life cycle cost

TRANSCRIPT

1

1

Aalto-yliopistoInsinööritieteiden korkeakoulu

Life Cycle Cost (LCC)Training toolkitNordplus, GreenIcon project 2010 - 2012

Helena Mälkki

2

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Life Cycle Cost (LCC) Yoshio Kawauchi and Marvin Rausand. 1999. Life Cycle Cost (LCC) analysis in oil and chemical process industries. 82 p. http://www.ntnu.no/ross/reports/lcc.pdf

Life Cycle Cost (LCC) analysis is a collective term comprising many kinds of analysis, e.g., reliability-availability-maintainability (RAM) analysis, economic analysis, risk analysis, and so on.

A main objective of the LCC analysis is to quantify the total cost of ownership of a product throughout its full life cycle, which includes research and development, construction, operation and maintenance, and disposal.

The predicted LCC is useful information for decision making in purchasing a product, in optimizing design, in scheduling maintenance, or in planning revamping.

2

3

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Life cycle cost consisting of acquisition costs and ownership costs

Dangel,R.: Integrated Logistic Support (ILS) Implementation in the Naval Ship System Command, ASE 6th annual technical symposium, pp. 1-25, (1969)

4

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Development of LCC analysis applicationsYoshio Kawauchi and Marvin Rausand. 1999. Life Cycle Cost (LCC) analysis in oil and chemical process industries. 82 p. http://www.ntnu.no/ross/reports/lcc.pdf

3

5

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Economic assessment It has several names, such as

Life Cycle Costing (LCC), Life-Cycle Cost Analysis (LCCA),Life Cycle Profit (LCP), Full Cost Accounting (FCA), Total Cost Assessment or Accounting (TCA), Total Ownership Cost (TOC) for defense systemsThe method is calculating the cost of a system over its entire life span.

6

External costs

Environmental costs - definition

Indirect & “hidden” costs

Traditional & conventional costs

= Total environmental Cost Assessment (TCA)

E.g. Add-on & process investments and O&M costs, environmental depts & personnel, waste management, liability costs (legal services, monitoring, taxes, charges, fees..), environmental

reports, brochures...

Value of lost inputs of raw materials, incremental costs of substitutes of raw materials; environmental costs of intermediates or of on-site power

generation; costs of environmental labelling, costs of take-back of used packaging; environmentally driven R&D

Social costs of environmental damages (health, corrosion, biodiversity…) external to market price system (economic valuation).

Internal + External

T.Loikkanen - MET / ABB 22.6.2000

4

7

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Life-Cycle Cost Analysis (LCCA)

The approach to making cost-effective choices for building-related projects can be quite similar whether it is called •cost estimating, •value engineering, or •economic analysis.

8

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

LCC Codes and StandardsYoshio Kawauchi and Marvin Rausand. 1999. Life Cycle Cost (LCC) analysis in oil and chemical process industries. 82 p. http://www.ntnu.no/ross/reports/lcc.pdf

IEC-60300-3-3: Life cycle costing

ISO 15663 Petroleum and natural gas industries – Life cycle costing

SAE-ARP4293: Life cycle cost- techniques and applications

SAE-ARP4294: Data Formats and Practices for the LCC of Aircraft Propulsion Systems.

5

9

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

The basic LCC processesin six steps

10

6

11

LCC = Cic + Cin + Ce + Co + Cm + Cs + Cenv + Cdhttp://www.dantes.info/Tools&Methods/Environmentalassessment/enviro_asse_lcc.html

where

• Cic: Initial cost: is the purchasing price of the component/system. This can be paid immediately or in several down payments over the years.Cin: Installation cost: start up costs that the operator has to pay that are not included in the purchasing price, e.g. staff training cost, material losses.Ce: Energy costs: the product of energy use and cost of different types of energy.Co: Operating costs: the yearly operating cost, excluding the energy cost.Cm: Maintenance costs: cost of service and planned repairs.Cs: Downtime costs: cost of unplanned stops.Cenv: Environmental costs: e.g. cost of environmental permits.Cd: Decommission cost: estimated costs to decommission a product/plant at the end of its lifetime.

12

LCC = Cic + Cin + Ce + Co + Cm + Cs + Cenv + Cd

• There are also financial factors to take into consideration if you choose to discount the costs to a certain year. These include:– Present energy price.– Expected annual energy price increase (inflation) during the life time.– Discount rate.– Expected equipment life.

• When determining the energy costs, the effects of fixed charges, power charges, penalty charges for reactive power demand etc., must be included if possible. Corresponding factors must also be considered for energy forms other than electricity.

• In addition, the user must decide which costs to include, such as, maintenance, down time, environmental, disposal, and other important costs.

7

13

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

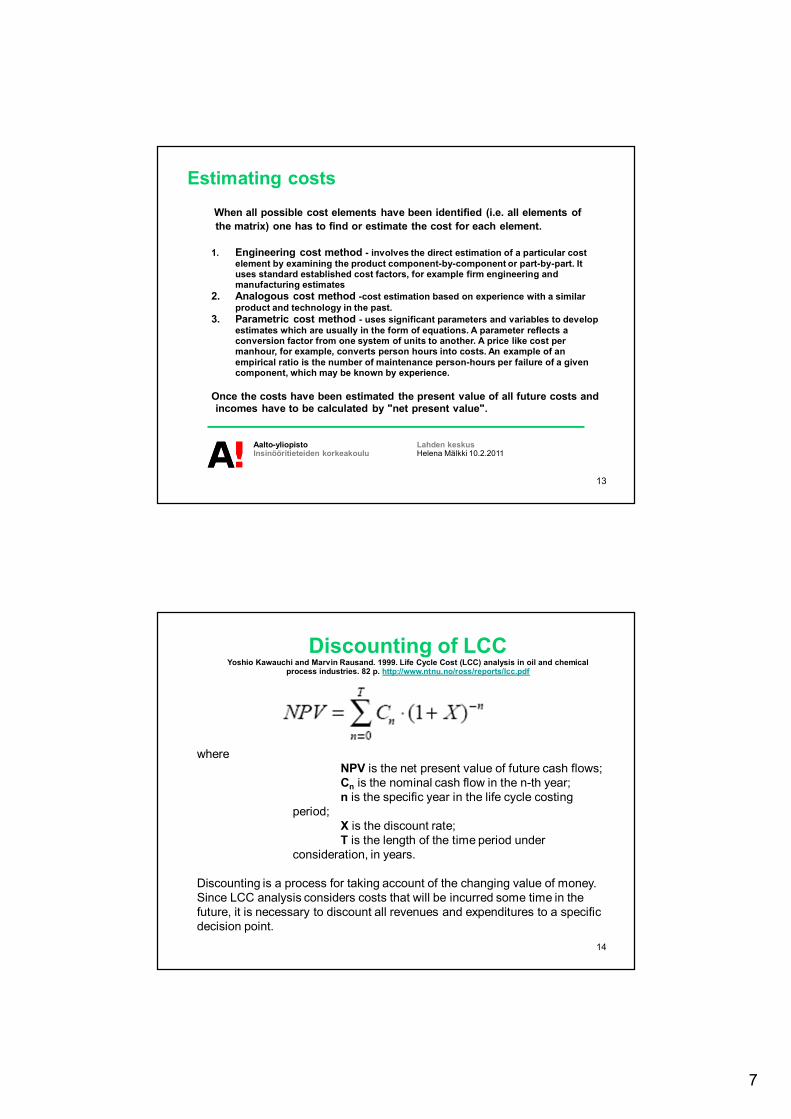

Estimating costs When all possible cost elements have been identified (i.e. all elements of the matrix) one has to find or estimate the cost for each element.

1. Engineering cost method - involves the direct estimation of a particular cost element by examining the product component-by-component or part-by-part. It uses standard established cost factors, for example firm engineering and manufacturing estimates

2. Analogous cost method -cost estimation based on experience with a similar product and technology in the past.

3. Parametric cost method - uses significant parameters and variables to develop estimates which are usually in the form of equations. A parameter reflects a conversion factor from one system of units to another. A price like cost per manhour, for example, converts person hours into costs. An example of an empirical ratio is the number of maintenance person-hours per failure of a given component, which may be known by experience.

Once the costs have been estimated the present value of all future costs and incomes have to be calculated by "net present value".

14

Discounting of LCCYoshio Kawauchi and Marvin Rausand. 1999. Life Cycle Cost (LCC) analysis in oil and chemical

process industries. 82 p. http://www.ntnu.no/ross/reports/lcc.pdf

where NPV is the net present value of future cash flows; Cn is the nominal cash flow in the n-th year; n is the specific year in the life cycle costing

period; X is the discount rate; T is the length of the time period under

consideration, in years.

Discounting is a process for taking account of the changing value of money. Since LCC analysis considers costs that will be incurred some time in the future, it is necessary to discount all revenues and expenditures to a specific decision point.

8

15

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

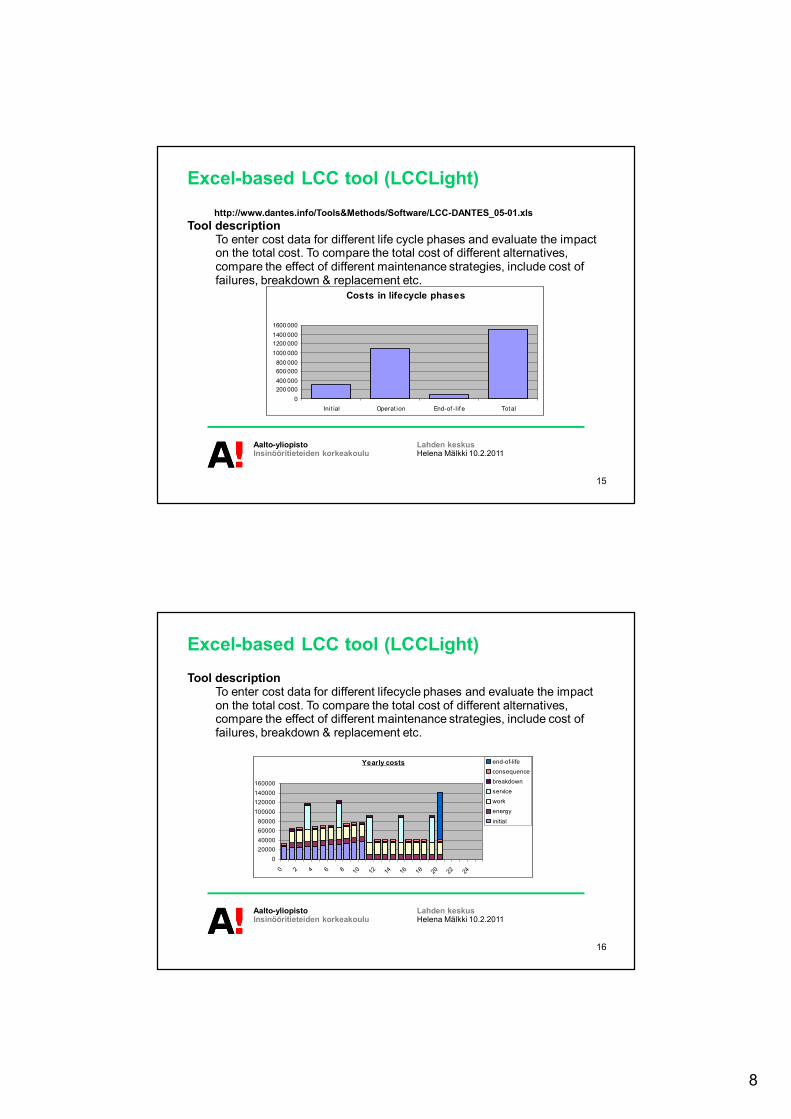

Excel-based LCC tool (LCCLight) http://www.dantes.info/Tools&Methods/Software/LCC-DANTES_05-01.xls

Tool descriptionTo enter cost data for different life cycle phases and evaluate the impact on the total cost. To compare the total cost of different alternatives, compare the effect of different maintenance strategies, include cost of failures, breakdown & replacement etc.

Costs in lifecycle phases

0200 000400 000600 000800 000

1 000 0001 200 0001 400 0001 600 000

Init ial Operat ion End-of -l if e Tot al

16

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Excel-based LCC tool (LCCLight) Tool description

To enter cost data for different lifecycle phases and evaluate the impact on the total cost. To compare the total cost of different alternatives, compare the effect of different maintenance strategies, include cost of failures, breakdown & replacement etc.

Yearly costs

020000400006000080000

100000120000140000160000

0 2 4 6 8 10 12 14 16 18 20 22 24

end-of-lifeconsequencebreakdownserviceworkenergy

initial

9

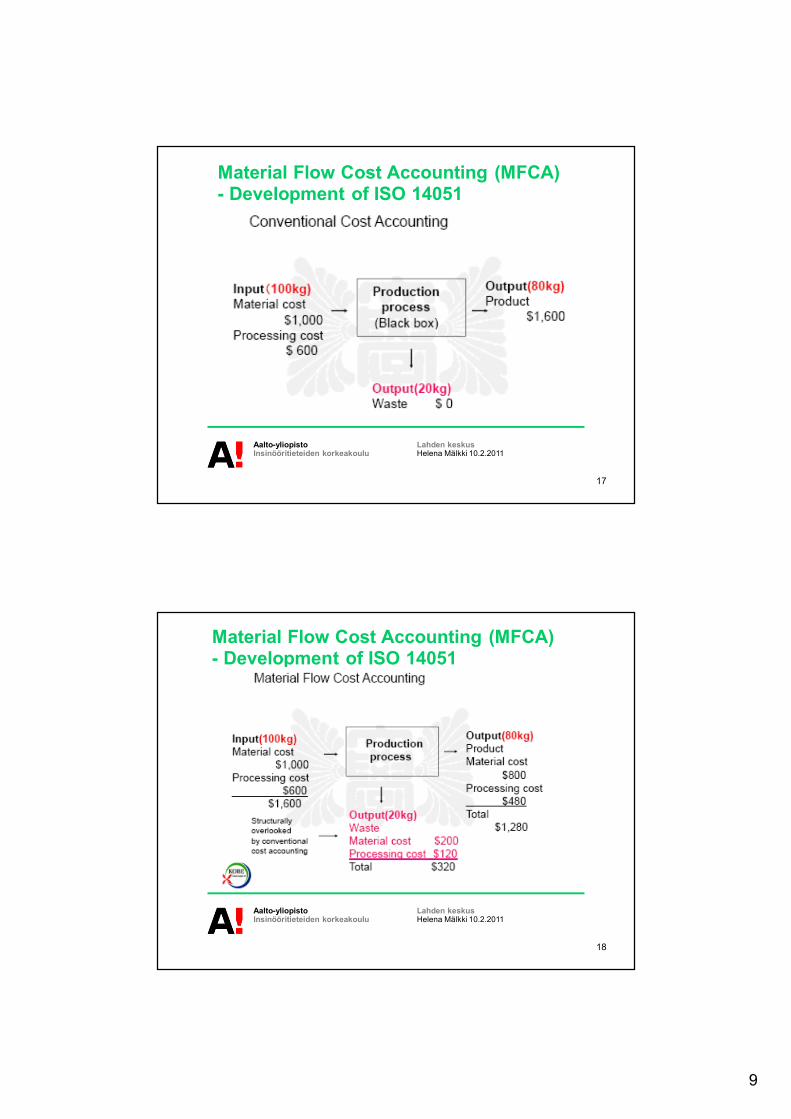

17

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Material Flow Cost Accounting (MFCA)- Development of ISO 14051

18

Aalto-yliopistoInsinööritieteiden korkeakoulu

Lahden keskusHelena Mälkki 10.2.2011

Material Flow Cost Accounting (MFCA)- Development of ISO 14051