lecture 1 the principles and practice of economics

TRANSCRIPT

1

Lecture 1

The Principles and Practice of Economics

2

Is Facebook free?

3

What is economics?

"Economics is the study of how men and society choose, with or without the use of money, to employ scarce productive resources that would have alternative uses, to produce various commodities and distribute them for consumption, now or in the future, among various people and groups in society." -Paul Samuelson

4

Economic Agents

Economic Agent – an individual or a group that makes choices Consumer – Surface Computer or Mac Student – Take Principles of Economics or Global

Histories Government – Attack ISIS or not Firm – CEO search outsider or insider Party – elect Jeb Bush or Ben Carson or Donald

Trump

5

Scarcity

Scarcity – the limited nature of society’s resources

Managing the resources of society is important because resources are scarce

Economics – the study of how society manages its scarce resources

6

Economist as a Scientist

Scientific method is the dispassionate development and testing of theories about how the world works Observation, theory, and more observation

Example: inflation vs. printing money

Conducting experiments Difficult or impossible

Observation Natural experiments offered by history

Positive vs. Normative

Positive economics – objective descriptions or predictions that can be verified with data Minimum-wage hike causes unemployment How are prices determined in US health-care?

Normative economics – prescribes what an individual or society ought to do The government should raise the minimum wage We should allocate more resources to education Should the U.S. attack ISIS?

7

Microeconomics and Macroeconomics

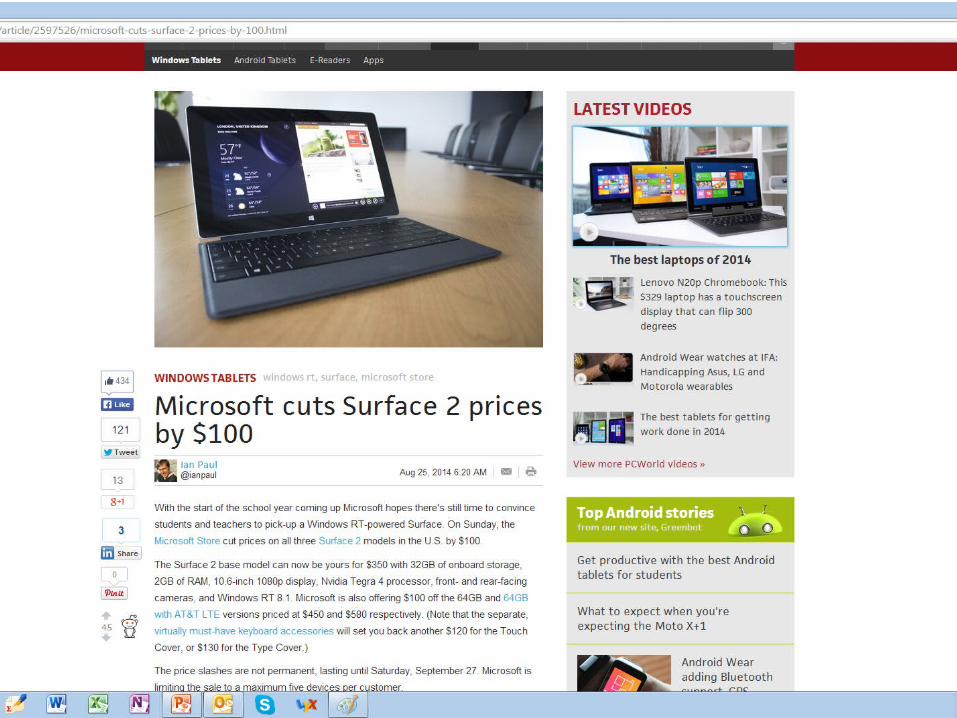

Microeconomics – the study of how individuals make decisions and how they interact in markets The effect of $100 discount on Surface 2 on sales? Are video streaming websites killing theaters?

Macroeconomics – the study of economy wide phenomena, including inflation, unemployment and economic growth What are the implications of a minimum wage on unemployme

nt hike to $10.10 from $7.50, requested by the president? Why did production and jobs expand so slowly in the US in

the 2000s?

8

9

10

11

Economists’ Objectives

1. To understand what is happening

2. To evaluate outcomes

3. To predict what will happen

Economic Modeling.

12

Economic Models

Model: A description of the relationship between two or more economic variables Diagrams and equations Omit many details Built with assumptions

Simplify reality to improve our understanding of it

13

The Role of Assumptions

Assumptions Can simplify the complex world (e.g. international

trade) Make it easier to understand

Focus our thinking – essence of the problem Different assumptions

To answer different questions Short-run or long-run effects of money printing

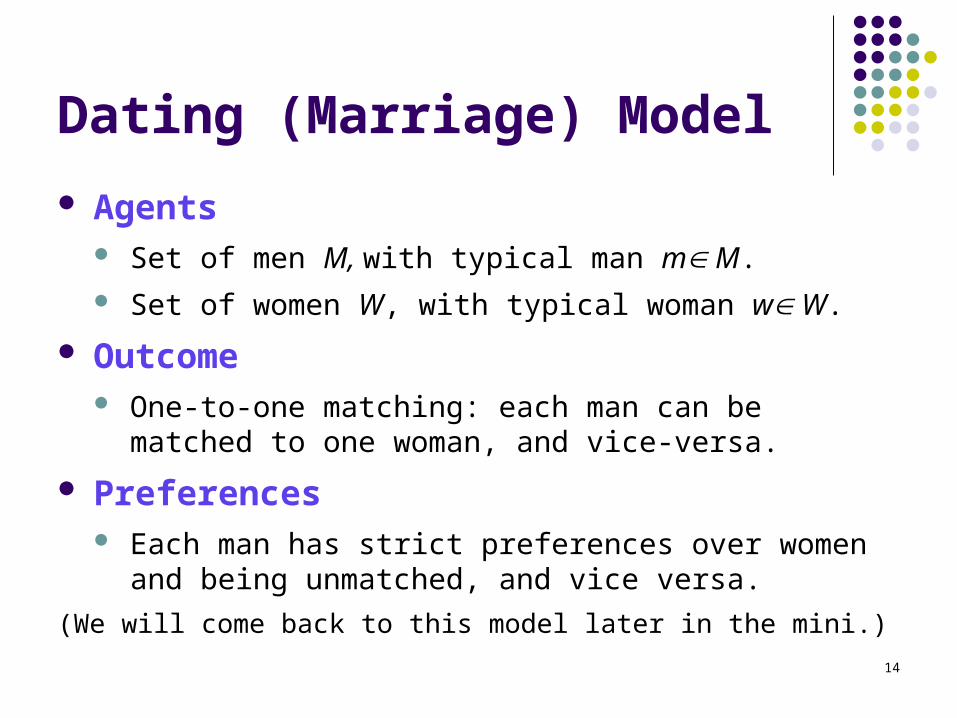

Dating (Marriage) Model

Agents Set of men M, with typical man m M. Set of women W, with typical woman w W.

Outcome One-to-one matching: each man can be matched to one

woman, and vice-versa.

Preferences Each man has strict preferences over women and being

unmatched, and vice versa.

(We will come back to this model later in the mini.)

14

15

Why study economics?

To understand the world

Evaluate economic policy

Learn a new way of thinking

16

Three Principles of Economics

Optimization – making the best choice possible with given information

Equilibrium – when agents interact no one would be better off with a different choice

Empiricism – using data to figure out answers to interesting questions

17

FIRST PRINCIPLE: OPTIMIZATION

18

1. Optimization

Making decisions requires comparing costs and benefits of alternatives (trade-off) College vs. work Playing vs. studying Movie vs. concert

Opportunity cost – the best alternative use of an item Budget-constraint – the bundles of goods that a

consumer can choose given her limited budget

19

20

How to decide?

Question Type 1:

“Should I do activity x?”

A: Yes, if Benefit(x) > Cost(x)

=>How do you measure B(x) and C(x)?

21

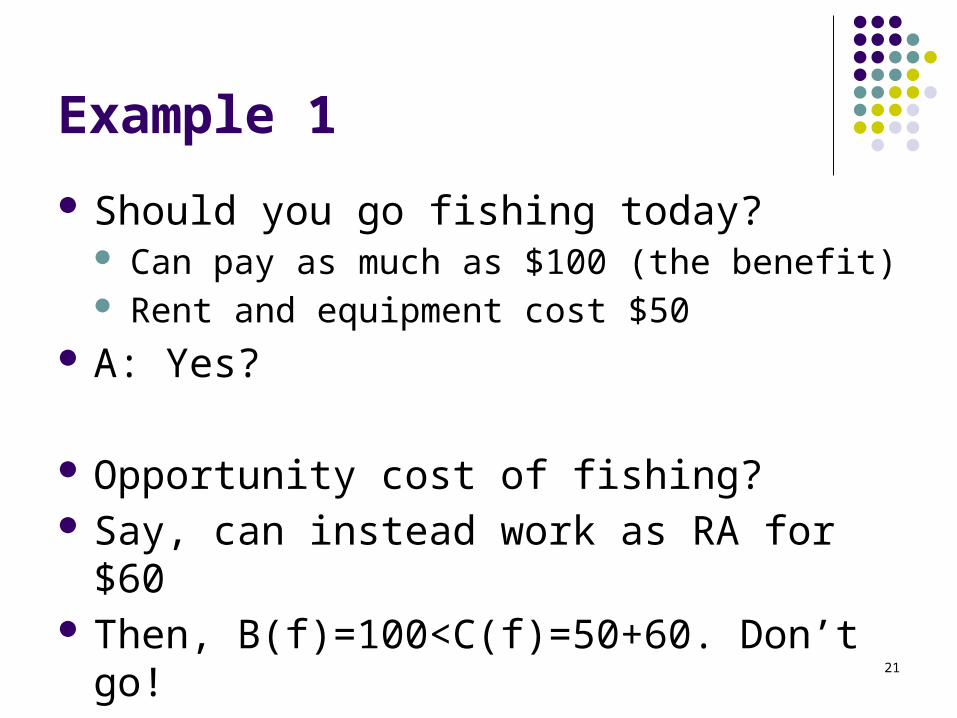

Example 1

Should you go fishing today? Can pay as much as $100 (the benefit) Rent and equipment cost $50

A: Yes?

Opportunity cost of fishing? Say, can instead work as RA for $60 Then, B(f)=100<C(f)=50+60. Don’t go!

22

Is Facebook Free?

23

Marginal thinking

To optimize think at the “margin” Marginal change is a small incremental

adjustment to a plan of action An airline may optimally sell the last ticket

below average cost A rational decision maker takes an action if

the marginal benefit of the action exceeds marginal cost

24

How to decide?

Question Type 2: “Should you continue doing x?”

A: Yes if ,

Benefit of an additional unit of x > Cost of an additional unit of x or,

Marginal Benefit (x) > Marginal Cost (x)

25

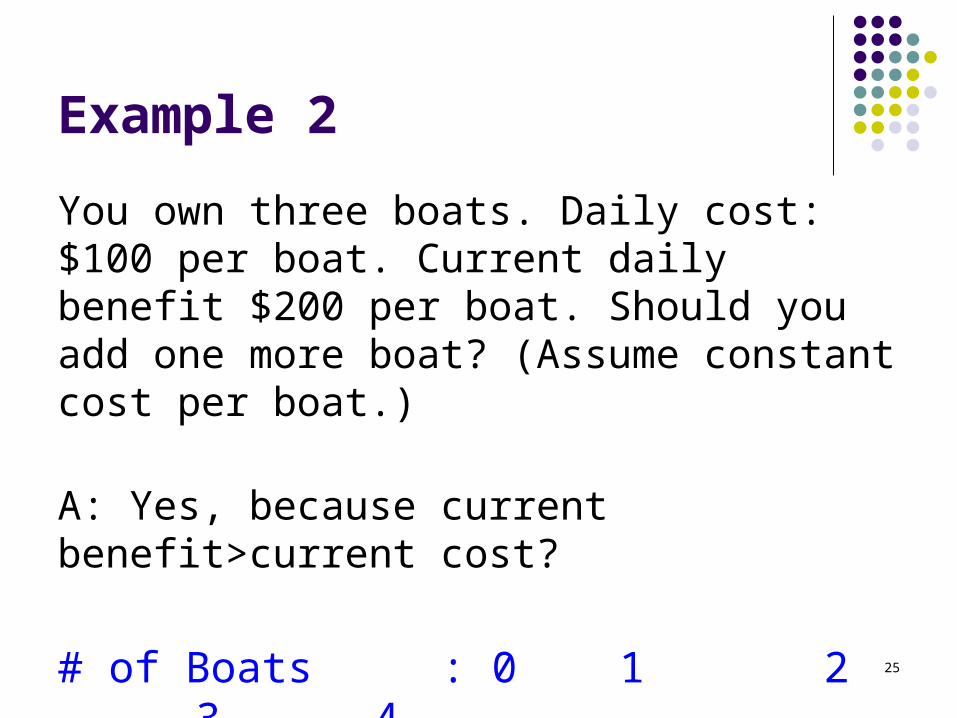

Example 2

You own three boats. Daily cost: $100 per boat. Current daily benefit $200 per boat. Should you add one more boat? (Assume constant cost per boat.)

A: Yes, because current benefit>current cost?

# of Boats : 0 1 2 3 4

Total Benefit : 0 300 480 600 640

26

SECOND PRINCIPLE:EQUILIBRIUM

27

Equilibrium

Multiple agents interact while optimizing Can we predict behavior?

Equilibrium – situation in which no one benefits by changing their behavior

I can make the exam hard or easy, you can work or shirk

Incentives matter

28

Agents Respond to Incentives

Incentive – something that induces a person to act

Changes in costs or benefits motivate people to respond When gas prices rise, consumers buy more

hybrid cars and fewer gas guzzling SUVs. When cigarette taxes increase, teen smoking

falls. Crucial for public policy!

29

Incentives at Work Around Us

Seat belt and airbag (safety vs. speeding) Auto insurance (deductible and driving record

vs. caution) Shopping discounts (e.g., buy one get one

free) Wild-bird feeders (cardinal vs. squirrel) This course (e.g. recitation attendance vs.

grade) Religions (e.g. actions vs. heaven-hell)

30

THIRD PRINCIPLE:EMPIRICISM

31

Empiricism

Empiricism – evidence-based analysis

Confronting theory with data Revising theory to fit the data

Conclusion

Economics is a social science using the scientific method “An economist is an expert who will know

tomorrow why the things he predicted yesterday didn't happen today.” Laurence J. Peter

Three principles: optimization, equilibrium, and empiricism

32

33

Homework Assignment

Read Chapter 4 “Demand, Supply, and Equilibrium”