leisure and hospitality hotel britain 2015 · leisure and hospitality hotel britain 2015 the guide...

TRANSCRIPT

LEISURE AND HOSPITALITY

HOTEL BRITAIN 2015THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK

CONTENTSECONOMY AND TOURISM

UK HOTEL TRANSACTIONS

UK HOTEL DEVELOPMENT TRENDS

2014 SURVEY RESULTS

WINNERS AND LOSERS

SUMMARY OF FIVE YEAR PERFORMANCE

THE ROAD AHEAD

COMPETITION

CLAIRVOYANT CORNER

SURVEY COVERAGE

BDO LEISURE AND HOSPITALITY SERVICES

4

10

14

20

26

29

34

36

38

40

42

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 2

As we write, global economic and geopolitical uncertainty is still upon us. The European Union continues to be plagued by a stagnating economy and sovereign debt issues; developments in the Ukrainian-Russian conflict have greatly affected international relations and consequently the economy of the Russian Federation; while, further afield, the Chinese economy grew at one of the slowest rates for the last 24 years in 2014.

However, despite the somewhat gloomy scenario, there is still some light at the end of the tunnel. In 2014, the US economy grew by 2.2-2.4% and is forecast to rise above 3% in 2015, the strongest economic growth in a decade for the country. But it is the UK that experienced the strongest rate of growth amongst all developed countries, up 2.8% on the previous year. This was driven by strong consumer spending. The drop in the oil price kept inflation at a record low, and boosted both consumer and business confidence, resulting in reduced unemployment and wage growth.

As a result of this overall economic optimism, hotels in the UK experienced a stellar 2014. Bucking the trend of last year, regional hotels outperformed their London counterparts. Rooms yield for hotels in the regions experienced double digit growth. As demand for hotels remained strong, hoteliers succeeded in pushing AARR up, and resulting in regional hotels experiencing a higher compound annual growth rate over the last five years when compared to the capital.

However, London hotels did not stand still. Despite the significant 4% increase in supply, occupancy remained robust, confirming the importance of the hotel sector in the capital, where hotel’s occupancy is one of the highest across Europe. In the capital, AARR continued to grow, albeit modestly and at a varying speed within different segments. Overall, London hotels continued to post growth in 2014,

with rooms yield for the year already surpassing the peak experienced in 2007.

The health of the UK hotel sector is confirmed by the increase in transactional activity, which reached £6.1bn in 2014, the highest figure since 2006. There has been a rush into regional transactions, where hotels have sold above the asking price last year.

2014 also cemented the importance of the budget segment. New concepts and a modernisation of the offer are underway, with a strong pipeline for the sector at about 47% of the total planned new supply.

Nevertheless, the outlook still remains unclear, especially as the general election in May could cast doubts in the short term, and the strength of the pound might affect inbound visitors. However, as already mentioned, the future of the hotel market is expected to continue on its upward path. The Rugby World Cup will showcase the UK abroad and should positively affect hotel performance for the current year. Furthermore, international visitors are expected to continue to increase in 2015, reaching 35m, boding well for future hotel performance.

FOREWORD

ROBERT BARNARDPartnerLeisure and Hospitality Services [email protected]

Go the regions!

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 4

ECONOMY AND TOURISM

In 2014, the UK economy grew at a faster rate than any other major advanced economy and recorded its best performance since 2007.The IMF estimates growth for the full year to be at 3.21%, however recent reports suggest that this momentum is now running out of steam, as the Office for National Statistics (ONS) claimed growth for 2014 was at 2.8%. Growth has primarily been attributable to the services sector, but forecasters believe that the recent fall in oil prices will help to fuel growth in the manufacturing sector. The IMF has forecast a slowdown of growth to less than 3% over the coming years.

CPI inflation remains below the Bank of England’s target of 2%, falling to 0.0% in February 2015. Tumbling energy prices, and the strength of the pound have been the main causes for this, and forecasters believe that this could turn negative in the short to medium term. However, this is generally good news for the UK economy, as it should fuel household spending which is an important driver. Inflation is expected to rebound by the end of the year as these effects are absorbed. The current account deficit stood at -4.22% of GDP. This figure highlights that with relatively stronger household spending the UK is becoming even more dependent on foreign capital.

The UK government’s gross debt increased slightly in 2014 to 91.89% of total GDP. According to the ONS, general government gross debt stood at £1,457.2bn at the end of November 2014, an increase of £89.7bn when compared with the previous year.

The labour market continues to show positive signs of recovery with the ONS reporting 30.9m people in work at the end of 2014. Between October and December 2014, the rate of unemployment fell to 5.7% (1.91m), the lowest level for six years. This was as a result of increasing

TABLE 1: UK economic indicators, 2012-2016f

2012 2013 2014f 2015f 2016f

Real GDP Growth (%) 0.28 1.74 3.21 2.71 2.44

CPI inflation (%) 2.82 2.56 1.63 1.80 2.00

Current account deficit (% GDP)

-3.83 -4.51 -4.22 -3.77 -3.30

Government gross debt (% GDP)

89.06 90.58 91.98 93.11 92.92

Unemployment (%) 7.95 7.60 6.35 5.78 5.47

SOURCE: International Monetary Fund, October 2014fforecast

VISITOR NUMBERS INCREASE International visitor numbers grew for the fourth consecutive year in 2014. Visitors increased by 5.8% to 34.8m, an all time high. Overall, the holiday segment remained the main driver of growth, up 7.7%, accounting for almost two-fifths of the total. However, results are still provisional and there is speculation that the total inbound visitor numbers will surpass the 35m mark during the current year.

signs of confidence in the economy and the number of vacancies at a 14 year high. Unemployment is forecast to continue declining further during 2015, albeit at a slower pace.

Notwithstanding the reported good figures, further struggles to grow in the Eurozone and uncertainty surrounding the imminent election could compromise recovery and a return to strong growth.

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK5

Europe continues to be the main inbound market for the UK, accounting for about three-quarters of the total, or 25.8m. North American visits for 2014 were up 4% to 3.7m. However, the segment has slowed its pace of growth, mainly due to the 11% drop in visits from Canada.

Figure 1 shows the seasonality of inbound visits to the UK. Total visits peaked during the month of June 2014, surpassing the 3m mark, up 13.6% on the same month the previous year. This was as a result of the increase in visits from Europe, while the North American market remained flat (-0.5%) and the rest of the world declined marginally by 1% to 444,000.

Overall January and March were the lowest performing months for inbound visits over the last two years, with the summer months generally welcoming more visitors to the UK.

Vis

itors

(in

thou

sand

s)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Dec

-14

Nov

-14

Oct

-14

Sep-

14Au

g-14

Jul-

14Ju

n-14

May

-14

Apr-

14M

ar-1

4Fe

b-14

Jan-

14D

ec-1

3N

ov-1

3O

ct-1

3Se

p-13

Aug-

13Ju

l-13

Jun-

13M

ay-1

3Ap

r-13

Mar

-13

Feb-

13Ja

n-13

Dec

-12

All visits Europe Other countries North America

FIGURE 1: Overseas visitors to UK, by source market 2013-2014

SOURCE: International Passenger Survey, ONS

2010 2011 2012 2013 2014 2014 % change 2014 market share

Holiday 11,668 12,008 11,961 12,781 13,760 7.7% 39.5%

Business 6,793 7,238 7,422 7,931 8,370 5.5% 24.1%

Visit friends or family (VFF) 8,408 8,841 8,948 9,369 9,840 5.0% 28.3%

Miscellaneous 2,935 2,710 2,752 2,812 2,830 0.6% 8.1%

All visits 29,803 30,798 31,084 32,893 34,800

Year-on-year growth -6.5% 3.3% 0.9% 5.8% 5.8%

SOURCE: VisitBritain Monthly Update: December 2014

2014 figures are provisional

TABLE 2: Overseas visitors to the UK, by purpose of visit (thousands)

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 6

Figure 2 shows the year-on-year percentage change for selected inbound markets to the UK during 2014. We note that visits from Southern Europe grew very strongly last year, with visits from Greece experiencing a second consecutive year of growth. Singapore (+24%) and Saudi Arabia (+29%) also grew considerably, with both countries reversing a negative trend experienced in 2013. Conversely, visits from Mexico (-15%) and China (-7%) declined during 2014 in contrast to the strong growth experienced during the previous year.

Figure 3 shows a comparison between inbound and domestic visits and spending to the UK. However, domestic visitor numbers for the full year were not available at the time of writing. Inbound visitor expenditure in 2014 mirrored the increase in visits. Expenditure was up 3.5% to £21.7bn. Domestic visitors for the year to date to October 2014 were down -6.5% to 96.7m when compared to the previous year. Domestic expenditure was also down, albeit to a lesser extent (-2.5% to £19.6bn). We note that, generally speaking, November is a strong month for corporate activity, and December sees a lot of visits to family and friends during the Christmas period, which could result in different figures for the full year.

TABLE 3: Domestic tourism by purpose of visit (YTD October)

2010 2011 2012 2013 20142013-2014 % change

Holiday 50.2 53.0 51.2 50.8 47.7 -6.1%

Business 13.5 15.4 15.4 15.1 13.9 -8.0%

Visit friends or family (VFF)

33.8 35.9 33.5 34.0 32.5 -4.5%

Miscellaneous 2.8 3.4 3.5 3.5 2.6 -26.2%

All visits 100.4 107.6 103.6 103.5 96.7

Year-on-year growth 7.2% -3.8% -0.1% -6.6%

SOURCE: ONS, Overseas Travel and Tourism; Great Britain Tourism Survey October 2014, Great Britain Tourism Survey 2013

-20

-10

0

10

20

30

40

Gre

ece

Port

ugal

Turk

ey

Sing

apor

e

Can

ada

Mex

ico

27%

35%

28%24%

-7%

-13%

Nig

eria

-11%-15%

Braz

il

New

Zea

land

Saud

i Ara

bia

Chi

na

12%

21%

29%

FIGURE 2: Percentage change in visits from selected countries

SOURCE: VisitBritain, Monthy Inbound Update: December 2014 (2014 figures are provisional)

0

20

40

60

80

100

120

140

2010 2011 2012 2013 2014

Vis

itors

(mill

ions

)

Spen

d (£

billi

ons)

Domestic visitors (millions)Inbound visitors (millions)

Domestic visitors (millions)Inbound visitors (millions)

0

5

10

15

20

25

30

FIGURE 3: All UK visitors expenditure 2010-2014

SOURCE: ONS, Overseas Travel and Tourism; Great Britain Tourism Survey October 2014, Great Britain Tourism Survey 2013 (Domestic figures as per October 2014)

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK7

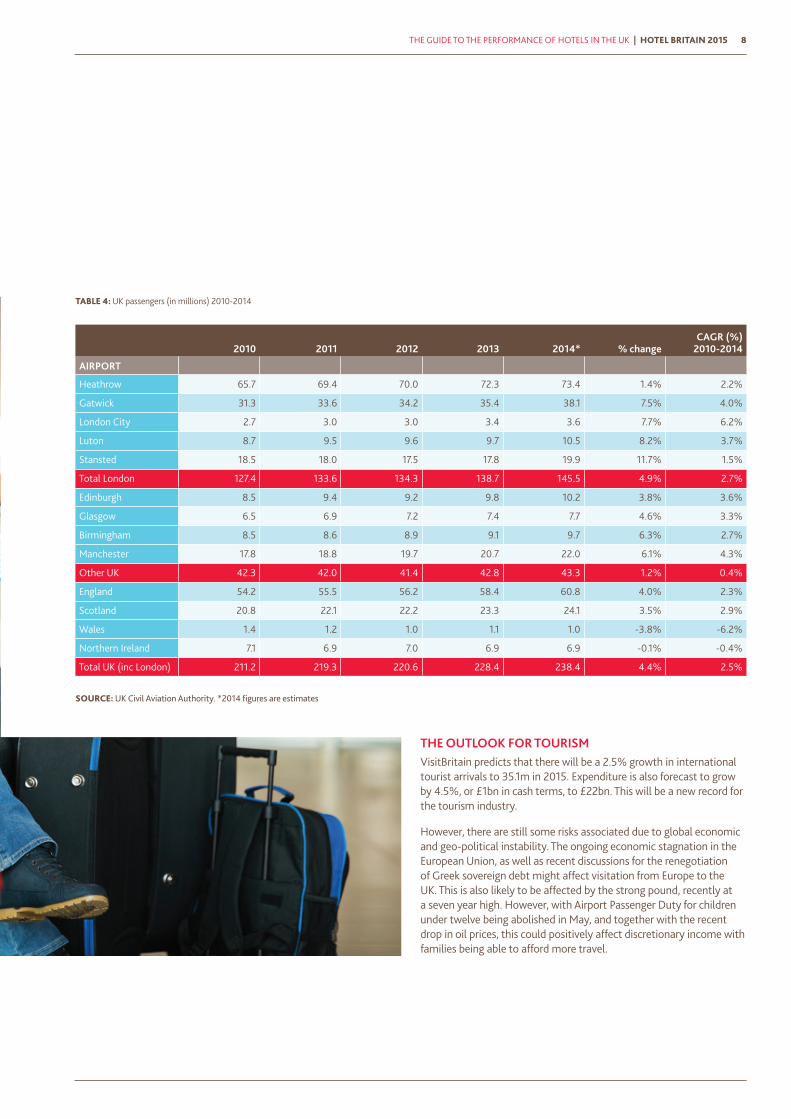

PASSENGER NUMBERSAccording to the UK Civil Aviation Authority (CAA), UK airports experienced another year of strong growth with passenger numbers up 4.4% to 238.4m in 2014, the fourth year of growth. The growth in passengers was distributed fairly evenly between London (up 4.9% to 145.5m) and regional UK (up 3.5% to 92.8m).

Excluding London airports, England was the best performing region for passenger traffic, up 4% to 60.8m. However, Scotland experienced the best compound of annual growth rate (CAGR) (2.9%), with strong growth reported by both Glasgow and Edinburgh. Edinburgh Airport surpassed the 10m mark, thanks to the addition of new long haul routes. The Barclays Tourist Dynamic Report also predicts that visitors to Scotland will increase by 40% by 2017, boding well for future tourism performance.

In Wales, Cardiff International Airport saw a -3.8% decline in passenger numbers to 1m. On the other hand, the flat performance for Northern Ireland airports is likely to reverse in 2015, with the introduction of seasonal Virgin Atlantic flights from Belfast during the summer.

Stansted was the only London airport to experience double digit growth in 2014, up 11.7% to 19.9m passengers. The airport now serves more than 170 destinations worldwide and it is linked to more EU destinations than any other UK airport. Acquired by the Manchester Airport Group in 2013, the airport has been under redevelopment with further talks at government levels for improved rail connections to the Essex hub.

Southend Airport also experienced strong growth in 2014, with a 13.6% increase in passenger numbers to 1.1m. The airport saw Flybe adding six new routes in the year, and also easyJet strengthening its presence at the airport.

Prestwick Airport saw a 20.3% decline in passenger numbers to 912,000 in 2014. After been purchased by the Scottish Government for one pound, the airport saw Ryanair moving some flights to Glasgow International. At present there are discussions about the possibility of the airport been made into the first UK spaceport.

Cambridge was the top performing airport for year on year growth in 2014, up a staggering 123.4% to 21,000 passengers. This was the result of Cityjet running summer flights to Dublin and Amsterdam. However, these air links were cancelled in the autumn and despite a £17m deal to upgrade its runway, the airport continues to suffer from the impact of strong seasonality.

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 8

TABLE 4: UK passengers (in millions) 2010-2014

2010 2011 2012 2013 2014* % changeCAGR (%)

2010-2014

AIRPORT

Heathrow 65.7 69.4 70.0 72.3 73.4 1.4% 2.2%

Gatwick 31.3 33.6 34.2 35.4 38.1 7.5% 4.0%

London City 2.7 3.0 3.0 3.4 3.6 7.7% 6.2%

Luton 8.7 9.5 9.6 9.7 10.5 8.2% 3.7%

Stansted 18.5 18.0 17.5 17.8 19.9 11.7% 1.5%

Total London 127.4 133.6 134.3 138.7 145.5 4.9% 2.7%

Edinburgh 8.5 9.4 9.2 9.8 10.2 3.8% 3.6%

Glasgow 6.5 6.9 7.2 7.4 7.7 4.6% 3.3%

Birmingham 8.5 8.6 8.9 9.1 9.7 6.3% 2.7%

Manchester 17.8 18.8 19.7 20.7 22.0 6.1% 4.3%

Other UK 42.3 42.0 41.4 42.8 43.3 1.2% 0.4%

England 54.2 55.5 56.2 58.4 60.8 4.0% 2.3%

Scotland 20.8 22.1 22.2 23.3 24.1 3.5% 2.9%

Wales 1.4 1.2 1.0 1.1 1.0 -3.8% -6.2%

Northern Ireland 7.1 6.9 7.0 6.9 6.9 -0.1% -0.4%

Total UK (inc London) 211.2 219.3 220.6 228.4 238.4 4.4% 2.5%

SOURCE: UK Civil Aviation Authority. *2014 figures are estimates

THE OUTLOOK FOR TOURISMVisitBritain predicts that there will be a 2.5% growth in international tourist arrivals to 35.1m in 2015. Expenditure is also forecast to grow by 4.5%, or £1bn in cash terms, to £22bn. This will be a new record for the tourism industry.

However, there are still some risks associated due to global economic and geo-political instability. The ongoing economic stagnation in the European Union, as well as recent discussions for the renegotiation of Greek sovereign debt might affect visitation from Europe to the UK. This is also likely to be affected by the strong pound, recently at a seven year high. However, with Airport Passenger Duty for children under twelve being abolished in May, and together with the recent drop in oil prices, this could positively affect discretionary income with families being able to afford more travel.

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 10

The UK hotel transaction market continued in an upward direction, building on the gains made in 2013. JLL reported that in 2014 the total of commercial real estate investment in the UK amounted to £65bn. This was 3% higher than the 2006 peak, as well as 13% higher than the 2013 figure. During the same year, hotel deals accounted for about 10% of the total, with Savills reporting that the total transaction value for UK hotels in 2014 was £6.1bn, the highest since 2006.

Our predictions in the 2014 issue of Hotel Britain proved correct. In 2014, the majority of transactions, i.e. about two-thirds of the total, were of single assets. Last year we also predicted notable activity in the midscale/ budget end of the market. This was evidenced by Kew Green buying 25 Holiday Inn hotels in four different transactions, as well as the sale of 144 Travelodges bought by a consortium of Avenue Capital, Goldentree Asset Management and Goldman Sachs for an estimated £520m. In addition, Lone Star and Somerston Capital bought twelve Holiday Inn Express hotels across the UK.

Notable single transactions for the year include the 200 bedroom Harrington Hall Hotel in London, bought for £89m by Middle Eastern investors; the 50% stake acquisition of The Savoy Hotel sold by Lloyds Banking Group; the acquisition of the Grand Hotel Brighton by a company owned by Galen & Hilary Weston; and the acquisition of the Turnberry Resort in Scotland sold by Leisurecorp to The Trump Organisation for an estimated £35.7m.

The average transaction value in 2014 was £66m, up 30.6% from the previous year. This was mainly attributed to the improved UK economic conditions which continued to boost investor confidence. Secondly, 2014 experienced less portfolio transactions when compared to the previous year, with only one-third of all transactions being multiple asset deals. This is also reflected in the average price per key, which increased by 5.3% to £169,085 in 2014 when compared to the previous year.

However, despite the increase in the overall value of transactions, the price per room did not increase significantly due to the high amount of mid- and lower-scale hotel transactions, as well as investors moving out of primary locations to seek better value for money.

UK HOTEL TRANSACTIONS

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012 2013 2014

14.902

66.763

54.700

32.403

50.521

65.968

Aver

age

valu

e pe

r tra

nsac

tion

(£m

)

FIGURE 4: Average value of transaction

SOURCE: BDO research

2009 2010 2011 2012 2013 2014

£149,045

£319,316

£197,967£216,525

£160,563 £169,085

Aver

age

pric

e pe

r roo

m (£

m)

0

£50,000

£100,000

£150,000

£200,000

£250,000

£300,000

£350,000

FIGURE 5: Average price per room in UK hotel transactions

SOURCE: BDO research

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK11

INVESTMENT TRANSACTIONS ARE ABOVE ASKING PRICESDespite seeking good value for money deals, investors were ready to pay above the asking price to secure assets. An example of this was the KSL acquisition of the De Vere Village Urban Resorts portfolio for a reported £480m, 6% above the asking price.

Kew Green is also reported to have paid £30m above the price tag for a deal including 19 Holiday Inn Hotels across UK. This represents a staggering 42.8% above the asking price.

The trend is likely to continue in 2015, with the Radisson Blu Royal Mile Hotel in Edinburgh being sold for more than the £59m price tag. This is primarily the result of increased economic conditions and a returning appetite for investments.

THE YEAR OF REGIONAL TRANSACTIONSJLL reported that overall the total commercial real estate investment in the UK regions was up 70% in 2014 to a combined value of £28bn. This is reflected in our study: about two-thirds of total hotel transactions were carried out in the regions during 2014. Investors continued to seek good investment opportunities in primary regional locations. However, the market also started looking to secondary locations.

Examples include the continued expansion of Topland in the regional market, with the company acquiring Hallmark Hotels in 2014 and The Feathers Group at the beginning of 2015. Starwood Capital also consolidated its presence by the acquisition of the Four Pillars hotel portfolio.

LONDON HOTEL PRICES STABILISE, REGIONAL HOTELS PRICES PICK UPTable 5 shows the comparison of price per room for transactions in London and the regions in 2014. It is interesting to note that the average price per room in regional UK was up by 30% when compared to the previous year. The median price was also up by about 14%.

However, as no hotel in London surpassed the £1m price per room tag, the average prices for the capital declined by 10% to £337,774 when compared to the previous year. We note that this was mirrored in the 8.8% decline in the highest price paid per room, which was for the Park City Hotel Kensington in December (£967,742).

As mentioned earlier, London hotels saw more stable average prices in 2014 when compared to the previous year. The average price per room was £337,774 and this was despite an increase in the top end of the market hotel transactions. However, the highest price per room paid in London in 2014 was below the £1m mark per room paid for the Parkes hotel in 2013. On the other hand, the lowest price per room paid in the capital was for the Travelodge Enfield, at £75,758, up 13.6% when compared to the comparable transaction last year.

In the regions, the highest price per room was for the five-star Lowry Hotel in Manchester, sold by Rocco Forte Hotels to Westmont Hospitality Group and Mount Kellett Capital Management for a total of £40m, or £272,727 per room. This compared to the Park Inn by Radisson Leigh which commanded a £18,519 price per room tag when purchased by Kro Hotels.

TABLE 5: Comparison of price per room for transactions in London and the regions 2014

Price per room (£)

Average (mean) Median Highest Lowest

London 337,774 258,621 967,742 75,758

Regions 97,236 71,148 272,727 18,519

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 12

THE FUTURE – 2015

2015 is expected to see continuing robust trading activity. Early indicators of this are the divestment of the Moorfield Real Estate Funds, as well as KSL seeking a buyer for the Malmaison and Hotel du Vin portfolio and the sale of the Jurys Inn group to Lone Star.

The year ahead will continue to see an increase in lenders willing to offer finance as their appetite for investment returns due to the improved overall economic conditions. There is also the possibility of an increase in sales of assets to crystallise profits from properties acquired during or shortly after the economic downturn.

Overall, there is still pressure on operating performance, with hotels needing to shore up their bottom lines in order to command premium prices during the sale process.

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK13

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 14

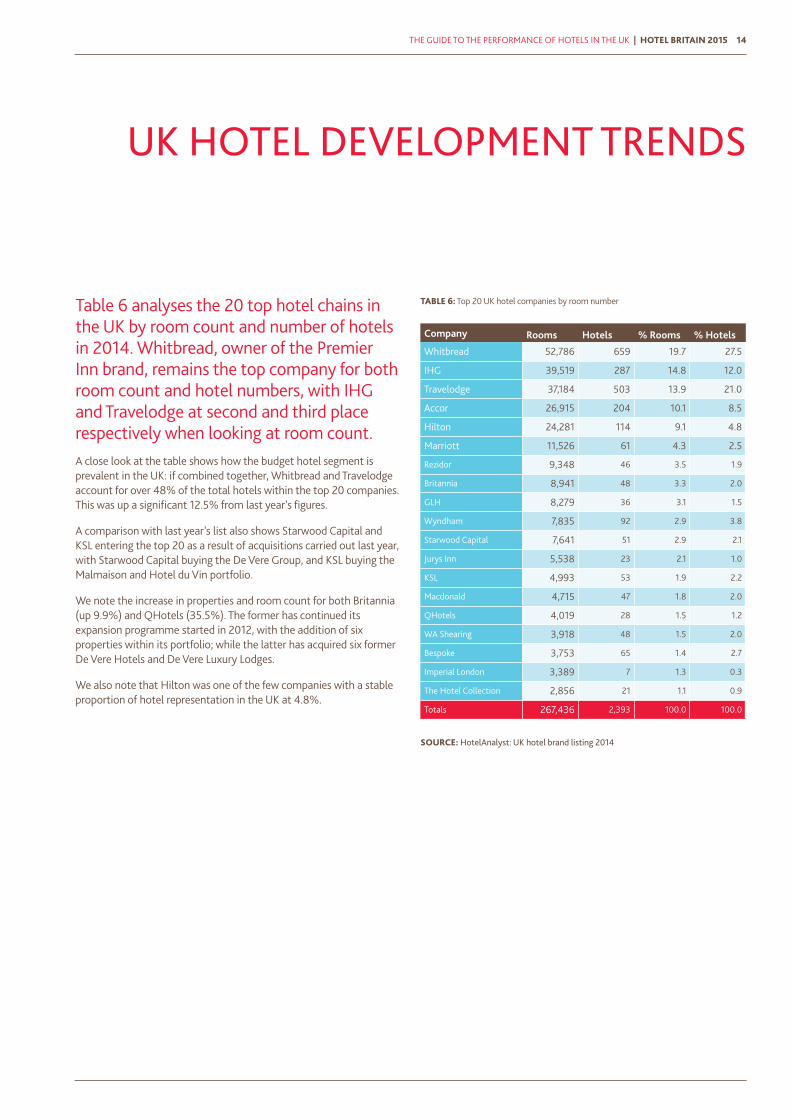

Table 6 analyses the 20 top hotel chains in the UK by room count and number of hotels in 2014. Whitbread, owner of the Premier Inn brand, remains the top company for both room count and hotel numbers, with IHG and Travelodge at second and third place respectively when looking at room count. A close look at the table shows how the budget hotel segment is prevalent in the UK: if combined together, Whitbread and Travelodge account for over 48% of the total hotels within the top 20 companies. This was up a significant 12.5% from last year’s figures.

A comparison with last year’s list also shows Starwood Capital and KSL entering the top 20 as a result of acquisitions carried out last year, with Starwood Capital buying the De Vere Group, and KSL buying the Malmaison and Hotel du Vin portfolio.

We note the increase in properties and room count for both Britannia (up 9.9%) and QHotels (35.5%). The former has continued its expansion programme started in 2012, with the addition of six properties within its portfolio; while the latter has acquired six former De Vere Hotels and De Vere Luxury Lodges.

We also note that Hilton was one of the few companies with a stable proportion of hotel representation in the UK at 4.8%.

UK HOTEL DEVELOPMENT TRENDS

TABLE 6: Top 20 UK hotel companies by room number

Company Rooms Hotels % Rooms % Hotels

Whitbread 52,786 659 19.7 27.5

IHG 39,519 287 14.8 12.0

Travelodge 37,184 503 13.9 21.0

Accor 26,915 204 10.1 8.5

Hilton 24,281 114 9.1 4.8

Marriott 11,526 61 4.3 2.5

Rezidor 9,348 46 3.5 1.9

Britannia 8,941 48 3.3 2.0

GLH 8,279 36 3.1 1.5

Wyndham 7,835 92 2.9 3.8

Starwood Capital 7,641 51 2.9 2.1

Jurys Inn 5,538 23 2.1 1.0

KSL 4,993 53 1.9 2.2

Macdonald 4,715 47 1.8 2.0

QHotels 4,019 28 1.5 1.2

WA Shearing 3,918 48 1.5 2.0

Bespoke 3,753 65 1.4 2.7

Imperial London 3,389 7 1.3 0.3

The Hotel Collection 2,856 21 1.1 0.9

Totals 267,436 2,393 100.0 100.0

SOURCE: HotelAnalyst: UK hotel brand listing 2014

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK15

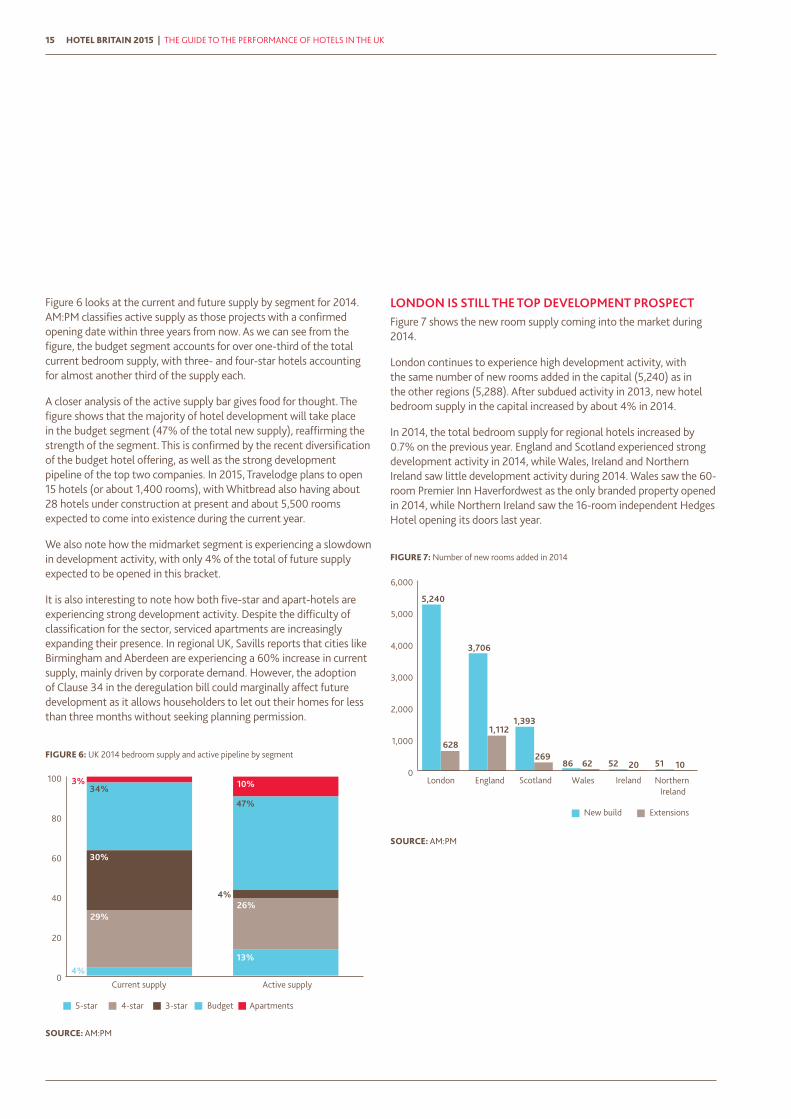

Figure 6 looks at the current and future supply by segment for 2014. AM:PM classifies active supply as those projects with a confirmed opening date within three years from now. As we can see from the figure, the budget segment accounts for over one-third of the total current bedroom supply, with three- and four-star hotels accounting for almost another third of the supply each.

A closer analysis of the active supply bar gives food for thought. The figure shows that the majority of hotel development will take place in the budget segment (47% of the total new supply), reaffirming the strength of the segment. This is confirmed by the recent diversification of the budget hotel offering, as well as the strong development pipeline of the top two companies. In 2015, Travelodge plans to open 15 hotels (or about 1,400 rooms), with Whitbread also having about 28 hotels under construction at present and about 5,500 rooms expected to come into existence during the current year.

We also note how the midmarket segment is experiencing a slowdown in development activity, with only 4% of the total of future supply expected to be opened in this bracket.

It is also interesting to note how both five-star and apart-hotels are experiencing strong development activity. Despite the difficulty of classification for the sector, serviced apartments are increasingly expanding their presence. In regional UK, Savills reports that cities like Birmingham and Aberdeen are experiencing a 60% increase in current supply, mainly driven by corporate demand. However, the adoption of Clause 34 in the deregulation bill could marginally affect future development as it allows householders to let out their homes for less than three months without seeking planning permission.

LONDON IS STILL THE TOP DEVELOPMENT PROSPECTFigure 7 shows the new room supply coming into the market during 2014.

London continues to experience high development activity, with the same number of new rooms added in the capital (5,240) as in the other regions (5,288). After subdued activity in 2013, new hotel bedroom supply in the capital increased by about 4% in 2014.

In 2014, the total bedroom supply for regional hotels increased by 0.7% on the previous year. England and Scotland experienced strong development activity in 2014, while Wales, Ireland and Northern Ireland saw little development activity during 2014. Wales saw the 60-room Premier Inn Haverfordwest as the only branded property opened in 2014, while Northern Ireland saw the 16-room independent Hedges Hotel opening its doors last year.

0

1,000

2,000

3,000

4,000

5,000

6,000

London England Scotland Wales Ireland

New build Extensions

Northern Ireland

5,240

628

3,706

1,1121,393

26951 1086 62 52 20

FIGURE 7: Number of new rooms added in 2014

SOURCE: AM:PM

0

20

40

60

80

100

Current supply Active supply

20.0%29%

4%

34%3%

30%

26%

13%

47%

10%

5-star 4-star 3-star Budget Apartments

4%

FIGURE 6: UK 2014 bedroom supply and active pipeline by segment

SOURCE: AM:PM

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 16

NEW TRENDSSharing economy

The rise of the likes of Airbnb is likely to affect future demand patterns for hotels. While the impact of such alternative forms of accommodation is not fully understood in the EU market, the reaction to this form of accommodation has varied. Barcelona has fined Airbnb €30,000 as the company breached local tourism laws, while Berlin has claimed that the rise of the practice led to an increase in rental prices and has banned short term lettings.

However, Amsterdam has passed a law aimed to allow the short term rentals in return for tax payments, while London’s proposal to overturn a 40 year-old law banning short term rental has encountered opposition from its local authorities.

Emergence of new markets

The emergence of travellers from other parts of the world will influence the offering and marketing of hotels across the globe, as widely demonstrated by hotels and hotel companies fully exploiting social media channels.

Tech and app friendly rooms

Hotel rooms are increasingly becoming an extension of mobile phones and other technology. Following the introduction of i-Pads to control room temperature and lighting and mobile key technology, there is a clear demand for techno-savvy hotel rooms. Smart TV, interactive tourism guides, and improved Wi-Fi connectivity are only some of the new improvements introduced by hotels. The latest example is the refurbishment of the Express by Holiday Inn concept which will be rolled out in Europe during the next three years.

Continued interest in the budget segment

Having driven strong growth in 2014, the budget segment has reaffirmed its status as one of the most important segments for the industry. Recently new brands and concepts have entered the UK hotel market, and this is expected to continue even further as customers remain highly price conscious and seek good value for money deals.

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK17

PLANNED HOTEL OPENINGS 2015:A selection of planned hotel rooms openings in key cities

Source: BDO Research and Hotelsdata

London

6,400

Aberdeen

540

Bath

99

Brentford

124

Birmingham

166

Chester

63

Edinburgh

304

Exeter

120

Glasgow

492

Liverpool

472

Manchester

838

Middlesbrough

138

Newcastle

250

Southampton

259

Southend on Sea

80Heathrow

184

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 18

LONDON (CIRCA 6,400)

CitizenM: 2 hotelsCompany: CitizenMRooms: 616

Crowne Plaza Albert EmbankmentCompany: Intercontinental Hotel GroupRooms: 130

Hilton London BanksideCompany: Splendid Hotel GroupRooms: 292

Holiday Inn Express London ExcelCompany: Intercontinental Hotel GroupRooms: 204

InterContinental Hotel The 02 Company: Intercontinental Hotel GroupRooms: 453

M by Montcalm Royal LondonCompany: Montcalm HotelsRooms: 269

Premier Inn: 3 hotels (Premier Inn, Hub by Premier Inn)Company: WhitbreadRooms: 358

Roomzzz London StratfordCompany: Roomzzz aparthotelRooms: 82

Travelodge: 3 hotelsCompany: TravelodgeRooms: 276

Z Hotels: 2 hotelsCompany: Z hotels Rooms: 221

REGIONAL (CIRCA 9,400)

AberdeenDean by Urban VillaCompany: Union Hanover SecuritiesRooms: 182

Holiday Inn- Crowne Plaza Aberdeen Airport ABZ ParkCompany: Dominvs GroupRooms: 358

BathThe Gainsborough, Bath SPA Company: YTL HotelsRooms: 99

BrentfordPremier Inn Brentford (opened February 2015)Company: WhitbreadRooms: 124

BirminghamIbis Styles Birmingham NECCompany: AccorRooms: 166

ChesterRoomzzz Aparthotel, Chester CityCompany: RoomzzzRooms: 63

EdinburghMercure Edinburgh QuayCompany: AccorRooms: 110

Premier Inn and Hub by Premier Inn (2 hotels)Company: WhitbreadRooms: 294

ExeterPremier Inn ExeterCompany: WhitbreadRooms: 120

GlasgowApex GlasgowCompany: Apex HotelsRooms: 100

Ibis Style GlasgowCompany: AccorRooms: 101

Travelodge Queen StreetCompany: Scot Sheridan/ TravelodgeRooms: 171

Villa Hotel Pacific QuayCompany: De Vere Village Urban ResortsRooms: 120

HeathrowMercure London Heathrow (opened March)Company: AccorRooms: 184

LiverpoolDoubletree Hilton Company: Sanguine HospitalityRooms: 87

Pullman Kings DockCompany: AccorRooms: 216

Roomzzz Aparthotel Liverpool CityCompany: Roomzzz HotelsRooms: 108

Shankley HotelCompany: Signature Living Rooms: 61

ManchesterGotham Hotel (opened April 2015)Company: Bespoke HotelsRooms: 60

Hotel Football (opened March 2015)Company: Gary Neville- Ryan Giggs/ GG HospitalityRooms: 140

Innside Manchester Company: Melia Hotels InternationalRooms: 208

King Street TownhouseCompany: Eclectic HotelsRooms: 40

Motel One PiccadillyCompany: Motel One hotelsRooms: 330

MiddlesbroughHoliday Inn ExpressCompany: Intercontinental Hotel GroupRooms: 138

NewcastleCrowne Plaza Stephenson QuarterCompany: Intercontinental Hotel GroupRooms: 250

SouthamptonHilton at the Ageas Bowl, SouthamptonCompany: HiltonRooms: 175

Travelodge West Quay (opened March 2015)Company: TravelodgeRooms: 84

Southend on SeaPremier Inn Easter Esplanade (opened March 2015)Company: WhitbreadRooms: 80

Source: BDO Research and Hotelsdata

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 20

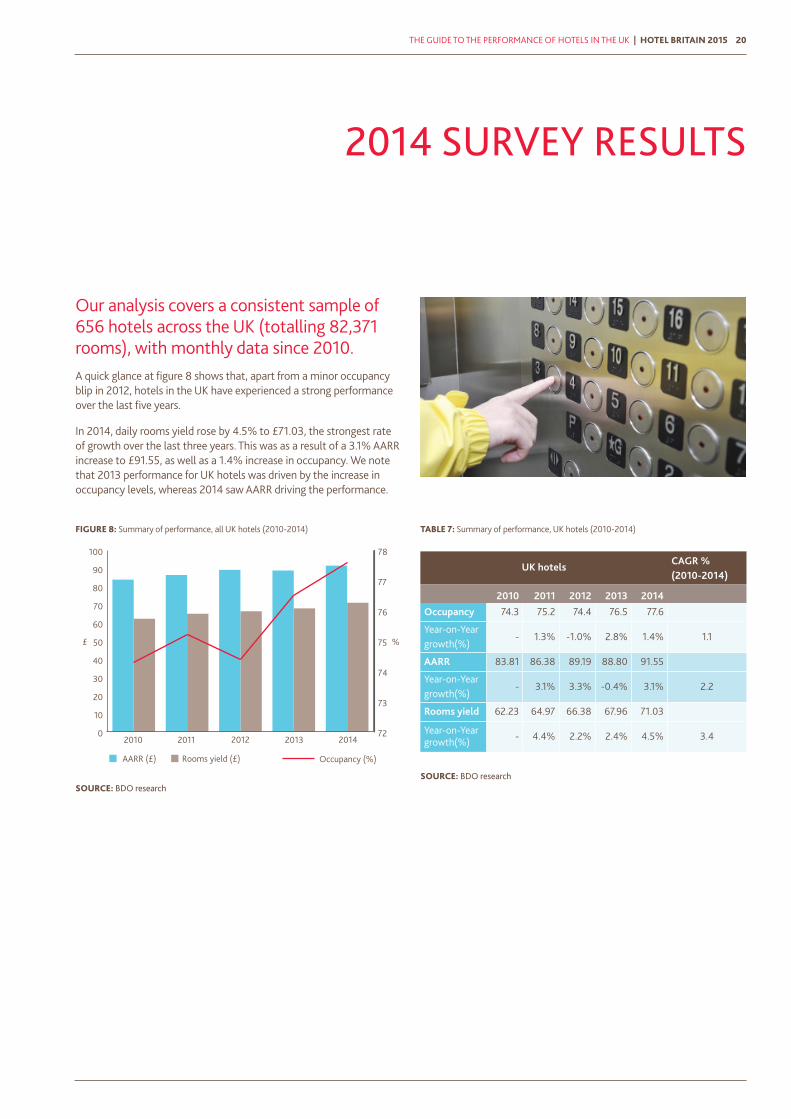

Our analysis covers a consistent sample of 656 hotels across the UK (totalling 82,371 rooms), with monthly data since 2010. A quick glance at figure 8 shows that, apart from a minor occupancy blip in 2012, hotels in the UK have experienced a strong performance over the last five years.

In 2014, daily rooms yield rose by 4.5% to £71.03, the strongest rate of growth over the last three years. This was as a result of a 3.1% AARR increase to £91.55, as well as a 1.4% increase in occupancy. We note that 2013 performance for UK hotels was driven by the increase in occupancy levels, whereas 2014 saw AARR driving the performance.

2014 SURVEY RESULTS

TABLE 7: Summary of performance, UK hotels (2010-2014)

UK hotels CAGR % (2010-2014)

2010 2011 2012 2013 2014

Occupancy 74.3 75.2 74.4 76.5 77.6

Year-on-Year growth(%)

- 1.3% -1.0% 2.8% 1.4% 1.1

AARR 83.81 86.38 89.19 88.80 91.55

Year-on-Year growth(%)

- 3.1% 3.3% -0.4% 3.1% 2.2

Rooms yield 62.23 64.97 66.38 67.96 71.03

Year-on-Year growth(%) - 4.4% 2.2% 2.4% 4.5% 3.4

SOURCE: BDO research

0

10

20

30

40

50

60

70

80

90

100

2010 2011 2012 2013 2014

£ %

AARR (£) Rooms yield (£) Occupancy (%)

72

73

74

75

76

77

78

FIGURE 8: Summary of performance, all UK hotels (2010-2014)

SOURCE: BDO research

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK21

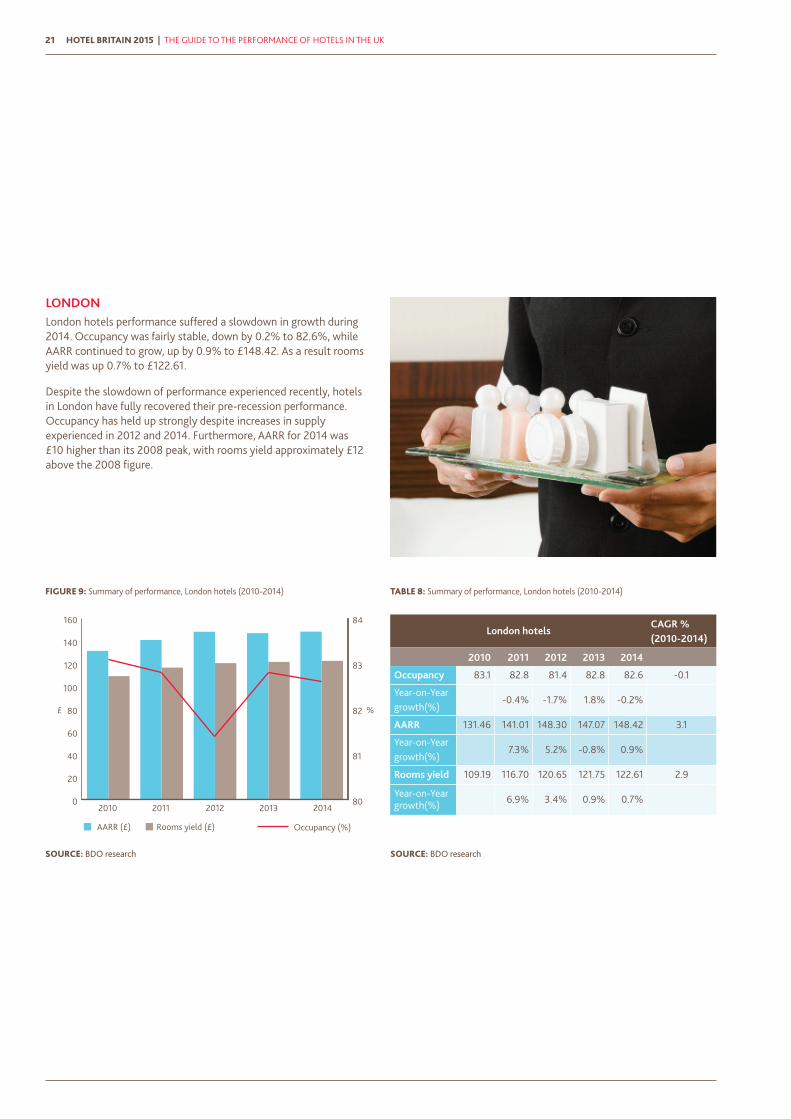

LONDON London hotels performance suffered a slowdown in growth during 2014. Occupancy was fairly stable, down by 0.2% to 82.6%, while AARR continued to grow, up by 0.9% to £148.42. As a result rooms yield was up 0.7% to £122.61.

Despite the slowdown of performance experienced recently, hotels in London have fully recovered their pre-recession performance. Occupancy has held up strongly despite increases in supply experienced in 2012 and 2014. Furthermore, AARR for 2014 was £10 higher than its 2008 peak, with rooms yield approximately £12 above the 2008 figure.

TABLE 8: Summary of performance, London hotels (2010-2014)

London hotelsCAGR % (2010-2014)

2010 2011 2012 2013 2014

Occupancy 83.1 82.8 81.4 82.8 82.6 -0.1

Year-on-Year growth(%)

-0.4% -1.7% 1.8% -0.2%

AARR 131.46 141.01 148.30 147.07 148.42 3.1

Year-on-Year growth(%)

7.3% 5.2% -0.8% 0.9%

Rooms yield 109.19 116.70 120.65 121.75 122.61 2.9

Year-on-Year growth(%) 6.9% 3.4% 0.9% 0.7%

SOURCE: BDO research

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014

£ %

AARR (£) Rooms yield (£) Occupancy (%)

80

81

82

83

84

FIGURE 9: Summary of performance, London hotels (2010-2014)

SOURCE: BDO research

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 22

REGIONAL UK 2014 was a strong year for regional hotels, which experienced more robust results than their London counterparts. Occupancy was up by 2.3% to 75.1%. This is the first time that regional hotels experienced occupancy levels above the 75% since the compilation of our Hotel Britain statistics began in 2004.

However, AARR was the main driver behind this successful growth. Hotels in the regions posted a 7.7% increase in average room rate, up to £60.71. However we note that this is still about £15 below the rate achieved in 2008.

As a result of the increases in occupancy and AARR, regional UK hotel rooms yield grew by 10.2% to £45.60 in 2014. Regional hotels have experienced the fourth consecutive year of rooms yield increase, with strong rates of growth experienced in 2013 and 2014. We note that thanks to the increases in occupancy, rooms yield is only about £10 below its 2008 peak figure.

TABLE 9: Summary of performance, regional hotels (2010-2014)

Regional hotelsCAGR % (2010-2014)

2010 2011 2012 2013 2014

Occupancy 69.9 71.5 71.0 73.4 75.1 1.8

Year-on-Year growth(%)

- 2.3% -0.7% 3.4% 2.3%

AARR 55.93 55.29 55.80 56.35 60.71 2.1

Year-on-Year growth(%)

- -1.2% 0.9% 1.0% 7.7%

Rooms yield 39.11 39.54 39.62 41.39 45.60 3.9

Year-on-Year growth(%) - 1.1% 0.2% 4.5% 10.2%

SOURCE: BDO research

0

10

20

30

40

50

60

70

2010 2011 2012 2013 2014

£ %

AARR (£) Rooms yield (£) Occupancy (%)

67

68

69

70

71

72

73

74

75

76

FIGURE 10: Summary of performance, regional hotels (2010-2014)

SOURCE: BDO research

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK23

FOCUS ON: THE BUDGET SEGMENT2014 saw the budget end of the market outperforming the other segments both in London and regional UK. One of the main reasons for this is the diversification of the budget offering with the development of new budget concepts such as Citizen M, hub by Premier Inn, Tune and the Qbic hotels among others. Furthermore, the two biggest budget hotel brands in the UK, namely Premier Inn and Travelodge, rolled out a major modernisation of their UK properties recently. Customers have changed and they are willing to sacrifice space for central locations, especially in the capital, while in the regions consumers still remain budget-conscious and seek out value for money deals.

In London, tourist hotels saw a year-on-year rooms yield increase of 9.9% in 2014, beating every other segment. This was driven by hoteliers being able to raise the average room rate as demand for the segment remained strong. We note that the top end of the market suffered a decline in rooms yield in 2014. This was mainly as a result of the increase in supply which introduced new competition.

CAGR ANALYSISFigure 11 analyses the compound of annual growth rate (CAGR) for occupancy, AARR and rooms yield for hotels in London and regional UK from 2010 to 2014.

As we can see from the graph, London hotels have experienced a flat occupancy over the last five years. However, this is despite the increase in supply experienced during the run-up to the Olympics in 2012, as well as increases in supply at the top end of the market experienced in 2014. In the capital, AARR continued to be the main driver behind hotel growth, as its five year rate of growth was 2.9%.

It is interesting to note that regional hotels experienced a higher occupancy CAGR rate over the same period, which grew by 1.8%. This was the result of record numbers of inbound visits in 2013 and 2014, as well as improved economic conditions. AARR also continued to grow on the back of strong demand. As a consequence, the compound of annual growth rate of rooms yield for regional hotels grew at a faster rate than that seen in London. This is the first time since the 2001-2005 period, emphasising the exceptional year experienced by regional hotels.

-1

0

1

2

3

4

5

Occupancy AARR Rooms Yield

CAG

R %

cha

nge

London Regional UK hotels

FIGURE 11: CAGR Analysis for UK hotels 2010-2014

SOURCE: BDO research

-6% -4% -2% 0% 2% 4% 6% 8% 10% 12%

2014 2013 2012 2011

Deluxe

Superior deluxe

International deluxe

First class

Business class

Tourist

Townhouse/boutique

FIGURE 12: Rooms yield growth, London hotels

SOURCE: BDO research

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 24

TABLE 11: Rooms yield growth regional hotels

Rooms yield growth regional hotels

Segment (AARR) 2011 2012 2013 2014

Country House 2.5% -0.8% 2.4% 3.5%

>£80 4.7% 2.1% 6.0% 5.5%

£70-£80 0.8% 0.2% 4.0% 8.4%

£60-£70 1.3% 1.4% 3.8% 9.2%

£50-60 0.1% 2.2% 2.8% 10.7%

<£50 -1.6% -4.1% 5.0% 17.9%

SOURCE: BDO research

TABLE 10: Rooms yield growth London hotels

Rooms yield growth London hotels

Segment (AARR) 2011 2012 2013 2014

Deluxe (>£150) 6.3% 4.5% 0.1% -1.8%

Superior deluxe (>£200) 5.1% 5.9% 0.1% -3.3%

International deluxe (£150-200) 8.3% 1.7% 0.4% 1.4%

First class (£100-150) 8.5% 3.2% 1.9% 2.8%

Business class (£75-100) 7.3% 1.1% 3.5% 4.1%

Tourist (<£75) 2.2% -4.7% 1.7% 9.9%

Townhouse/boutique (>£100) 4.4% 3.0% 2.0% -0.5%

SOURCE: BDO research

Hotels in the regions witnessed a similar pattern. In 2014, the top end of the market continued to post growth, although it was the slowest growing segment for rooms yield. Over £80 hotels’ rooms yield was up by 5.5%, well below the 17.9% increase experienced by the Under £50 hotels.

It is interesting to note that in the regions, AARR was the main driver for growth, as demand remained strong for all segments analysed.

-5% 0% 5% 10% 15% 20%

2014 2013 2012 2011

Country House

>£80

£70-£80

£80-£70

£50-60

<£50

FIGURE 13: Rooms yield growth, regional UK hotels

SOURCE: BDO research

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 26

Despite the global economic uncertainty over the last few years, hotels in the UK have proved their resilience and have experienced a blossoming year in 2014. Overall rooms yield grew by 10.2%, driven by the 7.7% increase in AARR. When compared to the previous year, Northern Ireland hotels saw a rooms yield growth of 8.4% in 2014, thanks to a buoyant hotel market. Over the last two years, operating performance for hotels in the area has improved, leading to a surge in hotel investment. Northern Ireland saw a CAGR rooms yield growth at 7.7% rate: the strongest rate of growth amongst all regions analysed over the last two years.

Wales hotels’ rooms yield also grew strongly in 2014, up 11.6%, driven by the increase in AARR (up 8.2%). This was the result of an increase in domestic day visits to the country (up 2% to 84m for the January to November 2014 period) as tourism demand for the area remained strong.

In 2014, Scotland’s hotel occupancy was affected by the uncertainty resulting from the Scottish referendum, and was virtually flat on the previous year. However, hotels were able to increase AARR considerably, resulting in rooms yield being up 10.9% to £56.44. Despite Scotland’s economy starting the year strongly, the recent drop in oil prices is likely to affect average room rate for hotels in the

WINNERS AND LOSERS

country. Overall, prospects for the medium term are positive, as the Barclays Tourist Dynamics Report predicts visitors to the country will increase by 40% by 2017.

English hoteliers also saw a strong rate of rooms yield growth (up 10%) driven by a healthy mix of occupancy and AARR increases.

2014 proved to be an exceptional year for regional UK destinations, with only three out of 41 locations experiencing negative rooms yield growth. Furthermore there were 16 destinations that saw double digit rooms yield growth during the same period.

Unsurprisingly, Glasgow hotels topped the list for rooms yield growth, up a whopping 23.4%. This was attributed to the city hosting the 2014 Commonwealth Games which pushed AARR up by 67% during the month of July.

Leeds hotels also enjoyed strong rooms yield growth, up 16.7% due to the high increases in AARR. Hotels in the city benefitted from the Tour de France in the summer and also with a buoyant corporate season in June and November.

Sheffield’s hotel performance was boosted by the budget segment, which helped to push its hotels’ average room rate up by 16.5%, resulting in rooms yield growing by 16.1%. The famous Sheffield Doc/Fest was extended to a six day event in 2014, with Marketing Sheffield also claiming that its Conference Ambassador Programme generated £13.5m revenue from the corporate sector last year.

Other robust rooms yield achievers were Swindon (up 15.9% to £39.95), thanks to increased occupancy levels (up 10.9%) with resurgent corporate and conference demand; and Norwich where increases in both occupancy and AARR led to rooms yield growing by 15.9% to £40.53.

Gatwick Airport reported one of the busiest ever years in 2014, with over 38m passengers, up 7.6% from the previous year. However, hotels experienced a 6.9% decline in rooms yield over the same period. Occupancy held stable, but the increase in supply led to a -8.4% decrease in average room rate as hotels competed for market share.

Nottingham’s story was more unstable. Having posted a positive performance in 2013, rooms yield declined by -3.4% in 2014. The relatively modest increase in AARR (2.7%) affected a fragile market and drove occupancy down (-5.9%) in overall terms. However, we note that some hotels in the city have outperformed the market, posting strong growth.

Solihull hotels saw a decline in rooms yield in 2014 (-2%). While occupancy remained positive, AARR was the main reason behind this decline (-4.6%).

0% 2% 4% 6% 8% 10% 12% 14%

CAGR 10-14 % ch. 13/14

Northern Ireland

Wales

Scotland

England

Regional UK 3.9%

10.2%

3.6%

10.0%

6.0%

10.9%

3.1%

11.6%

7.7%

8.4%

FIGURE 14: Rooms yield growth by country

SOURCE: BDO research

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK27

-8% -3% 2% 7% 12% 17% 22% 27%

Gatwick

Nottingham

Solihull

Oxford

Windsor/Maidenhead

Aberdeen

Inverness

Heathrow

Edinburgh

Portsmouth

Reading

Chester

Leicester

Manchester

Newcastle

Belfast

Bournemouth

Liverpool

Brighton

Birmingham

Cambridge

Cardiff

Maidstone

Bradford

Northampton

Stratford-upon-Avon

Derby

Gloucester

Milton Keynes

Southampton

Ashford

Bristol

York

Bath

Cheltenham

Coventry

Norwich

Swindon

Sheffield

Leeds

Glasgow

% ch. 13/14 CAGR 10-14

FIGURE 15: Rooms yield growth, regional UK cities

SOURCE: BDO research

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 28

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK29

2014 Occupancy (%) % ch. CAGR AARR (£) % ch. CAGR Rooms yield (£) % ch. CAGR

No. of hotels No. of rooms 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%)

All UK 656 82,371 74.3 75.2 74.4 76.5 77.6 1.4% 1.1% 83.81 86.38 89.19 88.80 91.55 3.1% 2.2% 62.23 64.97 66.38 67.96 71.03 4.5% 3.4%

All London hotels 147 27,731 83.1 82.8 81.4 82.8 82.6 -0.2% -0.1% 131.46 141.01 148.30 147.07 148.42 0.9% 3.1% 109.19 116.70 120.65 121.75 122.61 0.7% 2.9%

Deluxe (>£150) 54 9,310 81.2 80.9 81.1 82.1 81.2 -1.1% 0.0% 219.82 234.85 244.89 242.05 240.24 -0.7% 2.2% 178.60 189.90 198.52 198.81 195.16 -1.8% 2.2%

Superior deluxe (>£200) 32 5,241 81.0 80.1 80.4 81.2 79.8 -1.7% -0.4% 269.61 286.58 302.18 299.55 294.67 -1.6% 2.2% 218.37 229.52 243.03 243.25 235.28 -3.3% 1.9%

International deluxe (£150-£200) 22 4,069 81.6 81.9 81.9 83.3 83.0 -0.4% 0.4% 156.86 169.25 172.13 169.78 172.83 1.8% 2.5% 127.95 138.56 140.96 141.48 143.50 1.4% 2.9%

First class (£100-£150) 33 9,200 83.6 83.2 82.5 83.9 83.9 -0.1% 0.1% 108.95 118.81 123.68 123.86 127.41 2.9% 4.0% 91.11 98.89 102.07 103.96 106.88 2.8% 4.1%

Business class (£75-£100) 15 3,929 86.2 86.4 83.7 84.9 85.7 0.9% -0.2% 76.16 81.52 85.05 86.73 89.50 3.2% 4.1% 65.64 70.40 71.16 73.65 76.66 4.1% 4.0%

Tourist (<£75) 30 4,574 82.9 82.6 77.6 79.9 80.2 0.3% -0.8% 51.04 52.35 53.06 52.41 57.38 9.5% 3.0% 42.32 43.24 41.19 41.89 46.02 9.9% 2.1%

Townhouse/boutique (>£100) 15 718 80.6 80.4 79.3 79.0 80.3 1.7% -0.1% 258.27 270.36 282.23 289.19 282.97 -2.2% 2.3% 208.12 217.30 223.79 228.34 227.15 -0.5% 2.2%

Regional UK 509 54,640 69.9 71.5 71.0 73.4 75.1 2.3% 1.8% 55.93 55.29 55.80 56.35 60.71 7.7% 2.1% 39.11 39.54 39.62 41.39 45.60 10.2% 3.9%

England 427 45,720 69.4 70.8 70.3 72.8 74.7 2.6% 1.9% 55.18 54.42 54.95 54.95 58.93 7.2% 1.7% 38.29 38.55 38.62 40.01 44.02 10.0% 3.6%

Scotland 55 6,481 73.8 76.3 76.1 77.8 77.9 0.1% 1.4% 60.51 61.17 61.42 65.40 72.43 10.8% 4.6% 44.68 46.68 46.75 50.91 56.44 10.9% 6.0%

Wales 24 1,937 69.2 70.6 68.7 72.0 74.3 3.2% 1.8% 57.68 55.23 55.75 56.06 60.64 8.2% 1.3% 39.92 38.98 38.32 40.36 45.04 11.6% 3.1%

N Ireland 3 502 70.6 74.4 78.9 80.4 80.6 0.2% 3.4% 54.96 52.87 55.41 59.85 64.74 8.2% 4.2% 38.80 39.33 43.71 48.11 52.16 8.4% 7.7%

>£80 52 7,559 73.5 75.0 74.9 76.4 77.5 1.4% 1.3% 82.29 84.42 86.24 89.71 93.34 4.1% 3.2% 60.47 63.31 64.63 68.54 72.31 5.5% 4.6%

£70-£80 59 9,858 72.3 72.2 72.5 73.8 75.7 2.7% 1.2% 68.46 69.17 68.98 70.49 74.42 5.6% 2.1% 49.53 49.91 50.01 51.99 56.37 8.4% 3.3%

£60-£70 73 11,317 70.0 71.2 71.6 73.0 75.3 3.1% 1.8% 60.13 59.90 60.36 61.47 65.12 5.9% 2.0% 42.08 42.63 43.23 44.88 49.01 9.2% 3.9%

£50-60 49 7,030 70.2 70.6 71.2 72.8 74.7 2.6% 1.6% 50.41 50.14 50.90 51.11 55.16 7.9% 2.3% 35.40 35.42 36.21 37.23 41.21 10.7% 3.9%

<£50 276 19,026 67.1 70.3 68.2 72.6 73.9 1.8% 2.5% 37.04 34.78 34.36 33.90 39.25 15.8% 1.5% 24.85 24.46 23.45 24.62 29.02 17.9% 4.0%

Country House 25 2,282 67.0 67.4 67.0 67.8 69.6 2.5% 0.9% 85.03 86.66 86.50 87.48 88.34 1.0% 1.0% 56.96 58.41 57.96 59.34 61.45 3.5% 1.9%

Airport hotels 19 5,073 81.0 80.0 79.3 80.3 81.2 1.1% 0.1% 59.47 61.13 62.00 62.35 64.47 3.4% 2.0% 48.16 48.89 49.18 50.08 52.35 4.5% 2.1%

SUMMARY OF FIVE YEAR PERFORMANCE

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 30

2014 Occupancy (%) % ch. CAGR AARR (£) % ch. CAGR Rooms yield (£) % ch. CAGR

No. of hotels No. of rooms 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%)

All UK 656 82,371 74.3 75.2 74.4 76.5 77.6 1.4% 1.1% 83.81 86.38 89.19 88.80 91.55 3.1% 2.2% 62.23 64.97 66.38 67.96 71.03 4.5% 3.4%

All London hotels 147 27,731 83.1 82.8 81.4 82.8 82.6 -0.2% -0.1% 131.46 141.01 148.30 147.07 148.42 0.9% 3.1% 109.19 116.70 120.65 121.75 122.61 0.7% 2.9%

Deluxe (>£150) 54 9,310 81.2 80.9 81.1 82.1 81.2 -1.1% 0.0% 219.82 234.85 244.89 242.05 240.24 -0.7% 2.2% 178.60 189.90 198.52 198.81 195.16 -1.8% 2.2%

Superior deluxe (>£200) 32 5,241 81.0 80.1 80.4 81.2 79.8 -1.7% -0.4% 269.61 286.58 302.18 299.55 294.67 -1.6% 2.2% 218.37 229.52 243.03 243.25 235.28 -3.3% 1.9%

International deluxe (£150-£200) 22 4,069 81.6 81.9 81.9 83.3 83.0 -0.4% 0.4% 156.86 169.25 172.13 169.78 172.83 1.8% 2.5% 127.95 138.56 140.96 141.48 143.50 1.4% 2.9%

First class (£100-£150) 33 9,200 83.6 83.2 82.5 83.9 83.9 -0.1% 0.1% 108.95 118.81 123.68 123.86 127.41 2.9% 4.0% 91.11 98.89 102.07 103.96 106.88 2.8% 4.1%

Business class (£75-£100) 15 3,929 86.2 86.4 83.7 84.9 85.7 0.9% -0.2% 76.16 81.52 85.05 86.73 89.50 3.2% 4.1% 65.64 70.40 71.16 73.65 76.66 4.1% 4.0%

Tourist (<£75) 30 4,574 82.9 82.6 77.6 79.9 80.2 0.3% -0.8% 51.04 52.35 53.06 52.41 57.38 9.5% 3.0% 42.32 43.24 41.19 41.89 46.02 9.9% 2.1%

Townhouse/boutique (>£100) 15 718 80.6 80.4 79.3 79.0 80.3 1.7% -0.1% 258.27 270.36 282.23 289.19 282.97 -2.2% 2.3% 208.12 217.30 223.79 228.34 227.15 -0.5% 2.2%

Regional UK 509 54,640 69.9 71.5 71.0 73.4 75.1 2.3% 1.8% 55.93 55.29 55.80 56.35 60.71 7.7% 2.1% 39.11 39.54 39.62 41.39 45.60 10.2% 3.9%

England 427 45,720 69.4 70.8 70.3 72.8 74.7 2.6% 1.9% 55.18 54.42 54.95 54.95 58.93 7.2% 1.7% 38.29 38.55 38.62 40.01 44.02 10.0% 3.6%

Scotland 55 6,481 73.8 76.3 76.1 77.8 77.9 0.1% 1.4% 60.51 61.17 61.42 65.40 72.43 10.8% 4.6% 44.68 46.68 46.75 50.91 56.44 10.9% 6.0%

Wales 24 1,937 69.2 70.6 68.7 72.0 74.3 3.2% 1.8% 57.68 55.23 55.75 56.06 60.64 8.2% 1.3% 39.92 38.98 38.32 40.36 45.04 11.6% 3.1%

N Ireland 3 502 70.6 74.4 78.9 80.4 80.6 0.2% 3.4% 54.96 52.87 55.41 59.85 64.74 8.2% 4.2% 38.80 39.33 43.71 48.11 52.16 8.4% 7.7%

>£80 52 7,559 73.5 75.0 74.9 76.4 77.5 1.4% 1.3% 82.29 84.42 86.24 89.71 93.34 4.1% 3.2% 60.47 63.31 64.63 68.54 72.31 5.5% 4.6%

£70-£80 59 9,858 72.3 72.2 72.5 73.8 75.7 2.7% 1.2% 68.46 69.17 68.98 70.49 74.42 5.6% 2.1% 49.53 49.91 50.01 51.99 56.37 8.4% 3.3%

£60-£70 73 11,317 70.0 71.2 71.6 73.0 75.3 3.1% 1.8% 60.13 59.90 60.36 61.47 65.12 5.9% 2.0% 42.08 42.63 43.23 44.88 49.01 9.2% 3.9%

£50-60 49 7,030 70.2 70.6 71.2 72.8 74.7 2.6% 1.6% 50.41 50.14 50.90 51.11 55.16 7.9% 2.3% 35.40 35.42 36.21 37.23 41.21 10.7% 3.9%

<£50 276 19,026 67.1 70.3 68.2 72.6 73.9 1.8% 2.5% 37.04 34.78 34.36 33.90 39.25 15.8% 1.5% 24.85 24.46 23.45 24.62 29.02 17.9% 4.0%

Country House 25 2,282 67.0 67.4 67.0 67.8 69.6 2.5% 0.9% 85.03 86.66 86.50 87.48 88.34 1.0% 1.0% 56.96 58.41 57.96 59.34 61.45 3.5% 1.9%

Airport hotels 19 5,073 81.0 80.0 79.3 80.3 81.2 1.1% 0.1% 59.47 61.13 62.00 62.35 64.47 3.4% 2.0% 48.16 48.89 49.18 50.08 52.35 4.5% 2.1%

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK31

2014 Occupancy (%) % ch. CAGR AARR (£) % ch. CAGR Rooms yield (£) % ch. CAGR

No. of hotels No. of rooms 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%)

Aberdeen 8 989 72.5 75.7 79.3 77.8 76.1 -2.2% 1.2% 69.86 73.50 78.31 93.58 98.48 5.2% 9.0% 50.64 55.68 62.07 72.83 74.93 2.9% 10.3%

Ashford 3 391 67.7 69.5 69.5 71.1 71.8 1.0% 1.5% 46.28 48.65 48.65 49.32 54.13 9.8% 4.0% 31.33 33.81 33.81 35.05 38.87 10.9% 5.5%

Bath 3 238 74.9 76.3 75.8 76.5 79.3 3.8% 1.5% 50.93 49.71 46.88 47.63 51.43 8.0% 0.2% 38.14 37.93 35.53 36.42 40.80 12.0% 1.7%

Belfast 3 502 70.6 74.4 78.9 80.4 80.6 0.2% 3.4% 54.96 52.87 55.41 59.85 64.74 8.2% 4.2% 38.80 39.33 43.71 48.11 52.16 8.4% 7.7%

Birmingham 10 1,453 67.1 65.4 65.0 69.3 70.4 1.7% 1.2% 55.27 52.54 50.41 50.24 53.88 7.3% -0.6% 37.09 34.34 32.77 34.81 37.96 9.0% 0.6%

Bournemouth 3 262 71.6 75.0 73.3 75.3 77.7 3.1% 2.1% 82.77 80.24 81.94 80.93 85.13 5.2% 0.7% 59.23 60.16 60.05 60.97 66.13 8.5% 2.8%

Bradford 3 220 62.9 64.2 64.2 67.5 70.1 3.8% 2.7% 42.55 36.49 36.49 36.63 38.71 5.7% -2.3% 26.77 23.44 23.44 24.72 27.13 9.7% 0.3%

Brighton 4 703 69.2 72.8 73.3 74.0 74.9 1.2% 2.0% 62.15 65.69 66.68 67.19 72.12 7.3% 3.8% 43.01 47.85 48.85 49.75 54.04 8.6% 5.9%

Bristol 8 1,255 73.1 71.2 70.1 74.7 77.0 3.1% 1.3% 63.80 63.85 63.21 63.98 69.37 8.4% 2.1% 46.66 45.49 44.32 47.83 53.44 11.7% 3.4%

Cambridge 4 367 73.6 75.7 75.2 78.4 79.5 1.5% 1.9% 57.95 56.37 57.54 58.41 62.85 7.6% 2.1% 42.67 42.65 43.27 45.78 49.99 9.2% 4.0%

Cardiff 10 1,133 73.0 73.8 72.0 75.2 77.4 2.9% 1.5% 66.77 65.17 66.22 67.01 71.35 6.5% 1.7% 48.74 48.12 47.65 50.43 55.22 9.5% 3.2%

Cheltenham 3 351 71.9 71.0 71.0 72.5 75.4 4.0% 1.2% 53.23 52.72 51.89 53.20 57.98 9.0% 2.2% 38.28 37.42 36.85 38.58 43.73 13.3% 3.4%

Chester 4 402 65.9 67.5 68.9 72.3 74.4 2.8% 3.1% 58.92 56.00 56.90 59.42 61.28 3.1% 1.0% 38.82 37.78 39.23 42.99 45.59 6.0% 4.1%

Coventry 5 392 66.3 67.5 66.4 70.2 71.8 2.3% 2.0% 51.83 49.97 50.51 48.82 54.15 10.9% 1.1% 34.37 33.74 33.54 34.29 38.90 13.4% 3.1%

Derby 4 444 62.3 66.5 71.6 71.2 72.2 1.3% 3.7% 54.79 51.80 54.58 53.10 57.71 8.7% 1.3% 34.16 34.47 39.06 37.83 41.66 10.1% 5.1%

Edinburgh 15 1,985 75.4 79.3 77.3 79.5 78.3 -1.5% 1.0% 68.22 70.89 71.00 76.11 80.62 5.9% 4.3% 51.45 56.20 54.91 60.50 63.15 4.4% 5.3%

Gatwick 4 846 80.0 79.3 81.6 79.0 80.3 1.6% 0.1% 73.14 74.11 75.48 78.59 71.99 -8.4% -0.4% 58.52 58.79 61.56 62.11 57.82 -6.9% -0.3%

Glasgow 11 2,155 77.4 77.7 77.2 79.2 81.5 3.0% 1.3% 57.80 57.01 55.97 56.01 67.12 19.8% 3.8% 44.76 44.28 43.22 44.35 54.72 23.4% 5.2%

Gloucester 3 326 70.9 70.5 70.5 75.8 74.9 -1.2% 1.4% 51.95 48.85 48.85 49.26 55.01 11.7% 1.4% 36.83 34.43 34.43 37.32 41.20 10.4% 2.8%

Heathrow 13 3,953 81.3 79.5 77.8 78.8 80.3 1.9% -0.3% 59.67 61.57 62.54 61.82 62.95 1.8% 1.3% 48.52 48.95 48.66 48.72 50.55 3.8% 1.0%

Inverness 3 256 70.0 71.6 71.6 73.2 69.7 -4.8% -0.1% 48.24 45.68 45.68 47.97 51.99 8.4% 1.9% 33.76 32.71 32.71 35.10 36.22 3.2% 1.8%

Leeds 10 1,433 71.1 72.1 72.3 77.1 77.8 1.0% 2.3% 54.02 52.21 53.21 55.45 64.11 15.6% 4.4% 38.40 37.66 38.50 42.73 49.87 16.7% 6.8%

Leicester 4 568 64.9 64.7 62.3 70.3 71.0 1.0% 2.3% 56.63 56.24 55.84 55.24 58.57 6.0% 0.8% 36.73 36.40 34.81 38.86 41.60 7.1% 3.2%

Liverpool 9 1,351 70.8 70.4 67.2 68.3 71.8 5.1% 0.3% 61.03 60.28 59.30 64.15 66.18 3.2% 2.0% 43.21 42.44 39.84 43.81 47.51 8.5% 2.4%

Luton 3 640 62.4 69.2 68.5 71.0 69.9 -1.5% 2.9% 61.30 60.43 59.11 54.59 52.18 -4.4% -3.9% 38.27 41.79 40.49 38.76 36.50 -5.8% -1.2%

Maidstone 4 389 67.3 69.9 72.1 73.2 75.6 3.3% 3.0% 56.90 55.72 55.49 55.78 59.10 5.9% 1.0% 38.29 38.94 40.02 40.82 44.68 9.5% 3.9%

Manchester 15 2,304 71.2 73.6 73.3 75.2 77.6 3.2% 2.2% 59.21 59.60 59.85 62.39 65.24 4.6% 2.5% 42.13 43.87 43.89 46.93 50.64 7.9% 4.7%

Milton Keynes 3 501 72.3 74.6 74.3 76.2 76.0 -0.3% 1.2% 58.20 61.63 62.98 65.89 72.96 10.7% 5.8% 42.10 45.97 46.79 50.20 55.44 10.4% 7.1%

Newcastle 8 1,129 73.9 74.6 72.0 72.4 75.8 4.8% 0.7% 57.27 56.11 54.77 52.89 54.52 3.1% -1.2% 42.29 41.87 39.46 38.28 41.34 8.0% -0.6%

Northampton 3 285 67.4 65.9 69.2 70.4 73.9 5.0% 2.3% 57.20 58.24 56.85 56.64 59.26 4.6% 0.9% 38.57 38.38 39.35 39.89 43.81 9.8% 3.2%

Norwich 5 458 67.4 70.2 68.3 73.8 77.0 4.4% 3.4% 49.23 48.08 48.59 47.38 52.63 11.1% 1.7% 33.20 33.76 33.20 34.96 40.53 15.9% 5.1%

Nottingham 11 1,298 62.9 66.0 65.8 69.9 65.8 -5.9% 1.1% 52.38 51.62 52.41 51.03 52.41 2.7% 0.0% 32.95 34.05 34.49 35.68 34.49 -3.4% 1.1%

Oxford 4 538 73.4 73.8 74.4 81.2 78.9 -2.8% 1.8% 54.85 57.10 57.16 59.08 62.13 5.2% 3.2% 40.25 42.13 42.51 47.98 49.03 2.2% 5.1%

Portsmouth 4 576 79.1 79.0 77.3 81.9 81.1 -1.0% 0.6% 69.15 67.98 70.96 72.09 76.24 5.8% 2.5% 54.72 53.71 54.85 59.02 61.81 4.7% 3.1%

Reading 9 982 61.3 65.7 67.0 70.4 68.8 -2.3% 2.9% 49.36 50.20 53.11 54.77 59.15 8.0% 4.6% 30.28 33.00 35.59 38.57 40.71 5.5% 7.7%

Sheffield 3 424 60.7 66.4 62.8 70.8 70.5 -0.4% 3.8% 38.68 37.21 38.46 37.67 43.90 16.5% 3.2% 23.49 24.72 24.16 26.65 30.94 16.1% 7.1%

Solihull 4 754 65.7 63.5 63.8 65.9 67.7 2.7% 0.7% 79.36 76.79 76.95 78.13 74.52 -4.6% -1.6% 52.17 48.80 49.12 51.47 50.44 -2.0% -0.8%

Southampton 4 507 71.4 74.9 75.8 78.5 81.6 3.9% 3.4% 54.50 49.70 51.41 52.13 55.43 6.3% 0.4% 38.92 37.23 38.95 40.93 45.22 10.5% 3.8%

Stratford-upon-Avon 4 512 67.8 69.9 67.8 68.8 70.4 2.3% 0.9% 69.51 68.55 68.63 69.25 74.46 7.5% 1.7% 47.14 47.91 46.52 47.65 52.44 10.0% 2.7%

Swindon 5 702 61.3 64.2 63.5 66.9 74.2 10.9% 4.9% 51.06 52.35 55.77 51.54 53.86 4.5% 1.3% 31.30 33.63 35.43 34.46 39.95 15.9% 6.3%

Windsor/Maidenhead 3 425 70.8 71.9 74.7 73.7 72.5 -1.7% 0.6% 72.14 74.91 76.97 79.45 82.82 4.2% 3.5% 51.07 53.86 57.51 58.59 60.01 2.4% 4.1%

York 5 542 77.3 78.7 78.7 78.9 82.0 3.9% 1.5% 58.90 59.14 59.14 58.33 62.77 7.6% 1.6% 45.51 46.57 46.57 46.04 51.49 11.8% 3.1%

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 32

2014 Occupancy (%) % ch. CAGR AARR (£) % ch. CAGR Rooms yield (£) % ch. CAGR

No. of hotels No. of rooms 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%) 2010 2011 2012 2013 2014 % ch 13/14 CAGR (%)

Aberdeen 8 989 72.5 75.7 79.3 77.8 76.1 -2.2% 1.2% 69.86 73.50 78.31 93.58 98.48 5.2% 9.0% 50.64 55.68 62.07 72.83 74.93 2.9% 10.3%

Ashford 3 391 67.7 69.5 69.5 71.1 71.8 1.0% 1.5% 46.28 48.65 48.65 49.32 54.13 9.8% 4.0% 31.33 33.81 33.81 35.05 38.87 10.9% 5.5%

Bath 3 238 74.9 76.3 75.8 76.5 79.3 3.8% 1.5% 50.93 49.71 46.88 47.63 51.43 8.0% 0.2% 38.14 37.93 35.53 36.42 40.80 12.0% 1.7%

Belfast 3 502 70.6 74.4 78.9 80.4 80.6 0.2% 3.4% 54.96 52.87 55.41 59.85 64.74 8.2% 4.2% 38.80 39.33 43.71 48.11 52.16 8.4% 7.7%

Birmingham 10 1,453 67.1 65.4 65.0 69.3 70.4 1.7% 1.2% 55.27 52.54 50.41 50.24 53.88 7.3% -0.6% 37.09 34.34 32.77 34.81 37.96 9.0% 0.6%

Bournemouth 3 262 71.6 75.0 73.3 75.3 77.7 3.1% 2.1% 82.77 80.24 81.94 80.93 85.13 5.2% 0.7% 59.23 60.16 60.05 60.97 66.13 8.5% 2.8%

Bradford 3 220 62.9 64.2 64.2 67.5 70.1 3.8% 2.7% 42.55 36.49 36.49 36.63 38.71 5.7% -2.3% 26.77 23.44 23.44 24.72 27.13 9.7% 0.3%

Brighton 4 703 69.2 72.8 73.3 74.0 74.9 1.2% 2.0% 62.15 65.69 66.68 67.19 72.12 7.3% 3.8% 43.01 47.85 48.85 49.75 54.04 8.6% 5.9%

Bristol 8 1,255 73.1 71.2 70.1 74.7 77.0 3.1% 1.3% 63.80 63.85 63.21 63.98 69.37 8.4% 2.1% 46.66 45.49 44.32 47.83 53.44 11.7% 3.4%

Cambridge 4 367 73.6 75.7 75.2 78.4 79.5 1.5% 1.9% 57.95 56.37 57.54 58.41 62.85 7.6% 2.1% 42.67 42.65 43.27 45.78 49.99 9.2% 4.0%

Cardiff 10 1,133 73.0 73.8 72.0 75.2 77.4 2.9% 1.5% 66.77 65.17 66.22 67.01 71.35 6.5% 1.7% 48.74 48.12 47.65 50.43 55.22 9.5% 3.2%

Cheltenham 3 351 71.9 71.0 71.0 72.5 75.4 4.0% 1.2% 53.23 52.72 51.89 53.20 57.98 9.0% 2.2% 38.28 37.42 36.85 38.58 43.73 13.3% 3.4%

Chester 4 402 65.9 67.5 68.9 72.3 74.4 2.8% 3.1% 58.92 56.00 56.90 59.42 61.28 3.1% 1.0% 38.82 37.78 39.23 42.99 45.59 6.0% 4.1%

Coventry 5 392 66.3 67.5 66.4 70.2 71.8 2.3% 2.0% 51.83 49.97 50.51 48.82 54.15 10.9% 1.1% 34.37 33.74 33.54 34.29 38.90 13.4% 3.1%

Derby 4 444 62.3 66.5 71.6 71.2 72.2 1.3% 3.7% 54.79 51.80 54.58 53.10 57.71 8.7% 1.3% 34.16 34.47 39.06 37.83 41.66 10.1% 5.1%

Edinburgh 15 1,985 75.4 79.3 77.3 79.5 78.3 -1.5% 1.0% 68.22 70.89 71.00 76.11 80.62 5.9% 4.3% 51.45 56.20 54.91 60.50 63.15 4.4% 5.3%

Gatwick 4 846 80.0 79.3 81.6 79.0 80.3 1.6% 0.1% 73.14 74.11 75.48 78.59 71.99 -8.4% -0.4% 58.52 58.79 61.56 62.11 57.82 -6.9% -0.3%

Glasgow 11 2,155 77.4 77.7 77.2 79.2 81.5 3.0% 1.3% 57.80 57.01 55.97 56.01 67.12 19.8% 3.8% 44.76 44.28 43.22 44.35 54.72 23.4% 5.2%

Gloucester 3 326 70.9 70.5 70.5 75.8 74.9 -1.2% 1.4% 51.95 48.85 48.85 49.26 55.01 11.7% 1.4% 36.83 34.43 34.43 37.32 41.20 10.4% 2.8%

Heathrow 13 3,953 81.3 79.5 77.8 78.8 80.3 1.9% -0.3% 59.67 61.57 62.54 61.82 62.95 1.8% 1.3% 48.52 48.95 48.66 48.72 50.55 3.8% 1.0%

Inverness 3 256 70.0 71.6 71.6 73.2 69.7 -4.8% -0.1% 48.24 45.68 45.68 47.97 51.99 8.4% 1.9% 33.76 32.71 32.71 35.10 36.22 3.2% 1.8%

Leeds 10 1,433 71.1 72.1 72.3 77.1 77.8 1.0% 2.3% 54.02 52.21 53.21 55.45 64.11 15.6% 4.4% 38.40 37.66 38.50 42.73 49.87 16.7% 6.8%

Leicester 4 568 64.9 64.7 62.3 70.3 71.0 1.0% 2.3% 56.63 56.24 55.84 55.24 58.57 6.0% 0.8% 36.73 36.40 34.81 38.86 41.60 7.1% 3.2%

Liverpool 9 1,351 70.8 70.4 67.2 68.3 71.8 5.1% 0.3% 61.03 60.28 59.30 64.15 66.18 3.2% 2.0% 43.21 42.44 39.84 43.81 47.51 8.5% 2.4%

Luton 3 640 62.4 69.2 68.5 71.0 69.9 -1.5% 2.9% 61.30 60.43 59.11 54.59 52.18 -4.4% -3.9% 38.27 41.79 40.49 38.76 36.50 -5.8% -1.2%

Maidstone 4 389 67.3 69.9 72.1 73.2 75.6 3.3% 3.0% 56.90 55.72 55.49 55.78 59.10 5.9% 1.0% 38.29 38.94 40.02 40.82 44.68 9.5% 3.9%

Manchester 15 2,304 71.2 73.6 73.3 75.2 77.6 3.2% 2.2% 59.21 59.60 59.85 62.39 65.24 4.6% 2.5% 42.13 43.87 43.89 46.93 50.64 7.9% 4.7%

Milton Keynes 3 501 72.3 74.6 74.3 76.2 76.0 -0.3% 1.2% 58.20 61.63 62.98 65.89 72.96 10.7% 5.8% 42.10 45.97 46.79 50.20 55.44 10.4% 7.1%

Newcastle 8 1,129 73.9 74.6 72.0 72.4 75.8 4.8% 0.7% 57.27 56.11 54.77 52.89 54.52 3.1% -1.2% 42.29 41.87 39.46 38.28 41.34 8.0% -0.6%

Northampton 3 285 67.4 65.9 69.2 70.4 73.9 5.0% 2.3% 57.20 58.24 56.85 56.64 59.26 4.6% 0.9% 38.57 38.38 39.35 39.89 43.81 9.8% 3.2%

Norwich 5 458 67.4 70.2 68.3 73.8 77.0 4.4% 3.4% 49.23 48.08 48.59 47.38 52.63 11.1% 1.7% 33.20 33.76 33.20 34.96 40.53 15.9% 5.1%

Nottingham 11 1,298 62.9 66.0 65.8 69.9 65.8 -5.9% 1.1% 52.38 51.62 52.41 51.03 52.41 2.7% 0.0% 32.95 34.05 34.49 35.68 34.49 -3.4% 1.1%

Oxford 4 538 73.4 73.8 74.4 81.2 78.9 -2.8% 1.8% 54.85 57.10 57.16 59.08 62.13 5.2% 3.2% 40.25 42.13 42.51 47.98 49.03 2.2% 5.1%

Portsmouth 4 576 79.1 79.0 77.3 81.9 81.1 -1.0% 0.6% 69.15 67.98 70.96 72.09 76.24 5.8% 2.5% 54.72 53.71 54.85 59.02 61.81 4.7% 3.1%

Reading 9 982 61.3 65.7 67.0 70.4 68.8 -2.3% 2.9% 49.36 50.20 53.11 54.77 59.15 8.0% 4.6% 30.28 33.00 35.59 38.57 40.71 5.5% 7.7%

Sheffield 3 424 60.7 66.4 62.8 70.8 70.5 -0.4% 3.8% 38.68 37.21 38.46 37.67 43.90 16.5% 3.2% 23.49 24.72 24.16 26.65 30.94 16.1% 7.1%

Solihull 4 754 65.7 63.5 63.8 65.9 67.7 2.7% 0.7% 79.36 76.79 76.95 78.13 74.52 -4.6% -1.6% 52.17 48.80 49.12 51.47 50.44 -2.0% -0.8%

Southampton 4 507 71.4 74.9 75.8 78.5 81.6 3.9% 3.4% 54.50 49.70 51.41 52.13 55.43 6.3% 0.4% 38.92 37.23 38.95 40.93 45.22 10.5% 3.8%

Stratford-upon-Avon 4 512 67.8 69.9 67.8 68.8 70.4 2.3% 0.9% 69.51 68.55 68.63 69.25 74.46 7.5% 1.7% 47.14 47.91 46.52 47.65 52.44 10.0% 2.7%

Swindon 5 702 61.3 64.2 63.5 66.9 74.2 10.9% 4.9% 51.06 52.35 55.77 51.54 53.86 4.5% 1.3% 31.30 33.63 35.43 34.46 39.95 15.9% 6.3%

Windsor/Maidenhead 3 425 70.8 71.9 74.7 73.7 72.5 -1.7% 0.6% 72.14 74.91 76.97 79.45 82.82 4.2% 3.5% 51.07 53.86 57.51 58.59 60.01 2.4% 4.1%

York 5 542 77.3 78.7 78.7 78.9 82.0 3.9% 1.5% 58.90 59.14 59.14 58.33 62.77 7.6% 1.6% 45.51 46.57 46.57 46.04 51.49 11.8% 3.1%

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 34

After a strong 2014, the UK economy is forecast to continue to expand throughout 2015, with GDP growth expected to be between 2.5 and 2.7%. However, there are some variables that might reduce the pace of growth. The general election in May is one of the most obvious factors that could pose uncertainties in the short term. While companies remain positive, they are vigilant about possible scenarios that might arise from the election. In addition, the drop in the oil price is expected to continue to drive consumers’ consumption. However, there is a possible risk of short term deflation for the UK, as already experienced by some of its European counterparts. At the time of writing, UK inflation has fallen to essentially zero, a record low level, halting prospects of an imminent interest rate increase by the Bank of England.

Having said that, despite all the uncertainty surrounding future economic performance, the fundamentals of the economy in the UK remain strong, with wages continuing to grow and unemployment falling well below 6%, and the manufacturing sector growing at its fastest rate for over six months in February, according to the CBI.

CONTINUED GROWTH FOR UK HOTELSThe record number of visitors in 2014, coupled with the improved economic outlook, are likely to continue to have a positive affect on hotels across the country, with tourism expected to break the 35m barrier during 2015, assisted by the increase in disposable income.

London

After experiencing a somewhat bumpy 2013 and a difficult start to 2014, hotels in London enjoyed growth for the rest of 2014. The capital still continues to be one of the top global cities for hotel development. 2015 is poised to continue on an upward path, with both occupancy and AARR benefitting from strong demand. Occupancy is at one of the highest levels in the capital, and rates have also continued to grow throughout. We expect this healthy mix of growth to continue in 2015 for hotels in the capital.

Regions

After their record year in 2014, hotels in the regions are still poised to continue to post growth throughout 2015. However, the pace of growth could be affected by the troubles experienced in the Eurozone and the pound- euro exchange rate which could deter inbound visits.

THE ROAD AHEAD

CHANGES IN TOURISM VISITOR PATTERNSRecently there has been a slowdown of visitors from the BRIC economies that is likely to continue for the short to medium term. Apart from the obvious slowdown of incoming visitor numbers from countries like Russia, the Chinese market has also shown a decline in visitors in 2014. In the People’s Republic of China, GDP growth for 2014 has not matched earlier forecasts. Having said that, Asian companies are still investing and expanding in the UK, with the latest news that Peninsula Hotels have secured a London property, reaffirming the importance of the relationships between the UK and the Far East for both trade and tourism flows.

In addition to the reduced number of incoming visitors from the BRIC economies, the recent rise in the value of the pound, at a seven year historic high against the euro, is likely to affect the number of visitors from the continent, assuming that this trend is likely to continue during the current year.

However, Britons are expected to take more holidays in 2015 as a result of the recent decline in oil prices, lower inflation and increased household income. This should definitely boost domestic tourism and expenditure, as consumers remain confident, but, coupled with the exchange rate, could also result in increased outbound tourism to the continent as holidays may become cheaper.

RUGBY WORLD CUPHotels in the UK will be exposed globally when the Rugby World Cup takes place in the autumn. Apart from the obvious benefits of improvements for both occupancy and AARR, the country will have the opportunity to repeat its global showcase as experienced during the Olympic Games in 2012. This is likely to result in renewed interest in the UK and in turn to increased inbound visits. Hotels in the country traditionally have benefited from sporting events such as the Olympics, the Commonwealth Games, and indeed the Rugby World Cup.

CONTINUED TRANSACTION ACTIVITY2015 is poised to continue the trend for hotel transactions both in London and in the regions. As mentioned earlier, lenders are opening up to the improved economic conditions and are prepared to pay premium prices for the right property.

HOTEL BRITAIN 2015 | THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK35

The prize includes a one night stay for two at the Conrad London St James including breakfast and dinner. Subject to availability, valid until November 2016.

WIN A ONE NIGHT STAY FOR TWO AT THE CONRAD LONDON ST JAMES HOTEL, COURTESY OF THE SPLENDID HOSPITALITY GROUP

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 36

ABOUT THE GROUP AND THE HOTELControlled and directed by Shiraz and Nadeem Boghani, Splendid Hospitality Group is one of the UK’s fastest growing privately-owned hotel groups which has made a name for itself through the design, construction and operation of a full range of hotel styles and locations.

The group owns 15 properties across the UK, both franchised and unbranded. Splendid Hospitality Group are proud to be developing hotels in some of the UK’s best destinations including the 5 Star Conrad St James, the Grand Hotel and Spa in York, Vanbrugh House Oxford, Indigo Edinburgh, the Holiday Inn Wembley, as well as a the planned Hilton London Bankside and Indigo Hotel in York.

Ideally situated just steps from St James’s Park, Buckingham Palace and the Houses of Parliament, Conrad London St James offers a smart choice for the modern traveller. Navigate around the city with ease with convenient transport links nearby the hotel.

Encased in a historic 19th Century façade, the chic and contemporary interior of Conrad London St James showcases original art installations and locally inspired design.

HOTEL BRITAIN 2015 COMPETITION

HOW TO ENTERAll you need to do to enter is predict as accurately as you can the occupancy and average achieved room rate (AARR) per occupied room in BDO’s sample of hotels in Britain for the 2015 calendar year. Answers should be submitted in the following format:

1. Occupancy: ....................% (to 1 decimal place)

2. AARR: £..................... (to 2 decimal places)

You can submit your answer at the Hotel Britain Launch Event using the slips provided, or by emailing [email protected], with ‘Hotel Britain Competition Entry’ in the subject line. Entries close on 31 May 2015. Only one entry per person. The winner will be notified by 5 March 2016. The winner will receive a voucher valid for redemption until November 2016.

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 38

CLAIRVOYANT CORNERFROM LAST YEAR’S COMPETITION WINNER

JAKE EGBERTS Asset Manager – Hotels

Topland Group of Companies

When asked about the outlook for the UK hotel market last year during the Hotel Britain event, several influencing factors crossed my mind. These included the UK’s economic recovery, new supply entering the market adding further pressure on under-invested assets, the ongoing sophistication by guests to achieve a competitive rate and the Glasgow Commonwealth Games. London continues to be strong, combined with the continued resurgence in Provincial UK, has influenced the UK hotel market’s performance. I am really pleased that my prediction came within a whisker of the actual performance.

Following Topland’s acquisition in December 2013 of the Menzies Hotel Group, 2014 started with a rush which continued as the year progressed, it was a very exciting year for Topland as we further established ourselves in the UK hotel sector. The subsequent acquisition of Hallmark Hotels in August 2014 was soon followed in quarter four with a period of due diligence and travels around the North East as Topland evaluated The Feather Hotel portfolio. This culminated in the acquisition of Feathers in mid-January 2015. During the thirteen months from December 2013 to January 2015 Topland increased from one owned and operated hotel to twenty-eight hotels in addition to our Royal Crescent Hotel in Bath and nine more hotels leased to Thistle, Hilton and Ramada owned by Topland since 2006. Topland’s internal asset management team works closely with Bespoke who operate the hotels on behalf of Topland. Topland’s combined asset management expertise will continue to focus on driving revenue and exceeding EBITDA expectations across the portfolio to maximise value. Topland has exciting plans to consolidate the three portfolios which will assist in achieving growth through improved revenue strategies and procurement benefits from enhanced scale. Topland is investing capital to enhance its hotel portfolio and constantly seizing new opportunities to further grow the portfolio. We look forward to continued buoyancy in the hotel sector through 2015 and onwards.

THE GUIDE TO THE PERFORMANCE OF HOTELS IN THE UK | HOTEL BRITAIN 2015 40

Hotel Britain is the definitive guide to the performance and prospects of the UK’s hotel industry. It is compiled from the responses of a representative cross section of 656 hotels comprising 82,371 rooms, and including 147 London hotels and 509 around the rest of the country.The results of this survey are grouped for convenience according to geographic location. We breakdown the performance of hotels in key centres across the country, and analyse both London and the regions in terms of average room rate.

Hotels in the capital are divided into four main bands according to the average room rate achieved during 2014. The top rate band, Deluxe, comprises Superior Deluxe and International Deluxe properties. This is followed by First Class and Business properties, with the final category being Tourist hotels. There is also a separate performance breakdown, which extends across all these rate boundaries, for townhouse properties. Regional hotels have been placed in one of five rate bandings, with a separate performance breakdown, which extends across all these rate boundaries, for Country House properties.

To ensure that our year-on-year results are directly comparable, only properties able to contribute data from the last five years have been included. Hotels which have closed for a period of refurbishment or have opened during this period have been excluded.

GLOSSARYDefinitions of some of the terms used in this report are provided below.

• Room occupancy: the ratio of total occupied rooms to total available.