listing agreement

DESCRIPTION

listing agreements of stock exchanges the world over, their requirements and disclosure normsTRANSCRIPT

LISTING AGREEMENT

Submitted By:-

Amit Sareen (2313)

Arpan Majumdar (2314)

Priyanshi Gupta (2303)

Satish Kumar Gupta (2311)

Umang Jain (2331)

Vivek Verma (2332)

Listing

Listing means formal admission of a security to the trading platform of the Exchange. The securities may be of any public limited company, Central or State Government, quasi governmental and other financial institutions/corporations, municipalities, etc. The objectives of listing are mainly to:

provide liquidity to securities;

mobilize savings for economic development;

protect interest of investors by ensuring full disclosures.

Companies desirous of getting their securities listed are required to enter into an agreement with a Stock Exchange called the Listing Agreement, under which they are required to make certain disclosures and perform certain acts, failing which the company may face some disciplinary action, including suspension/delisting of securities.

Under the Listing Agreement, a company undertakes, amongst other things, to provide facilities for prompt transfer, registration, sub-division and consolidation of securities; to give proper notice of closure of transfer books and record dates, to forward 6 copies of unabridged Annual Reports, Balance Sheets and Profit and Loss Accounts to the stock exchange, to file shareholding patterns and financial results on a quarterly basis; to intimate promptly to the Exchange the happenings which are likely to materially affect the financial performance of the Company and its stock prices, to comply with the conditions of Corporate Governance, etc.

The Exchange has a separate Listing Department to grant approval for listing of securities of companies in accordance with the provisions of the Securities Contracts (Regulation) Act, 1956, Securities Contracts (Regulation) Rules, 1957, Companies Act, 1956, Guidelines issued by SEBI and Rules, Bye-laws and Regulations of the Exchange.

Benefits of Listing

Listing provides an opportunity to the Corporates / entrepreneurs to raise capital to fund new projects/undertake expansions/diversifications and for acquisitions.

Listing also provides an exit route to private equity investors as well as liquidity to the ESOP-holding employees.

Listing also helps generate an independent valuation of the company by the market.

2

Listing raises a company's public profile with customers, suppliers, investors, financial institutions and the media. A listed company is typically covered in analyst reports and may also be included in one or more of indices of the stock exchanges.

An initial listing increases a company's ability to raise further capital through various routes like preferential issue, rights issue, Qualified Institutional Placements and ADRs/GDRs/FCCBs, and in the process attract a wide and varied body of institutional and professional investors.

Listing leads to better and timely disclosures and thus also protects the interest of the investors.

Listing on a stock exchange provides a continuing liquidity to the shareholders of the listed entity. This in turn helps broaden the shareholder base.

Listing Requirements

Listing requirements are the set of conditions imposed by a given stock exchange upon companies that want to be listed on that exchange. Such conditions sometimes include minimum number of shares outstanding, minimum market capitalization, and minimum annual income.

Requirements by stock exchange

Companies have to meet the requirements of the exchange in order to have their stocks and shares listed and traded there, but requirements vary by stock exchange:

Bombay Stock Exchange: Bombay Stock Exchange (BSE) has requirements for a minimum market capitalization of Rs.250 Million and minimum public float equivalent to Rs.100 Million.

London Stock Exchange: The main market of the London Stock Exchange has requirements for a minimum market capitalization (£700,000), three years of audited financial statements, minimum public float (25 per cent) and sufficient working capital for at least 12 months from the date of listing.

New York Stock Exchange: To be listed on the New York Stock Exchange (NYSE) a company must have issued at least a million shares of stock worth $100 million and must have earned more than $10 million over the last three years.

Eligibility Criteria for Listing(NSE)

An company which desires listing of its securities with NSE must fulfill the following pre-requisites:

For Initial Public Offerings (IPOs)For Securities of Existing Companies

3

NSE staff welcome the opportunity to discuss a company’s eligibility to list before a formal application is made. On fulfillment of the eligibility criteria, the company is required to fill in the listing application form.

IPOs by Companies

Qualifications for listing Initial Public Offerings (IPO) are as below:

1. Paid up Capital

The paid up equity capital of the applicant shall not be less than Rs. 10 crores * and the capitalisation of the applicant’s equity shall not be less than Rs. 25 crores**

Provided however that where the market capitalisation (at issue price) of the applicant’s equity is not less than Rs.100 crores, the paid up capital of the applicant can be less than Rs. 10 crores but in any case it shall not be less Rs. 5 crores.

2. Conditions Precedent to Listing:

The Issuer shall have adhered to conditions precedent to listing as emerging from inter-alia from Securities Contracts (Regulations) Act 1956, Companies Act 1956, Securities and Exchange Board of India Act 1992, any rules and/or regulations framed under foregoing statutes, as also any circular, clarifications, guidelines issued by the appropriate authority under foregoing statutes.

3. Atleast three years track record of either:

a. the applicant seeking listing; orb. the promoters/promoting company, incorporated in or outside India orc. Partnership firm and subsequently converted into a Company (not in existence as a Company for three years) and approaches the Exchange for listing. The Company subsequently formed would be considered for listing only on fulfillment of conditions stipulated by SEBI in this regard.

For this purpose, the applicant or the promoting company shall submit annual reports of three preceding financial years to NSE and also provide a certificate to the Exchange in respect of the following:

• The company has not been referred to the Board for Industrial and Financial Reconstruction (BIFR).• The networth of the company has not been wiped out by the accumulated losses resulting in a negative networth• The company has not received any winding up petition admitted by a court.

4

4. The applicant desirous of listing its securities should satisfy the exchange on the following:

a) No disciplinary action by other stock exchanges and regulatory authorities in past three years

The applicant, promoters/promoting company (ies), group companies, companies promoted by the promoters/promoting company (ies) have not been in default in payment of listing fees to any stock exchange in the last three years or has not been delisted or suspended in the past, and has not been proceeded against by SEBI or other regulatory authorities in connection with investor related issues or otherwise.

b) Redressal Mechanism of Investor grievance

The points of consideration are:

o The applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) track record in redressal of investor grievances

o The applicant’s arrangements envisaged are in place for servicing its investor.

o The applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) general approach and philosophy to the issue of investor service and protection

o defaults in respect of payment of interest and/or principal to the debenture/bond/fixed deposit holders by the applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) shall also be considered while evaluating a company’s application for listing. The auditor’s certificate shall also be obtained in this regard. In case of defaults in such payments the securities of the applicant company may not be listed till such time it has cleared all pending obligations relating to the payment of interest and/or principal.

c) Distribution of shareholding

The applicant’s/promoting company(ies) shareholding pattern on March 31 of last three calendar years separately showing promoters and other groups’ shareholding pattern should be as per the regulatory requirements.

d) Details of Litigation

The applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) litigation record, the nature of

5

litigation, status of litigation during the preceding three years period need to be clarified to the exchange.

e) Track Record of Director(s) of the Company

In respect of the track record of the directors, relevant disclosures may be insisted upon in the offer document regarding the status of criminal cases filed or nature of the investigation being undertaken with regard to alleged commission of any offence by any of its directors and its effect on the business of the company, where all or any of the directors of issuer have or has been charge-sheeted with serious crimes like murder, rape, forgery, economic offences etc.

Note: a) In case a company approaches the Exchange for listing within six months of an IPO, the securities may be considered as eligible for listing if they were otherwise eligible for listing at the time of the IPO. If the company approaches the Exchange for listing after six months of an IPO, the norms for existing listed companies may be applied and market capitalisation be computed based on the period from the IPO to the time of listing.

Securities of Existing Companies

Existing Companies listed on other stock exchanges

1. Paid up Capital & Market Capitalisation

a. The paid-up equity capital of the applicant shall not be less than Rs. 10 crores and the market capitalisation of the applicant’s equity shall not be less than Rs. 25 crores.

Provided that the requirement of Rs. 25 crores market capitalisation under this clause 1(a) shall not be applicable to listing of securities issued by Government Companies, Public Sector Undertakings, Financial Institutions, Nationalised Banks, Statutory Corporations and Banking Companies who are otherwise bound to adhere to all the relevant statutes, guidelines, circulars, clarifications etc. that may be issued by various regulatory authorities from time to time.

or

b. The paid-up equity capital of the applicant shall not be less than Rs. 25 crores (In case the market capitalisation is less than Rs. 25 crores, the securities of the company should be traded for at least 25% of the trading days during the last twelve months preceding the date of submission of application by the

6

company on at least one of the stock exchanges where it is traded.)

or

c. The market capitalisation of the applicant’s equity shall not be less than Rs. 50 crores.

or

d. The applicant Company shall have a net worth of not less than Rs.50 crores in each of the three preceeding financial years. The Company shall submit a certificate from the statutory auditors in respect of networth as stipulated above.

2. Conditions Precedent to Listing:

The applicant shall have adhered to conditions precedent to listing as emerging from inter-alia, Securities Contracts (Regulations) Act 1956, Companies Act 1956, Securities and Exchange Board of India Act 1992, any rules and/or regulations framed under foregoing statutes, as also any circular, clarifications, guidelines issued by the appropriate authority under foregoing statutes.

3. Atleast three years track record of either:a. the applicant seeking listing; or b. the promoters/promoting company, incorporated in or outside India or

For this purpose, the applicant or the promoting company shall submit annual reports of three preceding financial years to NSE and also provide a certificate to the Exchange in respect of the following:

o The company has not been referred to the Board for Industrial and Financial Reconstruction (BIFR)

o The networth of the company has not been wiped out by the accumulated losses resulting in a negative networth.

o The company has not received any winding up petition admitted by a court.

2. The applicant should have been listed on any other recognised stock exchange for atleast last three years

3. The applicant has paid dividend in atleast 2 out of the last 3 financial years immediately preceding the year in which listing application has been made

7

or

The applicant has distributable profits ( as defined under section 205 of the Companies Act, 1956) in at least two out of the last three financial years (an auditors certificate must be provided in this regard).

or

The networth of the applicant is atleast Rs. 50 crores

While considering the profitability / ability to distribute dividend, the non recurring income/extraordinary income shall be excluded from the total income. Further in case of companies where networth criteria is satisfied on account of shares being issued at a premium for consideration other than cash, such cases be referred to the Listing Advisory Committee (LAC) for consideration.

"Provided that Clause 4 and Clause 5 shall not be applicable for listing of:

a) Equity shares and securities convertible into equity issued by

i. a banking company including a local area bank (i.e. Private Sector Banks) set up under sub-clause (c) of Section 5 of the Banking Regulation Act, 1949 and which has received license from the Reserve Bank of India or

ii. a corresponding new bank set up under the Banking Companies (Acquisition and Transfer of Undertakings) Act, 1970, Banking Companies (Acquisition and Transfer of Undertakings) Act, 1980, State Bank of India Act, 1955 and the State Bank of India (Subsidiary Banks) Act, 1959 (i.e. Public Sector Banks) or

iii. an infrastructure company – (a) whose project has been appraised by a Public Financial Institution or Infrastructure Development Finance Corporation (IDFC) or Infrastructure Leasing and Financial Services Limited (IL&FS) and (b) not less than 5% of the project cost is financed by any of the institutions referred to in clause (a) above, jointly or severally, irrespective of whether they appraise the project or not, by way of loan or subscription to equity or a combination of both.

b) Securities other than equity shares or securities convertible into equity shares at a later date issued by Government Companies, Public Sector Undertakings, Financial Institutions, Nationalised Banks, Statutory Corporations, Banking Companies and subsidiaries of Scheduled Commercial Banks.”

8

4. The applicant desirous of listing its securities should also satisfy the Exchange on the following:

a. No Disciplinary action has been taken by other stock exchanges and regulatory authorities in the past three years

The applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) have not been in default in payment of listing fees to any stock exchange in the last three years or has not been delisted or suspended in the past and has not been proceeded against by SEBI or other regulatory authorities in connection with investor related issues or otherwise.

b. Redressal mechanism of Investor grievance

The points of consideration are:

The applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) track record in redressal of investor grievances

The applicant’s arrangements envisaged are in place for servicing its investor

The applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) general approach and philosophy to the issue of investor service and protection

defaults in respect of payment of interest and/or principal to the debenture/bond/fixed deposit holders by the applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) shall also be considered while evaluating a company’s application for listing. The auditor’s certificate shall also be obtained in this regard. In case of defaults in such payments, the securities of the applicant company may not be listed till such time it has cleared all pending obligations relating to the payment of interest and/or principal.

c. Distribution of shareholding

The applicant company/promoting company(ies) shareholding pattern on March 31 of preceding three years separately showing promoters and other groups’ shareholding pattern should be as per the regulatory requirements.

9

d. Details of Litigation

The applicant, promoters/promoting company(ies), group companies, companies promoted by the promoters/promoting company(ies) litigation record, the nature of litigation, status of litigation during the preceding three years need to be clarified to the exchange.

e. Track Record of Director(s) of the Company

In respect of the track record of the directors, relevant disclosures may be insisted upon in the offer document regarding the status of criminal cases filed or nature of the investigation being undertaken with regard to alleged commission of any offence by any of its directors and its effect on the business of the company, where all or any of the directors of issuer have or has been charge-sheeted with serious crimes like murder, rape, forgery, economic offences etc.

f. Change in Control of a Company/Utilisation of funds raised from public

In the event of new promoters taking over listed companies which results in change in management and/or companies utilising the funds raised through public issue for the purposes other than those mentioned in the offer document, such companies shall make additional disclosures (as required by the Exchange) with regard to change in control of a company and utilisation of funds raised from public.

Note:

a) Where an unlisted company merges with a company listed on other stock exchanges and the merged entity seeks listing on the NSE, the Exchange may grant listing to the merged entity only if the listed company (prior to the merger with the unlisted company) meets all the criteria for listing on its own account or the unlisted company meets the requirements for listing on the Exchange, except for the market capitalisation condition, on its own account. In case either of the above conditions are not met then such company may be considered for listing after a minimum period of 18 months or after the publication of two annual reports whichever is later, provided it satisfies the criteria at that point of time.

Listing Procedure

An Issuer has to take various steps prior to making an application for listing its securities on the NSE. These steps are essential to ensure the compliance of certain requirements by the Issuer before listing its securities on the NSE. The various steps to be taken include:

Approval of Memorandum and Articles of Association

10

Approval of draft prospectus

Submission of Application

Listing conditions and requirements

In case your company fulfils the criteria, please send the following information for further processing:

1. A brief note on the promoters and management.2. Company profile.3. Copies of the Annual Report for last 3 years.4. Copies of the Draft Offer Document.5. Memorandum & Articles of Association.

Approval of Memorandum and Articles of Association

Rule 19(2) (a) of the Securities Contracts (Regulation) Rules, 1957 requires that the Articles of Association of the Issuer wanting to list its securities must contain provisions as given hereunder.

The Articles of Association of an Issuer shall contain the following provisions namely:

a. that there shall be no forfeiture of unclaimed dividends before the claim becomes barred by law; b. that a common form of transfer shall be used;

c. that fully paid shares shall be free from all lien and that in the case of partly paid shares the Issuer's lien shall be restricted to moneys called or payable at a fixed time in respect of such shares;

d. that registration of transfer shall not be refused on the ground of the transferor being either alone or jointly with any other person or persons indebted to the Issuer on any account whatsoever;

e. that any amount paid up in advance of calls on any share may carry interest but shall not in respect thereof confer a right to dividend or to participate in profits;

f. that option or right to call of shares shall not be given to any person except with the sanction of the Issuer in general meetings.

g. permission for Sub-Division/Consolidation of Share Certificate.

11

Note: The Relevant Authority may take exception to any provision contained in the Articles of Association of an Issuer which may be deemed undesirable or unreasonable in the case of a public company and may require inclusion of specific provisions deemed to be desirable and necessary.

If the Issuer's Articles of Association is not in conformity with the provisions as stated above, the Issuer has to make amendments to the Articles of Association. However, the securities of an Issuer may be admitted for listing on the NSE on an undertaking by the Issuer that the amendments necessary in the Articles of Association to bring Articles of Association in conformity with Rule 19(2)(a) of the Securities Contract (Regulation) Rules, 1957 shall be made in the next annual general meeting and in the meantime the Issuer shall act strictly in accordance with prevalent provisions of Securities Contract (Regulation) Act, 1957 and other statutes.

It is to be noted that any provision in the Articles of Association which is not in tune with sound corporate practice has to be removed by amending the Articles of Association.

Approval of draft prospectus

The Issuer shall file the draft prospectus and application forms with NSE. The draft prospectus should have been prepared in accordance with the statutes, notifications, circulars, guidelines, etc. governing preparation and issue of prospectus prevailing at the relevant time. The Issuers may particularly bear in mind the provisions of Companies Act, Securities Contracts (Regulation) Act, the SEBI Act and the relevant subordinate legislations thereto. NSE will peruse the draft prospectus only from the point of view of checking whether the draft prospectus is in accordance with the listing requirements, and therefore any approval given by NSE in respect of the draft prospectus should not be construed as approval under any laws, rules, notifications, circulars, guidelines etc. The Issuer should also submit the SEBI acknowledgment card or letter indicating observations on draft prospectus or letter of offer by SEBI.

Submission of Application

For Issuers listing on NSE for the first time

Listing of further Issues by Issuers already listed on NSE

Listing Fees

Security deposit (for new & fresh issues and when NSE is the Regional Stock Exchange)

Supporting documents

12

For Issuers listing on NSE for the first time

Issuers desiring to list existing/new securities on the NSE shall make application for admission of their securities to dealings on the NSE in the forms prescribed in this regard as per details given hereunder or in such other form or forms as the Relevant Authority may from time to time prescribe in addition thereto or in modification or substitution thereof.

Appendix 'A' - Clauses of Articles of Association.Appendix 'B'- Application Letter for Listing.Appendix 'C-1' - Listing Application providing pre-issue details of securities.Appendix 'C-2' - Listing Application providing post-issue details of securities.Appendix 'D'- Checklist for supporting documents ( as applicable to the issuer)Appendix 'E' - Schedule of DistributionAppendix 'F'- Listing Agreement

Listing of further Issues by Issuers already listed on NSE

Issuers whose securities are already listed on the NSE shall apply for admission to listing on the NSE of any further issue of securities made by them. The application for admission shall be made in the forms prescribed in this regard or in such other form or forms as the Relevant Authority may from time to time prescribe in addition thereto or in modification or substitution thereof.

Appendix 'E' - Schedule of DistributionAppendix 'G'- Application Letter for Listing of further issues.Appendix 'H' - Listing Application providing details of securities.Appendix 'I' - Checklist for supporting documents submitted (as applicable)

Listing Fees

The listing fees depend on the paid up share capital of your Company:

Particulars Amount (Rs.)

Initial Listing Fees 25,000

Annual Listing Fees (based on paid up share, bond and/or debenture and/or debt capital etc.)

Upto Rs. 1 Crore 10,000

Above Rs. 1 Crore and upto Rs.5 Crores 15,000

Above Rs. 5 Crore and upto Rs.10 Crores 25,000

Above Rs. 10 Crore and upto Rs.20 Crores 45,000

Above Rs. 20 Crore and upto Rs.30 Crores 70,000

Above Rs. 30 Crore and upto Rs.40 Crores 75,000

Above Rs. 40 Crore and upto Rs.50 Crores 80,000

13

Above Rs. 50 Crores and upto Rs.100 Crores 1,30,000

Above Rs. 100 Crore and upto Rs.150 Crores 1,50,000

Above Rs. 150 Crore and upto Rs.200 Crores 1,80,000

Above Rs. 200 Crore and upto Rs.250 Crores 2,05,000

Above Rs. 250 Crore and upto Rs.300 Crores 2,30,000

Above Rs. 300 Crore and upto Rs.350 Crores 2,55,000

Above Rs. 350 Crore and upto Rs.400 Crores 2,80,000

Above Rs. 400 Crore and upto Rs.450 Crores 3,25,000

Above Rs. 450 Crore and upto Rs.500 Crores 3,75,000

Companies which have a paid up share, bond and/ or debenture and/or debt capital, etc. of more than Rs.500 crores will have to pay minimum fees of Rs.3,75,000 and an additional listing fees of Rs.2,500 for every increase of Rs.5 crores or part thereof in the paid up share, bond and/ or debenture and/or debt capital, etc.

Companies which have a paid up share, bond and/ or debenture and/or debt capital, etc. of more than Rs.1,000 crores will have to pay minimum fees of Rs.6,30,000 and an additional listing fees of Rs.2,750 for every increase of Rs.5 crores or part thereof in the paid up share, bond and/ or debenture and/or debt capital, etc.

Security Deposit

(Payable only for new and fresh issues and only when NSE is the Regional Stock Exchange)

The Relevant Authority shall not grant admission to dealings of securities of an Issuer which is not listed or of any new (original or further) issue of securities of an Issuer excepting Mutual Funds, which is listed on the NSE unless the Issuer deposits and keeps deposited with the NSE (in cases where the securities are offered for subscription, whether through the issue of a prospectus, letter of offer or otherwise, and NSE is the Regional Stock Exchange for the Issuer) an amount calculated at 1% of the amount of securities offered for subscription to the public and or to the holders of existing securities of the Issuer, as the case may be for ensuring compliance by the Issuer within the prescribed or stipulated period of all requirements and conditions hereinafter mentioned and shall be refundable or forfeitable in the manner hereinafter stated:

1. The Issuer shall comply with all prevailing requirements of law including all requirements of and under any notifications, directives and guidelines issued by the Central Government, SEBI or any statutory body or local authority or any body or

14

authority acting under the authority or direction of the Central Government and all prevailing listing requirements and conditions of the NSE and of each recognized Stock Exchange where the Issuer has applied for permission for admission to dealings of the securities, within the prescribed or stipulated period;

2. If the Issuer has complied with all the aforesaid requirements and conditions including, wherever applicable, its obligation under Section 73 (or any statutory modification or re-enactment thereof) of the Companies Act, 1956 and obligations arising therefrom, within the prescribed or stipulated period, and on obtaining a No Objection Certificate from SEBI and submitting it to NSE , NSE shall refund to the Issuer the said deposit without interest within fifteen days from the expiry of the prescribed or stipulated period;

3. If on expiry of the prescribed or stipulated period or the extended period referred to hereafter, the Issuer has not complied with all the aforesaid requirements and conditions, the said deposit shall be forfeited by the NSE, at its discretion, and thereupon the same shall vest in the NSE. Provided the forfeiture shall not release the Issuer of its obligation to comply with the aforesaid requirements and conditions;

4. If the Issuer is unable to complete compliance of the aforesaid requirements and conditions within the prescribed or stipulated period, the NSE, at its discretion and if the Issuer has shown sufficient cause, but without prejudice to the obligations of the Issuer under the laws in force to comply with any such requirements and conditions within the prescribed or stipulated period, may not forfeit the said deposit but may allow such further time to the Issuer as the NSE may deem fit; provided that

a. the Issuer has at least ten days prior to expiry of the prescribed or stipulated period applied in writing for extension of time to the NSE stating the reasons for non-compliance, and

b. the Issuer, having been allowed further time by the NSE, has before expiry of the prescribed or stipulated period, published in a manner required by the NSE, the fact of such extension having been allowed; provided further that where the NSE has not allowed extension in writing before expiry of the prescribed or stipulated period, the request for extension shall be deemed to have been refused; provided also that any such extension shall not release the Issuer of its obligations to comply with the aforesaid requirements and conditions.

2. 50% of the above mentioned security deposit should be paid to the NSE in cash. The balance amount can be provided by way of a bank guarantee, in the format prescribed by or acceptable to NSE. The amount to be paid in cash is limited to Rs.3 crores.

15

Supporting Documents

Issuers applying for admission of their securities to dealings on the NSE shall submit to the NSE the following:

Documents and InformationThe documents and information prescribed in Appendix D or Appendix I (as the case may be) to this Regulation or such other documents and information as the Relevant Authority may from time to time prescribe, in addition thereto or in modification or substitution thereof together with any other documents and information which the Relevant Authority may require in any particular case;

Distribution SchedulesDistribution Schedules duly completed in respect of each class and kind of security in the form prescribed in Appendix E (Table I, II & III) to this Regulation or in such other form or forms as the Relevant Authority may from time to time prescribe in addition thereto or in modification or substitution thereof.

16

BSE

Guidelines for Listing

The Bombay Stock Exchange (BSE) has a dedicated Listing Department to grant approval for listing of securities of companies in accordance with the provisions of the Securities Contracts (Regulation) Act, 1956, Securities Contracts (Regulation) Rules, 1957, Companies Act, 1956, Guidelines issued by SEBI and Rules, Bye-laws and Regulations of BSE.

BSE has set various guidelines and forms that need to be adhered to and submitted by the companies. These guidelines will help companies to expedite the fulfillment of the various formalities and disclosure requirements that are required at various stages of

Public Issues o Initial Public Offering

o Further Public Offering

Preferential Issues

Indian Depository Receipts

Amalgamation

Qualified Institutions Placements

A company intending to have its securities listed on BSE has to comply with the listing requirements prescribed by it. Some of the requirements are as under :

I Minimum Listing Requirements for New Companies

II Minimum Listing Requirements for Companies already Listed on other Stock Exchanges

III Minimum Requirements for Companies Delisted by BSE seeking relisting on BSE

IV Permission to Use the Name of BSE in an Issuer Company's Prospectus

V Submission of Letter of Application

VI Allotment of Securities

VII Trading Permission

VIII Requirement of 1% Security

IX Payment of Listing Fees

X Compliance with the Listing Agreement

XI Cash Management Services (CMS) - Collection of Listing Fees

17

[I] Minimum Listing Requirements for New Companies

The following eligibility criteria have been prescribed effective August 1, 2006 for listing of companies on BSE, through Initial Public Offerings (IPOs) & Follow-on Public Offerings (FPOs):

1. Companies have been classified as large cap companies and small cap companies. A large cap company is a company with a minimum issue size of Rs. 10 crore and market capitalization of not less than Rs. 25 crore. A small cap company is a company other than a large cap company.

a. In respect of Large Cap Companies

i. The minimum post-issue paid-up capital of the applicant company (hereinafter referred to as "the Company") shall be Rs. 3 crore; and

ii. The minimum issue size shall be Rs. 10 crore; and

iii. The minimum market capitalization of the Company shall be Rs. 25 crore (market capitalization shall be calculated by multiplying the post-issue paid-up number of equity shares with the issue price).

b. In respect of Small Cap Companies

i. The minimum post-issue paid-up capital of the Company shall be Rs. 3 crore; and

ii. The minimum issue size shall be Rs. 3 crore; and

iii. The minimum market capitalization of the Company shall be Rs. 5 crore (market capitalization shall be calculated by multiplying the post-issue paid-up number of equity shares with the issue price); and

iv. The minimum income/turnover of the Company shall be Rs. 3 crore in each of the preceding three 12-months period; and

v. The minimum number of public shareholders after the issue shall be 1000.

vi. A due diligence study may be conducted by an independent team of Chartered Accountants or Merchant Bankers appointed by BSE, the cost of which will be borne by the company. The requirement of a due diligence study may be waived if a financial institution or a scheduled commercial bank has appraised the project in the preceding 12 months.

2. For all companies :

a. In respect of the requirement of paid-up capital and market capitalization, the issuers shall be required to include in the disclaimer clause forming a part of the offer document that in the event of the market capitalization (product of issue price and the post issue number of shares) requirement of BSE not being met, the securities of the issuer would not be listed on

18

BSE.

b. The applicant, promoters and/or group companies, shall not be in default in compliance of the listing agreement.

c. The above eligibility criteria would be in addition to the conditions prescribed under SEBI (Disclosure and Investor Protection) Guidelines, 2000.

[II] Minimum Listing Requirements for Companies already Listed on Other Stock Exchanges

The listing norms for companies already listed on other stock exchanges and seeking listing at BSE, made effective from August 6, 2002, are as under:

1. The company shall have a minimum issued and paid up equity capital of Rs. 3 crore. 2. The company shall have a profit making track record for the preceding last three years. The

revenues/profits arising out of extra ordinary items or income from any source of non-recurring nature shall be excluded while calculating the profit making track record.

3. Minimum net worth shall be Rs. 20 crore (net worth includes equity capital and free reserves excluding revaluation reserves).

4. Minimum market capitalization of the listed capital shall be at least two times of the paid up capital.

5. The company shall have a dividend paying track record for at least the last 3 consecutive years and the dividend should be at least 10% in each year.

6. Minimum 25% of the company's issued capital shall be with Non-Promoter shareholders as per Clause 35 of the Listing Agreement. Out of above Non-Promoter holding, no single shareholder shall hold more than 0.5% of the paid-up capital of the company individually or jointly with others except in case of Banks/Financial Institutions/Foreign Institutional Investors/Overseas Corporate Bodies and Non-Resident Indians.

7. The company shall have at least two years listing record with any of the Regional Stock Exchanges.

8. The company shall sign an agreement with CDSL and NSDL for demat trading.

[III] Minimum Requirements for Companies Delisted by BSE seeking Relisting on BSE

Companies delisted by BSE and seeking relisting at BSE are required to make a fresh public offer and

19

comply with the extant guidelines of SEBI and BSE regarding initial public offerings.

[V] Submission of Letter of Application

As per Section 73 of the Companies Act, 1956, a company seeking listing of its securities on BSE is required to submit a Letter of Application to all the stock exchanges where it proposes to have its securities listed before filing the prospectus with the Registrar of Companies.

[VI] Allotment of Securities

As per the Listing Agreement, a company is required to complete the allotment of securities offered to the public within 30 days of the date of closure of the subscription list and approach the Designated Stock Exchange for approval of the basis of allotment.

In case of Book Building issues, allotment shall be made not later than 15 days from the closure of the issue, failing which interest at the rate of 15% shall be paid to the investors.

[VII] Trading Permission

As per SEBI Guidelines, an issuer company should complete the formalities for trading at all the stock exchanges where the securities are to be listed within 7 working days of finalization of the basis of allotment.

A company should scrupulously adhere to the time limit specified in SEBI (Disclosure and Investor Protection) Guidelines 2000 for allotment of all securities and dispatch of allotment letters/share certificates/credit in depository accounts and refund orders and for obtaining the listing permissions of all the exchanges whose names are stated in its prospectus or offer document. In the event of listing permission to a company being denied by any stock exchange where it had applied for listing of its securities, the company cannot proceed with the allotment of shares. However, the company may file an appeal before SEBI under Section 22 of the Securities Contracts (Regulation) Act, 1956.

[VIII] Requirement of 1% Security

Companies making public/rights issues are required to deposit 1% of the issue amount with the Designated Stock Exchange before the issue opens. This amount is liable to be forfeited in the event of the company not resolving the complaints of investors regarding delay in sending refund orders/share certificates, non-payment of commission to underwriters, brokers, etc.

[IX] Payment of Listing Fees

All companies listed on BSE are required to pay to BSE the Annual Listing Fees by 30th April of every financial year as per the Schedule of Listing Fees prescribed from time to time.

20

The schedule of Listing Fees for the year 2008-09, prescribed by the Governing Board of BSE, is given here under:

SCHEDULE OF LISTING FEES FOR THE YEAR 2008-09

Securities *other than Privately Placed Debt Securities

Sl. No. Particulars Amount (Rs.)

1 Initial Listing Fees 20,000.00

2 Annual Listing Fees (i) Companies with listed capital* up to Rs. 5 crore

(ii) Above Rs. 5 crore and up to Rs. 10 crore

(iii) Above Rs. 10 crore and up to Rs. 20 crore

Companies which have a listed capital* of more than Rs. 20 crore are required to pay an additional fee @ Rs. 750 for every additional Rs. 1 crore or part thereof.

10,000.00

15,000.00

30,000.00

NOTE: In case of debenture capital (not convertible into equity shares) , the fees will be 25% of the above fees.

*includes equity shares, preference shares, fully convertible debentures, partly convertible debentures and any other security convertible into equity shares.

Privately Placed Debt Securities

Sl. No. Particulars Amount (Rs.)

1 Initial Listing Fees NIL

2 Annual Listing Fees (i)Issue size up to Rs.5 crore

(ii)Above Rs.5 crore and up to Rs.10 crore

(iii)Above Rs.10 crore and up to Rs.20 crore

Above Rs.20 crore

Rs.2,500.00

Rs.3,750.00

Rs.7,500.00

Additional fee of Rs.200.00 for every additional Rs.1 crore or part thereof

21

Subject to a maximum of Rs.30,000.00 per instrument.

The cap on the annual listing fee of debt instruments per issuer is Rs.5, 00,000.00 per annum.

PAYMENT DATE

The last date for payment of Listing Fee for the year 2008-09 is April 30, 2008. Failure to pay the Listing Fee (for equity and/or debt segment) by the due date will attract interest @ 12% per annum w.e.f. May 1, 2008.

[X] Compliance with the Listing Agreement

Companies desirous of getting their securities listed at BSE are required to enter into an agreement with BSE called the Listing Agreement, under which they are required to make certain disclosures and perform certain acts, failing which the company may face some disciplinary action, including suspension/delisting of securities. As such, the Listing Agreement is of great importance and is executed under the common seal of a company. Under the Listing Agreement, a company undertakes, amongst other things, to provide facilities for prompt transfer, registration, sub-division and consolidation of securities; to give proper notice of closure of transfer books and record dates, to forward 6 copies of unabridged Annual Reports, Balance Sheets and Profit and Loss Accounts to BSE, to file shareholding patterns and financial results on a quarterly basis; to intimate promptly to the Exchange the happenings which are likely to materially affect the financial performance of the Company and its stock prices, to comply with the conditions of Corporate Governance, etc.

The Listing Department of BSE monitors the compliance by the companies with the provisions of the Listing Agreement, especially with regard to timely payment of annual listing fees, submission of results, shareholding patterns and corporate governance reports on a quarterly basis . Penal action is taken against the defaulting companies.

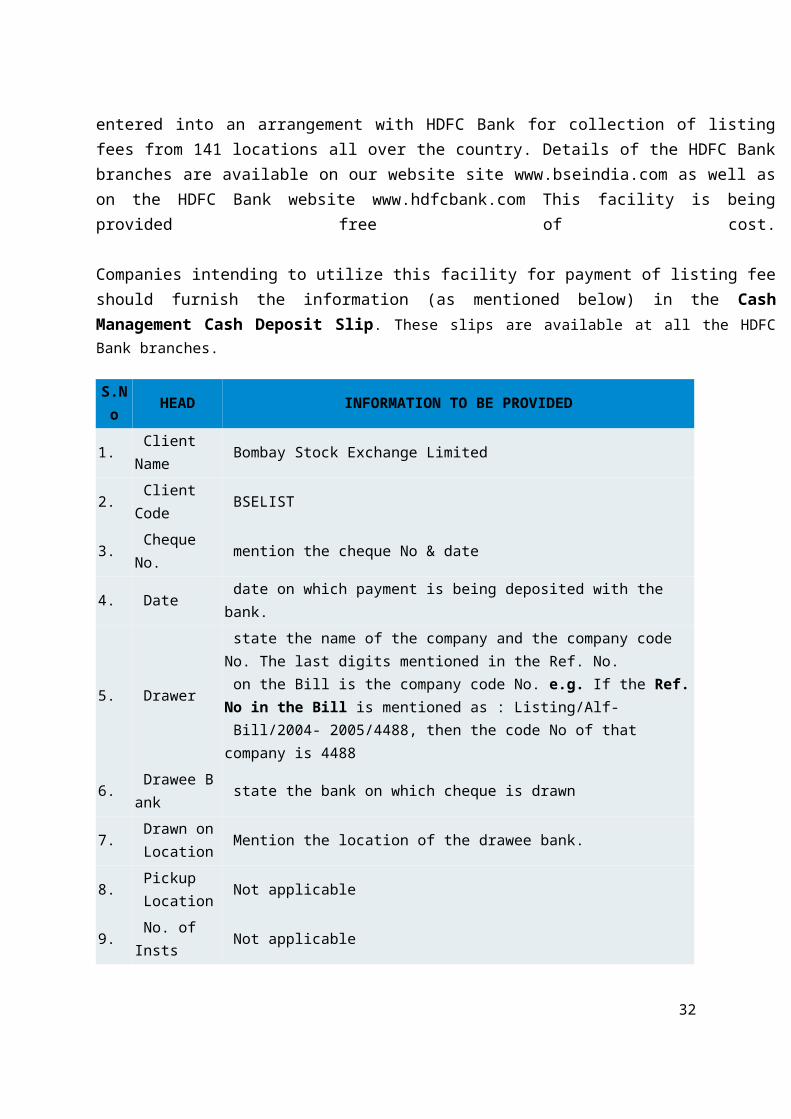

[XI] Cash Management Services (CMS) - Collection of Listing Fees

In order to simplify the system of payment of listing fees, BSE has entered into an arrangement with HDFC Bank for collection of listing fees from 141 locations all over the country. Details of the HDFC Bank branches are available on our website site www.bseindia.com as well as on the HDFC Bank website www.hdfcbank.com This facility is being provided free of cost.

Companies intending to utilize this facility for payment of listing fee should furnish the information (as mentioned below) in the Cash Management Cash Deposit Slip. These slips are available at all the HDFC Bank branches.

S.No HEAD INFORMATION TO BE PROVIDED

1. Client Name Bombay Stock Exchange Limited

2. Client Code BSELIST

3. Cheque No. mention the cheque No & date

4. Date date on which payment is being deposited with the bank.

22

5. Drawer

state the name of the company and the company code No. The last digits mentioned in the Ref. No. on the Bill is the company code No. e.g. If the Ref. No in the Bill is mentioned as : Listing/Alf- Bill/2004- 2005/4488, then the code No of that company is 4488

6. Drawee Bank state the bank on which cheque is drawn

7. Drawn on Location

Mention the location of the drawee bank.

8. Pickup Location

Not applicable

9. No. of Insts Not applicable

23

Listing Guidelines

EQUITY

SOME OF THE IMPORTANT CLAUSES UNDER LISTING AGREEMENT ARE:-

Clause 16

The Company on whose stocks, derivatives are available or whose stocks form part of an index on which derivatives are available, shall give a notice period of 30 days to stock exchanges for corporate actions like mergers, de-mergers, splits and bonus shares.

Clause 18

The Issuer will publish in a form approved by NSE such periodical interim statements of its working and earning as required by NSE, SEBI, or any statutory body or local authority or anybody or authority acting under the authority or direction of the Central Government.

Clause 20

The Issuer will, immediately after the meeting of its Board of Directors has been held to consider or decide the same, intimate to the Stock Exchanges where the company is listed, (within 15 minutes of the closure of the board meeting) by phone, fax, telegram, e-mail:

a) all dividends and/or cash bonuses recommended or declared or the decision to pass any dividend or interest payment;

b) the total turnover, gross profit/loss, provision for depreciation, tax provisions and net profits for the year (with comparison with the previous year) and the amounts appropriated from reserves, capital profits, accumulated profits of past years or other special source to provide wholly or partly for the dividend, even if this calls for qualification that such information is provisional or subject to audit

Clause 22

The Issuer will, immediately after the meeting of its Board of Directors has been held to consider or decide the same, intimate to the Stock Exchanges where the company is listed, (within 15 minutes of the closure of the board meeting) by phone, fax, telegram, e-mail :

a) short particulars of any increase of capital whether by issue of bonus shares through capitalization, or by way of right shares to be offered to the shareholders or debenture holders, or in any other way.

b) any other information necessary to enable the holders of the listed securities of the Issuer to appraise its position and to avoid the establishment of a false market in such listed securities.

Clause 31

24

The Issuer will forward to NSE promptly and without application:-

a) six copies of the Statutory and Directors’ Annual Reports, Balance Sheets and Profits & Loss Accounts and of all periodical and special reports as soon as they are issued and one copy each to all the recognized stock exchanges in India;

b) six copies of all notices, resolutions and circulars relating to new issue of capital prior to their dispatch to the shareholders;

c) three copies of all the notices, call letters or any other circulars including notices of meetings convened at the same time as they are sent to the shareholders, debenture holders or creditors or any class of them or advertised in the Press.

d) copy of the proceedings at all Annual and Extraordinary General Meetings of the Issuer;

e) three copies of all notices, circulars, etc., issued or advertised in the press either by the Issuer, or by any Issuer which the Issuer proposes to absorb or with which the Issuer proposes to merge or amalgamate, or under orders of the court or any other statutory authority in connection with any merger, amalgamation, re-construction, reduction of capital, scheme or arrangement, including notices, circulars, etc. issued or advertised in the press in regard to meetings of shareholders or debenture holders or creditors or any class of them and copies of the proceedings at all such meetings.

Clause 32

The Issuer will supply a copy of the complete and full Balance Sheet, Profit and Loss Account and the Directors’ Report to each shareholder and upon application to any member of NSE.

The issuer will also give cash flow statement along with the Balance Sheet and Profit and Loss Account. The Cash Flow Statement will be prepared in accordance with the Accounting Standard on Cash Flow Statement (AS-3) issued by the Institute of Chartered Accountants of India, and the Cash Flow Statement shall be presented only under the Indirect Method as given in AS-3. The statement shall be issued under the authority of the Board and shall be signed on behalf of the Board of Directors in the manner provided for the authentication of Balance Sheet and Profit and Loss Account in Section 215 of the Companies Act, 1956

25

Consolidated Financial Statement:

According to Accounting Standard (AS) 21 of ICAI:

Consolidated financial statements are the financial statements of a group presented as those of a single enterprise.

Consolidated Financial Statement:

Companies shall be mandatory required to publish Consolidated Financial Statements in the annual report in addition to the individual financial statements.

Audit of Consolidated Financial Statements by the statutory auditors of the company and the filing of Consolidated Financial Statements audited by the statutory auditors of the company with the stock exchanges shall be mandatory.

Related Party Disclosures :

According to Accounting Standard (AS) 18 of ICAI:

Related party - parties are considered to be related if at any time during the reporting period one party has the ability to control the other party or exercise significant influence over the other party in making financial and/or operating decisions.

Companies shall be required to make disclosures in compliance with the Accounting Standard on "Related Party Disclosures" in the annual reports.

The Issuer agrees to make the following disclosure in the Annual Report:

i) In case the shares are delisted, it shall disclose the fact of delisting, together with reasons thereof in its Directors Report

ii) In case the securities are suspended from trading, the Directors Report should explain the reason thereof.

The above disclosures shall be applicable to all listed companies except for listed banks.

Clause 35

The company agrees to file the following details with the Exchange on a quarterly basis, within 21 days from the end of each quarter, in the format specified as under:

Statement showing Shareholding Pattern Statement showing Shareholding of persons belonging to the category “Promoter and

Promoter Group” Statement showing Shareholding of persons belonging to the category “Public” and

holding more than 1% of the total number of shares Statement showing details of locked-in shares.

26

Clause 41

The company agrees to comply with the following provisions:-

I) Preparation and Submission of Financial Results

II) Manner of approval and authentication of the financial results

III) Intimation of Board Meeting

IV) Other requirements as to financial results

V) Formats

VI) Publication of financial results in newspapers

VII) Interpretation

We will explain some of the important subsections of this clause like I,IV,VI and VII

I) Preparation and Submission of Financial Results

A)The financial results filed and published in compliance with this clause shall be prepared on the basis of accrual accounting policy and in accordance with uniform accounting practices adopted for all the periods.

B)The company shall submit its quarterly, year to date and annual financial results to the stock exchange in the manner prescribed in this clause.

C)The company has an option either to submit audited or unaudited quarterly and year to date financial results to the stock exchange within one month of end of each quarter (other than the last quarter), subject to the following:

1)In case the company opts to submit audited financial results, they shall be accompanied by the audit report.

2) In case the company opts to submit unaudited financial results, they shall be subjected to limited review by the statutory auditors of the company (or in case of public sector undertakings, by any practicing Chartered Accountant) and a copy of the limited review report shall be furnished to the stock exchange within two months from end of the quarter.(vide SEBI order June 30, 2003)

D)In respect of the last quarter, the company has an option either to submit unaudited financial results for the quarter within one month of end of the financial year or to submit audited financial results for the entire financial year within three months of end of the financial year, subject to the following:

27

1) In case the company opts to submit audited financial results for the entire financial year, it shall intimate the stock exchange in writing within one month of end of the financial year, about such exercise of option.

2) In case the company opts to submit un-audited financial results for the last quarter, it shall also submit audited financial results for the entire financial year, as soon as they are approved by the Board. Such un-audited financial results for the last quarter shall also be subjected to limited review by the statutory auditors of the company (or in case of public sector undertakings, by any practicing Chartered Accountant) and a copy of the limited review report shall be furnished to the stock exchange within two months from end of the quarter.

E) If the company has subsidiaries, -

it may, in addition to submitting quarterly and year to date stand alone financial results to the stock exchange under item (c) i.e. within one month of the end of the quarter, also submit quarterly and year to date consolidated financial results within two months from the end of the quarter; and

while submitting annual audited financial results prepared on stand-alone basis under item (c), it shall also submit annual audited consolidated financial results to the stock exchange.

IV) Other requirements as to financial results

a) Where there is a variation between the unaudited quarterly or year to date financial results and the results amended pursuant to limited review for the same period, the company shall submit to the stock exchange an explanation of the reasons for variations, while submitting the limited review report.

b) If the auditor has expressed any qualification or other reservation in respect of audited financial results submitted or published under this clause, the company shall disclose such qualification or other reservation and impact of the same on the profit or loss, while publishing or submitting such results.

c) If the auditor has expressed any qualification or other reservation in his audit report or limited review report in respect of the financial results of any previous financial year or quarter which has an impact on the profit or loss of the reportable period, the company shall include as a note to the financial results –

◦ how the qualification or other reservation has been resolved; or

◦ if it has not been resolved, the reason therefore and the steps which the company intends to take in the matter.

d) If the company has changed its name suggesting any new line of business, it shall disclose the net sales or income, expenditure and net profit or loss after tax figures

28

pertaining to the said new line of business separately in the financial results and shall continue to make such disclosures for the three years succeeding the date of change in name.

If the company had not commenced commercial production or commercial operations during the reportable period, the company shall, instead of submitting financial results, disclose the details of amount raised, the portions thereof which is utilized and that remaining unutilized, the details of investment made pending utilization, brief description of the project which is pending completion, status of the project and expected date of commencement of commercial production or commercial operations.

e) The quarterly and year to date results shall be prepared in accordance with the recognition and measurement principles laid down in Accounting Standard 25 (AS 25 – Interim Financial Reporting) issued by the Institute of Chartered Accountants of India (ICAI)/Company (Accounting Standards) Rules, 2006, whichever is applicable.

f) All items of income and expenditure arising out of transactions of exceptional nature shall be disclosed.

g) Extraordinary items, if any, shall be disclosed in accordance with Accounting Standard 5 (AS 5 – Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies) issued by the Institute of Chartered Accountants of India (ICAI)/Company (Accounting Standards) Rules, 2006, whichever is applicable.

h) Changes in accounting policies, if any, shall be disclosed in accordance with Accounting Standard 5 (AS 5 – Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies) issued by the Institute of Chartered Accountants of India (ICAI)/Company (Accounting Standards) Rules, 2006, whichever is applicable.

i) Companies, whose revenues are subject to material seasonal variations, shall disclose the seasonal nature of their activities.

j) The company shall disclose any event or transaction which occurred during or before the quarter that is material to an understanding of the results for the quarter including but not limited to completion of expansion and diversification programmes, strikes and lock-outs, change in management and change in capital structure. The company shall also disclose similar material events or transactions that take place subsequent to the end of the quarter.

k) The company shall disclose the following in respect of dividends paid or recommended for the year, including interim dividends:

amount of dividend distributed or proposed for distribution per share; the amounts in respect of different classes of shares shall be distinguished and the nominal values of shares shall also be indicated.

29

l) The company shall disclose the effect on the financial results of material changes in the composition of the company, if any, including but not limited to business combinations, acquisitions or disposal of subsidiaries and long term investments, any other form of restructuring and discontinuance of operations.

V) Format

Segment Reporting

If the company has more than one reportable primary segment in terms of Accounting Standard 17 (AS 17 – Segment Reporting) issued by ICAI/Company (Accounting Standards) Rules, 2006, it shall also submit quarterly or annual segment information as part of financial results.

VIII) Interpretation

For the purposes of this clause, -

‘financial year’ means the period of twelve months commencing on the first day of April every year, subject however to items (e) to (h);

‘annual results’ mean the financial results prepared in accordance with this clause in respect of a financial year;

‘quarter’ means the period of three months commencing on the first day of April, July, October or January of a financial year, subject however to items (e) to (h);

quarterly results’ mean the financial results prepared in accordance with this clause in respect of a quarter;

Clause 43A

Statement of deviations in use of issue proceeds –

The company agrees to furnish to the stock exchange on a quarterly basis, a statement indicating material deviations, if any, in the use of proceeds of a public or rights issue from the objects stated in the offer document.

Clause 48

Companies should co-operate with the Credit Rating Agencies in giving correct and adequate information for periodical review of the securities during lifetime of the rated securities.

30

Clause 49

Corporate Governance

I)Board of Directors

(A) Composition Of Board

The Board of directors of the company shall have an optimum combination of executive and non-executive directors with not less than fifty percent of the board of directors comprising of non-executive directors. (SEBI in its circular to stock exchanges in October 2004).

Where the Chairman of the Board is a non-executive director, at least one-third of the Board should comprise of independent directors and in case he is an executive director at least half of the Board should comprise of independent directors.

(B) Non executive directors’ compensation and disclosures

All fees/compensation, if any paid to non-executive directors, including independent directors, shall be fixed by the Board of Directors and shall require previous approval of shareholders in general meeting. (SEBI vide its circular dated 26th August 2003)

(C) Additional duty on the independent director

An independent director would be supposed to periodically review the legal compliance reports prepared by the Company and steps taken by the Company to improve the taints. (SEBI vide its circular dated 26th August 2003)

(D) Code of Conduct for all Board members and senior management of the Company.

The Board shall lay down the code of conduct for all Board members and senior management of a company.

This code of conduct shall be posted on the website of the company. All Board members and senior management personnel shall affirm compliance with the code on an annual basis. The annual report of the company shall contain a declaration to this effect signed by the CEO and COO. ((SEBI vide its circular dated 26th August 2003)

II) Audit Committee

(A)Qualified and Independent Audit Committee

(B) Meeting of Audit Committee

(C)Powers of Audit Committee

Other sub sections under this clause are-

31

III. Subsidiary Companies

IV. Disclosures

V. CEO/CFO certification

VI. Report on Corporate Governance

VII. Compliance

There is some non-mandatory clauses for example- Whistle Blower Policy

Whistle Blower Policy(non-mandatory)

So as to detect frauds, irregularities and encouraging employees to come forward to Audit Committee, concept of "Whistle Blower "has been introduced. The following are the notable features of the 'Whistle Blower Policy" are:

1.Personnel who observe an unethical or improper practice (not necessarily a violation of law) shall be able to approach the audit committee without necessarily informing their supervisors.

2. Companies shall take measures to ensure that this right of access is communicated to all employees through means of internal circulars, etc. The employment and other personnel policies of the company shall contain provisions protecting "whistle blowers" from unfair termination and other unfair prejudicial employment practices.

Clause 50

Companies shall mandatorily comply with all the Accounting Standards issued by ICAI from time to time

Listing of Debt Instruments

Wholesale Debt Market

The Wholesale Debt Market segment deals in fixed income securities. The Wholesale Debt Market (WDM) segment of the Exchange commenced operations on June 30, 1994.This segment provides trading facilities for a variety of debt instruments including Government Securities, Treasury Bills and Bonds issued by Public Sector Undertakings/ Corporate/ Banks.

32

Retail Debt Market

With a view to encouraging wider participation of all classes of investors (including retail investors) in government securities, the Government, RBI and SEBI have introduced trading in government securities for retail investors. Trading in this retail debt market segment (RDM) on NSE has been introduced w.e.f. January 16, 2003.In the first phase, all outstanding and newly issued central government securities would be traded in the retail segment.

Important Clauses

The Issuer agrees to notify the Exchange regarding expected default in timely payment of interest or redemption amount or both in respect of the debentures listed on the exchange as soon as the same becomes apparent to the Issuer.

Delay in Payment of Interest / Principal Amount

The Issuer will promptly notify the Exchange, as and when there is a delay in timely payment of interest and / or the possibility of delay in repayment of the principal amount.

Listing of IDRs

Indian Depository Receipts (IDRs) are basically financial instruments that allow foreign companies to mobilise funds from Indian markets by offering equity and getting listed on Indian stock exchanges. This instrument is similar to the GDRs and ADRs that allow foreign companies to raise funds from European and American markets, respectively.

33

LISTING ON A FOREIGN STOCK EXCHANGE

BENEFITS AND DRAWBACKS

Benefits

There are many advantages that accrue to companies that attain a public listing of their

shares. Some of the key considerations and benefits are:

Creating a market for the company’s shares;

Enhancing the status and financial standing of the company;

Increasing public awareness and public interest in the company and its products;

Providing the company with an opportunity to implement share option schemes for

their employees;

Accessing to additional fund raising in the future by means of new issues of shares or

other securities;

Facilitating acquisition opportunities by use of the company’s shares; and

Offering existing shareholders a ready means of realising their investments.

Drawbacks

While there are benefits to going public, it also means additional obligations and reporting

requirements on the companies and its directors:

Increasing accountability to public shareholders

Need to maintain dividend and profit growth trends

Becoming more vulnerable to an unwelcome takeover

Need to observe and adhere strictly to the rules and regulations by governing bodies

Increasing costs in complying with higher level of reporting requirements

Relinquishing some control of the company following the public offering

Suffering a loss of privacy as a result of media interest

US accounting and reporting framework

34

The US securities markets represent the largest source of capital in the world and present

many opportunities to foreign companies seeking to raise capital and to increase their global

profile.

However, because of the extensive information and compliance standards required by the US

regulatory environment, companies seeking to list on NASDAQ/NYSE must prepare

themselves for the technical challenges of demonstrating their ability to manage their

operations and financial health, of establishing and maintaining effective corporate

governance and internal controls, and of increasing their reporting transparency.

The principal regulator of the US capital markets is the SEC. Based in Washington, DC, it is

tasked with ensuring a fair and level playing field for publicly listed companies and their

investors. Before a company can sell securities to the public in the United States, it must first

submit a registration statement to the SEC, which includes information that adequately

informs potential investors about the company. Among other things, management of the

company must prepare financial information of the company according to SEC rules, which

is then audited by the company’s independent registered public accountant.

Foreign companies seeking to list in the US markets need to educate their management and

employees about the accounting and reporting framework regulated by the SEC.

Companies entering the US capital markets must also comply with the Sarbanes- Oxley Act

of 2002. This requires the company’s chief executive officer and chief financial officer each

to provide, when submitting financial information to the SEC, certain certifications regarding

the company’s financial statements and the effectiveness of the company’s disclosure

controls and procedures (Section 302 certifications). In addition, in the company’s second

annual report after it becomes an SEC registrant, the company must provide management’s

assessment as to the effectiveness of the company’s internal controls over financial reporting

(Section 404), and the company’s independent accountants must issue an attestation report on

the company’s internal control over financial reporting.

Accounting and reporting requirements of a US public offering

The registration statement

Form F-1 is the form on which most foreign private issuers file their registration statement

with the SEC, although Form F-3 (known as the ‘short form’) requires less detail and may be

used by foreign private issuers that are already SEC registrants and meet specific

35

requirements. Companies wishing to list without raising capital may use the Form 20-F

registration statement.

Preparing the registration statement

The process of preparing and filing a registration statement is complicated, time consuming

and technical. Furnishing the requisite information and complying with all applicable SEC

rules in an efficient manner requires significant planning and coordination. The company’s

management team, lawyers and accountants will expend a great deal of effort to help the

company meet these requirements.

Financial information

The SEC has specific and sometimes complex rules regarding the content and age of the

financial statements that must be presented in a registration statement and a company’s

independent accountant can be invaluable in helping to interpret these rules.

In a Form F-1 registration statement, a foreign private issuer must generally present audited

financial statements under US GAAP, IFRS or another comprehensive body of accounting

principles. If the basis of financial statement presentation is other than US GAAP or IFRS,

reconciliation from that comprehensive basis of presentation to US GAAP must also be

provided.

In light of the convergence of IFRS and US GAAP, companies contemplating an IPO are

now carefully considering the selection of their primary basis of accounting.

As IFRS and US GAAP continue to converge, a company should consult its accountants on

its choice of an accounting basis on which to prepare the financial statements.

If a non-US company chooses to present its financial statements under US GAAP or is a first-

time IFRS filer, it is required only to present the two most recent financial years’ audited

financial statements (i.e., balance sheet, income statement, statement of cash flows and

statement of changes in shareholders’ equity, together with related footnotes) in its initial

registration statement.

Elimination of US GAAP reconciliation

For financial years ending prior to November 15 2007, all financial statements prepared on a

basis other than US GAAP required reconciliation to US GAAP. In December 2007 the SEC

issued a new rule which eliminated the requirement for this US

36

GAAP reconciliation for foreign private issuers with financial statements prepared in

accordance with IFRS as issued by the International Accounting Standards Board.

The SEC was very specific that in order to qualify for the elimination of the US GAAP

reconciliation, the financial statements must be prepared in accordance with IFRS as issued

by the International Accounting Standards Board and not an equivalent IFRS basis (e.g.,

IFRS as adopted by the European Union would not qualify). As such, financial statements

prepared in accordance with a comprehensive body of accounting principles other than US

GAAP or IFRS as issued by the International Accounting Standards Board will continue be

required to be reconciled to US GAAP.

If a company chooses to present its financial statements according to a comprehensive body

of accounting principles other than US GAAP or IFRS as issued by the International

Accounting Standards Board, the following must be included:

• A balance sheet for the two most recent financial years;

• An income statement (profit and loss account) for the last three years;

• A statement of cash flows for the last three years; and

• A statement of changes in shareholders’ equity for the last three years.

Net income and shareholders’ equity must be quantitatively reconciled to US GAAP for the

last two financial years, and all material US GAAP and Regulation S-X disclosures must be

provided for such years. Such disclosure is required to be provided in the audited footnotes.

The reconciliations need to be detailed - as a rule of thumb, a user of the financial statements

generally should be able to prepare a US GAAP income statement and balance sheet using

the information presented.

If the last audited financial statements included in the registration statement are more than

nine months old, the foreign private issuer must also include consolidated interim financial

statements covering at least the first six months of the current financial year with

comparatives from the same period of the prior year.

37

SEC annual reporting requirements

Once a foreign private issuer has publicly placed securities in the United States, it must file

an annual report on Form 20-F with the SEC no later than six months after each financial

year-end. Such statements will disclose any substantial items of unusual or non-recurrent

nature and will show either net income before and after income taxes or net income and the

amount of income taxes.

In February 2008, in order to enhance the information that is available to investors, the SEC

proposed to shorten the filing deadline from within six months of an issuer's fiscal year-end

to within 90 days of the foreign private issuer’s fiscal year-end. The proposed rule includes a

two-year transition period for fiscal years ending on or after December 15 2010.

In addition, the foreign private issuer must submit some of the other information about the

business required in Form F-1, such as:

• The identity of the directors, senior management and advisors;

• Key information relating to the foreign private issuer’s financial condition, capitalization

and risk factors;

• Information on the company, including its operations, products and services, and plans for

future increases or decreases;

• Information relating to directors, senior management and employees, including

compensation paid to the company’s directors and members of its administrative, supervisory

or management bodies. This may be shown on an aggregate basis if the individual

information is not otherwise publicly available; and

• Major shareholders and related-party transactions.

The Corporation will publish at least once a year and submit to its stockholders at least fifteen

days in advance of the annual meeting and not later than three months after the close of the

last preceding fiscal year of the Corporation:

a balance sheet and a surplus and income statement for such fiscal year of the

Corporation as a separate corporate entity and of each corporation in which it holds,

directly or indirectly, a majority of the equity stock; or in lieu thereof, eliminating all

intercompany transactions

38

a consolidated balance sheet of the Corporation and its subsidiaries as of the end of its

last previous fiscal year and a consolidated surplus statement and a consolidated

income statement of the Corporation and its subsidiaries for such fiscal year.

The Corporation will publish quarterly statements of earnings on the basis of the same degree

of consolidation as in the annual report.

NASDAQ listing requirements

Minimum of 1,250,000 publicly-traded shares upon listing, excluding those held by

officers, directors or any beneficial owners of more then 10% of the company.

The company must have aggregate pre-tax earnings in the prior 3 years of >= $11

million, in the prior 2 years >= $2.2 million, and no one year in the prior 3 years can

have a net loss.

Companies can be removed from the cash flow requirement if the average market

capitalization over the past 12 months is >= $850 million, and revenues over the prior

fiscal year are >=$90 million.

The company must have a minimum aggregate cash flow >= $27.5 million for the

past 3 fiscal years, with no negative cash flow in any of the 3 years. In addition, its

average market capitalization over the prior 12 months must be >= $550 million, and

revenues in the previous fiscal year must be >= $110 million.

An issuer may comply with the annual report requirement either:

by mailing the report to shareholders, or

by posting the annual report to shareholders on or through the company's website.

An issuer that chooses to satisfy this requirement via a website posting must, simultaneous

with this posting, issue a press release stating that its annual report has been filed with the

Commission (or other appropriate regulatory authority).

Interim requirements

NASDAQ requires a non-US issuer to provide in a press release, which also must be

submitted on a Form 6-K, an interim balance sheet and semi-annual income statement, no

later than six months following the end of the issuer’s second fiscal quarter. Under the rule,

the information provided must be translated into English, but does not have to be reconciled