legislative economic briefing - mississippi · legislative economic briefing ... since january...

TRANSCRIPT

Legislative Economic BriefingFebruary 16, 2017

Mississippi University Research CenterMississippi Institutions of Higher Learning

Darrin Webb, State [email protected]

(601)432-6556

To subscribe to our publications, including Mississippi’s Business email Janna Taylor at [email protected].

Visit our website for this presentation

www.mississippi.edu/urc/downloads/presentations/legislative_economic_briefing.pdf

Overview• US economy has momentum at the start of 2017

– Rebound in energy-sector capital spending

– Strong gains in single-family housing permits

– Orders and shipments of core capital goods are growing again

– January jobs gains were much improved

– Inflation is picking up – signaling improved growth in the economy

– One temporary headwind however is continuation of inventory drawdown in the first half of the year

• Signals are more mixed in Mississippi– Employment slowed considerably in the 4th quarter– Income growth appears to have likewise slowed in the 4th quarter– Transfers to GF have been weak, especially sales & income tax which are

perhaps the revenue sources most closely connected to economic activity– Building permits are improving – Manufacturing workweek length remains high– Initial unemployment claims continue to decline

February 2017 MS University Research Center, IHL 2

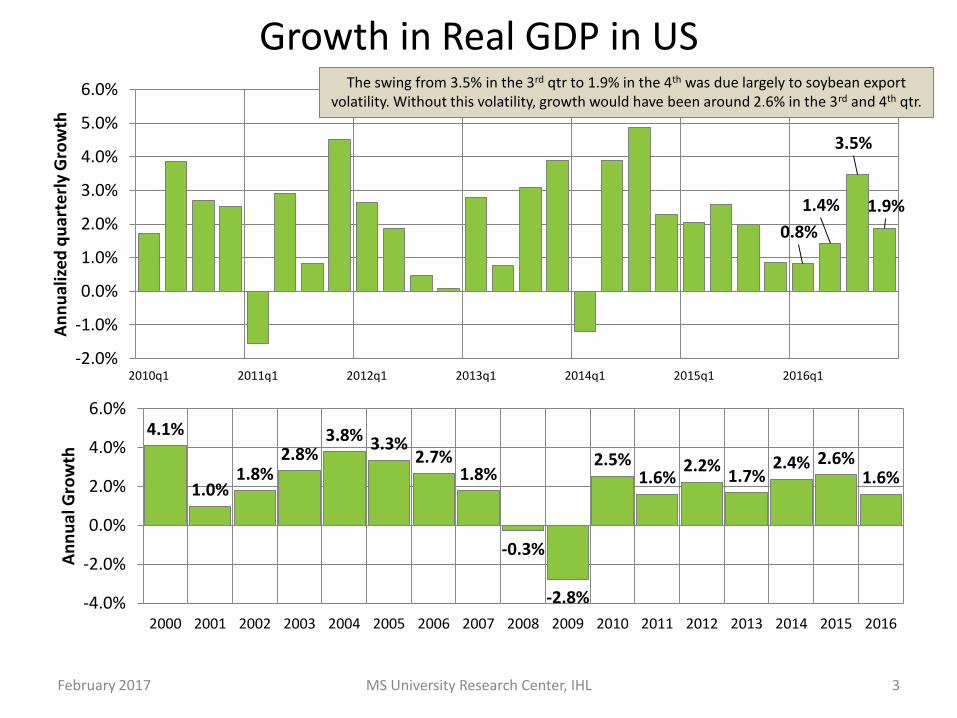

Growth in Real GDP in US

0.8%

1.4%

3.5%

1.9%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2010q1 2011q1 2012q1 2013q1 2014q1 2015q1 2016q1

An

nu

aliz

ed q

uar

terl

y G

row

th

MS University Research Center, IHL 3February 2017

4.1%

1.0%1.8%

2.8%3.8% 3.3%

2.7%1.8%

-0.3%

-2.8%

2.5%1.6%

2.2%1.7%

2.4% 2.6%1.6%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

An

nu

al G

row

thThe swing from 3.5% in the 3rd qtr to 1.9% in the 4th was due largely to soybean export

volatility. Without this volatility, growth would have been around 2.6% in the 3rd and 4th qtr.

US Real GDP Growth is Slowing

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1930 1940 1950 1960 1970 1980 1990 2000 2010

Annual Growth Avg. Growth During Expansion Yrs, By Decade

February 2017 MS University Research Center, IHL 4

Growth during the last expansion (1992-2007) was 3.2%Average growth between 2010-2016 period was 2.1%. We have not experienced a 3.0% growth rate since 2005Reasons: increased interdependence of international economies, high debt levels, aging population/demographic trends.Implications: more frequent recessions.

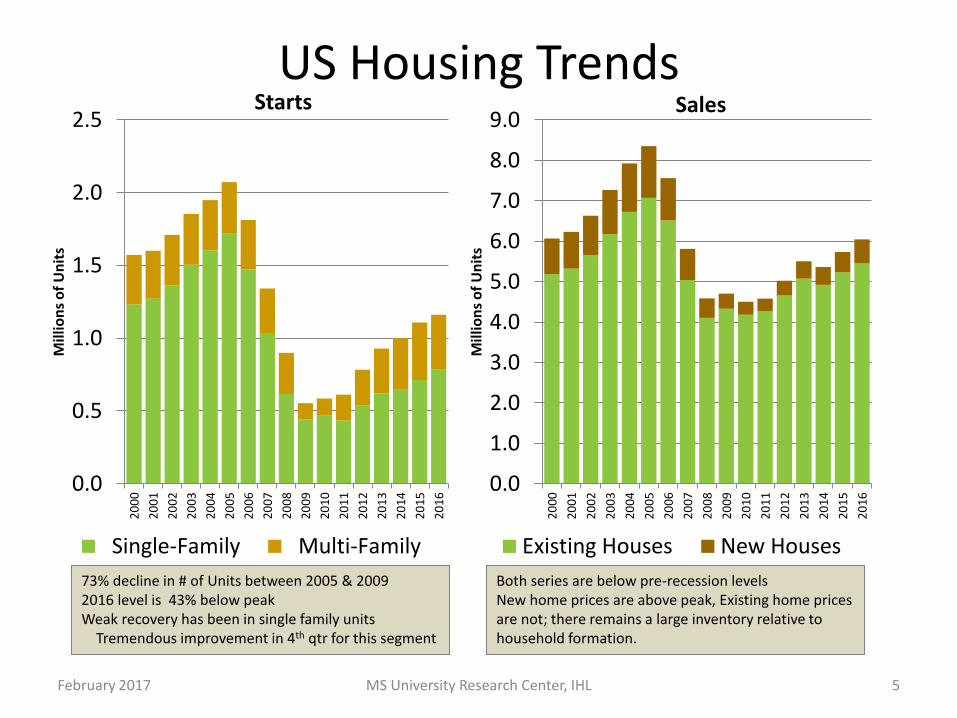

US Housing Trends

0.0

0.5

1.0

1.5

2.0

2.52

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Mill

ion

s o

f U

nit

s

Single-Family Multi-Family

February 2017 MS University Research Center, IHL 5

73% decline in # of Units between 2005 & 20092016 level is 43% below peakWeak recovery has been in single family units

Tremendous improvement in 4th qtr for this segment

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Mill

ion

s o

f U

nit

s

Existing Houses New Houses

Starts Sales

Both series are below pre-recession levels New home prices are above peak, Existing home prices are not; there remains a large inventory relative to household formation.

Housing Trends

• People are renting rather than buying

• Reflects modest income growth

• Household formation is down– During boom years young adults were buying

– Fueled by stronger income growth & easy mortgages

– After bust young adults started living with others• Due in part to high student load debt & decreased job

opportunities

• At some point household formation will again track population growth & boost housing

February 2017 MS University Research Center, IHL 6

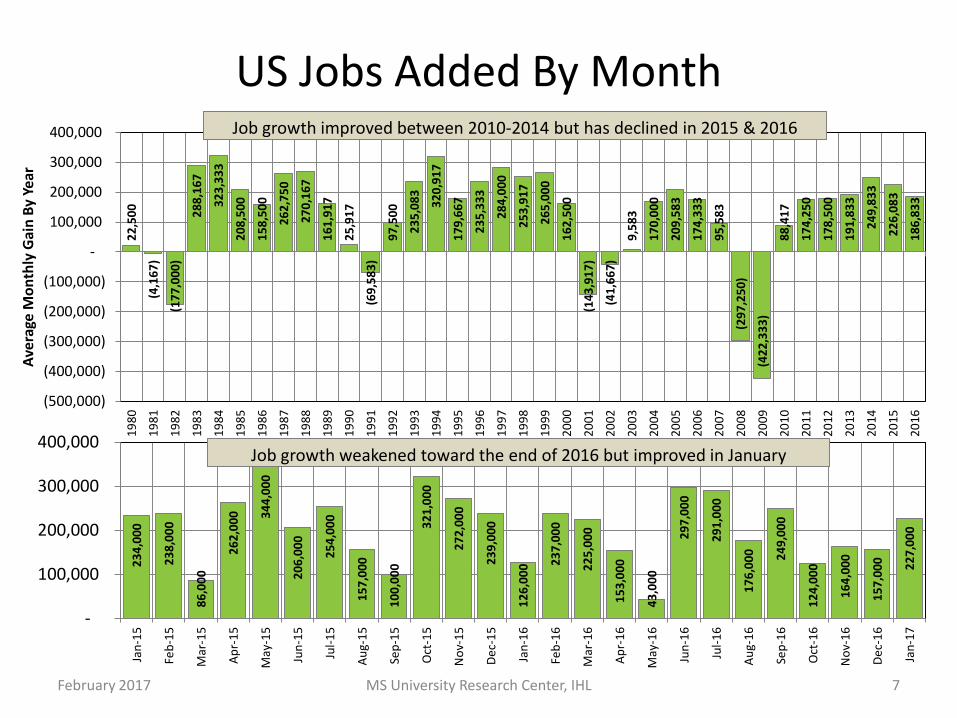

US Jobs Added By Month

MS University Research Center, IHL 7February 2017

22

,50

0

(4,1

67

)

(17

7,0

00

)

28

8,1

67

32

3,3

33

20

8,5

00

15

8,5

00

26

2,7

50

27

0,1

67

16

1,9

17

25

,91

7

(69

,58

3)

97

,50

0

23

5,0

83

32

0,9

17

17

9,6

67

23

5,3

33

28

4,0

00

25

3,9

17

26

5,0

00

16

2,5

00

(14

3,9

17

)

(41

,66

7)

9,5

83

17

0,0

00

20

9,5

83

17

4,3

33

95

,58

3

(29

7,2

50

)

(42

2,3

33

)

88

,41

7

17

4,2

50

17

8,5

00

19

1,8

33

24

9,8

33

22

6,0

83

18

6,8

33

(500,000)

(400,000)

(300,000)

(200,000)

(100,000)

-

100,000

200,000

300,000

400,0001

98

0

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Ave

rage

Mo

nth

ly G

ain

By

Year

Job growth improved between 2010-2014 but has declined in 2015 & 20162

34

,00

0

23

8,0

00

86

,00

0

26

2,0

00

34

4,0

00

20

6,0

00

25

4,0

00

15

7,0

00

10

0,0

00

32

1,0

00

27

2,0

00

23

9,0

00

12

6,0

00

23

7,0

00

22

5,0

00

15

3,0

00

43

,00

0

29

7,0

00

29

1,0

00

17

6,0

00

24

9,0

00

12

4,0

00

16

4,0

00

15

7,0

00

22

7,0

00

-

100,000

200,000

300,000

400,000

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

De

c-1

5

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

Job growth weakened toward the end of 2016 but improved in January

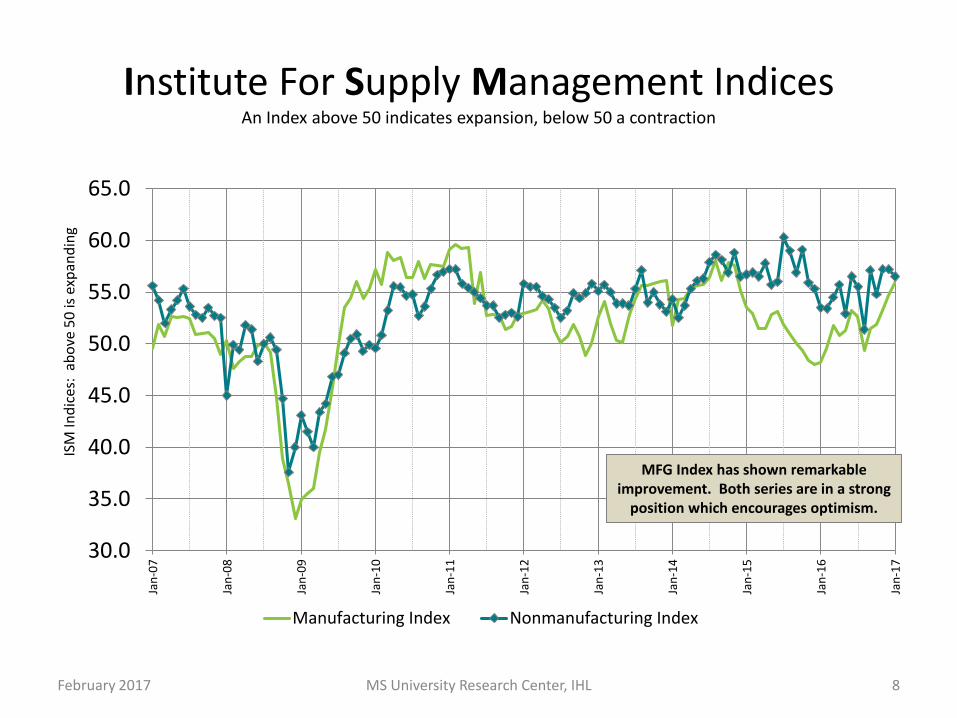

Institute For Supply Management IndicesAn Index above 50 indicates expansion, below 50 a contraction

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

ISM

Ind

ices

: ab

ove

50

is e

xpan

din

g

Manufacturing Index Nonmanufacturing Index

MS University Research Center, IHL 8February 2017

MFG Index has shown remarkable improvement. Both series are in a strong

position which encourages optimism.

Real US Retail SalesAdjusted for Inflation

$280,000

$290,000

$300,000

$310,000

$320,000

$330,000

$340,000

$350,000

$360,000

$370,000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Mo

nth

ly S

ale

s M

illi

on

s o

f 2

00

4 $

2010 3.8%

2016 1.7%

2015 2.2%

MS University Research Center, IHL 9February 2017

2011 4.1%

20122.7%

2014 2.3%

2013 2.4%

Retail sales in 2016 were low compared to the fairly modest growth of the past few years. Christmas sales struggled to meet expectations reaching near or only slightly above last year. This is a bit surprising given the increased optimism. Wage growth, while improving with a tightening labor force, remains relatively subdued

Weekly US Regular Retail Gasoline PricesDollars Per Gallon

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

February 2017 MS University Research Center, IHL 10

After falling dramatically in mid-2014 prices stabilized in late 2016. We have seen a slight uptick in recent weeks, but prices remain low

for relative to the past decade.

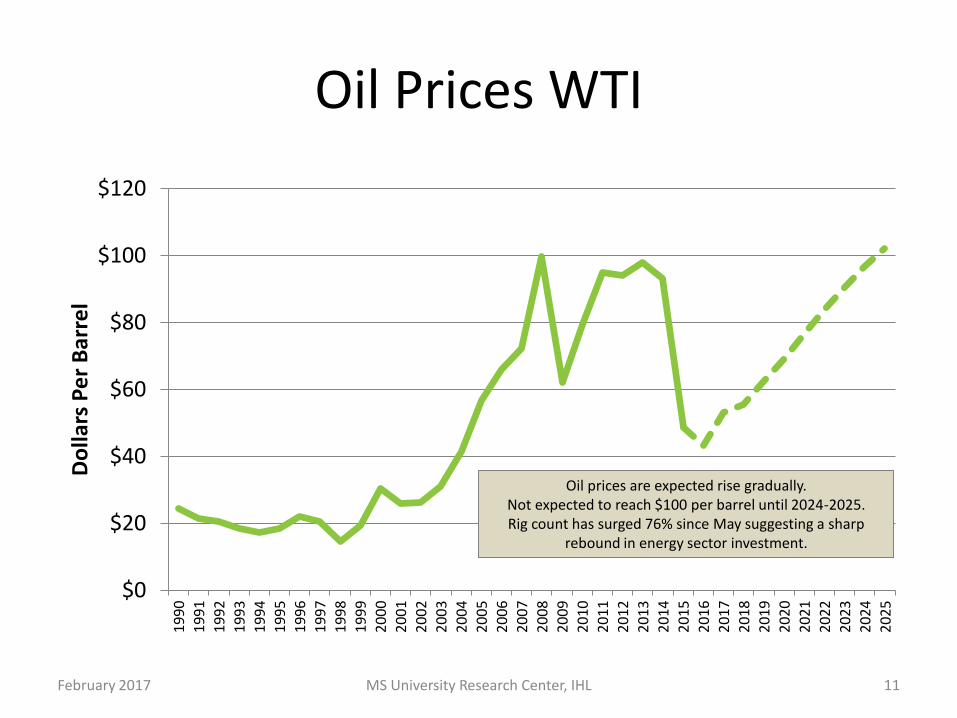

Oil Prices WTI

$0

$20

$40

$60

$80

$100

$1201

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Do

llars

Pe

r B

arre

l

February 2017 MS University Research Center, IHL 11

Oil prices are expected rise gradually. Not expected to reach $100 per barrel until 2024-2025.Rig count has surged 76% since May suggesting a sharp

rebound in energy sector investment.

US Light Vehicle Sales

9.00

11.00

13.00

15.00

17.00

19.00

21.00

23.00Ja

n-0

5

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Mill

ion

s o

f U

nit

s, S

AA

R

Monthly Annual Average

MS University Research Center, IHL 12February 2017

Average sales for 2013 -- 15.5 million unitsAverage sales for 2014 – 16.5 million unitsAverage Sales for 2015 – 17.4 million unitsAverage Sales for 2016 – 17.5 million units

Sales have stabilized at about 17.5 million units.

US Consumer Sentiment

0.0

20.0

40.0

60.0

80.0

100.0

120.0

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Annual Average

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Jan-14 Jan-15 Jan-16 Jan-17

Monthly

February 2017 MS University Research Center, IHL 13

Sentiment returned to the Pre-recession level in 2015.

January 2017 Index is at the highest level since January 2004. The Index was very close to this level in January 2015, but weakened

over the course of the year.

National Federation of Independent Businesses Optimism Index

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

80

85

90

95

100

105

110

NFI

B O

pti

mis

m In

dex

, 19

86

=10

0

MS University Research Center, IHL 14February 2017

Small Businesses confidence has risen sharply in recent months, reaching the highest level since 2004 fueled by the prospects of lower taxes and reduced regulations.

Year-Over-Year Growth in Real Personal Income Less Transfer Payments: United States

by Quarter

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Mar

-60

Mar

-62

Mar

-64

Mar

-66

Mar

-68

Mar

-70

Mar

-72

Mar

-74

Mar

-76

Mar

-78

Mar

-80

Mar

-82

Mar

-84

Mar

-86

Mar

-88

Mar

-90

Mar

-92

Mar

-94

Mar

-96

Mar

-98

Mar

-00

Mar

-02

Mar

-04

Mar

-06

Mar

-08

Mar

-10

Mar

-12

Mar

-14

Mar

-16

February 2017 MS University Research Center, IHL 15

Gray Areas Represent National Recessions

Declines are characteristic of recessions. While the series weakened in 2015 & 2016,

it remains well into positive territory.

US Employment Cost IndexWage and Salaries for All Civilian Workers

Growth Over The Prior Year by Quarter

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Mar

-01

Dec

-01

Sep

-02

Jun

-03

Mar

-04

Dec

-04

Sep

-05

Jun

-06

Mar

-07

Dec

-07

Sep

-08

Jun

-09

Mar

-10

Dec

-10

Sep

-11

Jun

-12

Mar

-13

Dec

-13

Sep

-14

Jun

-15

Mar

-16

Dec

-16

February 2017 MS University Research Center, IHL 16

Despite gains in recent years, wage growth remains well below

pre-recession levels.

Population Index

0

50

100

150

200

250

300

3501

96

0

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

20

14

20

17

20

20

20

23

20

26

20

29

20

32

20

35

20

38

20

41

20

44

19

60

= 1

00

US SE (excl. MS) MS

February 2017 MS University Research Center, IHL 17

Population is indexed to 1960 to allow all three regions to appear on the same graph. Comparisons can then be made by the slope of each line. Both the US and SE are growing at a much faster pace than MS. Current projections show this trend continuing for the foreseeable future.

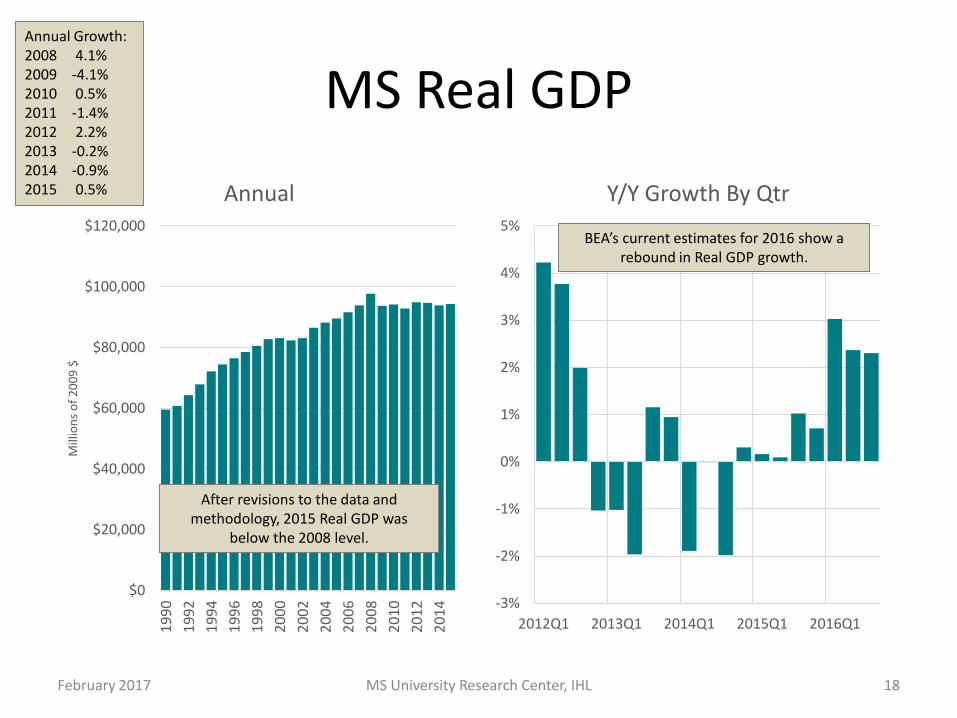

MS Real GDP

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

Mill

ion

s o

f 2

00

9 $

Annual

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2012Q1 2013Q1 2014Q1 2015Q1 2016Q1

Y/Y Growth By Qtr

February 2017 MS University Research Center, IHL 18

After revisions to the data and methodology, 2015 Real GDP was

below the 2008 level.

BEA’s current estimates for 2016 show a rebound in Real GDP growth.

Annual Growth: 2008 4.1%2009 -4.1%2010 0.5%2011 -1.4%2012 2.2%2013 -0.2%2014 -0.9%2015 0.5%

96

98

100

102

104

106

108

110

112

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Ind

ex 2

00

4=

100

MS Index of Coincident Indicators

19MS University Research Center, IHLFebruary 2017

The MSCI stalled in 2016. The index is largely an indicator of the labor market for the state.

The Mississippi Index of Coincident Indicators reflects economic conditions existing in a given month. The index is constructed by the Federal Reserve Bank of Philadelphia and re-indexed to 2004. The Index is based on changes in nonfarm employment, the unemployment rate, average manufacturing workweek length and wage and salary disbursements.

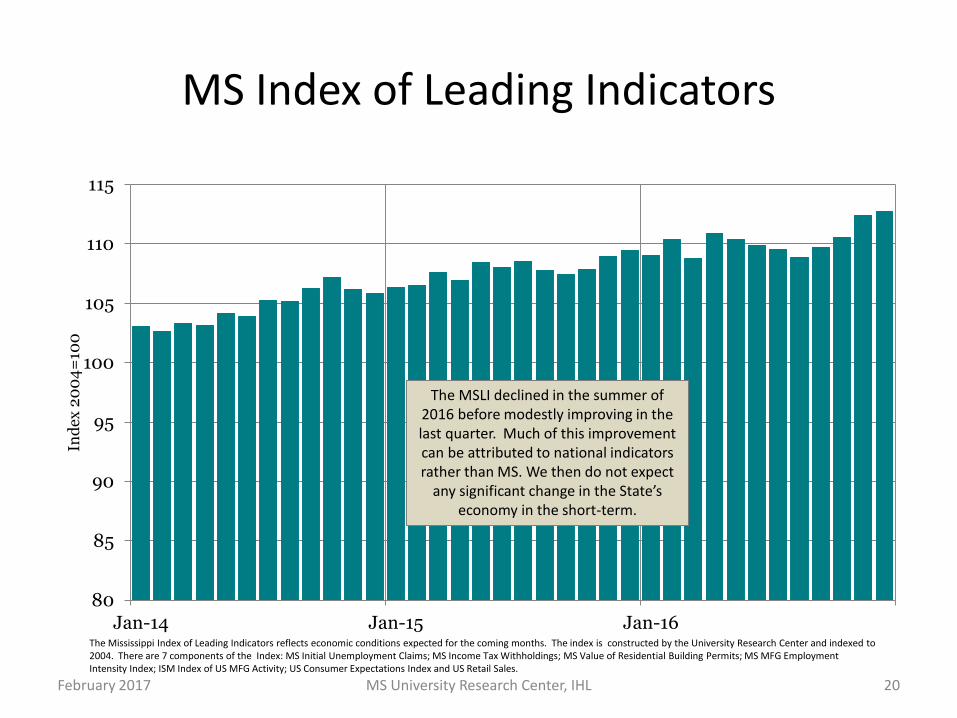

MS Index of Leading Indicators

80

85

90

95

100

105

110

115

Jan-14 Jan-15 Jan-16

Ind

ex 2

00

4=

100

20MS University Research Center, IHL

The MSLI declined in the summer of 2016 before modestly improving in the last quarter. Much of this improvement can be attributed to national indicators rather than MS. We then do not expect

any significant change in the State’s economy in the short-term.

February 2017

The Mississippi Index of Leading Indicators reflects economic conditions expected for the coming months. The index is constructed by the University Research Center and indexed to 2004. There are 7 components of the Index: MS Initial Unemployment Claims; MS Income Tax Withholdings; MS Value of Residential Building Permits; MS MFG Employment Intensity Index; ISM Index of US MFG Activity; US Consumer Expectations Index and US Retail Sales.

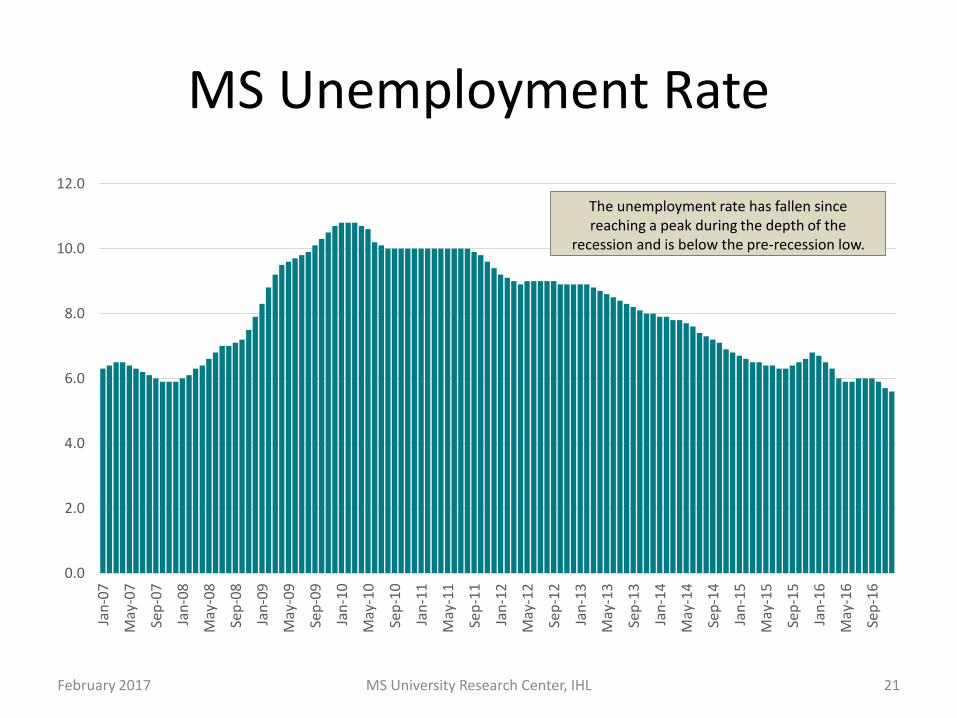

MS Unemployment Rate

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

February 2017 MS University Research Center, IHL 21

The unemployment rate has fallen since reaching a peak during the depth of the

recession and is below the pre-recession low.

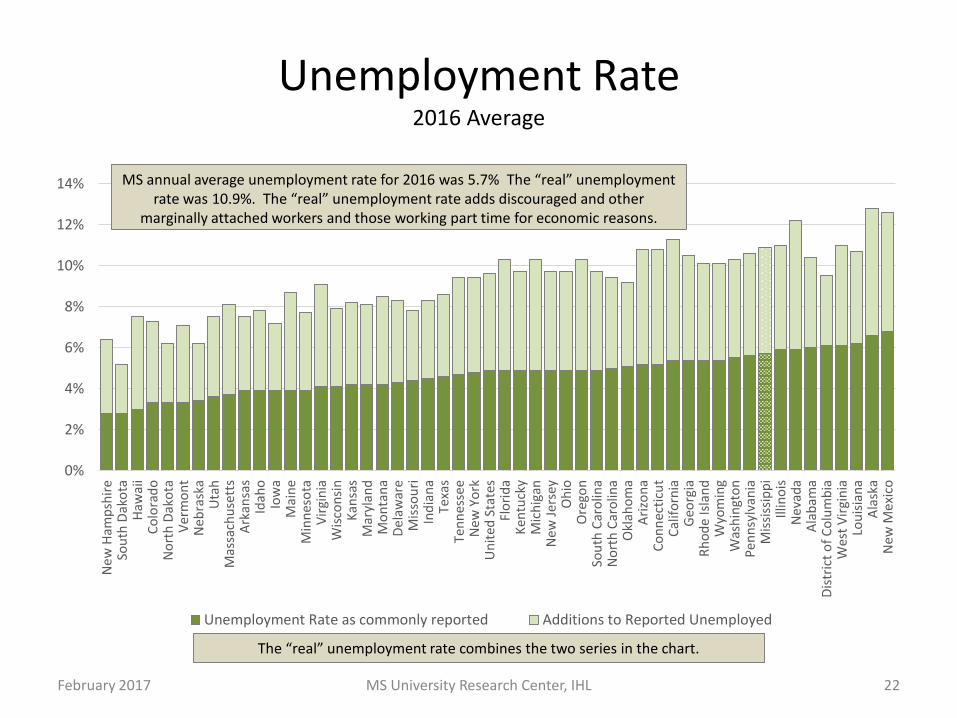

Unemployment Rate2016 Average

0%

2%

4%

6%

8%

10%

12%

14%

New

Ham

psh

ire

Sou

th D

ako

taH

awai

iC

olo

rad

oN

ort

h D

ako

taV

erm

on

tN

ebra

ska

Uta

hM

assa

chu

sett

sA

rkan

sas

Idah

oIo

wa

Mai

ne

Min

nes

ota

Vir

gin

iaW

isco

nsi

nK

ansa

sM

aryl

and

Mo

nta

na

Del

awar

eM

isso

uri

Ind

ian

aTe

xas

Ten

nes

see

New

Yo

rkU

nit

ed S

tate

sFl

ori

da

Ken

tuck

yM

ich

igan

New

Jer

sey

Oh

ioO

rego

nSo

uth

Car

olin

aN

ort

h C

aro

lina

Okl

aho

ma

Ari

zon

aC

on

nec

ticu

tC

alif

orn

iaG

eorg

iaR

ho

de

Isla

nd

Wyo

min

gW

ash

ingt

on

Pen

nsy

lvan

iaM

issi

ssip

pi

Illin

ois

Nev

ada

Ala

bam

aD

istr

ict

of

Co

lum

bia

Wes

t V

irgi

nia

Lou

isia

na

Ala

ska

New

Mex

ico

Unemployment Rate as commonly reported Additions to Reported Unemployed

February 2017 MS University Research Center, IHL 22

MS annual average unemployment rate for 2016 was 5.7% The “real” unemployment rate was 10.9%. The “real” unemployment rate adds discouraged and other

marginally attached workers and those working part time for economic reasons.

The “real” unemployment rate combines the two series in the chart.

MS Initial Unemployment Claims

-

50,000

100,000

150,000

200,000

250,000

300,000

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Annual Average

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan-14 Jan-15 Jan-16

3-Month Moving AverageSeasonally Adjusted

February 2017 MS University Research Center, IHL 23

Claims have trended down and are at historically low levels.

Claims fell in the last quarter. Declining claims mean fewer lay-offs.

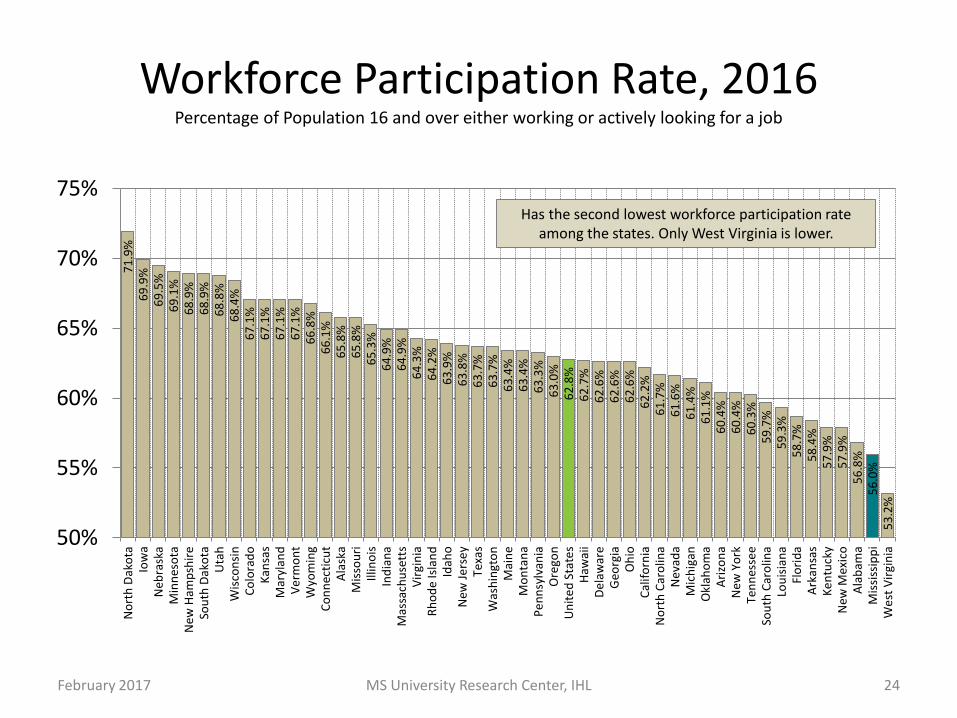

Workforce Participation Rate, 2016Percentage of Population 16 and over either working or actively looking for a job

71

.9%

69

.9%

69

.5%

69

.1%

68

.9%

68

.9%

68

.8%

68

.4%

67

.1%

67

.1%

67

.1%

67

.1%

66

.8%

66

.1%

65

.8%

65

.8%

65

.3%

64

.9%

64

.9%

64

.3%

64

.2%

63

.9%

63

.8%

63

.7%

63

.7%

63

.4%

63

.4%

63

.3%

63

.0%

62

.8%

62

.7%

62

.6%

62

.6%

62

.6%

62

.2%

61

.7%

61

.6%

61

.4%

61

.1%

60

.4%

60

.4%

60

.3%

59

.7%

59

.3%

58

.7%

58

.4%

57

.9%

57

.9%

56

.8%

56

.0%

53

.2%

50%

55%

60%

65%

70%

75%

No

rth

Dak

ota

Iow

aN

ebra

ska

Min

nes

ota

New

Ham

psh

ire

Sou

th D

ako

taU

tah

Wis

con

sin

Co

lora

do

Kan

sas

Mar

ylan

dV

erm

on

tW

yom

ing

Co

nn

ecti

cut

Ala

ska

Mis

sou

riIll

ino

isIn

dia

na

Mas

sach

use

tts

Vir

gin

iaR

ho

de

Isla

nd

Idah

oN

ew J

ers

ey

Texa

sW

ash

ingt

on

Mai

ne

Mo

nta

na

Pe

nn

sylv

ania

Ore

gon

Un

ite

d S

tate

sH

awai

iD

ela

war

eG

eorg

iaO

hio

Cal

ifo

rnia

No

rth

Car

olin

aN

evad

aM

ich

igan

Okl

aho

ma

Ari

zon

aN

ew Y

ork

Ten

nes

see

Sou

th C

aro

lina

Lou

isia

na

Flo

rid

aA

rkan

sas

Ke

ntu

cky

New

Mex

ico

Ala

bam

aM

issi

ssip

pi

We

st V

irgi

nia

February 2017 MS University Research Center, IHL 24

Has the second lowest workforce participation rate among the states. Only West Virginia is lower.

Workforce Participation Trends

• Participation has fallen in recent years for both the US and MS

• The gap between MS & US participation rate is highest among 16-19 year-olds & 45-65 year-olds

• MS lower participation rate due in a large part to higher incidence of disability– Census shows 10% of working age population in MS is disabled & not

in the work force; in the US the rate is 6%. The state’s higher rate translates into over 70 thousand people.

• MS participation rate exceeds that of the US for 35-44 year-old women; only category where this is the case

• See appendix for charts reflecting the above as well as other trends

February 2017 MS University Research Center, IHL 25

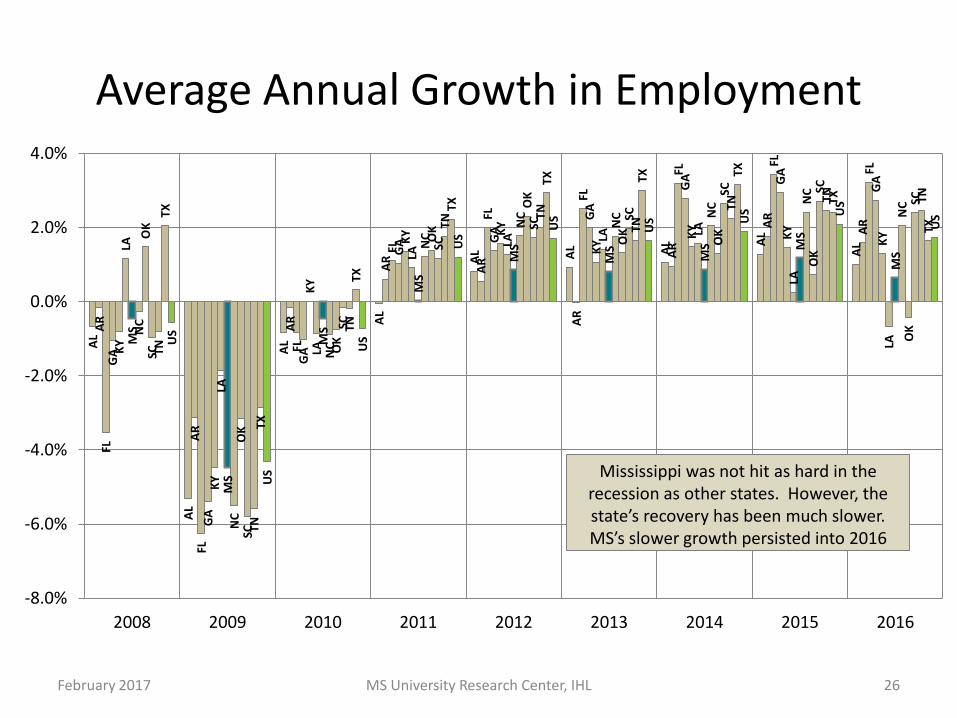

Average Annual Growth in EmploymentA

L

AL

AL

AL

AL AL AL A

L

AL

AR

AR

AR

AR

AR

AR

AR

AR

AR

FL

FL

FL

FL

FL

FL

FL

FL

FL

GA

GA

GA

GA G

A

GA

GA GA

GA

KY

KY

KY

KY K

Y

KY

KY

KY

KY

LA

LA

LA

LA

LA LA LA

LA

LAMS

MS

MS

MS

MS

MS

MS M

S

MS

NC

NC

NC

NC

NC

NC N

C NC

NC

OK

OK

OK

OK

OK

OK

OK

OK

OK

SC

SC

SC

SC

SC

SC

SC SC

SC

TN

TN

TN

TN

TN

TN

TN

TN TN

TX

TX

TX

TX

TX TX TX

TX

TX

US

US

US

US

US

US U

S US

US

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016

February 2017 MS University Research Center, IHL 26

Mississippi was not hit as hard in the recession as other states. However, the state’s recovery has been much slower. MS’s slower growth persisted into 2016

Employment Relative to Pre-RecessionDecember 2016 as a Percentage Above (Below) December 2007

4.9%

-2.3%

-5%

0%

5%

10%

15%

20%

25%

No

rth

Dak

ota

Texa

sU

tah

Co

lora

do

Was

hin

gto

nM

assa

chu

sett

sC

alif

orn

iaSo

uth

Dak

ota

Ore

gon

New

Yo

rkTe

nn

esse

eFl

ori

da

Idah

oSo

uth

Car

olin

aG

eorg

iaN

ebra

ska

Ala

ska

Un

ite

d S

tate

sN

ort

h C

aro

lina

Min

nes

ota

Vir

gin

iaH

awai

iD

ela

war

eM

on

tan

aM

aryl

and

Ke

ntu

cky

Okl

aho

ma

Iow

aN

ew H

amp

shir

eIn

dia

na

Ve

rmo

nt

Mic

hig

anLo

uis

ian

aA

rkan

sas

Wis

con

sin

Pe

nn

sylv

ania

Mis

sou

riA

rizo

na

Oh

ioN

evad

aR

ho

de

Isla

nd

Illin

ois

Kan

sas

New

Je

rse

yW

est

Vir

gin

iaC

on

nec

ticu

tA

lab

ama

Mis

siss

ipp

iN

ew M

exic

oM

ain

e

February 2017 MS University Research Center, IHL 27

MS is one of 8 states where the December 2016 employment was below that of December 2007. States rank from a high of 20.5% above to a low

of 5.6 below. MS is 2.3% below.

Annual AverageNonfarm Employment, 1950-2016

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

0

200

400

600

800

1,000

1,200

1,400

19

50

19

52

19

54

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

MS US

February 2017 MS University Research Center, IHL 28

MS grew at a relatively steady pace prior to 2000. Since 2000 the state has struggled to gain momentum or keep pace with the Nation. The Nation has especially outpaced the state since the

2008 recession.

Nonfarm Employment in MS

1,100

1,105

1,110

1,115

1,120

1,125

1,130

1,135

1,140

1,145

1,150

Jan-14 Jan-15 Jan-16

Thousands

29MS University Research Center, IHL

After fairly consistent gain in employment over the previous two

years, employment weakened substantially in late 2016. Average

annual growth for 2016 was 0.6%, half of the 1.2% growth observed in 2015.

Growth for 2014 was 0.9%

February 2017

MS Employment for Major Sectors

50

100

150

200

250

300

Tho

usa

nd

s

Manufacturing Retail Trade Health Care and Social Assistance Leisure and Hospitality Government

February 2017 MS University Research Center, IHL 30

MS’s slow growth over the past two decades has coincided with a movement away from manufacturing. That shift began in the 90s but was less apparent due to

growth in the casino industry. More people work in Government than any other major sector which has shown no upward momentum since the Great Recession

Where are the Jobs?Mississippi added an average 7,358 jobs in 2016 over 2015

-3,600

-1,092

-733

-375

-225

350

1,100

1,842

2,225

3,642

4,225

-4,000 -3,000 -2,000 -1,000 0 1,000 2,000 3,000 4,000 5,000

Professional Services

Financial Activities

Mining & logging

Other Services

Information

Construction

Manufacturing

Government

Education & Health Services

Leisure & Hospitality

Trade, Transportation & Utilities

February 2017 MS University Research Center, IHL 31

February 2017 MS University Research Center, IHL 32

Employment Gained (Lost) By County, 2015-2016

No change

Decline

Up to 250

251 to 500

Greater than 500

MS Residential Building PermitsNumber of Units

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Annual

0

100

200

300

400

500

600

700

Jan-14 Jan-15 Jan-16

3-Month Moving AverageSeasonally adjusted

February 2017 MS University Research Center, IHL 33

The momentum of 2015 did not continue into 2016. Permits fell through much of the year

before improving in the last quarter.

Graph may understate building activity as permits are not required in the county.

Between 2007 and 2011 there was a 73% decline in activity. Despite 5 years

of gain, we remain 56% below Peak

MS Construction Employment

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Annual Average

40.0

42.0

44.0

46.0

48.0

50.0

52.0

54.0

Jan-14 Jan-15 Jan-16

MonthlySeasonally Adjusted

February 2017 MS University Research Center, IHL 34

Employment improved in much of 2016 but fell sharply in the last quarter.

After strong growth in the 90s, employment has generally trended downward. The notable exceptions are the period following Katrina &

during large projects of 2013-2014.

MS Manufacturing Employment

0.0

50.0

100.0

150.0

200.0

250.0

300.0

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Annual Average

135.0

136.0

137.0

138.0

139.0

140.0

141.0

142.0

143.0

144.0

145.0

Jan-14 Jan-15 Jan-16

MonthlySeasonally Adjusted

February 2017 MS University Research Center, IHL 35

Much of the growth that took place in 2015 disappeared in 2016. The state

ended the year with a substantial decline in December.

MFG employment generally declined between 1994 and 2010. Since 2010

the state has experienced modest gains. In 2016, manufacturing

employment rose 0.8% or 1,100 jobs

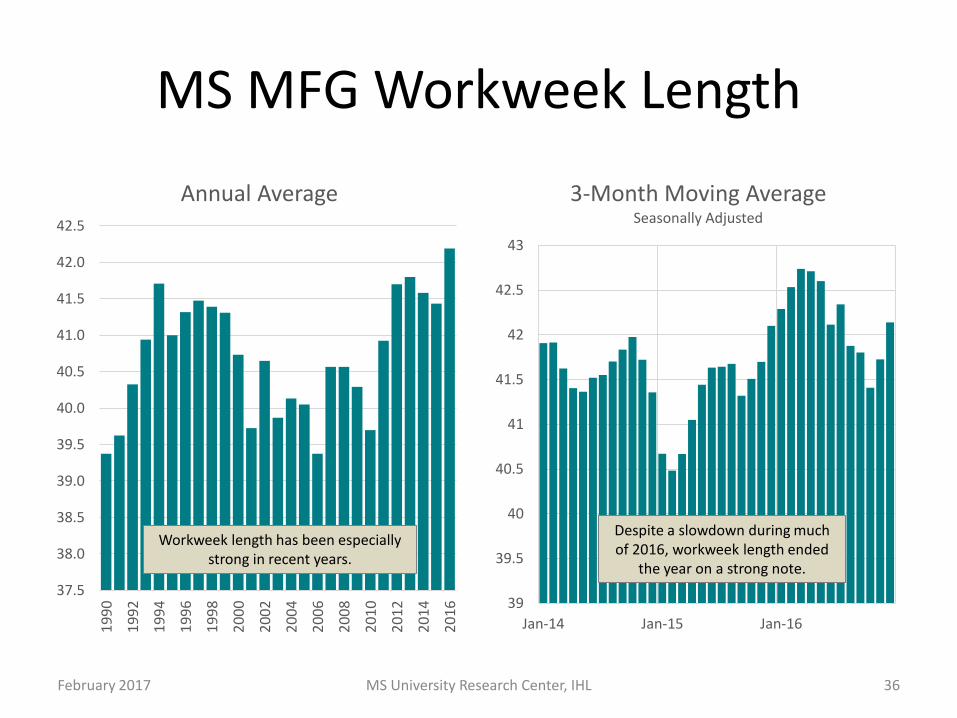

MS MFG Workweek Length

37.5

38.0

38.5

39.0

39.5

40.0

40.5

41.0

41.5

42.0

42.5

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Annual Average

39

39.5

40

40.5

41

41.5

42

42.5

43

Jan-14 Jan-15 Jan-16

3-Month Moving AverageSeasonally Adjusted

February 2017 MS University Research Center, IHL 36

Despite a slowdown during much of 2016, workweek length ended

the year on a strong note.

Workweek length has been especially strong in recent years.

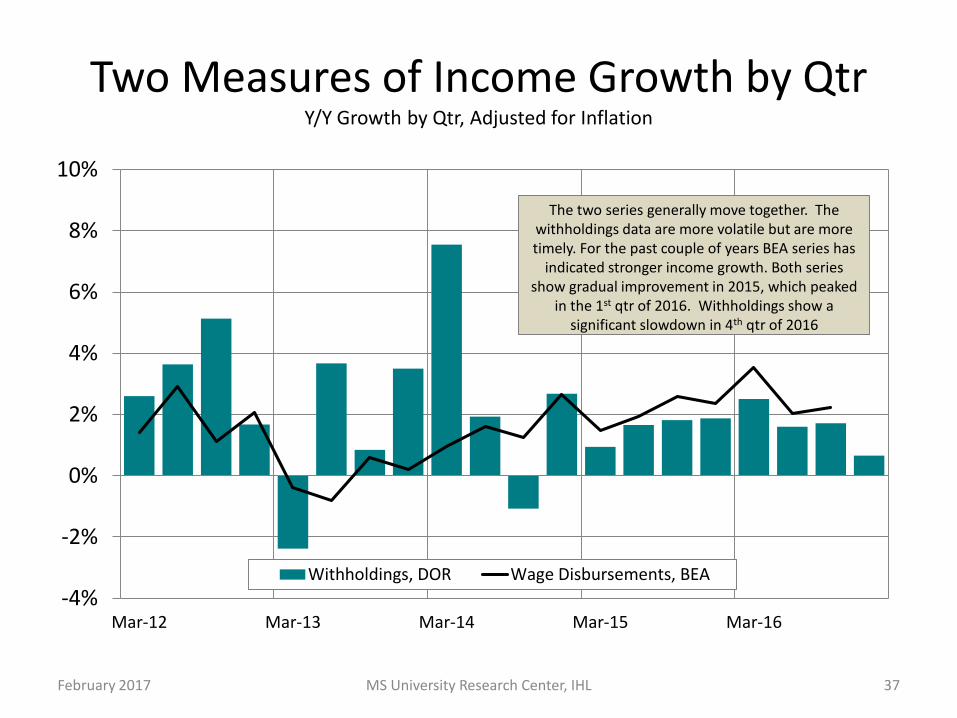

Two Measures of Income Growth by QtrY/Y Growth by Qtr, Adjusted for Inflation

-4%

-2%

0%

2%

4%

6%

8%

10%

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Withholdings, DOR Wage Disbursements, BEA

February 2017 MS University Research Center, IHL 37

The two series generally move together. The withholdings data are more volatile but are more timely. For the past couple of years BEA series has

indicated stronger income growth. Both series show gradual improvement in 2015, which peaked

in the 1st qtr of 2016. Withholdings show a significant slowdown in 4th qtr of 2016

MS Gaming Revenue

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,5001

99

5

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Lin

e G

rap

h: A

nn

ual

% C

HG

Bar

Gra

ph

: Mill

ion

s o

f D

olla

rs

Coast River Total % CHG Total

February 2017 MS University Research Center, IHL 38

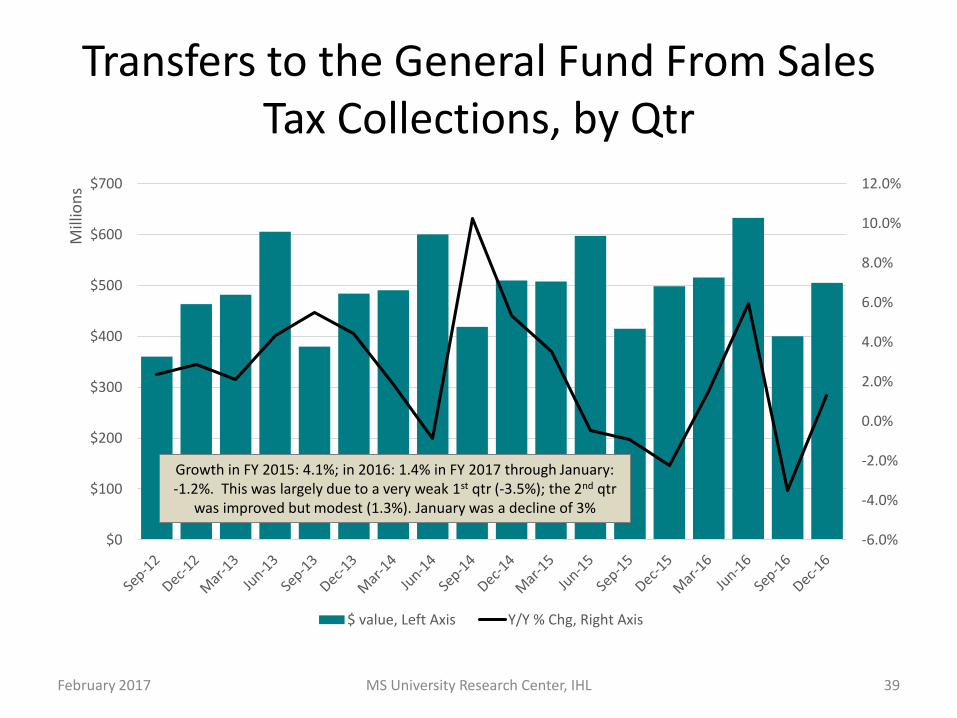

Transfers to the General Fund From Sales Tax Collections, by Qtr

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

$0

$100

$200

$300

$400

$500

$600

$700

Mill

ion

s

$ value, Left Axis Y/Y % Chg, Right Axis

February 2017 MS University Research Center, IHL 39

Growth in FY 2015: 4.1%; in 2016: 1.4% in FY 2017 through January: -1.2%. This was largely due to a very weak 1st qtr (-3.5%); the 2nd qtr

was improved but modest (1.3%). January was a decline of 3%

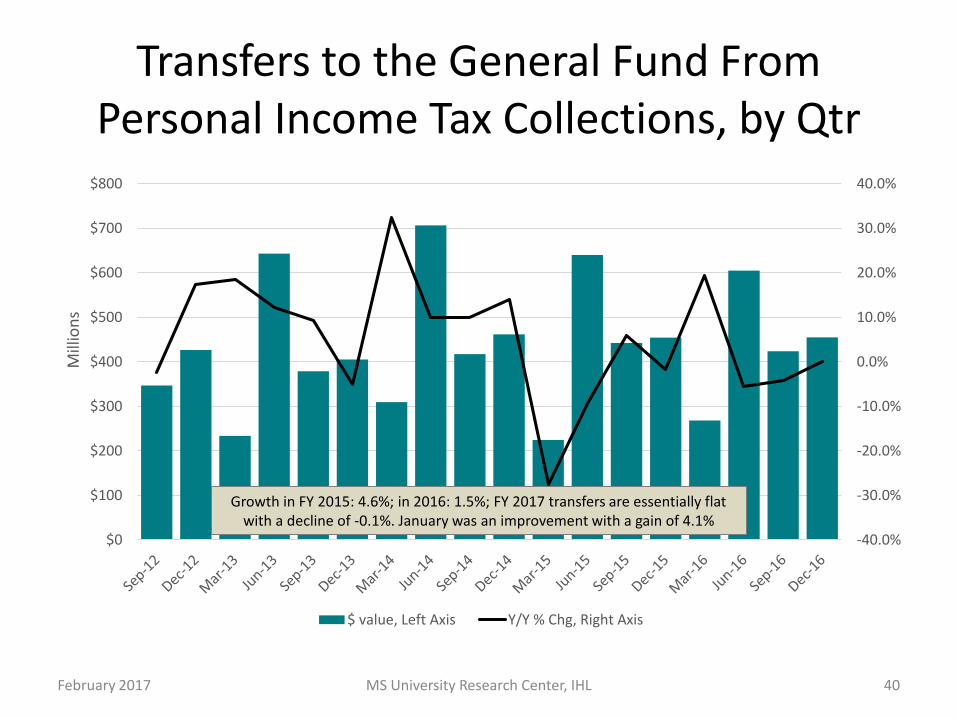

Transfers to the General Fund From Personal Income Tax Collections, by Qtr

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

$0

$100

$200

$300

$400

$500

$600

$700

$800

Mill

ion

s

$ value, Left Axis Y/Y % Chg, Right Axis

February 2017 MS University Research Center, IHL 40

Growth in FY 2015: 4.6%; in 2016: 1.5%; FY 2017 transfers are essentially flat with a decline of -0.1%. January was an improvement with a gain of 4.1%

Transfers to the General Fund

-10%

-5%

0%

5%

10%

15%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Mill

ion

s

Additional Transfers from settlements, WCSR Fund, budget reduction, etc., Left Axis

Transfers from DOR and "Other than DOR" Left Axis

Y/Y % Chg in Tota GF, Right Axis

February 2017 MS University Research Center, IHL 41

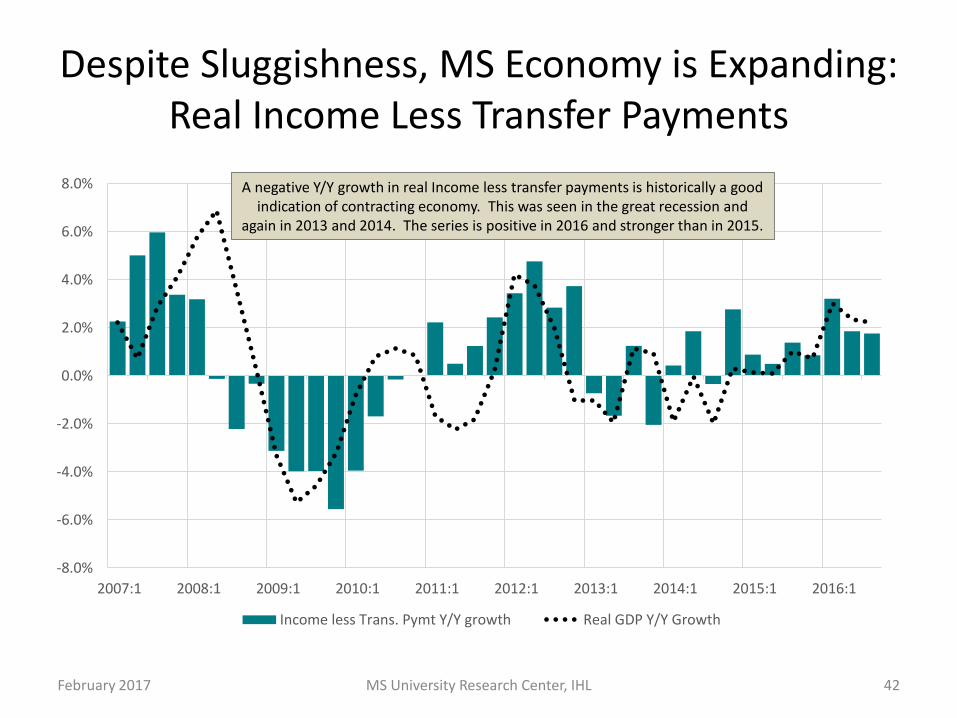

Despite Sluggishness, MS Economy is Expanding: Real Income Less Transfer Payments

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

2007:1 2008:1 2009:1 2010:1 2011:1 2012:1 2013:1 2014:1 2015:1 2016:1

Income less Trans. Pymt Y/Y growth Real GDP Y/Y Growth

February 2017 MS University Research Center, IHL 42

A negative Y/Y growth in real Income less transfer payments is historically a good indication of contracting economy. This was seen in the great recession and

again in 2013 and 2014. The series is positive in 2016 and stronger than in 2015.

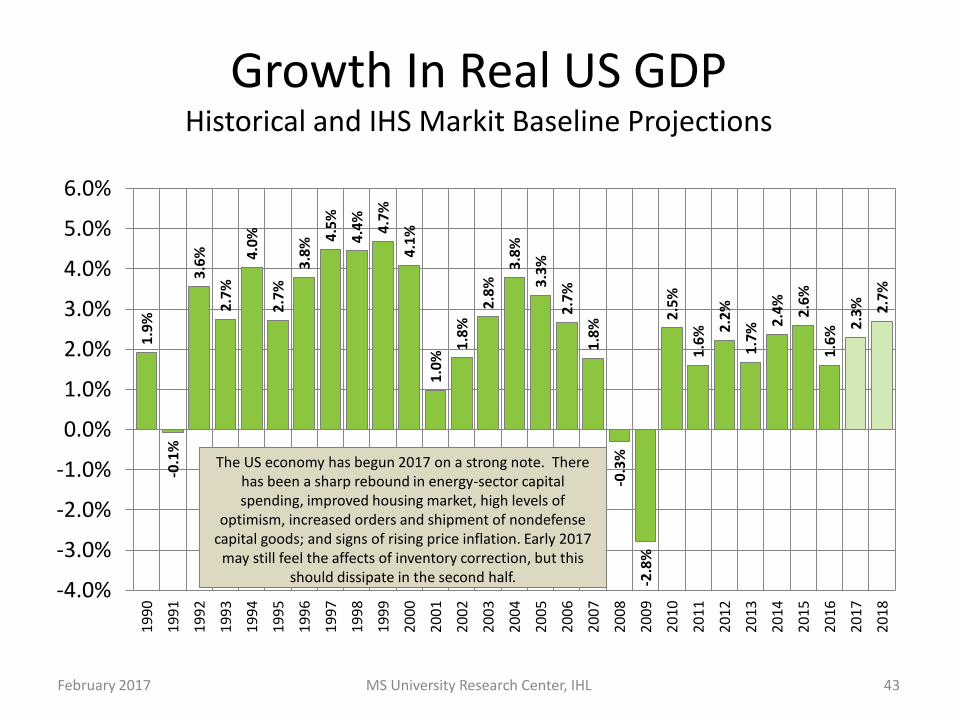

Growth In Real US GDPHistorical and IHS Markit Baseline Projections

1.9

%

-0.1

%

3.6

%

2.7

%

4.0

%

2.7

%

3.8

% 4.5

%

4.4

%

4.7

%

4.1

%

1.0

%

1.8

%

2.8

%

3.8

%

3.3

%

2.7

%

1.8

%

-0.3

%

-2.8

%

2.5

%

1.6

% 2.2

%

1.7

% 2.4

%

2.6

%

1.6

% 2.3

% 2.7

%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

MS University Research Center, IHL 43February 2017

The US economy has begun 2017 on a strong note. There has been a sharp rebound in energy-sector capital spending, improved housing market, high levels of

optimism, increased orders and shipment of nondefense capital goods; and signs of rising price inflation. Early 2017

may still feel the affects of inventory correction, but this should dissipate in the second half.

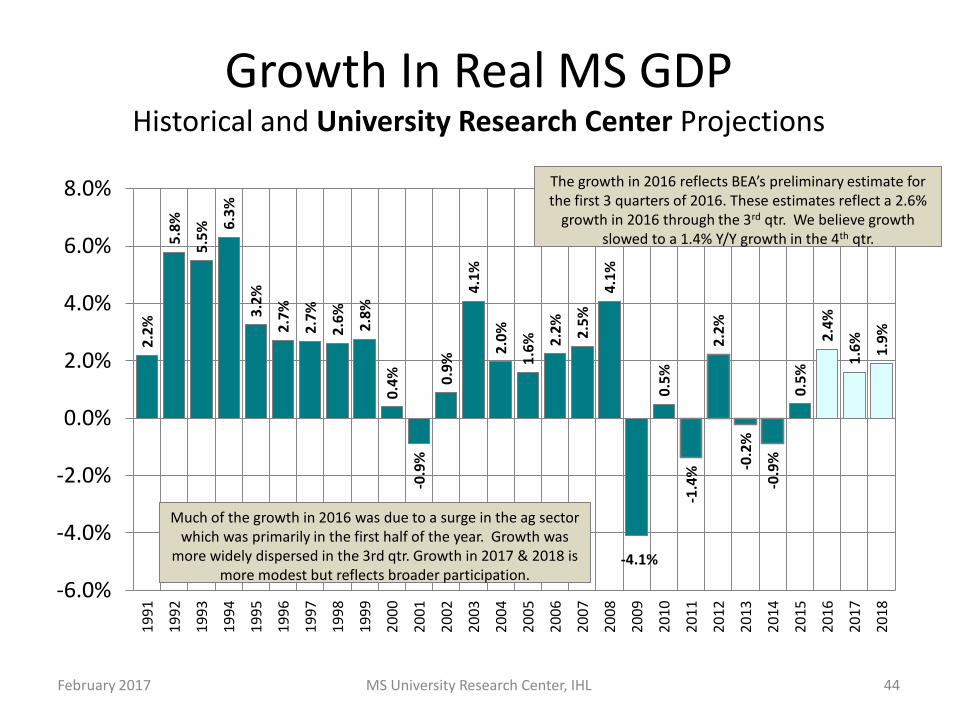

Growth In Real MS GDPHistorical and University Research Center Projections

2.2

%

5.8

%

5.5

% 6.3

%

3.2

%

2.7

%

2.7

%

2.6

%

2.8

%

0.4

%

-0.9

%

0.9

%

4.1

%

2.0

%

1.6

% 2.2

%

2.5

%

4.1

%

-4.1%

0.5

%

-1.4

%

2.2

%

-0.2

%

-0.9

%

0.5

%

2.4

%

1.6

%

1.9

%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

MS University Research Center, IHL 44February 2017

The growth in 2016 reflects BEA’s preliminary estimate for the first 3 quarters of 2016. These estimates reflect a 2.6%

growth in 2016 through the 3rd qtr. We believe growth slowed to a 1.4% Y/Y growth in the 4th qtr.

Much of the growth in 2016 was due to a surge in the ag sector which was primarily in the first half of the year. Growth was

more widely dispersed in the 3rd qtr. Growth in 2017 & 2018 is more modest but reflects broader participation.

Recap:

• US Economy has momentum in 2017– Risk of recession remains low

• MS has struggled since the great Recession.– 2016 is the 1st time the state has experienced 2 years

of consecutive growth since the recession– The strong headline growth of 2016 was driven by ag

volatility which will shave off growth in 2017– Growth in 2017 however will be more widespread and

will continue into 2018 at a modest pace.

• Despite a modest forecast, revenues have disappointed in FY 2017.

February 2017 MS University Research Center, IHL 45

APPENDIX

February 2017 MS University Research Center, IHL 46

Per Capita Personal Income2015

$6

8,7

04

$6

2,6

03

$5

9,9

49

$5

8,6

70

$5

6,1

47

$5

6,0

81

$5

5,9

72

$5

5,9

50

$5

5,9

05

$5

3,7

41

$5

2,0

52

$5

1,8

98

$5

0,8

99

$5

0,8

71

$5

0,2

95

$5

0,0

18

$4

9,7

45

$4

8,5

87

$4

8,5

44

$4

8,2

88

$4

8,1

12

$4

7,8

81

$4

7,6

33

$4

7,1

61

$4

6,9

47

$4

5,9

14

$4

5,9

02

$4

5,5

73

$4

4,4

29

$4

3,7

83

$4

3,5

66

$4

2,9

47

$4

2,8

12

$4

2,7

99

$4

2,3

00

$4

2,0

94

$4

1,9

40

$4

1,8

89

$4

1,8

09

$4

0,7

59

$4

0,3

06

$3

9,3

08

$3

9,1

56

$3

8,5

88

$3

8,3

92

$3

8,3

02

$3

8,2

52

$3

8,0

30

$3

7,9

38

$3

6,7

58

$3

4,7

71

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000C

on

nec

ticu

tM

assa

chu

sett

sN

ew J

ers

ey

New

Yo

rkA

lask

aW

yom

ing

Mar

ylan

dN

ort

h D

ako

taN

ew H

amp

shir

eC

alif

orn

iaV

irgi

nia

Was

hin

gto

nC

olo

rad

oM

inn

eso

taIll

ino

isR

ho

de

Isla

nd

Pe

nn

sylv

ania

Ve

rmo

nt

Neb

rask

aH

awai

iU

nit

ed

Sta

tes

Sou

th D

ako

taD

ela

war

eK

ansa

sTe

xas

Wis

con

sin

Iow

aO

klah

om

aFl

ori

da

Ore

gon

Oh

ioLo

uis

ian

aM

ich

igan

Mai

ne

Mis

sou

riTe

nn

esse

eIn

dia

na

Nev

ada

Mo

nta

na

No

rth

Car

olin

aG

eorg

iaU

tah

Ari

zon

aK

en

tuck

yId

aho

Sou

th C

aro

lina

Ark

ansa

sA

lab

ama

New

Mex

ico

We

st V

irgi

nia

Mis

siss

ipp

i

Per capita income is total personal income divided by total population.

February 2017 MS University Research Center, IHL 47

Per Capita Personal IncomeAdjusted for Cost of Living, 2015

$6

3,1

47

$

61

,14

8

$5

8,4

53

$

58

,29

6

$5

4,4

10

$

53

,58

1

$5

3,1

42

$

53

,11

9

$5

2,3

57

$

52

,12

2

$5

1,9

97

$

50

,83

3

$5

0,7

45

$

50

,73

3

$5

0,7

09

$

50

,67

7

$5

0,6

57

$

50

,58

0

$4

9,9

98

$

49

,94

5

$4

9,9

01

$

49

,15

8

$4

8,7

86

$

48

,59

9

$4

8,1

12

$

48

,01

1

$4

7,8

12

$

47

,31

5

$4

6,9

88

$

46

,74

5

$4

6,6

67

$

45

,88

6

$4

5,4

96

$

44

,83

2

$4

4,4

48

$

44

,38

3

$4

4,2

25

$

44

,07

7

$4

3,8

11

$

43

,71

7

$4

3,5

04

$

43

,31

4

$4

2,8

75

$

42

,32

3

$4

1,3

48

$

41

,34

2

$4

1,1

05

$

40

,61

8

$4

0,5

24

$

40

,10

5

$3

9,9

35

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000C

on

nec

ticu

tN

ort

h D

ako

taM

assa

chu

sett

sW

yom

ing

Sou

th D

ako

taN

ebra

ska

New

Ham

psh

ire

Ala

ska

New

Je

rse

yM

inn

eso

taK

ansa

sIo

wa

Mar

ylan

dV

irgi

nia

New

Yo

rkR

ho

de

Isla

nd

Pe

nn

sylv

ania

Okl

aho

ma

Was

hin

gto

nIll

ino

isC

olo

rad

oW

isco

nsi

nO

hio

Texa

sU

nit

ed

Sta

tes

Ve

rmo

nt

Cal

ifo

rnia

Mis

sou

riLo

uis

ian

aD

ela

war

eTe

nn

esse

eIn

dia

na

Mic

hig

anFl

ori

da

No

rth

Car

olin

aM

on

tan

aO

rego

nM

ain

eG

eorg

iaA

rkan

sas

Ke

ntu

cky

Ala

bam

aN

evad

aSo

uth

Car

olin

aW

est

Vir

gin

iaH

awai

iId

aho

Ari

zon

aU

tah

Mis

siss

ipp

iN

ew M

exic

o

Per capita income is total personal income divided by total population.

February 2017 MS University Research Center, IHL 48

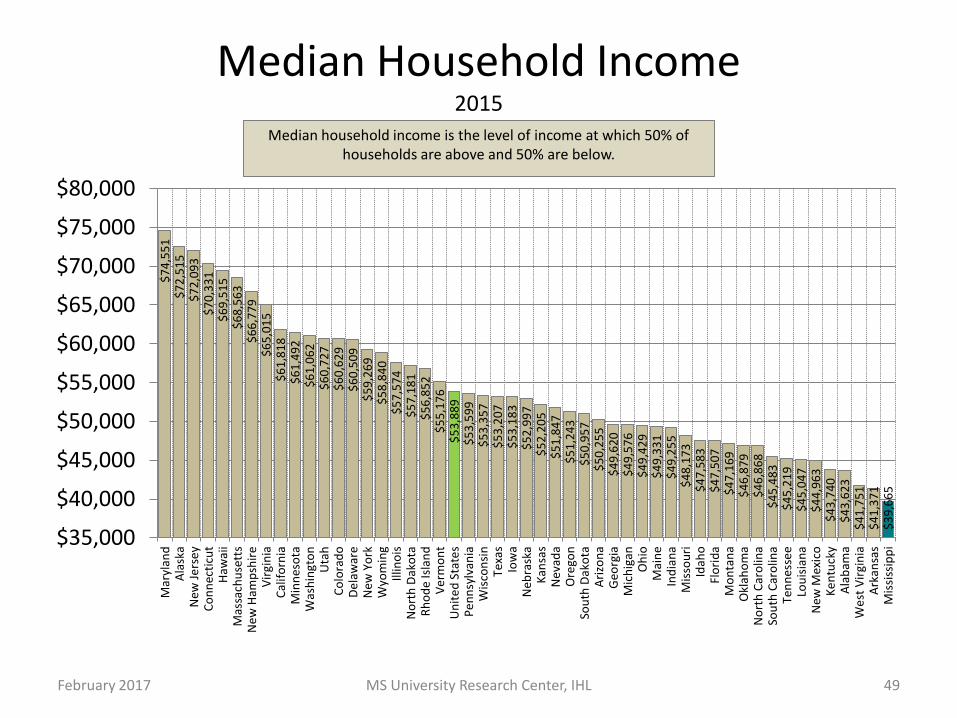

Median Household Income2015

$7

4,5

51

$7

2,5

15

$7

2,0

93

$7

0,3

31

$6

9,5

15

$6

8,5

63

$6

6,7

79

$6

5,0

15

$6

1,8

18

$6

1,4

92

$6

1,0

62

$6

0,7

27

$6

0,6

29

$6

0,5

09

$5

9,2

69

$5

8,8

40

$5

7,5

74

$5

7,1

81

$5

6,8

52

$5

5,1

76

$5

3,8

89

$5

3,5

99

$5

3,3

57

$5

3,2

07

$5

3,1

83

$5

2,9

97

$5

2,2

05

$5

1,8

47

$5

1,2

43

$5

0,9

57

$5

0,2

55

$4

9,6

20

$4

9,5

76

$4

9,4

29

$4

9,3

31

$4

9,2

55

$4

8,1

73

$4

7,5

83

$4

7,5

07

$4

7,1

69

$4

6,8

79

$4

6,8

68

$4

5,4

83

$4

5,2

19

$4

5,0

47

$4

4,9

63

$4

3,7

40

$4

3,6

23

$4

1,7

51

$4

1,3

71

$3

9,6

65

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000

$75,000

$80,000M

aryl

and

Ala

ska

New

Je

rse

yC

on

nec

ticu

tH

awai

iM

assa

chu

sett

sN

ew H

amp

shir

eV

irgi

nia

Cal

ifo

rnia

Min

nes

ota

Was

hin

gto

nU

tah

Co

lora

do

De

law

are

New

Yo

rkW

yom

ing

Illin

ois

No

rth

Dak

ota

Rh

od

e Is

lan

dV

erm

on

tU

nit

ed

Sta

tes

Pe

nn

sylv

ania

Wis

con

sin

Texa

sIo

wa

Neb

rask

aK

ansa

sN

evad

aO

rego

nSo

uth

Dak

ota

Ari

zon

aG

eorg

iaM

ich

igan

Oh

ioM

ain

eIn

dia

na

Mis

sou

riId

aho

Flo

rid

aM

on

tan

aO

klah

om

aN

ort

h C

aro

lina

Sou

th C

aro

lina

Ten

nes

see

Lou

isia

na

New

Mex

ico

Ke

ntu

cky

Ala

bam

aW

est

Vir

gin

iaA

rkan

sas

Mis

siss

ipp

i

Median household income is the level of income at which 50% of households are above and 50% are below.

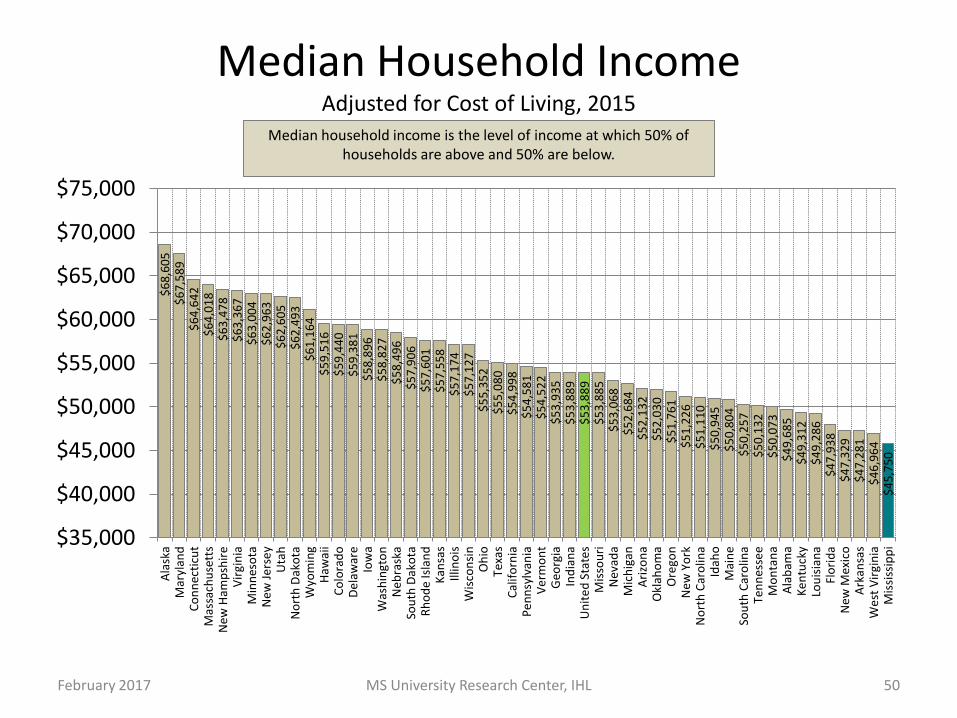

February 2017 MS University Research Center, IHL 49

Median Household IncomeAdjusted for Cost of Living, 2015

$6

8,6

05

$

67

,58

9

$6

4,6

42

$

64

,01

8

$6

3,4

78

$

63

,36

7

$6

3,0

04

$

62

,96

3

$6

2,6

05

$

62

,49

3

$6

1,1

64

$

59

,51

6

$5

9,4

40

$

59

,38

1

$5

8,8

96

$

58

,82

7

$5

8,4

96

$

57

,90

6

$5

7,6

01

$

57

,55

8

$5

7,1

74

$

57

,12

7

$5

5,3

52

$

55

,08

0

$5

4,9

98

$

54

,58

1

$5

4,5

22

$

53

,93

5

$5

3,8

89

$

53

,88

9

$5

3,8

85

$

53

,06

8

$5

2,6

84

$

52

,13

2

$5

2,0

30

$

51

,76

1

$5

1,2

26

$

51

,11

0

$5

0,9

45

$

50

,80

4

$5

0,2

57

$

50

,13

2

$5

0,0

73

$

49

,68

5

$4

9,3

12

$

49

,28

6

$4

7,9

38

$

47

,32

9

$4

7,2

81

$

46

,96

4

$4

5,7

50

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000

$75,000A

lask

aM

aryl

and

Co

nn

ecti

cut

Mas

sach

use

tts

New

Ham

psh

ire

Vir

gin

iaM

inn

eso

taN

ew J

ers

ey

Uta

hN

ort

h D

ako

taW

yom

ing

Haw

aii

Co

lora

do

De

law

are

Iow

aW

ash

ingt

on

Neb

rask

aSo

uth

Dak

ota

Rh

od

e Is

lan

dK

ansa

sIll

ino

isW

isco

nsi

nO

hio

Texa

sC

alif

orn

iaP

en

nsy

lvan

iaV

erm

on

tG

eorg

iaIn

dia

na

Un

ite

d S

tate

sM

isso

uri

Nev

ada

Mic

hig

anA

rizo

na

Okl

aho

ma

Ore

gon

New

Yo

rkN

ort

h C

aro

lina

Idah

oM

ain

eSo

uth

Car

olin

aTe

nn

esse

eM

on

tan

aA

lab

ama

Ke

ntu

cky

Lou

isia

na

Flo

rid

aN

ew M

exic

oA

rkan

sas

We

st V

irgi

nia

Mis

siss

ipp

i

Median household income is the level of income at which 50% of households are above and 50% are below.

February 2017 MS University Research Center, IHL 50

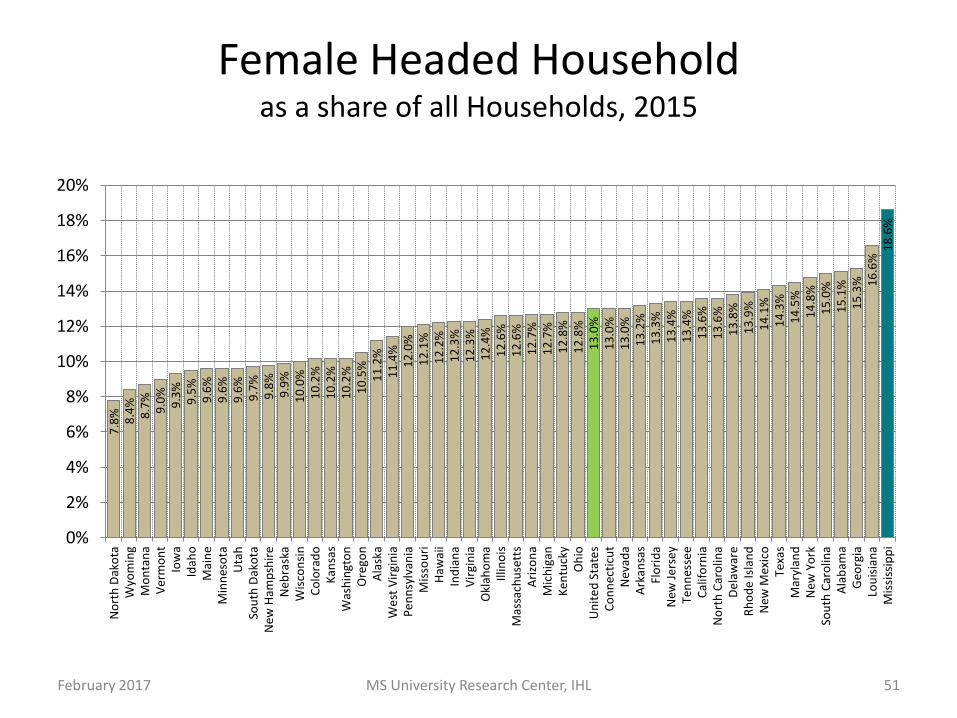

Female Headed Household as a share of all Households, 2015

7.8

% 8.4

%8

.7%

9.0

%9

.3%

9.5

%9

.6%

9.6

%9

.6%

9.7

%9

.8%

9.9

%1

0.0

%1

0.2

%1

0.2

%1

0.2

%1

0.5

%1

1.2

%1

1.4

%1

2.0

%1

2.1

%1

2.2

%1

2.3

%1

2.3

%1

2.4

%1

2.6

%1

2.6

%1

2.7

%1

2.7

%1

2.8

%1

2.8

%1

3.0

%1

3.0

%1

3.0

%1

3.2

%1

3.3

%1

3.4

%1

3.4

%1

3.6

%1

3.6

%1

3.8

%1

3.9

%1

4.1

%1

4.3

%1

4.5

%1

4.8

%1

5.0

%1

5.1

%1

5.3

% 16

.6%

18

.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

No

rth

Dak

ota

Wyo

min

gM

on

tan

aV

erm

on

tIo

wa

Idah

oM

ain

eM

inn

eso

taU

tah

Sou

th D

ako

taN

ew H

amp

shir

eN

ebra

ska

Wis

con

sin

Co

lora

do

Kan

sas

Was

hin

gto

nO

rego

nA

lask

aW

est

Vir

gin

iaP

en

nsy

lvan

iaM

isso

uri

Haw

aii

Ind

ian

aV

irgi

nia

Okl

aho

ma

Illin

ois

Mas

sach

use

tts

Ari

zon

aM

ich

igan

Ke

ntu

cky

Oh

ioU

nit

ed

Sta

tes

Co

nn

ecti

cut

Nev

ada

Ark

ansa

sFl

ori

da

New

Je

rse

yTe

nn

esse

eC

alif

orn

iaN

ort

h C

aro

lina

De

law

are

Rh

od

e Is

lan

dN

ew M

exic

oTe

xas

Mar

ylan

dN

ew Y

ork

Sou

th C

aro

lina

Ala

bam

aG

eorg

iaLo

uis

ian

aM

issi

ssip

pi

February 2017 MS University Research Center, IHL 51

Government DependenceShare of Total Personal Income From Transfer Payments and Government Earnings, 2015

12

.8%

14

.4%

14

.8%

14

.2%

13

.3%

12

.6%

14

.7%

15

.8%

15

.4%

14

.8%

14

.6%

13

.6%

15

.4%

17

.4%

15

.5%

15

.2%

19

.2%

19

.6%

17

.2%

17

.1%

12

.6% 17

.3%

20

.0%

17

.3%

18

.6%

17

.7%

17

.5%

13

.6%

13

.9% 2

0.6

%2

1.5

%2

0.1

%2

0.1

%2

0.3

%2

0.2

%2

0.0

%1

8.7

%2

0.2

%2

1.1

%2

0.9

%2

0.1

%2

2.6

%2

4.0

%2

2.8

%2

3.2

%1

5.7

%2

4.7

%1

5.9

%2

6.3

%2

8.2

%2

4.1

%

8.8

% 8.7

%9

.5%

10

.3%

11

.7%

12

.4%

10

.6%

9.8

%1

0.4

%1

1.5

%1

2.0

%1

3.1

%1

2.3

%1

0.7

%1

2.6

%1

3.3

% 9.5

%9

.0%

11

.5%

11

.6%

16

.2% 11

.9%

9.3

%1

2.5

%1

1.2

%1

2.2

%1

2.6

%1

6.6

%1

6.7

% 10

.2%

9.7

%1

1.1

%1

1.4

%1

1.3

%1

1.5

%1

1.7

%1

3.1

%1

1.7

%1

1.4

%1

2.6

%1

3.7

%1

2.1

%1

1.2

%1

3.8

%1

3.7

%2

2.1

%1

3.6

%2

3.3

%1

4.3

%1

3.2

%1

7.6

%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Co

nn

ecti

cut

New

Ham

psh

ire

Mas

sach

use

tts

New

Je

rse

yC

olo

rad

oN

ort

h D

ako

taTe

xas

Min

nes

ota

Illin

ois

Sou

th D

ako

taN

ebra

ska

Uta

hC

alif

orn

iaW

isco

nsi

nK

ansa

sW

ash

ingt

on

Pe

nn

sylv

ania

Ind

ian

aIo

wa

Nev

ada

Wyo

min

gU

nit

ed

Sta

tes

Flo

rid

aN

ew Y

ork

Idah

oG

eorg

iaO

klah

om

aV

irgi

nia

Mar

ylan

dTe

nn

esse

eM

ich

igan

Oh

ioM

isso

uri

Lou

isia

na

Rh

od

e Is

lan

dD

ela

war

eM

on

tan

aO

rego

nA

rizo

na

Ve

rmo

nt

No

rth

Car

olin

aM

ain

eA

rkan

sas

Sou

th C

aro

lina

Ala

bam

aH

awai

i*K

en

tuck

yA

lask

a*M

issi

ssip

pi

We

st V

irgi

nia

New

Mex

ico

February 2017 MS University Research Center, IHL 52

40.6% of Income in MS comes from the Government. 26.3 percent is from transfer payments and 14.4% is from government earnings. Only WV & NM are more dependent on the

government. MS has the highest share of income from transfer payments. These sources tend to grow slow and in the case of earnings have decreased in recent years.

Workforce Participation by Age, 2016

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

16 to 19 years 20 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65 years andover

MS US

February 2017 MS University Research Center, IHL 53

-11.4

-5.6-3.6 -1.4

-10.6 -10.7

-4.6

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

16 to 19 years 20 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65 years andover

MS-US Gap in Workforce Participation Rate by Age

The larger gap is due in part to higher incidence of disability.

Workforce Participation, Men

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

20 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65 years and over

MS US

February 2017 MS University Research Center, IHL 54

-3.7% -4.9% -4.6%

-10.1%-13.0%

-6.1%

-15.0%

-10.0%

-5.0%

0.0%

20 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65 years and over

MS-US Gap in Workforce Participation Rate, Men

Workforce Participation, Women

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

20 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65 years and over

MS US

February 2017 MS University Research Center, IHL 55

-7.0%-1.7%

1.9%

-10.6% -8.4%-3.3%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

20 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65 years and over

MS-US Gap in Workforce Participation Rate, Women

Workforce Participation In MS, 2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20 to 24years

25 to 34years

35 to 44years

45 to 54years

55 to 64years

65 yearsand over

By Gender and Age

Men Women

55.7% 56.5%

60.8%

51.7%

62.2%

58.3%

49.5%

54.9%

0%

10%

20%

30%

40%

50%

60%

70%

By Race and Gender

February 2017 MS University Research Center, IHL 56

The participation rate is higher for men for all age cohorts

There is very little difference between white and nonwhite. The lowest participation rate is

among white women.