lending assign draft part 1 (2)

DESCRIPTION

Lending Assignment MonashTRANSCRIPT

1.0 Introduction

Asia Poly Holdings Bhd (ASPY) is A-Cast® cast acrylic sheet manufacturer and is among the top

choice for world’s leading brands. The company had applied a loan of RM 7,500,000 with loan tenure of

5 years from the Bank. ASPY intends to expand its production capacity by building a new facility which

would include a new plant, fittings and machineries to cope with the increasing demand of A-Cast ®

sheets.

2.0 Company Profile

2.1 Name of Company

Asia Poly Holdings Berhad

2.2 Date of incorporation

1st January 2003

2.3 Duration of existence

Approximately 14 years

2.4 Objects of the company

The principal activity of company is manufacturing cast acrylic sheet wide range

colours, surfaces and finishes ranging from sanitary ware, fluorescent, silk, glass

look to opals.

The subsidiary of the group involves in research and development to develop new

products and services to keep the company a step ahead within the competitive

market and make it cost effective for the company.

2.5 The business of the company

1

Established on 1993, Asia Poly became the third Cast Acrylic Sheet manufacturer in

Malaysia producing wide range of cast acrylic sheet. Asia Poly’s brand of a-Cast Acrylic

Sheet is manufactured from 100% Virgin Methyl Methacrylate Monomer (MMA). The

cell-casting method used maximizes the chemical resistance and mechanical properties of

the acrylic sheets, making them suitable for indoor and outdoor applications. The

application includes building applications, food industry, domestic applications,

transport, medical applications and miscellaneous applications.

The company headquarters is in Malaysia at Klang, Selangor. After initiating its sales of

A-Cast® in Asia Pacific region, increased production and demand require Asia Poly to

broaden its product internationally. Continuous research and development leads to

improved A-Cast® product assortment capability, improved existing marketing

relationships, and attracting new customers. Despite the fire that destroyed the factory

completely in December 2007, with the help of excellent management and significant

investment in R&D, Asia Poly Industrial quickly re-established itself as premier

manufacturer of cell cast acrylic sheet in Malaysia 2 years later. The rapid growth of

business since 2009, supported by new and old customer bear testament to quality of A-

Cast® product and service shown that Asia Poly always putting customer satisfaction

first by conducting continual improvement in its product quality and production

efficiency.

2

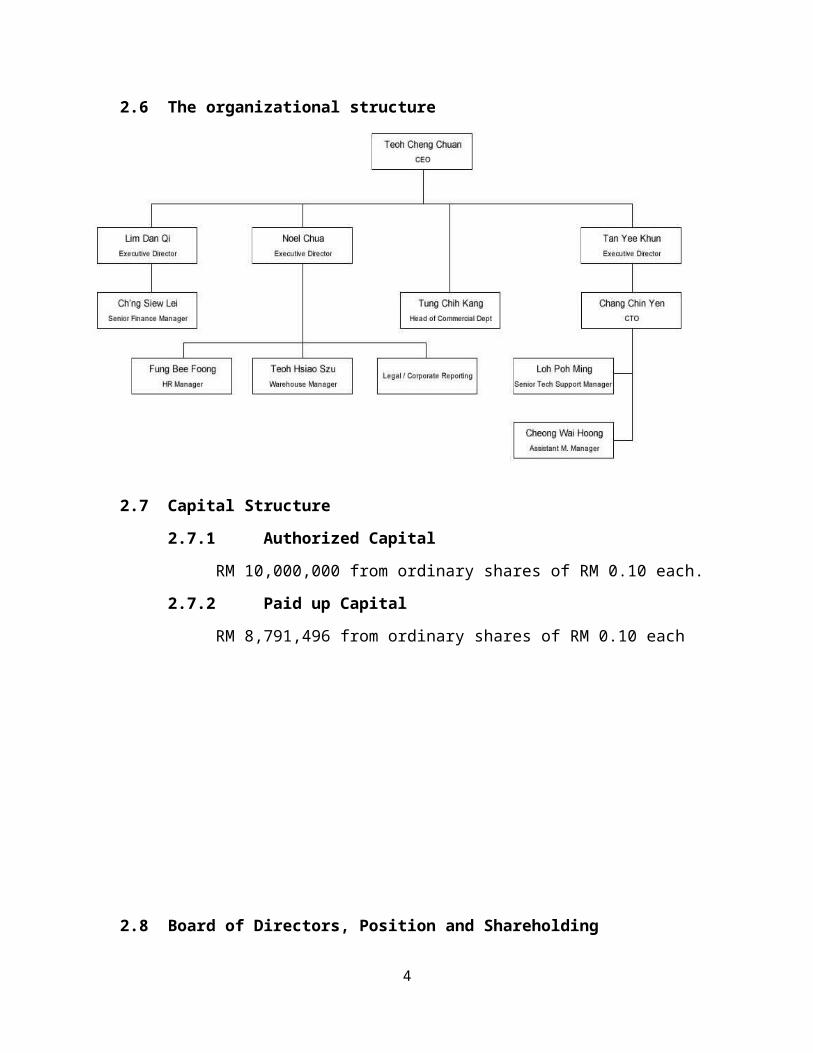

2.6 The organizational structure

2.7 Capital Structure

2.7.1 Authorized Capital

RM 10,000,000 from ordinary shares of RM 0.10 each.

2.7.2 Paid up Capital

RM 8,791,496 from ordinary shares of RM 0.10 each

2.8 Board of Directors, Position and Shareholding

No.

Directors Position Shareholding

(Number of ordinary shares held)

3

Direct Indirect

1 Hans Peter HolstChairman /

Independent Non- Executive Director

280,000 777,500

2 Teoh Cheng ChuanChief Executive

Officer20,000,000 -

3 Tan Yee Khun Executive Director 500,014 -4 Noel Chua Executive Director -

5 Kong Kok CheeIndependent Non- Executive Director

- -

6 Pang Hee KinIndependent Non- Executive Director

4,263,000 -

2.9 Senior Management

Name Position Summary

Hans Peter Holst Chairman / Independent

Non-Executive Director

Danish, age 69

Appointed to BOD of Asia Poly as

4

Independent Non-Executive Chairman,

Chairman of Audit Committee, Nomination

Committee and Remuneration Committee.

Obtained Master of Business Administration

from Copenhagen Business School in 1995.

Obtained Doctor Philosophy from University

of Malaya, Faculty of Business and

Accountancy in 2010.

Other qualification includes Alpha Certificate,

INSEAD in 1987 and Logisics-Projects

Certificates, Cranfield University in 1996.

Teoh Cheng Chuan Chief Executive Officer Malaysian, age 56

Appointed to BOD of Asia Poly as Chief

Executive Officer and member of

Remuneration Committee

In charge of Group’s operation, management

and strategic planning

Graduated with a Bachelor of Science in

Chemistry from University Malaya, in 1978

Accumulated experience in chemical industry

of over 20 years

Started as Business Executive with Sumitomo

Corporation in 1980. During his tenure as

Senior Manager of Business Development

with Sumitomo Corp (KL), he successfully

initiated and developed business in areas such

as export and domestic markets for chemical

based products, food products, wires, animal

feed, fatty acids and palm oil and its

derivative products for both export and local

markets.

Tan Yee Khun Executive Director Malaysian , age 52

Appointed to the BOD of Asia Poly as

Independent Non-Executive Director and

5

subsequently redesignated as Executive

Director on 29th May 2006 and also a member

of Audit Committee until 22nd January 2009

Graduated with Diploma in Science (with

merit) B.S. cum Laude

Worked as Chemist with Lam Soon Oils &

Fats Sdn Bhd from 1981 to 1983

Subsequently worked with Intercontinental

Specialty Fats SB as Chemist before

promoted to Technical Manager

From 2002 to 2004, employed as Chief

Chemist in Asia Poly Industrial Sdn Bhd

From 2004-2009, employed by Micronisers

(M) Sdn Bhd as GM

The table shown above summarizes the three important people in Asia Poly Holdings Berhad that make

important decisions that will affect the growth of the company. Based on their experience and knowledge,

this shows that Asia Poly Holdings Berhad is in good hands.

2.10 Bankers and Auditors

Principal Bankers:

AmBank (M) Berhad

AmIslamic Bank Berhad

6

Auditors:

Deloitte KassimChan (AF 0080) Chartered Accountants

Level 19, Uptown 1,

Jalan SS21/58, Damansara Uptown,

47400 Petaling Jaya, Malaysia.

7

The table shown the page before is the financial performance of Asia Poly Holdings Berhad for

the past 3 years to show the financial status of ASPLY is a standard operating procedure to evaluate the

companies for loan appraisal. The current ratio of the company is below the benchmark of 2 which is not

favourable and ratio of 0.9549 is shows that the company is having difficulty meeting current

obligations but this does not mean that it will go bankrupt. Compared to the past 2 years, the current

ratio of the company is improving over the time from 0.8731 (2011) to 0.8999(2012) and to 0.9549

8

(2013). Improved current ratio over time means the company ability to make payment has also

improved.

Quick ratio measure the ability of company to settle its current liabilities on short notice. As for

Asia Poly, quick ratio of less than 1 for 3 years consecutive indicates that company cannot currently

fully pay back its current liabilities. Because Asia Poly is a manufacturing company for plastic product,

the industry standard for quick ratio is 0.6 and the ratios calculated for the 3 years is all lower than the

industry standard. Quick ratio which is lower than the industry average may suggest that the company is

taking too much risk by not maintaining an appropriate buffer of liquid resources. Alternatively, a

company may have a lower quick ratio due to better credit terms with suppliers than the competitors.

Asia Poly working capital shows a negative figure for the past 3 years explains that uncertainty of ability

to repay its current liability in short term. However, if a company is growing, this can be the most

advantageous working capital position because it literally “coins” money for the company. Due to some

circumstances, Asia Poly is in their recovery period and still growing after the fire incident happened

back in 2007 that burn the factory completely and later fully reinstate their production in 2009.

The inventory turnover ratio shows the efficiency of management of inventory. The inventory

turnover ratio improved yearly from 4.89 times in 2011 to 5.77 times in 2013. Compared to industry

average inventory turnover of 5.4 times, Asia Poly may seem to not able to reach the industry average

for in 2011 but in 2012 and 2013, Asia Poly inventory turnover ratio is higher than the industry. This

shows that demand of Asia Poly’s cast acrylic demand are slowly increasing. Aside from that, the

inventory turnover days is improving from 75 days in 2011 to 63 days in 2013. This means that it take

shorter time to sell the stock, which is good news to Asia Poly. Besides that, the average collection

period is also one of the important ratios to look at in order to determine the efficiency of the company

in collecting the receivables. The collection period had decreased 23 days from 91 days to 68 days but

9

increased back to 88 days in 2013.Although the average collection period is not stable, but it is still

within the company standard credit period of 30 to 90 days.

As for the profitability ratio, the company gross profit-sales ratio as well as the net profit ratio

has increased tremendously especially from year 2011 to 2012. Asia Poly records a meagre 1.24% of

gross profit ratio and a negative ratio for net profit in year 2011, but improved a lot in 2012 and 2013.

The gross profit ratio jumped above 20% (20.07% in 2012 and 24.44% in 2013), while the net profit

ratio recorded both positive figure in year 2012 and 2013. Although the gross profits improved by more

than 20 percent, the net profit figure is relatively small compared to the improvements made in 2012 and

2013. This can be explained by the price increases obtainable from domestic and export customers

lagged behind the absorption of cost increases imposed by the company especially on ingredient

suppliers. Aside from that, Asia Poly was facing managing the absorption of minimum wage increase

mandated by the Government of Malaysia. Compared to industry benchmark of 32%, Asia Poly gross

profit is still lower than the benchmark. Reason being is the company is recovery period, and this can be

seen by observing the gross profit ratios are improving as the years goes.

Leverage ratio helps to assess the risk arising from the use of debt capital. The debt to equity ratio

shows how much the company is financed by debt compared to the proprietor’s own investment in

business. The ratio had increased from 0.0750 in 2011 to 0.0896 in 2013. This shows the ratio is

increasing slowly due to the fact that Asia Poly are conducting more R&D and purchased machineries to

develop the polymerization process to study the thermoforming performance of acrylic sheet. Aside

from that sophisticated laboratory equipment was installed to control the finished products to meet

customer’s general and unique requirement and to comply with the international standards. Machineries

purchased were under hire-purchase agreement. Interest coverage ratio explains the ability of company

to generate revenue to cover its interest expenses. The interest coverage ratio for 2011 and 2012 was not

10

satisfactory while in 2013, Asia Poly records 1.7 which is above the ideal figure of 1.5. As mentioned

before, Asia Poly is still growing and recovering from the fire incident.

4.0The Proposed Project

4.1 State the proposed project

The main purpose of this project is that ASPL intends to expand its production capacity to meet the increasing

demand of cast acrylic sheets in the market. Asia Poly is famous for not compromising their quality by using

only 100% virgin material sourced exclusively by reputable suppliers, explains the reason for being top

choice material to world leading brand such as Adidas and McDonalds. Asia Poly needs to increase its

11

production capacity with the intention of coping to be able to meet the high demand of cast acrylic in the

market. In addition, Asia Poly always conduct research and development (R&D) to achieve the higher quality

of the cast acrylic at the lowest overall cost at better efficiency rate. The proposed project of building new

facility would include R&D center in the new factory.

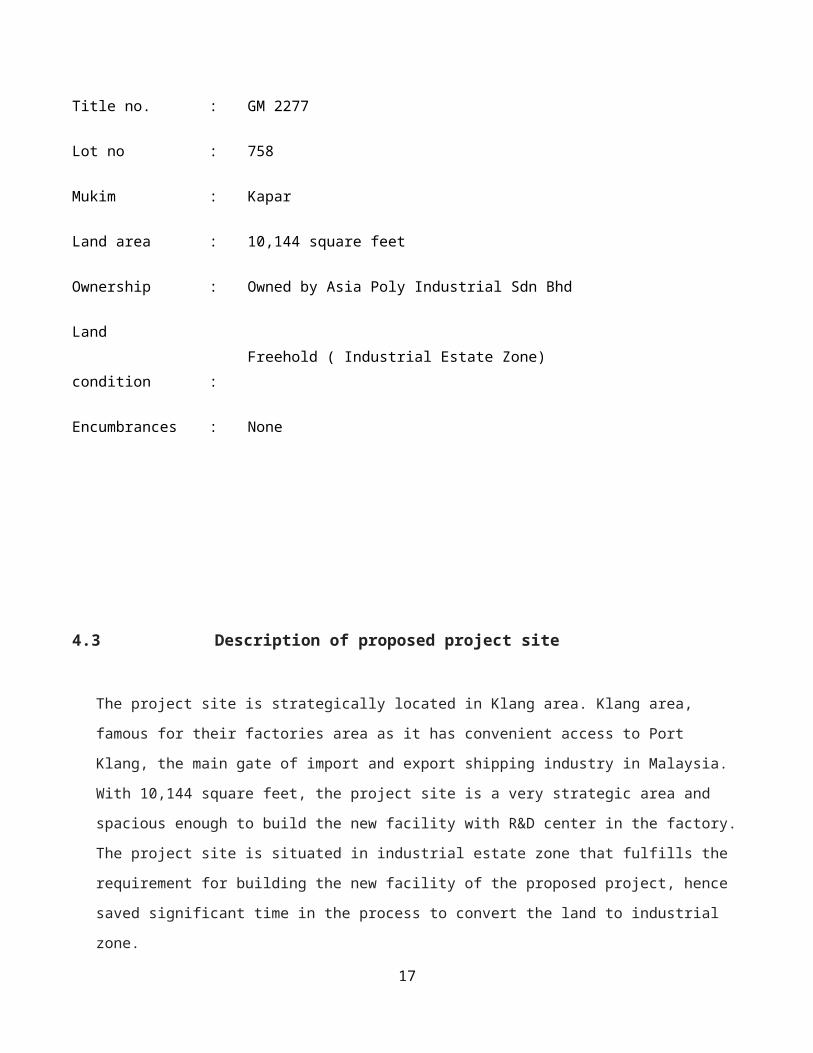

4.2 Particulars of the land

Title no. : GM 2277

Lot no : 758

Mukim : Kapar

Land area : 10,144 square feet

Ownership : Owned by Asia Poly Industrial Sdn Bhd

Land condition : Freehold ( Industrial Estate Zone)

Encumbrances : None

4.3 Description of proposed project site

The project site is strategically located in Klang area. Klang area, famous for their factories area as it has

convenient access to Port Klang, the main gate of import and export shipping industry in Malaysia. With

10,144 square feet, the project site is a very strategic area and spacious enough to build the new facility with

R&D center in the factory. The project site is situated in industrial estate zone that fulfills the requirement for

building the new facility of the proposed project, hence saved significant time in the process to convert the

land to industrial zone.

12

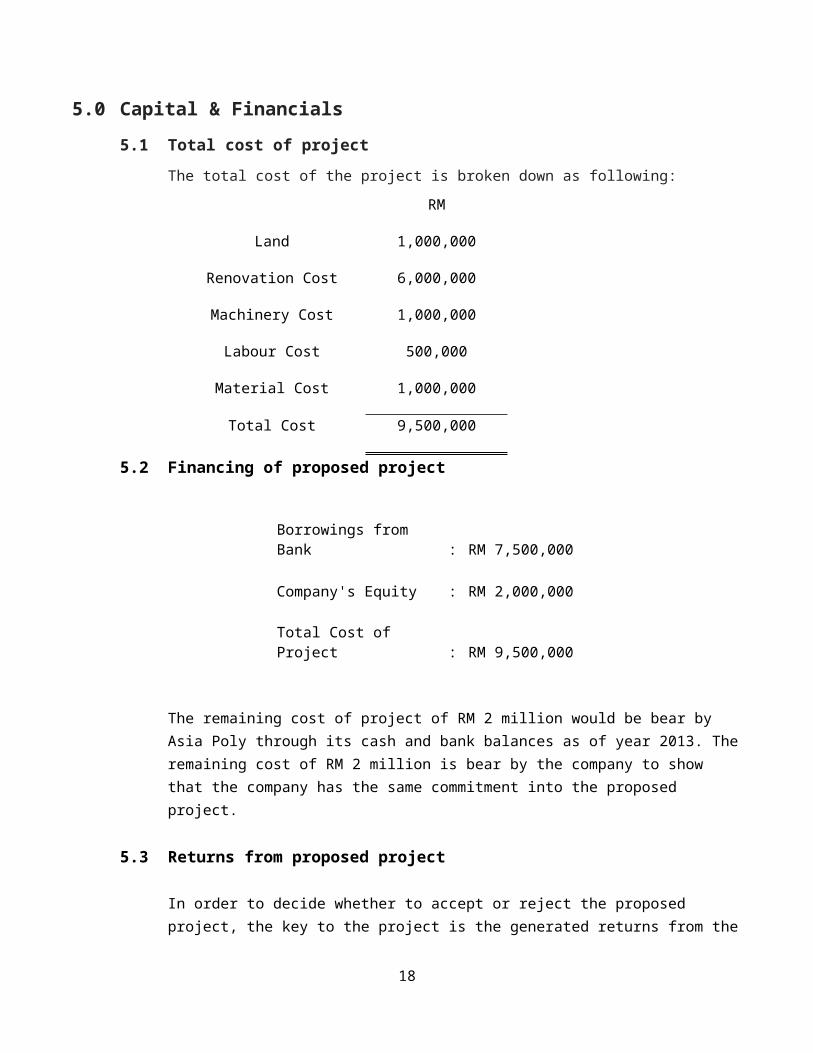

5.0 Capital & Financials

5.1 Total cost of project

The total cost of the project is broken down as following:

5.2 Financing of proposed project

Borrowings from Bank : RM 7,500,000

Company's Equity : RM 2,000,000

Total Cost of Project : RM 9,500,000

The remaining cost of project of RM 2 million would be bear by Asia Poly through its cash and bank balances as of year 2013. The remaining cost of RM 2 million is bear by the company to show that the company has the same commitment into the proposed project.

5.3 Returns from proposed project

In order to decide whether to accept or reject the proposed project, the key to the project is the generated returns from the project. To calculate the rate of return from proposed project, two formulas will be involved. They are Net Present Value (NPV) and Internal Rate of Return (IRR) of the project.

The discount rate of NPV of this project is 6.9% and the cost of capital equals to 8%.

YearProjected Outflow

(RM)Projected Inflow

(RM)Net Cash Flow

0 (9,500,000) Nil (9,500,000)

13

RM

Land 1,000,000

Renovation Cost 6,000,000

Machinery Cost 1,000,000

Labour Cost 500,000

Material Cost 1,000,000

Total Cost 9,500,000

1 (3,000,000) 5,000,000 2,000,0002 (2,034,342) 5,500,000 3,465,6583 (1,980,234) 5,775,000 3,794,7664 (1,800,345) 6,352,500 4,552,155

5 (1,435,223) 7,305,375 5,870,152

Total 10,182,731

The proposed project will take one year to complete and commission. Therefore, for the first year there is only outflow amounting RM 11,000,000 which is the total cost of the project. The company will only start to generate cash inflow or revenue when the factory commence in year 1 onwards. The projected total net cash flow at end of year 5 will be RM 10,182,731.

5.3.1 Net Present Value (NPV)

To calculate the NPV, the discount rates needs to be determined. The discount rate is the sum of interest rate of Treasury Bond and current inflation rate of Malaysia. According to Bank Negara Malaysia, the interest rate of Malaysia Government Security (MGS) is 3.5% and the inflation rate would be 3.4%. Therefore, the discount rate would sum up to the rate of 6.9%

= RM 6,200,0753.97

Decision Rule :NPV > 0, therefore proposed project can be approve.

5.3.2 Internal Rate of Return (IRR)

The IRR of the project need to be higher than the cost of capital of 8.0% in order for the Bank to approve the loan for the proposed project.

The IRR is calculated using the financial calculator and the IRR for this project is 25.21%.

The IRR of the project of 25.21% is higher than the cost of capital of 8.0%.According to IRR rule, the return of rate that is higher than the cost rate means that the returns generated from the proposed project outweigh the cost of capital of the project. Thus, the project should be accepted.

14

NPV¿−RM 9,500,000+ RM 2,00,000

(1+6.9 % )1+RM 3,465,658

(1+6.9 % )2+ RM 3,794,766

(1+6.9 % )3+RM 4,552,155

(1+6.9 % )4+RM 5,870,152

(1+6.9 % )5

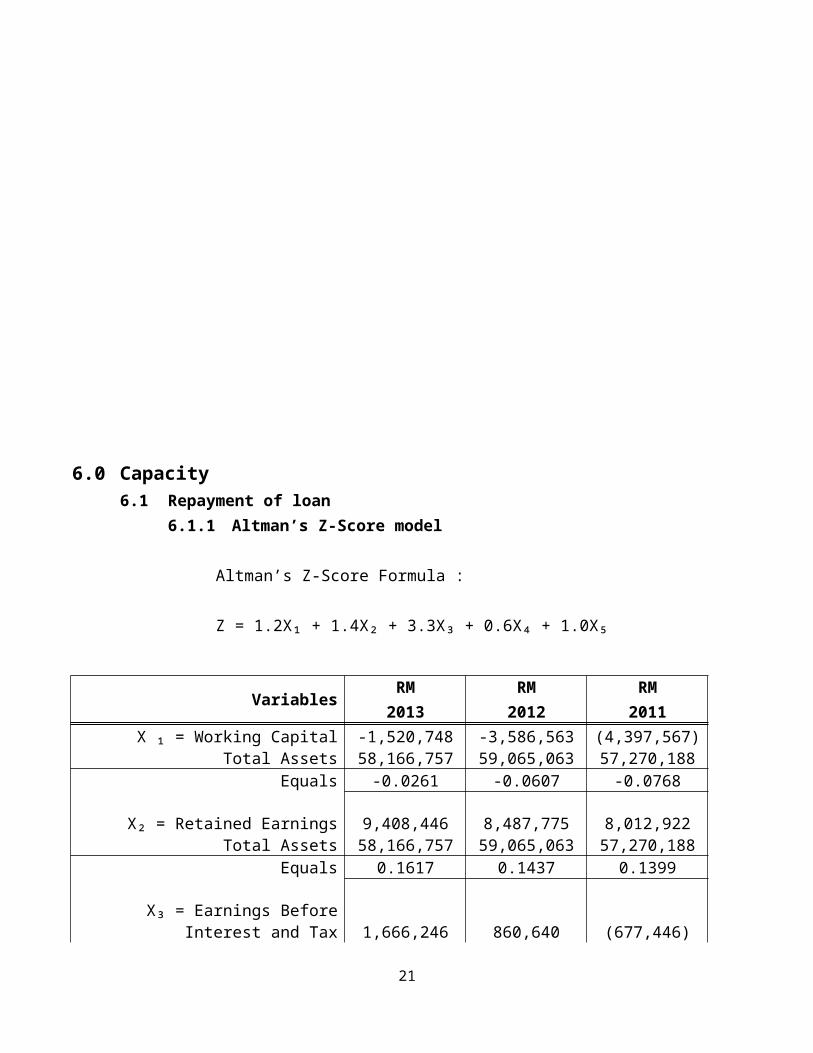

6.0 Capacity6.1 Repayment of loan

6.1.1 Altman’s Z-Score model

Altman’s Z-Score Formula :

Z = 1.2X₁ + 1.4X₂ + 3.3X₃ + 0.6X₄ + 1.0X₅

VariablesRM RM RM2013 2012 2011

X ₁ = Working Capital -1,520,748 -3,586,563 (4,397,567)Total Assets 58,166,757 59,065,063 57,270,188

15

Equals -0.0261 -0.0607 -0.0768

X₂ = Retained Earnings 9,408,446 8,487,775 8,012,922Total Assets 58,166,757 59,065,063 57,270,188

Equals 0.1617 0.1437 0.1399

X₃ = Earnings Before Interest and Tax 1,666,246 860,640 (677,446)Total Assets 58,166,757 59,065,063 57,270,188

Equals 0.0286 0.0146 -0.0118

X₄ = Market Value Equity 16,703,842 16,703,842 16,703,842Book Value Total Debt 35,743,855 35,838,950 36,242,810

Equals 0.4673 0.4661 0.4609

X₅ = Sales 77,704,663 79,784,896 61,953,160Total Assets 58,166,757 59,065,063 57,270,188

Equal 1.3359 1.3508 1.0818

Z Score 1.91 1.81 1.42

X ₁ = Working Capital / Total Assets

X ₂ = Retained Earnings / Total Assets

X₃ = Earnings Before Interest and Tax / Total Assets

X₄ = Market Value Equity / Book Value Total Debt

X₅ = Sales / Total Assets

Decision Rule of Altman’s Z-Score Model:

Z-score > 2.99 predicts non-fail

Z-score < 1.81 predicts fail

2.99<Z-score<1.81 is “zone of ignorance”

Based on the Z-score calculated in the table above, the latest 2 years which is 2013 and 2012 is in

the zone of ignorance while in 2011, the Z-score is predicted to fail. In 2011, the Z-scores are not

satisfactory as they are improving and recovering from the fire incident happened in 2007 that

forced them to stop their operation for more than 1 year. They fully resume their operation on 1st

16

April 2009 and started to recover their business gradually and improving. It can be seen that their

scores and ratios are improving tremendously from 2012 onwards. From Z-Score of 1.42 in 2011

(predicted to fail) to 1.91(zone of ignorance) in 2013.

Altman defines a zone of ignorance, a grey area, when the model produces a z-value 1.81 – 2.99,

where the model is unable to distinguish a bankrupt from a non-bankrupt firm.

Loan Repayment Schedule

The prime rate lending loan is 6.6% .The fact that Asia Poly is in the zone of ignorance or

gray area make the judgment harder as the Altman model is unable to distinguish Asia

Poly is a bankrupt or a non-bankrupt firm. Judging from its financial ratio performance,

Asia Poly is in their recovery period and it is uncertain that if their sales figure will

continue to increase, that place them into riskier company. Therefore, a higher profit

margin will be charged to Asia Poly and the figure would be 1.4 percent. The interest rate

will sum up to 8.0%

In order to calculate the monthly installment, the mortgage constant needs to be calculated using the formula of:

Mortgage constant

¿ r¿¿

¿

0.0812¿¿

= 0.02027639429

Where r is the interest rate charged on the loan which is 8 % per annum. The monthly

repayment (PMT) is then calculated using the following formula:

17

PMT = Amount of mortgaged loan X Mortgage Constant

= RM 7,500,000 x 0.02027639429

= RM 152,072.96

Therefore, Asia Poly would have to repay the Bank RM 152,072.96 monthly for the next

5 years in order to take up the loan of RM7, 500,000 from the Bank. The monthly

payment schedule is attached at the following page.

6.2 Tenure of Loan5 years

6.3 Source of Repayment

The proposed new facility is said to take 1 year to complete. This can be seen in the

projected cash flow where there is no cash inflow in year 0 due to the fact that the new

facility is still under construction. On the other hand, the expenses incurred in year 0

which will amount to RM9, 500,000 and to top of that, the expenses of monthly

repayment of the loan will be covered by the company existing cash flow. After going

through the relevant financial ratios and doing the necessary analysis on Asia Poly, the

result were favorable and shows that the company will not have any problem making the

monthly repayment and conducting the business as usual during the year of construction.

The income and profit of the company will be able to cover the expenses and repay the

monthly installment of RM 152,072.96 for 5 years to the bank.

Once the construction of the factory is completed and the factory starts its production, the

company will be able to earn positive net cash flow that will be enough to cover the

18

installment payment to the bank.

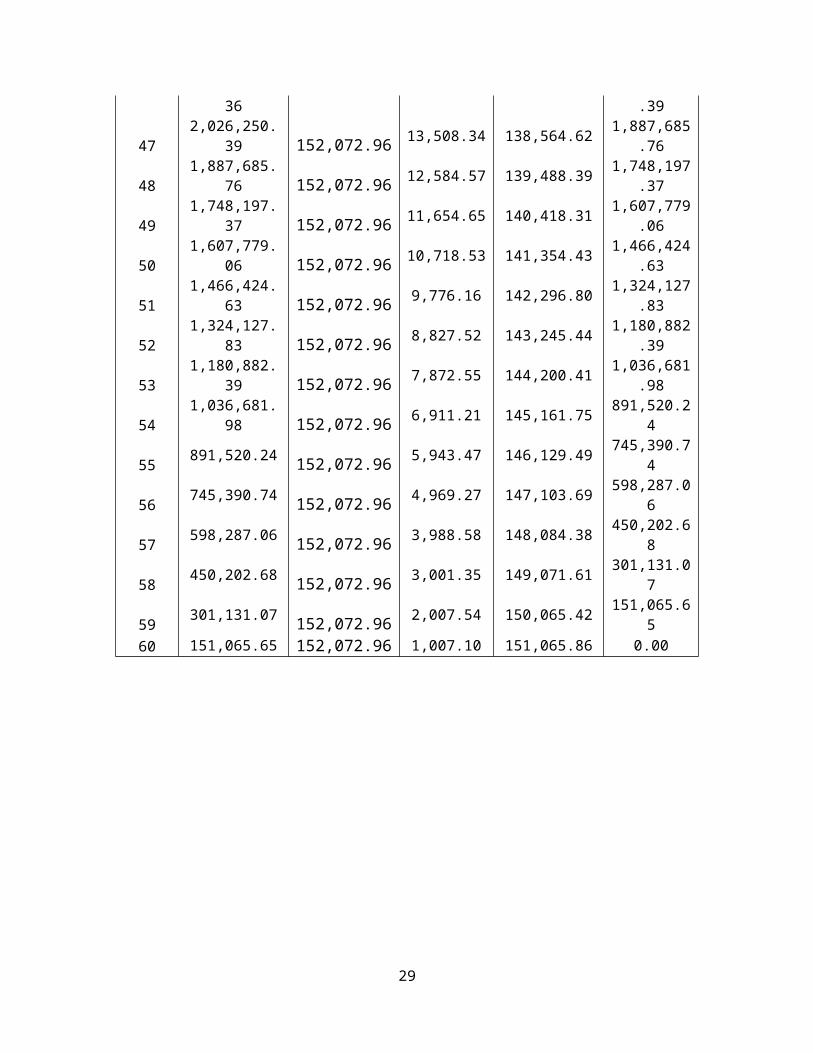

6.4 Loan Repayment Schedule

MonthBeginning Balance (RM)

Monthly Repayment

(RM)

Interest Expense (RM) (8 %)

Principal Payment (RM)

Ending Balance (RM)

1 7,500,000.00 152,072.96 50,000.00 102,072.96 7,397,927.04

2 7,397,927.04 152,072.96 49,319.51 102,753.45 7,295,173.59

3 7,295,173.59 152,072.96 48,634.49 103,438.47 7,191,735.12

4 7,191,735.12 152,072.96 47,944.90 104,128.06 7,087,607.07

5 7,087,607.07 152,072.96 47,250.71 104,822.25 6,982,784.82

6 6,982,784.82 152,072.96 46,551.90 105,521.06 6,877,263.76

7 6,877,263.76 152,072.96 45,848.43 106,224.53 6,771,039.22

8 6,771,039.22 152,072.96 45,140.26 106,932.70 6,664,106.52

9 6,664,106.52 152,072.96 44,427.38 107,645.58 6,556,460.94

10 6,556,460.94 152,072.96 43,709.74 108,363.22 6,448,097.72

11 6,448,097.72 152,072.96 42,987.32 109,085.64 6,339,012.08

19

12 6,339,012.08 152,072.96 42,260.08 109,812.88 6,229,199.20

13 6,229,199.20 152,072.96 41,527.99 110,544.97 6,118,654.23

14 6,118,654.23 152,072.96 40,791.03 111,281.93 6,007,372.30

15 6,007,372.30 152,072.96 40,049.15 112,023.81 5,895,348.49

16 5,895,348.49 152,072.96 39,302.32 112,770.64 5,782,577.85

17 5,782,577.85 152,072.96 38,550.52 113,522.44 5,669,055.41

18 5,669,055.41 152,072.96 37,793.70 114,279.26 5,554,776.16

19 5,554,776.16 152,072.96 37,031.84 115,041.12 5,439,735.04

20 5,439,735.04 152,072.96 36,264.90 115,808.06 5,323,926.98

21 5,323,926.98 152,072.96 35,492.85 116,580.11 5,207,346.86

22 5,207,346.86 152,072.96 34,715.65 117,357.31 5,089,989.55

23 5,089,989.55 152,072.96 33,933.26 118,139.70 4,971,849.85

24 4,971,849.85 152,072.96 33,145.67 118,927.29 4,852,922.56

25 4,852,922.56 152,072.96 32,352.82 119,720.14 4,733,202.42

26 4,733,202.42 152,072.96 31,554.68 120,518.28 4,612,684.14

27 4,612,684.14 152,072.96 30,751.23 121,321.73 4,491,362.41

28 4,491,362.41 152,072.96 29,942.42 122,130.54 4,369,231.86

29 4,369,231.86 152,072.96 29,128.21 122,944.75 4,246,287.11

30 4,246,287.11 152,072.96 28,308.58 123,764.38 4,122,522.74

31 4,122,522.74 152,072.96 27,483.48 124,589.48 3,997,933.26

32 3,997,933.26 152,072.96 26,652.89 125,420.07 3,872,513.19

33 3,872,513.19 152,072.96 25,816.75 126,256.21 3,746,256.98

34 3,746,256.98 152,072.96 24,975.05 127,097.91 3,619,159.07

35 3,619,159.07 152,072.96 24,127.73 127,945.23 3,491,213.84

36 3,491,213.84 152,072.96 23,274.76 128,798.20 3,362,415.64

37 3,362,415.64 152,072.96 22,416.10 129,656.86 3,232,758.78

38 3,232,758.78 152,072.96 21,551.73 130,521.23 3,102,237.55

39 3,102,237.55 152,072.96 20,681.58 131,391.38 2,970,846.17

40 2,970,846.17 152,072.96 19,805.64 132,267.32 2,838,578.85

41 2,838,578.85 152,072.96 18,923.86 133,149.10 2,705,429.75

42 2,705,429.75 152,072.96 18,036.20 134,036.76 2,571,392.99

43 2,571,392.99 152,072.96 17,142.62 134,930.34 2,436,462.65

44 2,436,462.65 152,072.96 16,243.08 135,829.88 2,300,632.77

45 2,300,632.77 152,072.96 15,337.55 136,735.41 2,163,897.36

46 2,163,897.36 152,072.96 14,425.98 137,646.98 2,026,250.39

47 2,026,250.39 152,072.96 13,508.34 138,564.62 1,887,685.76

48 1,887,685.76 152,072.96 12,584.57 139,488.39 1,748,197.37

49 1,748,197.37 152,072.96 11,654.65 140,418.31 1,607,779.06

50 1,607,779.06 152,072.96 10,718.53 141,354.43 1,466,424.63

51 1,466,424.63 152,072.96 9,776.16 142,296.80 1,324,127.83

52 1,324,127.83 152,072.96 8,827.52 143,245.44 1,180,882.39

20

53 1,180,882.39 152,072.96 7,872.55 144,200.41 1,036,681.98

54 1,036,681.98 152,072.96 6,911.21 145,161.75 891,520.24

55 891,520.24 152,072.96 5,943.47 146,129.49 745,390.74

56 745,390.74 152,072.96 4,969.27 147,103.69 598,287.06

57 598,287.06 152,072.96 3,988.58 148,084.38 450,202.68

58 450,202.68 152,072.96 3,001.35 149,071.61 301,131.07

59 301,131.07 152,072.96 2,007.54 150,065.42 151,065.65

60 151,065.65 152,072.96 1,007.10 151,065.86 0.00

7.0 Collateral

7.1 Collateral offered

For the proposed project, Asia Poly had offered the land and fixtures of the proposed

project as the collateral. The land is situated at Kapar, Selangor and it is acquired by Asia

Poly. It is a freehold land and located within the industrial estate zone. This loan will be

able to serve as collateral for the loan amount of RM 7,500,000 for loan tenure of 5 years.

7.2 Value of collateral

The land and fixtures had been valued by the Bank panel real-estate valuer and the

current market price of the collateral is RM 12,500,000.

21

7.3 Loan to Value

Loan Amount = RM 7,500,000

Value of collateral = RM 12,500,000

Loan to Value = RM 7,500,000/RM12,500,000= 0.6 / 60%

This fulfills the bank requirement of loan to value benchmark of 80%. The loan to value

of figure does not exceed 80%, therefore this land can be taken as the collateral of the

project and the loan.

7.4 Encumbrances

The land is free from encumbrances.

8.0 Conditions

8.1 External conditions (economics)

The economic environment and status of an industry is the key point that will affect the

performance of the company. Asia Poly share of the Malaysian market for cast acrylic sheets is

very strong and continues to grow, while export markets play an important role of the company’s

manufacturing and marketing strategy. The economic growth of Malaysia and the exports

markets and the foreign currency exchange rates are crucial factors to Asia Poly. As stated in the

annual report, Asia Poly claimed that the global economy, domestic and export markets of A-

Cast® are less predictable.

22

Recently, Budget 2014 was tabled by the Prime Minister Datuk Seri Najib announced the

implementation of Goods and Services Tax at a rate of 6% from 1st April 2015. One of the

changes would be no tax will be imposed on exports will make Malaysian export goods to be

cheaper, more competitive and sellable in foreign countries. Thus, this will make Asia Poly

goods cheaper and marketable in global market and hopefully, will increase the demand of A-

Cast®.

Due to the fierce competition, the company also did a lot of research and development in order to

improve the quality and lower the cost without compromising the quality. With continuous R&D

to improve the technological efficiency of its A-Cast® product assortment capability and

cementing will produce better marketing relationships and create new customers at this higher

level of efficiency. In addition to its ISO certifications, Asia Poly was certified for complying

with European Union's EN263 standard for sanitary grade sheets, and with Japan's JIS standard

for general purpose sheets. By complying with international standards, the market of A-Cast®

will expand internationally and will increase the revenue of Asia Poly. This means that the

revenue of Asia Poly will not only solely depend on Malaysian market and even if Malaysian

economy is not doing well, Asia Poly will not be badly affected because the demand of A-Cast®

is diverse. The sale of A-Cast® will not solely depend on Malaysian market but will also depend

on the international customers. As explained before, no tax on exports will further boost the

international orders on A-Cast®.

8.2 Internal Conditions

23

Asia Poly Holdings is in good hands as they are managed by experienced senior management

and not to forget, loyal workforce that stayed with the company regardless of the fire incident

that forced the factory to stop production for 15 months.

At the moment, Asia Poly third casting line is past the drawing board stage and can be

implemented relatively quickly when market conditions are deemed to be right. Asia Poly

believes that in order to support the company growth, continuous improvisation of technology is

important. Therefore, Asia Poly will continue to further to prioritize technological upgrading of

its production over an increase of capacity.

9.0 Compliance Issue

Asia Poly met the requirement of the Bank’s internal policy, of maintaining a good track of

payment record with the Bank with reference to the previous loans, facilities and services

undertaken with the Bank. After conducting detailed credit checks on the company and directors,

results shown that their past record is clean. Detailed analysis of the company’s financial report

for the past 3 years was conducted and Asia Poly can be concluded as a profitable and reputable

company in the industry. Besides that, the cash flow are seen to be able to meet the loan

repayment stated above. The product of Asia Poly; A-Cast® Precast is highly demanded and

rated by the customers locally and globally.

24

Besides that, the necessary permits and license for building the new facility was approved by the

government. The layout plan had been approved by the Land Office and buildings plans was

approved by the Town Council.

Since Asia Poly met the required benchmark and fulfill the Bank’s internal policy, the loan

should be approve.

10.0 Justification for the loan

Asia Poly has a team of experienced senior management placed according to their skills came from

reputable education qualification background that is useful in managing the company. After conducting

detailed credit checks on the company and directors, results shown that their past record is clean. The

company have good repayment track record for past loans approved by the bank. This shows that the

company is responsible in repaying their borrowed funds and debt on timely manner.

The borrower, Asia Poly, is a reputable company that manufactures their own brand of A-Cast® cast

acrylic sheets is manufactured from 100% Virgin Methyl Methacrylate monomer (MMA) with

25

worldwide demand. Based on the 3 financial years audited financial report, the financial ratios

calculated in part 3, the company gross profit is high but recorded a low net profit margin, higher

expenses due to stricter regulations set by the government. But, this is not an issue because Asia Poly is

still recovering from the fire incident and the recovery speed is moving very fast. Based on Altman’s Z-

score, Asia Poly score improved to zone of ignorance in 2013. Zone of ignorance means difficult to

determine whether Asia Poly is a bankrupt or non -bankrupt company, but the improvements made for

the past 3 years shows that Asia Poly has improved their sales figure and profitability ratio. The

company cash flow are able to meet the loan repayment as shown in the repayment schedule.

The proposed project is secured with the lands and buildings as collateral. The Bank had requested a

valuation report from the panel valuer of the Bank and a land visit was done to ensure the conditions of

land is as the same as stated. The loan to value of the collateral is 60% which is more than enough, as

the minimum bench of the Bank is 80%. A land search was done with the Land Office and confirmed

that Asia Poly have the full ownership of the land.

The proposed project cost RM 9,500,000 is financed up to 80% by the bank and the remaining of RM

2,000,000 is the capital contribution by the company. The corporation contributed more than 20%,

amounting RM 2 million in the proposed project means that the company is confident that project will

generate substantial amount to recover its capital.

While for the economic condition in the manufacturing industry, the cast acrylic sheets have high

demand in domestic and international market. The company is always conducting research and

development to improve its quality as a leading manufacturer and innovator in the production and

26

supply of cast acrylic sheets. Aside from quality measure, Asia Poly prides itself on its international

service and delivery capability, supporting many distributors worldwide with a wide portfolio of quality

products. With the recent announcement made by Government for absence of GST on exports, this will

boost the company’s revenue in international market. The company has strong team player and well

managed team that ensure the growth of business and also make sure that business practice comply with

general aspect for environment.

Lastly, the company had fulfilled all the requirement of the bank’s internal policy. Thus, I hereby

recommend the loan for approval.

11.0 Loan Decision and Loan Structuring

As a result after justified the loan as above, the loan structure and terms are as follow:

Loan Amount : RM 7,500,000

Loan Tenure : 5 years

Interest Rate : Fixed interest rate of 8% throughout 5 years

Monthly Repayment : RM 152,072.96 for 5 years

Repayment Term : Borrower will repay the monthly installment of RM 152,072.96

on the 10th of each month for 5 years.

Late charges : 1% p.a. above prescribed rate on any portion of principal and/or

interest that is overdue.

27

Default Term : In the event of any default or the Borrower fails to pay any

Monthly Instalments on the due date, default interest is at

the rate of one per centum (1%) per annum calculated on a

daily rests basis.

An immediate payment of entire remaining unpaid balance

of this lose is required, without prior notice by the Bank.

Lender has the right to retain the respective collateral

pledge.

Disbursement : In three stages, 30%. 40% and 30% of the loan amount. The last

installment will be disbursed three or four weeks prior to the

completion of the building.

Collateral : The Lender shall have the right to exercise and enforce all

rights and remedies now or hereafter available to it under this

Agreement, the Notes, the Collateral, any applicable law and

any other contract.

12.0 Conclusion

In conclusion, after evaluating the relevant information and documents from Asia Poly Holdings Berhad,

I hereby recommend this loan for approval based on justification and analysis made above with the terms

and conditions applied.

B Other loan/legal documents that I would like to require in order to make loan decisions are:

Sales and Purchase Agreement (SPA)

Photocopy of land title

Construction Agreement with the contractor supported by the Engineer and Quantity

Surveyor

28

Costing report for the Project

Approved layout plan and buildings plan

C Conditions I would impose are:

Disbursement subject to architect and contractor confirmation of stages of construction

The factory is not allowed to commission its operations prior to obtaining Certificate of

Completion & Compliance (CCC).

29