lecture notes - chapter 6 - macro - week 6

DESCRIPTION

Canadian Macroeconomics for the course of the lecture used in 2013 for classes business stocks and bondsTRANSCRIPT

1

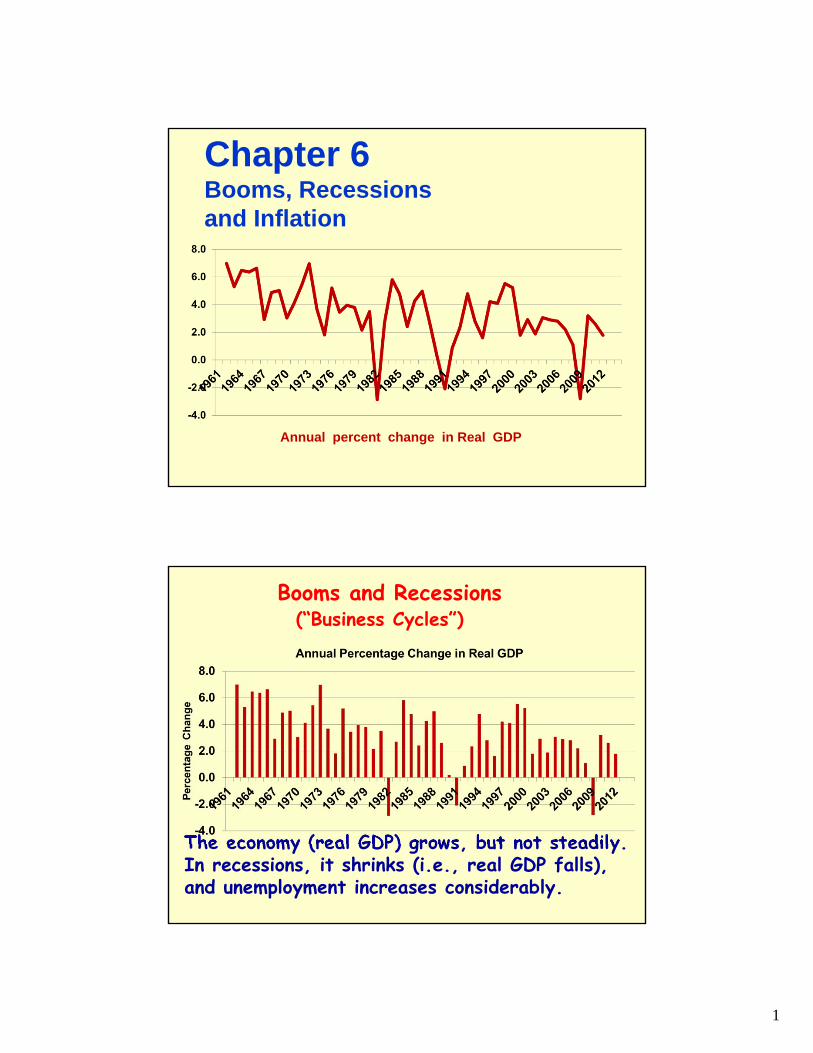

Chapter 6Booms, Recessions and Inflation

Annual percent change in Real GDP

The economy (real GDP) grows, but not steadily.In recessions, it shrinks (i.e., real GDP falls),and unemployment increases considerably.

Booms and Recessions(“Business Cycles”)

2

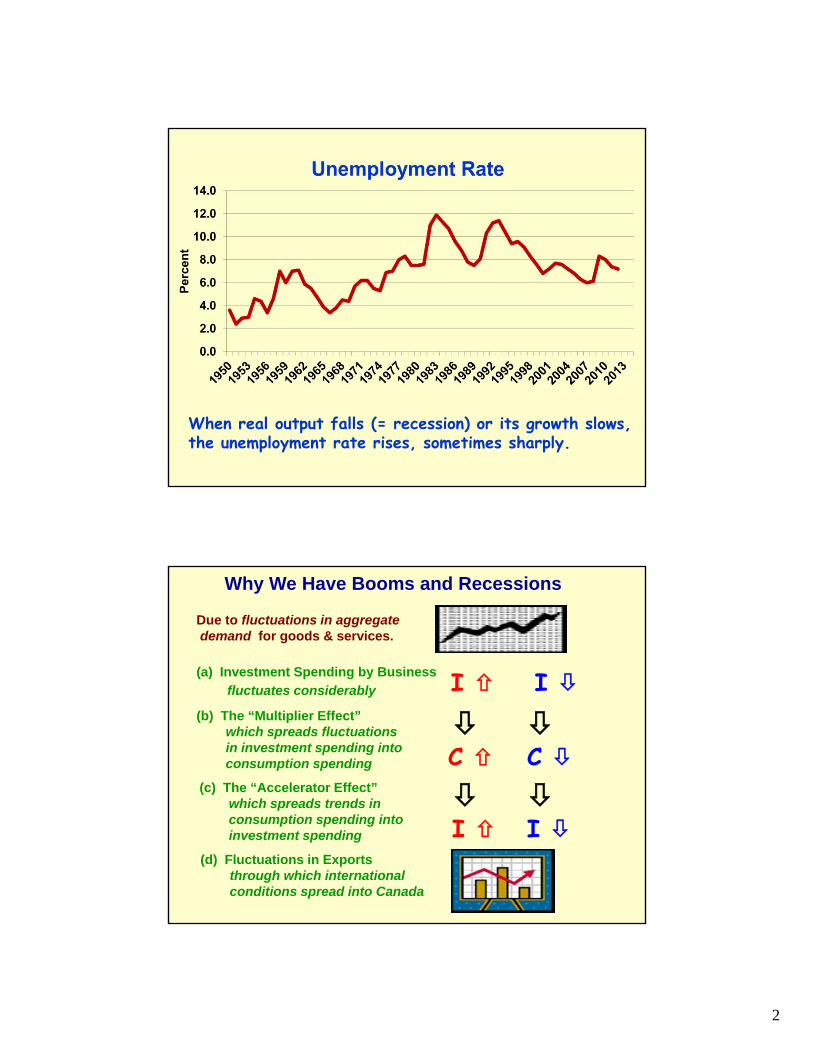

When real output falls (= recession) or its growth slows, the unemployment rate rises, sometimes sharply.

Why We Have Booms and Recessions

Due to fluctuations in aggregatedemand for goods & services.

(a) Investment Spending by Business

fluctuates considerably

(b) The “Multiplier Effect”which spreads fluctuationsin investment spending intoconsumption spending

(c) The “Accelerator Effect”which spreads trends inconsumption spending intoinvestment spending

(d) Fluctuations in Exportsthrough which internationalconditions spread into Canada

I

C I

I

C I

3

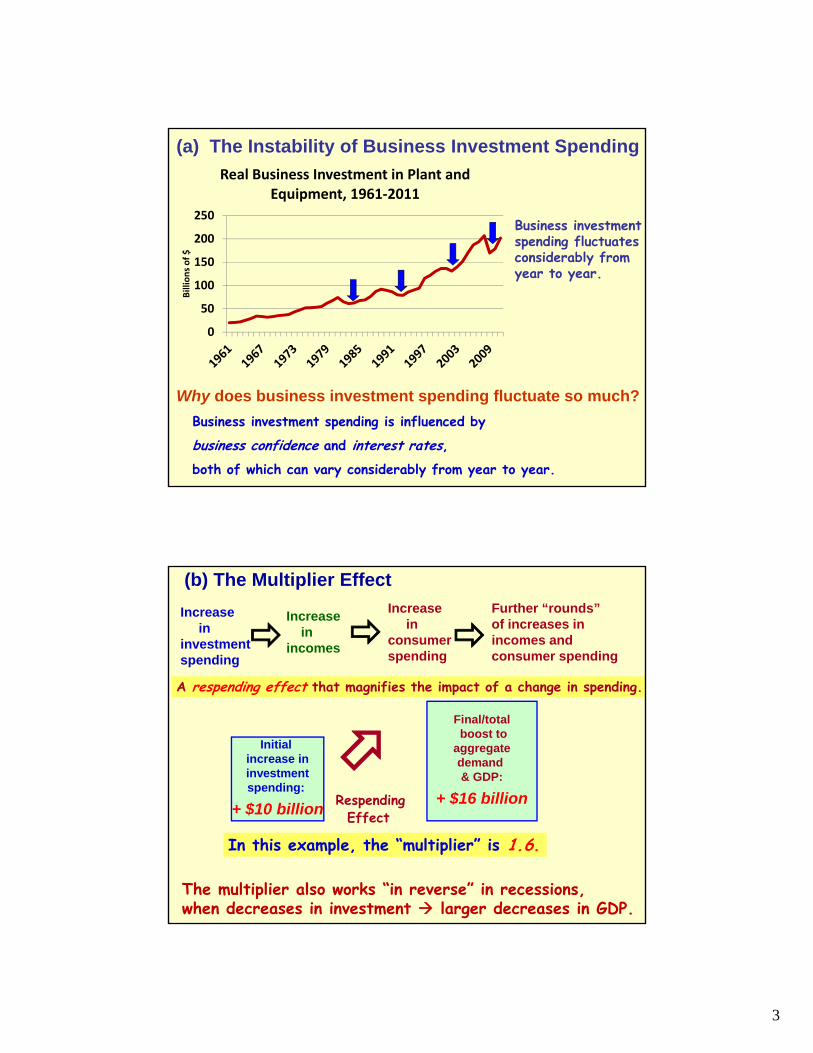

(a) The Instability of Business Investment Spending

Why does business investment spending fluctuate so much?

Business investment spending is influenced by

business confidence and interest rates,both of which can vary considerably from year to year.

Business investmentspending fluctuatesconsiderably from year to year.

0

50

100

150

200

250

Billions of $

Real Business Investment in Plant and Equipment, 1961‐2011

(b) The Multiplier Effect

RespendingEffect

In this example, the “multiplier” is 1.6.

Increasein

investmentspending

Increasein

incomes

Increasein

consumerspending

Further “rounds”of increases inincomes andconsumer spending

A respending effect that magnifies the impact of a change in spending.

Initial increase ininvestmentspending:

+ $10 billion

Final/totalboost to

aggregatedemand & GDP:

+ $16 billion

The multiplier also works “in reverse” in recessions,when decreases in investment larger decreases in GDP.

4

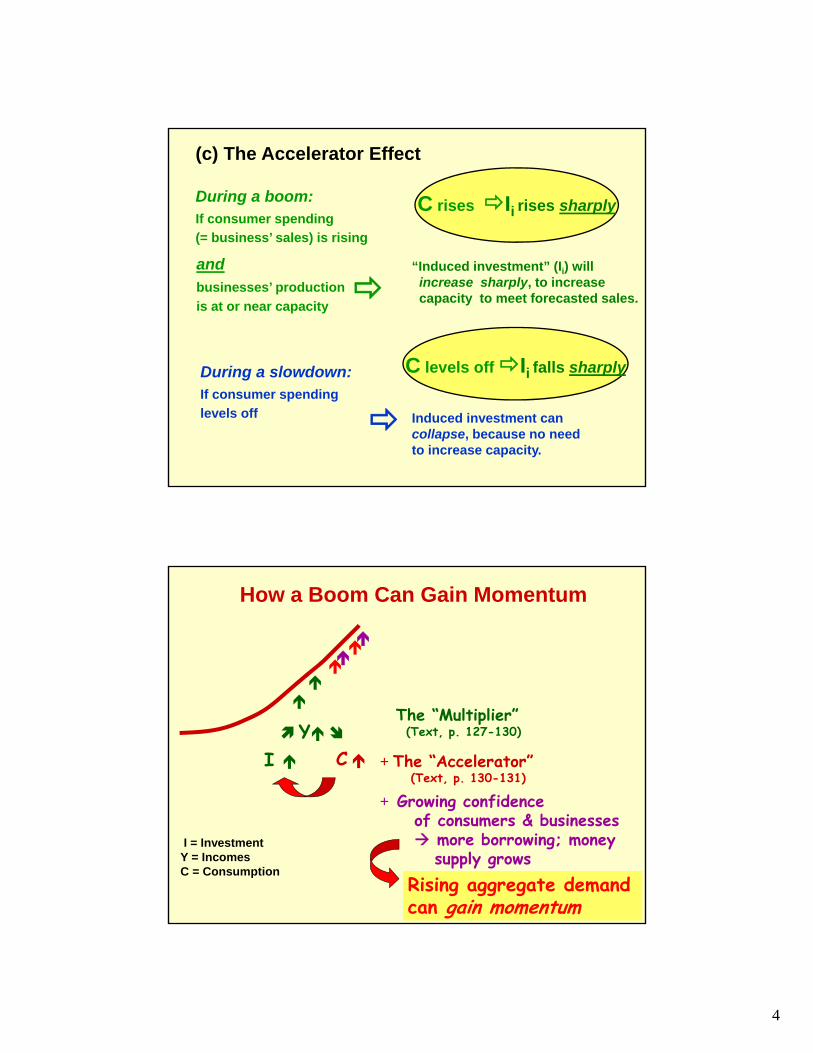

(c) The Accelerator Effect

During a boom:If consumer spending

(= business’ sales) is rising

andbusinesses’ production

is at or near capacity

“Induced investment” (Ii) will increase sharply, to increase capacity to meet forecasted sales.

Induced investment cancollapse, because no need to increase capacity.

During a slowdown:If consumer spending

levels off

C rises Ii rises sharply

C levels off Ii falls sharply

How a Boom Can Gain Momentum

C Y

I

The “Multiplier”(Text, p. 127-130)

+ The “Accelerator”(Text, p. 130-131)

+ Growing confidence of consumers & businesses more borrowing; money

supply grows

Rising aggregate demandcan gain momentum

I = InvestmentY = IncomesC = Consumption

5

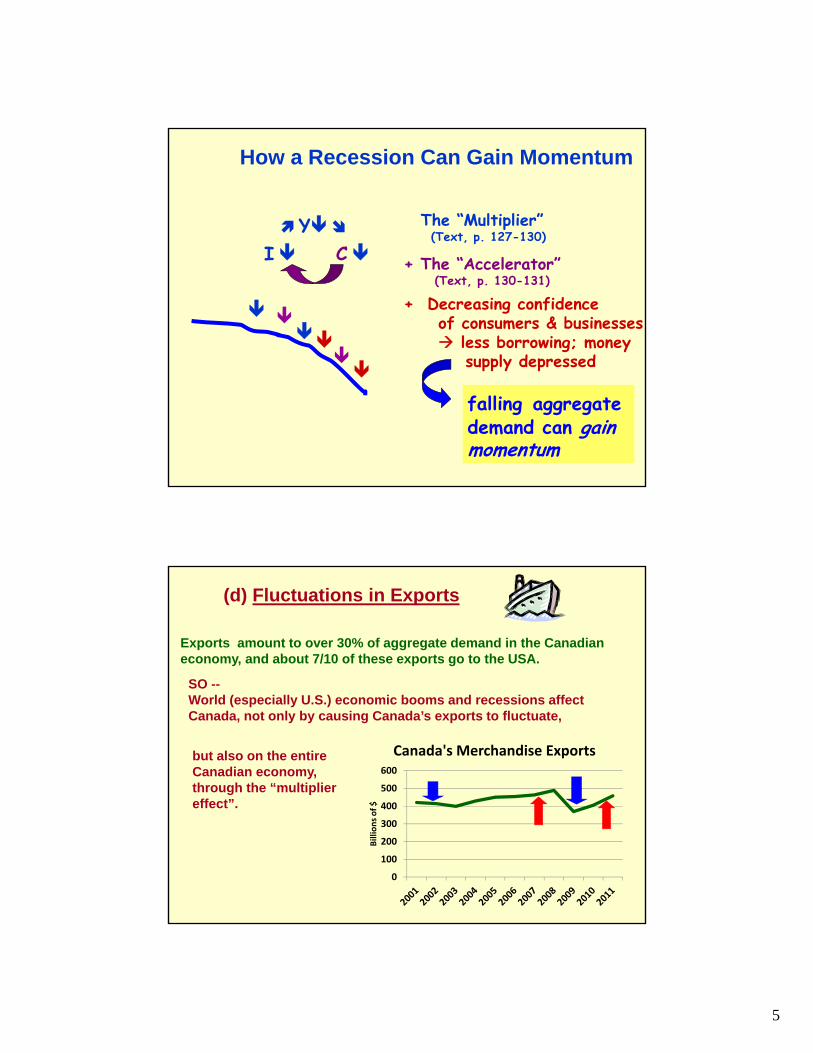

How a Recession Can Gain Momentum

C Y

I

The “Multiplier”(Text, p. 127-130)

+ The “Accelerator”(Text, p. 130-131)

+ Decreasing confidence of consumers & businesses less borrowing; money

supply depressed

falling aggregate demand can gain momentum

(d) Fluctuations in Exports

Exports amount to over 30% of aggregate demand in the Canadian economy, and about 7/10 of these exports go to the USA.

SO --World (especially U.S.) economic booms and recessions affectCanada, not only by causing Canada’s exports to fluctuate,

but also on the entire Canadian economy,through the “multiplier effect”.

0

100

200

300

400

500

600

Billions of $

Canada's Merchandise Exports

6

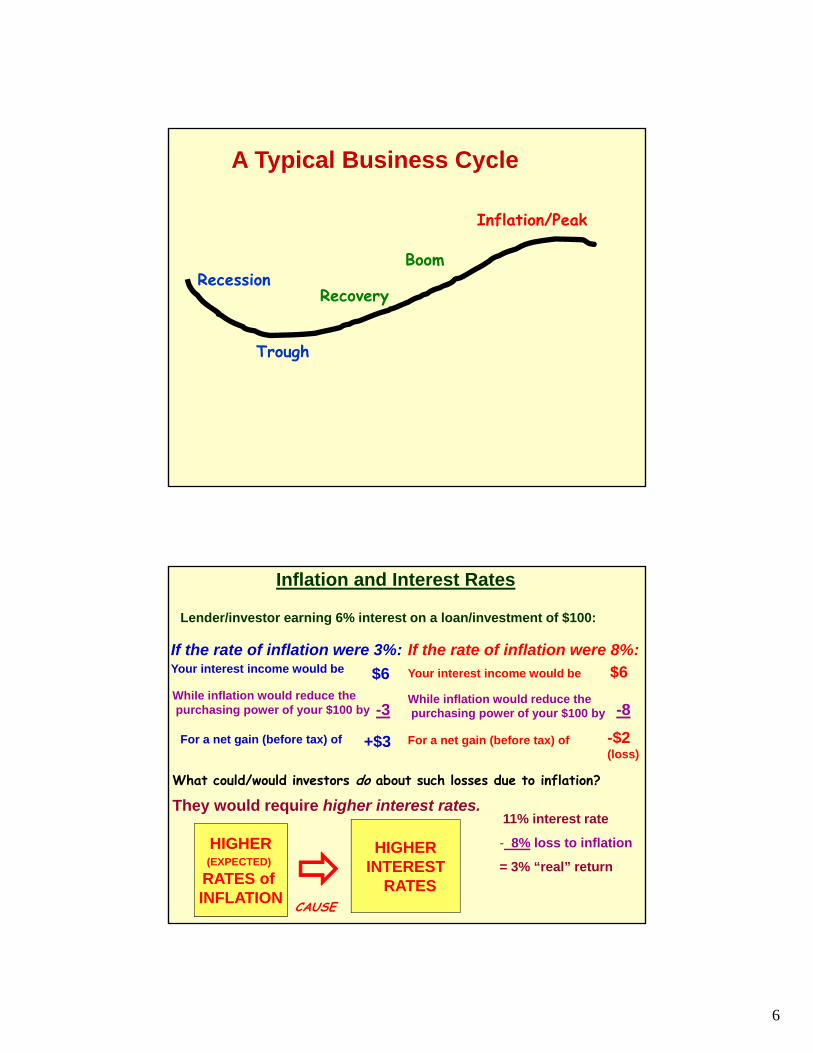

Recession

Trough

Recovery

Boom

Inflation/Peak

A Typical Business Cycle

Inflation and Interest Rates

Lender/investor earning 6% interest on a loan/investment of $100:

If the rate of inflation were 3%:Your interest income would be

While inflation would reduce thepurchasing power of your $100 by

$6

-3

For a net gain (before tax) of +$3

If the rate of inflation were 8%:Your interest income would be $6

While inflation would reduce thepurchasing power of your $100 by

For a net gain (before tax) of

-8

-$2(loss)

What could/would investors do about such losses due to inflation?

They would require higher interest rates.11% interest rate

- 8% loss to inflation

= 3% “real” returnCAUSE

HIGHER(EXPECTED)

RATES of INFLATION

HIGHERINTEREST

RATES

7

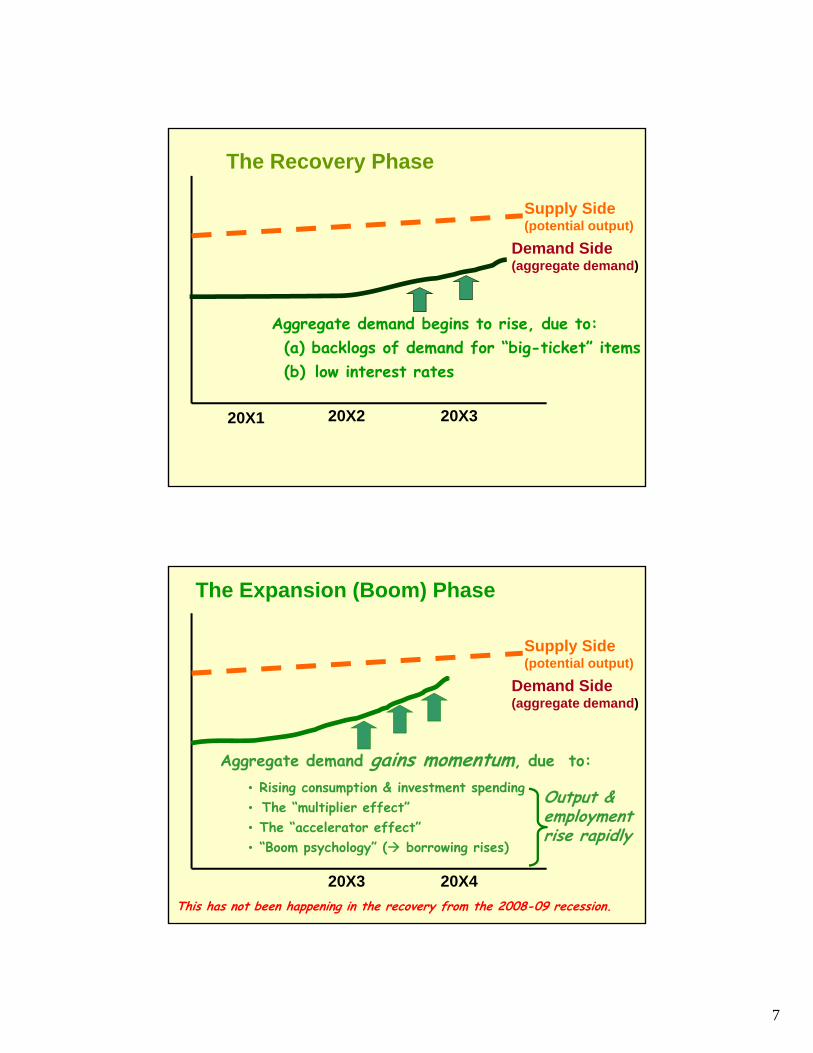

Supply Side(potential output)

20X1 20X2 20X3

Demand Side(aggregate demand)

Aggregate demand begins to rise, due to:(a) backlogs of demand for “big-ticket” items(b) low interest rates

The Recovery Phase

Supply Side(potential output)

20X3 20X4

Demand Side(aggregate demand)

The Expansion (Boom) Phase

Aggregate demand gains momentum, due to:• Rising consumption & investment spending• The “multiplier effect”• The “accelerator effect”• “Boom psychology” ( borrowing rises)

Output & employmentrise rapidly

This has not been happening in the recovery from the 2008-09 recession.

8

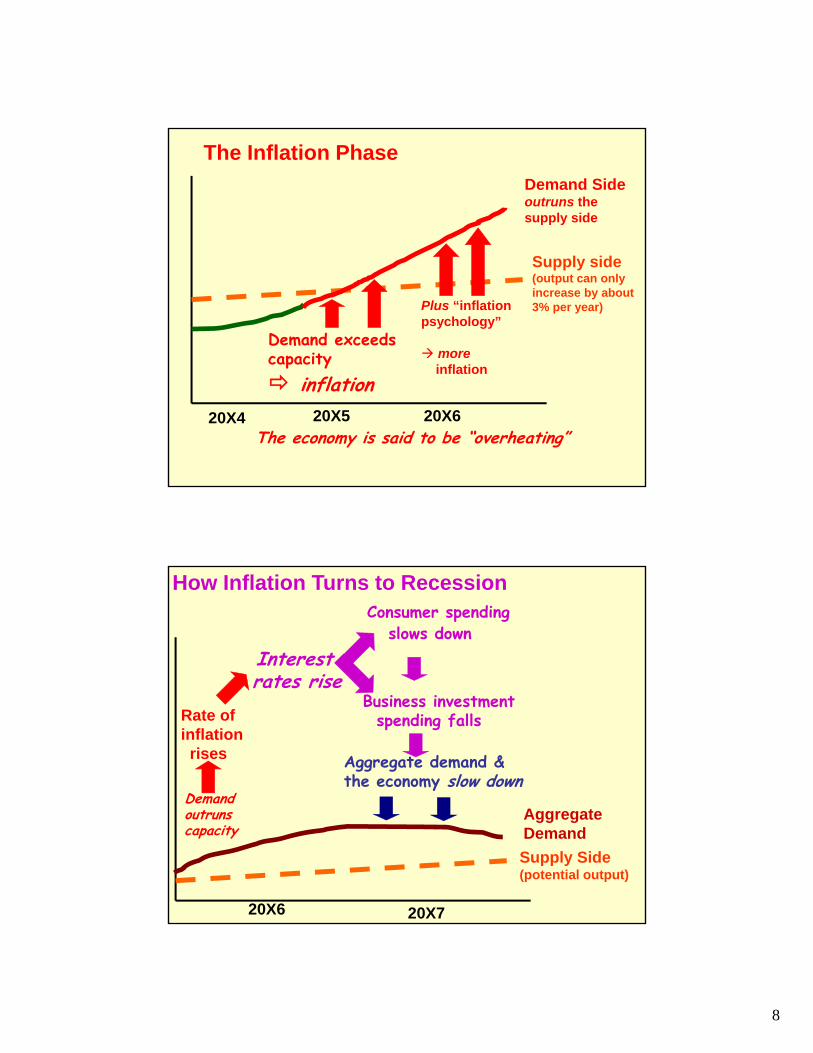

20X4 20X5 20X6

The Inflation Phase

Supply side(output can onlyincrease by about 3% per year)

Demand Sideoutruns the supply side

Demand exceeds capacity inflation

Plus “inflationpsychology”

moreinflation

The economy is said to be “overheating”

How Inflation Turns to Recession

Supply Side(potential output)

AggregateDemand

Demandoutrunscapacity

Interestrates rise

Consumer spendingslows down

Business investment spending falls

Aggregate demand & the economy slow down

Rate ofinflationrises

20X6 20X7

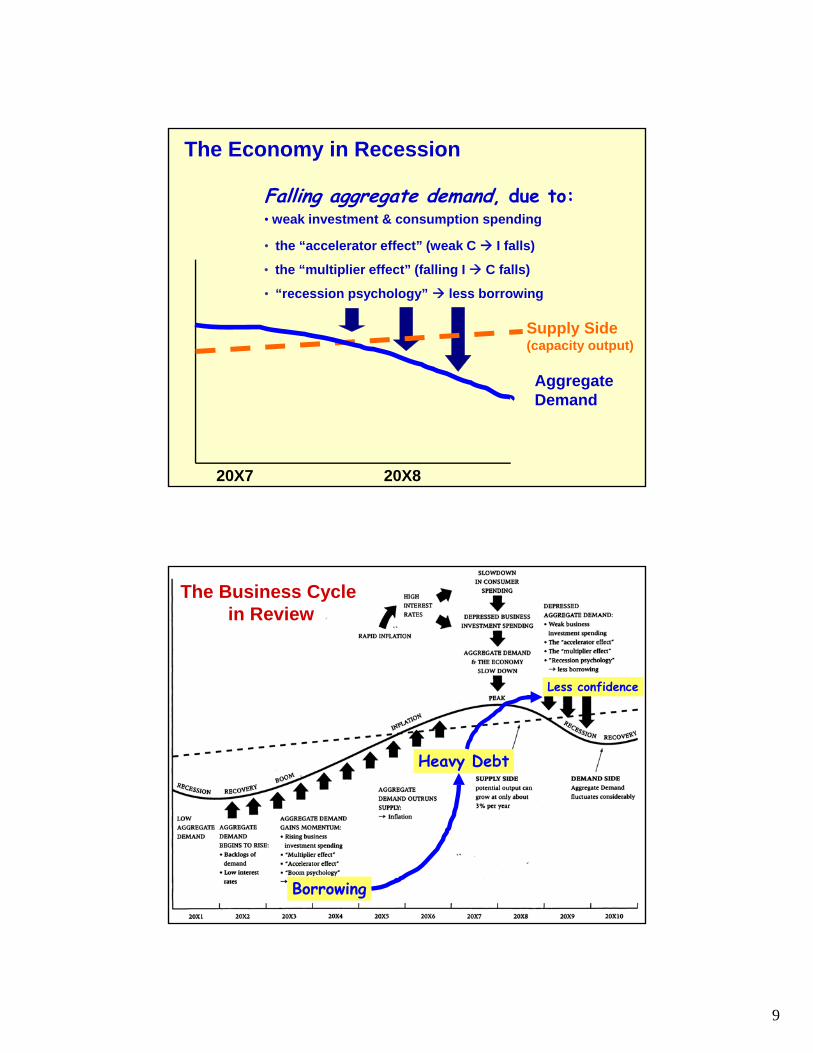

9

Supply Side(capacity output)

AggregateDemand

The Economy in Recession

Falling aggregate demand, due to:• weak investment & consumption spending

• the “accelerator effect” (weak C I falls)

• the “multiplier effect” (falling I C falls)

• “recession psychology” less borrowing

20X7 20X8

Heavy Debt

The Business Cycle in Review

Borrowing

Less confidence

10

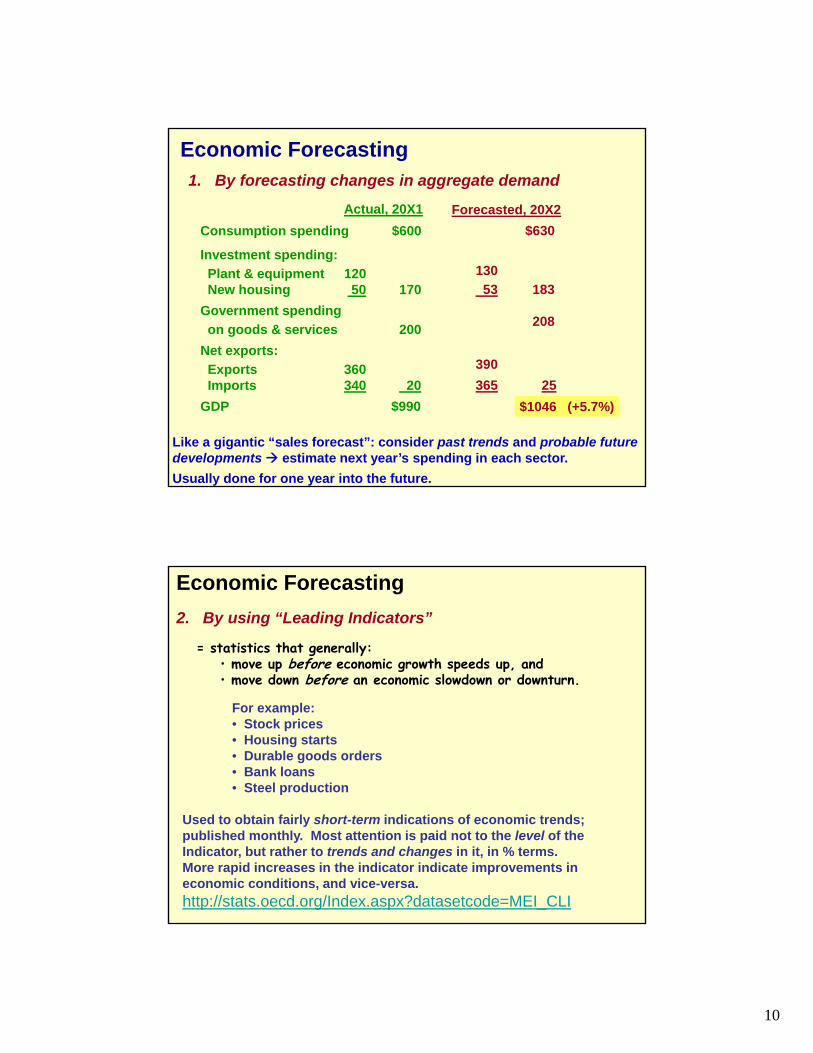

Economic Forecasting1. By forecasting changes in aggregate demand

Actual, 20X1

Consumption spending $600

Investment spending:

Plant & equipment 120New housing 50 170

Government spending

on goods & services 200

Net exports:

Exports 360Imports 340 20

GDP $990

Forecasted, 20X2

$630

130

53 183

208

390

365 25

Like a gigantic “sales forecast”: consider past trends and probable futuredevelopments estimate next year’s spending in each sector.

Usually done for one year into the future.

$1046 (+5.7%)

Economic Forecasting

2. By using “Leading Indicators”

= statistics that generally:• move up before economic growth speeds up, and • move down before an economic slowdown or downturn.

For example:• Stock prices• Housing starts• Durable goods orders• Bank loans• Steel production

Used to obtain fairly short-term indications of economic trends; published monthly. Most attention is paid not to the level of the Indicator, but rather to trends and changes in it, in % terms. More rapid increases in the indicator indicate improvements in economic conditions, and vice-versa.

http://stats.oecd.org/Index.aspx?datasetcode=MEI_CLI

11

http://stats.oecd.org/Index.aspx?datasetcode=MEI_CLI

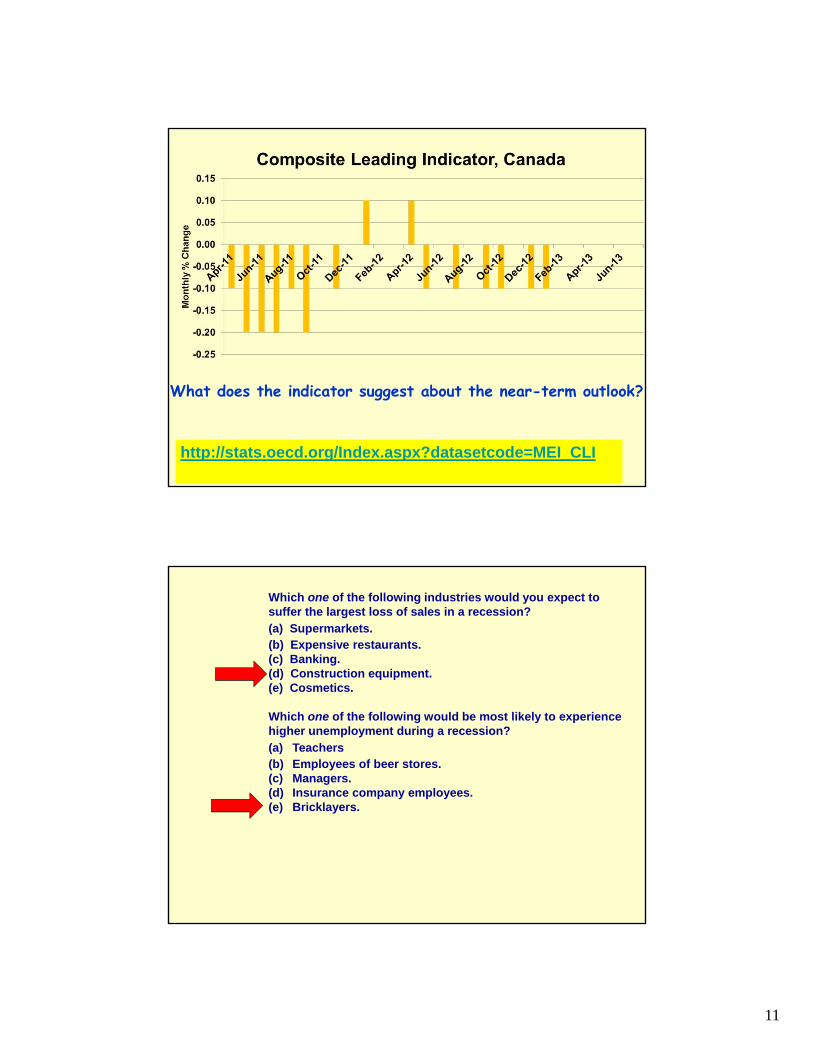

What does the indicator suggest about the near-term outlook?

Which one of the following industries would you expect tosuffer the largest loss of sales in a recession?

(a) Supermarkets.(b) Expensive restaurants.(c) Banking.(d) Construction equipment.(e) Cosmetics.

Which one of the following would be most likely to experiencehigher unemployment during a recession?

(a) Teachers(b) Employees of beer stores.(c) Managers.(d) Insurance company employees.(e) Bricklayers.

12

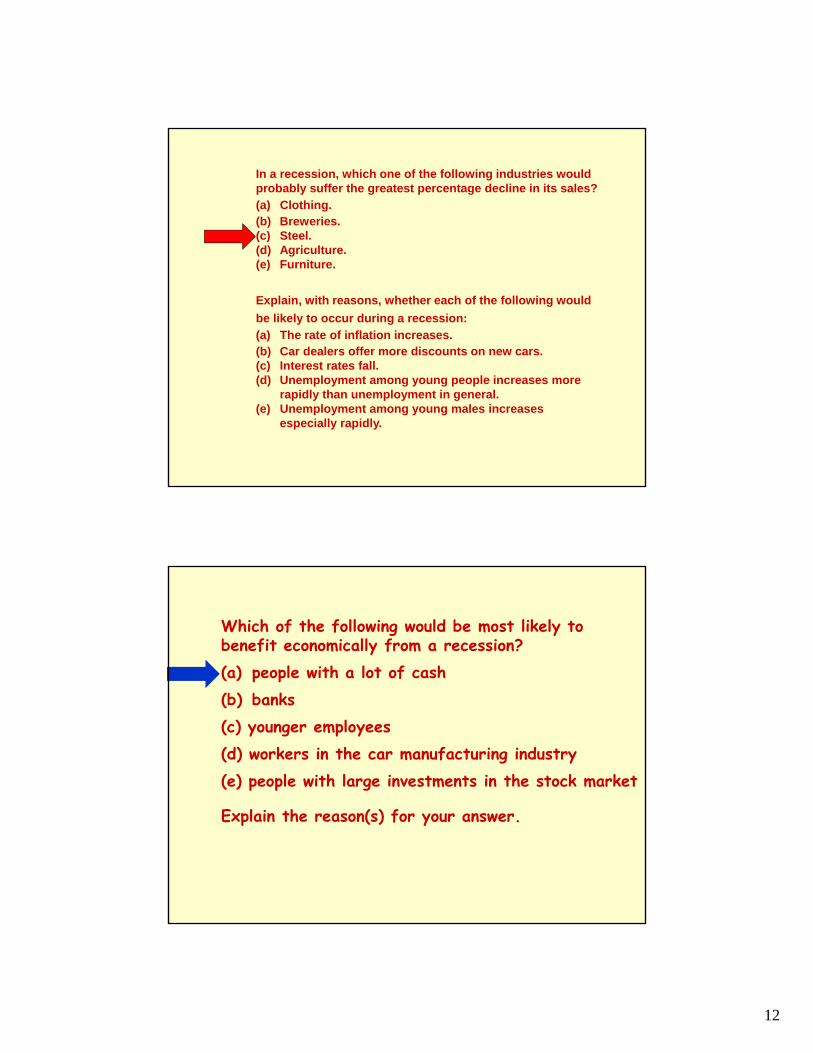

In a recession, which one of the following industries wouldprobably suffer the greatest percentage decline in its sales?

(a) Clothing.(b) Breweries.(c) Steel.(d) Agriculture.(e) Furniture.

Explain, with reasons, whether each of the following would

be likely to occur during a recession:

(a) The rate of inflation increases.(b) Car dealers offer more discounts on new cars.(c) Interest rates fall.(d) Unemployment among young people increases more

rapidly than unemployment in general.(e) Unemployment among young males increases

especially rapidly.

Which of the following would be most likely tobenefit economically from a recession?(a) people with a lot of cash(b) banks(c) younger employees(d) workers in the car manufacturing industry(e) people with large investments in the stock market

Explain the reason(s) for your answer.

13

Update on the current economic situation

Read the Chapter 6 “Recent Developments” file on SLATE.

UPDATE ON THE CURRENT SITUATION

Unusual nature of 2002-07 U.S. Economic Boom:

Boom was led by extremely high spending by U.S.consumers, largely financed by borrowing, and usingtheir homes as collateral.

AND high demand for housing created a housing price“bubble”, which increased the ability of consumersto borrow even more against their homes.

AND when the boom ended, it was not because rising interest rates slowed the economy down – it was muchmore serious, and sudden.

Credit was very readily available and demand high, butthe rate of inflation remained low, and interest ratesremained unusually low.

14

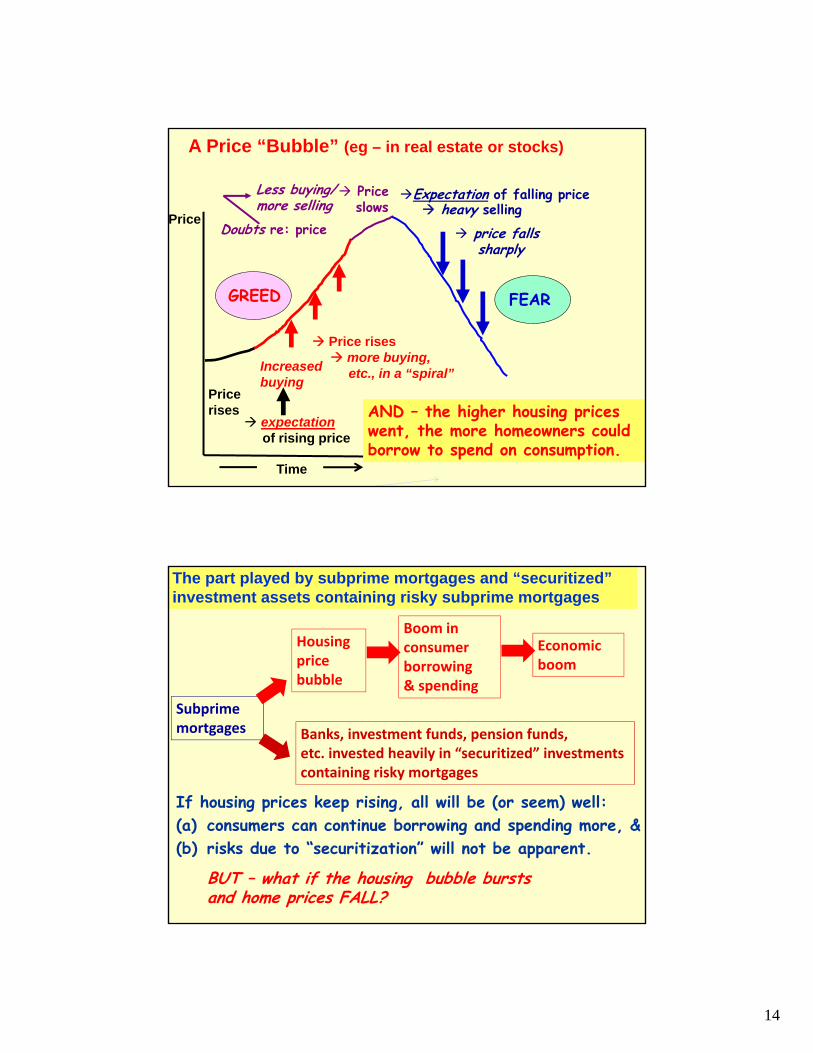

A Price “Bubble” (eg – in real estate or stocks)

Price

Pricerises

expectationof rising price

Increasedbuying

Price rises more buying,

etc., in a “spiral”

Doubts re: price

Less buying/more selling

Priceslows

Expectation of falling price

price fallssharply

GREED FEAR

heavy selling

Time

AND – the higher housing priceswent, the more homeowners couldborrow to spend on consumption.

Subprimemortgages

Housingprice bubble

Boom in consumer borrowing& spending

Economic boom

Banks, investment funds, pension funds, etc. invested heavily in “securitized” investments containing risky mortgages

If housing prices keep rising, all will be (or seem) well: (a) consumers can continue borrowing and spending more, &(b) risks due to “securitization” will not be apparent.

BUT – what if the housing bubble bursts and home prices FALL?

The part played by subprime mortgages and “securitized”investment assets containing risky subprime mortgages

15

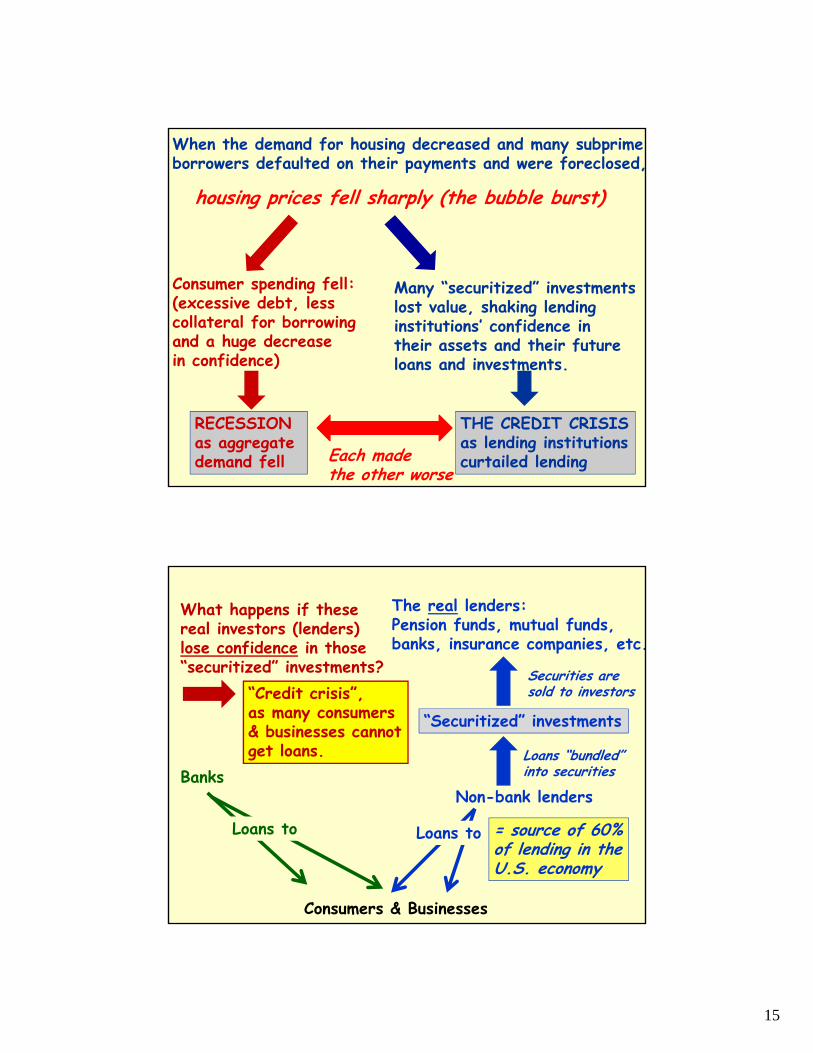

When the demand for housing decreased and many subprimeborrowers defaulted on their payments and were foreclosed,

housing prices fell sharply (the bubble burst)

Consumer spending fell:(excessive debt, lesscollateral for borrowingand a huge decrease in confidence)

Many “securitized” investmentslost value, shaking lending institutions’ confidence in their assets and their future loans and investments.

THE CREDIT CRISISas lending institutionscurtailed lending

RECESSIONas aggregate demand fell Each made

the other worse

Consumers & Businesses

BanksNon-bank lenders

= source of 60%of lending in theU.S. economy

“Securitized” investments

Loans “bundled” into securities

Securities aresold to investors

The real lenders:Pension funds, mutual funds,banks, insurance companies, etc.

What happens if thesereal investors (lenders)lose confidence in those“securitized” investments?

“Credit crisis”,as many consumers& businesses cannotget loans.

Loans to Loans to

16

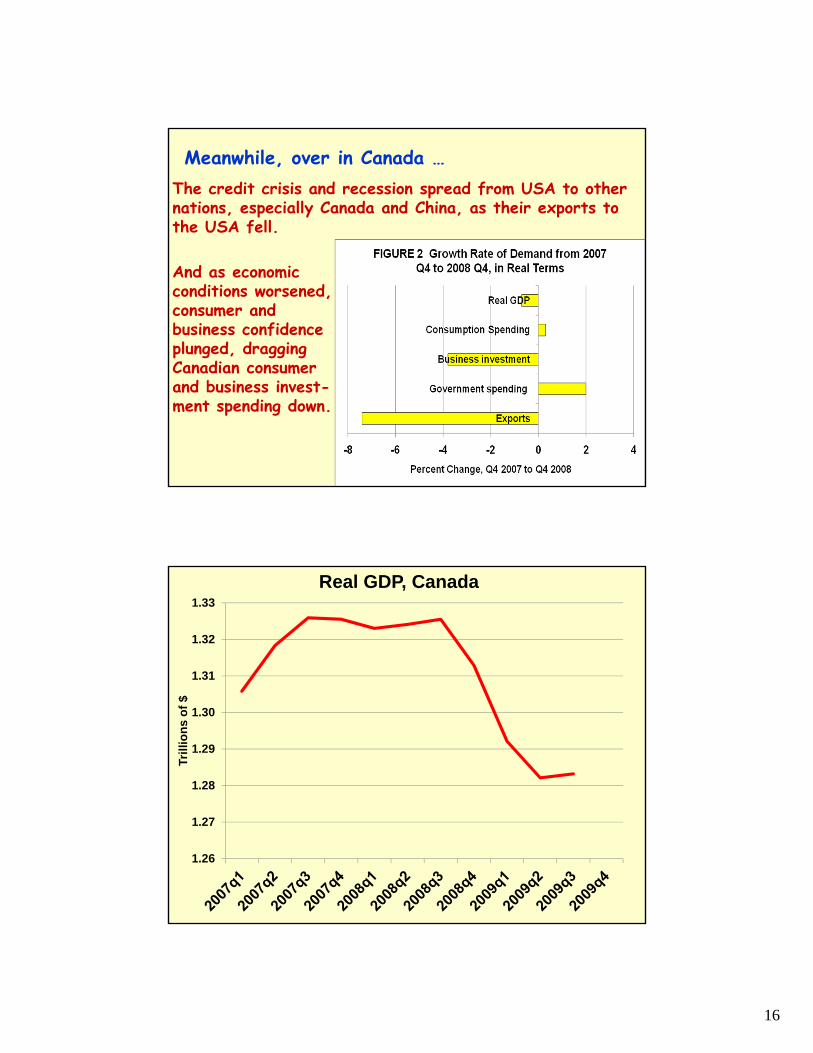

Meanwhile, over in Canada …The credit crisis and recession spread from USA to other nations, especially Canada and China, as their exports to the USA fell.

And as economic conditions worsened,consumer andbusiness confidenceplunged, dragging Canadian consumerand business invest-ment spending down.

1.26

1.27

1.28

1.29

1.30

1.31

1.32

1.33

Tri

llio

ns

of

$

Real GDP, Canada

17

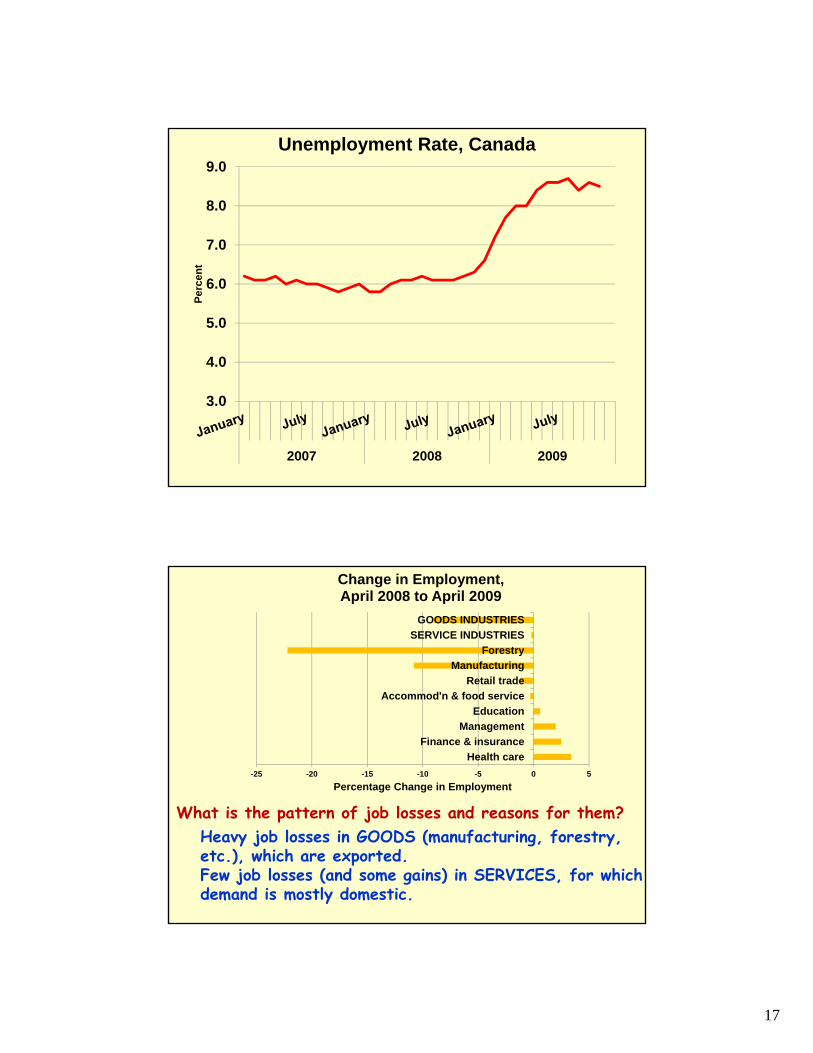

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2007 2008 2009

Per

cen

t

Unemployment Rate, Canada

-25 -20 -15 -10 -5 0 5

Health care

Finance & insurance

Management

Education

Accommod'n & food service

Retail trade

Manufacturing

Forestry

SERVICE INDUSTRIES

GOODS INDUSTRIES

Percentage Change in Employment

Change in Employment, April 2008 to April 2009

What is the pattern of job losses and reasons for them?Heavy job losses in GOODS (manufacturing, forestry, etc.), which are exported.Few job losses (and some gains) in SERVICES, for whichdemand is mostly domestic.

18

0

5

10

15

20

25

Sep

tem

ber

Oct

ob

er

No

vem

ber

De

cem

be

r

Jan

uar

y

Feb

ruar

y

Ma

rch

Ap

ril

Ma

y

2008 2009

Per

cen

t

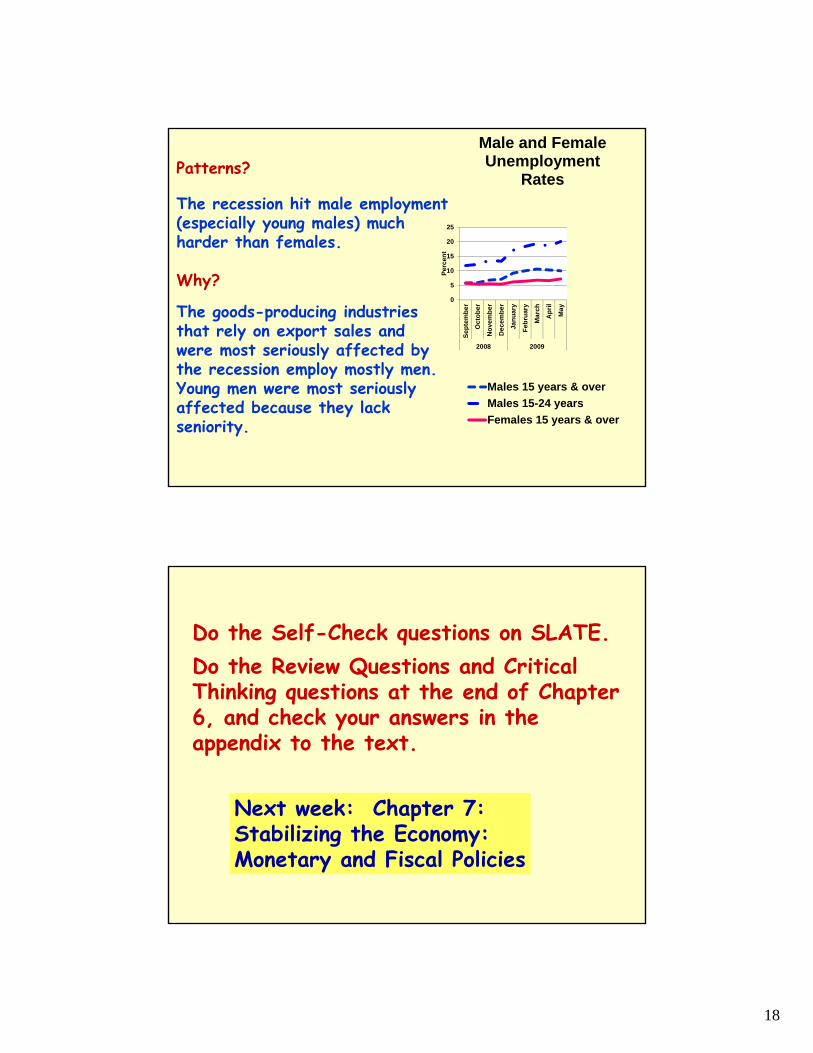

Male and Female Unemployment

Rates

Males 15 years & over

Males 15-24 years

Females 15 years & over

Patterns?

The recession hit male employment (especially young males) much harder than females.

Why?

The goods-producing industriesthat rely on export sales and were most seriously affected by the recession employ mostly men.Young men were most seriouslyaffected because they lackseniority.

Next week: Chapter 7:Stabilizing the Economy:Monetary and Fiscal Policies

Do the Self-Check questions on SLATE.Do the Review Questions and Critical Thinking questions at the end of Chapter 6, and check your answers in the appendix to the text.