liberty holdings limited · 3. customer journey designs experience design principles customer...

TRANSCRIPT

Liberty Holdings LimitedAnalyst day – 10 April 2019

2

Agenda

12:00 – Session 1: The why and what, defined and measuredDavid Munro, Liberty Holdings Ltd, CEO

• Welcome and introductions• Strategy Visualisation and the way forward

Johan Minnie, Managing Executive: Client and Adviser Experience

• Client and Adviser centricity principles that support our purposeYuresh Maharaj, Group FD

• Financial metrics and targets

13:35 – Session 2: How Liberty is changing the ways of workingBenjamin Marais, CIO / Sunil Nagar, Executive Retail Operations

• Liberty's digital journey

14:45 – Session 3: Understanding the SIPBrian Kipps, Executive: LibFin

• The Shareholder Investment Portfolio (SIP)

15:00 – Break• Refreshments will be served

15:15 – Session 4: Fulfilling our investment promiseDerrick Msibi, STANLIB CEO

• STANLIB's strategic journeyGiles Heeger, Executive: Asset Management

• STANLIB's investment strategy and philosophy

16:15 – Session 5: Regulatory updatePhilip Harrison, Chief Risk Officer

• Prudential regulatory regime SAM

16:30 – Closing commentsYuresh Maharaj, Group FD

Strategic overview (The why?)David Munro, Johan Minnie and Yuresh Maharaj

4

5

Strategy visualisation

6

Client and Adviser centricity principles that support our purpose

We will build trust by doing the right things, first time, every time, with a can-do attitude

Clients Financial Advisers

Employees

We are people obsessed and will differentiate everything we

do through our touch of humanity

We build partnerships to the benefit of our clients in pursuit of making their

financial freedom possible

We empower our employees, advisers and partners to deliver exceptional and

intuitive human experiences

We understand our clients and their unique responses to life events

We deliver solutions tailored to their life journeys

We use smart technology as a seamless and intuitive enabler

7

Advice philosophy

8

Our advice philosophy is centered around you

“MAKING YOU THE AUTHOR OF YOUR OWN LIFE STORY”

Wherever you are in your life, we meet you in your reality

Guiding you through life’s moments, holding your dreams as if they were our own

Empowering you to achieve your goals and live your best life

9

Strategy visualisation

10

Our Exco goals are aligned to our strategic delivery

11

Liberty strategic value driver model

The metrics are seeking to measure client, financial adviser and employee experience to deliver the desired financial outcome.

12

Strategic value driver model: Metrics used to measure value

Client and Adviser Experience

• Client Net promoter score • Client satisfaction Index • STANLIB SA investment

performance• IFA Net Promoter Score • IFA Satisfaction Score • Long term insurance net

customer cash flows • Asset management net customer

cash flows • IT system stability

Employee Engagement

• Employee net promoter score• Staff turnover • Employee equity

Risk and Conduct

• LGL Capital coverage • Group operational losses

Financial Outcome1

• 1Normalised operating earnings• 1Normalised Return on Equity • 1VoNB• 1Margin • 1Sales production• 1Indexed new business (Rm)• 1RoGEV • SA Retail gross VoNB• SA Retail acquisition costs• Management expenses

SEE impact

• Policy maturities and surrenders• Claims paid (death and disability)• Annuity payments• Group skills development spend• Unclaimed benefits

1References to Liberty Holdings Ltd consolidated financial results

13* 2017 comparative not applicable due to the new prudential regulatory regime effective 1 July 2018

Measures of progress on financial outcomes

Value ofnew business margin

0.9%Dec 2017: 0.5%

Robust capitalat upper end of range

1.87 timesDec 2017: *

Return on Group Equity Value

3.8%Dec 2017: 1.1%

Returnon equity

10.1%Dec 2017: 12.3%

1 2 3 4

1% - 1.5% target range 1.5 - 2.0x target range RoGEV >12% 15 - 18% target range

+ Stringent cost management

+ Product and margin initiatives

+ Improved sales volume in second half 2018

+ Robust balance sheet + Improved variances and basis changes +

Improved earnings from SA Retail and STANLIB South Africa

+ Strong risk management capability

+ Dividend maintained

+ Stringent cost management

- Low investment market returns

+ Improving value of new business

- Investment variances, economic basis changes

- Low investment market returns

14

Setting and delivering towards strategy is a continuous process

15

Our Exco goals aligned to our strategic delivery

Session 2Session 4

Questions

Liberty’s digital journeyBenjamin Marais

18

Liberty’s information technology strategy - 2019

Key focus areas

Client and Adviser Centricity

• Partner with our clients through their life journey, and in so doing to differentiate Liberty in terms of advice, trust, smart technology, strategic partners and empowered advisers and employees

Digitalisation

• Provide access to reliable and relevant information and services, to our clients, advisers and employees, any time and any place they want it

19

WE ARE HERE!

The data and analytics journey

Stocktake Stocktake of data and analytics initiatives Rationalise list of initiatives for delivery

Drive outcomes

Refreshed data and analytics strategy

Objectives Principles

Lay foundation Ways of working Capability build roadmaps Data ownership Capacity and skills

1

• Generate value

Setting direction

What we have banked

1

2

3 4

20

Digital transformational framework

FROM A product centric organisation

TO A digital insurer, centred around the client and adviser

Products Channel Operations

Corporate Services

Information Technology

Horizon 1 Horizons 2 and 3

Source: MIT CISR

Integrated experience• Customer gains a

(simulated) experience despite complex operations

• Strong design and UX• Rich mobile experiences

including purchasing products

Future ready• Both innovative and low cost• Great customer experience• Modular and agile• Data is a strategic asset• Ecosystems ready

Silos and Spaghetti• Product driven• Complex landscape

of processes, systems and data

• Perform via heroics

Industrialised• Plug and play products

/services• Service enabled ‘crown

jewels’• One best way to do each

key task• Single source of truth

Traditional Transformed

Trad

ition

alTr

ansf

orm

edOperational efficiency

Improving operating margins

Cus

tom

er e

xper

ienc

eIn

crea

sing

NPS

Liberty

Liberty

Enablement

Operations

Solutions

Advice

Client and Adviser

21

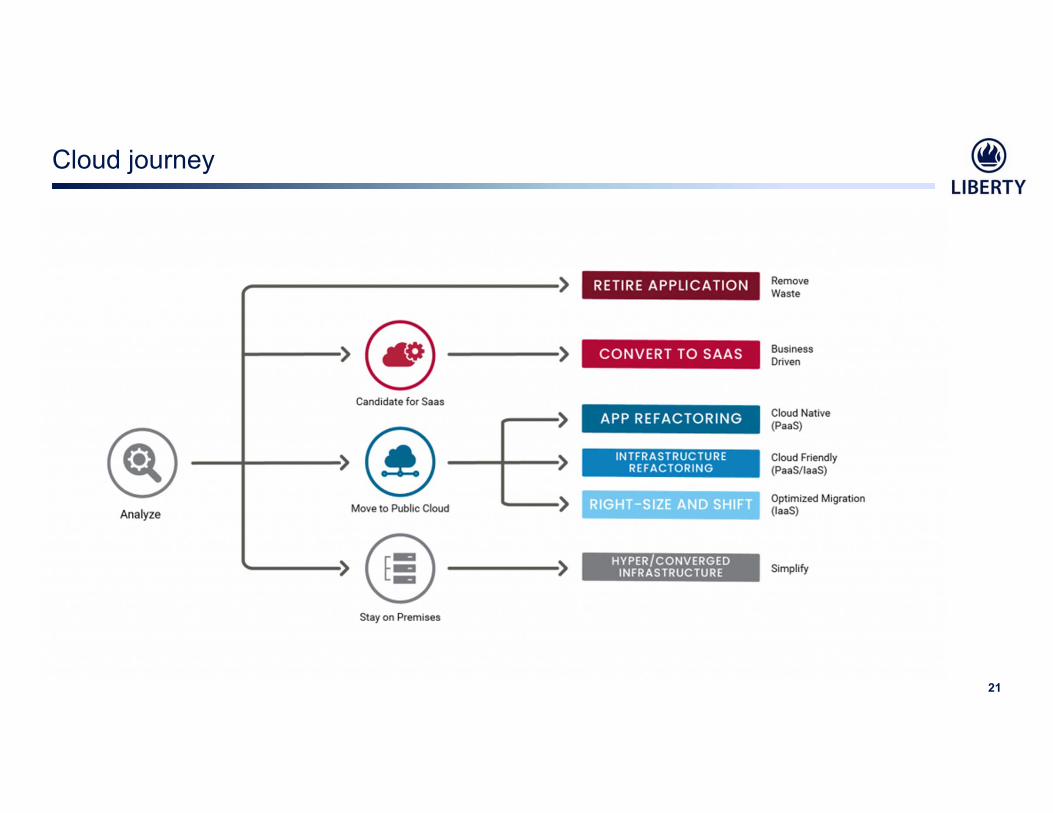

Cloud journey

22

• Integration management capability through MuleSoft enables feature teams to deliver faster by removing the complexity of integration into legacy systems

• MuleSoft allows for faster integration with third parties (e.g. atWORK) while managing security and usage – “bring your own software”

• Partnered with Standard Bank to leverage learnings and fast track the creation of a robotics process automation capability

Building enabling capabilities

23

Implementing foundational IT capabilities

Always On and Always Available

• Provide available and reliable tools and systems, at the right time for our clients, advisers and employees

Always Secure - Information Security and Cyber Resilience

• Gain the trust of our clients, advisers, employees and 3rd parties as it pertains to the security of our business platforms and the security of the information they share with us

Simplification (Simplicity for Clients, Advisers and Employees)

• Develop and implement a simplified architecture and principles guiding all simplification efforts

• Simplicity in all solutions developed for use by clients, advisers and employees, making engagement with the organisation easy

• Eliminate redundant, duplicated and fragmented capabilities, encourage reuse of developed capabilities

Data and Analytics

• Establish data as an asset to the organisation by making data services, which are used to create value for clients and advisers easily accessible

New Ways of Work (IT and Business Collaboration)

• Develop and implement the approach and structures that will enable the most efficient way for IT and Business to collaboratively drive the same outcomes

IT Employee Engagement

• Create an environment that is inclusive, values diversity and allows staff to realise their true potential whilst meaningfully participating in living out our vision

Customer experienceSunil Nagar

25

Connected experience - Context

Disbursements

Complex Servicing

Onboarding

Simple Servicing

Complaints

Collections

Claims

2. OBJECTIVES

3. CUSTOMER JOURNEY DESIGNS

EXPERIENCE DESIGN PRINCIPLES

CUSTOMER EXPERIENCE OUTCOMES

KEYCONCEPTS

CUSTOMER JOURNEYS

1. STRATEGIC CONTEXT

Focusing on delivering a simplified, connected & enhanced customer experience through better enabling our advisers & employees who ultimately deliver the experience

This will support the vision of transforming Liberty to be the trusted leader in South Africa and chosen markets by delivering superior value through exceptional client and adviser experiences

IMPROVE CUSTOMER & ADVISER EXPERIENCE

DRIVE SELF-SERVICE SCALE & ADOPTION

REDUCE COSTS IN THE SERVICE ENVIRONMENT

Reverse the downward trend in Net Promotor Score, while improving experience for advisers. Drive more consistent service quality scores across channels

Drive scale of customer self-service, with a focus on transferring ‘view’ and ‘basic do’ transactions from contact centre and email channels to self-service. A key imperative is onboarding customers to self-service

Generate costs savings in the servicing environment through the iterative deployment of self-service and automation related to customer and adviser servicing

$

26

Connected experience - Programme overview

DIGITAL ENGAGEMENT & SERVICING CARING CLAIMS EXPERIENCE EASY IN’S & STREAMLINED OUTS

CONNECTED EXPERIENCE FOCUS AREAS

DELIVERED THROUGH 6 AGILE FEATURE TEAMS

Service Management Claims Management Requirements Management

Automation Management Group API Services Data & Analytics

Risk Onboarding Knowledge Factories Regulatory Management

• Communication through Journeys

• Servicing quote refresh• Bulk Digital Signatures• Debit order tool

• NITIATIVES

FAST TRACKEXECUTION INITIATIVES

27

Adopting new ways of work and agile frameworks

• Co-located cross functional feature teams with genuine collaboration between IT and business areas

• Greater visibility of work

• Better coordination across teams through joint planning, retrospectives and scrum ceremonies

• Ongoing stakeholder engagement and showcasing of solutions

• Ensuring client centricity through the adoption of user experience design and testing

• Continuous improvement approach

• Ability to respond to change quickly

Questions

Shareholder Investment Portfolio (SIP)Brian Kipps

30

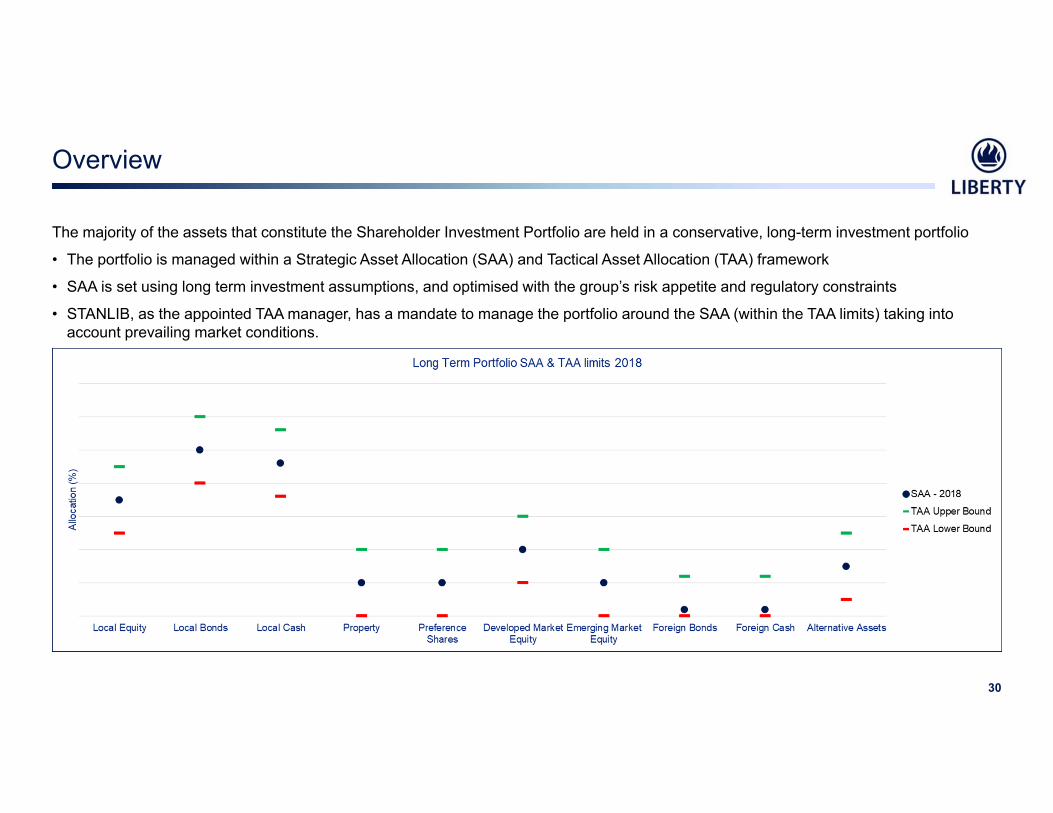

The majority of the assets that constitute the Shareholder Investment Portfolio are held in a conservative, long-term investment portfolio

• The portfolio is managed within a Strategic Asset Allocation (SAA) and Tactical Asset Allocation (TAA) framework

• SAA is set using long term investment assumptions, and optimised with the group’s risk appetite and regulatory constraints

• STANLIB, as the appointed TAA manager, has a mandate to manage the portfolio around the SAA (within the TAA limits) taking into account prevailing market conditions.

Overview

31

Portfolio construction

Earn

ings

at R

isk

Economic Value At Risk

Portfolio ConstructionOpportunity Set Set within EVAR Appetite Set within EAR Appetite SIP

Portfolio SAA constructed within risk and balance sheet constraints

The portfolio construct is designed within group risk appetite and other balance sheet constraints

Balance sheet constraints include, for example:

• Regulatory constraints

• Liquidity constraints

• Strategic investments

32

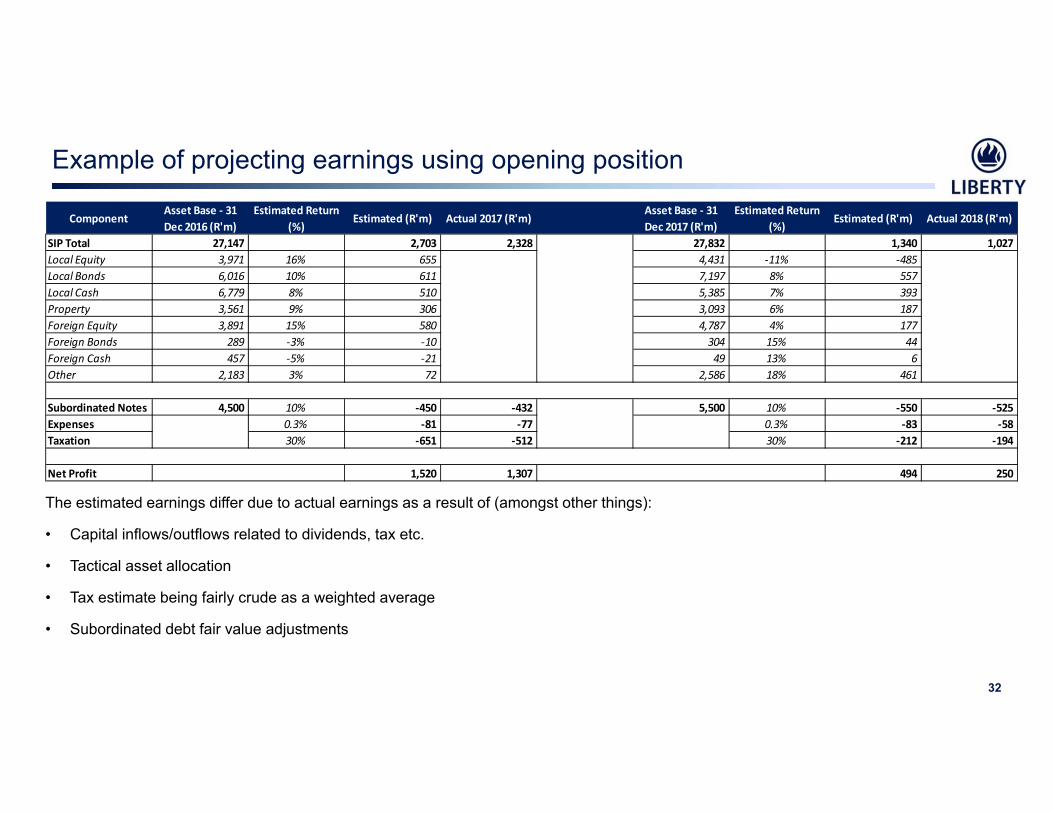

Example of projecting earnings using opening position

The estimated earnings differ due to actual earnings as a result of (amongst other things):

• Capital inflows/outflows related to dividends, tax etc.

• Tactical asset allocation

• Tax estimate being fairly crude as a weighted average

• Subordinated debt fair value adjustments

ComponentAsset Base ‐ 31 Dec 2016 (R'm)

Estimated Return (%)

Estimated (R'm) Actual 2017 (R'm)Asset Base ‐ 31 Dec 2017 (R'm)

Estimated Return (%)

Estimated (R'm) Actual 2018 (R'm)

SIP Total 27,147 2,703 2,328 27,832 1,340 1,027 Local Equity 3,971 16% 655 4,431 ‐11% ‐485 Local Bonds 6,016 10% 611 7,197 8% 557 Local Cash 6,779 8% 510 5,385 7% 393 Property 3,561 9% 306 3,093 6% 187 Foreign Equity 3,891 15% 580 4,787 4% 177 Foreign Bonds 289 ‐3% ‐10 304 15% 44 Foreign Cash 457 ‐5% ‐21 49 13% 6 Other 2,183 3% 72 2,586 18% 461

Subordinated Notes 4,500 10% ‐450 ‐432 5,500 10% ‐550 ‐525 Expenses 0.3% ‐81 ‐77 0.3% ‐83 ‐58 Taxation 30% ‐651 ‐512 30% ‐212 ‐194

Net Profit 1,520 1,307 494 250

Questions

STANLIB Derrick Msibi, Giles Heeger and Mark Lovett

Strategic update Derrick Msibi

36

Strategic update

Strengthened the Executive leadership

Comprehensive review and improvements of investment capabilities

Specific actions to address investment performance in Equity and Balanced

Appointment of:• Derrick Msibi (CEO) 2017• Giles Heeger (Exec Asset Management) 2017• Mark Lovett (HOI) 2018

• Ntobeko Nyawo (COO) 2018• Avashnee Ramdial (CFO) 2018

External review highlighted gaps to institutional quality

Development of a multi-year road map

1

2

3

STANLIB: Investment strategy Giles Heeger and Mark Lovett

38

Context to STANLIB’s strategy refresh

To be the leading asset manager in Africa and other emerging markets that we serve. We need to deliver:

Investment Alpha

Service Alpha

Group 2 3rd party

To get the time to build a credible 3rd party offering, we need to deliver investment performanceto maintain continued Group support

Requirement: Long-term, consistent risk adjust returns, with flexibility on time horizons

Deliver high quality equity and multi-asset offering using innovative solutions by combining active, (including 3rd party specialists), passive and multi manager capabilities

Creation of a multi-strategy capability

Requirement: Improved focus on understanding Liberty and SBK and delivering more appropriately

Appointment of dedicated Liberty and SBK teams for more focused engagement and delivery

Requirement: Top quartile, peer relative returns over the long term

Remove Liberty institutional funds from Equity and Balanced franchises: Reduce complexity by removing focus on short term goals

Eliminate impact of operating model

Allow Investment professionals to focus on delivering long term client outcomes

Requirement: Focus on retail offering versus tied offering

Professionalise teams to service retail offering Simplified product offering

Focus on operational platform to deliver improved client experience through increased digitization, minimising errors, upgrading technologies, leverage group where possible, and improved client and client onboarding

experience

39

2018 Investments - priority initiatives

Articulation of investment philosophy and process

Strengthen executive leadership

Strengthen the investment oversight function and improve analytics capability

1

2

3

Progress update

Appointment of experienced international HOI Investment analytics capability strengthened by appointment of

new Head and additional resourcesFormation of a multi-strategy dynamic asset allocation capability Identified a number of recruitment requirements

Refresh ESGWork to improve articulation of philosophy and process

across franchises Actions taken towards developing a performance culture:

• Semi annual FOC’s• Quarterly investment and risk reviews• Forums to improve cross franchise collaboration

40

Improvements in Equity and Balanced performance

Progress update

Consolidation of equity teams into a single team under Herman van VelzeEquity stock picking in the balanced fund moved to the Equity team in 2017Assumption of responsibility for the balanced fund (in additional to equities) by Herman van Velze in July 2018A significantly enhanced quarterly Tactical Asset Allocation meeting which encourages robust, open debate and sharing of views

across the franchises. Improving the forum to leverage asset class expertise.

Source: STANLIB performance data as at 31 December 2018

1 Year 3 Year

Franchise Fund Return % Bmk % Alpha % Quartile Ranking Return % Bmk % Alpha % Quartile

Ranking

Equity STANLIB Equity Fund -5,1 -11,7 6,6 1 1,5 3,7 -2,2 3

Multi-Asset STANLIB Balanced Fund -0,9 -3,7 2,8 1 2,9 5,7 -2,8 3

Liberty Liberty Preferred Assets -1,2 -3,3 2,1 1 2,9 4,6 -1,7 4

Whilst this performance is a desirable outcome, the team is aware that short-term (12 month) returns can be volatile and focus remains on improving long-term investment performance and strengthening the team

41

Fixed Income and Absolute Return performance remain consistent

1 Year 3 Year

Franchise Fund Return % Bmk % Alpha % Quartile Ranking Return % Bmk % Alpha % Quartile

Ranking

Fixed Income

STANLIB Bond Fund 8,3 7,7 0,6 3 12,6 11,1 1,6 1

STANLIB Income Fund 9,6 7,2 2,4 1 10,2 7,4 2,8 1

STANLIB Money Market 8,1 7,2 0,8 2 8,3 7,4 0,9 2

Absolute return Absolute Plus 1,8 7,8 -6,1 1 6,6 6,1 0,2 1

Source: STANLIB performance data as at 31 December 2018

42

Listed Property had a challenging year

Source: STANLIB performance data as at 31 December 2018

1 Year 3 Year

Franchise Fund Return % Bmk % Alpha % Quartile Ranking Return % Bmk % Alpha % Quartile

Ranking

ListedProperty

STANLIB Property Income Fund -27,4 -27,0 -0,4 4 -1,5 -2,0 0,4 3

STANLIB Global Property Fund -4,8 -5,6 0,8 1 1,0 2,3 -1,3 3

Industry trends, revenue and cost implications Derrick Msibi

44

Industry trends: Changes across customer, investments and business models

Customer segments• Evolving customer segments - different sources of growth. Retail AuM

growing faster than Institutional• Technology savvy – digital everything• Decline in revenue margins visible across client segments. • Institutional, driven by intense market competition and increasing

vigilance by institutional investors over fees. Growth in Retail distributors’ power and regulator’s push for fee transparency and fairness, compressing margins

Investments• The elusive alpha, tepid net flows and general negative and turbulent

performance of global financial markets• Solutions focus to meet specific client risk return requirements over

specified time horizon• Greater awareness and focus on socially responsible investing • Movement of AuM from traditional active to passives and on a lesser

scale alternatives Business models• Trend to outsource back-office operations• Move to more digital, technology based solutions – long payback

periods• Platform solutions that capture client and earn sticky administration fees

premised on value added services (low cost)

Implications• Reliance on rising financial markets to boost asset

values, no longer relevant – need to focus on long-term competitive advantage to generate net new flows

• Need to look at cost as a competitive advantage to delivering growing profits

• Business models need to cope with cost constraints – margin pressures and migration to lower margin product range, impacting profitability

• Competence in advanced data and analytics is seen as a differentiator and potential competitive advantage

• Need to design a comprehensive approach to risk management – alignment of regulatory compliance

• Acquire scale and capability (including data analytics)

45

Structural industry changes have resulted in negative earnings jaws

• Low revenue growth and drop in revenue margin driven by intense market competition and increasing vigilance by investors over fees.

• Growing power of distributors and regulator’s push for fee transparency and fairness compressing margins

• Changing asset mix with the introduction of passives and trend towards LDI solutions

• Market volatilities 0

5

10

15

20

25

30

35

40

45

2011 2012 2013 2014 2015 2016 2017 2018

Net Revenue Operating expenses

-20%

+16%

Net revenues and operating expenses as a share of AuM (bps)Industry dynamics

• Operational write-off’s

• Manual environment contributing to operational risk incidents

• Vendor / outsource management

STANLIB dynamics

• Optimising business processes, increased automation and digital initiatives to reduce risk of operational error including a system architecture review

• Simplify the business to reduce layers of complexity

• Instilling ZBB rigour into the business, redirecting savings to extract efficiencies

• Managing retention of critical skills while allowing for natural attrition

STANLIB initiatives to contribute to a more agile business

46

Restoring revenue is important

0

500

1000

1500

2000

2500

Revenue (Rm) Cost (Rm)

STANLIB Peer comparison

-R300m

-R30m

When benchmarked to peers STANLIB lags to a larger extent on a revenue basis and to a lesser

extent on the cost base

Revenue impacted by:

*Benchmarking using STANLIB 2018 budget and 2017 peer comparative

1. Distribution charge to market2. Legacy pricing on the Liberty book3. Liberty outflows4. Poor investment performance in core equity

and multi-asset offerings 5. Decreasing margin through changing margin

mix rotating to lower margin products

Addressing legacy pricing and distribution economics has a long lead time to extract business

benefits. In the interim STANLIB is implementing initiatives to optimize its cost base

STANLIB Peer

Cost to income ratio 73% 61%

47

Focused initiatives to optimise the cost base

Increased digital initiatives to extract benefits Increased automation across the business Increase in retail straight through processing and a reduction in costs per transaction On-line Broker transacting capability significantly reducing cost per transaction Reduced basic queries to call centre through improved digital access Improving efficiencies reduced errors on transactions

Optimising business processes, increased automation and digital initiatives to reduce operational risk incidents

Questions

SAM prudential regimePhilip Harrison

50

• The prudential regulatory regime changed to SAM on 1 July 2018

• Liberty incorporated the SAM basis into its management approach several years ago:

› Liberty (along with other industry players) supported the FSB in developing the SAM standards

› Liberty has been calculating economic balance sheets for approximately ten years

› The business has been managed on an economic basis for a number of years (e.g. SCR coverage is one of the dimensions used to measure group risk appetite); and

› Liberty submitted regulatory returns to the FSB during a parallel run period of four years

• Liberty was fully prepared for SAM by the time it was implemented

Change in prudential regime

51

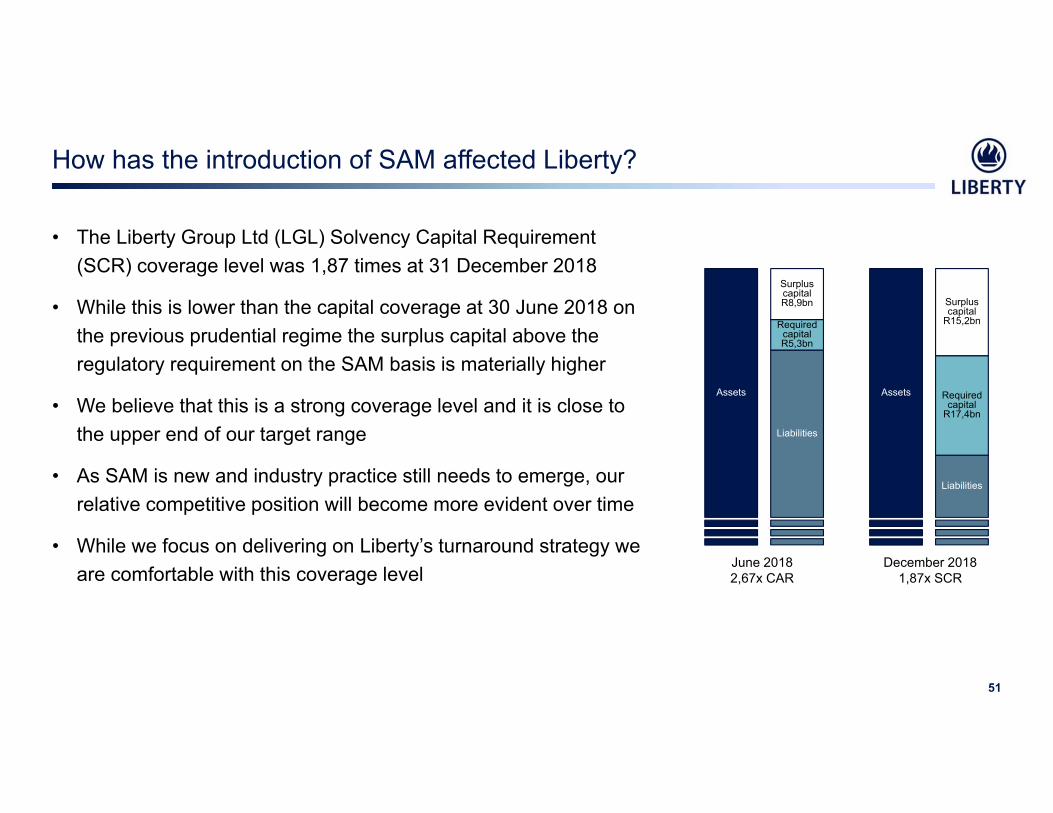

• The Liberty Group Ltd (LGL) Solvency Capital Requirement (SCR) coverage level was 1,87 times at 31 December 2018

• While this is lower than the capital coverage at 30 June 2018 on the previous prudential regime the surplus capital above the regulatory requirement on the SAM basis is materially higher

• We believe that this is a strong coverage level and it is close to the upper end of our target range

• As SAM is new and industry practice still needs to emerge, our relative competitive position will become more evident over time

• While we focus on delivering on Liberty’s turnaround strategy we are comfortable with this coverage level

How has the introduction of SAM affected Liberty?

Assets

Liabilities

Required capital

R17,4bn

Surplus capital

R15,2bn

Assets

Liabilities

Required capital R5,3bn

Surplus capital R8,9bn

June 20182,67x CAR

December 20181,87x SCR

52

• The new Actuarial Practice Note 107 (which governs the calculation of EV) became effective on 31 December 2018 effectively requiring companies to move to a SAM based EV calculation

• Liberty implemented the new EV basis as follows:

› The net worth and VIF calculations now reference the published liabilities (previously the SVM basis). This removed the need for the material and complex reconciliation items between the published NAV and the EV net worth. This further aligns with how Liberty manages market risk and reduces the volatility in the investment variances reported in the EV net worth. As noted in the year-end analyst booklet, this increased the net worth and reduced the VIF; and

› The approach used to determine the cost of required capital was adjusted to reference the SCR which led to an increase in the cost of required capital

• The impact of this change was an increase to the EV of R139m at 31 December 2017. Implementing the change as a year-open change meant that the EV earnings analysis for 2018 was disclosed on the new basis aiding understanding of the impact of the change on the various components in the EV analysis

Impact on embedded value (EV)

Questions

Thank you