between dates of inception and commencement should be within the scope of IAS 37 (Contingent Liabilities)

Guidance coming on:

• Costs incurred by a lessee prior to lease commencement • Lease payments made before lease commencement • Lease incentives, which the Boards tentatively decided a lessee should deduct from the carrying

amount of its right-of-use asset

Highlights – Purchase Options

36

Include the exercise price of a purchase option when measuring a lessee’s lease liability and a lessor’s lease receivable if the lessee has a significant economic incentive to exercise the purchase option

If it is determined that the lessee has a significant economic incentive to exercise the purchase option, then the leased asset would be amortized over the economic life of the underlying asset, rather than over the lease term

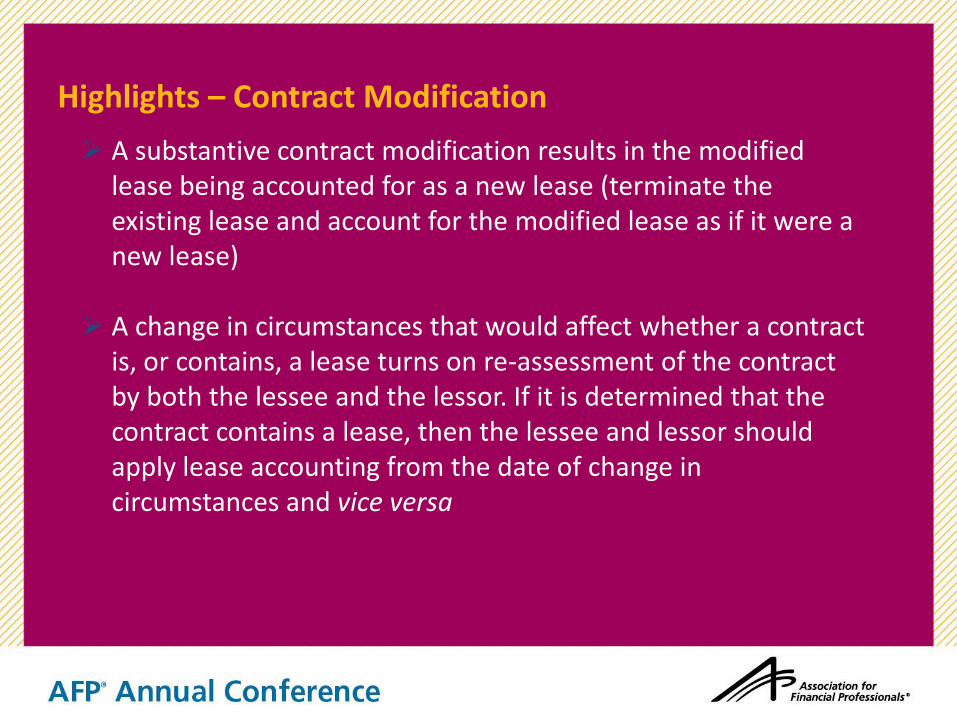

Highlights – Contract Modification

A substantive contract modification results in the modified lease being accounted for as a new lease (terminate the existing lease and account for the modified lease as if it were a new lease)

A change in circumstances that would affect whether a contract

is, or contains, a lease turns on re-assessment of the contract by both the lessee and the lessor. If it is determined that the contract contains a lease, then the lessee and lessor should apply lease accounting from the date of change in circumstances and vice versa

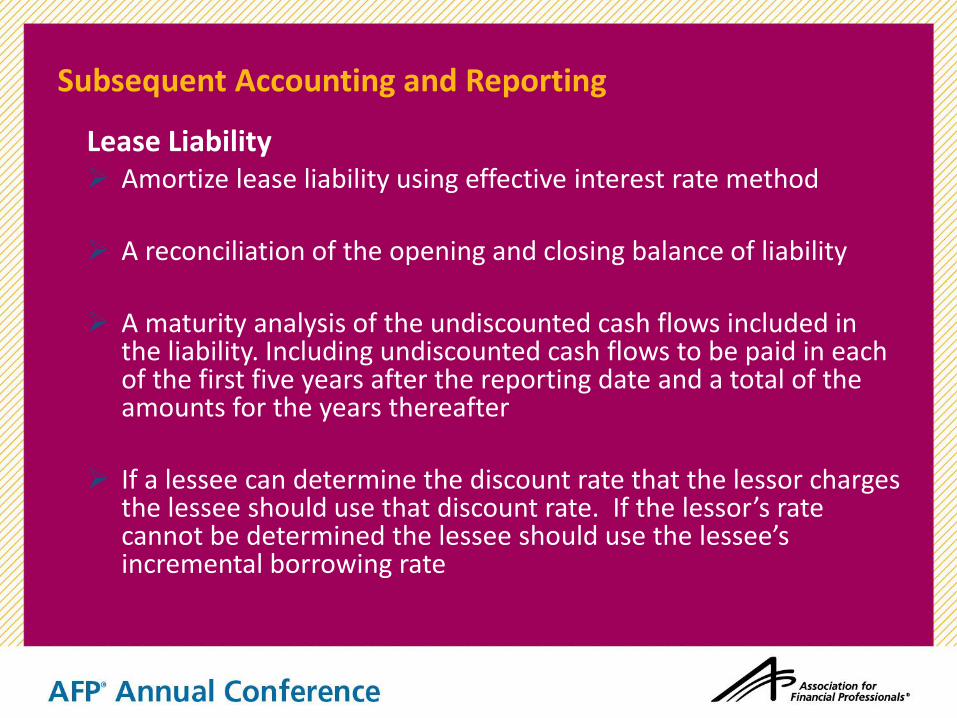

Subsequent Accounting and Reporting

Lease Liability Amortize lease liability using effective interest rate method

A reconciliation of the opening and closing balance of liability

A maturity analysis of the undiscounted cash flows included in

the liability. Including undiscounted cash flows to be paid in each of the first five years after the reporting date and a total of the amounts for the years thereafter

If a lessee can determine the discount rate that the lessor charges the lessee should use that discount rate. If the lessor’s rate cannot be determined the lessee should use the lessee’s incremental borrowing rate

38

Subsequent Accounting

38

Results Accelerated income statement recognition

Larger portion of cash payment attributed to interest expense in earlier periods

Remainder attributed to reduction of liability

Subsequent Accounting

Right to Use Asset Amortize asset on a systematic basis reflecting the pattern of

use • Will generally be straight line • A reconciliation of the opening and closing balance of right-

of-use assets, disaggregated by class of underlying asset

39

Miscellaneous Issues

Sale – Leaseback Transactions

Proposed model:

• Determine if transaction satisfies sales criteria – will be aligned with revenue recognition criteria

• Account for the sale and the lease separately

• If not a sale, account for as a financing

43

Transition for Lessees

Applies to All Outstanding Leases

Asset and liability measured at present value of remaining lease payments

Discount rate is incremental borrowing rate at time of adoption

Adjust right-of-use asset for recognized prepaid or accrued rent relating to previous rent calculations

Effective date is the subject of a separate project

44

An auditable process is required

Sarbanes Oxley – Who will sign off on subjective decisions? Consistent practice across company’s lease portfolio

• Term – Renewal and termination options

• Incremental borrowing rate

• Initial direct costs

Process / calculations / decisions revisited as circumstances change

Outside assistance / resources

Transition vs. New Deals vs. Monitoring

79

Emerging Best Practices

Where Accounting and Financial Risk Analysis Collide

Transition Planning

80

Its sooner than most realize

Lead time to gather necessary information and documents

Lead time to institute corporate process / standardization

Dual standards prior to effective date

Multiple stakeholders

Legal, risk, and compliance issues

ERP Financial reporting systems

Preparing for accounting change can open an opportunity for financial risk analysis

Date of Initial Application (DIA): • Effective Date is “transition” date, but need to report based on new standard sooner, based upon

comparative financial statement requirements of lessee

Determining DIA - Assuming 2015 +/- Effective Date

Comparative financial statements: • 5 years = DIA of 2011

• 4 years = DIA of 2012

• 3 years = DIA of 2013

Which leases to include: • All leases in effect on the lessee’s DIA.

• All leases executed between DIA and effective date

Transition Planning

81

Dual Standards: • Between today and effective date, report based on FAS13

• Between DIA and effective date:

• Report based on FAS 13

• Track based on New Standards

• Systems and reporting tracking both standards between DIA and Effective Date

Transition Planning

83

Direct involvement team members: • Corporate real estate leaders

• Business unit real estate team

• Corporate finance (CFO, Treasury, Controller)

• Business unit finance

• Third-party expert advisors and audit

• Legal

• Governance, risk and compliance

Transition Planning

85

Indirect involvement team members: • Brokerage teams

• Project managers

• Third party asset managers

• Domain experts

Accounting Pro-forma:

• Prepare pro-forma financial statements to determine impact of the changes on ratios, covenants and other related obligations

Economic Substance: • The new accounting rules call for new more comprehensive reporting of lease costs

• To prepare for these changes an analysis of past lease performance – the all-in cost of the program – can be invaluable

Adjust the Program: • Adjust the contracts and operational procedures to produce the best economic outcome in

the context of the new accounting requirements

Evaluating Equipment Lease Portfolios

88

Accounting Pro-Forma -- When Rules are Finalized

Quantify remaining contractually committed rents and pro-rata inception costs for active leases both on and off Balance Sheet (capital and operating under current guidance)

Analyze return, extension, notice, and other applicable contractual terms to evaluate if the options to extend or terminate create significant economic incentives

Conduct a gap analysis to identify any necessary contractual changes and investments in asset management programs and reporting systems to meet requirements

94

Accounting Pro-forma

Pro-forma Impact on Income Statement

Interest expense

Amortization expense

EBITDA will increase

• No rent expense

95

Pro-forma Impact on Balance Sheet

Ratios

Impact on Covenants

Economic Substance - Take a Step Back

What are the leasing program drivers? • Business imperatives behind the program

What are the program objectives? • Attributes of a successful program

What are the future plans for the program? • Expanding Program

• Status Quo

• Eliminating Program

90

Economic Substance - Take a Step Back

Vendor Selection Criteria.

Vendor Performance Measurement. All-in cost versus original equipment cost

Accounting Change Driven Considerations • Which contracts are leases?

• Specified Asset

• Customized

• Control Benefits

Term – 12 months or less

Variable rates, non renewal penalties, renewals (significant economic incentive)

91

Economic Substance – All-In Program Cost

Rents paid or committed to be paid to each lessor

Beginning of lease costs: • Interim rents

• Security Deposits

• Fees: Legal / Restocking / Other

• Evaluation of lessee’s financial condition

• Negotiating terms

• Preparing and processing documents

• Closing and other direct and incremental costs attributable to negotiating and arranging the lease

92

Economic Substance – All-In Program Cost

Mid-term upgrades – Lease schedule combinations / lease “rolls”

End of lease costs – Extension rents, partial extensions, renewals, prepaid fees, damages charges, etc.

Identify the contract terms and business processes responsible for each area of these costs

Determine service component of arrangement

93

Renewal Options: • Determining “significant economic incentive” • Are renewal options truly exercised in most cases • To what extent will income statement sensitivity drive renewal

decisions • Need auditable process / mechanism by which renewal

“decisions” can be tested • Renewal, etc.

• A few “what if?” examples

Impacts of Renewal / Termination Options

65

Adjust the Program

Change Program to Minimize Negative Consequences

Based on gap analysis identify contractual, operational, reporting system and other changes necessary to meet requirements

New standard innovations: • Which contracts are leases

• Specified Asset

• Customized

• Control Benefits

• Term – 12 months or less

• Variable rates, non-renewal penalties

• End of lease language: Extensions / renewals • (significant economic incentive)

96

Adjust the Program

Change Program to Minimize Negative Consequences

Internal Reporting

• Track all lease costs – particularly inception costs

• Ensure remaining contractually committed rents, inception costs, and other costs for active leases are accurately reflected

97

A Real Life Leasing Experience

Tony Plesner, CFO, IntraLinks

Case Study: INTRALINKS, Inc.

IntraLinks, Inc. provides its clients with secure, collaborative online digital workspaces for conducting financial transactions, discussing mergers and acquisitions, exchanging documents, and collaborating with advisers, customers, and suppliers.

NYSE – IL

Intralinks.com

98

“IntraLinks is one of four SaaS vendors to use for tactical deployments where speed and cost are key.”

“IntraLinks a pioneer

in cloud-based

cross-organizational

collaboration.”

Case Study: INTRALINKS, Inc. – Tony Plesner

Inherited risky lease portfolio and wanted to reduce financial and contract risk

Prior to going public recognized that the FMV back end leases would create a significant downstream unknown financial risk and decided to wind down the remaining lease contracts and establish a new low risk leasing program

Hired LPRS to evaluate the lease portfolio, scope, cap and reduce the exposure

Analysis defined the all-in cost of leasing over the life of the relationship and the clients’ contractual obligations

Using the analysis of past lease performance IntraLinks negotiated low risk lease arrangements with new vendor(s)

99

Portfolio Analysis – Risks / Red Flags 120 day certified mailed written notice to legal department

Open Interim Rent Period + Security Deposits

Commencement date can begin prior to lease schedule being signed • One schedule was signed on 11/17/2006, but began 10/1/2006 (instead of 12/1/2006) because last

equipment accepted 9/15/2006

Purchase Option Rider applied only to first schedule

No back-end conclusion option defined other than return: • One day de-installation period

• 10 Days from then for all gear to be at return location

• FMV not defined in MLA

Casualty Value table started at 112%

Significant default language

Portfolio Analysis -- Overview

Paying Cash Versus Leasing

Equipment (Time Value of Money

Adjusted)

Original Equipment Cost “OEC” is the

total cost of the gear in cash in Time

Period zero

IntraLinks was committed to pay

89.99% of OEC in regular term rents

(Present Valued) – Operating Lease

Interim Rents totaled 6% of OEC

Security Deposits totaled 5% of OEC

Total Initial Obligation: 101% of OEC

Lessor has negligible residual risk

Portfolio Analysis

Sources of Additional Cost:

Interim Rent

Security Deposits

Extension Rent

End of Lease Costs

Portfolio Analysis – IntraLinks’ future monetary risk

Sources of

Downstream Cost:

Lessor’s downstream

profit would be driven

by 12 month auto

extensions and other

End of Lease Costs

which were

significant financial

risks for IntraLinks

Security Deposits 5%

Interim Rent, 6%

Regular Term Rent (PV Adjusted)

90%

First Schedule Extension / Buyout

1%

12 Month Extension (remaining schedules)

31% of OEC

Back End Purchase 10% of OEC

IntraLinks Lease Costs

OEC

Total Exposure 143%

Next Steps

IntraLinks’ Options

Continue as is

• Attempt to return all leased assets on time per contract terms

• Gap between Operational reality vs. Contractual requirement made

asset return impossible

• Material financial risk

Cap and reduce exposure

• Negotiate a conclusion cost with lessor

• Pay fixed amount to eliminate future risk

Key Outcomes: INTRALINKS, Inc.

IntraLinks reduced the cost of an end of lease buyout for the balance of the portfolio by 30%.

In addition the IntraLinks benefitted from downstream savings of more than 31% realized through avoidance of lease extensions

New arrangements placed with new vendor both lower risk

Captured data which will allow for rapid and accurate adoption of new accounting standard

100

Lease Portfolio Recovery Services, LLC

• 5-10% Reduction in Lease Program Costs

• 30% Reduction in End of Lease Costs

• Saved Clients ~ $100 million

Select

Clients

Results

Services • Equipment Lease Restructuring

• Equipment Lease Program Redesign

• Equipment Lease Sourcing

• Equipment Lease Accounting Compliance