life insurance underwriting that’s fast, easy and just...

TRANSCRIPT

Life insurance

Underwriting that’s fast, easy and just right Underwriting guide

For financial professional use only. Not for distribution to the public.

For financial professional use only. Not for distribution to the public. 1

Table of contents

2 General overview

4 Accelerated underwriting

7 Automatic Standard Approval Program

9 Healthy Lifestyle Credits

10 Online Part B and TeleApp

12 Impairments

32 Height/weight charts

33 Super Standard/Preferred/

Super Preferred

38 Financial underwriting

For financial professional use only. Not for distribution to the public.

2 For financial professional use only. Not for distribution to the public.

Save time with the right programs and services

Helping clients achieve the best ratings possible and having more time to

sell is easy when you take advantage of our valuable programs and services.

The following is a high-level glance at our oNerings. Then for the remainder

of the guide, we’ll take a closer look at our programs and guidelines.

Competitive turnaround times

transfer of proceeds.

(for applicants who qualify).

Easy to work with

available, plus access to your underwriter

professionals to help guide clients through

the medical portion of the application.

This helps eliminate requirements with

medical portion of the application on their

own terms and timeline and submit directly

to us for faster processing.

Competitive survivorship features

Reconsideration

not required

Seven classes of uninsurable

than one year)

Opt-out underwriting

one year

For financial professional use only. Not for distribution to the public.

Business case advantage

Flexible, partnership approach – collaborate for

creative solutions

Multi-life underwriting

Nonqualified executive benefits – aggregate

funding on COLI

›

›

› Physical measurements + ECG + Labs + APS

›

› No inspections required

› Employer census provides

participants using TeleApp

requirements and APS reports for you

formal signatures

Online services

New business application forms

Principal® provides easy access to life new business

application forms in Virtual Supply on the advisor

companies to ensure our application materials

are available to customers who subscribe to

their services.

Submitting new applications

Submit new business applications electronically

to ensure new application submission is available

are also welcomed.

Pending case status

pending life and disability insurance new

to ensure our pending new business information is

available to customers who subscribe to

to ensure underwriting rules are available to

For financial professional use only. Not for distribution to the public.

How does it work?

Accelerated underwriting

What is accelerated

underwriting?

Get cases issued

faster and easier with

Principal Accelerated

Underwriting .

The elimination of lab testing and

applicants who qualify*

*Based on age, product, face amount and personal history.

Step 1.

Accelerated Underwriting case.

Step 2.

via a telephone interview. To complete using the online Part B, initiate the client email using

Accelerated Underwriting application.

TeleApp Contact Center hours:

Step 3.

proceeds to issue. If not approved, a paramed appointment will be scheduled plus any additional

percent who qualify.

For financial professional use only. Not for distribution to the public.

limits. See chart on following page.

page.

® coverage

was approved at Preferred or Super Preferred.

physician and evidence of routine physical within

product (i.e., cigar, patch, gum & marijuana)

years, or more than two moving violations in the

past three years.

activities may qualify subject to activity details

gathered during the TeleApp.

rated, ridered or declined.

completed in the prior 12 months for life or

completed by client.

member, and insured has regular check-ups targeted at early diagnosis.

Eligibility requirements

For financial professional use only. Not for distribution to the public.

Ages

Height Height

Ages

Height Height

Alcohol abuse and/or treatment

Atrial Fibrillation

Barrett’s Esophagus Gastric Bypass/Lap Band

Squamous Cell Carcinomas)Hepatitis

Chronic Obstructive Pulmonary Hypertension (diagnosed within Sleep Apnea

Stroke/Transient Ischemic Attack

(TIA)

SLE/Lupus Ulcerative Colitis (UC)

Underwriting build chart

NO major medical conditions, such as:

For financial professional use only. Not for distribution to the public.

How it worksGive clients a rating boost. Our Automatic Standard Approval Program

companies have eliminated their program or changed their guidelines,

Principal still supports ASAP.

How does our program di8er from other companies?

(HLC) program can be used in conjunction with ASAP. The combination of HLC and ASAP

use ASAP to get to a Standard rating.

Automatic Standard Approval Program

ASAP guidelines

›

›

› Permanent products only* (both lives are eligible for

Survivorship UL Protector II)

›

›

or lifestyle cases (drug/alcohol use)]

› Can be used with Healthy Lifestyle Credits

›

For financial professional use only. Not for distribution to the public.

What are the benefits?Our ASAP eliminates the low, substandard ratings that can be the most challenging to

present to your client. Consequently, you can present an oNer to a client that has a greater

your client without a reduction in the compensation paid to you.

Proposed insured

Product type

Underwriting oNer

UL

cholesterol, both controlled with

medication

Standard using Healthy

Lifestyle Credits and

ASAP together

SULStandard on both lives

using ASAP

CV risk factors

For product-specific eligibility, contact your home office underwriter.

ASAP in action

Unlike many of our competitors, Principal does not

Automatic Standard Approval Program.

For financial professional use only. Not for distribution to the public.

Proposed insuredOriginal rating

(based on medical history)

Improved rating

with HLCs

Sue has asthma Table 2

Brian’s build falls outside the guidelines Table 2 Standard

Betty has high blood pressure Preferred Super Preferred

1

pressure or cholesterol and have enough favorable factors for improvement.

Healthy Lifestyle Credits

How do HLCs help your clients?

eliminate a table rating or even improve Standard or better risks for the

proposed insured.1 Favorable HLCs can help your clients earn up to two

tables of credit that oNset table ratings that have been assessed and may

even improve Standard or better risks up to one class if they have enough

favorable credits. Our Automatic Standard Approval Program, which is

designed to help eliminate low substandard ratings, can also be used in

not all inclusive of covered conditions.)

enough HLCs for qualifying medical conditions, such as some cancers.

for non-medical ratings such as driving, aviation or alcohol and drugs.

Examples

HLC risk profile factors

› Blood pressure

› Cholesterol

› Pulse

›

› Family history

› Preventive cancer screening tests

› Preventive heart screening tests

›

A scoring system is used for each

factor, with positive points for

favorable factors and negative

points for less favorable factors.

If a factor is considered neutral,

the neutral result. These factors

combine to make up an insured’s

Healthy Lifestyle Credit score.

What are Healthy Lifestyle Credits?

All applicants should be given credit for doing the right things to take care of themselves.

Because of this philosophy, we use Healthy Lifestyle Credits (HLCs) as an underwriting tool to help clients get the most favorable rating possible. The underlying basis of our HLCs is an evaluation of several coronary and cancer risk factors of a client as follows.

For financial professional use only. Not for distribution to the public.

interview to help guide your clients through the insurability questions.

insight into medical impairments that the traditional application process doesn’t allow. That means

less back and forth between your client and underwriting trying to clarify vague paper application

medical questions, fewer routine requirements and reduced APS ordering.

Save time with the application

eet with your client and prepare to submit

the life insurance application.

Initiate the client email that contains the

calling the TeleApp Contact Center at

system will automatically send the client

an email with the online Part B link.

also receive copies of the reminder

emails).

Once your client has completed online

Part B and the rest of the application has

been received, the field o[ce contact

that was provided on the application

will receive an email with a copy of the

completed Part B attached.

1

2

3

4

Complete Part A (Part I) of the application, and

would prefer to submit the medical information

online or by scheduling a telephone interview.

TeleApp Guide (BB10268) provides step-by-step

instructions to help prepare your client.

Schedule the interview using our online

scheduling tool. Interviews may be scheduled

Submit the initial application and other

required forms (supplemental applications,

processing.

The TeleApp interviewer calls your client

at the scheduled time and completes the

insurability questions (Part B/Part II). The

copy of the completed interview responses will

be sent to you once the application is received

Deliver the policy to the client. The home

and signs both copies. One copy is attached

to the policy and remains with the client.

1

2

3

4

5

Here’s how it worksTeleApp Online Part B

Scheduling the TeleApp interviewYou can choose to have your client complete an

immediate interview or you can schedule a future

date and time when it is most convenient for your

client using the following options:

form at principal.com/teleapp.

When scheduling an interview, please provide

this information:

date of birth

Staying informed

advisor website at any time to monitor the status of

the TeleApp interview. Or you can call our TeleApp

Preparing your clients

being taken

medical providers

or conditions

Helpful TeleApp hints

› Immediate interviews are

› Scheduled interviews with

scheduled). If you’re not

completing an immediate

interview, it’s better to schedule

›

let us know the state in which

the application was signed.

questions.

› by the TeleApp counselor and the

date and time of the interview

should be recorded on the Field

For more information

› Go to principal.com/teleapp.

For financial professional use only. Not for distribution to the public. 11

12 For financial professional use only. Not for distribution to the public.

The impairment information on the following pages has been provided to help give you a

general idea of potential underwriting outcomes based on medical and non-medical life

insurance underwriting.

the right quote quickly and easily.

assessments based on hypothetical parameters using our underwriting guidelines at the time

of publication. Actual underwriting outcomes may possibly be more favorable than illustrated

using available Healthy Lifestyle Credits and our Automatic Standard Approval Program

The impairments table is set up as follows:

Impairments

Risk factors Typical requirements Likely underwriting decision

ImpairmentThe name of the impairment, including a short description. Conditions are listed alphabetically.

The criteria the underwriter

uses to classify the risk underwriter is likely to request in

addition to the routine age and

amount medical requirements

For faster decision:

include in your application

package to enable the

underwriter to quickly and easily

provide the right quote. This

information may be used to

determine appropriate APS

the underwriting process and

limiting the need for subsequent

requirement requests.

necessary for the impairment

based on the factors and

impairments outline a best-

case scenario, typical case and

worst-case rating.

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Alcohol abuse (Includes alcoholism and problem drinking)

Alzheimer’s disease

present alcohol

consumption declared

dependence

investigations, including

markers

consuming in moderation

group such as Alcoholics

Anonymous

including any history of

other substance abuse,

driving oNenses or

sports

job instability

medications

required

Requirements:

test, alcohol questionnaire,

inspection report selectively

For faster decision:

treatment.

care/treatment including

dates and length of treatment.

such as continued

employment, attendance in

Alcoholics Anonymous or

similar body, etc.

Requirements:

selectively

For faster decision:

such as cognitive or memory

testing

applicant’s age, time since last

use and any co-morbid factors.

Alcoholism:

Best Case:

consumption)

Worst Case:

Problem drinking:

Best Case:

and mild)

Worst Case:

All cases:

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Anemia

Aneurysm

referrals to specialists/

hematologists (include

dates, names of tests and

doctors seen)

aneurysm

aneurysm

coronary artery disease,

hypertension,

cerebrovascular, other

peripheral vascular or

Requirements:

APS

For faster decision:

and testing to include cause

and/or source of bleeding

of the condition, including

recent complete blood count

(CBC)

Requirements:

APS

For faster decision:

ongoing surveillance

lipid control

coronary artery disease,

hypertension, cerebrovascular,

other peripheral vascular or

symptoms

anemia and assume anemia is

fully investigated and stable.

Iron deficiency anemia: Preferred possible for

best-case scenario

Hemolytic anemia: Preferred possible for

best-case scenario

Can consider on a rated basis

depending on the type of

aneurysm.

Abdominal:

No surgery: Best case is Table

last three years or since

diagnosis

If diameter >5 cm:

With surgery: Individual consideration

Cerebral:

No surgery:if small, stable and no

complications

Large:

With surgery: Standard after two years

Thoracic:

No Surgery:

With Surgery:two years

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Risk factors

Risk factors

Typical requirements

Typical requirements

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Likely underwriting decision

Likely underwriting decision

Angina pectoris

Angioplasty

Arteriosclerosis

Apnea/sleep apnea

surgery)

treatment

disease and/or risk factors

including hypertension,

arrhythmias

or obesity

Requirement:

APS

For faster decision:

duration of symptoms

with treatment

industrial accidents attributed

to sleepiness

Mild disease and no complications: Preferred or Super Preferred

possible

Moderate disease untreated and no complications:

Moderate disease treated and compliant with therapy: Preferred possible

Severe disease untreated and no complications:

Severe disease treated and compliant with therapy. Best case: Standard after two

years compliance with

treatment

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Asthma

Atrial fibrillation

asthma attacks

frequency of use

medications

disorder, alcohol abuse,

at onset

complications

non-cardiac disease

anticoagulant medication

Requirement:

APS

For faster decision:

including pulmonary

function tests

treatment

symptoms

Requirement:

APS

For faster decision:

Investigations

Minimal or mild asthma: Preferred or Super Preferred

Moderate: Standard to Table 2

Severe:

Found on examination, no investigation: Postpone

Paroxysmal Atrial Fibrillation (PAF) with infrequent attacks: Standard

Chronic Atrial Fibrillation:

Less favorable outcome for

co-morbid complications

For financial professional use only. Not for distribution to the public.

Risk factors Typical requirements Likely underwriting decision

Barrett’s esophagus

including biopsy

treatment

treatment and surveillance

hemorrhage, perforation)

Requirement:

APS

For faster decision:

including biopsy

(e.g., endoscopy)

and alcohol use)

Best case: Preferred or Super Preferred if

no dysplasia and good follow-

up done on a regular basis

Typical case: Standard to Table 2

Worst case:

Risk factors

Risk factors

Risk factors

Typical requirements

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Likely underwriting decision

Blood pressure

Bypass surgery

Cancer

type of cancer.

For all forms of cancer: Consideration for insurance

begins once treatment has

been completed, assuming the

client is well followed.

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Cancer: Basal Cell Carcinoma/Squamous Cell Carcinoma

Cancer: Breast

basal cell carcinoma

has been removed

completely

dysplastic nevi or

dysplastic nevus syndrome

as multiple dysplastic nevi

and a propensity to

develop other skin cancers

from treatment

from treatment

Requirement:

APS

For faster decision:

post-operative

smoking)

Requirement:

APS

For faster decision:

treatment, including any

adjunct therapy

(mammograms,

bone scan, etc.)

Complete excision: Possible Preferred or Super

Preferred

Best case: Standard for carcinoma in situ

Typical case:

years after completion of

treatment (chemo or

radiation), then possible Table

depending on stage and grade

Worst case:

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Cancer: Colon

Cancer: Leukemia

tumor

that may be associated

with other types of cancer

cancer types of cancer

including colonoscopy

results

treatment

stage of cancer

secondary cancer

Requirement:

APS

For faster decision:

information

treatment

(colonoscopy and tumor

markers)

Requirements:

APS, blood testing if current

results are not available

For faster decision:

Best case: Standard after three years

Typical case:

years after completion of

treatment (chemo or

radiation), then possible Table

depending on stage and grade

Worst case:

Acute lymphoid leukemia/acute myeloid leukemia:

Best case: Standard

Typical case:

Worst case:

Chronic lymphoid leukemia/ hairy cell leukemia:

Best case:

Typical case:

Worst case:

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

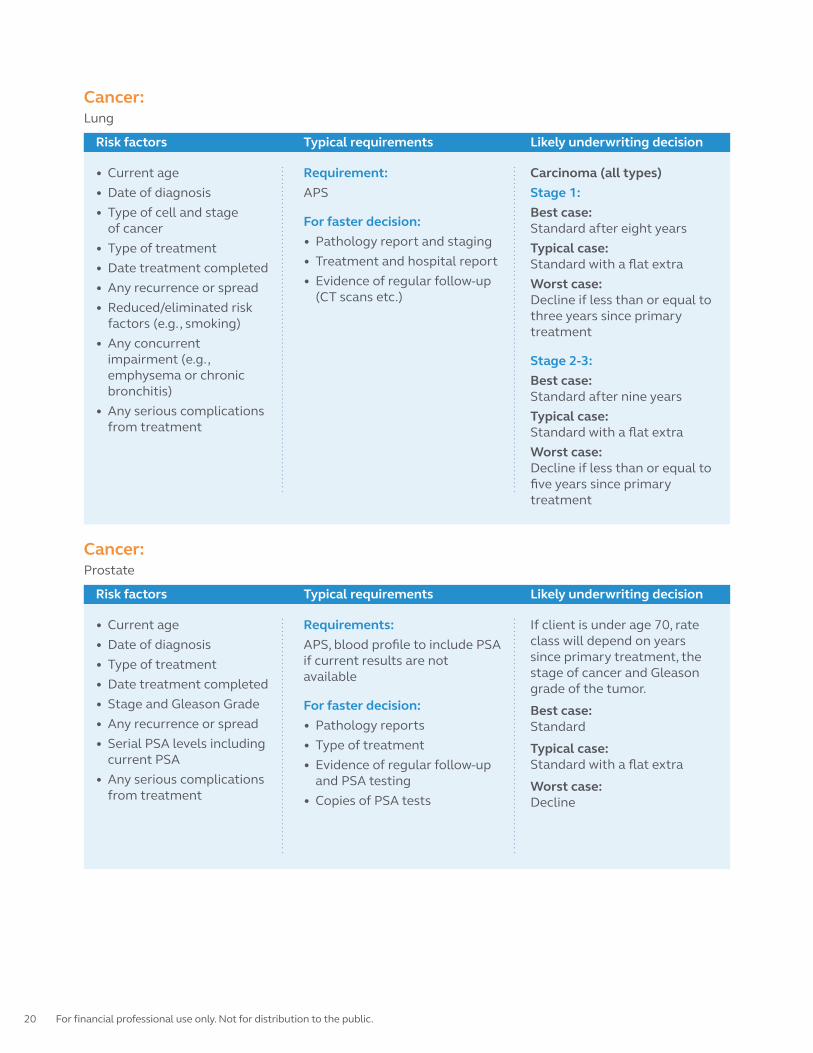

Cancer: Lung

Cancer: Prostate

of cancer

factors (e.g., smoking)

impairment (e.g.,

emphysema or chronic

bronchitis)

from treatment

current PSA

from treatment

Requirement:

APS

For faster decision:

(CT scans etc.)

Requirements:

if current results are not

available

For faster decision:

and PSA testing

Carcinoma (all types)

Stage 1:

Best case: Standard after eight years

Typical case:

Worst case:

three years since primary

treatment

Stage 2-3:

Best case: Standard after nine years

Typical case:

Worst case:

treatment

class will depend on years

since primary treatment, the

stage of cancer and Gleason

grade of the tumor.

Best case: Standard

Typical case:

Worst case:

For financial professional use only. Not for distribution to the public. 21

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Cancer:

Cancer: Thyroid

of tumor

multiple dysplastic nevi

and a propensity to

develop other skin cancers

from treatment

(papillary, follicular,

anaplastic, etc.)

date(s) performed

how long

treatment

Requirement:

APS

For faster decision:

dermatology follow-up

Requirements:

APS

For faster decision:

Best case: Standard

Typical case: Standard with

Worst case:

Best case: Standard

Typical case: Standard or Standard

Worst case:

22 For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Chronic obstructive pulmonary disease (COPD)

Coronary artery disease

current tobacco use

weight loss

respiratory function

progression

biochemical abnormality

cancer, malnutrition)

at onset

(how many vessels and

which ones)

impairment

heart failure or

arrhythmia

cholesterol readings

Requirement:

APS

For faster decision:

(PFT), serial PFTs

Requirements:

APS, EKG (or TST) if current test

is not available

For faster decision:

angiogram, recent stress tests,

perfusion)

Best ratings possible with

testing including perfusion

and stress echocardiograms

within the past 12 months

Best case: Standard

Typical case:

Worst case:

months post-surgery

Best case: Standard

Typical case:

Worst case:

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Crohn’s disease

Diabetes

steroid therapy

concurrent impairments

such as rheumatoid

arthritis or other

inflammatory disease

at onset

sugar readings

nephropathy or kidney

disease, neuropathy,

retinopathy, cardiovascular

disease

Requirement:

APS

For faster decision:

surveillance (colonoscopy)

hospital reports

Requirements:

APS, blood (if not already

required or current results not

available)

For faster decision:

at onset

(neurologist, nephrologist,

endocrinologist)

Hemoglobin A1c where

possible)

Best case: Standard

Typical case:

Worst case:

Type 1

Also known as Insulin

Best case:

Typical case:

Worst case:(complications,

poor or uncontrolled)

Type 2

Also known as Non-Insulin

Best case: Standard

Typical case:

Worst case:(complications, poor or

uncontrolled)

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Emphysema

Heart attack

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Epilepsy/seizure disorder

Gastric surgery for obesity

medication

activity

medical conditions

(such as diabetes,

hypertension, coronary

disease)

complications

(weight loss,

improvement of risk

factors)

For faster decision:

Requirements:

APS

For faster decision:

relating to the surgical

procedure and follow-up

Best case: Standard

Typical case:

Worst case:

months after surgery

Restrictive surgery (gastric banding or gastroplasty):

6 months to 3 years:

>3 years: Standard to Table 2

Malabsorptive surgery/bypass:

<1 year: Postpone

1-5 years:

>5 years: Standard to Table 2

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Risk factors

Typical requirements

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Likely underwriting decision

Hepatitis B

Hepatitis C

Hypertension

infection

function)

done

medical conditions

including liver function

tests

alcohol, and if so, amount

per day

(essential or secondary to

another impairment)

treatment

history of readings for past

2 years (demonstrate

stable course)

treatment and follow-up

disease, build)

Requirement:

APS

For faster decision:

Requirement:

APS

For faster decision:

including liver function

tests

scan results

Requirements:

selectively

For faster decision:

readings

investigation

Best case: Standard

Typical case:

Worst case:

If treated with sustained viral response

Best case: Standard

Typical case:

Worst case: complications including continued

liver disease on biopsy

Untreated

Best case:

Typical case:

Worst case:

of hypertension.

Super Preferred if well-

controlled and compliant

with medication.

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Risk factors

Typical requirements

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Likely underwriting decision

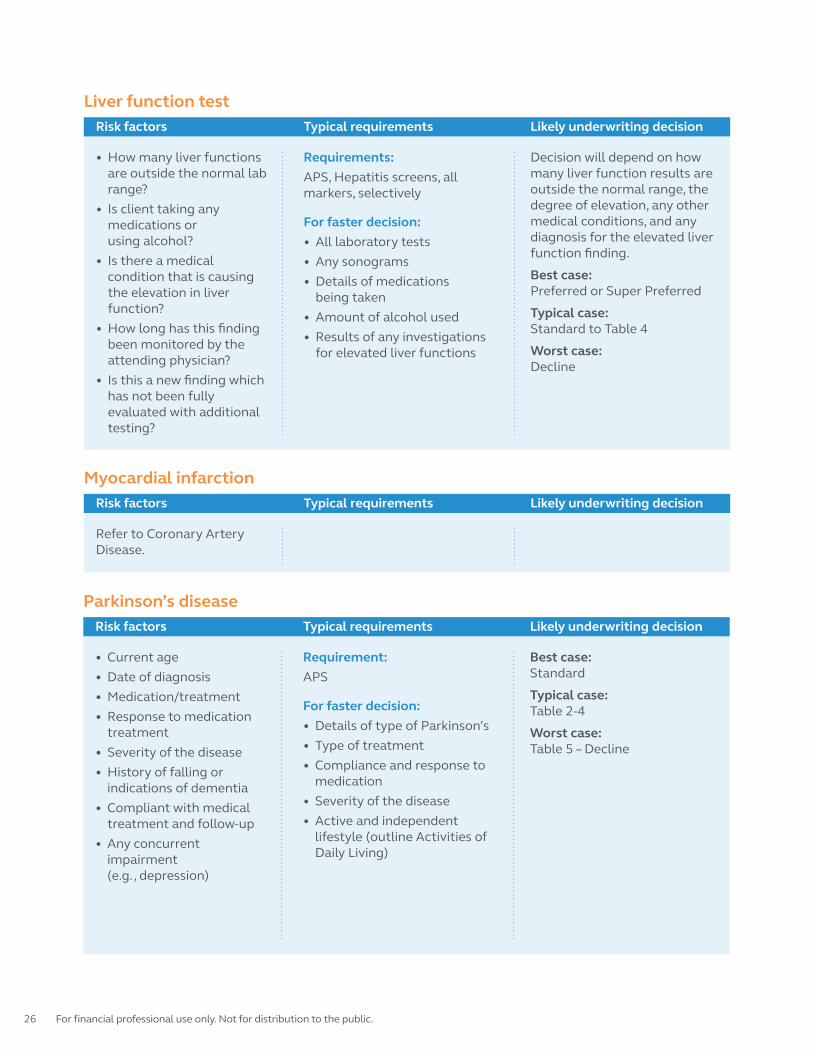

Liver function test

Myocardial infarction

Parkinson’s disease

are outside the normal lab

range?

medications or

using alcohol?

condition that is causing

the elevation in liver

function?

been monitored by the

attending physician?

has not been fully

evaluated with additional

testing?

treatment

indications of dementia

treatment and follow-up

impairment

(e.g., depression)

Requirements:

APS, Hepatitis screens, all

markers, selectively

For faster decision:

being taken

for elevated liver functions

Requirement:

APS

For faster decision:

medication

lifestyle (outline Activities of

many liver function results are

outside the normal range, the

degree of elevation, any other

medical conditions, and any

diagnosis for the elevated liver

Best case: Preferred or Super Preferred

Typical case:

Worst case:

Best case: Standard

Typical case:

Worst case:

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Risk factors

Typical requirements

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Likely underwriting decision

Peripheral artery disease (PAD)/peripheral vascular disease (PVD)

Pulmonary nodule

Rheumatoid arthritis

treatment

currently smoking this will

have a greater impact on

disease progression

treatment and follow-up

hypertension, build)

nodules

factors (e.g., smoking)

impairment (e.g.,

emphysema or chronic

bronchitis)

being taken

activities

medical condition(s)

Requirements:

For faster decision:

cardiac investigation

symptoms

score

Requirement:

APS

For faster decision:

nodule(s)

Requirement:

APS

For faster decision:

Laboratory results

Best case: Standard

Typical case:

Worst case:

Best case: Preferred possible

Typical case: Standard

Worst case:

Best case: Preferred possible

Typical case: Standard - Table 2

Worst case:

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Stroke

Transient ischemic attack (TIA)

at onset

cholesterol readings

impairment

at onset

cholesterol readings

impairment

Requirement:

APS

For faster decision:

Requirement:

APS

For faster decision:

Best case:

Typical case:

Worst case:

Best case: Standard

Typical case:

multiple TIAs

Worst case:

For financial professional use only. Not for distribution to the public.

Risk factors Typical requirements Likely underwriting decision

Ulcerative colitis

complications

steroid therapy)

Requirement:

APS

For faster decision:

surveillance (colonoscopy)

hospital reports

Best case: Standard

Typical case:

Worst case:

For financial professional use only. Not for distribution to the public.

Impairments / non-medical

Risk factors

Risk factors

Risk factors

Typical requirements

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

Likely underwriting decision

Aviation

Climbing and mountaineering

Driving

license held

number of flying hours

per year

established trails

Europe or elsewhere

number of suspensions

Requirement:

Aviation Statement

For faster decision:

Requirement:

Sport Statement, Foreign Travel

questionnaire, if applicable

For faster decision:

Requirement:

For faster decision:

of, and reason for suspension

Best case: Preferred or Super Preferred

possible*

Typical case: Standard*

Worst case:

*Flat extra may apply to base rating

Best case: Preferred or Super Preferred

possible*

Typical case: Standard*

Worst case:

*Flat extra may apply to base rating

Best case/typical case: Preferred or Super Preferred

for infrequent, minor violations

Worst case:

year since violation. Standard

For financial professional use only. Not for distribution to the public.

Risk factors

Risk factors

Typical requirements

Typical requirements

Likely underwriting decision

Likely underwriting decision

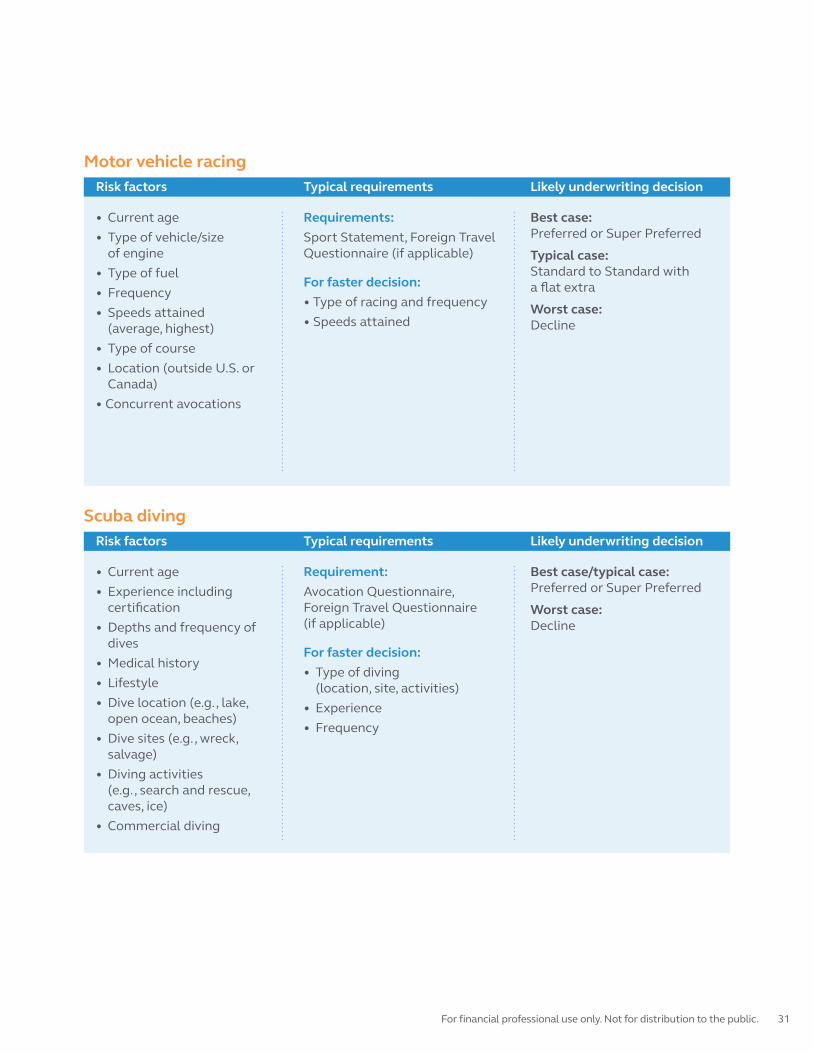

Motor vehicle racing

Scuba diving

of engine

(average, highest)

Canada)

dives

open ocean, beaches)

salvage)

(e.g., search and rescue,

caves, ice)

Requirements:

Sport Statement, Foreign Travel

For faster decision:

Requirement:

(if applicable)

For faster decision:

(location, site, activities)

Best case: Preferred or Super Preferred

Typical case: Standard to Standard with

Worst case:

Best case/typical case: Preferred or Super Preferred

Worst case:

For financial professional use only. Not for distribution to the public.

Height/weight charts

Super Preferred, Preferred, Super Standard, Standard build height

Height

Super Preferred

Preferred 222

Super Standard

211

Standard 212

Super Preferred, Preferred, Super Standard, Standard build height

Height

Super Preferred

212

Preferred

Super Standard

211

Standard 211

Super Preferred, Preferred, Super Standard, Standard build height

Height

Super Preferred

221

Preferred 211

Super Standard

Standard 211

For financial professional use only. Not for distribution to the public.

Super Standard/Preferred/Super Preferred

Give clients credit for managing their health.

Super Standard/Preferred/Super Preferred classes are designed for individuals whom we

oNset one negative risk factor/knockout if

the individual has enough favorable credits.

high blood pressure and cholesterol to qualify for a

Preferred rating.

for a Preferred rating if they have routine preventative

screening tests.

The following describes our criteria for rating a case

Healthy Lifestyle Credits can improve the rating up to one

class if they have enough favorable credits and only one

knockout for build, blood pressure or cholesterol.

of tobacco.

How does

our program

diNer from other

programs?

Basic

guidelines

For financial professional use only. Not for distribution to the public.

Examples

Scenario

colonoscopy and PSA. All

results were normal.

Scenario

mammogram, which was

within normal limits

have been within normal limits

Scenario

noted in family history

including a colonoscopy

and mammogram within

normal limits

Our rating

Client is Super Standard due to

a Preferred knockout for

can improve the rating to

Preferred using Healthy

Lifestyle Credits (HLCs) based

on his other favorable factors

and routine physicals.

Preferred

Our rating

Client meets criteria to remain

Super Preferred/Preferred.

family history due to favorable

HLCs and regular

mammograms.

Super Preferred

Our rating

Client is Super Standard due to

a Preferred knockout for build.

Preferred using HLCs based on

her other favorable factors and

routine physicals.

Preferred

Competitor rating

Client is not allowed the

Preferred class due to

Competitor rating

Client is not allowed

the Super Preferred

class due to family

history (mother died

of breast cancer at

Competitor rating

Client is not allowed

the Preferred class

due to her build and

Male, age 68

Female, age 52

Female, age 74

For financial professional use only. Not for distribution to the public.

GuidelinesSuper Standard/Preferred/Super Preferred

Super Standard

Super Standard

Preferred

Preferred

Super Preferred

Super Preferred

Family history•

Transient Ischemic Attack

Blood pressure

Breast Cancer,

Colon Cancer,

Ovarian Cancer,

Prostate Cancer,

•

colon cancer

• Family history not

considered for applicants

•

Breast Cancer

Colon Cancer

Ovarian Cancer

Prostate Cancer

•

• Family history not

considered for applicants

•

•

•

•

Breast Cancer

Colon Cancer

Ovarian Cancer

Prostate Cancer

•

• Family history not

considered for applicants

•

•

•

For financial professional use only. Not for distribution to the public.

Super Standard

Super Standard

Preferred

Preferred

Super Preferred

Super Preferred

Cholesterol

History of

• No personal history of

alcohol or drug abuse within 10 years

• No personal history of

diabetes or cancer ever

• Exception – Basal and Squamous Cell

• Personal history of certain

cancers will be allowed.

underwriter for criteria.

• No personal history of

alcohol or drug abuse,

diabetes or cancer ever

• Exception – Basal and Squamous Cell

For financial professional use only. Not for distribution to the public.

Super Standard

Super Standard

Super Standard

Preferred

Preferred

Preferred

Super Preferred

Super Preferred

Super Preferred

Foreign residency/travel

Driving2

Occupation/military/aviation/hazardous sports

•

•

permanent residents

• Not ratable for occupation and military

•

Super Standard Preferred Super Preferred

Tobacco1

• Exception – 24 or fewer cigars per year with a negative urine

•

• Exception – 24 or fewer cigars per year with a negative urine

• For Tobacco/Preferred rates

all preferred criteria must be

• No more than two moving violations in the past three years

•

•

• Exception - 12 or fewer cigars per year with a negative urine

1

negative urine specimen for nicotine qualify for non-tobacco.

For increased frequency and for other types of use (medicinal, non-smoked forms, etc.), please contact your home office

underwriter for details.

2 Subject to review of specific infractions.

For financial professional use only. Not for distribution to the public.

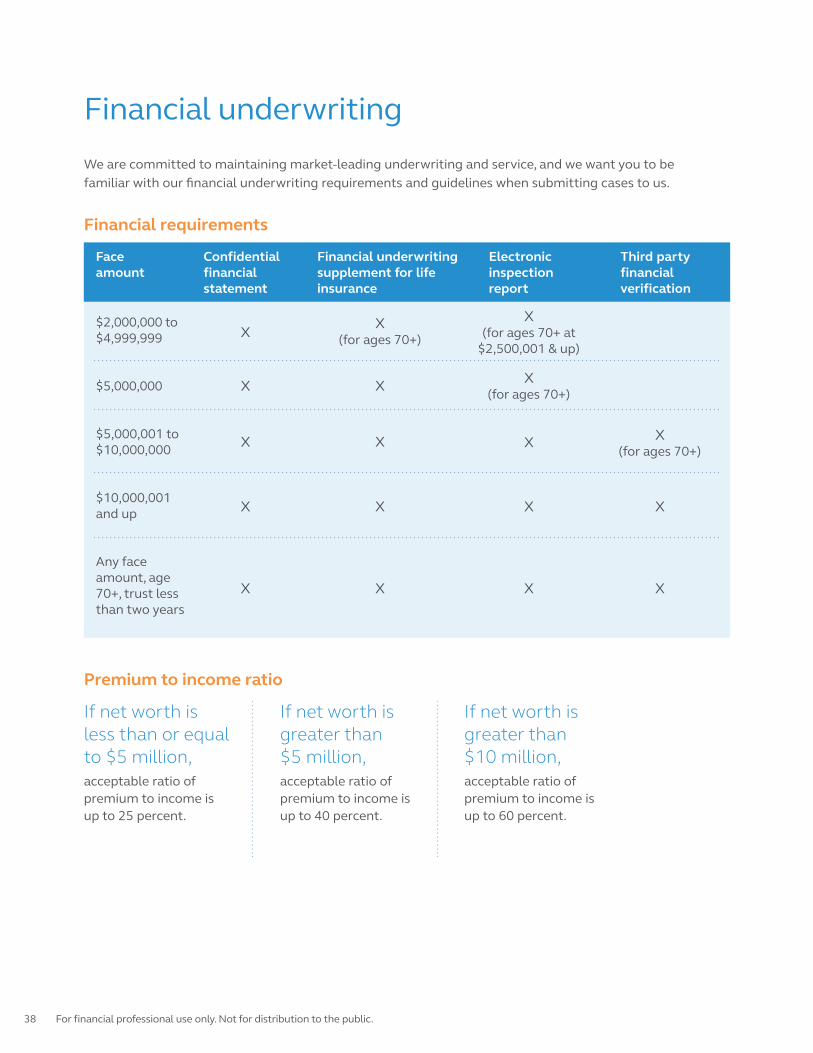

Financial underwriting

If net worth is less than or equal to $5 million, acceptable ratio of

premium to income is

If net worth is greater than $5 million, acceptable ratio of

premium to income is

If net worth is greater than $10 million, acceptable ratio of

premium to income is

Premium to income ratio

Face amount

Confidential financial statement

Financial underwriting supplement for life insurance

Electronic inspection report

Third party financial verification

Financial requirements

and up

Any face

amount, age

than two years

For financial professional use only. Not for distribution to the public.

Purpose of insurance Formulas and guidelines Information needed

Personal financial underwriting guidelines

Income replacement

Estate planning

was determined

pending with all carriers

was determined

1

Estate growth period

Growth

Up to

Use current

estate value

future estate value will be lost

estimated future estate value

For financial professional use only. Not for distribution to the public.

Purpose of insurance Formulas and guidelines Information needed

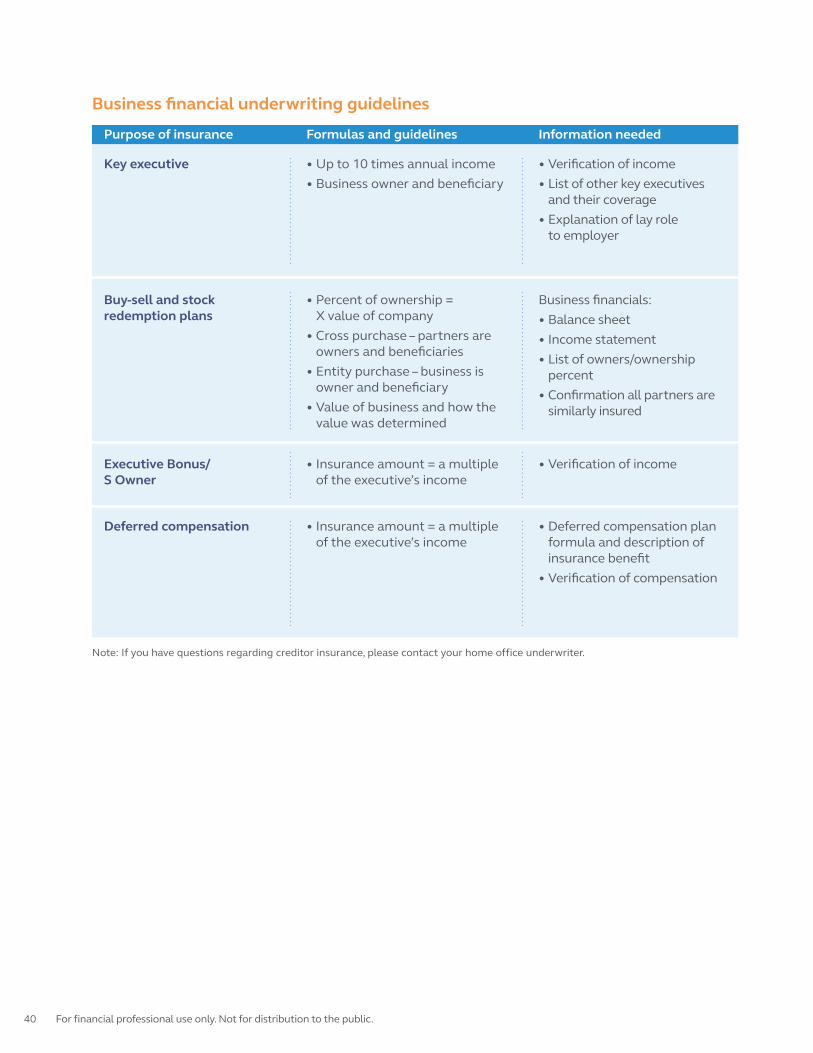

Business financial underwriting guidelines

Key executive

and their coverage

to employer

Buy-sell and stock redemption plans

Executive Bonus/ S Owner

Deferred compensation

percent

similarly insured

formula and description of

value was determined

Principal UnderRightFast. Easy. Just Right.

Toll-free fax: 866-542-1359

access to your underwriter when you need it.

Toll-free phone: 800-654-4278

principal.com/underwriting

For financial professional use only. Not for distribution to the public.

principal.com

Plan administrative services offered by Principal Life. Principal National and Principal Life are members of the Principal Financial Group®

For financial professional use only. Not for distribution to the public.

Principal, Principal and symbol design and Principal Financial Group

are trademarks and service marks of Principal Financial Services, Inc.,

a member of the Principal Financial Group.

Not FDIC or NCUA insured

Not insured by any Federal government agency