lerach coughlin stoia geller rudman & robbins...

TRANSCRIPT

1

2

3

4

5

6

7

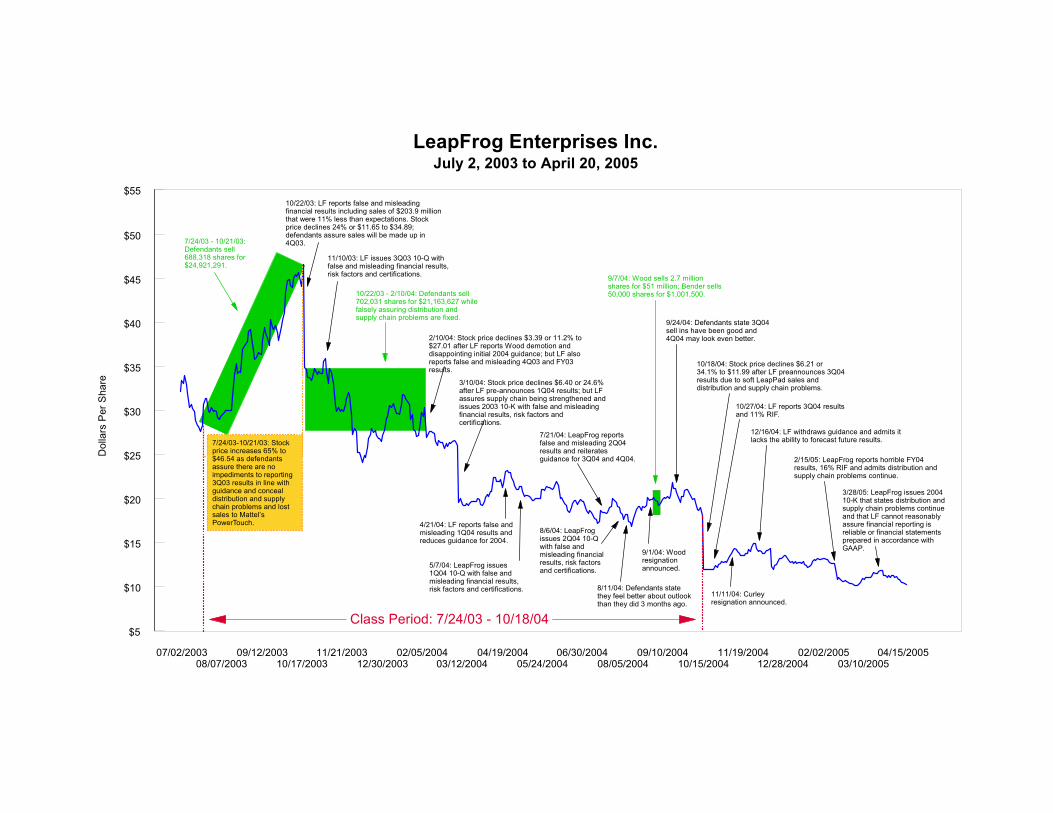

8

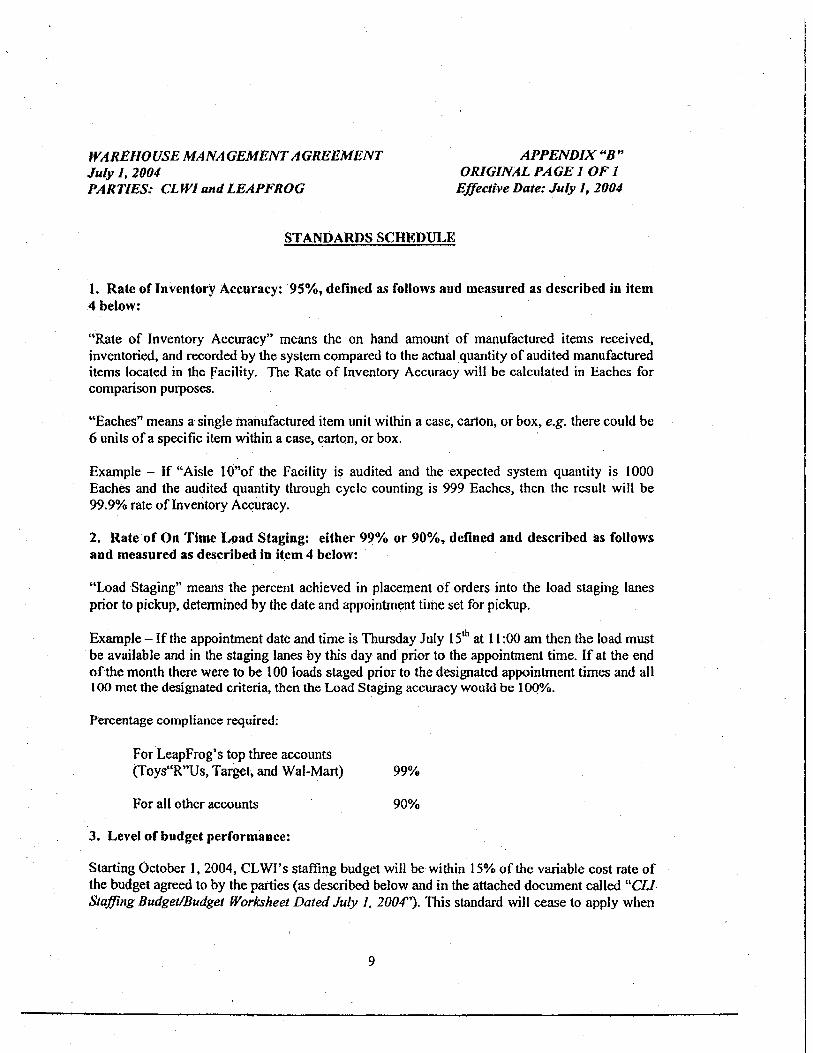

9

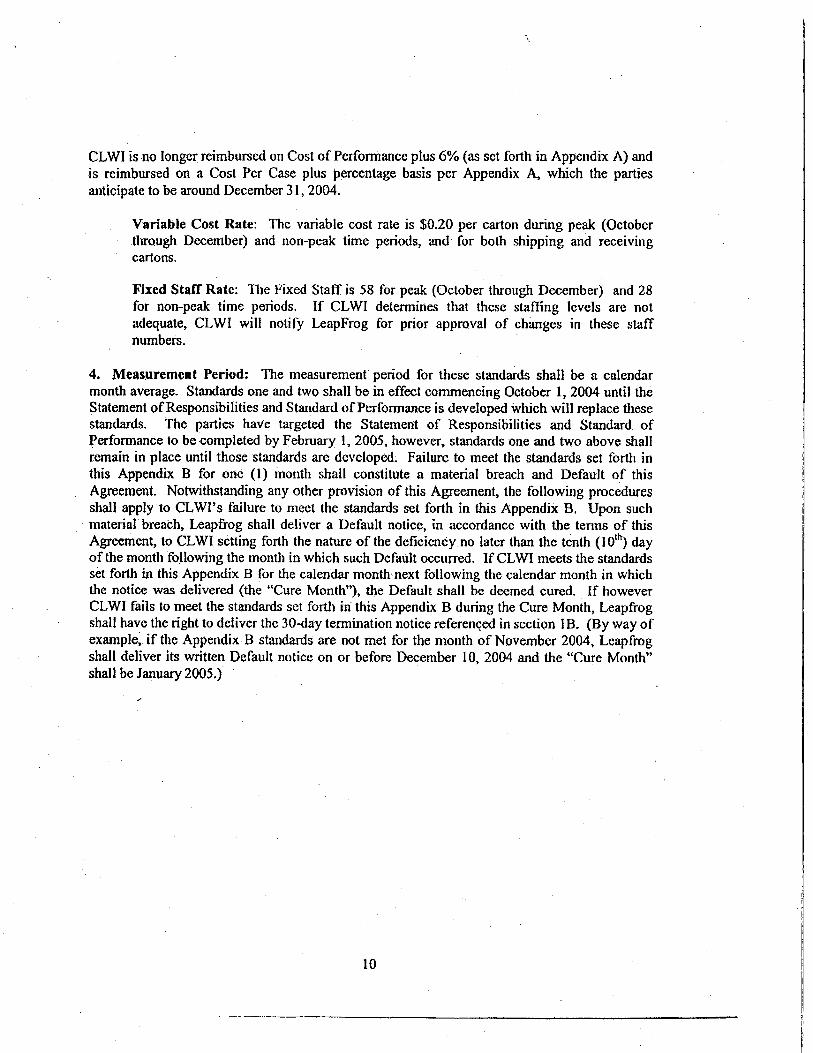

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

LERACH COUGHLIN STOIA GELLER RUDMAN & ROBBINS LLP PATRICK J. COUGHLIN (111070) CHRISTOPHER P. SEEFER (201197) 100 Pine Street, Suite 2600 San Francisco, CA 94111 Telephone: 415/288-4545 415/288-4534 (fax)

– and – WILLIAM S. LERACH (68581) DARREN J. ROBBINS (168593) 401 B Street, Suite 1600 San Diego, CA 92101 Telephone: 619/231-1058 619/231-7423 (fax)

Lead Counsel for Plaintiffs

UNITED STATES DISTRICT COURT

NORTHERN DISTRICT OF CALIFORNIA

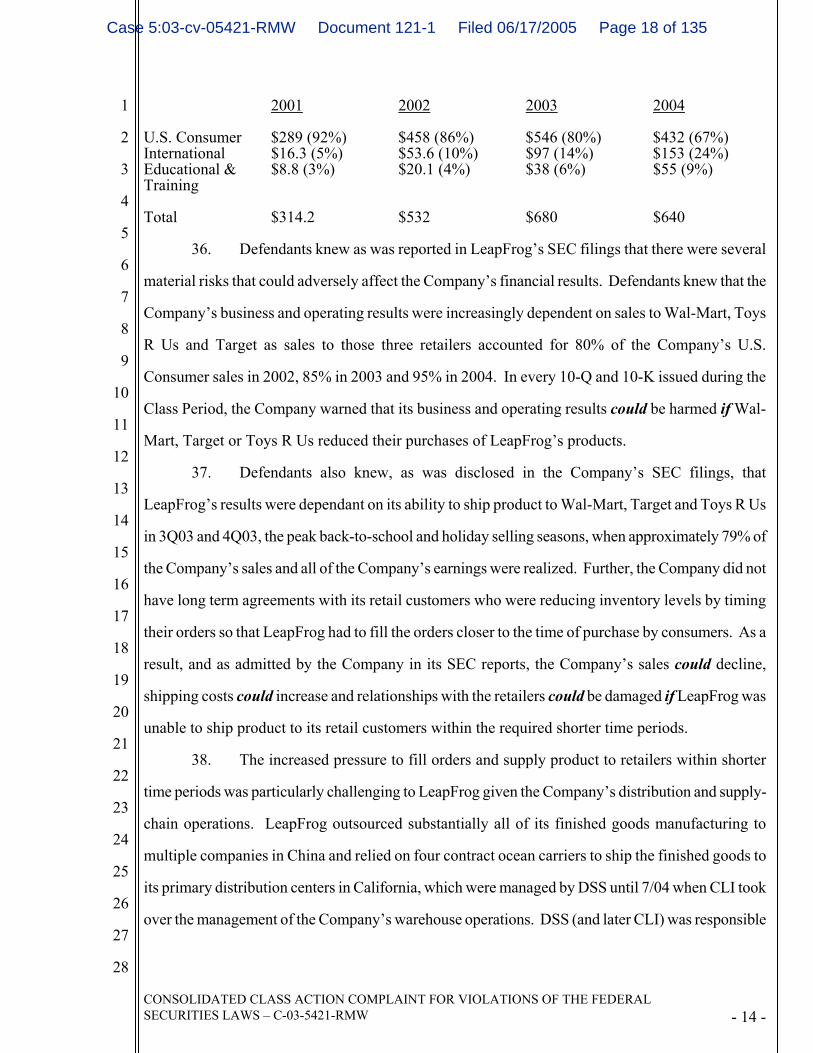

In re LEAPFROG ENTERPRISES, INC. SECURITIES LITIGATION

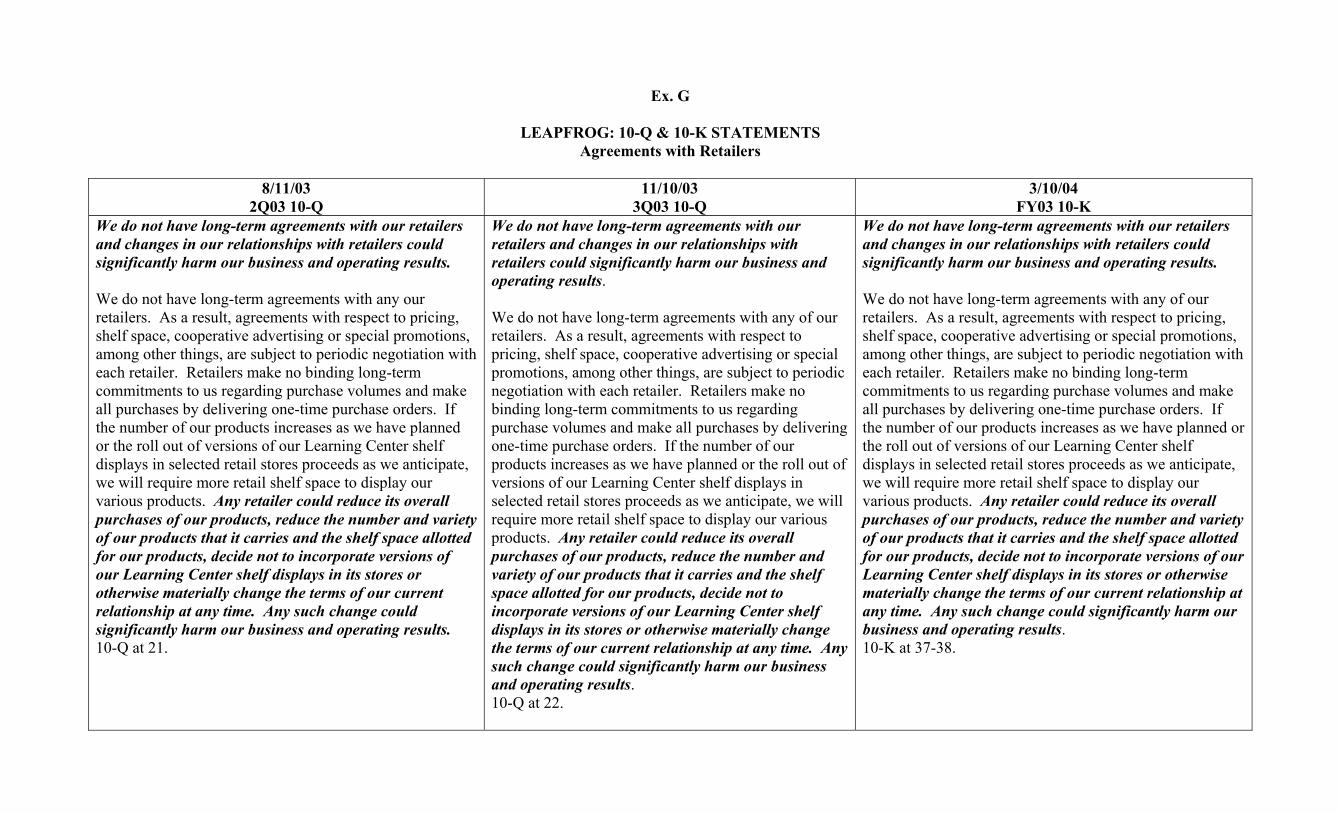

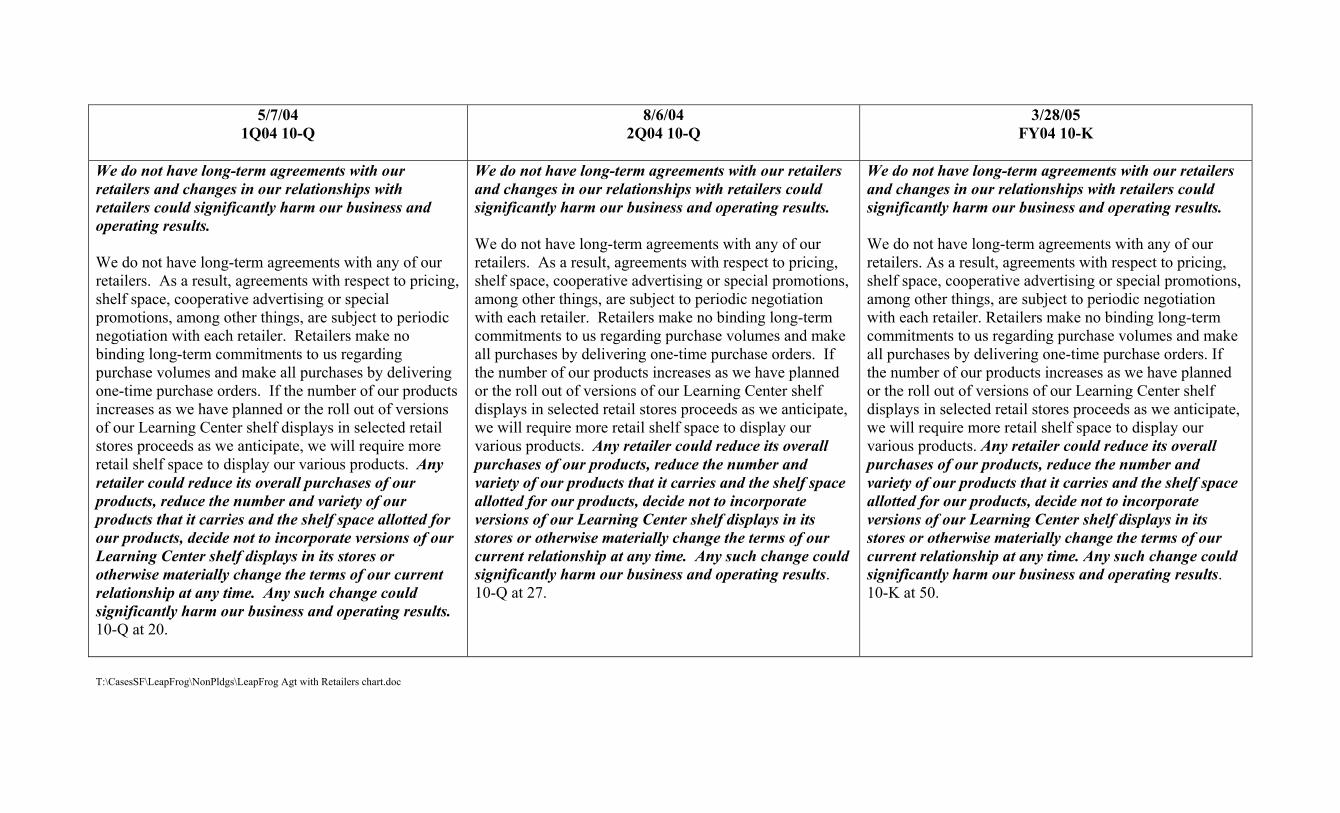

This Document Relates To:

ALL ACTIONS.

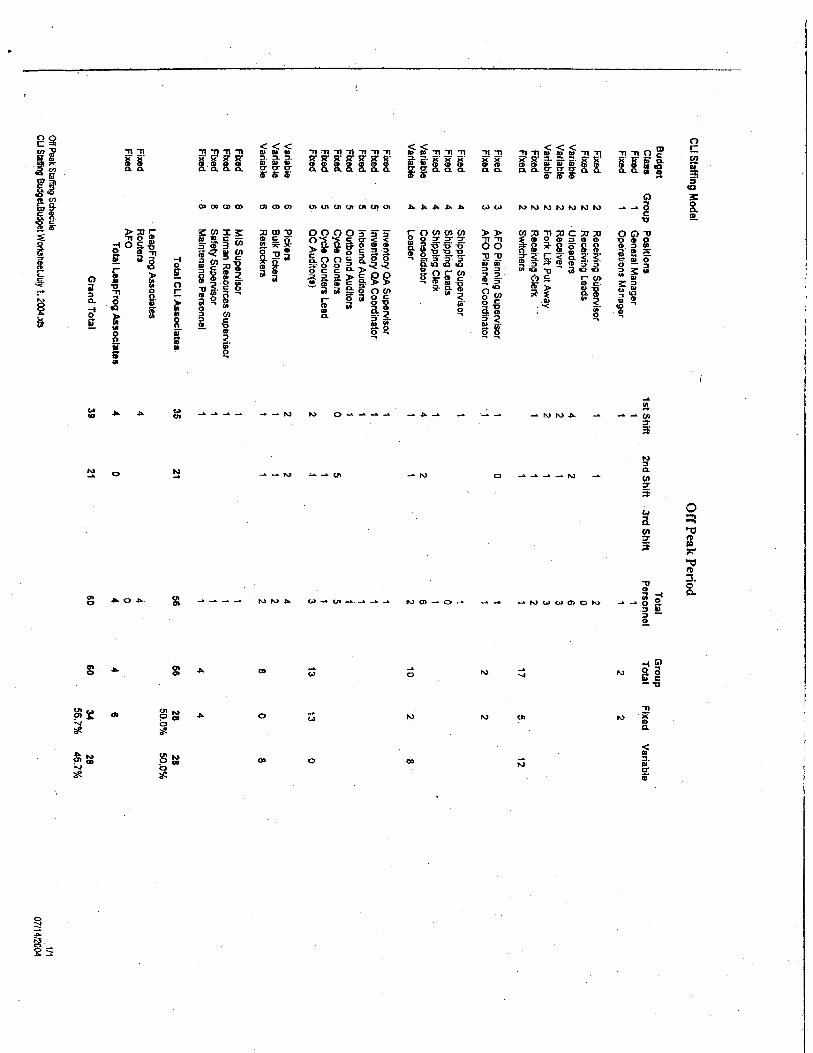

) ) ) ) ) ) ) )

No. C-03-05421-RMW

CLASS ACTION

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS

DEMAND FOR JURY TRIAL

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 1 of 135

TABLE OF CONTENTS

Page

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW

- i -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

INTRODUCTION ...........................................................................................................................1

JURISDICTION AND VENUE ......................................................................................................4

THE PARTIES.................................................................................................................................4

CONFIDENTIAL WITNESSES ...................................................................................................10

FACTS SHOWING DEFENDANTS’ KNOWLEDGE OF..........................................................13

MATERIAL ADVERSE INFORMATION ..................................................................................13

A. Defendants Knew There Were Several Material Risks that Could Adversely Effect LeapFrog’s Business and Operating Results .............................13

B. Defendants Knew There Were Numerous Problems with LeapFrog’s Distribution and Supply-chain Operations.............................................................16

1. Defendants Knew DSS Repeatedly Failed to Fulfill Customer Orders Which Caused the Sales Shortfall in 3Q03 and Other Problems ....................................................................................................18

2. Defendants Knew LeapFrog Cancelled the Implementation of Supply-Chain Software Before 3Q03 that Was Needed to Accurately Forecast Customer Demand and to Assure Sufficient Levels of Inventory to Meet Customer Demand........................................20

3. Defendants’ Failed Scheme to Fabricate Sales to Avoid the 3Q03 Shortfall......................................................................................................21

4. Defendants Knew that Delays in Consolidating Warehouse Operations, Changing Warehouse Providers and Implementing Supply-Chain Software Caused the Distribution and Supply-Chain Problems to Continue in 4Q03 and 2004...................................................22

5. Defendants Knew the Distribution and Supply-Chain Problems Caused LeapFrog to Report Materially False and Misleading Financial Results that Were Not Prepared in Accordance with GAAP or the Company’s Publicly Reported Accounting Policies............31

a. Improper Revenue Recognition .....................................................31

b. Failure to Accurately Report Inventories.......................................33

c. Understatement of Expenses and Liabilities..................................36

6. After the Class Period, Defendants Admitted There Were Numerous Material Weaknesses in LeapFrog’s Distribution and Supply-Chain Operations that Prevented the Company from Accurately Forecasting Results and from Reporting the Company’s Financial Results in Accordance with GAAP............................................37

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 2 of 135

Page

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS - CLASS ACTION

- ii -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

C. Defendants Knew that Mattel’s Competing PowerTouch Product Had Caused LeapFrog to Lose Sales and Lower Prices while they Falsely Told Investors that Mattel’s PowerTouch Product Was Only a Potential Risk to LeapFrog’s Sales....................................................................................................39

D. Defendants Knew that LeapFrog’s Results Were Dependant on a Few Customers that Were Deferring Orders to Reduce Their Levels of LeapFrog Inventory and Reducing Their Purchases Due to the Problems with LeapFrog’s Distribution and Supply-Chain Operations ................................48

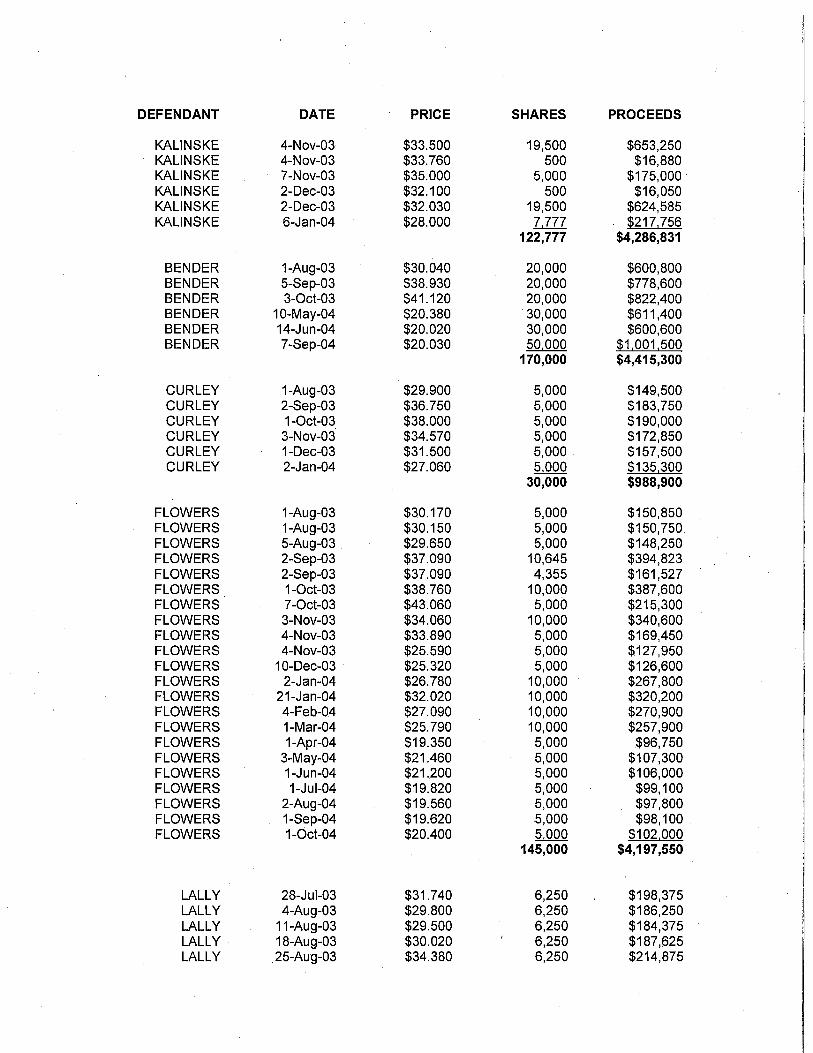

E. Defendants Received Millions of Dollars in Proceeds from Their Sales of LeapFrog Stock While Making Material Misrepresentations and Concealing Material Adverse Information from Investors....................................51

DEFENDANTS’ FALSE AND MISLEADING STATEMENTS ................................................53

ISSUED DURING THE CLASS PERIOD ...................................................................................53

A. False and Misleading Statements Between 7/24/03 and 10/20/03: Defendants Falsely Assure Investors There Are No Impediments to LeapFrog Meeting 3Q03 Guidance, Include Materially False and Misleading Risk Factors in the Company’s 2Q03 10-Q and Downplay the Impact of the PowerTouch.....................................................................................53

B. False and Misleading Statements Between 10/21/03 and 2/9/04: Defendants Cause LeapFrog to Report False and Misleading Financial Results in 3Q03, Falsely Assure Investors that the Distribution and Supply-Chain Problems that Caused the 3Q03 Revenue Shortfall Were Fixed, and Include False and Misleading Risk Factors in the Company’s 3Q03 10-Q .............................................................................................................67

C. False and Misleading Statements Between 2/10/04 and 3/9/04: Defendants Falsely Portray Management Changes, Cause LeapFrog to Report False and Misleading Financial Results for 4Q03 and FY03 and Provide Investors with Guidance for 2004 that They Knew LeapFrog Could Not Meet .......................................................................................................................78

D. False and Misleading Statements Between 3/10/04 and 4/20/04: Defendants Lose All Credibility by Preannouncing 1Q04 Results Just One Month After Providing Initial Guidance but Assure Investors the Supply-Chain Operations Are Being Strengthened and Include Materially False and Misleading Financial Results and Risk Factors in the Company’s FY03 10-K .............................................................................................................86

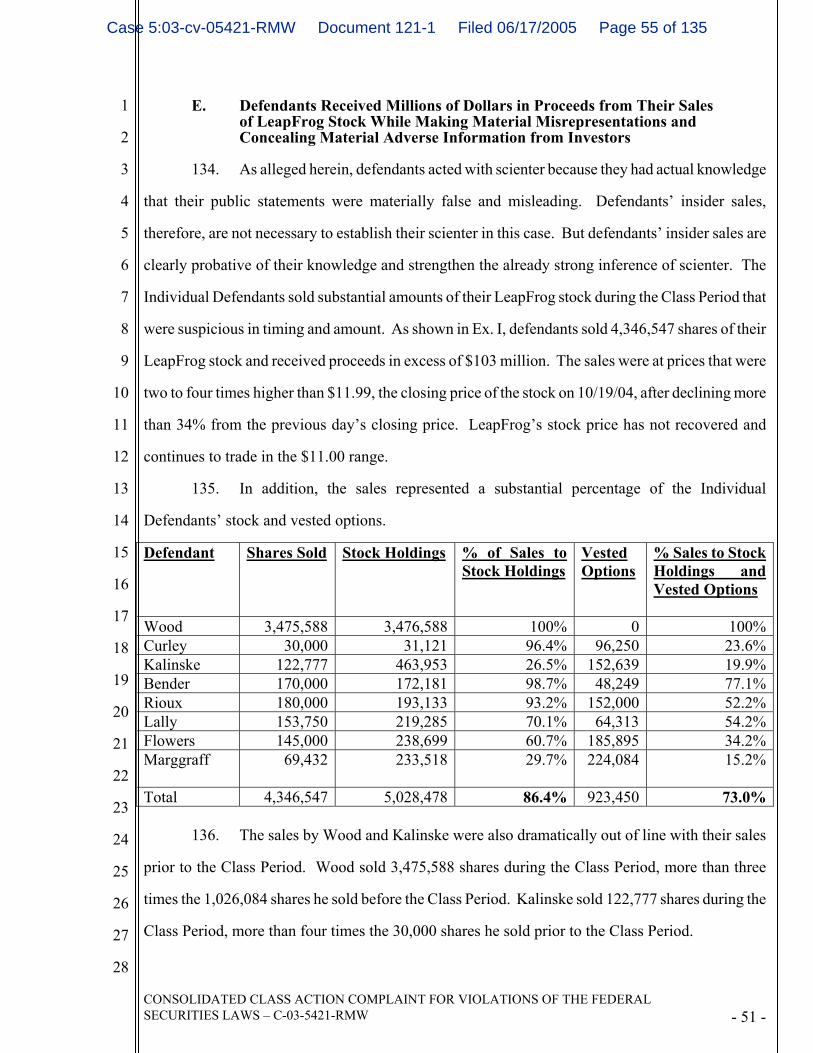

E. False and Misleading Statements Between 4/21/04 and 7/20/04: Defendants Cause LeapFrog to Report False and Misleading Financial Results for 1Q04 and Include Materially False and Misleading Risk Factors in the Company’s 1Q04 10-Q ...................................................................93

F. False and Misleading Statements Between 7/21/04 and 10/18/04: Defendants Cause LeapFrog to Report False and Misleading Financial

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 3 of 135

Page

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS - CLASS ACTION

- iii -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Results for 2Q04 and Include Materially False and Misleading Risk Factors in the Company’s 2Q04 10-Q .................................................................101

THE END OF THE CLASS PERIOD AND POST CLASS PERIOD .......................................112

EVENTS FURTHER DEMONSTRATING DEFENDANTS’ FRAUD ....................................112

LEAPFROG’S FALSE FINANCIAL REPORTING ..................................................................117

DURING THE CLASS PERIOD ................................................................................................117

A. LeapFrog’s Improper Revenue Recognition and Failure to Adequately Reserve for Accounts Receivable with Doubtful Collectibility ..........................118

B. LeapFrog’s Improper Accounting for Inventory .................................................119

C. LeapFrog’s Failure to Report Expenses Related to Goods and Services Purchased from Its Vendors.................................................................................120

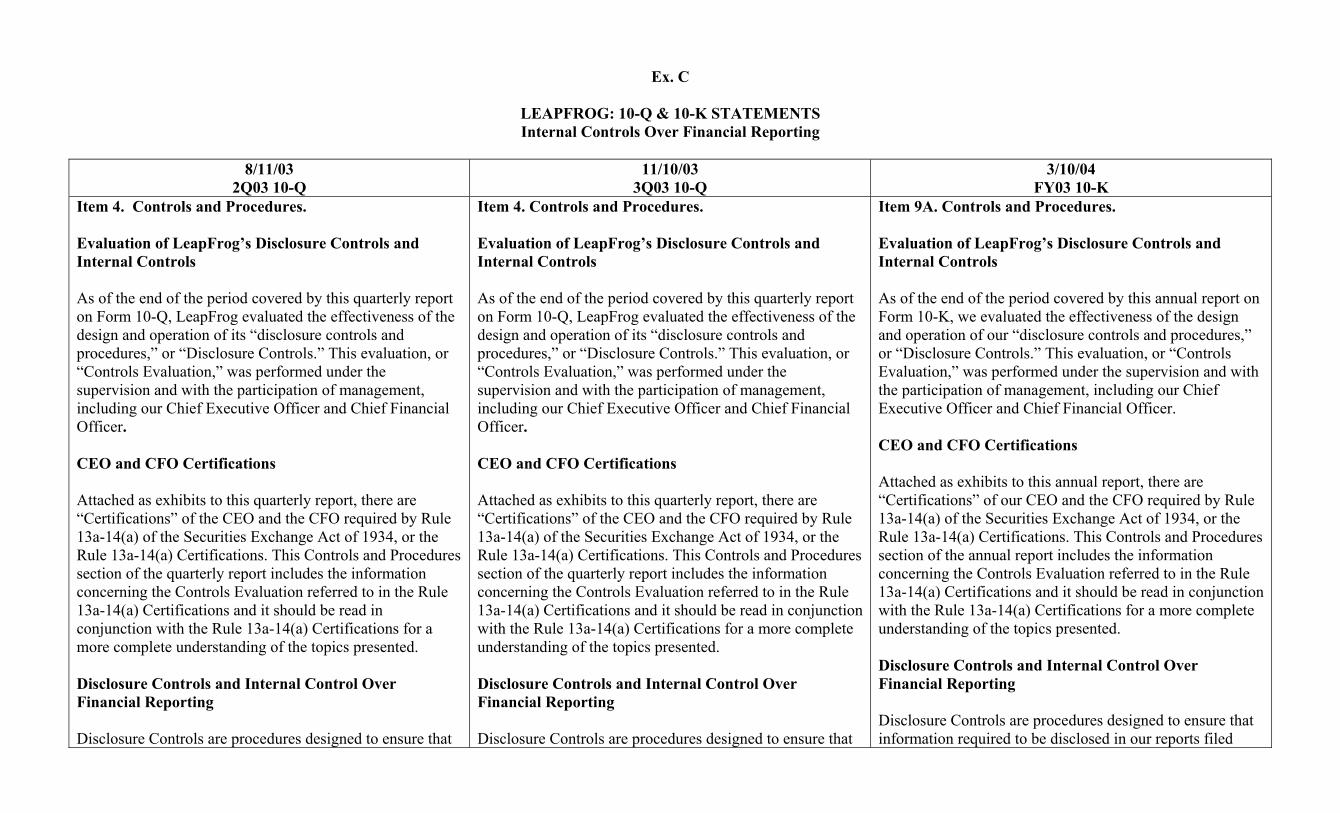

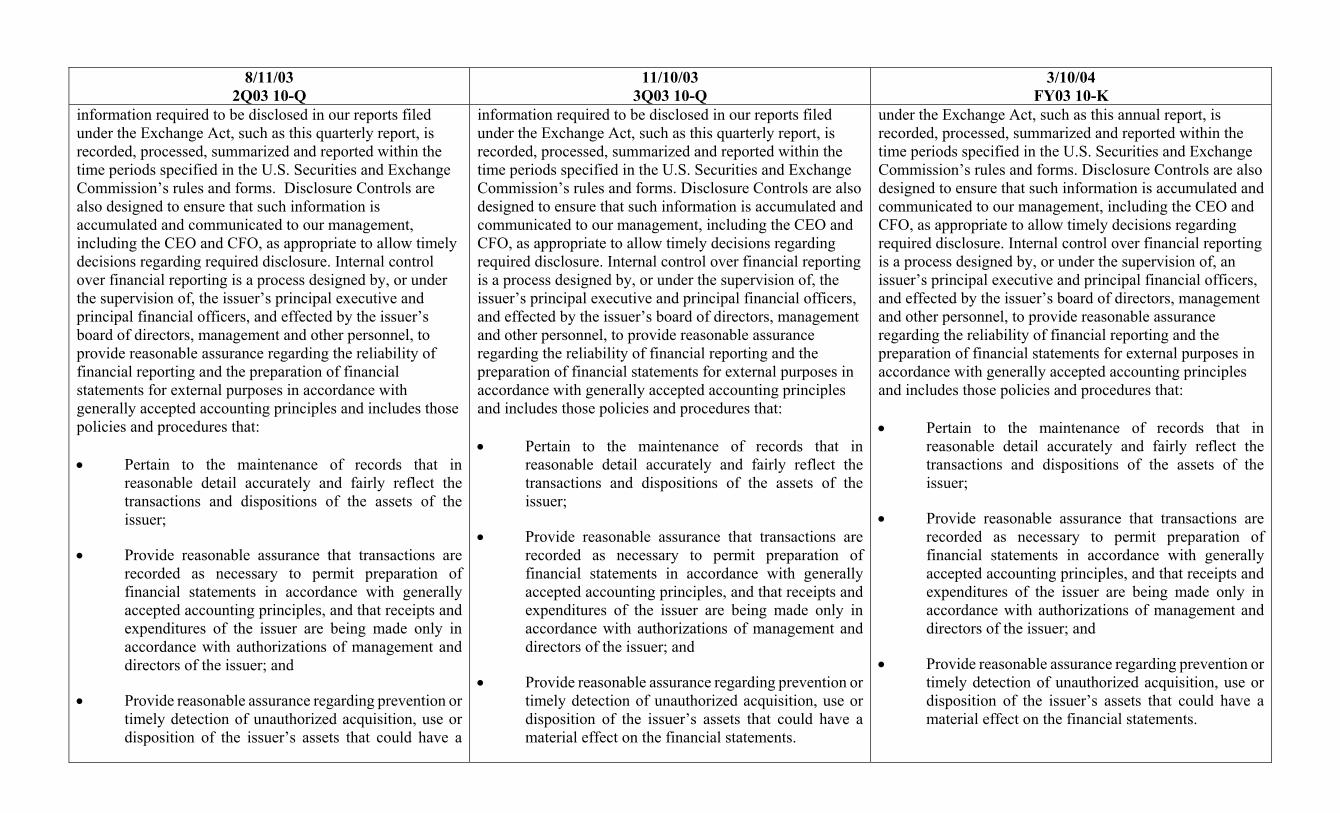

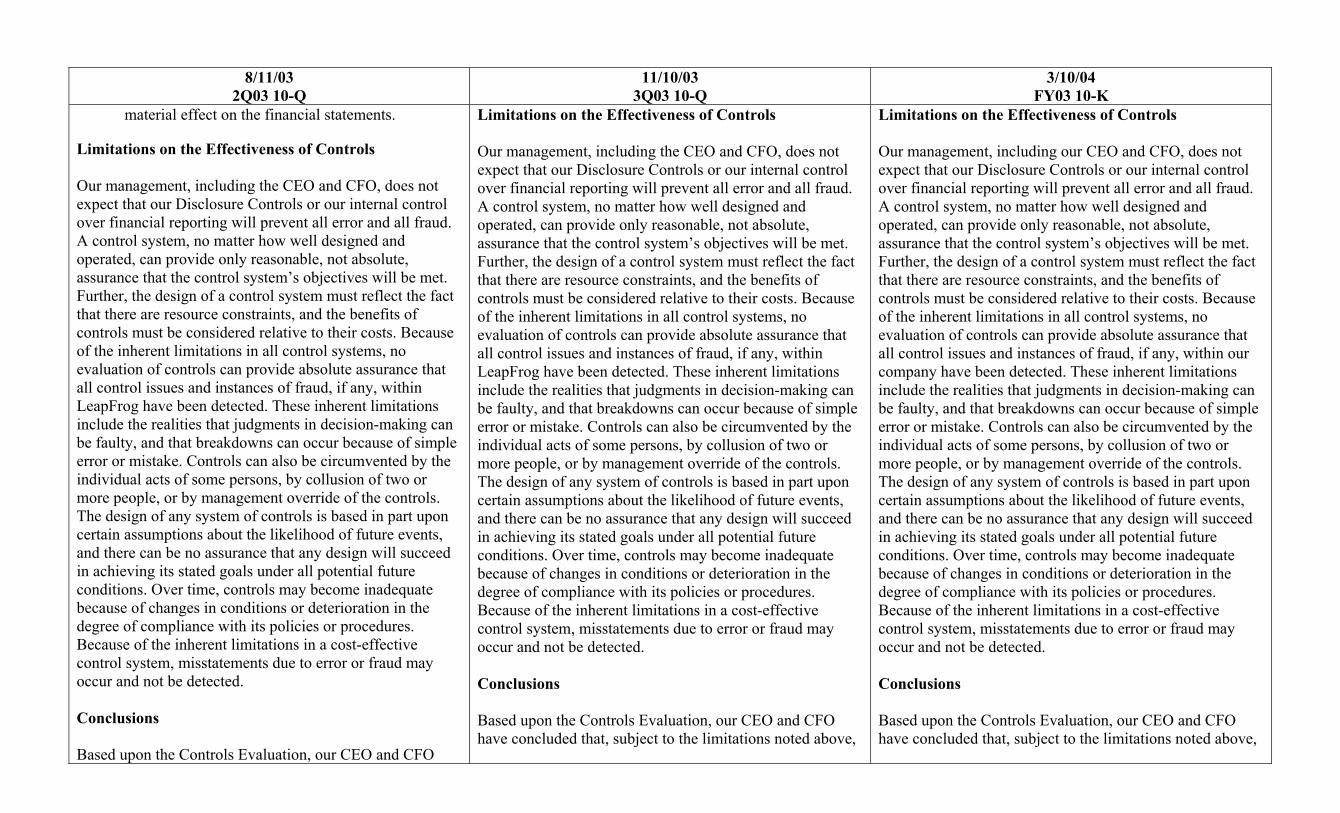

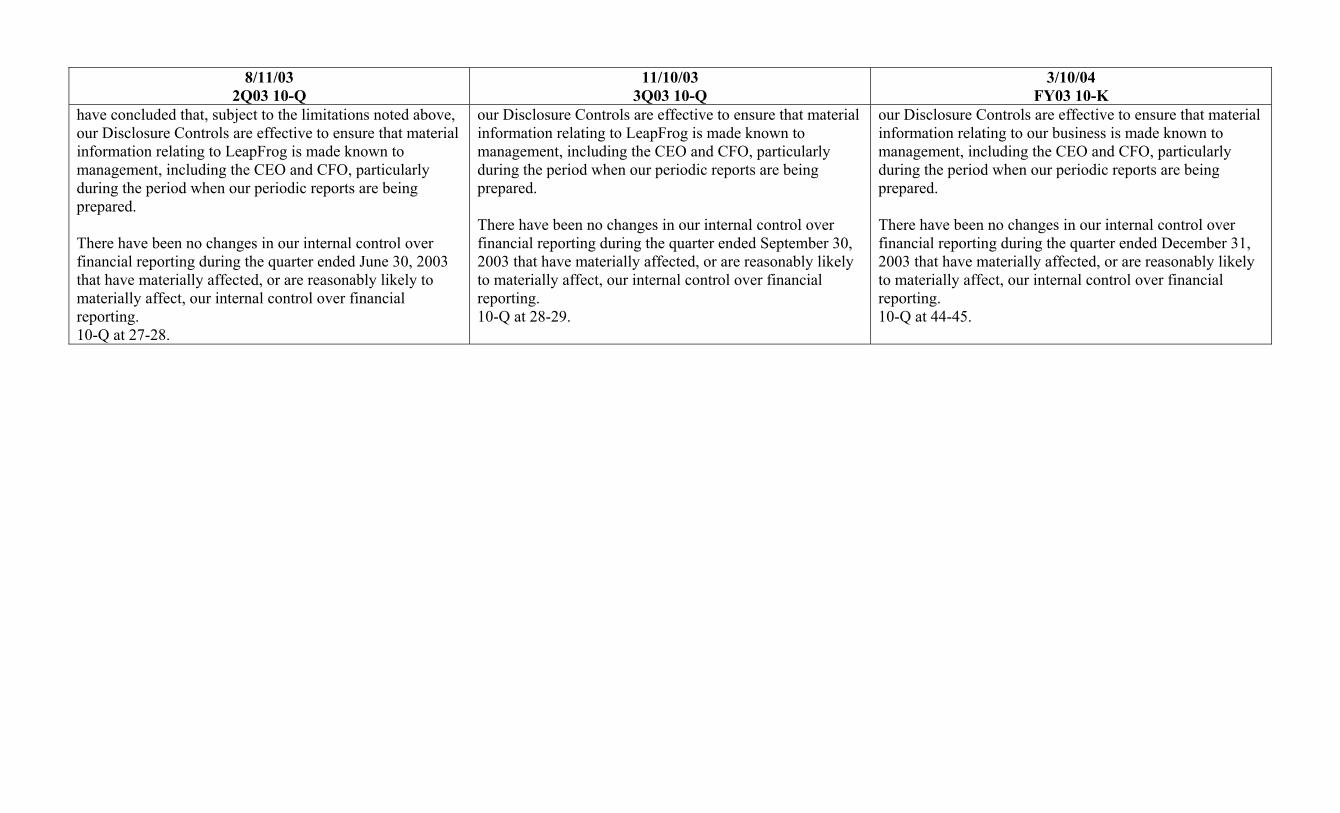

D. Defendants’ False Representations and Certifications that LeapFrog’s Financial Reporting Was Reliable, LeapFrog’s Financial Statements Were Prepared in Accordance with GAAP and that LeapFrog’s Disclosure Controls and Internal Controls over Financial Reporting Were Effective ..........120

E. Additional Violations of GAAP and SEC Regulations .......................................121

PROXIMATE LOSS CAUSATION ...........................................................................................123

CLASS ACTION ALLEGATIONS ............................................................................................124

FIRST CLAIM FOR RELIEF .....................................................................................................125

For Violation of §10(b) of the 1934 Act and Rule 10b-5 Against All Defendants .....................125

SECOND CLAIM FOR RELIEF ................................................................................................126

For Violation of §20(a) of the 1934 Act Against All Defendants ...............................................126

PRAYER FOR RELIEF ..............................................................................................................126

JURY DEMAND.........................................................................................................................127

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 4 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 1 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

INTRODUCTION

1. This is a securities class action on behalf of all persons who purchased the class A

common stock and options of LeapFrog Enterprises, Inc. (“LeapFrog” or the “Company”) between

7/24/03 and 10/18/04 (the “Class Period”), against LeapFrog and certain of its officers and directors

for violations of the Securities Exchange Act of 1934 (the “1934 Act”).

2. LeapFrog is a designer, developer and marketer of technology-based educational

products and related proprietary content, which are marketed both through retail outlets as

educational “toys” and to schools as learning devices. LeapFrog’s biggest retail product is its family

of LeapPad products which are hand-held or lap-held electronic platform devices marketed with a

variety of content books that use a game and entertainment technology to teach reading, writing and

math skills to children. The Company went public on 7/24/02, selling 9.96 million shares (including

1.35 million shares to cover over-allotments) of class A common stock at $13 per share. Before the

Class Period, LeapFrog grew rapidly, consistently reported quarterly revenues and earnings that

exceeded consensus analyst estimates and defendants told investors that sales and earnings growth

would continue in 2003 and 2004. Thus, defendants knew the market expected LeapFrog to report

increasing future sales and earnings at the beginning of the Class Period.

3. Defendants also knew that there were several impediments to the Company reporting

increasing sales and earnings. They knew the Company’s sales were increasingly dependant on

three U.S. retail customers – Wal-Mart Corporation (“Wal-Mart”), Toys R Us Inc. (“Toys R Us”)

and Target Corporation (“Target”) – who accounted for more than two-thirds of total sales. In

addition, they knew LeapFrog did not have long term agreements with the retailers who were

delaying orders to reduce inventory levels. As a result, the Company had to fill orders and supply

product to these retailers within shorter time periods. This was a particular challenge to LeapFrog

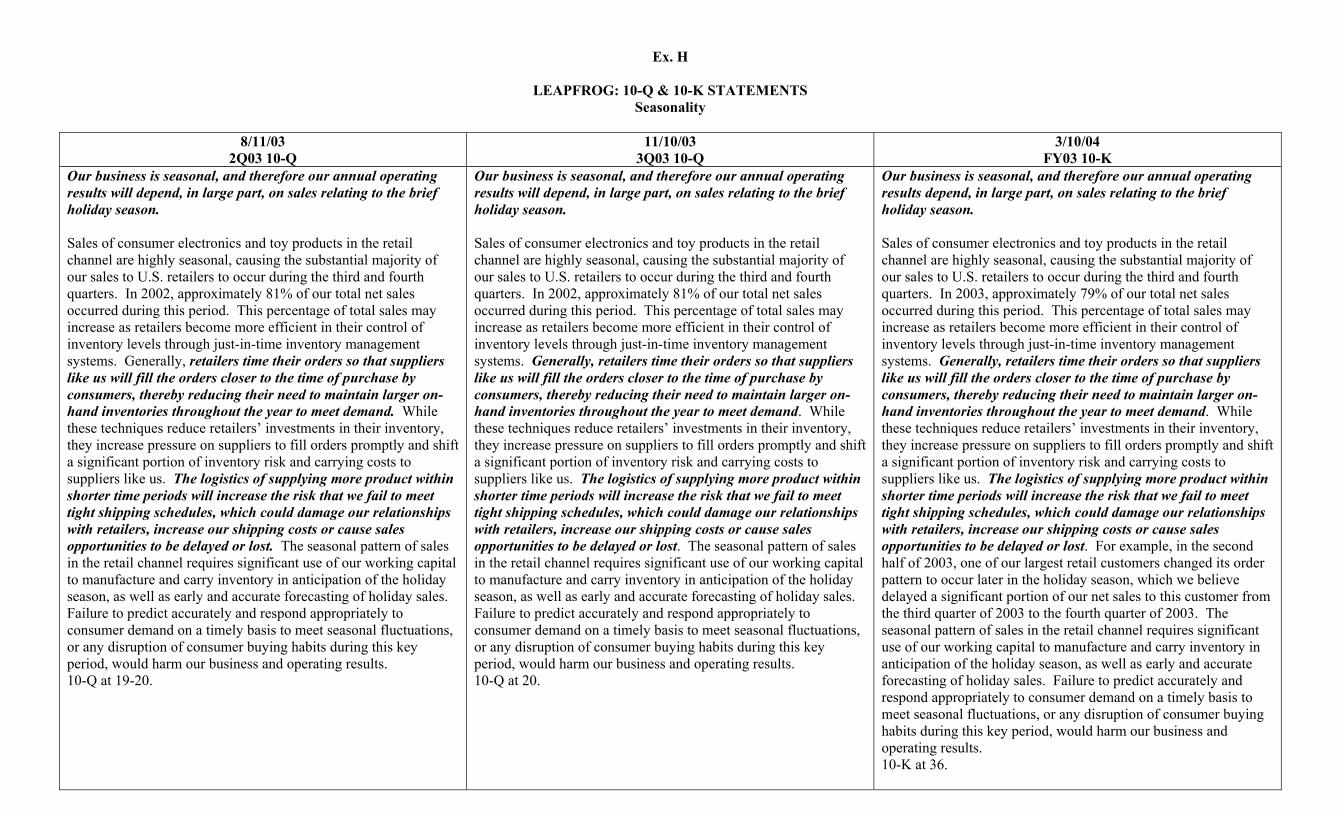

because the second half of the year was the peak back-to-school and holiday selling season for

LeapFrog (and other toy makers) when the Company generated 80% of its sales. Further, defendants

knew LeapFrog’s distribution warehouses were managed by third parties – DSS until it was replaced

by Commodity Logistics West, Inc. (“CLI”) in 7/04 – who were responsible for delivering product to

the Company’s retail customers within the shorter time periods.

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 5 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 2 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

4. Defendants also knew that LeapFrog had suspended implementation of new supply-

chain software designed to, among other things, ensure LeapFrog had sufficient levels of inventory

to meet actual and forecasted orders from the Company’s retail customers. In addition to the

distribution and supply-chain challenges, defendants knew that LeapFrog, which had no meaningful

competition prior to 7/03, now faced competition from Mattel, Inc.’s (“Mattel”) PowerTouch

product which was Mattel’s largest product launch in the company’s 73-year history.

5. As detailed herein, defendants misled investors by making numerous false and

misleading statements about LeapFrog’s current and future business results, concealing numerous

problems with the Company’s distribution and supply-chain operations that prevented the Company

from shipping product to its retail customers, concealing the fact that LeapFrog was losing millions

of dollars in sales and profits to Mattel’s competing PowerTouch product, and selling 4.3 million

shares of their class A stock at artificially inflated prices for more than $103 million.

6. As explained below, defendants knew that DSS and CLI were unable to ship product

within the required shorter time periods and that DSS and CLI shipped product to LeapFrog’s

customers that they had not ordered and would not pay for. Due to the shipping problems,

defendants also knew LeapFrog reported inflated revenues, earnings, receivables and inventories in

violation of Generally Accepted Accounting Principles (“GAAP”) and the Company’s publicly

reported revenue recognition policy which only permitted revenue to be recognized upon shipment if

collection was reasonably assured.

7. In addition, defendants knew that the distribution and supply-chain problems were

damaging LeapFrog’s relationship with the retail customers who comprised a majority of the

Company’s sales. They knew the retail customers continually complained about the repeated failure

to accurately fulfill orders or deliver products on time, and that the retail customers reduced their

purchases of the Company’s products and imposed millions of dollars in “vendor violation” penalties

when the problems were not solved.

8. Compounding the distribution and supply-chain problems was the fact that LeapFrog

was losing millions of dollars in sales and profits to Mattel and other competitors. Defendants

downplayed Mattel’s competing PowerTouch product (and other competition) and represented that

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 6 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 3 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

the Company’s sales and market share would actually increase. In the Company’s Securities and

Exchange Commission (“SEC”) filings, defendants represented that sales and market share could

decline if LeapFrog was unable to compete effectively with existing or new competitors, including

Mattel’s PowerTouch. LeapFrog’s patent infringement suit against Mattel, however, shows that

defendants misled investors by representing that a decline in sales and market share was only a

possibility. Defendants knew, as shown by their sworn testimony and pleadings filed in LeapFrog’s

patent infringement suit against Mattel, that sales of the PowerTouch caused LeapFrog’s market

share to decline 25%. Specifically, LeapFrog “drastically reduced” prices of LeapPad platforms and

to lose more than one million sales of LeapPad platforms and more than 2.9 million sales of content

books used with the platforms. Indeed, defendants have admitted that LeapFrog lost approximately

$85 million in profits – substantially more than the $66.2 million of profits LeapFrog reported in

2003 and 2004 combined.

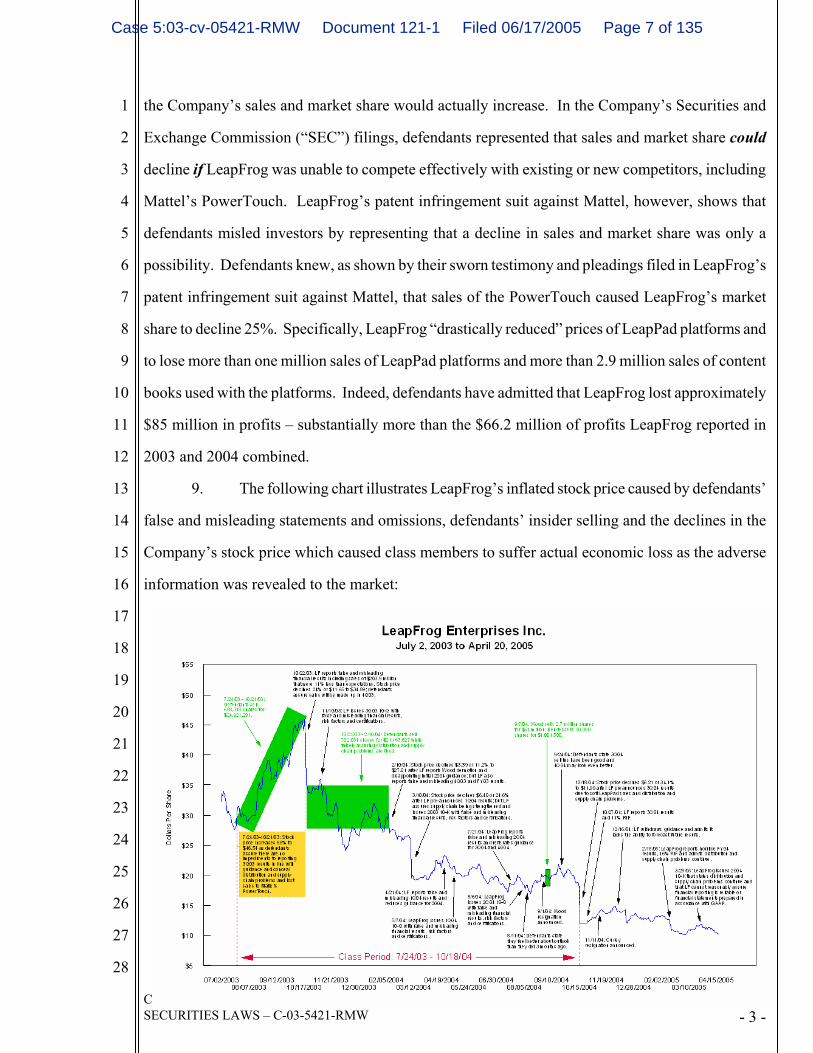

9. The following chart illustrates LeapFrog’s inflated stock price caused by defendants’

false and misleading statements and omissions, defendants’ insider selling and the declines in the

Company’s stock price which caused class members to suffer actual economic loss as the adverse

information was revealed to the market:

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 7 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 4 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

JURISDICTION AND VENUE

10. Jurisdiction is conferred by §27 of the 1934 Act. The claims asserted herein arise

under §§10(b) and 20(a) of the 1934 Act and Rule 10b-5.

11. (a) Venue is proper in this District pursuant to §27 of the 1934 Act. Many of the

false and misleading statements were made in or issued from this District.

(b) The Company’s principal executive offices are in Emeryville, California,

where the day-to-day operations of the Company are directed and managed.

THE PARTIES

12. Lead plaintiffs are William Sullivan and Alice Cupples. Each of these class members

purchased LeapFrog’s class A common stock at artificially inflated prices during the Class Period.

13. Defendant LeapFrog is a designer, developer and marketer of technology-based

educational products and related proprietary content, which are marketed both in retail stores and to

schools. During the Class Period, LeapFrog reported between 26.3 million and 33.2 million shares

of outstanding class A common stock which were traded on the New York Stock Exchange and

between 27.6 million and 31.6 million shares of class B common stock which were privately held.

According to the Company’s 2003 10-K, LeapFrog had 869 full time employees, including 11

executive officers. All of the Individual Defendants were executive officers.

14. According to the Company’s Reports on Form 10-K and Proxy Statements, defendant

Michael C. Wood (“Wood”) founded LeapFrog in 1995, served as President and Vice Chairman

since 9/97 and as Chief Executive Officer (“CEO”) from 3/02 until 2/04 when he was demoted to

Chief Vision and Creative Officer. Wood was forced out of the Company in 9/04. According to the

Company’s Amended and Restated Bylaws, as President and CEO, Wood was the senior most

officer of the Company and responsible for the general supervision, direction and control of the

business and its officers. According to the Amended and Restated Employment Agreement between

Wood and LeapFrog, Wood was responsible for managing the day-to-day operations of the

Company, supervising staff, and developing programs. The Amended Employment Agreement also

stated Wood was a “key executive” of the Company whose services were material and significant to

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 8 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 5 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

LeapFrog’s success and placed Wood in a position of confidence and trust which allowed him access

to confidential information.

(a) The false and misleading statements alleged herein were made by or are

attributable to Wood. Wood participated in the preparation of the Company’s press releases, many

of which included quotes by Wood. Before his demotion to Chief Vision and Creative Officer, he

participated in the Company’s quarterly earnings conference calls on 7/24/03, 10/22/03 and 2/11/04.

Wood signed the Company’s 2Q03 10-Q filed on 8/11/03, the 3Q03 10-Q filed on 11/10/03 and the

FY03 10-K filed on 3/10/04.

(b) According to the Company’s Proxy Statements and the Amended and

Restated Employment Agreement between Wood and LeapFrog, Wood received a salary of

$277,100 in 2003 and a salary of $239,321 in 2004 prior to his forced resignation in 9/04.

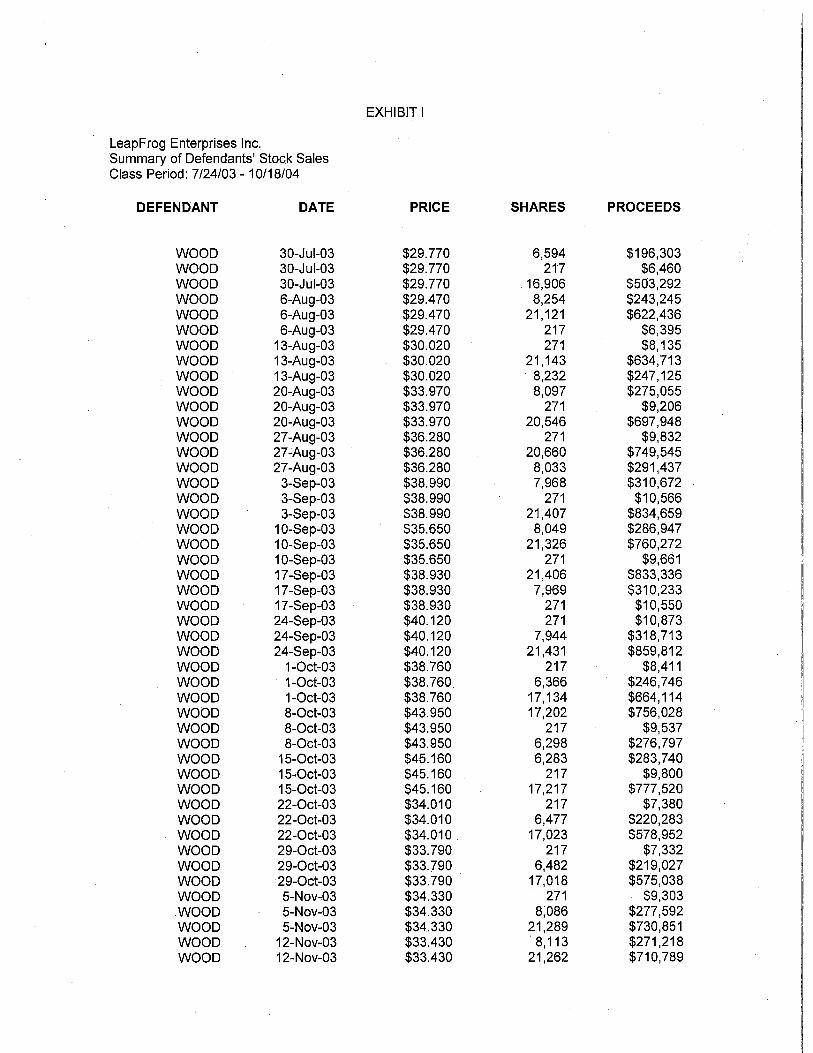

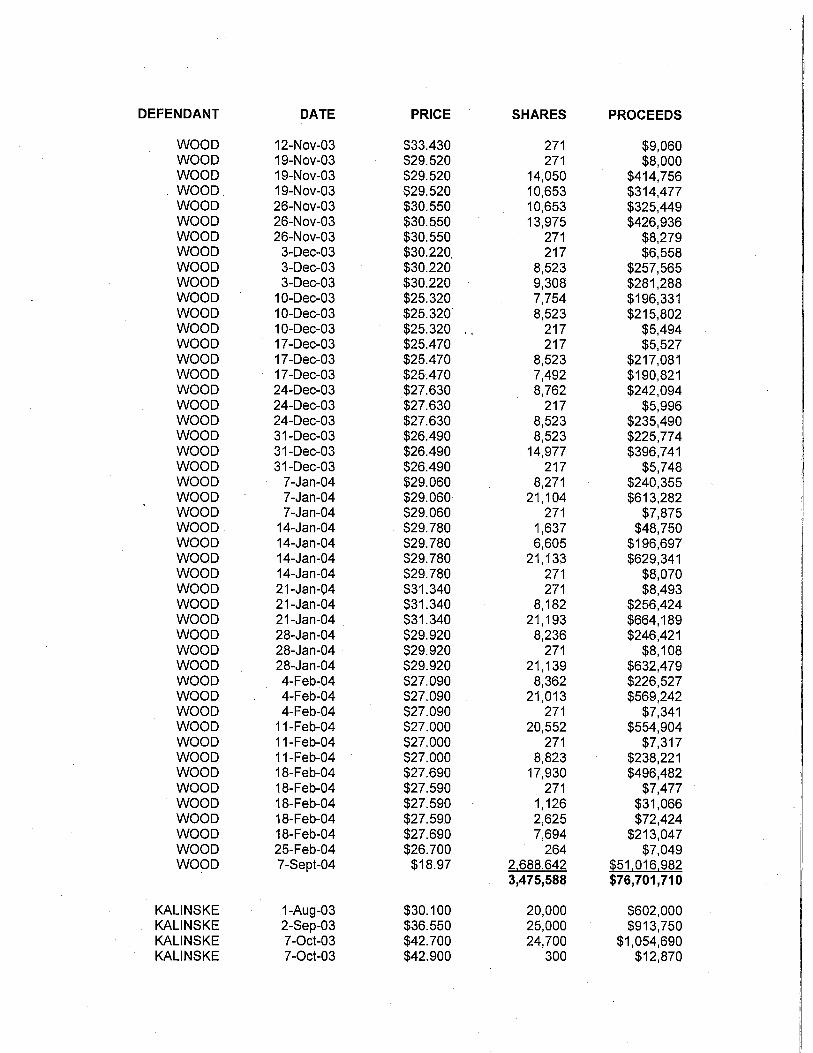

(c) During the Class Period, Wood sold substantial amounts of his LeapFrog class

A common stock that were suspicious in timing and amount. Wood sold 3,475,588 shares, or 100%

of his class A common stock and vested options during the Class Period at inflated prices for

$76,701,710. His sales during the Class Period were dramatically out of line with prior trading

practices. Prior to the Class Period, Wood sold 1,026,084 shares for proceeds of $25,157,492.

Wood’s sales during the Class Period were at prices ranging from $25.32 to $45.16 – two to four

times higher than the $11.99 price the stock traded at on 10/19/04.

15. According to the Company’s Reports on Form 10-K and Proxy Statements, defendant

Thomas J. Kalinske (“Kalinske”) was the Chairman of the LeapFrog Board of Directors since 9/97

and was CEO from 9/97 to 3/02, when Wood became CEO. Kalinske reassumed the position of

CEO in 2/04 when Wood was demoted to Chief Vision and Creative Officer. Since 1996, Kalinske

has also served as President of Knowledge Universe, Inc., LeapFrog’s parent corporation.

According to the Company’s Amended and Restated Bylaws, as CEO, Kalinske was the senior most

officer of the Company and responsible for the general supervision, direction and control of the

business and its officers. According to the Employment Agreement between Kalinske and

LeapFrog, Kalinske’s services were deemed by the Company to be material and significant to

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 9 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 6 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

LeapFrog’s success and placed Kalinske in a position of confidence and trust which allowed him

access to confidential information.

(a) The false and misleading statements alleged herein were made by or are

attributable to Kalinske. Kalinske participated in the preparation of the Company’s press releases,

many of which included quotes by Kalinske. He participated in the Company’s quarterly earnings

conference calls on 2/11/04, 4/21/04, 7/21/04 and 10/18/04. He made presentations at the Bank of

America Securities 33rd Annual Investment Conference and the ThinkEquity Partners Conference

on 9/17/03. Kalinske signed the Company’s FY03 10-K filed on 3/10/04, the 1Q04 10-Q filed on

5/7/04 and the 2Q04 10-Q filed on 8/6/04.

(b) According to the Company’s Proxy Statements and the original Employment

Agreement between Kalinske and LeapFrog, Kalinske received a salary of $269,000 in 2003. He

received a salary of $469,812 in 2004 after reassuming the job of CEO from Wood and entering into

a new Employment Agreement in 4/04.

(c) During the Class Period, Kalinske sold substantial amounts of his LeapFrog

class A common stock that were suspicious in timing and amount. Kalinske sold 122,777 shares, or

20% of his class A stock and vested options during the Class Period at inflated prices for $4,286,831.

His sales during the Class Period were dramatically out of line with prior trading practices. Prior to

the Class Period, Kalinske sold just 30,000 shares of his LeapFrog class A common stock.

Kalinske’s sales during the Class Period were at prices ranging from $28.00 to $42.90 – two to four

times higher than the $11.99 price the stock traded at on 10/19/04.

16. According to the Company’s Reports on Form 10-K and Proxy Statements, defendant

James P. Curley (“Curley”) was LeapFrog’s Chief Financial Officer (“CFO”) from 12/91 until

11/11/04, when he reportedly resigned. According to the Company’s Amended and Restated

Bylaws, as CFO, Curley was responsible for the financial reporting by LeapFrog.

(a) The false and misleading statements alleged herein were made by or are

attributable to Curley. Curley participated in the preparation of the Company’s press releases. He

participated in the Company’s quarterly earnings conference calls on 7/24/03, 10/22/03, 2/11/04,

4/21/04, 7/21/04 and 10/18/04. He made presentations at the Bank of America Securities 33rd

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 10 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 7 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Annual Investment Conference and the Think Equity Partners conference on 9/17/03. He signed the

Company’s 2Q03 10-Q filed on 8/11/03, the 3Q03 10-Q filed on 11/10/03, the FY03 10-K filed on

3/10/04, the 1Q04 10-Q filed on 5/7/04 and the 2Q04 10-Q filed on 8/6/04.

(b) According to the Company’s Proxy Statements Curley received a salary of

$258,125 in 2003. LeapFrog did not report his 2004 salary.

(c) During the Class Period, Curley sold substantial amounts of his LeapFrog

class A common stock that were suspicious in timing and amount. Curley sold 30,000 shares of his

LeapFrog class A common stock – 96.5% of his stock and 24% of his stock and vested options – at

inflated prices for $988,900. The sales were at prices ranging from $27.06 to $38.00 – two to three

times higher than the $11.99 price the stock traded at on 10/19/04.

17. According to the Company’s Reports on Form 10-K and Proxy Statements, defendant

Timothy M. Bender (“Bender”) was President, Worldwide Consumer Group of LeapFrog.

According to Bender’s 11/1/03 Employment Agreement, Bender reported to the President and CEO,

and was a key executive of LeapFrog whose services were deemed by the Company to be material

and significant to LeapFrog’s success, placing Bender in a position of confidence and trust which

allowed him access to confidential information.

(a) The false and misleading statements alleged herein were made by or are

attributable to Bender. Bender participated in the preparation of the Company’s press releases. He

participated in the Company’s quarterly earnings conference call on 7/24/03.

(b) According to the Company’s Proxy Statements, Bender received a salary of

$263,900 in 2003 and a salary of $283,900 in 2004.

(c) During the Class Period, Bender sold substantial amounts of his class A

common stock that were suspicious in timing and amount. Bender sold 170,000 shares of his class

A common stock, 98.7% of his stock and 77.1% of his stock and vested options, for $4,415,300.

The sales were at prices ranging from $20.02 to $41.12, two to four times the $11.99 price the stock

traded at on 10/19/04.

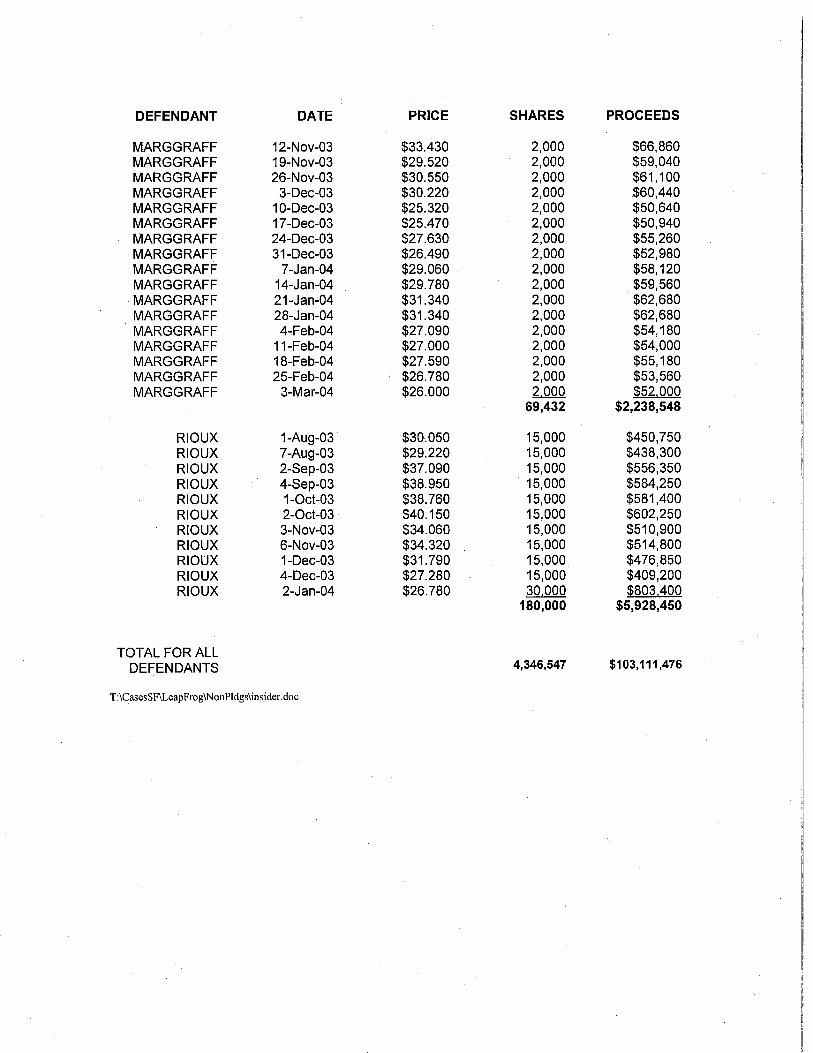

18. Defendant Paul A. Rioux (“Rioux”) was Co-Vice Chairman of the Board and a

director of LeapFrog since 1/01, LeapFrog’s acting Chief Operating Officer (“COO”) from 10/02 to

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 11 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 8 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

8/03, an advisor to the CEO, and Vice Chairman of the Board of Directors since 9/04. According to

the Employment Agreement between Rioux and LeapFrog, Rioux reported to the President of

LeapFrog and was a “key executive” of the Company whose services were material and significant

to LeapFrog’s success and placed Rioux in a position of confidence and trust which allowed him

access to confidential information. According to the Company’s Proxy Statements, Rioux

implemented LeapFrog’s planning, manufacturing and operating strategy in 2001 and 2002.

(a) The false and misleading statements alleged herein were made by or are

attributable to Rioux. He participated in the preparation of the Company’s press releases and signed

the 2003 10-K files on 3/10/04.

(b) According to the Company’s Proxy Statements, Rioux received a salary of

$374,000 in 2003, a salary of $307,300 in 2004 and a $47,250 bonus in 2004.

(c) During the Class Period, Rioux sold substantial amounts of his LeapFrog class

A common stock that were suspicious in timing and amount. Rioux sold 180,000 shares of his class

A common stock, 93.2% of his stock holdings and 52.2% of his stock holdings and vested options, at

inflated prices for $5,928,450. The sales were at prices ranging from $26.78 to $40.15, two to four

times higher than the $11.99 price the stock traded at on 10/19/04.

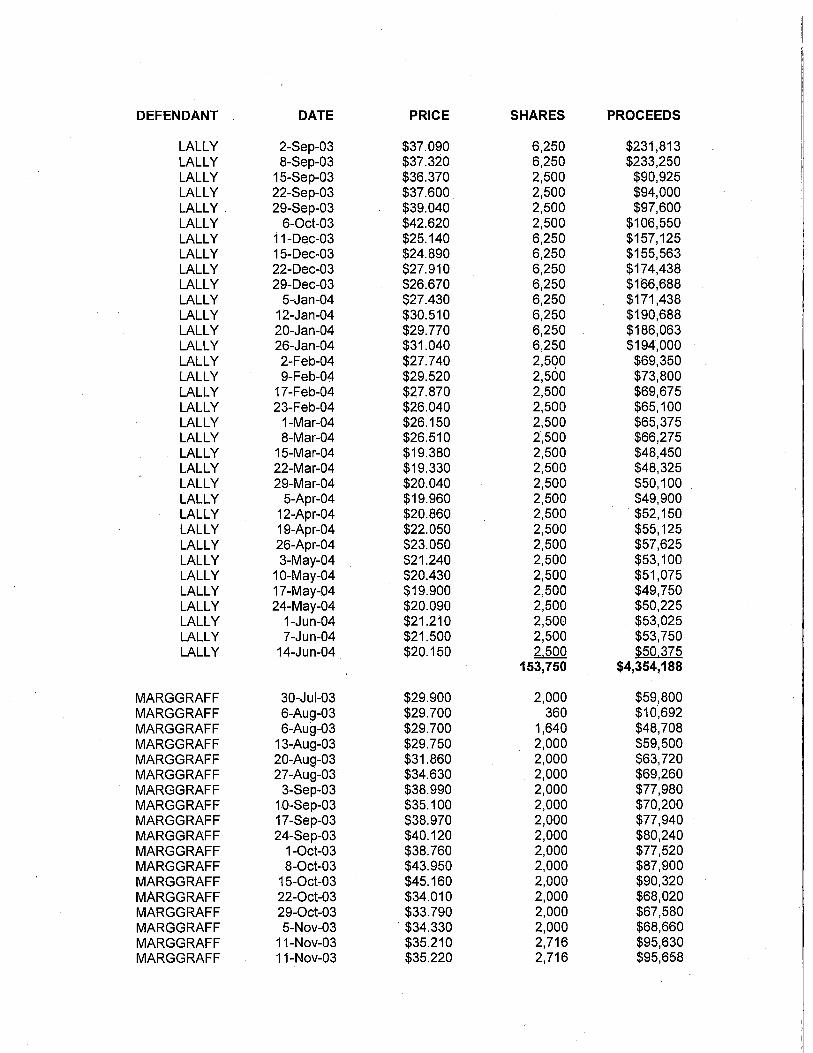

19. According to the Company’s Form 10-K, defendant James L. Marggraff

(“Marggraff”) was the Executive Vice President Worldwide Content of LeapFrog. During the Class

Period, Marggraff sold substantial amounts of his class A common stock that were suspicious in

timing and amount. Marggraff sold 69,432 shares of his LeapFrog class A common stock – 29.7%

of his stock and 15.2% of his stock and vested options – for $2,238,548.

20. According to the Company’s Form 10-K, defendant Mark B. Flowers (“Flowers”)

was the Executive Vice President, Chief Technology Officer of LeapFrog. During the Class Period,

Flowers sold substantial amounts of his class A common stock that were suspicious in timing and

amount. Flowers sold 145,000 shares of his LeapFrog class A common stock – 60.7% of his stock

and 34.2% of his stock and vested options – for $4,197,550.

21. According to the Company’s Form 10-K, defendant Robert W. Lally (“Lally”) was

the Executive Vice President, Education and Training Group and President, SchoolHouse Division

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 12 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 9 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

of LeapFrog until his forced resignation on 12/14/04. He participated in the Company’s 7/21/04

conference call. During the Class Period, Lally sold substantial amounts of his class A common

stock that were suspicious in timing and amount. Lally sold 153,750 shares of his LeapFrog class A

common stock – 70.1% of his stock and 54.2% of his stock and vested options – for $4,354,188.

22. The individuals named as defendants in ¶¶14-21 are referred to herein as the

“Individual Defendants.” The Individual Defendants, because of their positions with the Company,

possessed the power and authority to control the contents of LeapFrog’s quarterly reports, press

releases and presentations to securities analysts, money and portfolio managers and institutional

investors, i.e., the market. Each defendant was provided with copies of the Company’s reports and

press releases alleged herein to be misleading prior to or shortly after their issuance and had the

ability and opportunity to prevent their issuance or cause them to be corrected. Defendants regularly

received information on the status of LeapFrog’s sales, sales of Mattel’s PowerTouch and the

Company’s distribution and supply-chain operations. Bender testified in LeapFrog’s patent

infringement trial against Mattel that the Company (1) tracked sales of platforms, (2) tracked sales of

content books by platform and by year (the “tie ratio”), (3) tracked sales of Mattel’s competing

PowerTouch product, (4) conducted market research on the impact of Mattel’s competing

PowerTouch product on the market for educational toys, (5) tracked retail pricing of LeapFrog’s

products, (6) had 20-30 executive team meetings to discuss reducing the price of the LeapPad family

of platforms in response to the PowerTouch, and (7) had online access to look at retail inventory

levels for any item by store and by chain from which the Company prepared reports. Ex. A at 714-

15, 720-23, 730, 736-37. In addition, he testified that the Company tracked orders it was unable to

ship due to the distribution and supply-chain problems. Ex. A at 790-792.

23. Because of their executive positions and access to material non-public information

available to them but not to the public, each of these defendants knew that the adverse facts specified

herein had not been disclosed to and were being concealed from the public and that the positive

representations which were being made were then materially false and misleading. The Individual

Defendants are liable for the false statements pleaded herein at ¶¶143, 153, 160, 164, 166, 171, 177,

179, 183, 185 and 190, as those statements were each “group-published” information, the result of

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 13 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 10 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

the collective actions of the Individual Defendants. Moreover, when defendants sold their LeapFrog

stock, they had a duty to disclose adverse information that was not publicly available.

24. Each defendant is liable for (i) making false statements or (ii) failing to disclose

adverse facts known to him about LeapFrog in connection with his stock sales. Defendants’

fraudulent scheme and course of business that operated as a fraud or deceit on purchasers of

LeapFrog common stock was a success, as it (i) deceived the investing public regarding LeapFrog’s

prospects and business; (ii) artificially inflated the prices of LeapFrog’s common stock; (iii) allowed

defendants to arrange to sell and actually sell over $103 million worth of LeapFrog shares at

artificially inflated prices while in possession of material non-public information; and (iv) caused

plaintiffs and other members of the class to purchase LeapFrog common stock at inflated prices and

suffer economic loss when the inflation was removed from the stock price as defendants’ fraud was

revealed.

CONFIDENTIAL WITNESSES

25. Several of the allegations included herein are based on information provided by

several former LeapFrog employees referred to as confidential witnesses (“CW”). The information

provided by the former employees is reliable and credible because (1) each of the witnesses stated

they had personal knowledge of the information provided, (2) the witnesses worked at LeapFrog

during the Class Period, (3) the witnesses’ job titles and responsibilities show they had personal

knowledge of the information provided, (4) many of the witness accounts corroborate one another

and (5) the witness accounts are corroborated by other information alleged herein.

26. CW1 was an allocations analyst at LeapFrog from 6/03 through approximately 10/04,

when CW1 resigned. As an allocations analyst, CW1 was supposed to utilize the Company’s

supply-chain software to compare actual and projected levels of inventory against current and

forecasted customer orders to determine what products LeapFrog’s various customers were to

receive. As explained herein, however, CW1 was never able to perform the allocations analyst job

function because LeapFrog did not implement the necessary supply-chain software before CW1

resigned.

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 14 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 11 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

27. CW2 was a director of information technology at LeapFrog from 12/99 through

approximately 6/04, when CW2 resigned. During the Class Period, CW2 reported to John Casella,

LeapFrog’s Chief Information Officer, who reported to Curley and Director of Credit John Forsyth

(“Forsyth”). CW2 was involved in all aspects of LeapFrog’s IT infrastructure. As detailed below,

CW2 has personal knowledge about the delayed implementation of supply-chain software from

Manugistics, the problems with DSS, and the delay in transitioning from DSS to CLI.

28. CW3 was a manager of credit and collections at LeapFrog from 7/04 through 2/05,

when CW3 was laid-off as part of the Company’s 180-person reduction in force. CW3 reported to

Director of Credit Forsythe who reported to defendant Curley until Curley’s forced resignation in

11/04. CW3 was responsible for the day-to-day operations of the credit and collection department

including (1) the release of customer orders after performing credit checks, (2) collecting past due

accounts, and (3) resolving disputes with customers about amounts owed to LeapFrog. As detailed

below, CW3 has personal knowledge about LeapFrog improperly recognizing revenues and

overstating receivables due to problems with the Company’s distribution and supply-chain

operations that resulted in customers not receiving products they ordered and receiving products they

had not ordered.

29. CW4 was an accounts receivable specialist at LeapFrog from 11/00 through 11/04

when CW4 resigned. Like CW3, CW4 reported to Director of Credit Forsythe who reported to

defendant Curley until Curley’s forced resignation in 11/04. CW4 was responsible for invoicing

customers, tracking cash receipts from customers and analyzing chargebacks claimed by customers

against LeapFrog invoices. As detailed below, CW4 has personal knowledge that problems with the

Company’s distribution and supply-chain operations caused the sales shortfall in 3Q03. In addition,

CW4 stated that LeapFrog tried unsuccessfully to make up the 3Q03 sales shortfall by having DSS

prematurely ship product (due to be shipped to Toys R Us in 4Q03) from one of the Company’s

warehouses to an empty warehouse around the corner. However, the Company’s auditors discovered

the impropriety and required LeapFrog to reverse the revenue.

30. CW5 was a director of supply-chain finance and accounting, a contract position with

LeapFrog, from 7/04 through 2/05 when CW5 was laid-off as part of the Company’s 180-person

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 15 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 12 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

reduction in force. CW5 reported to Peter David (“David”), LeapFrog’s senior director of supply-

chain finance and accounting, who reported to Curley until Curley’s forced resignation in 11/04.

CW5 was very involved in the Company’s supply-chain operations. CW5 was responsible for

determining whether LeapFrog’s inventory was properly reported, including whether there was

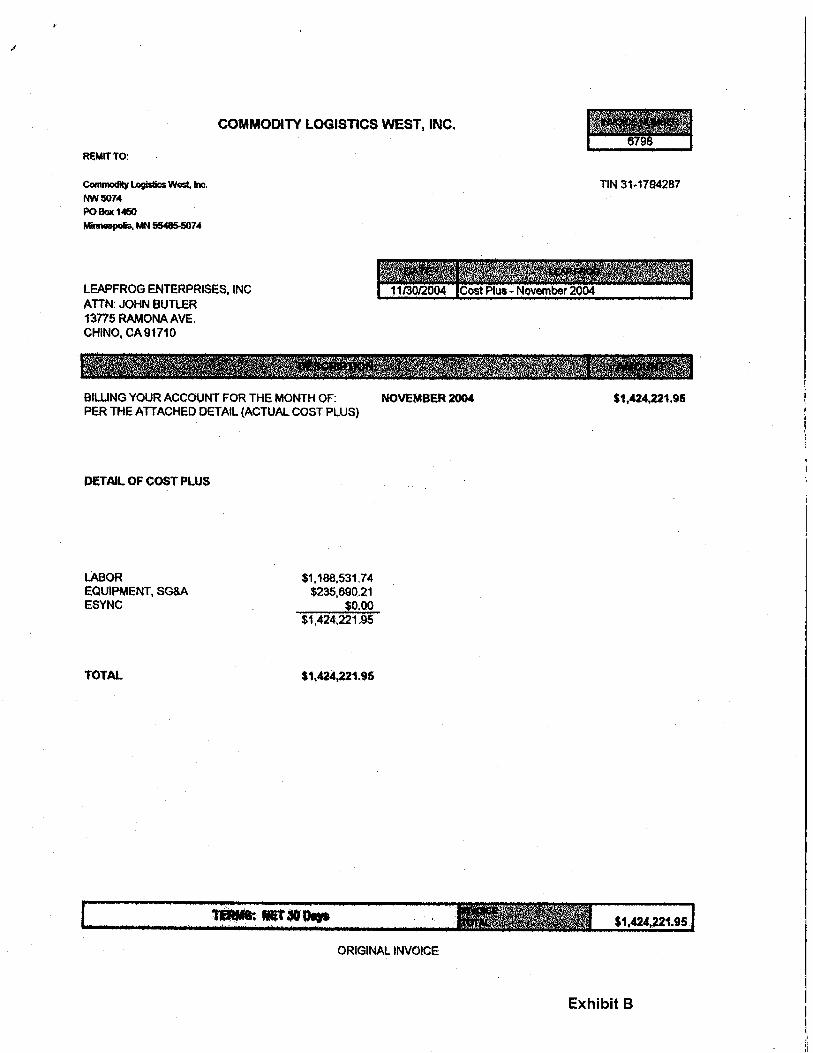

excess and obsolete inventory. CW5 was also responsible for reviewing the bills from CLI to ensure

the charges were valid and determining the amount to accrue and report on LeapFrog’s financial

statements. As detailed below, CW5 has personal knowledge about the delay in transitioning from

DSS to CLI until the peak selling season in 2004, why it was known that delay would cause

problems, CLI’s inability to deliver product to LeapFrog’s retail customers in accordance with the

customers’ purchase orders, and how those problems caused strained relations between LeapFrog

and its retail customers and between LeapFrog and CLI.

31. CW6 was an operations analyst at LeapFrog from 10/00 through 2/05 when CW6 was

laid-off as part of the Company’s 180-person reduction in force. CW6 worked on site at the

warehouse managed by DSS and provided support and assistance to John Gleason, LeapFrog’s

former Director of National Distribution. As detailed below, CW6 has personal knowledge of the

problems with DSS and problems caused by the delay in replacing DSS with CLI.

32. CW7 was an engineering procurement analyst at LeapFrog’s Los Gatos research and

development facility from 6/01 through 2/05 when CW7 was laid-off as part of LeapFrog’s 180-

person reduction in force. CW7 supported ten different engineering divisions (mechanical,

hardware, quality assurance, general R&D, software, manufacturing, concept, toy, documentation

and facilities) and was responsible for handling engineering purchases, coding budgets so they

would reconcile with general ledger accounts, data entry of purchase orders and fixing miscellaneous

problems that occurred in the procurement process. As explained herein, CW7 has personal

knowledge about LeapFrog incurring expenses related to the purchase of materials and components

used to manufacture and assemble products that were not reflected in the Company’s financial

statements because purchase orders were not created, approved or entered into the general ledger.

33. CW8 was a director of international distribution at LeapFrog from 1/02 until 11/04

when CW8 was laid off. Although CW8 was the director if international distribution, during the

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 16 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 13 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Class Period, CW8 was responsible for overseeing domestic and international distribution, including

distribution of products by DSS and CLI. CW8’s duties were expanded to oversee domestic

distribution because of the severe operational problems with DSS in 3Q03. CW8 reported to Andrew

Murrer (“Murrer”) who reported to G. Frederick Forsyth, LeapFrog’s COO. As detailed below,

CW8 has personal knowledge about the problems with DSS in 2003 and 2004, the problems caused

by the delay in replacing DSS with CLI until the peak selling season in 2004 and the problems

caused by the failure to implement supply-chain software before the peak selling season in 2004.

FACTS SHOWING DEFENDANTS’ KNOWLEDGE OF MATERIAL ADVERSE INFORMATION

A. Defendants Knew There Were Several Material Risks that Could Adversely Effect LeapFrog’s Business and Operating Results

34. LeapFrog is a designer, developer and marketer of technology-based educational

products and related proprietary content, which are marketed both in retail stores and to schools.

LeapFrog’s biggest retail product is its family of LeapPad products which are hand-held or lap-held

electronic platform devices which are marketed with a variety of content books that use a game and

entertainment technology to teach reading, writing and math skills. Prior to the Class Period,

LeapFrog reported substantial sales growth and enjoyed a near monopoly on the educational retail

electronic toy market until the beginning of the Class Period when Mattel introduced its competing

PowerTouch product. The financial press reported that LeapFrog had been “virtually unchallenged”

until Mattel introduced its competing PowerTouch product and the Company has admitted (in its

lawsuit against Mattel) that it had stable pricing and no meaningful competition before the

introduction of the PowerTouch. As a result, by 2003 LeapFrog was the third largest toy

manufacturer, only behind Hasbro, Inc. (“Hasbro”) and Mattel.

35. The Company operated in three business segments – U.S. Consumer, Education and

Training, and International. The majority of LeapFrog’s significant sales growth from 2001 through

2003, was in the U.S. Consumer business segment (in millions):

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 17 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 14 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

2001 2002 2003 2004

U.S. Consumer $289 (92%) $458 (86%) $546 (80%) $432 (67%) International $16.3 (5%) $53.6 (10%) $97 (14%) $153 (24%) Educational & Training

$8.8 (3%) $20.1 (4%) $38 (6%) $55 (9%)

Total $314.2 $532 $680 $640

36. Defendants knew as was reported in LeapFrog’s SEC filings that there were several

material risks that could adversely affect the Company’s financial results. Defendants knew that the

Company’s business and operating results were increasingly dependent on sales to Wal-Mart, Toys

R Us and Target as sales to those three retailers accounted for 80% of the Company’s U.S.

Consumer sales in 2002, 85% in 2003 and 95% in 2004. In every 10-Q and 10-K issued during the

Class Period, the Company warned that its business and operating results could be harmed if Wal-

Mart, Target or Toys R Us reduced their purchases of LeapFrog’s products.

37. Defendants also knew, as was disclosed in the Company’s SEC filings, that

LeapFrog’s results were dependant on its ability to ship product to Wal-Mart, Target and Toys R Us

in 3Q03 and 4Q03, the peak back-to-school and holiday selling seasons, when approximately 79% of

the Company’s sales and all of the Company’s earnings were realized. Further, the Company did not

have long term agreements with its retail customers who were reducing inventory levels by timing

their orders so that LeapFrog had to fill the orders closer to the time of purchase by consumers. As a

result, and as admitted by the Company in its SEC reports, the Company’s sales could decline,

shipping costs could increase and relationships with the retailers could be damaged if LeapFrog was

unable to ship product to its retail customers within the required shorter time periods.

38. The increased pressure to fill orders and supply product to retailers within shorter

time periods was particularly challenging to LeapFrog given the Company’s distribution and supply-

chain operations. LeapFrog outsourced substantially all of its finished goods manufacturing to

multiple companies in China and relied on four contract ocean carriers to ship the finished goods to

its primary distribution centers in California, which were managed by DSS until 7/04 when CLI took

over the management of the Company’s warehouse operations. DSS (and later CLI) was responsible

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 18 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 15 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

for ensuring the purchase orders from LeapFrog’s retail customers were fulfilled on time and

accurately.

39. Defendants also knew, as was disclosed in the Company’s SEC filings, that

LeapFrog’s operating results could suffer if it failed to develop and maintain management systems

that were sufficient to keep pace with the Company’s rapid growth. Specifically, defendants knew

that LeapFrog needed to implement supply-chain software that would allow the Company to

accurately forecast and fulfill retailer orders during the peak selling season by providing information

on actual and projected orders, inventory levels and manufacturing.

40. Defendants knew, as was reported in the Company’s SEC filings that LeapFrog’s

sales and market share could decline if the Company was unable to effectively compete with other

toy companies, particularly Mattel which launched the PowerTouch in 7/03.

41. In the four quarters that followed the 7/02 IPO, LeapFrog reported quarterly financial

results that exceeded consensus estimates and the Company’s stock price increased from $13 on the

date of the IPO to $34 on 7/8/03. For example, on 7/23/03, Merrill Lynch analyst Lauren Rich Fine

issued a Research Bulletin following LeapFrog’s release of its 2Q03 financial results entitled “LF

Bounds Past Estimates Again” which reported the Company’s earnings per share (“EPS”) was $0.08

better than consensus estimates and the “fourth consecutive quarter of large positive surprises.”

42. Ms. Fine and other analysts noted, however, that the price of the Company’s stock

had declined 17% over the past two weeks due to the shipping of Mattel’s competing PowerTouch

product, general industry retail softness and recent insider selling following the expiration of the

180-day lock-up period following LeapFrog’s 7/02 IPO. As a result, the analysts cautioned investors

to wait for the Company to provide details on product sales trends at retail and 2003 market share

gains. In addition, the analysts wanted to see if the Company would be changing its previous

guidance of 3Q03 revenues of $225-$235 million, 3Q03 EPS of $0.55-$0.58, 4Q03 revenues of

$277-$297 million, and 4Q03 EPS of $0.68-$0.74.

43. Thus, prior to the Class Period, defendants knew that (1) a substantial majority (80%)

of the Company’s sales and all of the Company’s net income would occur in the third and fourth

quarters, (2) the sales were dependant on three retail customers, Wal-Mart, Toys R Us and Target,

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 19 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 16 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

who were reducing inventory levels and requiring LeapFrog to fill orders within shorter time

periods, (3) the Company relied on DSS to fill the retailers’ orders within the required shorter time

periods, (4) LeapFrog had suspended the implementation of supply-chain software designed to

enable LeapFrog to assure it had sufficient inventory to meet actual and projected demand, and (5)

LeapFrog had to compete with Mattel’s PowerTouch product after going “virtually unchallenged”

prior to its release. In addition, they knew that the Company’s stock price had declined from almost

$34 on 7/8/03 to $27.65 on 7/22/03 and that they had told investors that LeapFrog would continue to

report growth in sales and earnings.

B. Defendants Knew There Were Numerous Problems with LeapFrog’s Distribution and Supply-chain Operations

44. On 7/24/03, during the Company’s 2Q03 earnings conference call, defendants

reported that LeapFrog’s 2Q03 financial results exceeded consensus estimates for the fourth

consecutive quarter since the 7/02 IPO and reiterated guidance for 3Q03 and 4Q03. In addition,

defendants assured investors that they felt “very positive” and that there were “no impediments” to

reporting sales and earnings in line with the reiterated guidance. Defendants knew these positive

statements were false and misleading. They knew problems with LeapFrog’s distribution and

supply-chain operations were very real impediments to reporting financial results in line with

guidance; indeed, defendants knew the distribution and supply-chain operations were in total

disarray.

45. Witness accounts, other documents and information and defendants’ admissions

during and after the Class Period show that defendants knew there were material weaknesses with

LeapFrog’s distribution and supply-chain operations throughout the Class Period that prevented

LeapFrog from (1) shipping retailers’ product within the shorter time periods they required, (2)

shipping the retailers’ products they actually ordered, (3) reporting LeapFrog’s financial results in

accordance with GAAP and the Company’s publicly reported accounting policies, and (4)

forecasting the Company’s future financial results.

46. According to several former LeapFrog employees, DSS and CLI repeatedly failed to

ship product ordered by LeapFrog’s U.S retail customers within the required shorter time periods (or

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 20 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 17 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

at all) and also shipped the wrong product to them. The shipping problems damaged the Company’s

relationship with the retail customers who repeatedly complained about LeapFrog’s inability to

fulfill their orders, returned and refused to pay for product they had not ordered, threatened to, and

did, reduce and cancel their orders when the problems were not fixed and imposed tens of millions

of dollars of vendor violation penalties.

47. The shipping problems also caused LeapFrog to improperly recognize revenues in

violation of GAAP and the Company’s publicly reported revenue recognition policy which only

permitted revenue to be recognized upon shipment if collection was reasonably assured. Defendants

knew collection was not reasonably assured because DSS and CLI were shipping product to the

retailers that they did not order and would not pay for. After the Class Period, LeapFrog admitted in

its 2004 10-K that it could not reasonably assure the reliability of its financial reporting or that its

financial statements were prepared in accordance with GAAP because there were numerous material

weaknesses with the Company’s internal controls related to, inter alia, revenues and accounts

receivable and the distribution and supply-chain operations.

48. Defendants also knew the failure to implement supply-chain software during the

Class Period caused LeapFrog to overstate inventory in violation of GAAP and LeapFrog’s publicly

reported inventory policy. The witness accounts describe how the lack of supply-chain software

prevented LeapFrog from accurately reporting inventory levels and from establishing sufficient

reserves for excess and obsolete inventory. After the Class Period, the Company increased the

reserve for excess and obsolete inventory by 400%, or $14 million. During the 10/18/04 conference

call, Curley admitted that the lack of supply-chain software during the Class Period prevented

LeapFrog from identifying obsolete and excess inventory: “as we started getting into our supply-

chain system, we also identified, you know, inventory – excess component inventory that we never

had visibility clearly on before, but now that we’ve, you know, have a system that’s not manual,

it’s giving us long-term visibility.” In addition, the Company admitted in its 2004 10-K that it could

not reasonably assure the reliability of its financial reporting or that LeapFrog’s financial statements

were prepared in accordance with GAAP because of numerous material weaknesses in the areas of

costs of goods sold and inventory and distribution and supply-chain operations.

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 21 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 18 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

49. The witness accounts show that defendants also knew LeapFrog was underreporting

expenses and liabilities because the Company’s engineering department was purchasing materials

and components from vendors that were used to manufacture and assemble products without a

written purchase order. As a result, the purchases were not reflected in the Company’s financial

statements. After the Class Period, the Company admitted in its 2004 10-K that it could not

reasonably assure the reliability of its financial reporting or that its financial statements were

prepared in accordance with GAAP due to material internal control weaknesses related to the

creation of purchase orders, inventory purchasing, the purchase of materials and components used to

manufacture and assemble products and payments to vendors.

50. Defendants also knew the shipping problems and the impact of Mattel’s PowerTouch

on the Company’s sales and lack of supply-chain software precluded LeapFrog from accurately

forecasting and fulfilling customer orders which in turn prevented the Company from accurately

forecasting LeapFrog’s future financial results. As detailed herein, the Company repeatedly missed

or revised guidance during the Class Period due to the shipping problems and lost sales. After the

Class Period, defendants stopped providing guidance, effectively admitting they never had a

reasonable basis for the guidance provided during the Class Period. Indeed, as Kalinske admitted

during the Company’s 12/16/04 conference call, “we’ve been so horrible at providing guidance I

just don’t think there’s any benefit in continuing the practice for the rest of this year.”

1. Defendants Knew DSS Repeatedly Failed to Fulfill Customer Orders Which Caused the Sales Shortfall in 3Q03 and Other Problems

51. Several witnesses, including CW1, CW2, CW4, CW6 and CW8 stated that DSS was

the company that managed and oversaw the receipt, warehousing and shipping of goods from 2000

until 7/04 when LeapFrog replaced DSS with CLI. The witnesses also stated that DSS repeatedly

failed to ship product ordered by LeapFrog’s retail customers and also shipped them the wrong

product.

52. CW6, the former operations analyst who worked at the DSS warehouse, stated that

LeapFrog had to closely monitor DSS throughout the time DSS managed the Company’s warehouse

operations to ensure DSS fulfilled its obligations. Because DSS did not provide reports showing

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 22 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 19 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

what products had been shipped to the Company’s retail customers, LeapFrog maintained staff,

including CW6, on-site at the warehouse to make sure products were shipped in accordance with the

retail customers’ purchase orders. CW6 stated that LeapFrog management was unhappy with the

degree of oversight required and wanted a warehouse provider that did not require the same level of

oversight. As a result, LeapFrog decided to change warehouse providers sometime before 3Q03.

53. CW6 stated that after DSS found out LeapFrog intended to change warehouse

providers their performance deteriorated and became unacceptable during 3Q03 and 4Q03, the

critical peak selling season for LeapFrog’s products. CW8 also stated DSS management knew

LeapFrog had decided to replace DSS with CLI by 11/03 because the decision was discussed with

the DSS senior managers. CW6 stated that DSS failed to fulfill many customer orders during the

peak selling season including $12-$13 million of orders from Toys R Us in 3Q03. CW6 stated that

Toys R Us sent its trucks to the DSS warehouse on multiple occasions to pick-up orders but DSS

was unable to deliver the product. During LeapFrog’s patent infringement trial against Mattel,

Bender testified that LeapFrog lost 1.2 million in LeapPad orders from Target and 2.8 million

LeapPad orders from Toys R Us in 3Q03 because of the inability to ship the product. Ex. A at 790-

92.

54. Other witnesses confirmed DSS was unable to ship product to the Company’s retail

customers. CW2, the former information technology director, said that the primary reason for the

3Q03 sales shortfall was the deteriorating relationship between LeapFrog and DSS. CW4, the

former accounts receivable specialist, also stated that LeapFrog began experiencing a lot of

warehouse problems in 3Q03 and that DSS’s inability to fulfill customer orders caused the 3Q03

sales shortfall. CW4 stated that DSS “quit on LeapFrog” because DSS knew LeapFrog was going to

switch warehouse providers. CW4 stated that the 3Q03 sales shortfall was also caused by LeapFrog

not having sufficient amounts of product available to fill customer orders. CW8, the former director

of international distribution, stated the inability of DSS to ship product to fulfill customer orders in

3Q03 was the reason CW8’s duties were expanded to include the oversight of domestic distribution.

CW8 also said the problems continued in 4Q03. CW8, who worked at the DSS warehouse in 4Q03,

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 23 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 20 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

stated that most of the orders that were not shipped in 3Q03 and additional orders that DSS was

unable to ship in 10/03 were lost and not shipped at a later date.

55. After LeapFrog reported 3Q03 sales of $203.9 million that were substantially less

than the $225-$235 million they previously represented there were no impediments to reporting,

defendants admitted shipping problems caused the shortfall. During the Company’s 10/22/03

conference call, Wood stated that the inability to ship product to the Company’s retailers caused the

sales miss and that defendants knew about the problems much earlier in the quarter. In fact, Wood

admitted LeapFrog “thought about pre-announcing and made the decision not to.”

2. Defendants Knew LeapFrog Cancelled the Implementation of Supply-Chain Software Before 3Q03 that Was Needed to Accurately Forecast Customer Demand and to Assure Sufficient Levels of Inventory to Meet Customer Demand

56. In addition to the shipping problems, defendants knew that LeapFrog had not

developed, implemented or maintained adequate supply-chain software needed to ensure LeapFrog

had sufficient inventory to meet actual and projected demand. According to CW1, LeapFrog

intended to implement supply-chain logistics software applications from Manugistics and Valdero in

2003 that were designed to link up and synchronize orders and projected orders from the Company’s

retailers to the inventory on hand and projected inventory. The software applications were intended

to extract information from LeapFrog’s Oracle database and to generate tailored reports that the

Oracle system could not generate. The software and the reports generated by the software would

allow CW1 to compare inventory on hand and inventory expected to arrive against current and

forecasted orders so that CW1 could allocate available inventory to the Company’s customers. CW1

stated that Wal-Mart, Toys R Us and Target were “Tier One” customers that received priority over

LeapFrog’s other customers to ensure they received their orders in full. Other customers would only

receive product that was not needed to fulfill orders received from Wal-Mart, Toys R Us and Target.

57. CW1 and CW2 stated that LeapFrog cancelled the implementation of the Manugistics

software prior to 3Q03 and that the software was supposed to perform supply-chain functions that

the Oracle system was unable to perform satisfactorily. As a result, CW1 was unable to perform a

forward looking allocation analysis. Instead, CW1 extracted data from the Oracle database and

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 24 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 21 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

prepared spreadsheet reports that compared how many products were shipped in a particular period

to what had been forecasted. CW2 stated that the Oracle supply-chain module was very lacking and

very rudimentary. Thus, as CW2 stated, LeapFrog’s software applications did not keep pace with

the increasingly complex requirements that accompanied the Company’s rapid growth. CW2 stated

that the Company’s business systems required ever-increasing amounts of manual processes because

the software applications did not perform the functions and because there was concern whether the

information generated by the software was accurate. As a result, the Company relied on manually

prepared spreadsheets to support their operations.

58. Other sources corroborate the witnesses. In a 10/30/03 article in Baseline magazine,

LeapFrog spokesperson Cherie Stewart (“Stewart”), stated that LeapFrog suspended deployment of

new supply-chain logistics software (version 6.15) before the beginning of 3Q03. On 11/13/03, Bear

Stearns analyst Jennifer Childe (“Childe”) reported that LeapFrog began deploying Manugistics

supply-chain software in the first half of 2003 but could not complete the implementation and

ultimately abandoned it prior to 3Q03.

3. Defendants’ Failed Scheme to Fabricate Sales to Avoid the 3Q03 Shortfall

59. Defendants’ knowledge of the 3Q03 sales miss is also shown by their unsuccessful

attempt to fabricate sales. CW4 stated that LeapFrog tried unsuccessfully to fabricate sales in 3Q03

to make-up the shortfall caused by the problems with DSS and the cancelled implementation of the

supply-chain software. CW4 stated that DSS shipped product in 3Q03 that was schedule to be

shipped to Toys R Us in 4Q03 to an empty warehouse around the corner from the warehouse

managed by DSS. Curley then caused LeapFrog to improperly recognize the revenue on the

fabricated sales. But according to CW4, LeapFrog’s auditors discovered the scheme and required

the Company to reverse the improperly recognized revenue. In addition, CW4 stated that the scheme

was also discovered when LeapFrog attempted to collect on the sales and were informed by Toys R

Us that it never received the product for which collection was being sought. CW4 also stated that

DSS and the freight company confirmed that the product had simply been shipped around the corner

to an empty warehouse.

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 25 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 22 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

60. CW4 first learned of the scheme from Forsythe in 9/03 when Forsythe informed CW4

and others in the accounting department that they were going to have to work long hours to reverse

the improperly recognized revenue. In 9/03, CW4 and other accounting personnel began reviewing

the numerous invoices that had been generated to book the Toys R Us orders prematurely to ensure

the revenue was reversed and not included in LeapFrog’s reported results. CW4 stated this project

was a “mad scramble” and was not completed until 10/03, just two days before the Company

announced 3Q03 results on 10/21/03. Curley cautioned the accounting personnel that worked on

reversing the improperly recognized revenue, including CW4, that they must never speak about what

happened. After the project was completed, Curley treated the accounting personnel to lunch at

Trader Vics restaurant in Emeryville which, according to CW4, was understood to be a reward for

having to work such long hours and a reminder not to speak about what had transpired.

4. Defendants Knew that Delays in Consolidating Warehouse Operations, Changing Warehouse Providers and Implementing Supply-Chain Software Caused the Distribution and Supply-Chain Problems to Continue in 4Q03 and 2004

61. Several witnesses, CLI’s suit against LeapFrog (Ex. B) and statements by defendants

after the Class Period show that defendants knew delays in (1) replacing DSS with CLI, (2)

consolidating warehouse operations, and (3) implementing supply-chain software until the peak

selling season in 2004 would cause the distribution and supply-chain problems to continue. Delays

in consummating the relationship with CLI resulted in DSS managing the Company’s warehouses

through 7/04. CW2 stated that CLI was supposed to take over warehouse operations from DSS in

3Q03 but the change was delayed. CW6 and CW8 also stated that LeapFrog decided to replace DSS

with CLI in late 10/03 or 11/03, but postponed executing a contract with CLI until 5/04.

62. CLI’s lawsuit against LeapFrog (which was filed on 1/12/05 in the U.S. District

Court, Southern District of Ohio) corroborates the witness accounts and confirms the delay. Ex. B.

In its complaint, CLI stated that LeapFrog and CLI began discussions about CLI overseeing and

managing the receipt, warehousing and shipping of goods from LeapFrog’s Fontana warehouse in or

around 11/03 but did not execute the warehouse management agreement (which is attached to the

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 26 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 23 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

complaint) until 7/1/04. Curley, former COO Forsyth and Murrer, LeapFrog’s Senior Vice President

of Operations and Logistics, signed the warehouse agreement on behalf of LeapFrog.

63. Delays in consolidating LeapFrog’s warehouse operations from several warehouses to

one warehouse located in Fontana, California contributed to the supply-chain problems and the delay

in replacing DSS with CLI. According to CLI’s suit against LeapFrog, when LeapFrog began

discussions with CLI in 2003 about CLI taking over management and operation of the Company’s

warehouses, the plan was to have CLI manage one warehouse located in Fontana. Ex. B. But

LeapFrog did not execute the lease for the Fontana warehouse until 3/31/04 and the term of the lease

did not commence until the later of 6/15/04 or substantial completion of required tenant

improvements. Like the warehouse agreement with CLI, Curley, Forsyth and Murrer signed the

Fontana warehouse lease on behalf of LeapFrog.

64. Due to the delays, DSS continued to manage LeapFrog’s warehouse operations

through 7/04. CW4, CW6 and CW8 stated that problems with DSS continued in 4Q03 and that

LeapFrog was scrambling in an attempt to repair customer relationships after the shipping problems

in 3Q03. For example, CW4 stated that in 11/03, Target threatened to stop doing business with

LeapFrog because Target was not receiving the products it had ordered.

65. CW6 stated that LeapFrog management was furious at DSS for the problems in 3Q03

and sent down additional reinforcements during 4Q03 in an attempt to salvage the remainder of

4Q03. Those reinforcements included CW8, John Gleason (“Gleason”), Wood, Forsyth and Murrer.

CW6 stated that the problems became a crisis in 11/03 when large numbers of LeapFrog personnel

were sent to the DSS warehouse to resolve various issues impeding the fulfillment of orders.

66. In 11/03, Murrer told CW8 to go to the DSS warehouse to help fix the shipping

problems that occurred in 3Q03 and 10/03. CW8 said that a number of additional LeapFrog

personnel, including Murrer and Forsyth, were on-site at the DSS warehouse on a regular basis in

4Q03. CW8 initiated daily conference calls between the sales and operations personnel in

LeapFrog’s Emeryville headquarters building and personnel at the DSS facility in an attempt to

make sure there were clear communications regarding what product needed to be shipped to each

customer and when the shipments needed to be made. CW8 said that LeapFrog had to ship products

Case 5:03-cv-05421-RMW Document 121-1 Filed 06/17/2005 Page 27 of 135

CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS – C-03-5421-RMW - 24 -

1

2

3

4

5

6

7

8

9

10

11