let’s talk energy - home page - hong kong institute of...

TRANSCRIPT

Issue 5 / Volume 13 / May 2017

LET’S TALK ENERGY

Richard Lancaster, CEO of CLP Holdings,

explains the company’s powerful

role in the global conversation of

renewable energy

Plus:CPAs wantedFirms face talent shortage

Hong Kong’s pegCan it survive Trump?

LifeDetermined dragon boaters

HK$70.00

C

M

Y

CM

MY

CY

CMY

K

HKICPA_Cork_Back cover.pdf 1 12/29/14 5:38 PM

Aplus Ad.indd 1 29/8/2016 3:05 PM

President’smessage

aplus

May 2017 1

Dear members,

This month, the Council conducted its annual visit to Beijing and Shanghai where we exchanged views with Mainland authorities, including the Ministry of Finance, Chinese Institute of CPAs, State Administration of Taxation, China Securities Regulatory Commission, China Certified Tax Agents Asso-ciation, and Shanghai Institute of CPAs. We also visited the Shanghai Free Trade Zone.

The fruitful discussions have deepened our relations with Main-land counterparts and officials. We discussed many topics during this visit, and one of them was about how to facilitate cross-border busi-nesses conducted by our members.

Our visit coincided with the high-profile Belt and Road Forum for International Cooperation held in Beijing. Attended by 29 world leaders, it aimed to inaugurate a new intercontinental order to bring Asian countries closer to one another, and collectively to Europe and Africa.

The Belt and Road initiative seeks to connect 65 countries across three continents, thereby impacting the lives of 4.4 billion people, and accounting for a total gross domestic product of US$2 trillion once the vision is realized.

There will certainly be business opportunities for Hong Kong as a super connector. As CPAs, we should play an active role in pro-viding our expertise services, from assurance, due diligence, financial analysis, merger and acquisition, restructuring, strategic planning to taxation advisory.

The Institute is now analysing the results of its 4th membership survey, which was conducted to seek members’ input in the areas of learning needs, the outlook of the profession, business develop-ment, earning power, and work-life balance.

With a better understanding of these areas, the Institute can make better strategic and long-term action plans to serve your needs.

Members indicated that they are seeking more professional and technical training from the Institute in a more diversified and accessible way. The Institute has listened and has been rolling out courses on a series of hot topics as well as webcasting popular events.

These include the favoured IT series, which is designed to equip members with knowledge on how to get the most out of the latest information technologies to

enhance business performance. Upcoming courses will cover topics such as cloud computing, digital boardroom, and modern finance in the digital age.

The Environmental, Social and Governance series is another popular course. It helps members develop their knowledge in relation to ESG reporting, its benefits and the relevant challenges faced by Hong Kong-listed companies.

Don’t miss these and many other great opportunities to equip yourself and further develop your career.

One convenient way to get instant information on the latest training events is through our new mobile app, which was just launched this month. Apart from CPD pro-grammes, you can also enrol in lei-sure and networking activities, make online payments, and track your enrolment and CPD record. Down-load it from the App Store or Google Play on your phone now.

More survey results and the Institute’s follow-up actions will be communicated to you in due course. In the meantime, I would like to thank the 3,748 members who par-ticipated for taking the time to share their views, which are important to the development of the profession.

“ Members indicated that they are seeking more professional and technical training from the Institute in a more diversified and accessible way.”

Mabel Chan President

ContentsIssue 5 / Volume 13 / May 2017

01NEWS

01 President’s message

04 Institute news

06 Accounting news

10FEATURES

10 The durable dollar Can the United States and Hong Kong dollar currency peg survive the Trump administration?

17 Thought leadership: Alice Telfer and Michelle Crickett The Head of Business Policy and Public Sector and the Director of Research at the Institute of Chartered Accountants of Scotland on the new ICAS guidance for making professional judgments

18 Leadership: Richard Lancaster Chief Executive Officer of CLP Holdings Richard Lancaster explains what good corporate governance means to him

25 How to… Yin Toa Lee on how Hong Kong companies can change their business practices in preparation for IFRS 16

26 Hiring for the future A Plus examines the reasons behind the shortage of accountants in Hong Kong and what firms are doing to attract and retain talent

32 Success ingredient: Y.K. Lee The Chief Financial Officer of Branded Lifestyle shares how he manages the back offices of several clothing brands in Asia and how data has become an important part in his decision making process

38 Moving as one Institute members share why dragon boating can be a thrilling and rewarding sport

45SOURCE

45 Hong Kong’s proposed preferential tax regime for offshore aircraft leasing activities extended to cover onshore market The Hong Kong government, by way of Committee Stage Amendments made on 19 May to the original bill, proposes to extend the scope of the original bill to cover onshore aircraft leasing

48 Technical update Examining the importance of utilizing professional judgment in accounting and how to make them effectively

50 TechWatch 174

26Hiring for the futureWith the shortage of accounting talent in and outside of Hong Kong, A Plus examines firms’ recruitment and retainment strategies

About our nameA PLUS stands for excellence, a reference to our top-notch accountant members who are success ingredients in business and in society. It is also the quality that we strive for in this magazine — going an extra mile to reach beyond Grade A.

Editor Gerry HoEmail: [email protected]

Copy Editor Jemelyn Yadao

Contributors Julian Hwang, George W. Russell

Editorial Assistant Queenie Lee

Production Manager Jasmine Hu

Editorial Office G/F, Bangkok Bank Building, 18 Bonham Strand West, Sheung Wan, Hong Kong

ADVERTISING ENQUIRIESAdvertising Director Derek TsangEmail: [email protected]: (852) 2164-8901

A PLUS is the official magazine of the Hong Kong Institute of Certified Public Accountants. The Institute retains copyright in all material published in the magazine. No part of this magazine may be reproduced without the permission of the Institute. The views expressed in the magazine are not necessarily shared by the Institute or the publisher. The Institute, the publisher and authors accept no responsibilities for loss resulting from any person acting, or refraining from acting, because of views expressed or advertisements appearing in the magazine.

© Hong Kong Institute of Certified Public Accountants May 2017. Print run: 7,160copiesThe digital version is distributed to all 40,806 members, 18,645 students of the Institute and 2,293 business stakeholders every month. Subscription: HK$760 for 12 issues per year.See www.hkicpa.org.hk/aplus for details.

President Mabel Chan

Vice Presidents Eric Tong, Patrick Law

Chief Executive and Registrar Raphael DingEmail: [email protected]

Head of Member & Public Relations Margaret Lam

Editorial Manager John So

Editorial Coordinator Maggie Tam

Office Address37/F, Wu Chung House, 213 Queen’s Road East, Wanchai, Hong KongTel: (852) 2287-7228 Fax: (852) 2865-6603

Member and Student Services Counter27/F, Wu Chung House, 213 Queen’s Road East, Wanchai, Hong Kong Email: [email protected] Website: www.hkicpa.org.hk 52

AFTER HOURS

52 Books TED TALKS: The Official TED Guide to Public Speaking reviewed, and a few tips on storytelling from Chris Anderson

54 Life and everything From the city’s top vegetarian restaurants to stylish charging cables and the Hong Kong Academy for Performing Arts’ Academy Festival, as recommended by Institute members

56 Let’s get fiscal Nury Vittachi on the ethical issues arising from the merging of money and technology

38Moving as oneWith the summer dragon boat competitions approaching, members of the Institute’s Dragon Boat Interest Group share their commitment to both the sport and the team

Book review

Editorial OfficeG/F, Bangkok Bank Building, 18 Bonham Strand West, Sheung Wan, Hong Kong

ADVERTISING ENQUIRIESAdvertising DirectorEmail: [email protected]: (852) 2164-8901

A PLUSCertiall material published in the magazine. No part of this magazine may be reproduced without the permission of the Institute. The views expressed in the magazine are not necessarily shared by the Institute or the publisher. The Institute, the publisher and authors accept no responsibilities for loss resulting from any person acting, or refraining from acting, because of views expressed or advertisements appearing in the magazine.

© Hong Kong Institute of CertiMay 2017. Print run: 7,160copiesThe digital version is distributed to all 40,806 members, 18,645 stakeholders every month. Subscription: HK$760 for 12 issues per year.See

Book review

Moving as oneWith the summer dragon boat competitions approaching, members of the Institute’s Dragon Boat Interest Group share their commitment to both the sport and the team

News Institute news Accounting news

Institute news

New app launchedThe Institute has launched its new app that instantly updates members and students on Institute events, and enables users to easily enrol in them.

Specifically, the app allows users to enrol in the Institute’s continuing professional development programmes – both face-to-face and e-learning – leisure and networking events, as well as Qualification Programme seminars. Users can also make online payments for enrolment, as well as keep track of their individual CPD history and other enrolment records.

To find specific events, users can effectively filter all events by selecting the event category, type, date range, and entering keywords.

Members and students can down-load the app now from the Apple App Store or Google Play on their phones by searching “HKICPA”.

Highlight of eventsThe Financial Services Interest Group will hold an evening seminar on 9 June

covering the topic of the future of cryptocurrencies, such as Bitcoin, which was created in 2009. The speaker, Dr. Julian Hosp, will discuss the likely regulation and government scrutiny, acceptance among consumers and other considerations for investment in cryptocurrencies. Dr. Hosp is a Blockchain expert and the author of 25 Stories I Would Tell My Younger Self.

The Corporate Finance Interest Group has organized a lunch semi-nar on 22 June that will provide an overview of the collective investment scheme. Using case studies, Penelope Shen, Partner at Kwok Yih & Chan, will explore the latest issues and trends from the commercial and the legal perspectives, covering areas such as fund structures (traditional structures and the new open-ended investment fund company structure), and who the target investors are (pub-lic vs. professional investors).

Meanwhile the new IT series of

seminars kicked off this month and will run until 11 July. Topics covered include how to differentiate true cloud technologies from fake ones, and how the finance function can reap the benefit of cloud computing; how companies can apply analytics to business data to describe, predict, and improve business performance, recommend action, and guide decision making; why customers need modern cloud enterprise resource planning to stay relevant; and how a properly designed cloud strategy can help small- and medium-sized entities gain a competitive advantage.

These seminars are designed to provide professionals with knowledge of the latest information technologies available, and their implications for businesses and the accounting profession.

ObituaryThe Institute notes with regret the passing away of Wong Kamyen, Peter.

4 May 2017

C

M

Y

CM

MY

CY

CMY

K

1068_Comm_APlusAD_output.pdf 1 1/7/16 2:56 PM

Aplus Ad.indd 1 11/3/16 8:12 PM

Aplus Ad.indd 1 29/8/2016 3:04 PMAplus Ad.indd 1 14/10/2016 10:44 AM

NewsAccounting

6 May 2017

The Financial Reporting Council, the accounting watchdog in the United Kingdom, opened an investigation into KPMG’s 2010-2013 audit of Rolls-Royce in May.

In January, the British luxury car and aero-engine manufacturing company was indicted of long-running corruption and agreed to pay £671 million in penalties to settle a deferred prosecution agreement with the U.K.’s Serious Fraud Office.

Rolls-Royce was found guilty of issuing bribes to middlemen over three decades that were worth millions of pounds in cash, as well as offering a luxury car, to secure orders from Indonesia, Russia, China, Thailand, India and Nigeria.

For example, from 1991 to 2005, it was revealed that the company issued more than £28 million to agents in Thailand in order to win three contracts and supply

aero engines to Thai Airways.In a statement, the Big Four firm stated

that it will fully cooperate with the FRC’s investigation, which follows the SFO’s probe into the company, and is confident in the quality of all of its audit work, including the five-year period that the FRC is examining. In addition, the firm said that “it is important that regulators acting in the public interest should review high profile cases.”

KPMG’s Rolls-Royce audit under investigation

Illus

trat

ion

by H

arry

Har

rison

Risks to accounting estimates receive uneven scrutinyThe risk of error due to imprecise measurement methods and the risk of management bias in arriving at accounting estimates are not given the same level of attention by auditors, according to recent research from the University of Arizona, despite both being equally important. The study found that auditors respond to a high risk of management bias with a high level of audit effort, but loosen up on both bias and imprecision when management bias is at a lower risk, reported Compliance Week. It suggested that a more balanced focus on both management bias and measurement imprecision “would likely help mitigate auditors’ behavioural tendency to under-audit when the risk of bias is low.”

Barclays to pay settlement in SEC claimBarclays agreed to pay a fine of more than US$97 mil-lion from the United States’ Securities and Exchange Commission after it allegedly overbilled clients almost US$50 million. The SEC said the British bank commit-ted three violations: the first involving two Barclays advisory programmes that charged clients for due dili-gence and monitoring of third-party investment manag-ers, which were not performed as promised; the second regarding the bank’s collection of “excessive” mutual-fund sales fees; and the third involving billing errors that resulted in multiple accounts making overpayments as fees to the bank.

aplus

Hong Kong urged to set up FinTech officeHong Kong should set up a financial technology office to position itself as FinTech hub in the region, accord-ing to a research report by the Financial Services Development Council, reported the South China Morn-ing Post. The FSDC urged Hong Kong to take a more proactive approach in developing distributed ledger technology, such as blockchain, for applications in the financial sector. The report also recommended the government to focus on developments in cybersecurity, payments and securities settlements, digital identifica-tion for know-your-client, as well as wealth, insurance and regulatory technology.

Hong Kong vs. London in China finance hub bidAt the Belt and Road Forum for International Coopera-tion held in Beijing this month, Hong Kong and London challenged each other over which city was best placed to serve as the finance hub for China’s Belt and Road global trade and commerce strategy, which would reportedly need trillions of U.S. dollars in funding. Hong Kong’s Chief Executive, C.Y. Leung, claimed that the city was “the preferred destination” due to its status as the largest offshore settlement centre for yuan trade and the world’s top stock market for new listings in 2016. Philip Ham-mond, the British Chancellor of the Exchequer, argued that London remains the world’s financial centre, and is “not an alternative to Hong Kong.” C. Y. Leung

May 2017 7

The percentage of CFOs in China who are optimistic about the

economic outlook despite policy uncertainties and geopolitical concerns, according to the Q1

findings of Deloitte China’s CFO Survey 2017.

26%

A world of numbers

The amount that the U.K.’s Financial Reporting Council has fined PwC for“misconduct” in its audit of Connaught, a social housing maintenance group,

which collapsed in 2010. During the Connaught tribunal in March, PwC admitted failure to exercise

appropriate scepticism for the audit of the 2009 accounts.

£5million

The number of businesses in the U.K. “significantly concerned” about

potential cyber threats arising from the new avenues for attacks created by the Internet of Things and smart technologies, such as batteries, electric vehicles and

systems controls, according to a PwC survey.

2/3

C

M

Y

CM

MY

CY

CMY

K

1075_Comm_APlus_output.pdf 1 6/18/15 12:25 PM

aplusNewsAccounting

SFC warns on undervalued assets in M&AsHong Kong’s Securities and Futures Commission warned company directors and financial advisors to ensure assets are properly valued in all mergers and acquisitions to protect shareholders’ interests, or face penalties. Valuers who provide materially false or misleading information may become liable, and face a fine or court orders for investor compensation, the SFC said in a statement. In its guidance note, the SFC reminded directors to thoroughly investigate the value of the assets to be bought, and act in the interests of the company.

Snap Inc.’s Q1 loss may have tax benefitSnap Inc., the company behind the photo messaging app Snapchat, reported a US$2.2 billion first quarter loss that will likely lead to a tax reduction, reported The Wall Street Journal. Around US$2 billion of the loss came in the form of a stock compensation expense, where tens of millions of restricted shares and stock options were issued to employees as a form of payment, with the stock slated to vest once the company became public, the Journal said. Given the difference between the price at the time stock was granted and the market price when it was vested, Snap would be eligible for a tax deduction, provided that employees report the stock’s vesting value as income.

Sylvester Stallone to sue Warner Bros. Hollywood action-star Sylvester Stallone announced that he will file a lawsuit with his production company, Rogue Marble, against Warner Bros. Entertainment for alleged breach of contract, unfair business practices and accounting fraud in relation to his 1993 sci-fi film Demolition Man. According to the lawsuit, Stallone believes he is owed profits and accuses the film studio and entertainment company of being “unfair, unlawful and offensive” and “know-ingly playing fast and loose” with the film’s revenues. The lawsuit also underlines a wider motive of reforming “Hollywood account-ing” for the benefit of “all talent” in Hollywood, wrote USA Today. Warner Bros. did not yet respond to the suit.

Fujifilm postpones earnings announcementFujifilm announced that it has delayed its earnings announcement for the year ended in March until it has the results of an investigation into questionable accounting practices at its New Zealand unit. The Japanese photography and imaging company will set up a third-party panel of accountants and lawyers to look into the validity of the subsidiary’s accounting, due to uncertainty over lease transactions at Fuji Xerox New Zealand for the periods prior to the financial year of 2015. The findings are scheduled to be delivered to the company around mid-May, said Fujifilm.

May 2017 9

Sylvester Stallone in Demolition man (1993 )

Warner Bros/Silver Pictures/C

ollection Christophel

CurrenciesHong Kong peg

10 May 2017

aplus

THE DURABLE DOLLAR

Many significant financial events – from property boom to bust, from bank run to recession – have previously put pressure on the currency peg between the United States

and Hong Kong dollars. The exchange-rate mechanism has proved remarkably durable but, as George W. Russell asks,

can it survive Donald Trump?Illustrations by Ester Zirilli

T he peg between the Hong Kong and United States dollars, formally known as the linked exchange rate

mechanism, ties Hong Kong’s economic policy to that of the U.S. Thus it’s no sur-prise that whenever Janet Yellen, Chair of the Board of Governors of the U.S. Federal Reserve System, announces a change in interest rates, as she did in March, all eyes in Hong Kong turn to the peg.

Normalization of Fed policy, after a period of historically low interest rates, is the latest in a spate of events thrusting the peg into the spotlight. Others include the renminbi’s inclusion in the basket of currencies that makes up the International Monetary Fund’s de facto unit in Sep-tember 2016, and Beijing’s push for the renminbi’s internationalization in 2014.

Now the peg is back under scrutiny since the U.S., under President Donald Trump, appears to be on a collision course with China over trade. Although Trump has eased off accusations that China is a “currency manipulator,” there is the awkward political situation of a significant part of China being tied to an obstreperous rival.

Some analysts, such as Ramkishen Sundara Rajan, Professor of Economics at ESSEC Business School, Asia-Pacific, suggest that now might be a good time to revisit the effectiveness of the peg.

With greater global exchange-rate volatility due to U.S.-China tensions (as well as the United Kingdom’s exit from the European Union and other trade con-cerns), Rajan says Hong Kong can expect more frequent and not always anticipated shocks. “In this regard, a greater degree of exchange rate flexibility could help allevi-ate the burden on the domestic economy.”

Henry Group Holdings, a listed com-mercial property developer in Hong Kong, highlighted currency-related woes in its

latest annual report: “The retail market remained fragile with the Hong Kong dollar peg to the strong [United States] dollar sup-pressing both the number of inbound tour-ists from Mainland China and retail sales.”

Indeed, the peg crops up often as a boilerplate reference in management and discussion analyses. As Ronny Lee, Chief Financial Officer of Henry Group and a Hong Kong Institute of CPAs member, points out, statements often note the peg’s effect on the overall economy.

Speculation riskThe peg was introduced in 1983 to provide Hong Kong’s small economy with an international underpinning (See Currency in crisis on page 15). A currency tends to strengthen when investment pours in (although exports become less competitive). When a country hits economic trouble, its currency often weakens. To hold exchange rates stable, many central banks deploy foreign reserves, buying and selling in currency markets.

Another option to stave off high vola-tility, especially for small countries, is to fix the value of their money to another

“ A greater degree of exchange rate flexibility could help alleviate the burden on the domestic economy.”

May 2017 11

CurrenciesHong Kong peg

12 May 2017

aplus

currency, through a peg, a band or a board. At least 50 curren-cies are pegged to a major unit: about half to the U.S. dollar, while others are linked to the British pound, euro, South Afri-can rand or Australian and New Zealand dollars.

There is no doubt that pegs cause stresses. Speculators hope to catch bankers off guard or exert enough pressure to break the link. In 1998, investors betted the exchange rate was inappropriately strong for Hong Kong. In more recent years, the pressure has been coming on the “strong side” of the rate, with bankers struggling to deal with excessive inflows.

“Investors have occasionally questioned whether the currency board is the most suitable frame-work for Hong Kong and, in turn, this has prompted specula-tive pressures in the past,” says Claudio Piron, Managing Director of Global Research at Bank of America Merrill Lynch in Singapore. “The current cur-rency board is not necessarily the optimal regime.”

Some speculative attacks are deliberate. Financier George Soros, who pocketed US$1 billion in 1992 by betting the British pound would be forced off the European Exchange Rate Mechanism, was less successful in his 1998 Hong Kong venture. Then financial secretary Donald Tsang deployed vast reserves to defend the peg, buying nearly HK$120 billion in stocks.

Maintaining the peg can require great effort: the Hong Kong Monetary Authority, Hong Kong’s de facto central bank, has invested HK$3.63 trillion worth of assets in the Exchange Fund, which is used to maintain financial stability, including propping up the peg. (The fund made HK$61 billion last year on higher returns from stock investments).

The peg forces the HKMA to synchronize local interest rates with those of the U.S., even when the two economies are in different cycles. Interest rates are set according to growth: when an economy accelerates, central banks often raise rates to

slow inflation or, sometimes, to tame asset bubbles.

Questions of relevanceIn recent years, Hong Kong has been forced by its dollar peg to mirror monetary policy more appropriate for a crisis-struck U.S. than a still-growing Hong Kong. Most analysts believe inappropriately low interest rates are to blame for the more than doubling of property prices in Hong Kong since 2009.

Now that the U.S. Federal Reserve is in a tightening cycle, households in Hong Kong – which already had to take on much debt to buy expensive property – will face an added burden of rising monthly mort-gage payments.

Hong Kong’s broader economy, which has been dealing with heated inflows in recent years, especially from the Mainland, now faces the risk of outflows. “It’s expected that some of the US$130 billion of capital inflow into Hong Kong since 2008 will be exchanged back to the U.S. dollar,” HKMA

“ Investors have occasionally questioned whether the currency board is the most suitable framework for Hong Kong and, in turn, this has prompted speculative pressures in the past.”

At least 50 currencies are

pegged to a major unit. About half

are pegged to the U.S. dollar, while

others are linked to the British pound,

euro, South African rand or Australian and New Zealand

dollars.

May 2017 13

CurrenciesHong Kong peg

14 May 2017

aplus

Currency in crisis

The Hong Kong dollar’s peg to the U.S. dollar was born amid the chaos of a recession in the early 1980s. Many Hong Kong property companies went bust and seven local banks collapsed between 1983 and 1986, while political uncertainties added a further twist. In August 1983, China declared it would take back Hong Kong on or before 1 July 1997, regardless of the outcome of its negotiations with the United Kingdom.

Sino-British talks on the weekend of 23–24 September 1983 ended in a stalemate. On those two days, the Hong Kong dollar fell 13 percent against the U.S. greenback, closing at a record low of HK$9.60 to US$1. Ordinary Hongkongers were rattled, former legislator and union organizer Chan Kam-chuen recalled. “People rushed to the supermarkets and emptied the shelves of food and other daily necessities.”

The government developed the peg with utmost secrecy in case speculators saw an advantage. “[Because] of the immediate effect on sensitive financial markets of everything we may say and do… we must proceed with care and caution,” then governor Sir David Wilson told the Legislative Council on 5 October 1983.

Nevertheless, Hong Kong’s savvy business community knew something was afoot. “Smaller manufacturers… refused to accept orders with Hong Kong dollar payments… dealers in raw materials also did likewise,” Chan said. “Some parents who were just able to afford to send their children overseas for education had to make the heart-breaking decision to recall them.”

The peg was finally fixed on 16 October 1983 – a Sunday. The Wall Street Journal called it a “drastic effort to bolster the… sagging currency,” while the Financial Times suggested it would cause problems as well as cure them, particularly the high cost of maintenance. But for many Hongkongers it was a decisive act that brought a level of calm amid troubled times.

Chief Executive Norman Chan warned in December 2016.

Economic concerns have traditionally underpinned oppo-sition to the peg. In 2012, Chan’s predecessor at the HKMA, Joseph Yam, argued in favour of a switch to a more flexible currency regime similar to that of Singapore, a market more like Hong Kong’s.

Economists such as Rajan say times may have changed, noting that if China focuses on domestic demand and greater intra-Asian trade linkages, and Trump’s U.S. becomes more inward-looking, “then the Hong Kong dollar peg may become much more con-straining going forward.”

Analysts warn of the need not to signal a change too early. “If you do not show your com-mitment to a specific decision, you risk that currency markets start speculating on upcoming changes,” notes Bert Burger, Senior Economist at trade credit insurer Atradius in Amsterdam and author of a 2016 research report, The Hong Kong dollar peg: change will come.

The Mainland unit has long been considered the most likely currency to constitute a hypo-thetical new peg, or at least be part of a trade-weighted group of currencies. Burger argues in favour of an eventual shift to a

peg with the renminbi. “First, the renminbi has to be fully con-vertible, and after that the Hong Kong dollar could be pegged to a basket.”

In February, outgoing finan-cial secretary John Tsang noted that, “In the short term, there is no possibility to see any change” to the current peg but suggested that this could be reviewed in the very long term as the renminbi would one day be liberalized and convertible.

However, that could be far in the future. “I don’t think the renminbi is likely to become that important to Hong Kong in the short term,” says Kun Li, Senior Analyst at Selerity, a research house in New York. “Few coun-tries use the renminbi as a trade currency. While Hong Kong is a major offshore renminbi centre, this offers benefits only to a few financial firms.”

Economists believe China is unlikely to apply undue pressure on Hong Kong. “Those in Beijing are realists,” says Steve Hanke, Professor of Applied Econom-ics at Johns Hopkins University in Baltimore and an architect of several successful currency boards. “Why would the Chinese government, or anyone in Hong Kong, want to give up a link to the world’s premier international currency?”

May 2017 15

“Like” and recommend us on Facebook

www.facebook.com/hkicpa.official

Hong Kong Institute of CPAs

Like Us.indd 1 15/1/16 7:04 PM

Thought leadershipAlice Telfer & Michelle Crickett

aplus

May 2017 17

Making a judgment in a com-plex world, with principles-based accounting standards,

is not an easy task. The success of narrative and financial reporting relies on our ability to be able to make sound judgments and demonstrate our reason-ing for these judgments.

We asked a group of senior char-tered accountants (including finance directors, audit partners, audit com-mittee chairs, regulators and standard setters) to share their key principles for making a sound judgment.

A new guideThe result is A Professional Judgment Framework for Financial Reporting Decision Making, offering practical guidance for decision makers involved in narrative and financial reporting.

Irrespective of whether you are a preparer, auditor, audit committee member, or regulator, this practical guide provides a structure to help you come to a sound judgment when you have a complex reporting decision to make or are new to decision making.

“Confidence in financial report-ing and in principles-based standards requires us to demonstrate collectively that, as professionals, we are capable of making sound judgments. I believe that this professional judgment framework is vital for the future of the profession,” said Sir David Tweedie, former chair of the International Accounting Standards Board and former ICAS president.

Core principlesThe framework identifies core prin-ciples and provides a structured process

to guide decision makers through how to make, assess, and document signifi-cant judgments. Some of the principles supporting the formulation and chal-lenge of a professional accounting judg-ment are considered below.

Ensure that all relevant and determinable information has been collected and analysed – this requires an understanding of the purpose, legal terms and economic substance of the transaction, as well as expected cash flows and any uncertainties.

Assess the applicable accounting standards and other relevant guid-ance – in the absence of a relevant standard or specific standards, it can help to consider the treatment of similar transactions. The conceptual framework can be useful to clarify overarching principles on definition, recognition and measurement. There may also be precedents, accepted industry practice or national generally accepted accounting practice which can provide a steer. Ultimately, one needs to consider if the resulting relevant and reliable and gives a fair presentation of the transaction.

Ensure due process is followed – aspects include assessing a range of alternative accounting treatments, identifying any threats to objectivity, managing this and consulting with others before obtaining appropriate endorsement for the judgment.

Assess and challenge the judgment it is helpful for auditors to stand back and review the overall picture. Individual client judgments may appear reasonable but cumulatively may result in a higher risk of misstatement.

Applying appropriate scepticism in discussions with the client is key. For audit committees, creating the right environment to effectively review and challenge the judgment is critical. At the meeting, this requires the facts to be clearly laid out, the right people in attendance, sufficient time for debate and a culture conducive to debate and challenge.

At each stage, from preparation to audit, challenge by the audit com-mittee and assessment by regula-tors, a professional judgment can only be made based on the facts and circumstances at the time, without hindsight. The basis of a significant judgment and its subsequent assess-ment and challenge must be suitably documented. This includes noting any disagreements, or difficulties in the assessment as well as how they have been overcome.

A principles-based approach to standard setting is a key driver of quality reporting. You can help contribute to improved narrative and financial reporting worldwide by using this guidance and building it into your current decision making procedures. The guide can be downloaded free of charge from www.icas.com.

We welcome comments on this framework from A Plus readers. Any queries or feedback regarding this publication can be sent to [email protected] more about professional judg-ment, what it is and how to handle it, on page 48 (Technical update).

This article originally appeared on the ICAS website.

Alice Telfer, Head of Business Policy and Public Sector and Michelle Crickett, Director of Research at the Institute of Chartered Accountants of Scotland, report on the new ICAS guidance on making a professional judgment

Navigating principles-based standards in financial reporting

com.–

Leadership profileRichard Lancaster

18 May 2017

aplus

POWER TO THE PEOPLECLP Holdings, one of Hong Kong’s two electricity providers, is a frequent winner at the Institute’s annual corporate governance awards. Chief Executive Officer Richard Lancaster explains to George W. Russell how the company provides affordable and reliable service while practising sound community stewardship

R ichard Lancaster remembers the days when telling fellow dinner-party guests that he worked for a power company was a conver-sation stopper. “Nobody knew what to say,” recalls the Chief

Executive Officer of CLP Holdings, Hong Kong’s largest utility company. “Today,” he adds, “it’s like a lightning rod. Everybody wants to talk about renewable energy.”

But the idea of a Hong Kong powered by renewable energy remains a distant dream. The most visible source is the solitary wind turbine on top of a hill on Lamma Island, which was opened in 2006 as a demonstration facility by Hongkong Electric, and which produces just 100 kilowatts of electricity, enough to power 250 of Hong Kong’s 2.5 million households.

At that time, CLP was also asked to build a demonstration wind turbine. “We looked all over Kowloon and the New Territories to find a site where we could do it but much of the land outside the urban area is country park,” Lancaster recalls. “We couldn’t actually find a site on land here, and we did identify a site for an offshore wind farm but the cost was prohibitive.”

Today, CLP generates much of Hong Kong’s electricity through the coal-fired Castle Peak Power Station in Tuen Mun and the gas-fired plant at Black Point, also in Tuen Mun. However, the Castle Peak facility is a significant source of air pollution in Hong Kong, underlying a global problem with fossil fuels.

Photography by Juliet Shayne Lui

May 2017 19

Leadership profileRichard Lancaster

“To reduce our carbon emissions we need to reduce the amount of coal we are using and shift towards natural gas and nuclear power,” Lancaster acknowledges. (CLP buys about 80 percent of the output from the Daya Bay nuclear power station in Guangdong for its Hong Kong customers).

But he warns that any global transition will be gradual. “Coal currently supplies most of the world’s electricity,” Lancaster says. “You can’t shut down coal-fired power stations and stop coal mining today because the lights would go out all over the planet.”

The heart of CLP Group’s mission, after all, is to keep Hong Kong up and running. “If we don’t do our job properly the lights go out,” says Lancaster. “We’re an important part of Hong Kong’s economy and we are part of the fabric of society,” he adds. “You can call it corporate social responsibility, you can call it what you like, but it’s a big responsibility that’s always fallen on our shoulders.”

Defining data pointsGood corporate governance, says Lan-caster, is about being in touch with stake-holders. “In simple terms, I look at it as doing the right thing and what’s right for the business with a long-term view in mind,” he says. “It’s about understanding what the issues are, and moving your business at the right pace to be in line with what expecta-tions are of you as a company.”

The company is a consistent winner at the Institute’s Best Corporate Gover-nance Awards. Last year, CLP was the only diamond award winner – the highest category – as was the case at the 2015 and 2014 awards and has won more top awards in the Hang Seng Index category than any other company.

CLP is one of a handful of companies that produce financial statements largely

in line with the principles of the Interna-tional Integrated Reporting Framework. “I think our business is quite a good fit with integrated reporting,” he says. “[It] is an effective and efficient way for us to commu-nicate the complexity of our business to our many stakeholders.”

One source of that complexity is new technology. “The information that’s avail-able is revolutionizing the way that we approach our business,” says Lancaster. “We are seeing customers installing their own renewable-energy systems on their rooftops, so no longer is electricity a one-way flow. It’s going backwards and for-wards between customers and the utility.”

Not long ago in Hong Kong, Lancaster points out, a meter reader visited a house-hold every two months. “That means you had six pieces of data on how a customer uses electricity in a year. With smart meters, we have real-time information. How we can help make sense of that is revolutionizing the way we interface with our customers.”

The Internet of Things, where almost every appliance is interconnected, is the next technological revolution. “You have a fridge these days that’s got more computing power than some of the first computers,” Lancaster says. “Everything you buy means that there is a huge amount of new informa-tion available and that is revolutionizing electricity networks as well.”

As CEO, Lancaster sees his role as one of temporary stewardship over a 115-year-old institution through a period of funda-mental change. “It’s my job to steer the ship through this period and see it in a better position, and in a more successful position, than when I started.”

Mixed market signalsOriginally from Sydney, Lancaster gradu-ated with a degree in electrical engineering

“ You can call it corporate social responsibility, you can call it what you like, but it’s a big responsibility that’s always fallen on our shoulders.”

20 May 2017

aplus

“ It’s my job to steer the ship through this period [of change] and see it in a better position, and in a more successful position, than when I started,” says Richard Lancaster

from the University of New South Wales and worked with power companies in Aus-tralia before joining CLP Group 25 years ago. He became CEO in 2013.

Like accountants, he notes, engineers are familiar with numbers and have innate problem-solving skills. “I also come with an operational background,” he says. “I’ve worked in large industries managing large and complex workforces. Managing people is also a skill that I’ve developed over the years and I think that combination fits well for CLP in this current chapter of its history.”

As well as experiencing technological change, Lancaster has witnessed the company expansion to the Mainland, India and Australia. “There are 300 million people in India that still don’t have access to electricity,” Lancaster points out. “Just having enough electricity to charge a mobile phone, to keep a light on so that the children can study at night, and having a television set going would be life-changing for many families.”

While nearly all of the population have access to electricity in China, pollution is a life-threatening problem. “Transitioning

May 2017 21

Leadership profileRichard Lancaster

from reliance on coal towards more renew-ables and nuclear power – and keeping that transition affordable – is a key issue.”

Australia is a different market again, with an abundance of energy resources yet pricing levels almost double that of Hong Kong. “There are different regulatory authorities – the federal government and the state governments – so getting a consistent policy in Australia in a very complex market environment has been a challenge.”

In Hong Kong, another challenge for CLP is human resources. “There’s very little industry in Hong Kong, and in the electricity industry there’s nowhere we can go to bring in skilled people, so we have to develop

our own,” says Lancaster. “That’s been our approach right from the start: we grow our own talent, we train our own people.”

Hong Kong’s ever-expanding financial services sector has been luring university students away from the science, technol-ogy, engineering and mathematics majors that CLP needs. “We worked tradition-ally with universities, but now we’re going down into the secondary schools to encourage people into engineering as a career,” he says.

“We work hard to be an attractive employer,” Lancaster adds, “so we offer competitive pay and benefits, but it’s really about making sure we’re

providing interesting and fulfilling career opportunities.”

Lighting the way aheadLancaster expects the future will require a more participatory role for CLP. “We are experts, we do know this industry, we’ve known it for more than a century,” he says. “We know all the day-to-day issues that need to be managed and it is a complex business just keeping the lights on in a territory the size of Hong Kong with seven million people.”

CLP will continue to expand in its existing markets. This year, the company completed its acquisition of a 17-percent

22 May 2017

aplus

CLP is a consistent winnerat the Institute’s Best Corporate

Governance Awards. It was

the only diamond award winner, the highest category, last year as well

as in the 2015 and 2014 awards.

stake in Mainland-based Yangjiang Nuclear Power. And Lancaster sees a more public role in terms of thought leadership through an eventual transition to non-fossil fuels. “I think the change that we’re seeing is that we need to be more at the forefront of public policy and debate and contributing our views and expertise,” he says.

He says it is important that the energy industry work very closely with governments in developing long-term energy plans. “It’s not to say that we should be deciding public policy but we should be informing the government

and the communities and outlining the choices, the options, the trade-offs and the pros and cons.”

Stabilizing greenhouse gas emis-sions, Lancaster points out, means that there’s no net increase in tempera-ture. “Effectively that means at the end of the day that whatever green-house gas emissions we produce have to be reabsorbed back into the oceans and the forests so that there is a zero-net level of emissions. To get to that we will have to have the majority of our power produced from zero carbon emitting sources.”

The intangible nature of electricity as a commodity is paradoxical, Lan-caster observes. “We are producing and selling a product that is invisible – you only see it when it is in action, but you can’t put your hands on it, you can’t smell it, it has no colour, it has no per-sonality,” he says. “It’s just an invisible product. So utilities have tended to be behind the scenes, feeling that they’re doing the best job when cus-tomers are not thinking about them. That’s all changing.”

“ We know all the day-to-day issues that need to be managed and it is a complex business just keeping the lights on in a territory the size of Hong Kong with seven million people.”

Before joining CLP Group, Lancaster graduated with a degree in electrical engineering from the University of New South Wales and worked with power companies in Australia

May 2017 23

C

M

Y

CM

MY

CY

CMY

K

1065_Comm_HKICPA_sourceAD_1_output.pdf 1 5/11/15 3:03 PM

How to...Yin Toa Lee

aplus

May 2017 25

For many Hong Kong compa-nies, especially in the retail sector, leases play a critical

role in their business operations. Because most lease transactions (e.g. operating leases) are off-balance sheet today, accounting for leases under current lease standards often does not require significant efforts. Many preparers understand that the new IFRS 16, effective in 2019, would require a company to do more than simply converting its existing operating lease com-mitments disclosure to lease assets and liabilities. They are aware that its implementation could result in changes to the policies, processes, controls and information technology systems that support lease account-ing and tax. However, what is the commercial reality around IFRS 16 that has often been overlooked?

Under the new standard, lessees will recognize the present value of lease payments over the lease term as a lease liability on the balance sheet. Similar to current accounting, the definition of lease payments excludes certain variable payments, and the lease term includes only those options that are reasonably certain of being exercised. For example, as the consumption appetite on high-end luxury stores from Chinese tourists has declined recently, Hong Kong lessees may reassess their needs when negotiating their lease terms and payments with their premium mall landlords. A higher proportion of variable payments tied to monthly sales as compared with fixed payments or shorter initial lease terms may result in smaller lease liabilities.

Some Hong Kong lessees may reassess whether buying an asset

would be more advantageous than leasing it, even though the real estate prices in Hong Kong are still very high as compared with the rest of the world. In buying a property, a company needs to either have plenty of cash reserves on hand or be able to obtain financing from banks. For a newer property, it would be easier to obtain financing with a more extended term than an older property. If financing is obtained, the impact of having the self-use property and bank borrowing on balance sheet would be similar to the accounting under IFRS 16 to have the right of use assets and lease obligation grossed up. However, there are certain considerations to keep in mind between deciding to buy or lease. When buying, you actually make an investment to own the property down the road as your own assets as opposed to be paying for the landlord’s assets. In Hong Kong, with the escalating real estate prices particularly in the higher end premium properties, there could be substantive capital gains when those self-owned properties are sold off in the future which are tax exempt.

Typically, companies would separate the operating legal entities responsible for running the business with the entities holding the prop-erties to keep the properties clean from being comingled with the rest of the group’s business when the properties are sold or replaced with better properties. Such properties could be leased back to the operat-ing companies intragroup for a more reasonable rent as opposed to having unpredictable rent increases after the current lease term for third-party leases. However, when buying with bank loans, if you do not have a strong relationship with banks to

negotiate to exclude the repayable on demand clause, the total bank borrowing on balance sheet would be classified as current as opposed to current and non-current as in the case of lease obligation. Buyers should be cautious of such provi-sion as they could be obscured in fine prints in the loan contract and auditors could require it be classi-fied as current during an audit. At a minimum, companies deciding whether to buy or lease today should be aware of the potential commer-cial impact of the new standard on their business on top of the financial statements.

Lessees should understand that there are certain risks associated with the terms of such commercial approaches. Hong Kong companies should consider any changes to their commercial approach to lease contracts in the context of whether to be opportunistic when a good chance arises rather than sticking to their long-term plans. For example, a company may consider balancing a lower lease liability from a shorter lease term for a property against the security of longer-term access to the properties at a higher lease liability. However, lessors that are the larger real estate companies in Hong Kong may have more superior bargaining power to not take on the additional risk associated with variable pay-ments and shorter initial lease terms. While companies should not only make commercial decisions based on accounting results or vice versa, they should be aware of the account-ing consequences associated with their commercial reality.

The views reflected in this article do not necessarily reflect the views of the global EY organization or its member firms.

…prepare for the commercial reality of IFRS 16 in Hong Kong

The implementation of IFRS 16 Leases is less than two years away. Capital Markets Partner at EY looks at the resulting changes to business practices for Hong Kong companies

RecruitmentTalent shortage

A recent survey conducted by the International Federation of Accountants revealed a worrying shortage of accountants in major economies, especially in small- and mid-sized practices. A Plus looks at the recruitment situation in Hong Kong and what firms are doing to attract and retain talent

HIRING FOR THE FUTURE

Illustrations by Yau Hoong Tang

How can the accounting profession attract the millennial generation? The work-life balance issue faced

by junior staff, competition from jobs in the financial and other sectors, fewer students undertaking accountancy at university, and an uncertain economic outlook are combining to create a shortage of talent, especially in small- and mid-sized accounting firms.

Hong Kong’s recruitment woes reflect a global shortfall in the number of accountants working for non-Big Four firms. A recent survey by the International Federation of Accountants showed that attracting and retaining staff ranked among the top four challenges for them for the first time. (See IFAC survey takes note of smaller firms’ issues on page 31).

While supply and demand of accountants has fluctuated over the decades, this might be the first time the profession has been overlooked by a generation. “The accounting sector has been less appealing to the millennial generation because of its demanding working environment,” suggests Stephen Weatherseed, Managing Director of Mazars Hong Kong and a Hong Kong Institute of CPAs member.

Furthermore, fewer students are entering the profession. “We have seen a general drop in the number of students applying for the undergraduate accounting degree programme in the past few years,” says Edmund Wong, Associate Director of the School of Accountancy at Chinese University of Hong Kong and an Institute member.

Recent changes in regulation – from anti-money laundering efforts to tighter banking compliance and massive reshaping of global tax regimes – have created new challenges for businesses and a need for more people. “Capable staff in the area of forensic and compliance are in high demand,” says Weatherseed.

In addition, Hong Kong’s financial sector is expanding into new areas such as financial technology (FinTech), biotechnology, information technology and start-ups in banking, insurance, retailing and other areas – serving both Hong Kong and Mainland markets – where accountants will be needed.

It is not just the specialized accounting roles that are experiencing a shortfall, say Hong Kong-based recruiters. “Traditional audit and assurance are also still in demand,” says Jacky Cheung, Manager, Commerce & Industry (Accounting and Finance, Audit and Taxation), at Morgan McKinley.

Clement Chan, Managing Director, Assurance, at BDO and a former Institute president, says the biggest shortfall for his firm is junior staff. “The shortage is clearly on the grades between three years and five years of experience, where the attrition is most damaging.”

New market dynamicsThe worsening staff shortages are underscoring the important role of recruiters.

e also hel them rms n e an ng talent options,” says Carol Cheung, Associate Director, Financial Services, at Robert

“We have seen a general drop in the number of students applying for the undergraduate accounting degree programme in the past few years.”

26 May 2017

aplus

May 2017 27

RecruitmentTalent shortage

28 May 2017

aplus

Walters, and an Institute member. “Employers sometimes come to us with a job title, and instead of just looking for talent with that title, we help them identify alternative options such as talent with transferrable skills who fit.”

Market considerations – from a slowing economy in China, a fluctuating trade environment given the threat of protectionism from the United States, political instability in Europe and uncertainty over Hong Kong’s future status as a gateway to China – are also affecting accountants’ career choices.“Although most candidates are still open to opportunities, we are finding that they are being more conservative in their job searches,” says Jay Bhatnagar, Associate Director, Accounting and Finance, at Hudson, another recruitment firm. “Given the changing market dynamics, we find that most candidates need to be sure about a new role before they make a decision.”

Bhatnagar says recruitment firms are increasingly employed to use their influencing abilities to help CPA firms “poach” staff from rivals. “Sometimes it is difficult, given the sensitivities involved for CPA firms to directly approach talent from their competition, but this is an area where recruitment firms have been adding value,” he says.

Smaller firms face a two-fold competitive threat to retaining key staff. The first is larger accounting firms that are looking for people with previous experience in CPA firms so that they know their basic auditing skills are sound. The second threat is from private-sector companies, often at a higher salary. “There is a strong demand for accounting professionals with compliance and the latest regulatory knowledge who at the same time could apply those skills under business circumstances,” says Cheung at Robert Walters.

In response, say recruiters, CPA firms will have to devise strategies to retain talent. “Some of these,” says Cheung, “include fast-track and clear career progression opportunities for current personnel, better bonuses given out half-yearly, and secondment opportunities, such as to overseas offices.

Shifts in influenceAs the IFAC survey illustrated, the dearth of talent is not confined to Hong Kong. “There is a talent shortage in the U.S. accounting profession,” Gary Bolinger, President and Chief Executive Officer of the Indiana CPA Society in Indianapolis, tells A Plus. “Among the factors is the increasing competition from other professions seeking people with similar kinds of skill sets required in the accounting profession.”

And Indiana is not alone. From the West Coast to New England, the U.S. accounting sector could barely cope with this year’s tax season. “There are more jobs than there are accountants at the moment,” Amy Pitter, President and Chief Executive Officer of the Massachusetts Society of CPAs, told The Boston Globe in February.

In the United Kingdom, accountants are entering the corporate sector earlier than before, creating a brain drain from firms.

“Candidates who are interested in pursuing careers in specialized functions such as audit or taxation tend to be light on the ground,” says Paul Buchan, Principal Consultant at the Edinburgh office of Eden Scott, a recruitment service.

Other English-speaking nations experiencing an accountant shortage include Canada and South Africa. New Zealand, a relatively small economy of just 4.6 million people, has been historically short of CPAs. “Those becoming qualified go on to their overseas experience, such as to the U.K.,” explains Angela Cameron, Managing Director of Consult Recruitment in Auckland.

New Zealand, like Australia, saw an influx of Hong Kong-qualified accountants immigrating in the years before the 1997 handover of the territory to China, but that exodus has slowed since then.

Instead, CPAs are now flocking to the Mainland, exacerbating the domestic short-age. “We can see cases where corporations relocate their regional office from Hong Kong to other locations such as Shanghai and Singapore,” says Cheung at Morgan McKin-ley. “Often they will offer opportunities for staff to relocate and some corporations who set up offices in China may still prefer Hong Kong candidates to take up the role.”

Chinese companies are also hiring more in Hong Kong, due to an “increase in focus by Chinese insurance, asset management and banking institutions to grow a stronger foothold in Hong Kong,” a Morgan McKinley report noted in January.

The focus on China is changing overseas recruitment patterns. “The common challenge for recruitment outside Hong Kong is a lack of Chinese-language capability,” notes Chan at BDO. “If we look outside Hong Kong, normally we turn to the Mainland, Malaysia or Singapore.” Chan says the firm considers

“Given the changing market dynamics, we find that most candidates need to be sure about a new role before they make a decision.”

May 2017 29

aplus

candidates from the U.K., U.S. or Australia on an individual basis.

Cheung at Morgan McKinley agrees, noting that Hong Kong accounting firms’ need for external hiring is no longer high. “The majority of local accounting professionals can already fulfil the requirements from employers,” he says. One exception, he adds, is the globalization of tax. “Some positions require [knowledge of] specific countries’ accounting or taxation systems.”

Appealing to millennialsTo ensure talent remains available – and to attract more young people into the profession – Hong Kong’s accounting community will have to refashion its image. “We should focus on presenting the right message,” says Weatherseed at Mazars. “We have a strong culture and attractive working environment – friendly, creative, dynamic, international – which is what millennials are looking for.”

Some firms are moving away from fixed working hours to accommodate the demands of the new generation. “A number of our staff either currently or used to work on a schedule that is different from our normal working hours and days,” says Weatherseed. “We are more open to explore flexible working arrangements.”

Recruitment firms suggest accounting firms embrace the latest communications and media technology and spread a globalized mes-sage. “Accounting firms are increasingly using social media to build up their brand and attract talent,” says Bhatnagar at Hudson. “There is an increased focus on campus recruitment and they are also looking at luring Hong Kong people from other parts of the world.”

Cheung at Robert Walters says that even though international recruitment has declined, Hong Kong accountants gain exposure through talent exchanges. “Overseas accountants are seconded to Hong Kong offices and vice versa,” he says. “This is a good way to retain existing accountants.”

Wong says CUHK has streamlined its professional accountancy programme to lure more candidates. “It aims to prepare our students to acquire a global mindset and an understanding of international accounting practices and issues,” he says.

Global accounting stream students will work as summer interns in the Shanghai, Chongqing and Shenzhen offices of the Big Four firms, take a two-week course at Utrecht University in the Netherlands and visit companies and professional accountancy bodies in London.

Accounting students will also be more exposed to new technology at CUHK. “The school will launch a new course in big data in the coming academic year,” Wong adds. “We expect to offer more courses related to technology and analytics in the near future.”

Millennials, say accounting firm consultants, value flexibility, work-life balance and organizational culture. “They want to know your firm’s values,” says Jeff Phillips, Chief Executive Officer of Accountingfly, an accounting recruitment platform in Florida. “Give them a great place to work and they will transform your organization.”

IFAC survey takes note of smaller firms’ issues

The annual International Federation of Accountants Global SMP Survey attracted 5,060 responses from 164 countries, and was held from October to November 2016.

Attracting new staff and retaining existing staff ranked among the top four challenges identified by respondents for the first time. The other three were attracting new clients, keeping up with new regulations and standards, and pressure to lower fees.

Many of the questions addressing the impact of personnel issues were asked for the first time. Finding qualified staff (at all levels) and retaining qualified staff (at all levels) were considered to have the greatest impact, with 45 percent and 41 percent, respectively, viewing the impact as high or very high.

Of the respondents, 31 percent were based in Asia Pacific. Among the others, 38 percent came from Europe, 14 percent were from Africa, Central and South America and the Caribbean accounted for 7 percent, and 5 percent each were based in North America and the Middle East.

In terms of practice size, 35 percent were sole practitioners, while 36 percent came from practices with two to five partners and staff. Partners, sole proprietors or owners made up 76 percent of respondents, with directors representing 7 percent and senior managers and managers accounting for 12 percent.

“We have a strong culture and attractive working environment – friendly, creative, dynamic, international – which is what millennials are looking for.”

May 2017 31

Success ingredientY.K. Lee

From his busy Taipei headquarters, Y.K. Lee manages the back-office functions of Branded Lifestyle, a company with several clothing brands and more than a thousand of bricks-and-mortar stores stretching from Korea to Malaysia. He tells George W. Russell why he relies more on data than instinct

TAILOREDSOLUTIONS

The evening rain is momentarily torrential, lashing the windows of the Fung Group building located in Taipei’s busy Neihu District, a gentrifying neighbourhood of cheap noodle stands and chic cafés,

pristine technology parks and crumbling shop houses. Inside, the offices are abuzz as senior managers leave a meeting

convened to discuss a potential transaction. They don coats and scarves to brave the chilly Friday evening, their cold-weather gear incongruous in a conference room lined with racks of short shorts and skimpy tops from the group’s Hang Ten range.

“Every day is like being a fire fighter,” says Y.K. Lee, Chief Financial Officer of Branded Lifestyle, a retail clothing company with operations in Taiwan, Korea, China, Singapore, Malaysia and Hong Kong. “Even if I’m busy, people still come to me and ask questions – that’s my day.”

Lee, a Hong Kong Institute of CPAs member, runs the company’s finance and accounting, human resources, information technology and corporate services. “Basically I’m the head of the operational support group,” he says. “My role is overseeing the back office of every country that we operate in.”

Apart from the casual Hang Ten brand, founded in the United States in 1960, Branded Lifestyle operates the Arnold Palmer sportswear label; Roots, a Canadian outerwear brand; Hong Kong’s Leo clothing range and H:Connect, a Korean fashion house established in 2006.

Photography by Craig Ferguson

32 May 2017

aplus

Y.K. Lee worked at KPMG for eight years before joining Fung Group’s corporate governance division

May 2017 33

Success ingredientY.K. Lee

34 May 2017

aplus

Lee says his group’s key task is to support the company’s “front office”, such as its design, sourcing, retail and marketing departments. “They all face our customers and we have got to serve them,” he says. “At the same time we have to make sure there are proper checks and balances.” Thus, the back offices of each individual country operation report not to their own country head, but to Lee.

He joined the retail apparel sector in 2007, as it began to ex-perience fundamental changes caused by the rise of electronic commerce. “Retailing is basically about knowing your customers and how to serve them,” he says. The way they bought in the past is not the way they buy now. “Even next month, you don’t know how they would want to buy.”

Today, Lee finds himself in the world of global fast fashion, where consumer tastes change even more rapidly, dead-on logistics are vital, and bricks-and-mortar stores compete with the Internet. “It’s more challenging because we make a lot of decisions based on data instead of instinct.”

Bricks versus clicksBranded Lifestyle is unusual in that it is a regional multinational – its parent, Branded Lifestyle Holdings, is part of the retailing arm of the Fung Group, which also owns the Li & Fung sourcing and logistics empire – with its

headquarters not in Hong Kong or Shanghai or Singapore but in Taipei.

“There are a lot of designers here and the major departments are all here in Taiwan,” says Lee. “The previous owner was also from Hong Kong who lived here and set up the head office.” More importantly, he says, Taiwan remains the company’s largest operation. “In Taiwan we have about 430 shops and it contributes 40 percent of the group’s total sales.”

Korea, Lee adds, has about the same number of stores and contributes a similar share of sales. China has about 235 stores, of which 208 are H:Connect. There are a total of 20 stores in Singapore, 12 in Malaysia and 9 in Hong Kong and Macau.

From the Taipei headquarters, Lee and his team crunch sales numbers. “We set up a data

analytics team here centrally, so we can go into, say Korea, and look at the numbers,” he says. “We say, ‘Hey, we noticed that this shop yesterday was not doing well – the average amount per transaction was very low – so what’s the problem?’”

Lee has discovered there is no one-size-fits-all remedy for every market. “In Taiwan, customers still prefer to go to the shops and buy. In China, it’s totally different – there they buy online and Tmall is our biggest platform. If you look at the logistics costs, countries with e-commerce tend to have a higher cost because you need more people to do the picking and packing and deliver every individual pack.”

Thus the logistics costs in Taiwan are much lower as a percentage of sales than in China. “We can’t standardize everything,” Lee notes. “We can’t say we’ll limit the logistics cost to 2 percent of the transaction. It wouldn’t work. Colleagues in China would have to go back to bricks-and-mortar.”

Most of Branded Lifestyle’s products are made in China. Lee has witnessed an easing of cross-strait restrictions over the years. “In the past, there were shirts you couldn’t import from China and they had to be made in Taiwan at a higher cost,” he recalls. “Now the costs in China are getting higher, so we’re going to places like Bangladesh and Vietnam, but still China has better quality.”

Branded Lifestyle has 430 stores both in Taiwan and Korea, 235 in China, 20 in Singapore, 9 in

Malaysia, and two each in Hong Kong

and Macau.

“ In Taiwan, customers still prefer to go to the shops and buy. In China, it’s totally different – there they buy online and Tmall is our biggest platform.”

May 2017 35

Success ingredientY.K. Lee

Return to the regionThe Malaysia-born Lee has led a cosmopoli-tan life ideal for an executive at an Asia-Pacif-ic multinational. He grew up speaking Manda-rin at home but is also fluent in Malay, English and Cantonese, which he picked up from watching television. “When I went to school people would ask, ‘Did you watch that TV pro-gramme last night?’ So I had to learn it.”

As the son of a businessman, Lee found accounting an easy career choice. “When I was in secondary school I knew I wasn’t very good in science,” he says. “Even before I went to university I knew I wanted to study

business, and if you want to study business you had to choose accounting.”

He left Malaysia to attend the University of Manchester in England. After graduation he worked with a local accounting firm before joining Grant Thornton in Oxford. “That’s where I qualified as a chartered accountant,” says Lee. “By then I had spent five or six years in England and I thought that was enough.”

Lee began to plan an Asia-Pacific return, with Tokyo and Hong Kong at the top of his wish list. “At that time there were a lot of things going on in Asia,” he recalls of the late 1990s. “China was booming. Back then,

KPMG would recruit 40-50 people who were semi-senior. I went to an interview in London and they made me an offer as an auditor in Hong Kong.” He became a member of the Hong Kong Institute of CPAs in 2000.

It was a decision Lee would not regret. “Hong Kong was very dynamic and so fast and very challenging,” he says, still with enthusiasm. “I think what you learn in three years in Hong Kong is the equivalent of what you learn in six years in the United Kingdom.In Hong Kong, you are treated like a trainee for six months, then you’re all on your own. Go into battle and just fight.”

36 May 2017

aplus

Lee says he is head of Branded Lifestyle’s operational support group, which supports the company’s “front office,” such as its design and marketing departments

“ I saw every single part of the business – the supply chain, the retail, the design – and that’s how I learned about retailing in more depth.”

Lee spent eight years at KPMG before deciding he wanted to enter the commercial sector. It was not a rushed decision. “I didn’t want to leave before I got a really good job, so I was actually looking for nearly two years,” he says. “Then I joined Fung Group in their corporate governance division.”

Joining the company in 2007, Lee’s first task was to shepherd a recent acquisition – Trinity, which owns the Gieves & Hawkes, Kent & Curwen and Cerruti 1881 brands – towards a Hong Kong listing.

Data versus instinctThe Trinity listing role also included the internal audit function. “One thing good about being an internal auditor at that time was that I was actually involved in operations,” Lee says. “I saw every single part of the business – the supply chain, the retail, the design – and that’s how I learned about retailing in more depth.”

In 2012, Fung Group bought Branded est le. th ts e bran s ran e

Lifestyle works with suppliers by lever-aging its high volumes to obtain cotton more cheaply, and help manufacturers with financing. “A lot of suppliers in China borrow at 10-20 percent interest,” says Lee. “We work with our bank to of-fer less than 2 percent so they can reduce the cost to us.”

The company’s major cost pressure is rent. In Taiwan, says Lee, landlords are

flexible. “We normally sign for three to five years but sometimes when busi-ness is not doing so great, we’ll go back to the landlord and say we know that we have committed to paying NT$100,000 (HK$25,600) a month, but can we reduce the rent for this year?”

Lee says most landlords are willing to accept less rent due to the long business relationship – but the strategy has its limits. “If the next year business is still not good we go back to them and say can we reduce the rent again,” Lee explains. “Most landlords will not agree to that but there’s no harm in trying.” The gambit doesn’t work at all in Hong Kong. “You don’t even bother looking for the landlord,” says Lee.

Outside Taiwan, Lee’s team works with staff on the ground. “I look at the profit-and-loss and if a store is about to be making losses, we suggest they need to talk to the landlord and find a way to reduce the rental. If not, maybe they need to close the shop.”

Before heading back out into Taipei’s rain, Lee has a thought. “The front office staff here make a lot of decisions based on instinct: ‘It will be raining tomorrow, so let’s sell this.’ But if you look at the number of rainy days versus the sales of that par-ticular product, it may not sell that well.

“You might think your instinct tells you something but you’re going to go back to the data,” he muses. “Perhaps instinct should be backed by data.”

May 2017 37

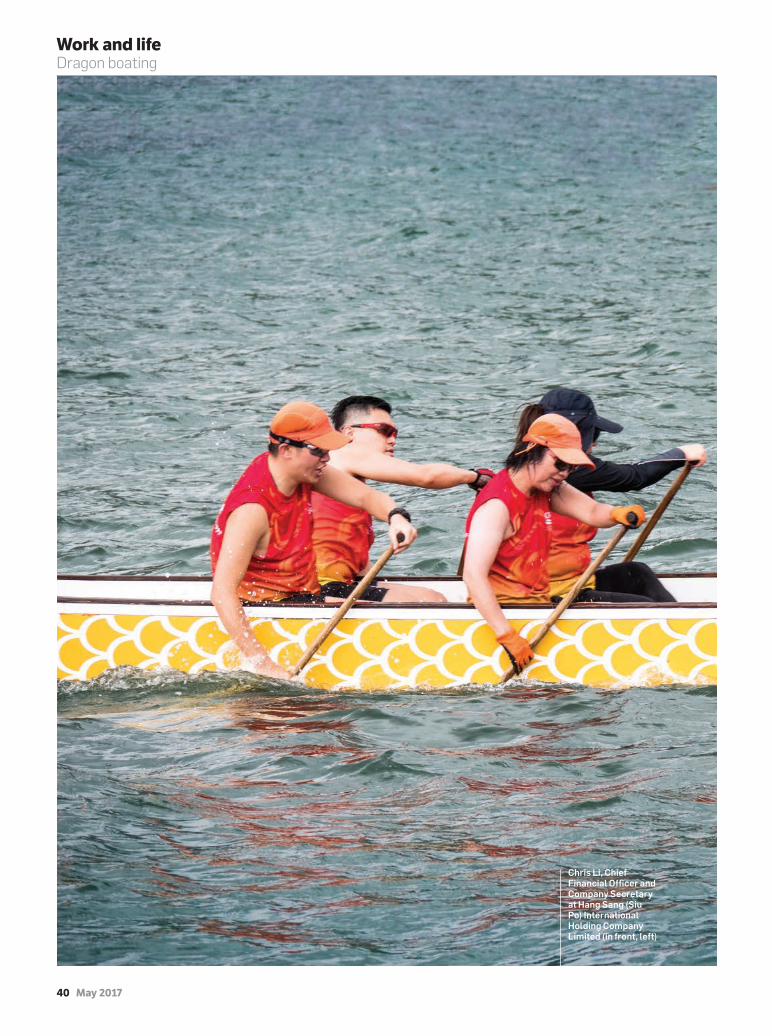

Work and lifeDragon boating

A s the first glimmers of light begin to appear on a Sunday morning, it’s not unusual to

find people still tucked into their beds and sneaking in a few extra hours of sleep after a long week of work, but for a passionate group of CPAs, the dawns of Sundays are a time of action. Chris Li, a member of the Hong Kong Institute of CPAs’ Dragon Boat Inter-est Group, gathers at Stanley’s Main Beach at 7:30 a.m. with his like-mind-ed teammates for a training session. “Dragon boating is the definition of a fun sport,” says Li, the Chief Finan-cial Officer and Company Secretary at Hang Sang (Siu Po) International Holding Company Limited. “It pro-vides a great full-body workout, and I think water sports are also excellent for taking your mind off work.”

However, dragon boating possesses benefits beyond recreation and stress relief. For Institute members like Li, they also believe the sport is highly inspirational due to the tight-knit bonds that can be formed among teammates. “Dragon boating is a sport that promotes teamwork above all else,” says Li. “With 22 people together in one boat, we all play hard to achieve one goal. It’s how the term ‛one boat one heart’ was formed.”

When asked about his most memorable experience with the team, Li brought up his first year of dragon boating with the interest group. “It was May 2013 and we were competing in the Stanley Warm Up Race,” Li remembers. The weather was poor with heavy downpours, which forced the race to be postponed temporarily until

Dragon boating is the epitome of Hong Kong’s heritage and international culture. In the heat of the summer dragon boat competitions, Julian Hwang talks to Institute members to find out how this dynamic sport extends beyond simple camaraderie

Photography by Anthony Tung

MOVING AS ONE

38 May 2017

aplus

The Dragon Boat Interest Group celebrates with its new boat in 2013

May 2017 39

Work and lifeDragon boating

Chris Li, Chief Financial Officer and Company Secretary at Hang Sang (Siu Po) International Holding Company Limited (in front, left)

40 May 2017

aplus

the rain let up. “We waited a long time, and even when it finally did lighten, it still felt like heavy drops hitting your face,” he says.