listing in london: guide for cis companies

DESCRIPTION

London Stock Exchange Guide for CIS companies.TRANSCRIPT

Listing in London: CIS Practice

Published by White Page Ltd in association with the London Stock Exchange, with contributions from:

CLYDE&CO

Listing in London: CIS Practice

© 2010 White Page Ltd

Copyright in individual chapters rests with the co-publishers No photo-

copying copyright licences do not apply

his handbook is written as a general guide only t should not be relied

upon as a substitute or speci ic legal, accounting or inancial advice

Pro essional advice should always be sought be ore taking any action

based on the in ormation provided Every e ort has been made to

ensure that the in ormation in this handbook is correct at the time o

publication he views expressed in the articles contained in this hand-

book are those o the authors

London Stock Exchange and the coat o arms device are registered

trademarks o London Stock Exchange plc he publishers and authors

stress that this publication does not purport to provide investment

advice, nor do they bear the responsibility or any errors or omissions

contained herein

Listing in London: CIS Practice

is published by

White Page Ltd, 17 Bolton Street, London W1J 8BH,

United Kingdom

Phone + 44 20 7408 0268

ax + 44 20 7408 0168

Email mail@whitepage co uk

Web www whitepage co uk

irst published 2010

SBN 0-9552069-8-7

Editor: Nigel Page

Design: Rick Marsland

Production: Adrian Preston

Publisher: Nigel Page

Printing and binding: 1010 Printing nternational Ltd

Contents

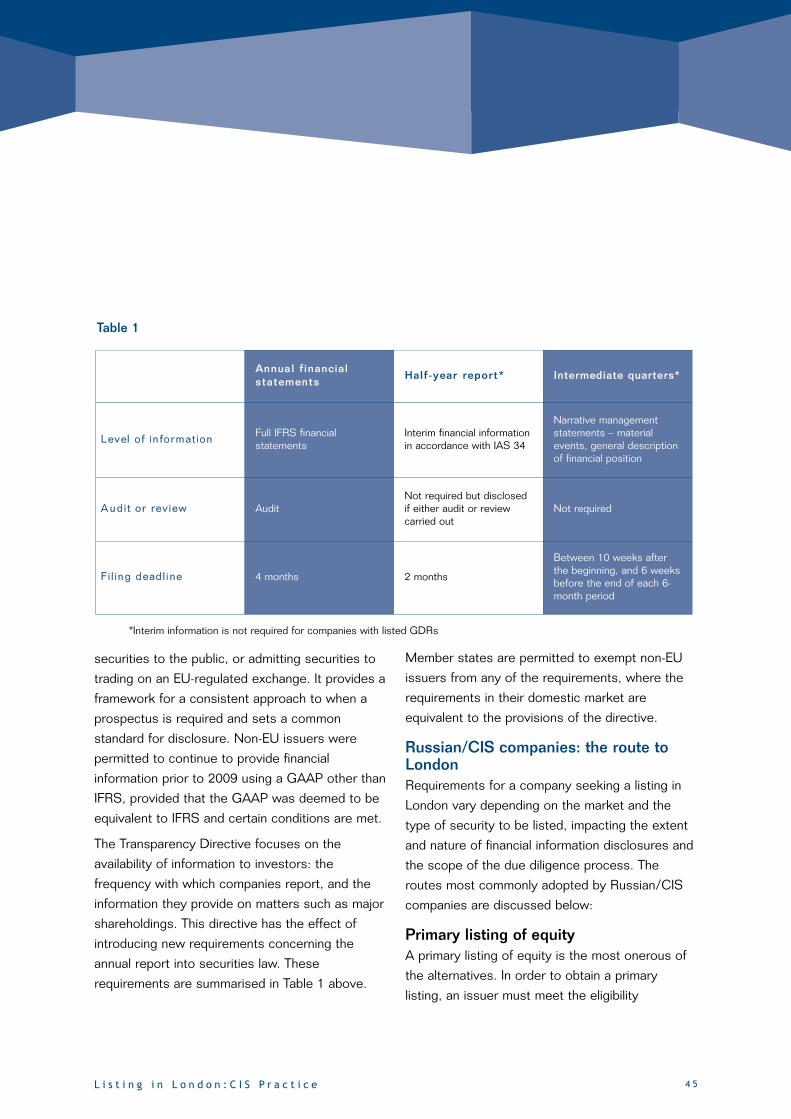

4 Listing in London: CIS Practice The London Stock Exchange

14 Role of the investment bank in a Main Market listing Nomura International plc

34 Role of the law firm in a Main Market listingAshurst

44 Role of the accountant in a Main Market listing PricewaterhouseCoopers LLP

58 Role of the financial PR/IR company in a Main Market listing and AIM flotationCitigate Dewe Rogerson

68 Role of the nominated adviser in an AIM flotationGrant Thornton UK LLP

84 Role of the law firm in an AIM flotationClyde & Co

98 The Professional Securities Market explainedAshurst

Listing in London: CIS Practice

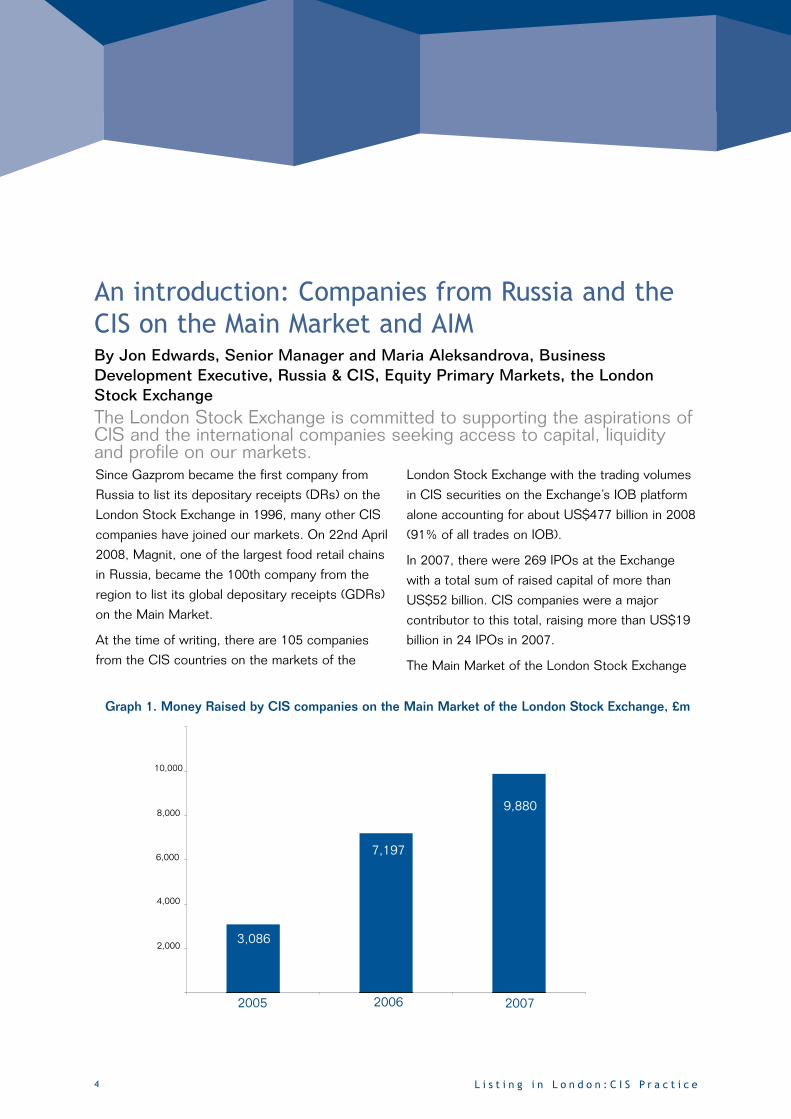

Since Gazprom became the first company from

Russia to list its depositary receipts (DRs) on the

London Stock Exchange in 1996, many other CIS

companies have joined our markets. On 22nd April

2008, Magnit, one of the largest food retail chains

in Russia, became the 100th company from the

region to list its global depositary receipts (GDRs)

on the Main Market.

At the time of writing, there are 105 companies

from the CIS countries on the markets of the

4 L i s t i n g i n L o n d o n : C I S P r a c t i c e

An introduction: Companies from Russia and theCIS on the Main Market and AIMBy Jon Edwards, Senior Manager and Maria Aleksandrova, BusinessDevelopment Executive, Russia & CIS, Equity Primary Markets, the LondonStock ExchangeThe London Stock Exchange is committed to supporting the aspirations ofCIS and the international companies seeking access to capital, liquidityand profile on our markets.

London Stock Exchange with the trading volumes

in CIS securities on the Exchange’s IOB platform

alone accounting for about US$477 billion in 2008

(91% of all trades on IOB).

In 2007, there were 269 IPOs at the Exchange

with a total sum of raised capital of more than

US$52 billion. CIS companies were a major

contributor to this total, raising more than US$19

billion in 24 IPOs in 2007.

The Main Market of the London Stock Exchange

2005 2006 2007

2,000

4,000

6,000

8,000

10,000

3,086

7,197

9,880

Graph 1. Money Raised by CIS companies on the Main Market of the London Stock Exchange, £m

5L i s t i n g i n L o n d o n : C I S P r a c t i c e

is the Exchange’s flagship international market for

established companies across all sectors.

Currently there are 57 companies from Russia and

the CIS on the Main Market of the London Stock

Exchange. Among these companies there are

some which have listed shares (such as

Kazakhmys, ENRC and Ferrexpo), and others

which have listed depositary receipts.

FTSE 100 and primary listingsKazakhmys and ENRC are two companies with

assets in the CIS that are currently in the FTSE

100. Both Kazakhmys and ENRC established PLC

structures and conducted primary listings of their

shares on the London Stock Exchange. Becoming

a constituent of the FTSE UK Index Series helps

to build greater liquidity for Main Market

companies by providing investors with clear and

independent benchmarking of stocks, sectors and

the market as a whole. It also creates the basis

for portfolio trading by both active and passive

investors. Institutional investors offering retail

funds, which explicitly benchmark the FTSE 100,

FTSE 250, FTSE SmallCap and FTSE All-Share

indices, account for almost £50 billion of

investment - over 60% of which are held in tracker

funds that are obliged to purchase exposure to

the constituents of those indices.

IOBMost of the Main Market companies from the CIS

have come to market by listing GDRs under

Chapter 18 of the Listing Rules and admitting

them to trading on the London Stock Exchange’s

International Order Book (IOB). As this market is

intended for professional investors, not all the

provisions applying to their primary listed peers

attach to DR issuers. A comparison checklist of

share and DR listing and continuing obligations

requirements is available in Russian and English

on the London Stock Exchange’s corporate

website.

2530

36

4964

50

80

51207

83375

63

477

46

49% 42%56%

61%

71%

86%

91%

100

200

300

400

500

600

Total IOB Trading Value ($b

n)

CIS Trading Value ($bn)Other countries IOB Trading Value ($bn)

Graph 2: IOB: Seven years of growth

2002 2003 2004 2005 2006 2007 2008

The IOB, originally conceived along the lines of the

SETS platform for UK securities, has developed

into one of the most liquid trading platforms for

international securities in the world. CIS securities

on the IOB have been among the most actively

traded and accounted for over 91% of dollar

volume traded in 2008 on the IOB (US$477

billion).

One of the key drivers behind the liquidity of

Russian and other CIS GDRs on the IOB is the

active participation of the 10 London Stock

Exchange member brokers whose parent

organisations were founded in Russia. Together

these brokers (listed below) accounted for US$57

billion in trades in 2008:

• Alfa Capital Holdings (Cyprus) Ltd

• AS KIT Finance Europe

• Metropol (UK) Ltd

• Otkritie Securities Ltd

• Renaissance Capital Ltd

• Troika Dialog (UK) Ltd

• Unicredit Aton International Ltd

• URALSIB Securities Ltd

• VTB Bank Europe Ltd

• Broker Credit Service.

EDX In December 2006, the London Stock Exchange’s

EDX group launched its Russian derivatives

service. Since launch, there has been

£40,613,522,060 (US$50 billion) in notional value

6 L i s t i n g i n L o n d o n : C I S P r a c t i c e

traded on EDX Russian derivatives. Futures and

options contracts on GDRs of Gazprom, Lukoil

and Rosneft are among the most liquid of the EDX

Russian derivatives. The EDX Russian derivatives

service is another example of the services the

London Stock Exchange has developed to

promote a liquid market in GDR trading.

Table 1. Top five most active contracts based onnotional value

No Company Notional value (in US$)

1 Gazprom 28,210,533,173

2 Lukoil 11,427,455,460

3 Rosneft 7,660,582,353

4 Norilsk Nickel 4,865,117,066

5 Surgutneftegaz 2,398,028,737

CCP IOBOne of the most important developments on the

IOB is the introduction of the Central

Counterparty Clearing (CCP) service for the

International Order Book (IOB). This service was

launched at the end of the first quarter 2009.

Recent market events have highlighted the value

of central clearing services in helping to mitigate

counterparty risk, increase market efficiency and

in turn provide participants with a greater level of

confidence in their transactions. The introduction

of a CCP model, initially to the 50 most liquid

securities by value that trade on the IOB, will

deliver appreciable benefits to both issuers and

7L i s t i n g i n L o n d o n : C I S P r a c t i c e

investors. Market participants will gain full

counterparty risk protection, enjoy post-trade

anonymity and experience improvements in

straight-through processing. Firms will also have

access to an optional netting facility to reduce

transaction management costs and financial

exposure at the settlement level.

AIMSmall and mid-cap companies from the CIS have

also found a home on AIM, the London Stock

Exchange’s growth market, where there are

currently 48 companies with assets and

operations across the CIS (see

www.londonstockexchange.com/rus). The CIS

companies quoted on AIM have come to market

to access the deep pool of funds available for

fast-growth companies, from a variety of different

sectors. Companies from the CIS region have

been able to raise considerable amounts of

growth capital at IPO (£1.7 billion cumulatively)

and in further financing rounds (£2.1 billion

cumulatively). It is the ability to raise further capital

for growth companies to continue to develop their

businesses that really sets AIM apart from other

growth markets. Businesses from all over the

world are attracted to AIM because it enables

them to raise relatively small amounts of capital,

from knowledgeable, predominantly institutional

investors.

AIM – investing in a diversified base ofcompaniesInvestors who buy shares in companies quoted on

AIM are participating in the world's leading stock

market for smaller growing companies. AIM

companies come from 26 different countries and

range across 39 industry sectors and 90 sub-

sectors, providing all types of investors with a

vast range of choice in investing in businesses to

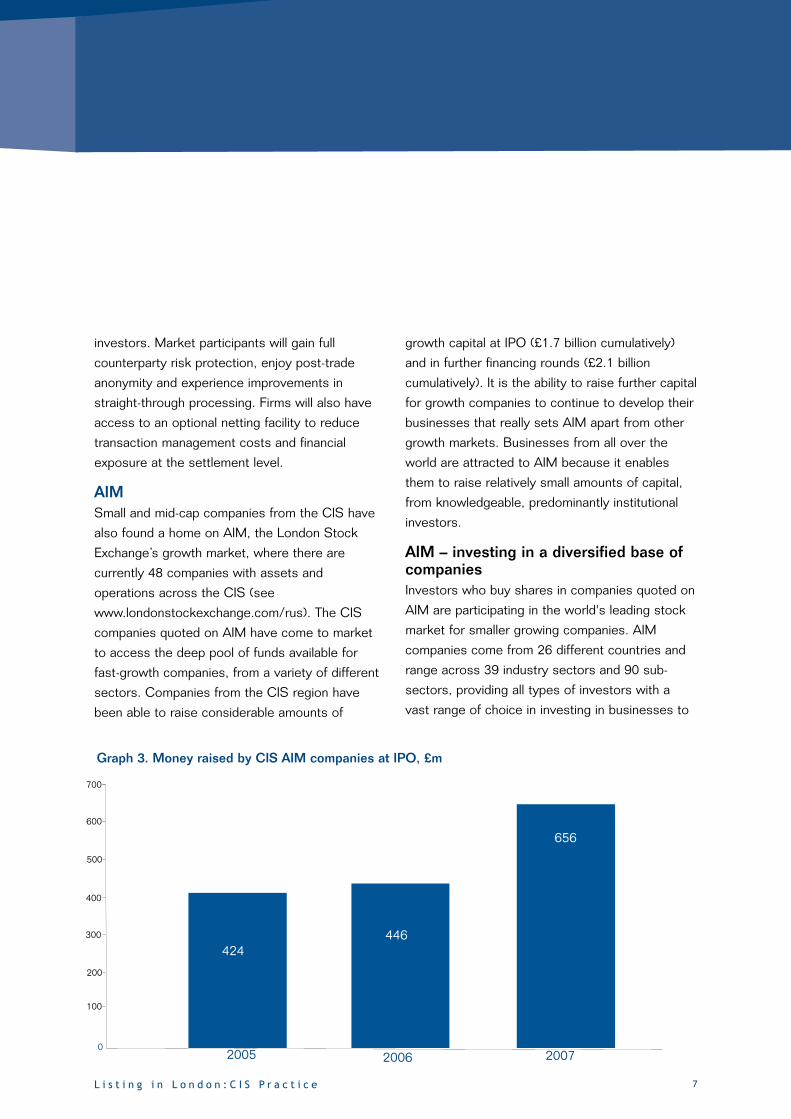

2005 2006 2007

424446

Graph 3. Money raised by CIS AIM companies at IPO, £m

656

0

700

100

200

300

400

500

600

suit their investment profile. In 2006 and 2007,

AIM companies raised a combined £31 billion from

investors (see Table 2), many of whom were large

institutional fund managers such as BlackRock,

Invesco, Fidelity International, Prudential Group,

AVIVA, Artemis Investment Management and QVT

Financial.

Investors also benefit from the FTSE AIM Index

Series. This series – part of FTSE’s global range

8 L i s t i n g i n L o n d o n : C I S P r a c t i c e

of world-class market indices – provides investors

with greater transparency, and helps them identify

AIM companies based on their inclusion in the

FTSE AIM Index Series or the FTSE AIM All-Share

Supersector Indices.

The diversity of AIM’s constituents, demonstrated

by the 39 sectors represented, is supported by

the in-depth and broad experience of the UK’s

financial advisory community who really

2005 2006 2007

118

646

Graph 4: Further money raised by CIS companies, £m

542

Year IPOs (£m) Further issues (£m) Total money raised (£m)

2003 1,095 1,000 2,095

2004 2,776 1,880 4,656

2005 6,461 2,481 8,942

2006 9,944 5,734 15,678

2007 6,581 9,603 16,206

2008 1,108 3,204 4,312

Total 27,965 23,902 51,890

* Data for the above table is taken from the statistics section of the Exchange’s website.

Table 2: Total investment made- 2003 -2008

0

700

100

200

300

400

500

600

9L i s t i n g i n L o n d o n : C I S P r a c t i c e

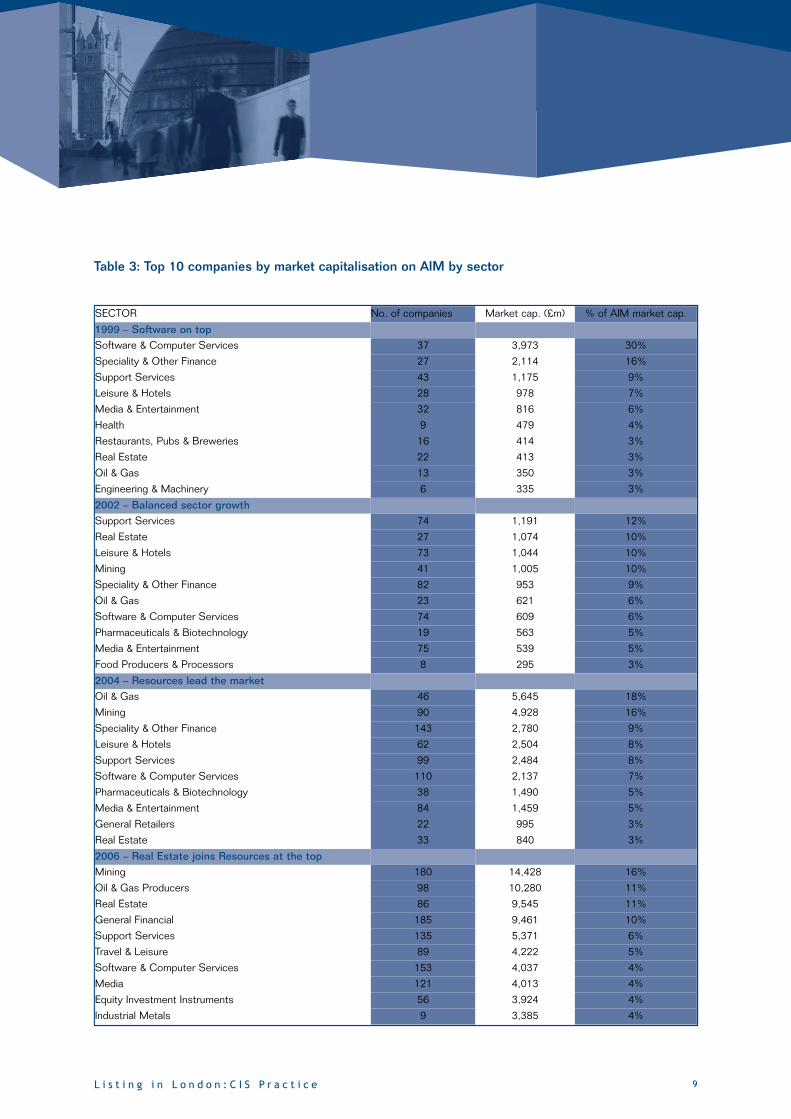

SECTOR No. of companies Market cap. (£m) % of AIM market cap.

1999 – Software on topSoftware & Computer Services 37 3,973 30%

Speciality & Other Finance 27 2,114 16%

Support Services 43 1,175 9%

Leisure & Hotels 28 978 7%

Media & Entertainment 32 816 6%

Health 9 479 4%

Restaurants, Pubs & Breweries 16 414 3%

Real Estate 22 413 3%

Oil & Gas 13 350 3%

Engineering & Machinery 6 335 3%

2002 – Balanced sector growthSupport Services 74 1,191 12%

Real Estate 27 1,074 10%

Leisure & Hotels 73 1,044 10%

Mining 41 1,005 10%

Speciality & Other Finance 82 953 9%

Oil & Gas 23 621 6%

Software & Computer Services 74 609 6%

Pharmaceuticals & Biotechnology 19 563 5%

Media & Entertainment 75 539 5%

Food Producers & Processors 8 295 3%

2004 – Resources lead the marketOil & Gas 46 5,645 18%

Mining 90 4,928 16%

Speciality & Other Finance 143 2,780 9%

Leisure & Hotels 62 2,504 8%

Support Services 99 2,484 8%

Software & Computer Services 110 2,137 7%

Pharmaceuticals & Biotechnology 38 1,490 5%

Media & Entertainment 84 1,459 5%

General Retailers 22 995 3%

Real Estate 33 840 3%

2006 – Real Estate joins Resources at the topMining 180 14,428 16%

Oil & Gas Producers 98 10,280 11%

Real Estate 86 9,545 11%

General Financial 185 9,461 10%

Support Services 135 5,371 6%

Travel & Leisure 89 4,222 5%

Software & Computer Services 153 4,037 4%

Media 121 4,013 4%

Equity Investment Instruments 56 3,924 4%

Industrial Metals 9 3,385 4%

Table 3: Top 10 companies by market capitalisation on AIM by sector

understand the needs of smaller growth

companies. AIM is supported by a wide

community of expert advisers, ranging from

Nominated Advisers (Nomads) and brokers to

accountants, lawyers and PR/IR firms.

The sectoral diversity on AIM remains one of the

market’s core strengths and has helped AIM avoid

reliance on one particular industry, even when

another sector goes through a relative period of

slow growth. In Table 3, several distinct periods

are highlighted to show how AIM has developed

over the years, where certain sectors experienced

a significant increase in investor interest. With the

exception of 1999 during the ‘dot.com’ boom, no

one sector has accounted for more than 20% of

AIM’s total market capitalisation. Since 2004,

sectors such as natural resources, financial

services and real estate have all experienced peak

periods of growth while leaving the market

relatively balanced and diverse. Owing to the large

number of advisers and sector specialists working

with the AIM market, AIM has always been able to

serve as a platform to attract companies from new

sectors and new investment opportunities.

AIM introductionsWhile, on average, CIS companies have raised

£35 million at IPO, several have come to market

raising small amounts of capital. Teleset, the

telecommunications operator from Tartarstan,

admitted its shares to AIM without raising initial

capital. Once on market, it then raised US$14.987

million, the major investors being Templeton Asset

Management Limited, the Black Sea Trade

1 0 L i s t i n g i n L o n d o n : C I S P r a c t i c e

Development Bank and Deutsche Bank. A further

US$9.8 million was raised the following year in a

pro rata offer to existing shareholders. Companies

such as Teleset, which have chosen to undertake

an introduction of shares to market, are looking to

gain access to a platform where they will trade

alongside peer companies of a similar size and

profile. Once on AIM, these companies have an

opportunity to demonstrate their strengths and

position themselves for future fund-raisings by

ensuring that they adhere to disclosure best

practices.

AIM regulation & the role of NomadsEach company applying to AIM must appoint a

Nomad to guide it through the admission process

and its subsequent life as a publicly-quoted

company. Firms that wish to seek approval to act

as Nomads must satisfy strict criteria set by the

London Stock Exchange. To be granted

authorisation they must demonstrate that they

have the relevant experience to assess whether a

company is appropriate to be admitted to AIM and

that they can support the company once admitted

to the market. By ensuring that AIM companies

are properly regulated, investors benefit from

increased certainty and security. Over the last five

years, the number of AIM Nomads working with

international companies has grown significantly.

Their continued work with the companies that they

act for has helped to raise the level of

understanding in the UK of the risks and

opportunities in overseas markets.

The unique solid principles-based regulatory

1 1L i s t i n g i n L o n d o n : C I S P r a c t i c e

system, combined with the Exchange’s robust and

sophisticated trading platforms, provides both

private and institutional investors with the

confidence that AIM is a secure market that

enables them to participate in these companies’

success and support the companies of tomorrow.

Funds on AIM and SFMHedge funds and private equity are an increasingly

important asset class to which pension funds and

other institutional investors want access, in order

to diversify their overall portfolios and improve

their returns. Through both the Main Market and

AIM, the London Stock Exchange was already

offering investors and issuers a choice of routes

to market, according to the types of investors that

issuers wish to target and the risk premiums

sought by investors. All of the real estate and

development companies listed in Table 4 are

examples of fund structures that are quoted on

AIM.

In 2007, the London Stock Exchange further

enhanced the range of available options,

introducing the Specialist Fund Market (SFM), a

separate, clearly-labelled market for alternative

assets such as single-strategy hedge funds and

private equity vehicles. It enables the London

markets to continue to meet what is a strong

demand among issuers and investors for a

regulated market quotation suitable for these

more complex entities, while remaining clearly

delineated as a professional market.

The Specialist Fund Market is open to both UK

and international funds, and will be complementary

to the FSA’s Unitary Regime for investment

entities listing on the Main Market. Issuers that

wish to market funds to a wider audience,

including retail investors, will continue to have

access to the Main Market, which offers the

potential for inclusion in index tracker funds in

addition to AIM, and has been very successful in

attracting investment entities, primarily property

funds or other conventional investment funds.

The Specialist Fund Market is a Regulated Market

operated in accordance with EU Directives. The

FSA will approve issuers’ prospectuses in line

with the Prospectus Directive and monitor issuers’

conformity on an ongoing basis with the

Transparency Directive, Market Abuse Directive

Company – Real Estate Money raised (in £m)

Aisi Realty Public Ltd 16

Dragon – Ukrainian Properties 103

KDD Group NV 64

Mirland Development Corporation 143

RGI International Ltd 89

Raven Russia Ltd 153

XXI Century Investments 68

Table 4: Real Estate sector review

and other EU requirements. Once approved by the

UKLA, securities must also meet the Exchange’s

Admission and Disclosure Standards in order to

be admitted to trading on dedicated segments of

the Exchange’s next-generation trading services,

1 2 L i s t i n g i n L o n d o n : C I S P r a c t i c e

Opportunities for CIS companies in London

The London Stock Exchange is committed to supporting the aspirations of the CIS and international

companies seeking access to capital, liquidity and profile on our markets. The significant amounts

raised by CIS companies via IPO and the large volumes traded on IOB are testament to the

confidence investors and advisors have in our markets and the companies profiled there. The highly

successful IPOs of Russian companies in 2006-2007 have helped to attract a critical mass of the

best analysts and investors knowledgeable about the region. In this publication you will have an

opportunity to hear from many of these advisors about the role they play in bringing CIS companies

to London.

English and Russian language information available here:

www.russianipo.com

Please contact the CIS team if you are interested in learning more about this initiative

Jon EdwardsSenior Manager - Russia & CIS Equity Primary Markets London Stock Exchange Direct: +44 (0) 20 7797 1599 Fax: +44 (0) 20 7920 4788 [email protected]

Maria AleksandrovaBusiness Development Executive - Russia & CIS Equity Primary Markets London Stock Exchange Direct: +44 (0) 20 7797 1444 Fax: +44 (0) 20 7959 [email protected]

SETS and SETSqx. Specialist Fund Market

securities will not be included in the FTSE UK

Index Series and will therefore not be included in

index tracker funds.

Copyright © February 2009. London Stock Exchange and the coat of arms device are registered trade marks of London Stock Exchange plc. IOB is a trade mark of London Stock Exchange plc.

International Order BookThe International Order Book (IOB) enables investors to unlock the potential of some of the world’s fastest growing markets.

The service offers easy, cost efficient and direct access to developing markets around the world such as Central and Eastern Europe, Asia, Middle East and Africa via depositary receipts.

More than 270 securities from 46 countries are trading on the service, supported by the quality of our primary markets and global reputation of leading depositary banks.

The IOB benefits from a central counterparty service, providing participants with increased market efficiency and a greater level of confidence in their transactions.

To find out about listing in London or trading on the London Stock Exchange, please visit

www.londonstockexchange.com

There are many reasons for a company to list its

securities on a stock exchange, but the most

common reason to go public is to raise equity

capital. Other objectives may include gaining

access to a highly liquid market and broadening a

company’s investor base. Equity financing is not

only an immediate reinforcement of the capital

base, but also a means of improving the

company’s profile and transparency, as well as

offering an opportunity to raise cheaper debt in

the future as a publicly-listed company. A listing

can also lead to commercial benefits, such as

sales increases in a specific region through added

brand recognition.

Most companies combine a listing on the London

Stock Exchange (the Exchange) with an equity

offering, which can be undertaken by issuing new

shares, selling existing shares or a combination of

both. This process is referred to as an Initial

Public Offering (IPO).

This article will focus on listing on the Main

Market of the Exchange, in the context of Russian

corporates, and on offerings of Global Depositary

Receipts (GDRs).

1 4 L i s t i n g i n L o n d o n : C I S P r a c t i c e

Role of the investment bank in a Main Market listingMichael Boardman, Myles Evanson and Victor Kuzmenko, Nomura International plc

The investment bank plays a crucial role in listing Russian and CIScompanies on the London Stock Exchange

Key considerations

Benefits of a listing on the LondonStock ExchangeLondon remains the international stock exchange

of choice for foreign companies, reflecting

London’s leading position as an international

financial centre. A significant number of Russian

companies have already chosen to list in London

and, with Russia becoming an increasingly

important source of equity capital market

transactions (37 Russian companies have sought

listings on international stock exchanges since

early 2002), more are expected to do so during

2010/2011 (Source: Dealogic).

The Exchange offers a number of benefits for

companies that complete a listing:

• Flexibility in the choice of securities to be listed:

The Exchange provides listing and trading

platforms for all types of shares, depositary

receipts (DRs), or equity-linked securities

• Access to a vast pool of international capital:

The Exchange offers companies the opportunity

to enlarge their existing investor base and gain

access to capital from the international financial

community

1 5L i s t i n g i n L o n d o n : C I S P r a c t i c e

• Enhancement of the company’s profile: listing

on the Exchange encourages broader

recognition of the company, both domestically

and internationally

• Broad analyst coverage: listing on the Exchange

provides access to comprehensive research

coverage by different country and sector

analysts; this plays a vital role in securing

recognition from the international investor

community

• Sector knowledge and depth: an Exchange

listing provides access to investors with in-

depth knowledge of companies and sectors. The

Exchange itself hosts a broader range of

sectors than any other exchange and contains

an extensive depth of peers

• Potentially higher valuation of the company: as

a recognised platform for the international

investor community, an Exchange listing offers

improved valuation potential. Because the

Exchange also offers Russian corporates the

greatest number of peers, this makes the

investors’ task of looking at a new opportunities

easier and provides a wider range of peers to

benchmark against

• Listed securities: listing on the Exchange

creates a liquid currency for future acquisitions,

management remuneration, etc

• Investor confidence: an Exchange listing helps

generate investor confidence via disclosure

requirements

• Flexible approach to regulation and direct

access to regulatory authority: the Exchange’s

regulatory standards are high, but also flexible,

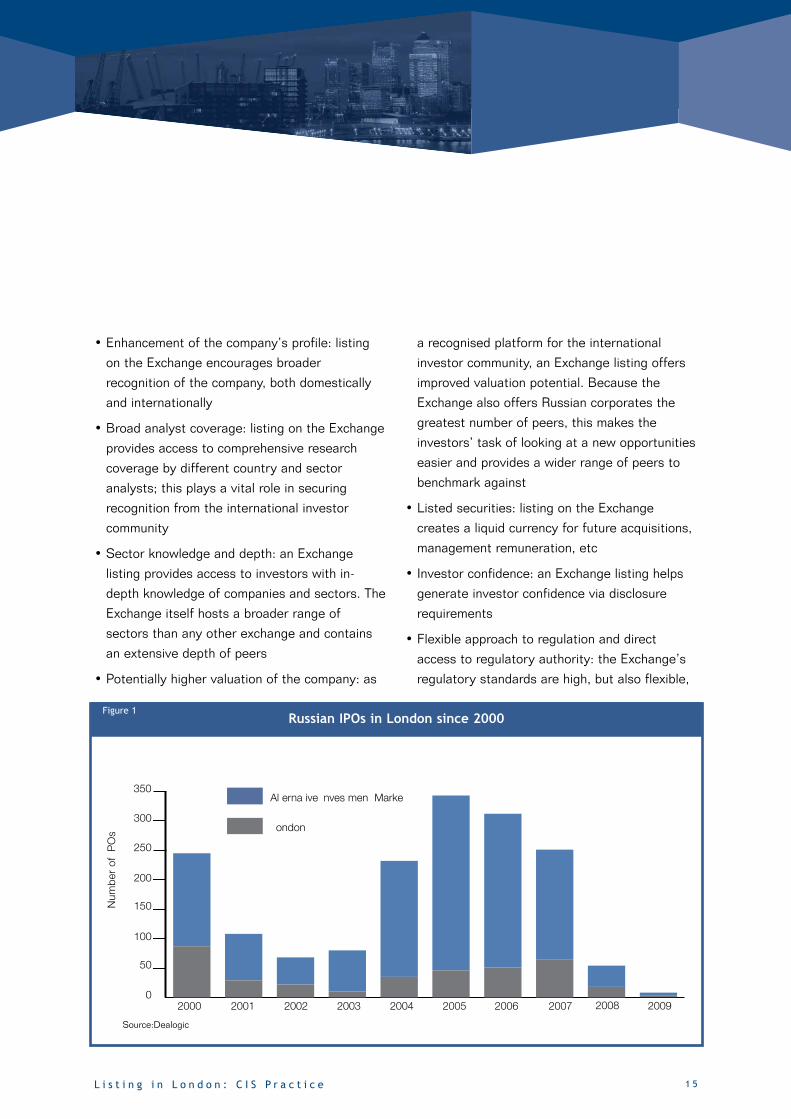

Russian IPOs in London since 2000Figure 1

300

50

100

150

200

250

02000 2001 2002 2003 2004 2005 2006 2007

Al erna ive nves men Marke

ondon

Num

ber

of

PO

s

350

2008 2009

Source:Dealogic

with rules that can be applied on a case-by-case

basis

• Reasonable costs and fees: fees and costs for

the Exchange’s services are competitive in

comparison with other stock exchanges.

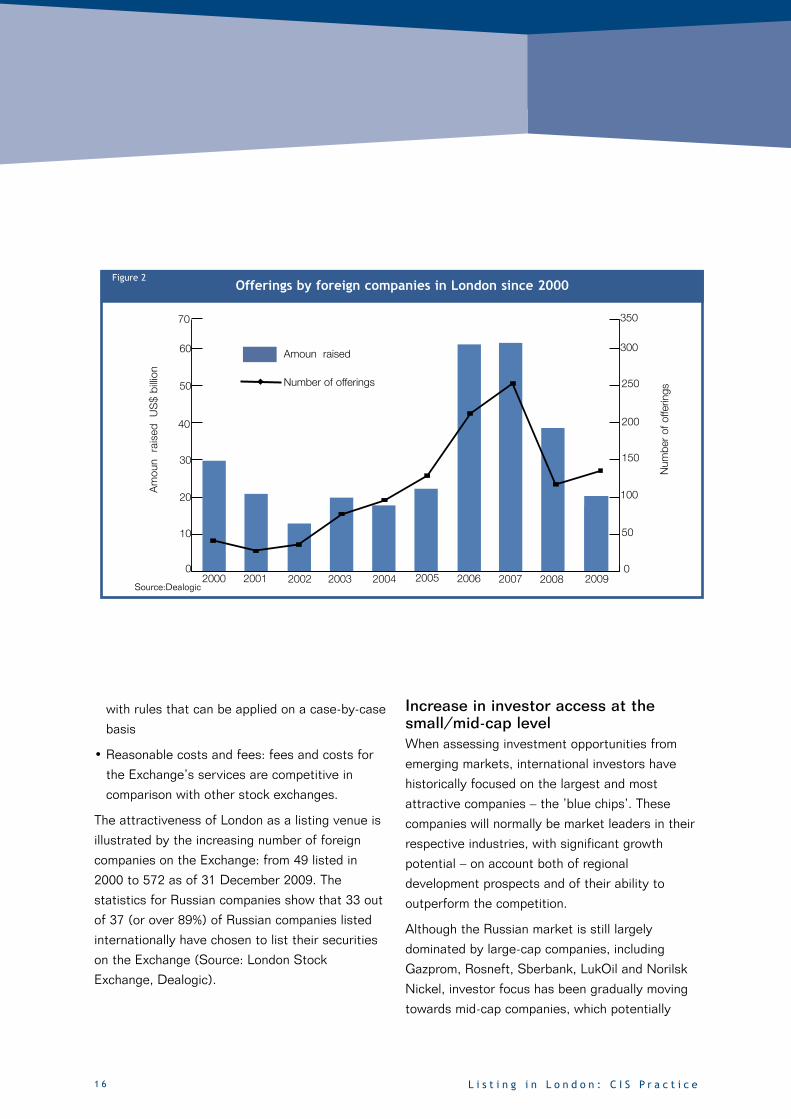

The attractiveness of London as a listing venue is

illustrated by the increasing number of foreign

companies on the Exchange: from 49 listed in

2000 to 572 as of 31 December 2009. The

statistics for Russian companies show that 33 out

of 37 (or over 89%) of Russian companies listed

internationally have chosen to list their securities

on the Exchange (Source: London Stock

Exchange, Dealogic).

1 6 L i s t i n g i n L o n d o n : C I S P r a c t i c e

Increase in investor access at thesmall/mid-cap levelWhen assessing investment opportunities from

emerging markets, international investors have

historically focused on the largest and most

attractive companies – the ’blue chips’. These

companies will normally be market leaders in their

respective industries, with significant growth

potential – on account both of regional

development prospects and of their ability to

outperform the competition.

Although the Russian market is still largely

dominated by large-cap companies, including

Gazprom, Rosneft, Sberbank, LukOil and Norilsk

Nickel, investor focus has been gradually moving

towards mid-cap companies, which potentially

Source:Dealogic

Offerings by foreign companies in London since 2000Figure 2

60

10

20

30

40

50

02000 2001 2002 2003 2004 2005 2006 2007 2009

Amoun raised

Number of offerings

Am

oun

rais

ed

US

$ b

illio

n

70

300

50

100

150

200

250

0

Num

ber

of

offe

rings

350

2008

1 7L i s t i n g i n L o n d o n : C I S P r a c t i c e

offer higher returns and stronger growth potential.

Thus, since 2000, there have been 19 mid-cap

Russian companies which have listed in London.

Listing considerations

Listing typesThe listing regime in London has recently been

amended, and the new regime is effective from

April 2010.

Under the new regime, there are two choices of

listing - a "Premium" listing and a "Standard" listing

(which replaces the old "primary" and "secondary"

listings, respectively). Both options are available

to UK and non-UK corporates.

1 Premium listing

Premium listing is available for listing equity (NB:

but not GDRs) and requires compliance with the

super-equivalent regime ie more than the basic

requirements set out by the EU Prospectus

Directive. Examples of additional higher standards

are corporate governance, share dealing and pre-

emption rules (to provide anti-dilution protection),

three year track record and 12 month working

capital statement. The key benefit is that once

the issuer is Premium listed, it will qualify for the

inclusion in the FTSE family of indices.

2 Standard listing

The standard listing requires compliance with EU

Prospectus Directive minimum standards only and

not the additional UK super-equivalent points

required for a Premium listing. So it would have to

comply with Transparency and Disclosure Rules

only, making it less demanding to list on the

Standard platform, but there would be no

qualification for FTSE indices. Russian issuers

listing GDRs on the Exchange are only eligible to

have a Standard listing.

The UKLA is responsible for the vetting and

admission of companies to trading on the

Exchange, and maintains the Official List. The

majority of Russian incorporated companies listing

in London opt for a Standard (previously

secondary) listing of GDRs. (See Figure 1 above

'Russian IPOs in London since 2000' for further

details).

International vs domestic offeringBefore considering listing possibilities on the

Exchange, the company, its shareholders and

management need to be aware of the

requirements placed on Russian corporates by

Russian law.

The regulatory body for Russian corporates is the

Federal Financial Markets Service (FFMS). FFMS

places a number of limitations on a company’s

ability to offer its shares to foreign investors.

According to the new FFMS order registered with

the Russian Ministry of Justice on 6 October

2009 and expected to enter into force on 1

January 2010, the maximum amount of shares or

other securities that Russian issuers can place on

foreign markets will be determined, inter alia, by

the listing level of a Russian company on Russian

stock exchange(s) (MICEX and/or RTS). The

maximum limit is set at 25% for companies in

listing category “A” (ie the largest and most liquid

stocks). In addition, the new order specifies that

the maximum percentage of shares that can be

offered abroad by a company or its shareholders

in an equity offering is 50%.

If the company is not incorporated in Russia, it

will not be bound by Russian corporate legislation

and it can seek a sole international listing without

being required to offer the company’s securities

to domestic Russian investors.

Securities to be listedThe Exchange is the largest stock exchange

globally by number of listed companies with 2,792

listed corporates (including those quoted on AIM)

as of the end of December 2009 (Source: the

London Stock Exchange). The cumulative market

capitalisation of these companies was over

US$5.8 trillion as of December 2009 (Source:

London Stock Exchange).

Both shares and DRs can be listed on the

1 8 L i s t i n g i n L o n d o n : C I S P r a c t i c e

√ Investor familiarity with the product

√ No foreign investment restrictions

√ Enhanced liquidity

√ Ease of trading and settlement

√ Dividends paid in freely convertible currency

√ Easier access to corporate information

√ Flexible GDR nominal value

√ Simple listing requirements

√ No costs involved

√ Wide investor participation

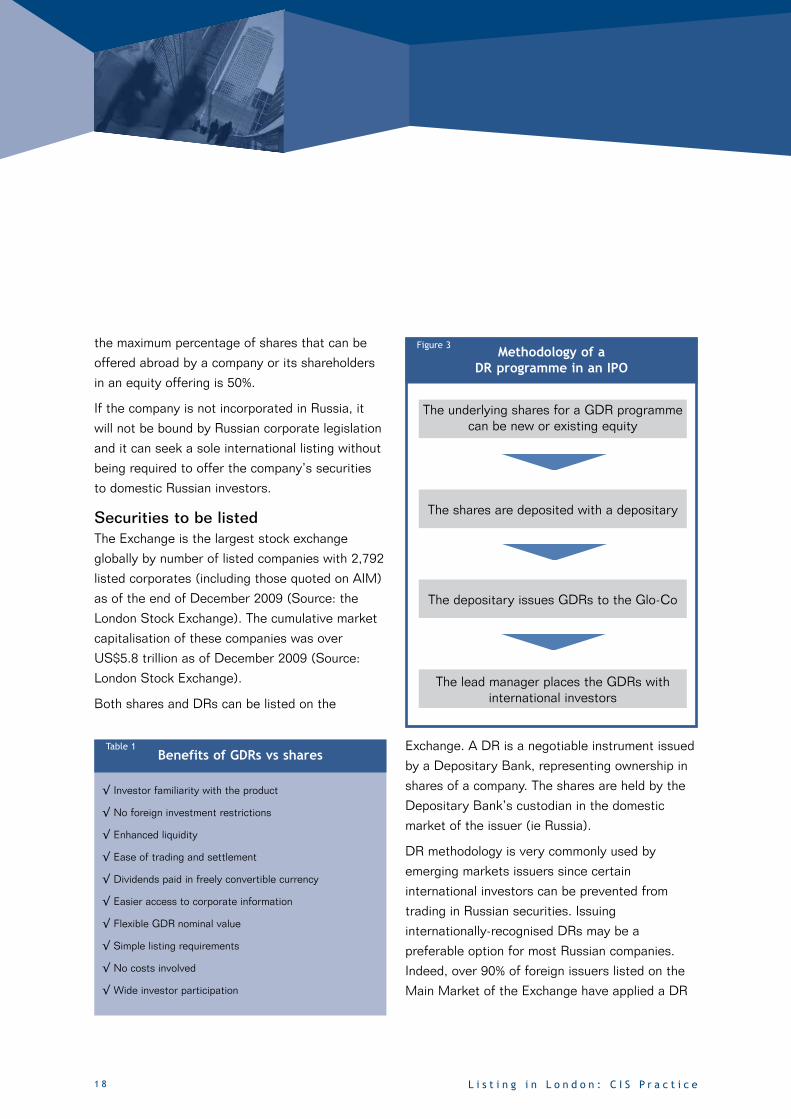

Benefits of GDRs vs sharesTable 1 Exchange. A DR is a negotiable instrument issued

by a Depositary Bank, representing ownership in

shares of a company. The shares are held by the

Depositary Bank’s custodian in the domestic

market of the issuer (ie Russia).

DR methodology is very commonly used by

emerging markets issuers since certain

international investors can be prevented from

trading in Russian securities. Issuing

internationally-recognised DRs may be a

preferable option for most Russian companies.

Indeed, over 90% of foreign issuers listed on the

Main Market of the Exchange have applied a DR

Methodology of a

DR programme in an IPO

Figure 3

The underlying shares for a GDR programmecan be new or existing equity

The lead manager places the GDRs withinternational investors

The depositary issues GDRs to the Glo-Co

The shares are deposited with a depositary

1 9L i s t i n g i n L o n d o n : C I S P r a c t i c e

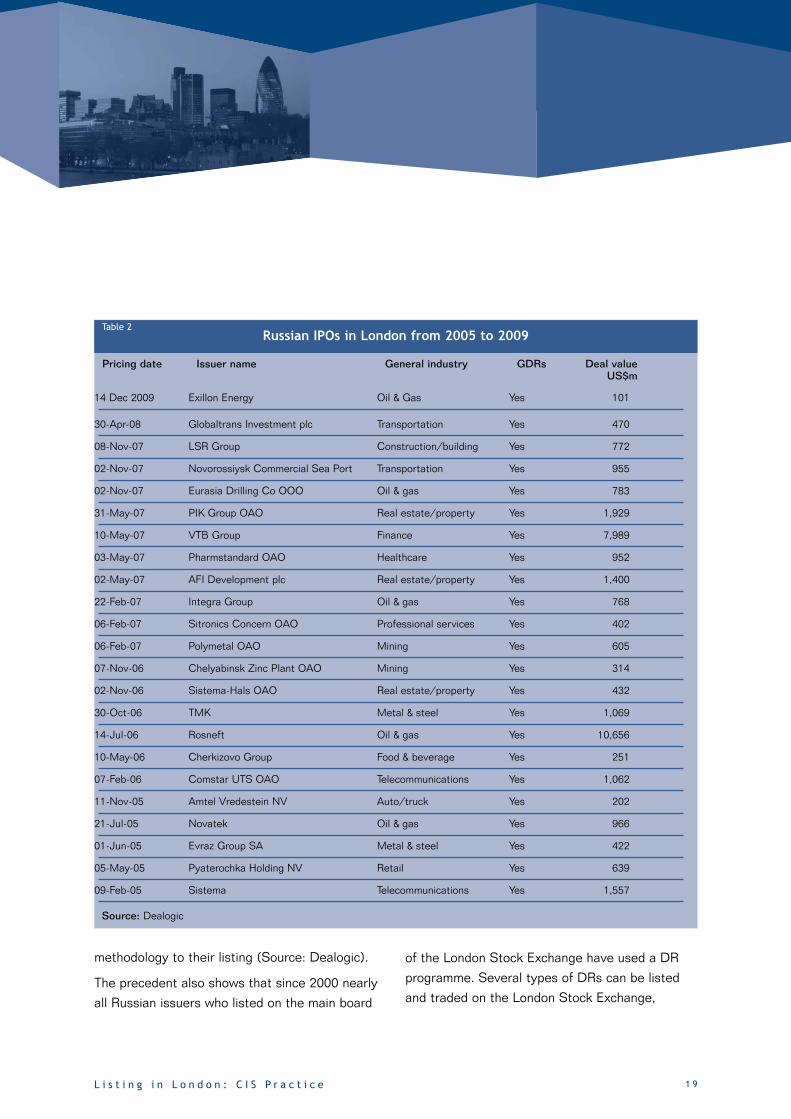

methodology to their listing (Source: Dealogic).

The precedent also shows that since 2000 nearly

all Russian issuers who listed on the main board

of the London Stock Exchange have used a DR

programme. Several types of DRs can be listed

and traded on the London Stock Exchange,

14 Dec 2009 Exillon Energy Oil & Gas Yes 101

30-Apr-08 Globaltrans Investment plc Transportation Yes 470

08-Nov-07 LSR Group Construction/building Yes 772

02-Nov-07 Novorossiysk Commercial Sea Port Transportation Yes 955

02-Nov-07 Eurasia Drilling Co OOO Oil & gas Yes 783

31-May-07 PIK Group OAO Real estate/property Yes 1,929

10-May-07 VTB Group Finance Yes 7,989

03-May-07 Pharmstandard OAO Healthcare Yes 952

02-May-07 AFI Development plc Real estate/property Yes 1,400

22-Feb-07 Integra Group Oil & gas Yes 768

06-Feb-07 Sitronics Concern OAO Professional services Yes 402

06-Feb-07 Polymetal OAO Mining Yes 605

07-Nov-06 Chelyabinsk Zinc Plant OAO Mining Yes 314

02-Nov-06 Sistema-Hals OAO Real estate/property Yes 432

30-Oct-06 TMK Metal & steel Yes 1,069

14-Jul-06 Rosneft Oil & gas Yes 10,656

10-May-06 Cherkizovo Group Food & beverage Yes 251

07-Feb-06 Comstar UTS OAO Telecommunications Yes 1,062

11-Nov-05 Amtel Vredestein NV Auto/truck Yes 202

21-Jul-05 Novatek Oil & gas Yes 966

01-Jun-05 Evraz Group SA Metal & steel Yes 422

05-May-05 Pyaterochka Holding NV Retail Yes 639

09-Feb-05 Sistema Telecommunications Yes 1,557

Russian IPOs in London from 2005 to 2009Table 2

Pricing date Issuer name General industry GDRs Deal valueUS$m

Source: Dealogic

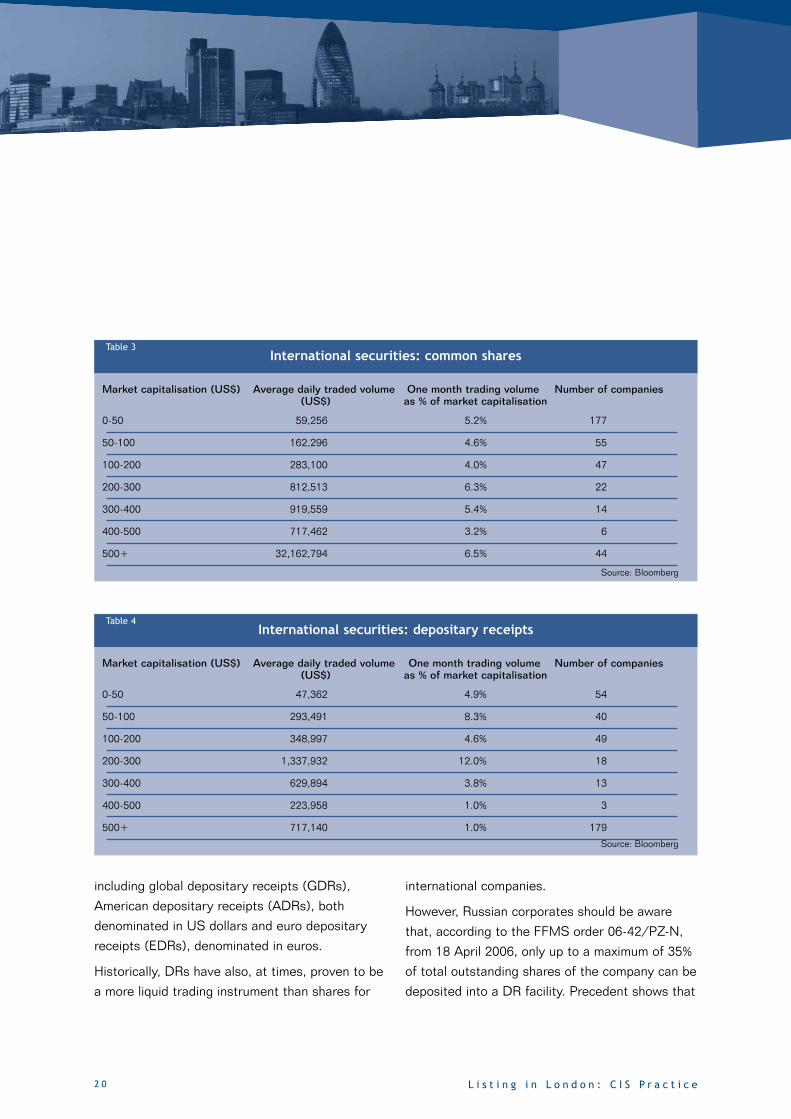

including global depositary receipts (GDRs),

American depositary receipts (ADRs), both

denominated in US dollars and euro depositary

receipts (EDRs), denominated in euros.

Historically, DRs have also, at times, proven to be

a more liquid trading instrument than shares for

2 0 L i s t i n g i n L o n d o n : C I S P r a c t i c e

international companies.

However, Russian corporates should be aware

that, according to the FFMS order 06-42/PZ-N,

from 18 April 2006, only up to a maximum of 35%

of total outstanding shares of the company can be

deposited into a DR facility. Precedent shows that

0-50 59,256 5.2% 177

50-100 162,296 4.6% 55

100-200 283,100 4.0% 47

200-300 812,513 6.3% 22

300-400 919,559 5.4% 14

400-500 717,462 3.2% 6

500+ 32,162,794 6.5% 44

International securities: common sharesTable 3

Market capitalisation (US$) Average daily traded volume One month trading volume Number of companies(US$) as % of market capitalisation

0-50 47,362 4.9% 54

50-100 293,491 8.3% 40

100-200 348,997 4.6% 49

200-300 1,337,932 12.0% 18

300-400 629,894 3.8% 13

400-500 223,958 1.0% 3

500+ 717,140 1.0% 179

International securities: depositary receiptsTable 4

Market capitalisation (US$) Average daily traded volume One month trading volume Number of companies(US$) as % of market capitalisation

Source: Bloomberg

Source: Bloomberg

2 1L i s t i n g i n L o n d o n : C I S P r a c t i c e

most Russian corporates do not utilise the full

threshold.

In addition to this, in May 2008 the Russian

government passed a law which will limit the level

of foreign ownership in 42 industries, which have

been classified as ‘strategic’. For example military,

space technology, nuclear technology, metals and

mining, oil and gas, energy fall into this strategic

category. Foreign investors will need a

government approval before acquiring a majority

(ie over 50%) interest in companies from these

sectors. In certain sectors, including natural

resources companies exploiting subsoil plots of

federal significance, the threshold has been set as

low as 10%. This law will ultimately have impact

on the size of DR programmes of issuers

operating in these sectors.

Listing venueAs mentioned previously, there are two segments

of the London Stock Exchange where Russian

corporates can list:

• Main board of the Exchange; and

• Alternative Investment Market (AIM).

While the main board is an established

international listing venue for large companies,

AIM attracts corporates by offering a more

streamlined, flexible and cost-efficient process for

smaller, high-growth and other younger

companies. Thus, an average market cap for

companies listed on the main board is US$3.9

billion, compared to US$70 million for AIM

(Source: the London Stock Exchange).

Although technically possible, AIM strongly

discourages foreign companies from listing DRs

on AIM due to the insufficient regulatory

framework around this product on AIM. As of

31 December 2009, there are only three GDRs

trading on AIM, as opposed to 190 on the Main

Market. As a result of this, companies

incorporated in Russia generally list on the main

board of the Exchange, whereas companies with

operations in Russia but which are incorporated

outside of Russia have a choice between AIM and

main board listing, depending on the company’s

profile, size, investor base etc.

Requirements for a listing in LondonRegulatory and legal requirements that are

imposed by the regulatory body on all companies

wanting to list on the Exchange (as discussed

above) are a prerequisite for Russian companies

listing their shares on the Exchange. In addition,

corporates need to be sensitive to what would

make their company look more attractive to the

investor community. International investors target

investments on recognised international

exchanges, such as London, because they provide

comfort regarding international standards of

disclosure, accounting and historical performance.

Transparency is also becoming key, especially for

emerging market companies, and precedent has

shown that investors will pay more for companies

with a high commitment to transparency and

disclosure. International investors will also seek

out companies which can demonstrate value,

attractive growth prospects and dedicated

management.

Corporate profileListing on an international stock exchange, such

as the Exchange, is always connected with raising

the profile of the company from the domestic to

international level and may include restructuring,

rebranding etc. This can become crucial for the

marketing of the investment case and therefore

needs to be addressed at the preparatory stage

of the IPO by the company and its advisers (See

‘Company Restructuring’ for further detail).

FinancialsAs Russian Accounting Standards are not

recognised on an international level, IFRS and US-

GAAP accounts have been adopted by Russian

corporates wanting to list on the Exchange. The

financial statements need to be consolidated in the

case of a group structure. High levels of financial

disclosure and transparency are needed to ensure

that the market is comfortable with the company

and a comprehensive annual report, with detailed

notes accompanying any financial statements, will

be expected. Normally the companies are expected

to have a three-year trading record to be eligible to

list on the Exchange; however the rule can be

waived on a case-by-case basis.

If an offering is combined with new capital being

raised, the amount and use of proceeds need to

be consistent with the company’s existing and

planned financial performance and its capital

spending plans. Investors will also pay attention

to the company’s liquidity and indebtedness

ratios, which need to be fairly robust, otherwise

the business model will be perceived as high risk

2 2 L i s t i n g i n L o n d o n : C I S P r a c t i c e

and investors will demand a higher discount at

pricing, or may simply not participate in the

offering.

Corporate governance

Corporate governance is a set of rules, principles,

customs and policies that define the way a

corporation is managed, administered or

controlled. It regulates the relationship between

all the stakeholders of the company and the

operating management who have immediate and

direct control over the company’s actions. Due to

potential conflicts of interest that can exist

between shareholders and the management of the

company, it is imperative that there are systems

in place that can regulate and ensure the efficient

functioning of the company. Corporate

governance is a particular concern with family-

owned companies, where the management also

tend to be the ultimate shareholders of the

company.

Corporate governance for Exchange-listed

companies is regulated either by the Combined

Code, which is binding for all companies listed on

the premium segment of the Exchange, or by the

‘best practice’ standards for all other companies.

The Combined Code uses the ‘comply or explain’

approach, which means that if a company does

not comply with certain provisions of the Code,

they are obliged to explain to investors the

reasons for this.

Establishing a talented board is the cornerstone

of an effective corporate governance system –

this accountability is highlighted by the opening

statement of the Combined Code: ‘Every

company should be headed by an effective Board,

which is collectively responsible for the success of

the company’. The Board of Directors should

comprise of the executive directors, who perform

operational day-to-day activities; and non-

executive directors, who are the custodians of the

governance process. They are not involved in the

day-to-day running of the business, but monitor

the executive activity and contribute to the

development of strategy.

The Combined Code also requires that at least

half of the Board, excluding the chairman, should

comprise non-executive directors determined by

the Board to be independent. There are many

factors that can challenge the independence of a

director, including their previous or current

relationship with the company and its

management/shareholders, material interests

involved and/or time spent with the company, all

of which are stated in the Combined Code.

The Combined Code also provides that the Board

should establish various committees to ensure a

system of internal controls and safeguards

regarding remuneration and nomination of Board

members, as well as dealing with auditors.

Hence, corporate governance has become

increasingly important for Russian companies

recently, as investors have been demanding

greater transparency and management efficiency.

Although not legally binding for Russian

corporates, any foreign company listing on

theLondon Stock Exchange is advised to reflect

2 3 L i s t i n g i n L o n d o n : C I S P r a c t i c e

on the Combined Code and offer certain

corporate governance provisions to increase its

appeal to the international investor community.

ManagementThe experience, qualification and constitution of

the management team are all important factors

that international investors will carefully assess

when considering investing in a company. Since

most of them are passive investors (ie they take

no active role in the management of the company

and are not represented on the Board), they need

to ensure that the management team has the

ability and capabilities needed to run the business

efficiently.

The management team must also have a set of

clearly-defined objectives and a strategy on how

to achieve these objectives. In addition, it must be

able to communicate the strategy clearly and to

show evidence of this in the company’s financial

performance.

Special attention should also be paid to

management remuneration packages – investors

are very keen to see compensation structures tied

into the company’s performance, such as, for

instance, an option scheme, as this ensures that

management’s interests are aligned with those of

the shareholders.

Preliminary steps Once a company has formally decided to IPO, it

will need to appoint one or more advisers to

manage the process. The leading role is normally

given to one or several investment banks, often also

referred to as Global Co-ordinator(s) or Bookrunner(s).

These investment banks take the pivotal role in the

structuring and distribution of the transaction, and

ensuring smooth and effective execution.

Syndicate structureIn order to generate demand, the investment

bank, which is normally appointed at the very

start of the process and is also acting as adviser

to the company through all the steps of an IPO,

usually invites a number of international, regional

and local banks to form a syndicate.

This structure will vary depending on several

factors, including:

• size and type of the issue

• geographical targeting of the offering

• company’s preference as to the participation of

certain banks.

The size of the issue is the main reason for a

multiple bookrunner syndicate. The ‘rule of thumb’

is that the larger the offering, the more banks

should be invited. Precedent shows that for

offerings of over US$200m, Russian corporates

usually involved at least two bookrunners.

This syndicate team mobilises the resources

needed to generate the necessary momentum and

demand to ensure a successful placement. The

selection of banks is generally based on a number

of key criteria, including but not limited to the

following:

• track record in relevant offerings

• sector and regional experience

2 4 L i s t i n g i n L o n d o n : C I S P r a c t i c e

• proposed team and experience

• research capability

• distribution capabilities, and

• relationship with the company.

The experience and commitment of the

syndicate’s members are critical, since this gives

confidence to both the company and institutional

investors.

Other advisersApart from the banks, the issuer should also

appoint certain other advisors, who will help the

company successfully go through all the stages up

to the closing of the transaction. These include:

• Legal advisers normally include issuer’s

counsel and counsel to the underwriter(s), as

well as any other legal advisors for certain

jurisdictions

• Auditors are responsible for the audit of the

produced financial statements of the company

• Technical auditors are responsible for the

production of an independent technical report

(CPR – Competent Party Report), which is

sometimes required to be filed together with the

Offering Circular of the companies operating in

particular sectors and having a substantial asset

base which is important for their business (eg

mining or real estate companies)

• Public relations agency is responsible for all

communications with the press

• Financial pr int ing company is in charge of

printing and distributing the prospectus.

Pre-IPO financingMany companies may find themselves in a

position where they would like to complete some

financing at a time when they are preparing for –

but not yet ready to complete – an IPO. In this

case, the so-called pre-IPO financing can be

arranged, which can be in a variety of forms from

straight debt, pre-IPO convertible bonds to

straight equity.

Straight debt financing, which is commonly

arranged by the investment bank(s) mandated for

the IPO, provides the company with bridge

financing until the IPO has taken place. The

conditions of this agreement are also very often

subject to the completion of the IPO.

A pre-IPO convertible bond issue is an innovative

type of pre-IPO financing. The company issues

bonds, normally with a much lower coupon than

straight debt for a private company, which are

convertible into shares at an agreed conversion

rate upon the completion of the future IPO. The

main benefits of this type of financing include:

Direct benefits

• the coupon is lower on the pre-IPO bond than

on a traditional bank bridge loan because of the

attractiveness of exposure to an upcoming IPO,

either in the form of a convertible or IPO shares

• there are typically none of the performance-

based covenants usually associated with bank

finance

• it delays and/or reduces the dilution associated

with a capital increase

2 5 L i s t i n g i n L o n d o n : C I S P r a c t i c e

• in many cases, original shareholders can often

enjoy the upside in equity valuation until the

IPO takes place.

Indirect benefits

• introduces new investors who are potentially

‘future shareholders’ in the company

• builds momentum towards an IPO, but removes

near-term pressure to complete an IPO within a

narrow timetable

• sets a clear time-frame for the IPO.

The structuring process for this instrument is not

as straightforward as for straight debt and the

company should involve specialist advisers (ie an

investment bank) who will be experienced in

executing this type of transaction.

Offering processThe investment bank must be committed to

executing the transaction – often within a

challenging time-frame – without compromising

any of its duties. All parts of the offering process,

from the inception of the transaction through to

its execution, must be meticulously planned and

agreed by the company. The due diligence

process, prospectus drafting and roadshows take

up significant amounts of senior management

time and so it will be important to ensure that

there are no disruptions to the company’s ongoing

operations.

Among external factors, local and global market

conditions need to be taken into consideration to

ensure that the company accesses the public

markets during favourable and stable market

2 6 L i s t i n g i n L o n d o n : C I S P r a c t i c e

Company restructuringIn order to maximise the valuation of the company

and hence the proceeds from the offering, it is

imperative that the structure of the company is

optimised before marketing to investors gets

underway. The structure should be transparent and

it should fully reflect the company’s true value. The

restructuring exercise may involve inclusion or

exclusion of certain company divisions prior to the

offering, registration of a holding company, change

of domicile and restructuring of the Board etc. The

global co-ordinator/bookrunner will typically advise

the company on this during the preparatory phase.

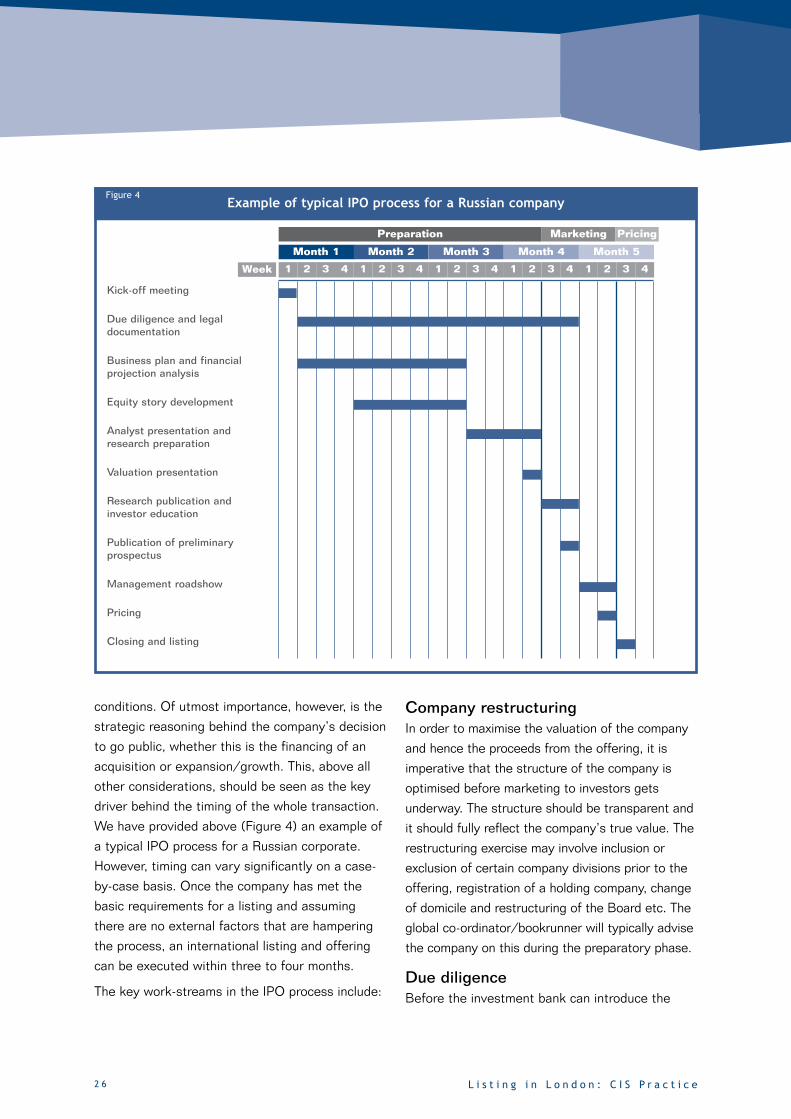

Due diligenceBefore the investment bank can introduce the

Example of typical IPO process for a Russian companyFigure 4

1

Month 1

Kick-off meeting

Due diligence and legaldocumentation

Business plan and financialprojection analysis

Equity story development

Analyst presentation andresearch preparation

Valuation presentation

Research publication andinvestor education

Publication of preliminaryprospectus

Management roadshow

Pricing

Closing and listing

2 432143214321432143

Month 5Month 4Month 3Month 2

Preparation Marketing Pricing

Week

conditions. Of utmost importance, however, is the

strategic reasoning behind the company’s decision

to go public, whether this is the financing of an

acquisition or expansion/growth. This, above all

other considerations, should be seen as the key

driver behind the timing of the whole transaction.

We have provided above (Figure 4) an example of

a typical IPO process for a Russian corporate.

However, timing can vary significantly on a case-

by-case basis. Once the company has met the

basic requirements for a listing and assuming

there are no external factors that are hampering

the process, an international listing and offering

can be executed within three to four months.

The key work-streams in the IPO process include:

2 7L i s t i n g i n L o n d o n : C I S P r a c t i c e

company to the international investor community,

it must obtain a detailed understanding of its

operations and activities. It is important to ensure

that these are presented in a transparent,

accurate and objective manner to international

investors.

The due diligence process involves business, legal

and financial due diligence and the timing of it can

vary depending on a number of factors, including the

complexity of the corporate structure and the level of

transparency in disclosure of corporate and financial

information.

The investment bank will undertake and manage the

business due diligence (eg review of strategy and

business plans, financial model and projections,

review of Board structure as well as full legal and

financial due diligence for the company) with the

assistance of the company’s auditors and the legal

advisers to both the company and the investment

bank. During this process, the investment bank will

thoroughly examine all aspects of the company in

order to provide the appropriate levels of comfort for

the lead manager(s), the international investor

community, as well as for the stock exchange where

the company’s securities will be listed and traded.

The due diligence can often raise issues that must be

resolved prior to the offering, in order to satisfy

investor, regulatory and/or investment bank

requirements. The success of the transaction

depends on full and accurate disclosure, which is the

result of a comprehensive and positive due diligence

process.

It is therefore very important to involve all the

relevant parties in the transaction from the outset

and to communicate, promptly and clearly, the tasks

that must be performed.

Drafting and publication of theprospectusA prospectus is the main disclosure and marketing

document that the company publishes in connection

with the IPO and it serves two main purposes:

• as a marketing document, which provides a full and

detailed description of the company and the

securities offered; and

• as a disclosure and risk mitigation document

covering all material disclosure issues relevant to

Key work-streams in an IPO process

Preparation Marketing Pricing• Market analysis • Due diligence• Valuation analysis • Equity story• Financial reporting • Analyst presentation• Offering strategy • Research preparation• Corporate governance • Prospectus• Incentives for management • Transaction documentsand employees • Stock exchange

• Business plan review discussions • Board structure• Timing and timetable

• Research• Investor targeting• Pre-marketing• Roadshow planning• Roadshow• One-on-ones• Group meetings

• Pricing• Bookbuilding and allocation• Closing and payment ofproceeds

• Listing

• Trading• Stabilisation• Investor relations• Research• Financing strategy andadvice

Figure 5

10-12 weeks 4 weeks Ongoing

an investor making a decision on the offering.

Legal counsel to the company will primarily be

responsible for drafting the prospectus with input

from underwriters and their counsel where

necessary. Other parties, including the company,

syndicate banks and accountants will also provide

input and comments on the relevant sections in

the prospectus.

The prospectus will normally include the following

sections:

• Summary of the offering

• Risk factors

• The offering

• Dividend policy

• Capitalisation / share capital

• Selected consolidated financial information

• Operating and financial review

• Industry

• Business description

• Regulation

• Management

• Principal and selling shareholders (if applicable)

• Description of the GDRs (if applicable)

• Taxation

• Subscription and sale

• Settlement and delivery

• Legal matters

• Independent auditors

2 8 L i s t i n g i n L o n d o n : C I S P r a c t i c e

• Index to financial statements.

The publication of the prospectus normally happens

in two forms:

• one in preliminary form (also called a ‘Red

Herring’) with an indicative price range on the front

cover, on the basis of which investors are

encouraged to place orders with the bookrunner(s)

and

• one in final form upon pricing, outlining the final

price and the final number of shares to be

issued/sold etc.

Research Research production and publication, which is

normally handled by the syndicate banks, is the first

step in marketing the company. Any company would

like to ensure coverage by as many research

analysts as possible to ensure that the maximum

number of investors are educated about the

company’s investment case. The role of research

analysts is of paramount importance to an equity

offering. The main tasks accomplished by research

analysts would normally be as follows:

• independent assessment of the company’s

investment case

• identification and evaluation of comparable

companies

• preparation and publication of independent

research report (including forecasts)

• education of syndicate’s sales force

• co-ordination of investor education effort

• identification of key investor concerns to be

2 9L i s t i n g i n L o n d o n : C I S P r a c t i c e

addressed during roadshow

• follow-up calls to institutional investors.

Other documentation Apart from the prospectus, there are a number of

additional documents to be signed/issued during

the IPO process. Key documentation would

normally include:

• Underwriting agreement

The main legal agreement in an international

offering is a subscription or underwriting

agreement. It is entered into by the issuer,

selling shareholders and directors (where

appropriate), the global coordinators and all the

managers. It is normally signed after pricing and

constitutes a firm commitment by the managers

to underwrite the offering subject to certain

conditions precedent and force majeure. The

key provisions of the underwriting agreement

include representations and warranties,

principally dealing with the accuracy and

completeness of the prospectus and compliance

with certain legal matters, undertakings of the

issuer (including lock-up provisions), fees and

expenses, conditions precedent, selling

restrictions and termination events.

• Legal opinions

Typically in international equity offerings

managers receive legal opinions from

transaction counsel covering such areas as the

due incorporation of the issuer, the

enforceability of the legal documents under

their governing law, taxation, US securities law,

and depending on the type of offering, a

disclosure opinion verifying aspects of the

disclosure in the prospectus.

• Auditor’s comfort letters

Comfort letters are letters written to the

issuer and the managers and will typically aim

to achieve two goals:

(i) confirm the accurate extraction of the

financial statements in the prospectus from the

audited accounts; and

(ii) provide comfort on the financial situation of

the issuer in the period from the date of the

disclosed accounts and the offering.

There may be other documents that will need to

be signed at different stages of IPO execution;

however, they are subject to individual

arrangements and are often of a technical nature.

Investor educationOnce the research report has been published, the

investor education period begins (it normally

continues right through to pricing). During this

period, sales people from the syndicate banks will

contact investors and market the company’s

equity story to them. Investors would normally

have received research report(s) by then and will

therefore be able to make initial assessment of

their potential interest and involvement in the

deal. The involvement of the research analyst is

paramount to the success of investor education,

answering investors’ questions with regard to the

research report and providing details to them on

the company’s positioning, as well as key sector

trends. The main aim of investor education is to

get a market view on the company’s investment

case and its valuation.

RoadshowOnce the market has been informed about the

company’s investment case and investors have

had some time to review the research reports and

the prospectus, the roadshow period commences.

The roadshow involves key members of the

management team meeting a number of potential

investors in major financial centres across Europe,

US and Asia, communicating the company’s

investment case to them and addressing any

queries they may have.

Very often, the decision over whether or not to

invest in a certain business will centre on the

calibre of the management involved and so

personal contact plays an important part in this

process (by helping potential investors to feel

more comfortable about their investment, as well

as building up trust and confidence).

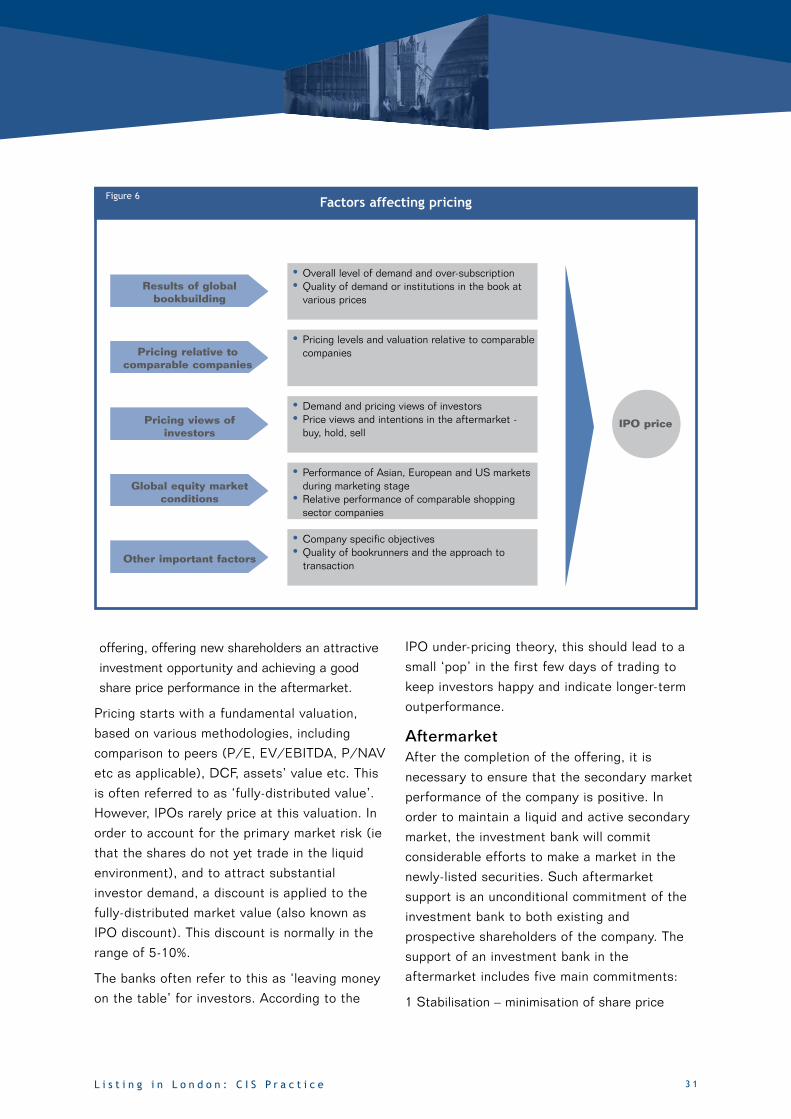

Pricing and allocation Pricing is one of the most complex processes in

the IPO as it ultimately defines the market

valuation of the company. Whilst there are many

pricing methodologies that can be utilised in IPOs

by Russian issuers, book-building is the most

common. Under this methodology, the pricing

process is implemented in two stages:

Stage 1: Setting the pr ice range.

Following the investor education period and

usually before the start of the roadshow, the

3 0 L i s t i n g i n L o n d o n : C I S P r a c t i c e

company and the syndicate agree on a price

range, within which the offering will be marketed

to investors. Even though it is becoming more

common in emerging market IPOs, a price range

may not be set at the end of the investor

education process, but rather at some stage

during the roadshow itself. This is commonly

referred to as a ‘decoupled’ approach. Whether a

decoupled approach is utilised will depend on the

particular circumstances of the offering at the

time.

The width of this price range (usually around

20%) is primarily dependant on the level of

certainty about the valuation of the company, on

market volatility and on received investor

feedback. Once the price range becomes public,

normally via publication of a preliminary

prospectus, investors are allowed to place orders

with bookrunners for the issuer’s shares within

the indicated price range. The price range is

designed to provide guidance to investors as to

the indicative/intended valuation of the company.

Although the price range can be revised upwards

or downwards later in the process, depending on

the demand for the offering, it is not considered

to be best market practice.

Stage 2: Pric ing.

Based on the order book at the end of the book

building, the issuer and the syndicate decide on

the uniform price at which the shares will be

offered to institutional investors, as well as on

how many shares each of the investors will

receive. Key pricing considerations include the

following: maximising the proceeds from the

3 1L i s t i n g i n L o n d o n : C I S P r a c t i c e

offering, offering new shareholders an attractive

investment opportunity and achieving a good

share price performance in the aftermarket.

Pricing starts with a fundamental valuation,

based on various methodologies, including

comparison to peers (P/E, EV/EBITDA, P/NAV

etc as applicable), DCF, assets’ value etc. This

is often referred to as ‘fully-distributed value’.

However, IPOs rarely price at this valuation. In

order to account for the primary market risk (ie

that the shares do not yet trade in the liquid

environment), and to attract substantial

investor demand, a discount is applied to the

fully-distributed market value (also known as

IPO discount). This discount is normally in the

range of 5-10%.

The banks often refer to this as ‘leaving money

on the table’ for investors. According to the

IPO under-pricing theory, this should lead to a

small ‘pop’ in the first few days of trading to

keep investors happy and indicate longer-term

outperformance.

AftermarketAfter the completion of the offering, it is

necessary to ensure that the secondary market

performance of the company is positive. In

order to maintain a liquid and active secondary

market, the investment bank will commit

considerable efforts to make a market in the

newly-listed securities. Such aftermarket

support is an unconditional commitment of the

investment bank to both existing and

prospective shareholders of the company. The

support of an investment bank in the

aftermarket includes five main commitments:

1 Stabilisation – minimisation of share price

Factors affecting pricingFigure 6

Results of globalbookbuilding

Pricing relative tocomparable companies

Pricing views of investors

Global equity marketconditions

Other important factors

• Overall level of demand and over-subscription• Quality of demand or institutions in the book atvarious prices

• Pricing levels and valuation relative to comparablecompanies

• Performance of Asian, European and US marketsduring marketing stage

• Relative performance of comparable shoppingsector companies

• Company specific objectives• Quality of bookrunners and the approach totransaction

• Demand and pricing views of investors• Price views and intentions in the aftermarket -buy, hold, sell

IPO price

3 2 L i s t i n g i n L o n d o n : C I S P r a c t i c e

4 Research coverage – timely and ongoing

research coverage of the company can

consistently raise the company’s profile in the

investor community and keep investors updated

on the recent company’s developments.

5 Support of investor relations programme – an

investment bank will assist its client to set up

and maintain regular investor relations activities

to ensure that all outside existing and potential

investors in the company are well informed

about the company’s recent progress and

developments.

In addition to the aftermarket support roles

outlined, the investment bank will usually monitor

the company’s performance and continuously

offer recommendations to the company on various

matters. This ensures that a long-term

relationship is built up with a view to ongoing

support being provided to the company and its

shareholders.

volatility post-listing and, if applicable, exercise

of the over-allotment option, if granted. The

ability of a bank to do this is strictly regulated.

An over-allotment option is an option granted to

the investment bank lead-managing the offering

to over-allot usually up to 15% of the overall

number of shares in the offering to investors in

case of strong demand. By using the over-

allotment option, the investment bank can

support the share price, but only if it drops

below the offering price.

2 Trading and market making – in order to ensure

the minimum level of liquidity and constant

availability of a market bid/ask price for the

listed securities, the investment bank will

normally commit to market-making in the stock

following the completion of the offering.

3 Capital commitment – if necessary, the

investment bank should use its own capital to

encourage an active secondary aftermarket in

the stock.

Nomura – a changing landscape

o

Moscow, Warsaw, Budapest and Vienna. www.nomura.com

John-Paul Warszewski

Managing Director

Investment Banking

Nomura International plc

Tel: +44 (0) 207 102 2535

Michael Boardman

Managing Director

Global Finance

Nomura International plc

Tel: +44 (0) 207 103 4660

Myles Evanson

Executive Director

Global Finance

Nomura International plc

Tel: +44 (0) 207 103 4664

Nomura is the global marketing name of Nomura Holdings, Inc. (Tokyo) and its direct and indirect subsidiaries worldwide including Nomura International (Hong Kong) Limited, licensed and regulated by the Hong Kong Securities and Futures Commission, Nomura Securities International, Inc (New York), a member of NASD, NYSE and SIPC and Nomura International plc (London), authorised and regulated by the Financial Services Authority and member of the London Stock Exchange.

Contact:

take we Nomura, At

leading a As . viewent ferdifa take

Nomura – a changing landscape

oup grservices financial leading

Nomura – a changing landscape

Asia, in based oup

Nomura – a changing landscape

, Budapest and Varsaw, WMoscow

longstanding and dedicated

today’in success for

clients with partner we

Contact:

Investment Banking

ectorManaging Dir

arszewskiJohn-Paul W

.nomura.com wwwienna., Budapest and V

well as London in teams longstanding

links Nomura markets. s today’

making world the ound arclients

Global Finance

ectorManaging Dir

dmanMichael Boar

.nomura.com

oss acround grthe on as well

owth grs ope’Eurand s Asia’

delivering and connections making

Global Finance

ectorExecutive Dir

Myles Evanson

including ope, Eur

ough thrmarkets

solutions ed tailor

ector

Myles Evanson

.stekraMlabolG

el: +44 (0) 207 102 2535TTel: +44 (0) 207 102 2535

national plcNomura Inter

Investment Banking

M.gniknaBtnemtsevnI

el: +44 (0) 207 103 4660TTel: +44 (0) 207 103 4660

national plcNomura Inter

Global Finance

tessA.gniknaBtnahcre

el: +44 (0) 207 103 4664T

national plcNomura Inter

Global Finance

el: +44 (0) 207 103 4660

national plc

.tnemeganaM

el: +44 (0) 207 103 4664

national plc

Financial Services Authority and member of the London Stock Exchange.Hong Kong Securities and Futur

Financial Services Authority and member of the London Stock Exchange.national, Inc (New Yes Commission, Nomura Securities InterHong Kong Securities and Futur

okyo) and its dirokyo) and its dir

ork), a member of NASD, NYSE and SIPC and Nomura International, Inc (New Yect subsidiaries worldwide including Nomura Interect and indirokyo) and its dir

national plc (London), authorised and rork), a member of NASD, NYSE and SIPC and Nomura International (Hong Kong) Limited, licensed and rect subsidiaries worldwide including Nomura Inter

egulated by the national plc (London), authorised and regulated by the national (Hong Kong) Limited, licensed and r

Despite market volatility, a number of companies,

whose principal operations or assets are based in

one or more of the 12 countries comprising the

Commonwealth of Independent States (CIS),

continue to consider listing their securities on the

London Stock Exchange (the Exchange). Many

have achieved such a listing.

Companies with operations in the CIS may list

their equity securities on the Exchange either (a)

by listing shares; or (b) by listing depositary

receipts (DRs).

This article focuses primarily on the listing of DRs

by a company incorporated in the CIS. However,

we note that there are also a growing number of

companies incorporated outside of the CIS whose

shares are listed on the Exchange but whose

principal operations are in the CIS. This article

does not address in any detail the listing of debt

securities.

The purpose of this article is to summarise the

role which the company’s UK legal counsel will

typically play, and the main legal issues which the

company will encounter on a listing, in

chronological order. Securities are technically

listed on the Official List of the FSA and Admitted

3 4 L i s t i n g i n L o n d o n : C I S P r a c t i c e

Role of the law firm in a Main Market listingSergei Ostrovsky, Partner, Ashurst and Jonathan Parry, Senior Associate,Ashurst

The company’s lawyers play a central role in the process of representingthe interests of the company and its directors throughout the process ofachieving a listing on the Main Market of the London Stock Exchange.

to trading on the Main Market of the London

Stock Exchange. For ease of reference, this

article will refer to “listing on the `Main Market of

the Exchange”.

Engagement by the company of its UKlegal counselTypically there will be at least two different law