lessons in corporate governance: the role of the...

TRANSCRIPT

Lessons in Corporate Governance: The Role of the Securities Regulator

Alex Berg April 2012

Overview

• Corporate governance defined • WB corporate governance assessment program • Lessons learned for securities regulators • Questions…

2

3

Corporate Governance Defined

Perspectives on corporate governance

Company perspective:

• “The system by which companies are directed and controlled.” • The set of relationships between:

• A company’s management • Board of directors • its shareholders and • Other stakeholders

The policymaker’s perspective:

• Corporate governance = how to regulate the governance of public interest entities in order to maximize productivity and value while preserving company flexibility and minimizing costs

4

5

The company perspective …

Shareholders

DirectorsManagers

Regularly report and update

Monitor and guide

Repre

sents a

nd re

port to

Ele

ct and d

ismiss

Pro

vid

e c

apital to

Report

tra

nsp

are

ntly to

6

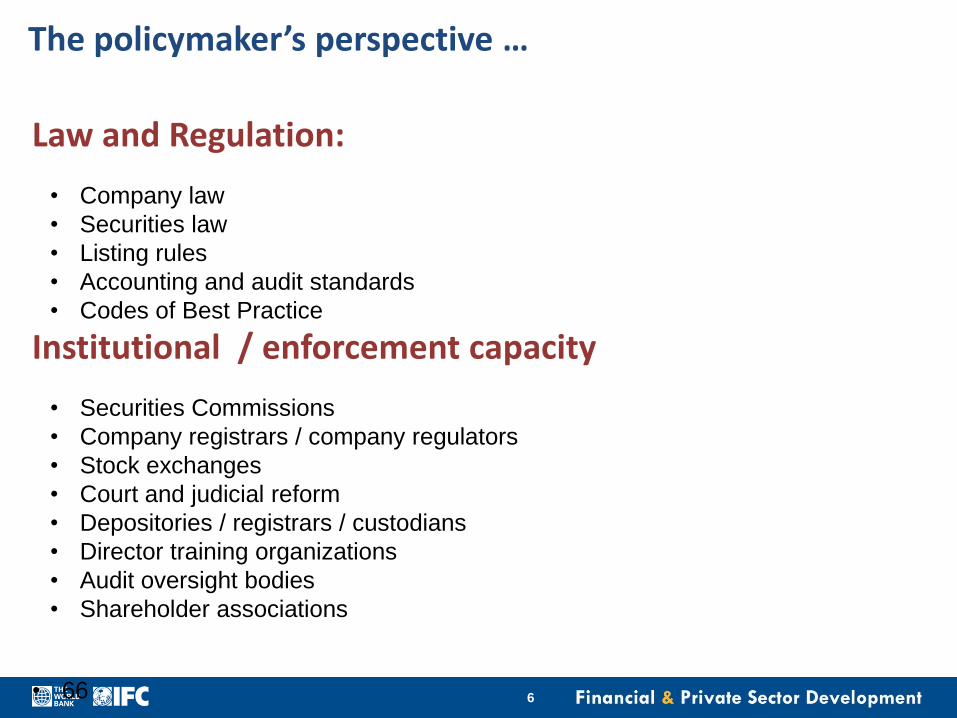

The policymaker’s perspective …

Law and Regulation:

• Company law

• Securities law

• Listing rules

• Accounting and audit standards

• Codes of Best Practice

Institutional / enforcement capacity

• Securities Commissions

• Company registrars / company regulators

• Stock exchanges

• Court and judicial reform

• Depositories / registrars / custodians

• Director training organizations

• Audit oversight bodies

• Shareholder associations

• 66

Go

od

bo

ard

pra

cti

ces

an

d C

on

tro

l S

tru

ctu

res

Ma

nag

ing

Sta

keh

old

er

Re

lati

on

s

Str

on

g d

isclo

su

re &

tra

nsp

are

ncy r

eg

ime

Pro

tecti

on

of

(min

ori

ty)

sh

are

ho

lder

rig

hts

Achieving Good Corporate Governance

Robust legal & regulatory environment

Strong enforcement regime

7

The value of improved corporate governance …

For companies:

• Streamlined business processes, better operating performance & lower

capital expenditures

• improved access to finance (both equity and debt)

• Higher valuations

• Better decision-making

For shareholders (including pension beneficiaries):

• Protection from abuse

• Increased shareholder value

• Protection from “reputational risk”

For regulators and supervisors:

• A first line of prudential defense

• Increased financial stability

For markets and economies:

• Higher market capitalization and liquidity

• More “champion” companies that can compete and grow internationally

• Higher economic growth

8

Why does it matter?

Better Corporate Governance =

Bigger capital markets + more listed companies =

Better access to finance and higher growth Market capitalization to GDP

Note: Relationships remain significant when controlling for income per capita. Higher values on the strength of investor protection index indicate greater protection. Source: Doing Business database, World Bank (2010).

Higher entry level to capital markets Number of listed firms

Levels of Investor Protection (as measured by Doing Business)

9

10

What is corporate governance? Regulator versus company perspectives …

Valu

ation

Quality of corporate governance

Country with poor governance framework

Country with good governance framework

11

The Corporate Governance ROSC Assessments

International Consensus:

the OECD Principles of Corporate Governance

• Certain basic principles apply in all countries:

• The Rights of Shareholders

• The Equitable Treatment of Shareholders

• The Role of Stakeholders

• Disclosure and Transparency

• The Responsibilities of the Board

• Designed to apply to companies listed on stock exchanges

12

13

The Corporate Governance ROSC program:

Overview

• Benchmarking exercise against the OECD Principles of Corporate

Governance

• Standardized and systematic diagnostic, including ratings, report,

and policy recommendations

• Engage a local consultant to complete a standard questionnaire

• Country participation and publication is voluntary

• Updates: measure progress over time

• 85 carried out or underway since 2000 in 64 countries

• Impacts include country action plans, legal / regulatory reform,

Code drafting / updates, creation of new institutions

14

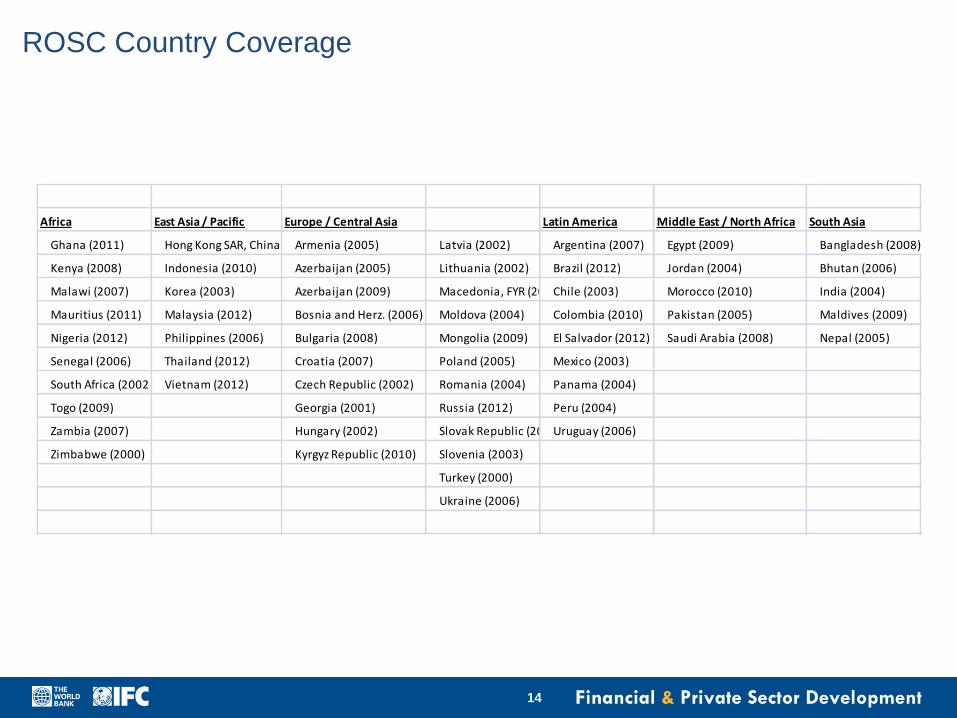

ROSC Country Coverage

Africa East Asia / Pacific Europe / Central Asia Latin America Middle East / North Africa South Asia

Ghana (2011) Hong Kong SAR, China (2003)Armenia (2005) Latvia (2002) Argentina (2007) Egypt (2009) Bangladesh (2008)

Kenya (2008) Indonesia (2010) Azerbaijan (2005) Lithuania (2002) Brazil (2012) Jordan (2004) Bhutan (2006)

Malawi (2007) Korea (2003) Azerbaijan (2009) Macedonia, FYR (2005)Chile (2003) Morocco (2010) India (2004)

Mauritius (2011) Malaysia (2012) Bosnia and Herz. (2006) Moldova (2004) Colombia (2010) Pakistan (2005) Maldives (2009)

Nigeria (2012) Philippines (2006) Bulgaria (2008) Mongolia (2009) El Salvador (2012) Saudi Arabia (2008) Nepal (2005)

Senegal (2006) Thailand (2012) Croatia (2007) Poland (2005) Mexico (2003)

South Africa (2002) Vietnam (2012) Czech Republic (2002) Romania (2004) Panama (2004)

Togo (2009) Georgia (2001) Russia (2012) Peru (2004)

Zambia (2007) Hungary (2002) Slovak Republic (2003)Uruguay (2006)

Zimbabwe (2000) Kyrgyz Republic (2010) Slovenia (2003)

Turkey (2000)

Ukraine (2006)

Example: Indonesia (Chapter 2: Shareholder Rights)

87

90

94

68

94

100

75

83

75

85

88

59

65

63

43

63

35

67

78

56

46

46

46

92

IIA: Basic shareholder rights

IIA 1: Secure methods of ownership registration

IIA 2: Convey or transfer shares

IIA 3: Obtain relevant and material company information

IIA 4: Participate and vote in general shareholder meetings

IIA 5: Elect and remove board members of the board

IIA 6: Share in profits of the corporation

IIB: Rights to part in fundamental decisions

IIB I: Amendments to statutes, or articles of incorporation

IIB 2: Authorization of additional shares

IIB 3: Extraordinary transactions, including sales of major …

IIC: Shareholders GMS rights

IIC 1: Sufficient and timely information at the general meeting

IIC 2: Opportunity to ask the board questions at the general …

IIC 3: Effective shareholder participation in key governance …

IIC 4: Availability to vote both in person or in absentia

IID: Disproportionate control disclosure

IIE: Control arrangements allowed to function

IIE 1: Transparent and fair rules governing acquisition of …

IIE 2: Anti-take-over devices

IIF: Exercise of ownership rights facilitated

IIF 1: Disclosure of corporate governance and voting policies …

IIF 2: Disclosure of management of material conflicts of …

IIG: Shareholders allowed to consult each other

15

Example: Indonesia vs. Region

55

70 66

73

65

56 60 60 60

68 73

62

72 68

I. Enforcement & Institutional Framework

II. Shareholder Rights and Ownership

III. Equitable Treatment of Shareholders

V. Disclosure and Transparency

VI. Board Responsibilities

Indonesia Country Assessment vs. Asia Regional Average

Indonesia (2009) Indonesia (2004) Asia and Pacific Region (India, Malaysia, Thailand, Philippines, Vietnam)

16

Roadmap to For CG Reforms

Assessment

Country Action Plan

Implementation

17

18

Lessons Learned

Lessons learned (for regulators / supervisors)

1. Enforcement of shareholder rights 2. Improving disclosure 3. Improving board practices 4. Regulatory governance

19

Enforcement of shareholder rights

• Courts don’t function well for minority shareholders in most countries

• Company law has no effective regulator in most countries • Strongest enforcement of company law happens when securities

regulator can take action on behalf of shareholders. • “Mirrored” company law provisions in securities regulation

(Indonesia) • Special “court” where shareholders can complain (Egypt) • Impose administrative penalties if company law violated

(Brazil) • Stock exchange approval of related party transactions (South

Africa)

20

Improving disclosure

• Financial and non-financial disclosure radically improving everywhere

• But almost all countries still rely on 19th century disclosure mechanisms (annual reports)

• Way forward: • On-line updates of wide variety of financial and non-

financial disclosure (Brazil’s “reference form”) • Adaptation of new web-based technologies • Removal of expensive requirements to publish (e.g.

annual reports to all shareholders, publication in newspapers and government gazettes).

21

Improving board practices

• Board is at core of modern corporate governance reform • Big changes everywhere including:

• Role and responsibility of board • Liabilities of directors • Board objectivity and independence

• In terms of regulation – biggest idea of the past 10 years has been introduction of “corporate governance codes’ in many countries.

• But how should they be introduced?

22

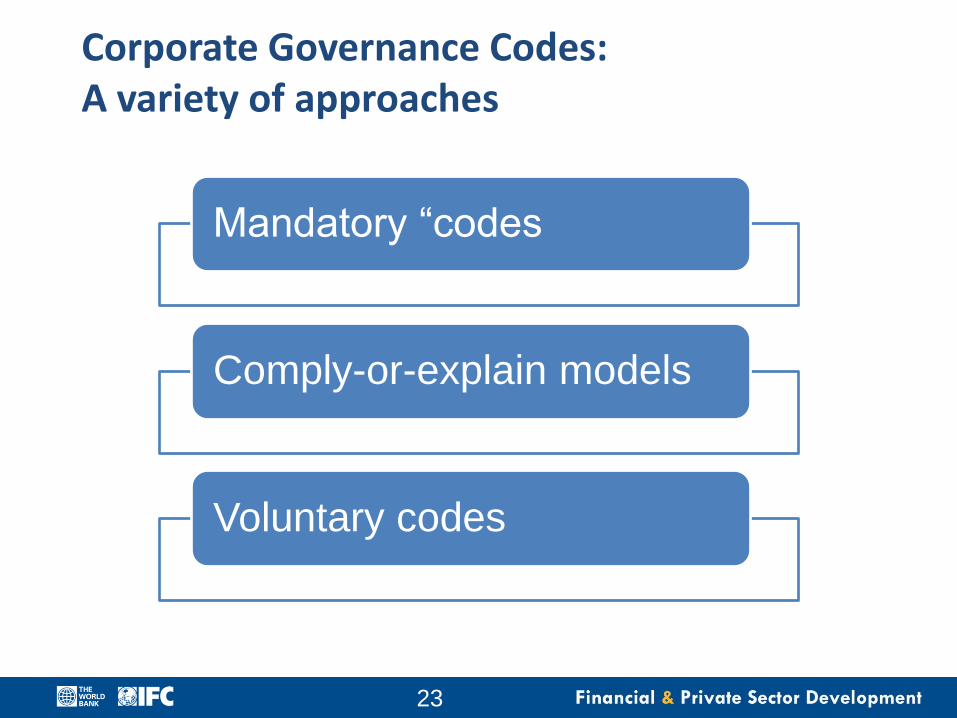

Corporate Governance Codes: A variety of approaches

Mandatory “codes

Comply-or-explain models

Voluntary codes

23

Improving Board Practices (cont.)

Our observations from working in many countries are: • Corporate governance codes are most influential when

they are supported by the securities regulator and well anchored in regulation (on a comply or explain basis).

• Codes add something to mandatory regulation, for those areas that are “aspirational” and hard to measure / enforce (like board practices)

• The influece of a Code is increased if a single code can be adopted across many sectors (e.g. capital markets, banks, insurance companies)

24

Regulatory Governance

• Impact of securities regulator is driven by policy, regulatory framework, resources, and authority – but governance of regulator is also crucial.

• Global financial crisis = a catalyst for reexamining of the effectiveness and efficacy of existing financial regulatory structures.

• To the extent regulatory power expands and is consolidated in fewer entities, their performance becomes even more important.

25

Regulatory Governance (continued)

• Regulatory governance involves decisions about: • Independence, autonomy and accountability of the regulator from and to

government.

• Independence and accountability of the regulator from and to regulated

financial institutions.

• Formal and informal decisionmaking processes.

• The composition and role of the board of directors of the regulator (if any)

and its relationship to management.

• Transparency, predictability, and accessibility of decisionmaking

• Organizational structure and resources available to the regulator.

• WB now working to develop a diagnostic framework for regulatory governance • How we should define good governance for securities commissions?

• What are basic standards of and key challenges to good regulatory

governance?

• What can governments do to improve their regulatory governance?

26