lecture 6 managerial finance fina 6335 bond and stock valuation ronald f. singer

TRANSCRIPT

Lecture 6

Managerial FinanceFINA 6335

Bond and Stock Valuation Ronald F. Singer

Present Value of Bonds & Stocks

• At this point, we apply the concept of present value developed earlier to price bonds and stocks.

Present Value of Bonds & Stocks

• At this point, we apply the concept of present value developed earlier to price bonds and stocks.

• Price of Bond = Present Value of Coupon Annuity

Present Value of Principal

+

Example

Consider a 20 year bond with 6% coupon rate paid annually. The market interest rate is 8%. The face value of the bond is $100,000. (referred to as par) • PV of coupon annuity = 20 6000 = 58,908 t=1 (1 + 0.08)

• PV of principal = 100,000 = 21,455

(1 + 0.08)20

• Present Value of Total = 80,363 • OR

Yield to Maturity

• By Calculator

N = 20

I%YR = 8

PMT = 6,000

FV = 100,000

PV => 80,363.71 or 80.364% of par.

Yield to Maturity

• YTM: The Annual Yield you would have to earn to exactly achieve the cash flow promised by the bond

• It is the internal rate of return of the bond IF the promised payments are all paid.

• It is that interest rate which makes the price of the bond equal the present value of the promised payments.

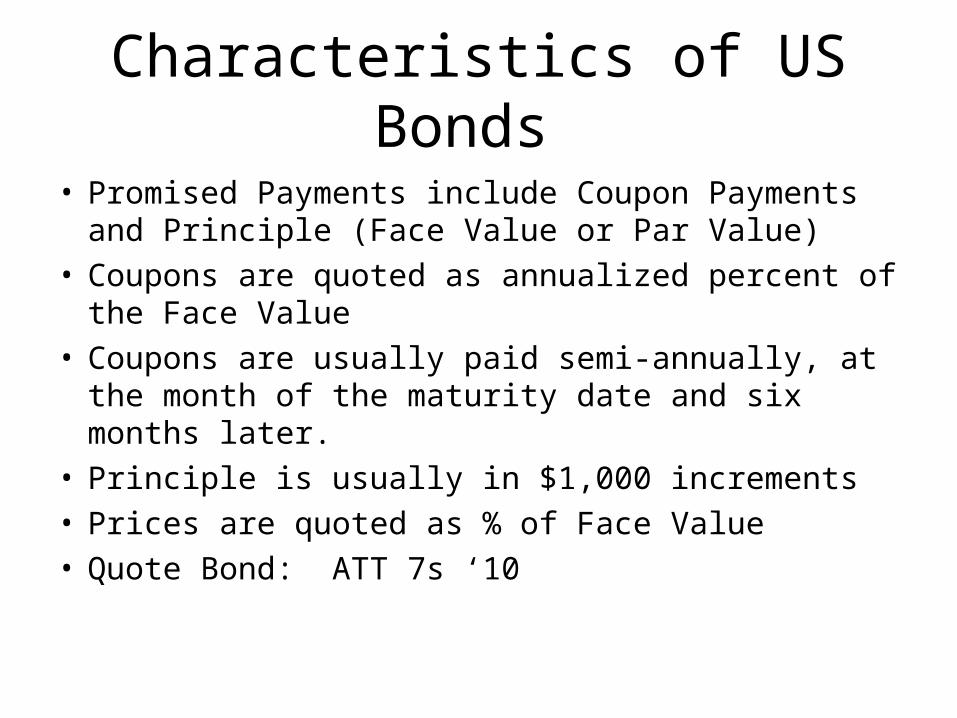

Characteristics of US Bonds

• Promised Payments include Coupon Payments and Principle (Face Value or Par Value)

• Coupons are quoted as annualized percent of the Face Value

• Coupons are usually paid semi-annually, at the month of the maturity date and six months later.

• Principle is usually in $1,000 increments • Prices are quoted as % of Face Value • Quote Bond: ATT 7s ‘10

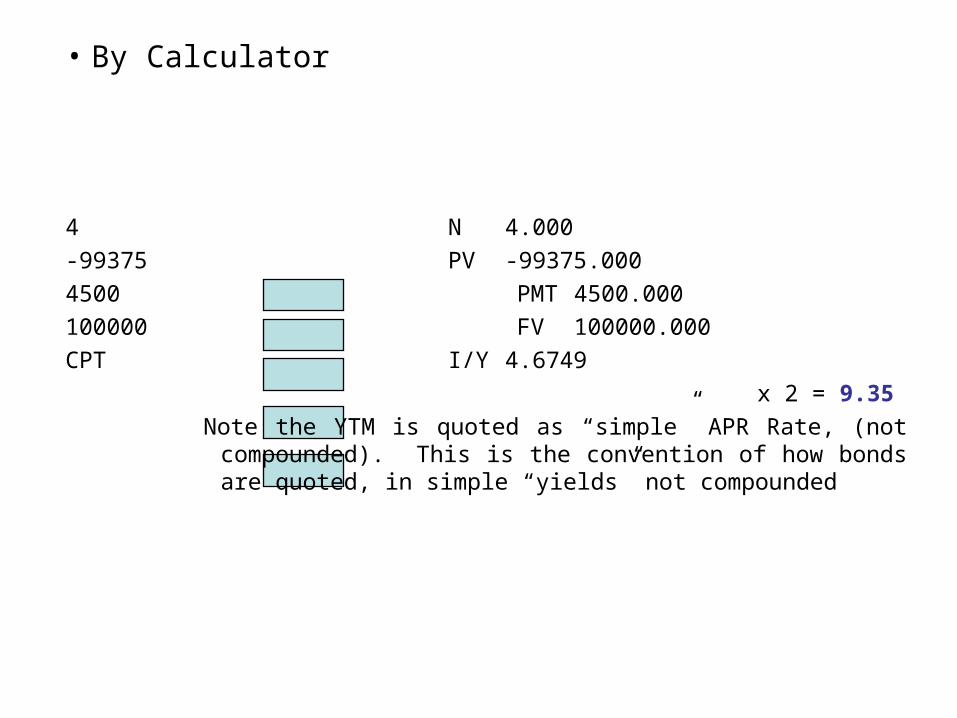

• Consider a bond with principal of $100,000 and a coupon, paid semiannually, of 9%, selling for 99.375 (This is percent of the face value), so that the actual price is 100,000 x .99375 = $99,375.

Maturity date is March 1, 2010.The semiannual coupon payments are: 4.5% of 100,000 or 4,500.(As of March 1, 2008) 4,500 4,500 4,500 104,500 0 1 2 3 4

9/08 3/10 • 99,375 99,375 = 4500 + 4500 + 4500 + 104,500

(1+YTM) (1+YTM)2 (1+YTM)3 (1+YTM)4 2 2 2 2

• The Yield to Maturity is 9.35%.

• By Calculator

4 N 4.000

-99375 PV -99375.000

4500 PMT 4500.000

100000 FV 100000.000

CPT I/Y 4.6749

x 2 = 9.35

Note the YTM is quoted as “simple” APR Rate, (not compounded). This is the convention of how bonds are quoted, in simple “yields” not compounded

Bond Pricing

From Yahoo! Finance (finance.yahoo.com) Click: Investing>bonds>Bond Center Current FitchType Issue Price Coupon Maturity YTM Yield Rating Corp ABBOTT 96.38 3.750 3/15/11 4.825 3.891 AA

LABS

18.75 18.75 18.75…………………………1018.75

$963.80 3/08 9/08 3/09 3/11

– Principal: $1,000 (most US Corporate bonds have $1,000 principal).

– Coupon (Annual): $37.50– Maturity : March 15, 2011– Current yield: 3.891%

Current = Coupon = 3.75 = 3.891% Yield Price 96.38

Price = ..9638 x 1000 = $963.80 What is the bond's Accrual (we can assume 90 day

quarters) So Accrual = Coupon (Days from last Coupon/Days in

coupon period) = (37.5) X (162) = 16.875

2 180

Cash (Dirty) price is = $963.80 + 16.875 = 980.675Note in this case: YTM > Current Yield > Coupon: Why?

Calculating Bond Price

Suppose we know the appropriate Yield to Maturity ("Discount Rate")

For Example: 5% (NB: Bond Quotes are in simple interest)

The Bond Value is

P0= 18.75 + 1000 t=1 (1.025)t (1.025)7

P = $960.32 or 96.03 (% of par)

Calculating YTM

• Suppose price was 98 ($980). What is the yield to maturity?

• N = 7

• PV = -98

• PMT = 1.875

• FV = 100

• CPT I% = 2.1862 X 2 = YTM = 4.37

Treasury Bonds, Notes and Bills Current Fitch

Type Issue Price Coupon Maturity YTM Yield Rating

Zero US Treas 89.74 0.000 8/15/10 3.733 0.000 AAATreas US Treas 105.03 5.750 8/15/10 3.912 5.474 AAA Treas US Treas 100.60 4.125 8/15/10 3.904 4.100 AAA

Valuing Bonds Using Law of One Price

• Strips: Zero Coupon Treasuries. These are called “strips” because it is a regular (coupon) bond with the coupons stripped away, so that you only have the principal or face value.

From Yahoo Finance

Strips

Maturity Price 8/15/08 96.82

2/15/09 95.09

8/15/09 93.44

2/15/10 91.39

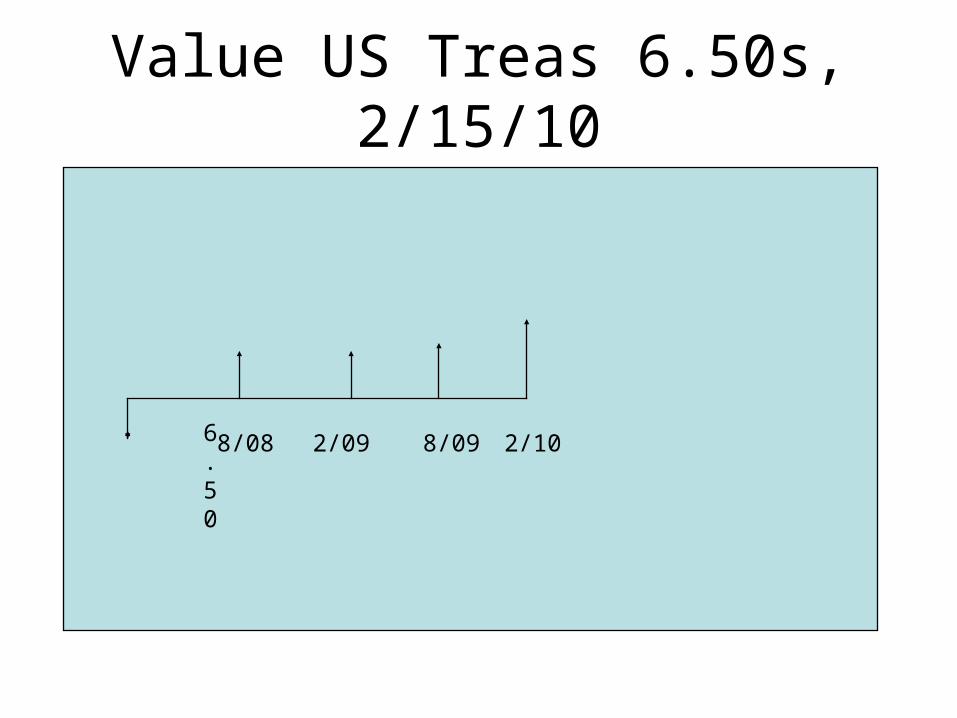

Value US Treas 6.50s, 2/15/10

6.50

8/08 2/09 8/09 2/10

Value US Treas 6.50s, 2/15/10

3.25 3.25 3.25 103.25 6.50

8/08 2/09 8/09 2/10

Value US Treas 6.50s, 2/15/10

To Value this Bond using Zero’s Date Paid PV

First coupon 8/15/08 .9682*3.25 = 3.1467

Second coupon 2/15/09 .9509*3.25 = 3.0904 Third coupon 8/15/09 .9344*3.25 = 3.0368Fourth coupon 2/15/10 .9139*103.25 =94.3602 + Principal 103.63

YTM = ???

Valuation of Common Stock

• The Annual Expected Return on a share of common stock is composed of two components:

Dividends and Capital Gains Expected Returns: E(R0) = Dollar Return = E(Div1) + E (P1) - Po

Price P0 P0

Where P0 = The current per share price E(Div1) = Expected dividend per share at time 1 E(P1) = Expected price per share at time 1

E(Ro) = Expected Return • E(R0) = expected dividend yield + expected capital gain return

• From Yahoo! Finance

• OCCIDENTAL PET (NYSE:OXY)

• Last Trade:79.16 Trade Time:11:47AM ET

• Change: 0.46 (0.58%) Prev Close:78.70

• Open:78.29 1y Target Est:82.73

• Day's Range:78.29 - 79.9152

• wk Range:44.85 - 80.83

• Volume:1,884,459 Avg Vol (3m):7,065,790

• Market Cap:65.36B P/E (ttm):12.30

• EPS (ttm):6.44 Div & Yield:1.00 (1.30%)

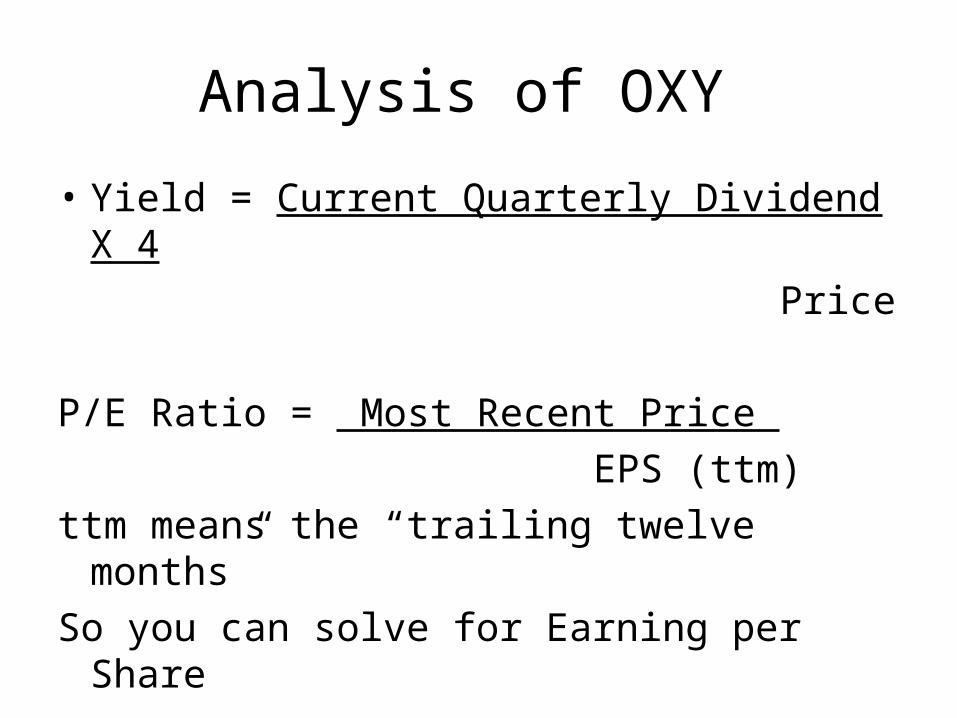

Analysis of OXY

• Yield = Current Quarterly Dividend X 4

Price

P/E Ratio = Most Recent Price

EPS (ttm)

ttm means the “trailing twelve months”

So you can solve for Earning per Share

• Note, we don't observe E(Ro) but we observe prices and promised payoffs.

If we solve for Po, the current value of the stock

Po = E(Div1) + E (P1) 1 + E(R)

This relation will hold through time, therefore,

P1 = E (Div2) + E(P2) 1 + E(R)

Substitute for P1

Po = E(Div1) + E(Div2) + E(P2) 1 + E(R) ( 1 + E(R))2 (1 + E(R))2

In general, Po = T E (Divt) + E(PT) t=1 (1 + E(R))t (1 + E(R))T

You can think of E(PT) as a liquidating dividend equal to the value of firm's assets at time T.

As T ----> 00,

Present Value of E(PT)----> 0 And the stock price is the present value of all future dividends paid to existing stockholders

Po = 00 E (Divt) t=1 (1 + E(r))t What happened to capital gain?

Consider the value of the stock (or the per share Price of the stock)

The basic rule is: The value of the stock is the present value of the cash flows to the stockholder. This means that it will be the present value of total dividends (or dividends per share), paid to current stockholders over the indefinite future.

That is: oo

V(o) = E{ Dividend(t)} t=1 (1 + r)t

or: P(0) = E{ DPS(t) }t=1 (1 + r)t

Capitalized Value of Dividends

Capitalized Value of Dividends

The problem is how to make this OPERATIONAL.That is, how do we use the above result to get at actual valuation? We can use two general concepts to get at this result: They all involve

the above equation under different forms.

(1) P = EPS1 + PVGO r(2) P = (Free Cash Flow per Share(t)) t=1 (1 + r)t

EPS1 is the expected earnings per share over the next period.PVGO is the "present value of growth opportunities.r is the "appropriate discount rate

Free Cash Flow per Share is the cash flow available to stockholders after the bondholders are paid off and after investment plans are met.

Capitalized Dividend Model

Simple versions of the Capitalized Dividend ModelDIV(1) = DIV(2) = . . . = DIV(t) = ...The firm's dividends are not expected to grow. essentially, the firm is planning no additional investments to propel growth. thus:

with investment zero:DIV(t) = EPS(t) = Free Cash Flow(t)PVGO = 0therefore the firm (or stock) value is simply:

P0 = DIV= EPS r r

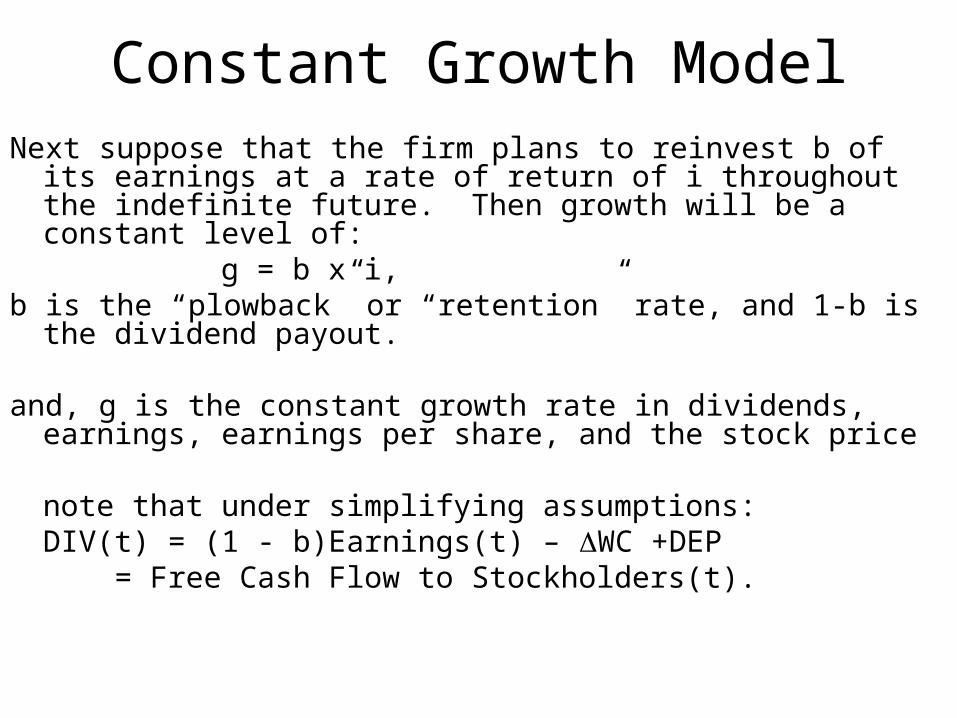

Constant Growth ModelNext suppose that the firm plans to reinvest b of its earnings at a

rate of return of i throughout the indefinite future. Then growth will be a constant level of: g = b x i,

b is the “plowback” or “retention” rate, and 1-b is the dividend payout.

and, g is the constant growth rate in dividends, earnings, earnings per share, and the stock price

note that under simplifying assumptions:DIV(t) = (1 - b)Earnings(t) – WC +DEP

= Free Cash Flow to Stockholders(t).

Total Payout Model

• Sometimes firms substitute share repurchase for dividends. Under those circumstances we can think of the cash flow to stockholders, as the sum of Dividends plus share repurchases. Then, the Total payout model would be the present value of future dividends and repurchases, and the share price is simply that present value per CURRENT outstanding shares.

Lets assume that WC +DEP = 0, and there are no interest payments, for simplicity, so that (EPS) = Cash Flow from Operations per share. we can write the valuation formula as:

P0 = DIV(1) = (1-b)EPS(1) = Free Cash Flow(1) r - g r - g r - g

= EPS(1) + PVGO r

Constant Growth Model

Example: ABC corporation has established a policy of simply maintaining its real assets and paying all earnings net of real depreciation out as a dividend. Assume, Change in working capital is 0 throughout:

suppose that: r = 10% Net Investment = ?

Current Net Earning per Share is 10. then: EPS(1) = EPS(2) . .=. . EPS(t). = 10

Year 1 2 3 ....

growth 0 0 0dividends 10 10 10free cash flow 10 10 10

Thus: Po = 10 = 100 0.10

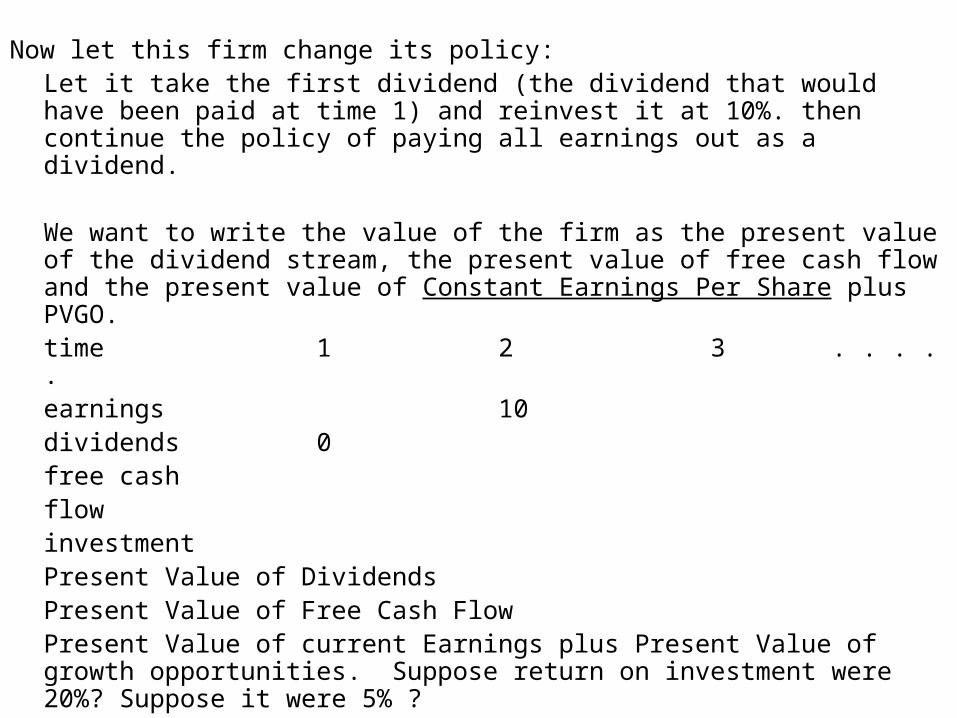

Now let this firm change its policy: Let it take the first dividend (the dividend that would have been paid

at time 1) and reinvest it at 10%. then continue the policy of paying all earnings out as a dividend.

We want to write the value of the firm as the present value of the dividend stream, the present value of free cash flow and the present value of Constant Earnings Per Share plus PVGO.time 1 2 3 . . . . . earnings 10 dividends 0 free cash flow investment Present Value of DividendsPresent Value of Free Cash FlowPresent Value of current Earnings plus Present Value of growth opportunities. Suppose return on investment were 20%? Suppose it were 5% ?

Now let this firm change its policy: Let it take the first dividend (the dividend that would have been paid

at time 1) and reinvest it at 10%. then continue the policy of paying all earnings out as a dividend.

We want to write the value of the firm as the present value of the dividend stream, the present value of free cash flow and the present value of Constant Earnings Per Share plus PVGO.time 1 2 3 . . . . . earnings 10 11 11 dividends 0 11 11 ………. free cash 0 11 11 flow investment 10 0 Present Value of Dividends Present Value of Free Cash FlowPresent Value of current Earnings plus Present Value of growth opportunities. Suppose return on investment were 20%? Suppose it were 5% ?

This value of the firm can be represented by

Po = EPS1 + PVGO:

r

where,

PVGO = NPV(t)

t=1 (1+r)t

Notice: if the NPV of future projects is positive then the value of the stock, and its price per share will be higher, given its current earnings and its capitalization rate

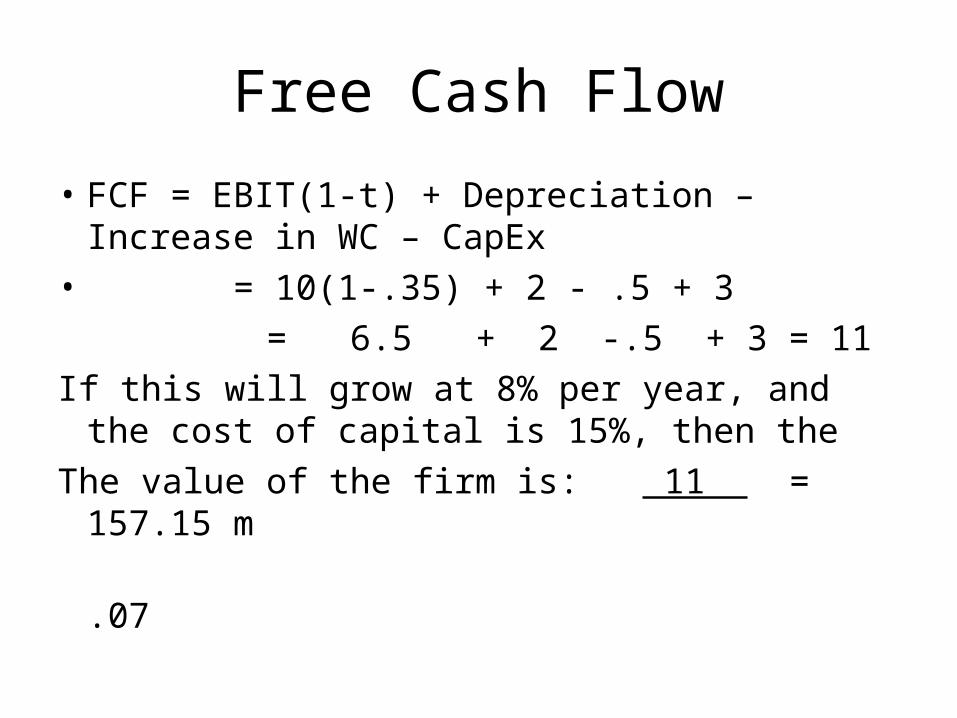

Free Cash Flow Model

Free Cash Flow = EBIT(1-t) +Depreciation

- CapExp – WC

Then the Value of the Firm, V = PV of FCF

And Equity value = V – Debt + Cash P = (Equity value)/(Shares outstanding)

Discounted Free Cash Flow Model

• Approach: Determine the (present) value of the total cash flow to all Security holders, and then subtract the value of all securities other than equity to get the Equity Value of the firm.

•

Cash Flow to all Security Holders

• The Cash flow to all security holders is the firm’s Free Cash Flow. So!

• Free Cash Flow = EBIT(1-t) +Depreciation – Capital Expenditures – Increase in Working Capital

A Simple Example

• Assume Free Cash Flow grows at a constant rate over time. Historically this has been 8% Suppose we have the following data:

• Earnings = 5.2 million • EBIT = 10 million• Depreciation = 2 million• Interest = 3 million• Increase in Working capital is .5 million • Capital Expenditures is 3 million • Legal tax rate is 35%

Free Cash Flow

• FCF = EBIT(1-t) + Depreciation –Increase in WC – CapEx

• = 10(1-.35) + 2 - .5 + 3

= 6.5 + 2 -.5 + 3 = 11

If this will grow at 8% per year, and the cost of capital is 15%, then the

The value of the firm is: 11 = 157.15 m

.07

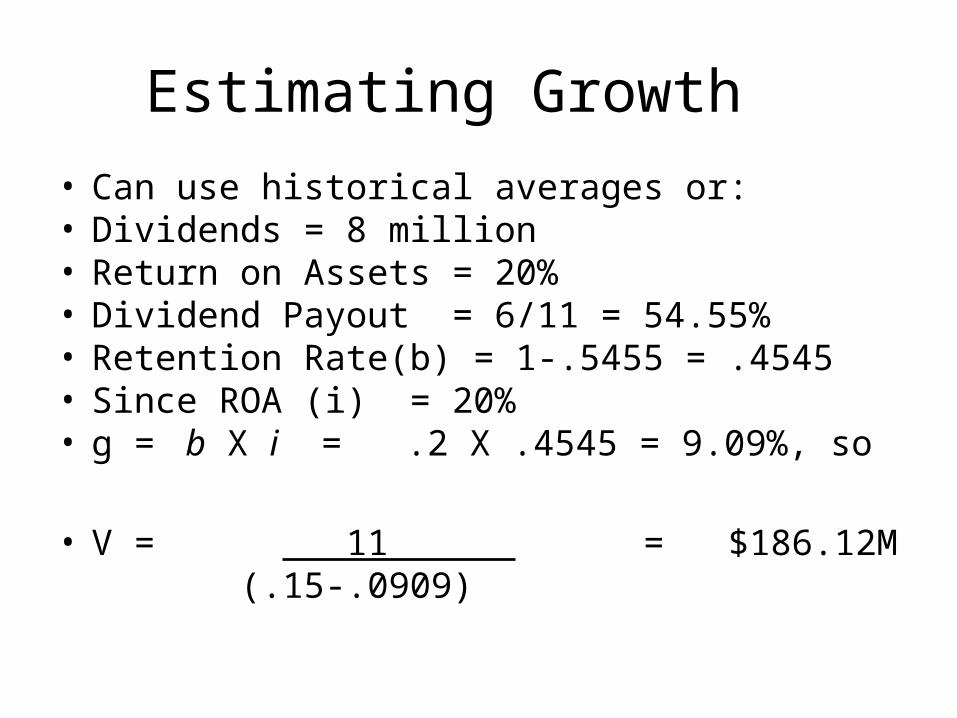

Estimating Growth

• Can use historical averages or: • Dividends = 8 million • Return on Assets = 20% • Dividend Payout = 6/11 = 54.55%• Retention Rate(b) = 1-.5455 = .4545• Since ROA (i) = 20%• g = b X i = .2 X .4545 = 9.09%, so

• V = 11 = $186.12M (.15-.0909)

The Discount Rate

• We are using the Cash Flow to all security holders, and we want to know what the appropriate rate to discount that cash flow.

• We will see that the appropriate discount rate is the WACC, which is the average return required by all security holders having a claim to that cash flow.

• More about this later