legal aspects of doing business in belgium - loyens &...

TRANSCRIPT

Legal aspects of doing business in Belgium

Legal aspects of doing business in Belgium

Editor Geert Bogaert

Share the Expertise www.loyensloeff.com

Loyens & Loeff is an independent full-service law firm

specialised in providing legal and tax advice to companies,

financial organisations and governments. The intensive

cooperation between lawyers and tax attorneys (and in the

Netherlands, civil law notaries) places Loyens & Loeff in a

unique position in its home market, the Benelux.

When providing international advice, Loyens & Loeff

maintains close ties with leading foreign law firms and

tax advisers. Worldwide, Loyens & Loeff has over 1.600

employees, including about 900 tax attorneys and lawyers

in our six Benelux offices and eleven branches in the major

international financial centres.

Share the Expertise

12-12-EN

-LAB

1loyens & loeff Legal aspects of doing business in Belgium

Legal aspects of doing business in Belgium

Editor: Geert Bogaert

2 3loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

Preface

A legal guide to the broad spectrum of issues related to doing business is bound to be incomplete: what has been attempted is to provide a condensed inventory of the most commonly encountered issues. An attempt is made to be sufficiently specific and detailed, but each factual situation may have particular aspects not covered in the text.

This publication is the product of a large team. Each is a specialist in the area covered. The purpose of the guide is to respond to the increased need for instant information on various legal aspects of doing business. It is a product of the firm’s continued effort to invest in knowledge and to share this result with its clients.

The present information hopefully allows for a better understanding of the legal business environment, and should allow the reader to more easily identify detailed issues as well as assist in raising focused questions. It is our belief that a law firm should, in the first place, create added value and this starts with making sure the basics are readily available.

The law changes constantly. We have taken account of the law, as it stands at 31 January 2013. Readers are, therefore, well advised to always seek up to date or more detailed specialised advice.

Marc Vermylen and Xavier Clarebout Geert BogaertManagement Team Editor

© Loyens & Loeff, 2013

Although the Legal aspects of doing business in Belgium booklet has been compiled with great care, Loyens & Loeff cannot

accept any responsibility for the consequences of making use of this publication without its cooperation. The contributions to this

book contain personal views of the authors and therefore do not reflect the opinion of Loyens & Loeff.

All rights reserved. No publications may be duplicated, saved in an automated database or made public, in any form or in any

way, whether electronically, mechanically, by photocopying, recording or in any other manner, without the prior written consent

of Loyens & Loeff.

4 5loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

2. Miscellaneous corporate issues: liability of directors and shareholders 322.1 Introduction 322.2 Directors’ liability 322.2.1 General 322.2.2 Civil liability 322.2.3 Criminal liability 392.3 Shareholders’ liability 402.3.1 General principle: limited liability for shareholders of an NV/SA and a BVBA/SPRL 402.3.2 Exceptions: statutory and judicial limitations to the principle of limited liability 412.3.3 Shareholders’ liability in tort 43

3. Financial law 443.1 Secured lending 443.1.1 General introduction 443.1.2 Licences 443.1.3 Corporate resolutions 443.1.4 Financial assistance 443.1.5 Corporate interest 463.1.6 Security in accordance with Belgian law 473.1.7 Security agents and trustees 503.2 Securitisation 513.2.1 Optional regime 513.2.2 Regulated securitisation 513.2.3 Contractual securitisation 523.2.4 Mobilization Act 533.3 Euroclear 543.3.1 The Euroclear System 543.3.2 Taking collateral in Euroclear 543.4 Future legislation 55

4. Competition law 564.1 Introduction: Competition rules modelled on their European counterparts 564.2 Agreements restricting competition 574.3 Abuse of dominance 574.4 Merger control 584.5 Enforcement of the prohibition on restrictive agreements and abuse of dominance 594.6 Review of the Belgian Competition Act 61

Index

Preface 31. The legal framework for one’s business 131.1 Introduction 131.2 Summary of Main differences between the NV/SA and the BVBA/SPRL 131.3 Establishing an NV/SA or BVBA/SPRL 141.3.1 No governmental control 141.3.2 Founders 151.3.3 Incorporation procedure – contribution – financial plan 151.3.4 Capital tax 161.3.5 Pre-incorporation transactions 171.3.6 Corporate books 171.3.7 Filing with the Commercial Court and publication 171.3.8 Registration with the Crossroads Database for Enterprises 171.3.9 Other filing requirements 181.3.10 Registration with the VAT authorities 181.3.11 Registration with the social security administration 191.4 Articles of association 191.4.1 General 191.4.2 Corporate name 201.4.3 Registered office 201.4.4 Corporate purpose 201.4.5 Corporate capital 201.5 Shares 211.5.1 Types of shares 211.5.2 Transfer of shares 221.6 Mandatory internal bodies 231.6.1 General 231.6.2 Board of directors – (Board of) managers 241.6.3 General meeting of shareholders 261.6.4 Management Committee (optional body within an NV/SA) 271.6.5 Daily management 281.7 Annual accounts 281.8 Dissolution and liquidation 291.8.1 General 291.8.2 Standard procedure for liquidation of an NV/SA or BVBA/SPRL 29

6 7loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

7.2.1 International sources 837.2.2 National sources 847.3 Union representation 847.3.1 Trade unions 847.3.2 Works Council (plant/company level) 857.3.3 Committee for Prevention and Protection at Work 857.3.4 Social elections 867.3.5 Union Delegation 867.3.6 Employer’s federations 867.4 Strikes and plant closures 867.5 Employment contracts 877.5.1 Characteristics 877.5.2 Form 877.5.3 Contracts for an indefinite term 887.5.4 Contracts for a fixed term or a specific task 887.5.5 Part-time employment 887.5.6 Particular employment contracts 887.6 Clauses 897.6.1 Probation period 897.6.2 Non-compete clauses 897.6.3 Invention and copyrights 917.7 Salary 927.7.1 Fixed salary 927.7.2 Variable salary 937.7.3 Fringe benefits 937.8 Suspension 947.9 Termination 947.9.1 Termination of indefinite term contracts 957.9.2 Termination of fixed-term contracts 987.9.3 Termination for serious cause 987.10 Protected employees 987.10.1 Candidates and members of the Works Council or Committee for Prevention and Protection 987.10.2 Members of the Union Delegation 997.11 Work regulations 997.11.1 Working hours 997.11.2 Overtime work 1007.11.3 Annual holidays 1007.11.4 National holidays 1007.11.5 Time credit (career break) 100

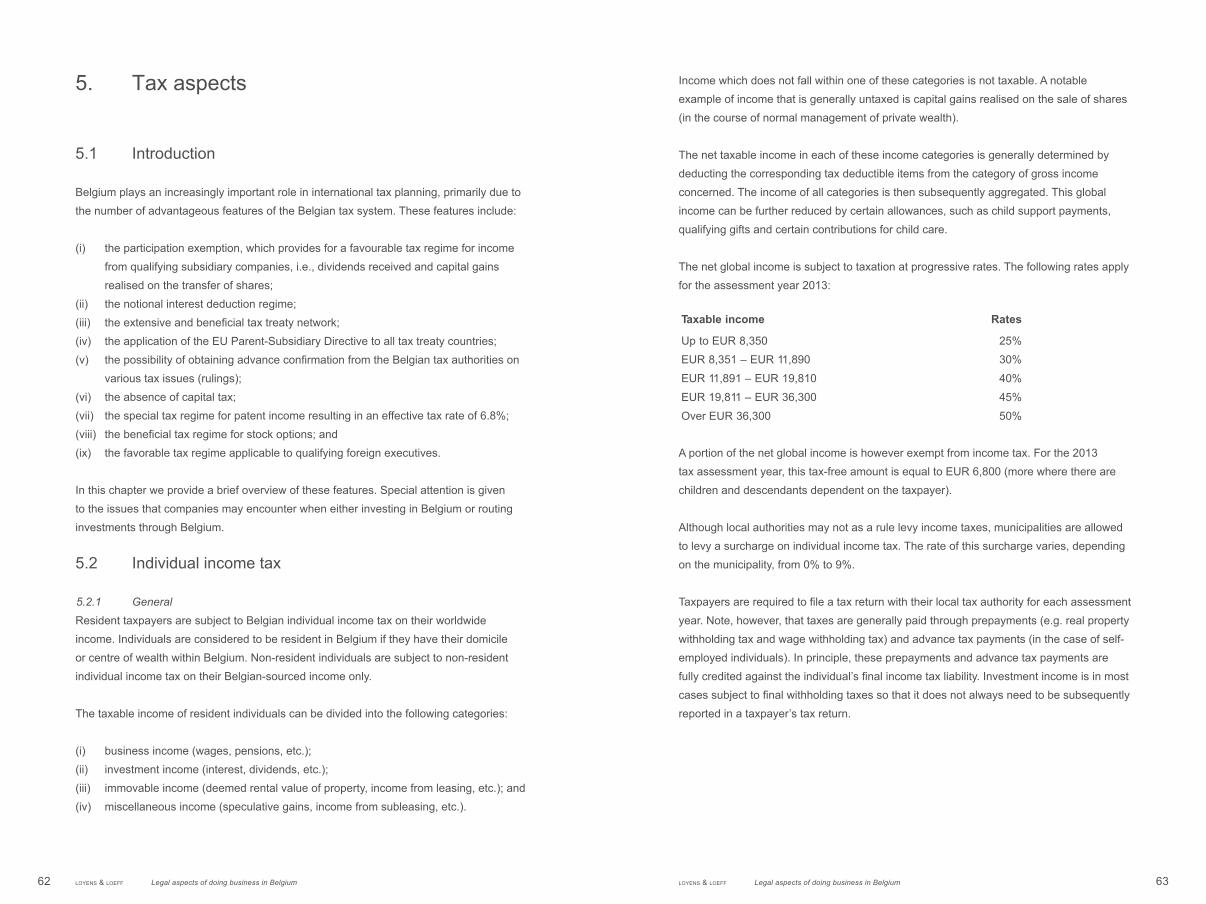

5. Tax aspects 625.1 Introduction 625.2 Individual income tax 625.2.1 General 625.2.2 Stock options 645.2.3 Special taxation regime for foreign executives 655.3 Corporate income tax 665.3.1 General 665.3.2 Participation exemption 675.3.3 Deductibility of costs in the acquisition of a participation 695.3.4 Ruling policy 695.3.5 Incentive regulations 705.3.6 Non-resident companies 725.4 Withholding taxes 735.4.1 Dividend withholding tax 735.4.2 Withholding tax on interest and royalties 745.5 Capital tax 745.6 Other taxes 745.6.1 Transfer tax 745.6.2 Tax on stock exchange transactions 745.7 Tax treaty network 75

6. VAT and import duties 776.1 Value added tax 776.1.1 General 776.1.2 Taxable persons 776.1.3 Tax base 786.1.4 Exemptions 786.1.5 Tax rates 786.1.6 VAT on imported goods 786.1.7 Formalities 796.2 Import duties 796.2.1 General 796.2.2 Key elements to establish whether an imported good is dutiable 796.2.3 The Modernized Customs Code and its Implementing provisions 816.2.4 Introduction of the Authorised Economic Operator (AEO) 82

7. Employment law & social security 837.1 Introduction 837.2 Sources of employment law 83

8 9loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

8.3.3 Scope 1208.3.4 Formation 1218.3.5 Duration 1218.3.6 Termination 1228.3.7 Repurchase of inventory 1278.3.8 Sub-distributors 1278.3.9 Statute of limitations 1278.3.10 Jurisdiction (courts/arbitration), governing law and conflicts of laws 1288.4 Franchising 1298.4.1 General 1298.4.2 Definition 1298.4.3 Different categories of franchise agreements 1308.4.4 Formation 1318.4.5 Pre-contractual relationship: the Act of 19 December 2005 regarding pre-contractual information within the framework of commercial co-operation agreements the ‘Act’) 1318.4.6 Contractual relationship 1348.4.7 Jurisdiction (courts/arbitration), governing law and conflicts of laws 134

9. Intellectual property rights 1369.1 Introduction 1369.2 Patents 1369.2.1 Registration under Belgian law 1369.2.2 Registration under the European Patent Convention (EPC) 1389.2.3 Registration as Unitary Patent (UP) 1399.2.4 Registration under the Patent Cooperation Treaty 1409.2.5 Competition/EC Treaty 1419.3 Trademarks 1419.3.1 Benelux registration 1419.3.2 International trademarks 1449.3.3 Community trademarks 1459.4 Copyright (or author’s right) 1459.4.1 Legal framework 1459.4.2 Protectability 1469.4.3 Duration 1479.4.4 Assignment and license 1479.4.5 Employees’ works – commissioned work 1479.4.6 Miscellaneous 1489.5 Protection for (industrial) designs 1489.5.1 Benelux registration 148

7.12 Use of language 1017.13 Discrimination 1017.14 Social documents 1017.15 Employee liability 1027.16 Posting 1027.17 Health and safety 1027.18 Violence and moral or sexual harassment at work 1037.19 Privacy 1037.20 Social security 1037.20.1 General 1037.20.2 Unemployment 1047.20.3 Health insurance 1047.20.4 Family allowance 1057.20.5 Retirement 1057.20.6 Occupational illnesses 1057.20.7 Self-employed 1067.21 Regulatory 1067.21.1 Work permits 1067.21.2 Professional cards 1077.21.3 Residence permits 107

8. Commercial agency, distributorship and franchising 1088.1 Introduction 1088.2 Commercial agency 1088.2.1 Definition of the agency agreement/Scope 1088.2.2 Commercial agent vs. sales representative (handelsvertegenwoordiger/représentant de commerce) 1098.2.3 Formation of the commercial agency agreement 1108.2.4 Duration 1118.2.5 Remuneration 1118.2.6 Termination 1138.2.7 Clientele and goodwill indemnity 1158.2.8 Supplementary indemnity 1168.2.9 Non-compete clause 1178.2.10 ‘Delcredere’ clause 1188.2.11 Statute of limitations 1188.2.12 Jurisdiction (courts/arbitration), governing law and conflicts of laws 1198.3 Distribution 1198.3.1 General 1198.3.2 Definition 120

10 11loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

12.4.3 Bankruptcy proceedings 17812.4.4 Creditors’ rights 18012.4.5 Claw-back provisions 181

13. Arbitration and mediation in Belgium 18313.1 Introduction 18313.2 Mediation 18313.2.1 Legislation and General Principles 18313.2.2 Conditions and characteristics of a mediation 18413.2.3 Different types of mediations 18513.2.4 Conclusion about mediation 18713.3 Arbitration 18713.3.1 General Principles 18713.3.2 Different types of arbitrations 18813.3.3 Conditions for a valid arbitration 19013.3.4 Importance and effects of the arbitration agreement 19413.3.5 Proceedings 19913.3.6 Arbitral Awards 19713.3.7 Enforcement 19813.3.8 Annulment 19913.3.9 Conclusion about arbitration 200

14. Useful addresses 20114.1 Official authorities 20114.1.1 Europe 20114.1.2 Belgium 20114.1.3 Flemish Community in Belgium and Flemish Region 20114.1.4 Walloon Region 20114.1.5 French Community in Belgium 20114.1.6 German-speaking Community in Belgium 20114.1.7 Brussels-Capital Region 20214.2 Legal 20214.3 Business and Trade 20214.4 Corporate 20314.5 Financial 20314.6 Taxation 20414.7 Labour and Social Security 20414.7.1 Labour 20414.7.2 Social security 20414.7.3 Employer organisations 205

9.5.2 Protectability 1489.5.3 Duration 1499.5.4 Assignment and license 1499.5.5 Employee rules 1499.5.6 Copyright (or author’s rights) 1499.5.7 Community designs 1499.6 Databases 150

10. Data protection 15110.1 Introduction 15110.2 General principles for lawful data processing 15210.3 Rights of the data subject: right of access, rectification and opposition 15310.4 Confidentiality and security of processing 15310.5 Prior notification and public nature of the processing 15410.6 Transfer of personal data 15410.7 Rules regarding the use of cookies 154

11. Real Estate, Town Planning and Environment 15611.1 Investing in Real estate 15611.2 Entitlements to real estate 15611.2.1 Immovable property 15611.2.2 Rights in rem 15711.2.3 Public and private domain 16111.3 Town planning and environment 16211.3.1 Town planning: building permits and zoning plans 16211.3.2 Environmental permits 16411.3.3 Soil contamination 16611.3.4 Energy performance of buildings (EPB) 168

12. Companies in distress 17112.1 Introduction 17112.2 Amicable arrangement outside judicial reorganisation 17112.3 Judicial reorganisation 17212.3.1 Purpose of the judicial reorganisation proceedings 17212.3.2 Conditions for judicial reorganisation 17212.3.3 Judicial reorganisation proceedings 17212.3.4 Creditors’ rights 17612.4 Bankruptcy 17712.4.1 Purpose of bankruptcy proceedings 17712.4.2 Conditions for bankruptcy 178

12 13loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

1. The legal framework for doing business

1.1 Introduction

When a foreign company decides to set up a business in Belgium, it must decide whether it wants to do so through a branch (which does not have legal personality itself) or through a subsidiary (being a separate entity with legal personality).

Most foreign companies opt for a subsidiary. Such subsidiaries can take several legal forms under Belgian law but the most commonly used are:

(i) the public limited liability company (naamloze vennootschap or ‘NV’ in Dutch/société anonyme or ‘SA’ in French); and

(ii) the private limited liability company (besloten vennootschap met beperkte aansprakelijkheid or ‘BVBA’ in Dutch/société privée à responsabilité limitée or ‘SPRL’ in French).

As the NV and the BVBA are used in the vast majority of cases, we will concentrate on their main features in this publication, without going into further detail on other types of companies.

1.2 Summary of main differences between the NV/SA and the BVBA/SPRL

Originally, the NV/SA was mainly seen as a vehicle for medium-sized or large undertakings, whereas the BVBA/SPRL was intended to be used for small businesses where management and ownership often coincide. To this day, the BVBA/SPRL is mostly used for smaller (privately-owned) businesses. Large multinational groups tend to incorporate their Belgian subsidiaries under the form of an NV/SA (though some may opt for the BVBA/SPRL for foreign tax transparency reasons).

From a Belgian tax perspective, an NV/SA and a BVBA/SPRL are subject to the same corporate tax rules.

14.7.4 Organisations for self-employed workers 20514.7.5 Trade Unions 20514.8 Intellectual property 20514.9 Town planning and Environment 20614.9.1 Federal 20614.9.2 Flanders 20614.9.3 Wallonia 20614.9.4 Brussels 20614.10 Energy 20614.10.1 Federal 20614.10.2 Flanders 20714.10.3 Wallonia 20714.10.4 Brussels 207

15. Loyens & Loeff contacts 208

16. Loyens & Loeff offices 209

14 15loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

However, if the company intends to engage in certain regulated activities (e.g. banking or insurance activities, pharmaceuticals, transport, etc.), prior approval from the relevant governmental authorities will be required.

1.3.2 FoundersA BVBA/SPRL can be incorporated by one or more persons ans so it can have only one founder/shareholder. This possibility is however subject to several restrictions which have an important impact on the liability of the sole founder/shareholder:

• If the sole founding shareholder of a BVBA/SPRL is a legal entity, this legal entity will be jointly and severally liable for all obligations and liabilities of the BVBA/SPRL;

• If, during the existence of a BVBA/SPRL, a legal entity becomes the sole shareholder of a BVBA/SPRL and remains the sole shareholder for more than one year, it will become jointly and severally liable for all obligations and liabilities incurred by the BVBA/SPRL as from the moment the legal entity became its sole shareholder; and

• An individual who is the sole shareholder of a BVBA/SPRL will become jointly and severally liable for all obligations and liabilities of any other BVBA/SPRL of which it becomes the sole shareholder (either through incorporation or through transfer of shares).

An NV/SA must be incorporated by at least two persons, individuals or legal entities. If one or more of these founding shareholders together holds at least one-third of the capital, it or they may be designated as “founders” resulting in the other shareholders being considered as mere subscribers. This has important consequences as there are specific rules on the liability of founders of an NV/SA which do not apply to mere subscribers (or subsequent shareholders) (see Chapter 2).

The founders of an NV/SA or a BVBA/SPRL may be of any nationality and may be domiciled anywhere.

All founding shareholders must be present or represented at the incorporation meeting, which must take place before a notary. A shareholder can be represented by means of a written power of attorney. In principle, such power of attorney does not have to be notarised or legalised.

1.3.3 Incorporation procedure – contribution – financial planThe incorporation of an NV/SA or a BVBA/SPRL is recorded by a notary in a notarial deed of incorporation (oprichtingsakte/acte de constitution). This deed of incorporation must contain, among other things, the company’s first articles of association (statuten/statuts) and a description of the contribution made by each founding shareholder.

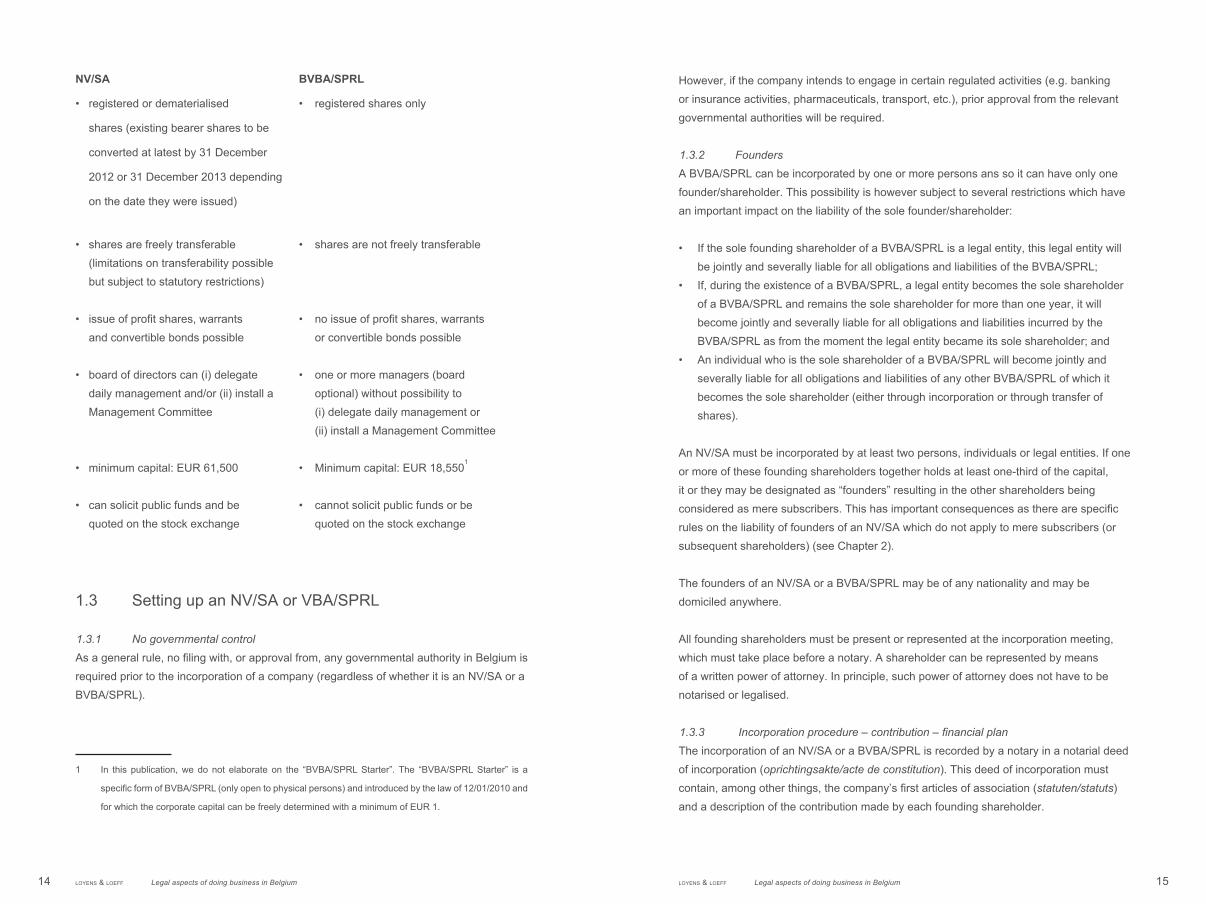

NV/SA BVBA/SPRL

• registered or dematerialised • registered shares only

shares (existing bearer shares to be

converted at latest by 31 December

2012 or 31 December 2013 depending

on the date they were issued)

• shares are freely transferable • shares are not freely transferable (limitations on transferability possible but subject to statutory restrictions)

• issue of profit shares, warrants • no issue of profit shares, warrants and convertible bonds possible or convertible bonds possible

• board of directors can (i) delegate • one or more managers (board daily management and/or (ii) install a optional) without possibility to Management Committee (i) delegate daily management or (ii) install a Management Committee

• minimum capital: EUR 61,500 • Minimum capital: EUR 18,5501

• can solicit public funds and be • cannot solicit public funds or be quoted on the stock exchange quoted on the stock exchange

1.3 Setting up an NV/SA or VBA/SPRL

1.3.1 No governmental controlAs a general rule, no filing with, or approval from, any governmental authority in Belgium is required prior to the incorporation of a company (regardless of whether it is an NV/SA or a BVBA/SPRL).

1 In this publication, we do not elaborate on the “BVBA/SPRL Starter”. The “BVBA/SPRL Starter” is a

specific form of BVBA/SPRL (only open to physical persons) and introduced by the law of 12/01/2010 and

for which the corporate capital can be freely determined with a minimum of EUR 1.

16 17loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

1.3.5 Pre-incorporation transactionsPrior to its incorporation/obtaining legal personality, a Belgian company may enter into contractual commitments. Such commitments are entered into on behalf of the company “in the course of incorporation”.

Unless the contrary is explicitly stated, all persons who act in the name of a company “in the course of incorporation” will be jointly and severally liable for those acts unless the company (i) obtains legal personality within two years following the act and (ii) ratifies the act within two months after obtaining legal personality.

1.3.6 Corporate booksIf registered shares have been issued, the company (be it an NV/SA or a BVBA/SPRL) must keep a shareholders’ register at its registered office. The shareholders’ register must contain such details as the name and address of each shareholder, the number of shares each holds, the amount paid-up on each share, the date of any share transfer, as well as pledges and other encumbrances. The shareholders’ register is of crucial importance as registration in the share register constitutes proof of ownership of the shares towards third parties (including the company itself). Similar obligations apply if registered bonds are issued.

The company must also keep a separate register of minutes for both shareholders’ meetings and board or any other management body meetings. These are separate from the accounting records which must be prepared and kept in accordance with Belgian accounting law.

1.3.7 Filing with the Commercial Court and publicationAs mentioned above, an extract of the deed of incorporation must be filed with the Clerk’s Office of the relevant Commercial Court within 15 days of the incorporation meeting in the presence of a notary. The Company acquires legal personality through this filing.

Approximately 15 days after filing with the Clerk’s Office of the Commercial Court, an extract of the deed of incorporation will be published in the Annexes to the Belgian Official Gazette.

1.3.8 Registration with the Crossroads Database for EnterprisesSimultaneously with the filing of an extract of the deed of incorporation with the Clerk’s Office of the Commercial Court, the company will be registered with the Crossroads Database for Enterprises and will obtain its enterprise number. The company must complete the registration process by filing details of all its business units, directors (for an

Depending on the location of the company’s registered office, the deed of incorporation will have to be in Dutch, French or German.

It should be noted that the legal personality of an NV/SA and a BVBA/SPRL is only conferred by and as of the filing of an extract of the notarial deed of incorporation with the Clerk’s Office of the relevant Commercial Court (being the commercial court of the judicial district of the company’s registered office).

As mentioned above, the deed of incorporation must describe the contribution made by each shareholder. Such contributions can be made in cash or in kind.

In the event of a contribution in cash, the money must be deposited on a blocked bank account, opened with a bank in Belgium for this specific purpose in the name of the company “to be incorporated”. The bank will issue (to the notary) a certificate confirming the amount of cash contributed by the shareholders into the blocked bank account. These funds will only be released (to the company) once the notary provides the bank with a certificate confirming the incorporation of the company.

A contribution in kind must consist of assets (other than cash) having an economic value (e.g. real estate, shares in another company, etc.). Except in some exceptional circumstances explicitly mentioned in the Belgian Companies Code, contributions in kind require an appraisal report by an external auditor, as well as a report issued by the founders.

The founding shareholders of an NV/SA or a BVBA/SPRL must also file a “financial plan” (justifying the amount of the corporate capital) with the notary at the time of incorporation. The notary will keep the financial plan, which, in principle will remain confidential. He can only be required to release it to the Commercial Court if the company becomes bankrupt within three years after incorporation (in order to help the court in its assessment of any founders’ liability – see Chapter 3). In view of the importance of the financial plan for the assessment of the founders’ liability and although the Belgian Companies Code does not impose a specific format for the financial plan, it is usually construed as a budget forecast for at least the first two years of the company’s operations.

1.3.4 Capital taxIn general, no capital tax is due on the amount of capital contributed. If real estate located in Belgium is contributed in kind by an individual and is entirely or partially used or intended for habitation, a capital tax of 10% or 12,5% will be due (depending on whether the real estate is located in the Flemish Region or elsewhere).

18 19loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

1.3.11 Registration with the social security administration

1.3.11.1 Registration requirements for the companyAll companies which are subject to Belgian corporate income tax must register with a social insurance fund for self-employed persons (sociale verzekeringskas voor zelfstandigen/caisse d’assurances sociales pour travailleurs indépendants) within three months after their incorporation and pay annual contributions.

1.3.11.2 Registration requirement for employeesIn addition, if the company has employees in Belgium, it must register with the Belgian social security administration for salaried workers (‘RSZ’/‘ONSS’) and comply with all Belgian social security regulations applicable to employers.

The registration procedure is usually handled by specialised payroll offices (sociale secretariaten/secrétariats sociaux).

1.3.11.3 Registration requirement for directors/managers and the managing director The directors (in case of an NV/SA) and managers (in case of a BVBA/SPRL) must register with a social insurance fund for self-employed persons, as they are not salaried employees but self-employed persons, regardless of whether or not they receive any actual remuneration for the performance of their duties as directors/managers. They must register within three months of their appointment.

This registration requirement also applies to the managing directors of an NV/SA if they are not salaried employees but work as a self-employed person, regardless of whether or not they receive any actual remuneration for the performance of their duties as managing directors.

The amount of the contribution due by these persons depends on the level of their remuneration (with a minimum amount to be paid even if they receive no remuneration). In some exceptional cases, no contribution will be due (e.g. if these persons are foreign citizens who benefit from a treaty between Belgium and their home country).

1.4 Articles of association

1.4.1 GeneralThe articles of association of a company contain the rules for its internal regulation and management.

NV/SA) or managers (for a BVBA/SPRL), and persons with daily management powers (if any) with an ‘Approved Business One-Stop Shop’ (erkende ondernemingsloketten/guichets d’entreprises agréés).

When registering with the Crossroads Database for Enterprises, small- and medium-sized companies (referred to as KMOs/PMEs), are required to provide proof that the person in charge of the day to day operational management of the company.has adequate management skills.These skills can be proven either by submitting diplomas or by providing proof of management experience.

This formality can be avoided if more than 25% of the shares in the capital of the company or the voting rights attaching to them are held by a company-shareholder fulfilling at least one of the following criteria:

(i) the annual average number of workers employed by this shareholder has exceeded 50 over the last two financial years; or

(ii) the annual turnover of this shareholder has exceeded EUR 7 million and the total of the balance sheet has exceeded EUR 5 million over the last two financial years.

In such case, the company will not be considered as a KMO/PME and, therefore, proof of appropriate management skills does not have to be provided. Previously a declaration upon honour of its shareholder confirming that at least one of the above mentioned criteria was met was sufficient to register the company with the Crossroads Database for Enterprises. Now, however, a declaration upon honour must be accompanied by other documents attesting that at least one of the above mentioned criteria is met (survey of number of employees, balance sheet, annual accounts, profit and loss account, copy of shareholders’ register).

1.3.9 Other filing requirementsIf the company intends to engage in certain regulated activities, a copy of the company’s permits or licences must be filed with the Crossroads Database for Enterprises.

1.3.10 Registration with the VAT authoritiesMost companies must be registered with the VAT (Value Added Tax) authorities. Applications can be filed with the VAT authorities directly or through an Approved Business One-Stop Shop.

20 21loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

(i) the issued capital (geplaatst kapitaal/capital souscrit), which reflects the aggregate nominal value of the issued shares; and

(ii) the paid-up capital (gestort kapitaal/capital libéré), which is the amount of the issued capital which has actually been paid up by the shareholders to the company.

For a BVBA/SPRL the minimum issued capital required is EUR 18,550, of which at least EUR 6,200 must be paid up at incorporation (EUR 12,400 if the BVBA/SPRL has only one shareholder).

For an NV/SA, the minimum issued capital required is 61,500 (which must be fully paid up at incorporation).

In addition, at least 20% (for a BVBA/SPRL) or 25% (for an NV/SA) of the nominal value or the par value of each share must be paid up when it is issued. If a share premium is due, it must be paid up in full on issue.

1.5 Shares

Both an NV/SA and a BVBA/SPRL can issue shares and bonds.

An NV/SA can also issue other securities such as warrants, convertible bonds or profit shares (winstbewijzen/part bénéficiaires).

1.5.1 Types of shares

a) Nature of the sharesA BVBA/SPRL may only issue registered shares (entailing, as mentioned above, an entry in the shareholders’ register).

An NV/SA can issue registered shares (entailing an entry in the shareholders’ register), or “dematerialised” shares (i.e. shares held in a depository account).

Until 31 December 2007, an NV/SA could also issue bearer shares. There is now a gradual phasing out system, under Belgian law, to do away with bearer shares. Depending on when they were issued, existing bearer shares must be converted into registered or dematerialised shares by no later than 31 December 2012 or 31 December 2013. An identical transition period exists for other bearer securities.

They must be in the official language (Dutch, French or German) of the region where the company’s registered office is located.

The main issues to be considered when preparing the articles of association are set out below.

1.4.2 Corporate nameThe proposed corporate name or trade name of the company should be sufficiently distinguishable from other existing corporate or trade names, whether or not registered, so as to avoid confusion. The Belgian Companies Code provides that the words “naamloze vennootschap”/”besloten vennootschap met beperkte aansprakelijkheid” (in Dutch), “société anonyme”/”société privée à responsabilité limitée” (in French), or the abbreviations “NV”/”BVBA”, “SA”/”SPRL”, as the case may be, must appear on all documents used by a company incorporated as an NV/SA or BVBA/SPRL. There is, however, no legal obligation to incorporate these words or abbreviations into the company’s corporate name itself. To retain a maximum degree of flexibility, it is recommended to exclude these words or abbreviations from the corporate name. To ensure that the proposed name does not infringe, or conflict with, existing names, a name search should be made in both public and private databases for a nominal fee.

1.4.3 Registered office The registered office is the address where the company is located according to its articles of association and where the corporate records are kept. In principle, all annual shareholders’ meetings and meetings of the board of directors are held at the registered office, although it is possible to hold them elsewhere. A company’s registered office may be different from its “management head-quarters”, in which case, the latter would determine the company’s nationality under Belgian law (see 1.6.2(c)).

1.4.4 Corporate purposeThe corporate purpose clause, in the articles of association, describes the company’s business and activities. As a company may only act within the limits of its corporate purpose, proper attention should be paid to the drafting of the corporate purpose clause in the deed of incorporation. It is of course possible to amend the corporate purpose but this involves formalities (including not only an amendment to the articles of association but also special reports from the statutory auditor and the board of directors/managers as well as a statement of assets and liabilities).

1.4.5 Corporate capitalFor both the NV/SA and the BVBA/SPRL a distinction must be made between two types of share capital:

22 23loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

Under Belgian law, standstill clauses (prohibiting a transfer of shares) are valid provided they are limited in time and are in the company’s corporate interest.

In addition, if share transfers are subject to “right of approval” (whereby the transfer is subject to the approval of e.g. the company’s board of directors), or a pre-emption right of the other shareholders, the restrictions must not prevent the transfer for more than six months as from the date of the request for approval or the invitation to exercise the pre-emption right. If any such clause provides for a total term exceeding six-months, the term is automatically limited to six months.

1.5.2.2 Shares of a BVBA/SPRLShares of a BVBA/SPRL are, as a general rule, not freely transferable: a transfer of shares of a BVBA/SPRL requires the approval of at least 50% of the shareholders, representing at least 75% of the share capital (excluding the shares for which the approval is requested). Such approval is, however, not required for transfers to other shareholders, spouses, parents, children or other persons approved in the articles of association. The articles of association of a BVBA/SPRL (or a shareholders’ agreement) cannot exclude or reduce these mandatory restrictions. They can however provide for more stringent restrictions.

1.6 Mandatory internal bodies

1.6.1 GeneralFor the NV/SA and the BVBA/SPRL, Belgian corporate law prescribes as mandatory at least two internal bodies, namely:(i) a board of directors (for an NV/SA) (raad van bestuur/conseil d’administration), or the

manager(s) (for a BVBA/SPRL) (zaakvoerder(s)/gérant(s)), or alternatively a board of managers (college van zaakvoerders/conseil de gérance); and

(ii) a general meeting of shareholders (algemene vergadering van aandeelhouders/assemblée générale des actionnaires).

The optional body of a Management Committee (directiecomité/comité de direction) is only possible within an NV/SA. Within an NV/SA, it is also possible to delegate the company’s day to day management to specific persons, whether they are directors or not.

b) Classes of sharesAn NV/SA can issue different classes of shares whose rights are determined in the company’s articles of association. This allows for example for:(i) the creation of different classes of shares entitling the holders to specific corporate

rights (e.g. the right to make (binding) recommendations with respect to the appointment of directors); and

(ii) the creation of “preferred shares” entitling the holder thereof to a preferred part of dividends and/or liquidation bonuses.

The creation of different classes of shares and/or of preferred shares is not possible in a BVBA/SPRL.

Both an NV/SA and a BVBA/ SPRL can also issue non-voting shares representing up to one-third of the issued capital. By law, such non-voting shares entitle their holders to a preferred part of dividends, liquidation bonuses and reimbursements of capital. It should be noted that these “non-voting” shares do, in fact, have limited voting rights (which cannot be excluded) in certain specific circumstances enumerated in the Belgian Companies Code.

c) Shares and voting-rightsThe voting rights attached to a share are, as a general rule, proportional to the amount of the capital represented by each share. In practice, each share issued by an NV/SA or a BVBA/SPRL usually represents an equal portion of the capital and carries one vote. Multiple vote shares are prohibited.

Shareholders may, however, be barred from voting with all their shares at a shareholders’ meetings, as the company’s articles of association may restrict the number of votes each shareholder may cast at the shareholders’ meetings. Such voting restrictions are valid provided they apply to all shareholders regardless of the type of shares with which they participate in the vote.

1.5.2 Transfer of shares

1.5.2.1 Shares of an NV/SAShares of an NV/SA are, as a general rule, freely transferable. Share transfers may, however, be restricted by provisions contained, in particular, in the company’s articles of association or in shareholders’ agreements (e.g. stand-still clause, pre-emption right, approval right for the board of directors of the company).

24 25loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

six years. Both managers and directors may be removed at any time, without cause (ad nutum), by a simple majority vote of the shareholders, except – but only as far as the BVBA/SPRL is concerned – if the articles of association provide otherwise. However, a statutory manager (i.e. a manager whose appointment is incorporated in the articles of association) of a BVBA/SPRL can only be removed on “serious grounds” or with the unanimous approval of all shareholders.

The appointment, resignation or removal of a director or manager must be filed with the Clerk’s Office of the Commercial Court and published in the Annexes to the Belgian State Gazette.

c) MeetingsAs mentioned above, in a BVBA/SPRL, each manager (if more than one manager is appointed) has the right to act individually. The articles of association may however stipulate that the managers must act as a board, in which case the articles of association should set out the rules governing the functioning of that board of managers.

In an NV/SA, the directors must act as a board, i.e. as a “collegial body”. The articles of association should set out the rules for the convening and functioning of the board of directors but the Belgian Companies Code does provide for a number of guidelines:

• As a general rule, all board meetings should be held in Belgium. They can be held abroad from time to time but this should not become habitual, as it could result in the company being deemed to be a foreign entity, (under Belgian law, the nationality of a company is determined on the basis of the location of its “management head-quarters”, i.e. the place from where it is effectively managed and where its centre of decision- making is located.

• Board meetings must be “proper” meetings where directors are given the opportunity to discuss the items on the agenda and the proposed resolutions. Consequently, at least two directors (or more if the company’s articles of association so require) must actually attend each board meeting.

The Belgian Companies Code only allows the board of directors of an NV/SA to adopt resolutions by circular letter, signed by all directors in the absence of any actual meeting, in exceptional circumstances, when the resolution needs to be taken urgently and when the corporate interest requires immediate action. This method of decision making, which must be explicitly allowed for in the articles of association, may not, however, be used for the approval of the annual accounts, for a decision to increase the capital within the limits of the “authorised capital” procedure (allowing the board of directors to increase the

1.6.2 Board of directors – (Board of) managers

a) GeneralAll corporate powers not explicitly granted to any other body of the company by law or the articles of association are vested in the board of directors (for an NV/SA) or the (board of) manager(s) (for a BVBA/SPRL).

Belgium has adopted the principle of the one-tier board structure and so makes no institutional distinction between supervision and managerial tasks. However, through the use of a Management Committee (see 1.6.4 below), a structure close to a two-tier system can be achieved.

An NV/SA is managed by a board of directors composed of at least three persons who may, but need not, be shareholders. The minimum number of directors can be reduced to two if, and only as long as, the company has only two shareholders.

A BVBA/SPRL is managed by one or more managers (zaakvoerders/gérants), who may but not need be shareholders, each with the power to act alone. The articles of association, however, can provide that if the company has two or more managers, they must act as a board.

b) AppointmentThe directors and managers are appointed and can be removed by the general meeting of shareholders, except for the first directors and managers who are appointed by the founders. A cooptation system for directors does not exist, except, in an NV/SA, to fill existing positions on a provisional basis.

There is no legal requirement as to the nationality or residence of the directors or managers.

The directors and managers are usually individuals but legal entities can also be appointed as directors or managers. In this case, the legal person entity must designate a “permanent representative” among its partners, managers, directors or employees who must be an individual and who will assume the activities of director or manager in the name and for the account of the legal entity. This permanent representative will have the same (criminal and civil) liabilities, as if he/she holds the office of director/manager in his/her own name and for his/her own account.

Managers of a BVBA/SPRL can be appointed for a definite or an indefinite period of time whereas directors of an NV/SA can only be appointed for a renewable term of maximum

26 27loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

The main special majority requirements are as follows:

(i) 80% for any amendment to the company’s corporate purpose or for the acquisition by the company of its own shares;

(ii) 75% for any other amendment to the company’s articles of association (including a capital increase or decrease), a merger, a demerger or the dissolution of the company; and

(iii) 25% for the dissolution of the company when the net assets have decreased, as a result of losses, to less than 1/4th of the corporate capital.

Except for resolutions that must be taken in the presence of a notary (e.g. capital increases or other amendments to the articles of association, merger,…), the shareholders can decide in writing on all issues for which the general shareholders’ meeting has power of decision, provided such decision is taken unanimously.

1.6.4 Management Committee (optional body within an NV/SA)The articles of association of an NV/SA can give the board of directors power to delegate its management powers to a Management Committee (Directiecomité/ Comité de Direction). Such delegation of authority may not, however, include the determination of the general policy of the company and any powers explicitly reserved by law to the board of directors (such as e.g. the use of the authorised capital). The board of directors must supervise the Management Committee.

The articles of association may also authorise the members of the ManagementCommittee to represent the company, acting individually or jointly.

Any limitation on the powers delegated to the Management Committee (other than those contained in the Belgian Companies Code) and any assignment of tasks to specific persons within the Management Committee will not be binding on third parties, even if made public.

A Management Committee is composed of two or more persons, who may but need not be members of the board of directors. The articles of association or, (in absence of specific provisions in the articles of association,) the board of directors will determine the rules relating to the appointment, removal, remuneration, etc. of Management Committee members.

company’s corporate capital) or for any other decisions explicitly excluded in the articles of association.

d) RepresentationIn an NV/SA, the board of directors is fully entitled to represent the company in dealings with third parties. The articles of association, however, may provide that (for example) one or two directors (and/or members of the Management Committee) may solely or jointly represent the company vis-à-vis third parties.

In a BVBA/SPRL, each manager can represent the company towards third parties, unless the articles of association explicitly provide for a system of joint representation by (for example) two managers if the BVBA/SPRL has multiple managers.

Any further limitations on these representation powers (e.g. in terms of amount) will not be binding on third parties, even if made public.

1.6.3 General meeting of shareholdersThe shareholders’ meeting of both the NV/SA and the BVBA/SPRL has specific powers granted by the Belgian Companies Code (such as the power to amend the company’s articles of association, the approval of the annual accounts or the appointment of the directors/managers and the statutory auditor).

As a general rule, shareholders’ meetings must be held in Belgium. A shareholder who is unable to attend a shareholders’ meeting may appoint another person to represent him at the meeting. Unless the company’s articles of association provide otherwise, a proxy holder need not be a shareholder.

All shareholders must be convened to each shareholders’ meeting. The directors/managers as well as the statutory auditor (and the holders of bonds or certificates issued with the company’s co-operation and, for the NV/SA, the holders of warrants) must also be convened to each shareholders’ meeting.

In the absence of more restrictive provisions in the company’s articles of association, the resolutions of a shareholders’ meeting usually require adoption by a simple majority of the votes cast, regardless of the number of shares present or represented at the meeting.

For certain important resolutions, however, the Belgian Companies Code requires, a quorum as well as special majority vote.

28 29loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

1.8 Dissolution and liquidation

1.8.1 GeneralAlthough there may be different legal causes for the liquidation of a company, this section will only discuss the voluntary dissolution of an NV/SA or a BVBA/SPRL on the basis of a resolution to that effect by the general meeting of shareholders.

The standard liquidation procedure is rather formalistic and time consuming (see section1.8.2 for an overview of the main procedural steps). It should be noted however that recent legislation (the Law of 19 March 2012) permits dissolution and liquidation in one notarial deed (avoiding the formalities and court preceedings required in the standard procedure). This “fast track” is however subject to a number of conditions (such as the absence of any debt).

1.8.2 Standard procedure for liquidation of an NV/SA or BVBA/SPRLThe liquidation of a company consists of two stages: the dissolution of the company and the liquidation of its assets and liabilities.

Dissolution restricts the objects of the company, which only continues to exist to the extent required for the liquidation of its assets and liabilities. As from the moment of dissolution, it cannot conduct any business other than what is required for the liquidation.

The liquidation consists of the settlement of the accounts (including paying the company’s creditors) and the sale of the non-financial assets for the purpose of paying off the creditors and paying the remaining proceeds – if any- to the shareholders and any other parties entitled to share in the liquidation proceeds by virtue of the articles of association. Please note that in general, 10% withholding tax is due on the distribution of liquidation bonuses (i.e. the part of the liquidation proceeds that exceeds the capital).

The liquidation procedure starts with a resolution of an extraordinary shareholders meeting, to be held in the presence of a notary, to dissolve the company, liquidate its assets and appoint liquidators (vereffenaars/liquidateurs). If there are two or more liquidators, they will act as a board.

Before an extraordinary shareholders meeting can decide to dissolve and liquidate the company, the board of directors (for an NV/SA) or the (board of) manager(s) (for a BVBA/SPRL) must submit to the meeting (i) a special board report, (ii) an interim balance sheet - not older than three months - and (iii) a special auditor’s report.

1.6.5 Daily managementThe manager(s) of a BVBA/SPRL are in charge of the day to day management of the company. They are not permitted to delegate this responsibility to other persons or bodies (except for specific, limited proxies).

The board of directors of an NV/SA, though also in charge of the day to day management, may delegate it to directors, referred to as “managing directors” (gedelegeerd bestuurders/administrateurs délégués), or non-directors often referred to as “general managers” (algemeen directeuren/directeurs général).

1.7 Annual accounts

The board of directors or the (board of) manager(s), as the case may be, must prepare annual accounts and must submit them to the annual shareholders’ meeting for approval within six months following the closing of the financial year. The annual accounts must be filed with the National Bank of Belgium within thirty days after their approval and within seven months following the closing of the financial year at the latest. These obligations are subject to criminal, civil and/or administrative sanctions.

The annual accounts must consist of a balance sheet, a profit and loss account and explanatory notes and must be prepared in accordance the Belgian accounting laws and Belgian GAAP. If an NV/SA or BVBA/SPRL qualifies as a “small company” (as defined below) it will be allowed to prepare less extensive annual accounts, in accordance with a more reduced format.

The company must appoint a statutory auditor, being a member of the Institute of Chartered Accountants (Instituut der Bedrijfsrevisoren/Institut des Réviseurs d’Entreprises), to audit the annual accounts and issue an accountant’s statement. Small companies (unless listed on a regulated stock exchange), however, are normally exempted from the obligation to have their annual accounts audited by a statutory auditor.

The board of directors or the (board of) manager(s), as the case may be, must prepare an annual report in which it explains and accounts for its policy. Such annual report must contain specific information about the company and its operations. Small companies (unless listed on a regulated stock exchange) are exempted from this requirement.

A company qualifies as a small company if it has not exceed more than one of the following thresholds during the last two closed financial year(s):(i) the average number of employees: 50;(ii) the net annual turnover (excluding VAT): EUR 7,300,000;(iii) the value of the assets according to the balance sheet: EUR 3,650,000

30 31loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

distribution plan. For the sake of completeness, it should be noted that, in principle, a loss making liquidation is not excluded under general Belgian corporate law.

After the liquidation, the liquidator must file all accounts and other supporting documents, verified by the company’s auditor (if applicable), at the registered office of the company. The liquidator must convene an extraordinary shareholders’ meeting to be held at the earliest one month after the filing of the accounts and the supporting documents. This extraordinary shareholders’ meeting will decide on the distribution of the liquidation proceeds, the discharge of the liquidator, the location where the company’s books and records will be kept for the next five years and the closing of the liquidation. This extraordinary shareholders’ meeting does not have to be held before a notary (unless real estate is to be be distributed in kind as liquidation proceeds to any or all of the shareholders but that is somewhat unusual).

An original copy of the minutes of the extraordinary shareholders’ meeting must be filed with the Clerk’s Office of the Commercial Court, together with an extract for publication in the Annexes to the Belgian Official Gazette.

Creditors or beneficiaries whose claims have not been taken into account in the liquidation may file a claim against the company (through the liquidator) within five years following the publication of the closing of the liquidation.

The liquidator is liable for the proper discharge of his duties and for any performance related shortcomings. Furthermore, non-compliance with certain, specific duties could attract criminal charges.

In the absence of a provision stating otherwise in the articles of association, or failing the specific appointment of another person or persons in the shareholders’ resolution to dissolve the company, the directors or the managers, as the case may be, in office at the time of the adoption of the shareholders’ resolution, will act as liquidators.

The appointment of the liquidator(s) by the extraordinary shareholders’ meeting only becomes effective after verification and approval by the relevant Commercial Court. The company must file a petition with the Commercial Court to that effect. The Commercial Court will, in principle, check the integrity of the proposed liquidator(s) and render its decision, within 24 hours of the filing of the petition. If the Commercial Court decides that the proposed liquidator(s) lack(s) the necessary integrity, it may appoint another liquidator.

The resolution to dissolve and liquidate and a copy of the court’s decision must be filed with the Clerk’s Office of the Commercial Court, together with an extract for publication in the Annexes to the Belgian Official Gazette. The registration with the Crossroads Database for Enterprises must also be updated to reflect the decision to dissolve and liquidate. From the moment of the dissolution, all publications, letters, announcements and other documents emanating from the company must mention that the company is in liquidation.

The liquidation process starts as of the moment of the dissolution of the company. However, as the appointment of the liquidator(s) must be verified and approved by the Commercial Court, it is advisable to wait for its formal approval before proceeding with any liquidation initiative. The liquidator(s) have the same powers, obligations and liabilities as the former directors/managers. The liquidation basically consists of three phases:

(i) drawing up an inventory and selling all assets; (ii) repaying all debts; and(iii) distributing the balance to the shareholders (or other persons entitled to part of the

liquidation proceeds).

Between the sixth and twelfth months of the liquidation, the liquidator must file a detailed statement (indicating the revenues, expenditures and distributions as well as what still remains to be liquidated) with the Clerk’s Office of the Commercial Court. As from the second year, such filing is only required every twelve months. In addition to the detailed statement, the liquidator must prepare and provide the shareholders with annual accounts every year (explaining why the liquidation has not yet been finalised).

Before the liquidation of the company can be finalised, the liquidator must submit to the Commercial Court for approval a plan for the distribution of the assets among the various creditors. The Commercial Court may question the liquidator as it deems fit to verify the

32 33loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

not, therefore, sanction any fault which clearly does not exceed that margin (“marginal control”). Furthermore, the assessment must be based on the information available at the time the director took the decision .

(ii) DamageLosses incurred, including loss of profit, are recoverable. Although damages must be provable, they can also include future damage. The value of the damages is, in principle, limited to the foreseeable damage resulting from the fault that has been committed. In the case of tortious acts or fraud however, all losses (including unforeseeable losses) give rise to liability which must be compensated.

(iii) Causal relationshipThe third condition required for proving liability is the causal link between the director’s fault and the damage. Damages will only be due to the extent that the loss is an immediate and direct consequence of the fault. In other words, this includes all losses which would not have been incurred in the absence of the fault. The court has complete discretion to determine the existence of a causal link between the loss and the fault.

2.2.2.2 Civil faults

(i) Mismanagement

• Concept Directors are agents (“lasthebbers” / “mandataires”) of the company. In that context,

they are liable vis-à-vis the company for the discharge of their responsibilities and for any shortcoming in the performance of their duties (article 527 of the Belgian Companies Code). It is generally accepted that only the company can claim this type of liability.

• Individual liability In principle, the liability imposed by article 527 of the Belgian Companies Code is an

individual liability. A director can only be held liable for his own management errors.

However, there are exceptions to the principle of individual liability. Indeed, there may be instances where (i) different directors together commit a fault (“faute commune - gemeenschappelijke fout” – joint fault) and (ii) each of the different directors makes an error, the accumulation of these separate errors resulting in the same loss (“fautes concurrentes - samenlopende fouten” – concurring faults).

2. Miscellaneous corporate issues: Liability of directors and shareholders

2.1 Introduction

This section contains a short overview of various provisions of Belgian law on the liability of the directors and shareholders of a Belgian NV/SA. The same rules apply, in principle, to the managers and shareholders of a Belgian BVBA/SPRL.

2.2 Directors’ liability

2.2.1 GeneralA distinction must be made between civil and criminal liability. In terms of civil liability, a director can be liable under several heads of faults such as :• tortious acts, in general, (article 1382 of the Belgian Civil Code);• mismanagement (article 527 of the Belgian Companies Code);• contravention of the articles of association or of the Belgian Companies Code (article

528 of the Belgian Companies Code); or• specific breaches.

2.2.2 Civil liability

2.2.2.1 Evidence of liabilityAs a general rule, a finding of liability requires proof of three factors: a fault, resulting damage and a causal link between the two.

(i) FaultProof of fault depends on whether the alleged breach is of a specific obligation or of an obligation requiring only a general duty of due care.

If a rule requires compliance with a specific obligation, the mere breach of that obligation will amount to sufficient evidence of fault.

But there can also be fault if directors fail to comply with the general duty of due care and diligence in the performance of their responsibilities. The litmus test is that of a normal prudent director and raises the question of what a reasonably prudent and diligent director would have done under the specific circumstances of the case? A court will have to make allowance for the director’s margin of discretion in making policy and decisions. It may

34 35loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

association. Again, fault, loss and causal link must be established for a liability claim on this ground to be successful.

A finding of fault must be based on a violation of the Belgian Companies Code or the company’s articles of association. As the Belgian Companies Code (including the Royal Decree of 30 January 2001 implementing the Belgian Companies Code) contains several accounting law provisions, a violation of these provisions will also fall within the scope of article 528 of the Belgian Companies Code.

• Joint and several liability If the fault is proven, a presumption of joint and several liability rests on all directors.

Any individual director can thus be held liable for the payment of the full amount of the damages for which all or some of the directors are liable as a result of a breach of the Belgian Companies Code or the articles of association of the company, without the claimant having to prove which director specifically committed the violation.

A director can rebut this joint and several liability if he/she can prove that he/she: (a) did not participate in committing the violation;(b) was not otherwise negligent; and(c) had no knowledge of the violation, or informed the shareholders of it at the first

shareholders’ meeting following the date on which he/she became aware of it.

• Who can bring a legal action? A liability claim for violation of the Belgian Companies Code or the articles of

association can be initiated by the company as well as by third parties.

Legal proceedings can be initiated by the company, on the basis of a simple majority decision of the general meeting of shareholders. Should the company or one or more minority shareholders wish to bring legal proceedings, the same rules as set out under 2.2.2.2 (i) apply.

Third parties (such as public authorities, creditors or employees) may also initiate a liability claim for violation of the Belgian Companies Code or the articles of association. A discharge granted to the directors by the annual shareholders’ meeting does not bar a claim from such third parties.

Directors will be held jointly and severally liable if the damage is triggered by a joint fault, i.e. different people knowingly contributed to the act causing loss.

In the case of concurring faults causing damage, each director will be held liable in solidum.

Both in the case of liability in solidum and of joint and several liability, each director is accountable for the entire amount of damages. Any director may be sued and the payment by one director releases all other liable directors from claims from the party who incurred the loss.

• Who can bring a legal action? In principle, liability claims against directors for mismanagement (“actio mandati”

on the basis of article 527 of the Belgian Companies Code) can only be initiated by the company itself, on the basis of a simple majority decision of the general meeting of shareholders. In the absence of such a decision, the board of directors cannot initiate claim proceedings, and any such claim will be declared inadmissible. Such inadmissibility would however be remedied if the general meeting of shareholders confirms the board of directors’ action. This confirmation has to take place before the claim is time barred (five years) and before a court decision on the admissibility of the claim.

The actio mandati can, furthermore, only be initiated by the company if the annual general meeting of shareholders does not grant a valid discharge (release of liability) to the directors in question.

An actio mandati may, however, also be initiated by the minority shareholders, acting on behalf of the company, provided their shareholdings (i) are equal to at least 1% of the votes attached to all issued shares of the company or (ii) have a minimum value of EUR 1,250,000. These criteria must be met on the day the general meeting of shareholders deciding on the matter of a discharge to be granted to the directors. In addition, minority shareholders can only initiate the actio mandati if they did not grant a valid discharge to the director(s) concerned.

(ii) Liability for violations of the articles of association or the Belgian Companies Code

• Concept Article 528 of the Belgian Companies Code states that directors may be held jointly

and severally liable towards the company and third parties for all losses resulting from a breach of the provisions of the Belgian Companies Code or the articles of

36 37loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

It should be noted, however, that directors benefit from the theory of quasi- immunity of an agent. If a director performs a contractual obligation on behalf of a company, he/she cannot be held personally liable for tort, unless:(a) he/she has violated the duty of due care; and(b) he/she was responsible for a loss other than the loss caused by the poor

performance of a given contractual obligation of the company.

An example of a violation which results in a crossover in liabilities, is the continuation of a business when it should be obvious to a diligent and reasonable business person that there was no possibility of recovery, as the indebtedness was on the increase. In such a case, the director will have violated article 527 of the Belgian Companies Code vis-à-vis the company and article 1382 of the Belgian Civil Code vis-à-vis the company’s creditors (as such continuation is a criminally offence).

On 20 June 2005, the Belgian Supreme Court nevertheless decided that a company’s liability due to a fault of its director during negotiations prior to the signing of an agreement, did not exclude the director’s liability. The liability of the company and that of the director, coexisted. This decision appears not to be in line with previous landmark decisions of the Belgian Supreme Court regarding the theory of quasi-immunity of an agent and is inconsistently followed by case law and scholars. This creates some legal uncertainty.

2.2.2.3 Specific liabilities

(i) Liability in the event of insolvencyLiability in the event of gross and manifest negligence having contributed to the bankruptcy (article 530 of the Belgian Companies Code).

• Concept In the case of bankruptcy, a director can be held liable (jointly or individually) for

all or part of the company’s debts if that director has been grossly and manifestly negligent, thereby contributing (i.e. not causing) to the bankruptcy. Gross and manifest negligence requires a fault which a normal careful and reasonable director would obviously not have committed.

It should be noted that, if such gross and manifest negligence is proven, a clear causal link does not have to be proven. It suffices to demonstrate that the gross and manifest negligence contributed to the bankruptcy.

(iii) Tortious liability

• Concept The common rules of tortious liability, set out in articles 1382 and 1383 of the Belgian

Civil Code, also apply to directors. Under these articles, if, as a result of a tort being committed, anyone suffers loss, that person is entitled to claim damages. The party claiming the tort must establish that there was fault, resulting loss and a causal link between the two.

A tort is committed if the general duty of due care or a specific, non-contractual obligation is infringed. In the first case, the test is what a diligent director would have done under the same circumstances. When determining the fault, the court has a margin of appreciation and must evaluate the director’s action at the moment of the alleged negligent action or omission.

In case of tortious liability, any loss which is necessarily caused by the tort, is recoverable.

• Individual liability For a director to be held liable on a tortious basis there must be a violation of a duty

which is personally binding on the director. A director is not, therefore, automatically liable for every tortious action committed by the company.

• Who can bring a legal action?

Relationship of director - company A company can only initiate a claim against its directors, based on articles 1382 and

1383 of the Belgian Civil Code, if the fault constitutes both a breach of the agreement between the relevant directors and the company, and a breach of the general duty of due care and diligence applying to everybody. In addition, the loss suffered in tort must differ from the loss resulting from the negligent performance of the management duties of a director. This difference is, in practice, difficult to establish.

Tort liability will, in most instances, be claimed by the company if the instance of mismanagement constitutes a criminally sanctioned violation.

Relationship of director – third parties Third parties, including creditors and shareholders, can hold the directors personally

liable for all losses incurred as a result of the violation of a specific legal provision or of the general duty of due care.

38 39loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

(iii) Liability for failure to pay VAT (article 93, undecies C of the Belgian VAT-Code) Directors are jointly liable for non-payment of VAT (including interest or additional costs) if they are at fault (under article 1382 of the Belgian Civil Code) in the performance of their management duties. Again, this applies, not only to the managing director, but also to other directors, and even de facto directors, if it is proven that they have committed a fault contributing to the failure to pay.

There is a (rebuttable) presumption of fault if at least two or three due debts are not paid within a period of one year (depending on whether the company must submit its VAT declaration quarterly or monthly).

There is no presumption of fault if the non-payment is due to financial difficulties leading to judicial reorganization, bankruptcy or dissolution proceedings.

2.2.3 Criminal liability

2.2.3.1 Both director and company

(i) Director’s liability A director who commits a criminal offence in the performance of his/her function, can be personally held criminally liable. The prosecutor has to prove that the director personally committed the offence.

If there are several directors, it is frequently difficult to establish which of them committed the criminal offence. The court will then determine who was responsible, after a thorough examination of the facts and circumstances of the case. The actual performance of duties will be decisive (and not the legal division of tasks).

In practice, directors are often held to be criminally liable for acts for which they gave instructions, without being the material author of the criminal offence. Likewise, a criminal omission by a director can also be prosecuted to ensure that the legal obligations are complied with.

(ii) Liability of the companyA company can also directly be held criminally liable. For this to happen, the criminal offence committed needs to be attributable to the company, both materially as well as morally.

• Individual/joint liability The court has discretionary power to hold the directors jointly or individually liable as

well as to order them to pay part or all of the company’s outstanding debts.

• Who can bring a legal action? The trustee in bankruptcy, as well as the creditors, can bring an action against the

directors. Individual creditors who initiate a claim can only receive compensation for the loss they suffered. This compensation will be for the sole benefit of the creditor bringing the action, irrespective of any claim initiated by the trustee in bankruptcy, in the interest of the general body of creditors.

• Special liability towards Social Security Authorities Current directors, former directors and “persons who have exercised actual

management powers regarding (“de facto directors”) may be held liable (individually or jointly and severally) by the Institute for Social Security and by the trustee in bankruptcy for all or part of the social security contributions, contribution increases, interest and the “fixed remuneration”, outstanding at the time of the bankruptcy, if their gross negligence was at the origin of the bankruptcy.

Any form of flagrant and organized financial fraud is characterised as gross negligence. Another possible instance of gross negligence would be where the company is managed by a director or representative who has been involved in at least two bankruptcies, liquidations or similar operations, leaving debts owed to one of the institutions which collects Social Security contributions.

(ii) Liability for failure to pay corporate tax prepayments (article 44, 2quater of the Belgian Income Tax Code).

Directors are jointly liable for non-payment of corporate tax prepayments if the failure (under article 1382 of the Belgian Civil Code) to do so is due to their mismanagement. Not only the managing director, but also other directors, and even de facto directors, may be held liable if it is proven that they were at fault and that the fault contributed to the failure to pay.

There is a (rebuttable) presumption of fault if at least two quarterly or three monthly prepayments per year have not been paid (depending on whether the prepayment is to be paid quarterly or monthly).

There is no presumption of fault if the failure to prepay is due to financial difficulties leading to judicial reorganization, bankruptcy or dissolution proceedings.

40 41loyens & loeff Legal aspects of doing business in Belgium loyens & loeff Legal aspects of doing business in Belgium

For the sake of completeness, it should be noted that not all types of companies under Belgian law have such limited liability. In some types of companies, some or all of the shareholders or partners are personally liable for the obligations of the company. Whether or not a specific type of company provides for limited liability, will of course be one of the key elements in deciding which type of company to incorporate.

2.3.2 Exceptions: statutory and judicial limitations to the principle of limited liability Both Belgian legislation and Belgian case law provide for exceptions to the principle of the limited liability of the shareholders of an NV/SA and a BVBA/SPRL through scenarios where their shareholder(s) become(s) personally liable for (specific) debts of the company.

The most important exceptions are briefly discussed below.

2.3.2.1 Statutory exceptions to limited liability

a) Liability of the foundersThe Belgian Companies Code provides for specific liabilities for the founders of an NV/SA and a BVBA/SPRL.

The incorporators can be held jointly and severally liable towards third parties for irregularities or inaccuracies in relation to (i) the incorporation of the company and (ii) the subscription and payment of the corporate capital (articles 229 and 456 of the Belgian Companies Code).

Probably the most important of the founders’ liabilities, however, is their liability with respect to the undercapitalization of the company. If the company is declared bankrupt within three years of its incorporation and if it appears that its initial corporate capital was clearly insufficient to ensure its planned activities for at least two years, the founders of the company will be jointly and severally liable for any loss sustained by third parties in proportions to be determined by the court.

Such insufficiency is a factual question which will be determined by the court on the basis of the specific circumstances. The undercapitalization must be manifest and must be considered at the time of the incorporation and not at the time of the bankruptcy.

Materially, a criminal offence can be attributed to a company if the facts are intrinsically related to the accomplishment of its objects, to the monitoring of its interests, or, where specific circumstances apply, the fault has been committed on its account. In practice, the court will verify whether the activities giving rise to the alleged criminal offence relate to the company’s purpose.

Moral accountability implies that the guilt of the company needs to be proven. The prosecutor will have to prove that a deliberate decision or negligence within the company caused the criminal offence every time that the criminal offence depends on the existence of a special interest condition.

If that can be proved, the company will, in principle, be criminally responsible.

However, if a company is criminally liable exclusively because of the actions of an identified natural person, that person will be convicted if he/she committed the most severe fault.

In principle, there is no accumulation of criminal responsibility of the company and the natural person acting within that company. Accumulation is only possible if the identified natural person was voluntarily and knowingly at fault. In the case of mere negligence, accumulation is not possible.