live coaching classes

TRANSCRIPT

LIVE COACHING CLASSESBOARD OF STUDIES(A), ICAI

CA FINALTOPIC NAME – 4. EXEMPTIONS FROM GST

PAPER 4: TAXATION SEC B – INDIRECT TAXES

Faculty Name: CA Sumeet Maru

Date: 20th July 2021

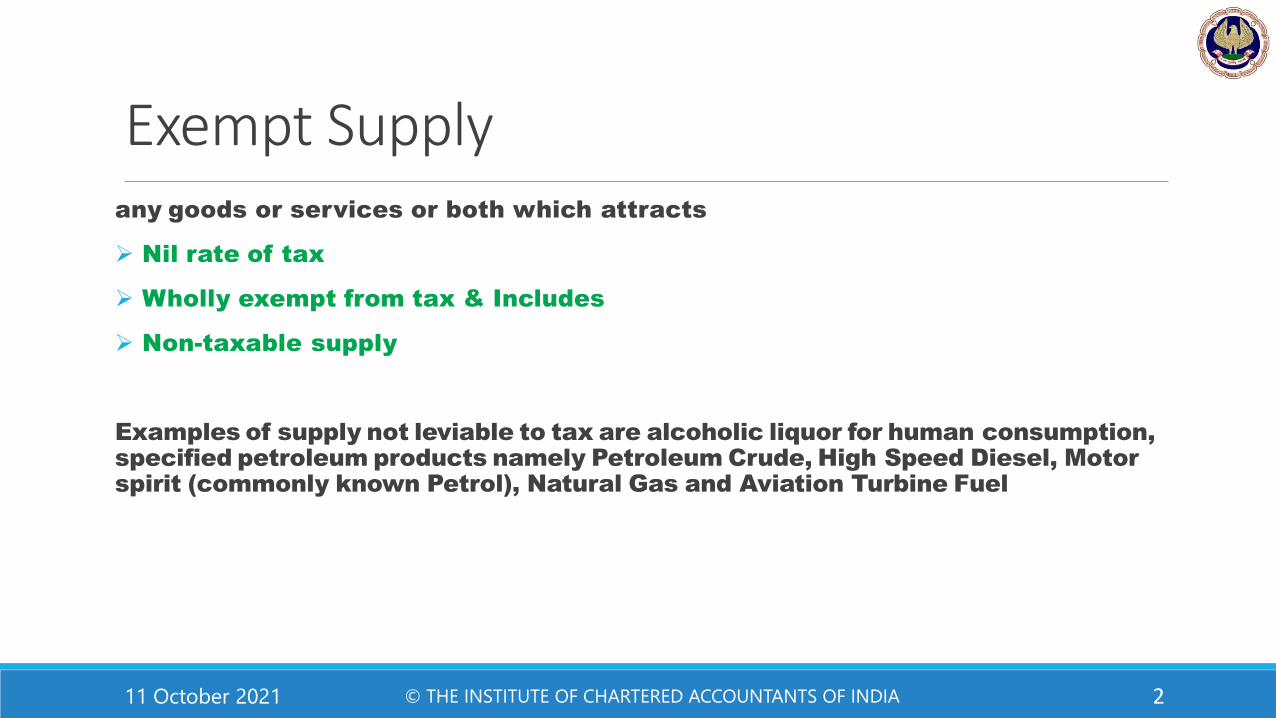

Exempt Supplyany goods or services or both which attracts

➢ Nil rate of tax

➢ Wholly exempt from tax & Includes

➢ Non-taxable supply

Examples of supply not leviable to tax are alcoholic liquor for human consumption,specified petroleum products namely Petroleum Crude, High Speed Diesel, Motorspirit (commonly known Petrol), Natural Gas and Aviation Turbine Fuel

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 2

Exemptions Exemptions under GST Can be provided in any of the Following Manner :

➢Exemption to specified activities or transactions

➢Exemption to specified suppliers

➢Exemption to specified recipients

➢Exemption to specified suppliers and specified recipients

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 3

Power to Grant ExemptionGST law empowers the Central Government or State Government, as the case may be, to grant exemption from tax. The exemption is granted on recommendation of the GST Council

➢Exemption can be from whole of tax or part of tax

➢Exemption can be granted by a notification or by a special order

➢Unconditional exemption is mandatory

➢Conditional exemption is optional

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 4

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 5

Exemption by NotificationExplanation inserted within 1 year, for the purpose of clarifying the scope or applicability of any notification/order, to have retrospective effect:

Wherever the Government feels that there is a need to clarify the scope or applicability of any notification/order issued under this section, itcan issue an explanation within 1 year of issue of said notification/ order. Such explanation shall have effect as if it was there when firstsuch notification/ order was issued, i.e. explanation so inserted would be effective retrospectively

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 6

Goods Exempt from TaxUnder GST, everyday items used by the common man have been included in thelist of exempted items. Items such as unbranded atta/ maida/ besan, unpacked food grains, milk, eggs, curd, lassi and fresh vegetables are among the itemsexempted from GST

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 7

Services Exempt from Tax

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 8

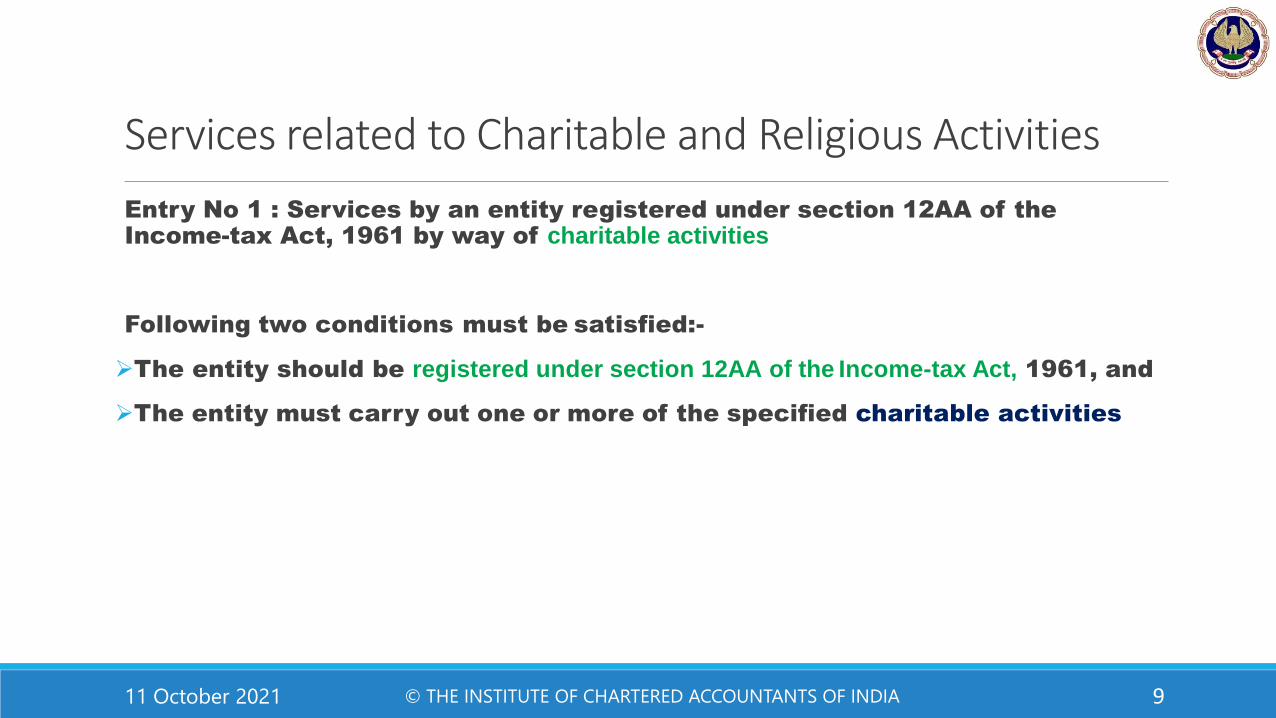

Services related to Charitable and Religious Activities

Entry No 1 : Services by an entity registered under section 12AA of the Income-tax Act, 1961 by way of charitable activities

Following two conditions must be satisfied:-

➢The entity should be registered under section 12AA of the Income-tax Act, 1961, and

➢The entity must carry out one or more of the specified charitable activities

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 9

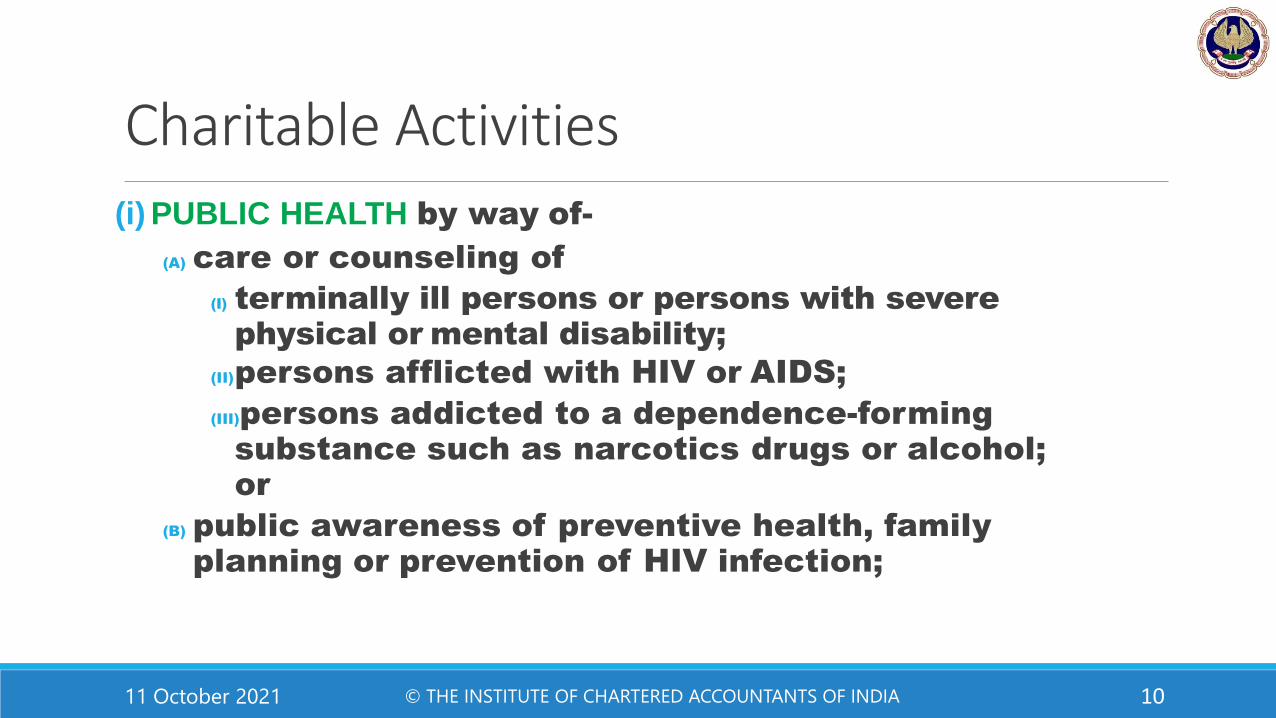

Charitable Activities(i) PUBLIC HEALTH by way of-

(A) care or counseling of

(I) terminally ill persons or persons with severe physical or mental disability;

(II)persons afflicted with HIV or AIDS;

(III)persons addicted to a dependence-forming substance such as narcotics drugs or alcohol;or

(B) public awareness of preventive health, familyplanning or prevention of HIV infection;

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 10

Charitable Activities(ii) ADVANCEMENT OF RELIGION, spirituality or yoga

(iii) ADVANCEMENT OF EDUCATIONAL PROGRAMME/SKILL DEVELOPMENT relating to,-

(A) abandoned, orphaned or homeless children;

(B) physically or mentally abused and traumatized persons;

(C) prisoners; or

(D) persons over the age of 65 years residing in a rural area;

(iv) PRESERVATION OF ENVIRONMENT including watershed, forests & wildlife.

Thus, Any other Services Provided by Charitable Trust will be Chargeable to Tax

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 11

Services by Charitable Institute➢Management of educational institutions by charitable trusts

Activities of schools, colleges or any other educational institutions run by charitable trusts by way of education or skill development of abandoned, orphans, homeless children, physically or mentally abused persons, prisonersor persons over age of 65 years or above residing in a rural area, will be considered as charitable activities and income from such supplies will be wholly exemptfrom GST.

Activities of a school, college or an institution run by a trust which do not come within the ambit of charitable activities will not be exempt under Entry 1of the Notification. However, such activities may be exempt under Entry 66 ofthe Notification [discussed later in this chapter] provided the school, college orinstitution qualifies as an 'educational institution'.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 12

Charitable Activities➢Hostel accommodation provided by trusts

Hostel accommodation services provided by trusts to students do not fall within the ambit of charitable activities as defined above.

However, accommodation service in hostels including such services provided bytrusts having value of supply upto ` 1,000 per day is exempt under Entry 14 ofthe

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 13

Charitable Activities➢Religious yatras or pilgrimage

As per Entry 60, the services provided by the Haj Committee and Kumaon Mandal Vikas Nigam Limited (KMVN), a Government of Uttarakhand Undertaking in relation to pilgrimage to Mecca and Kailash- Mansarovar respectively are not liable to GST

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 14

Charitable Activities➢Training or coaching in recreational activities

Services by way of training or coaching in recreationalactivities relating to-

(a) arts or culture, or

(b) sports by charitable entities registered undersection 12AA of the Income-tax Act are exemptfrom GST.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 15

Services to Charitable Trust

➢NO Exemption

Unless specifically provided

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 16

B. CONDUCT OF ANY RELIGIOUS CEREMONYamount charged, by whatever name called, for the conduct of any religious ceremony is exempt from GST. Religious ceremonies are life-cycle rituals including special religious poojas conducted in terms of religious texts by a person so authorized by such religious texts. Occasions like birth, marriage, and death involve elaborate religious ceremonies

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 17

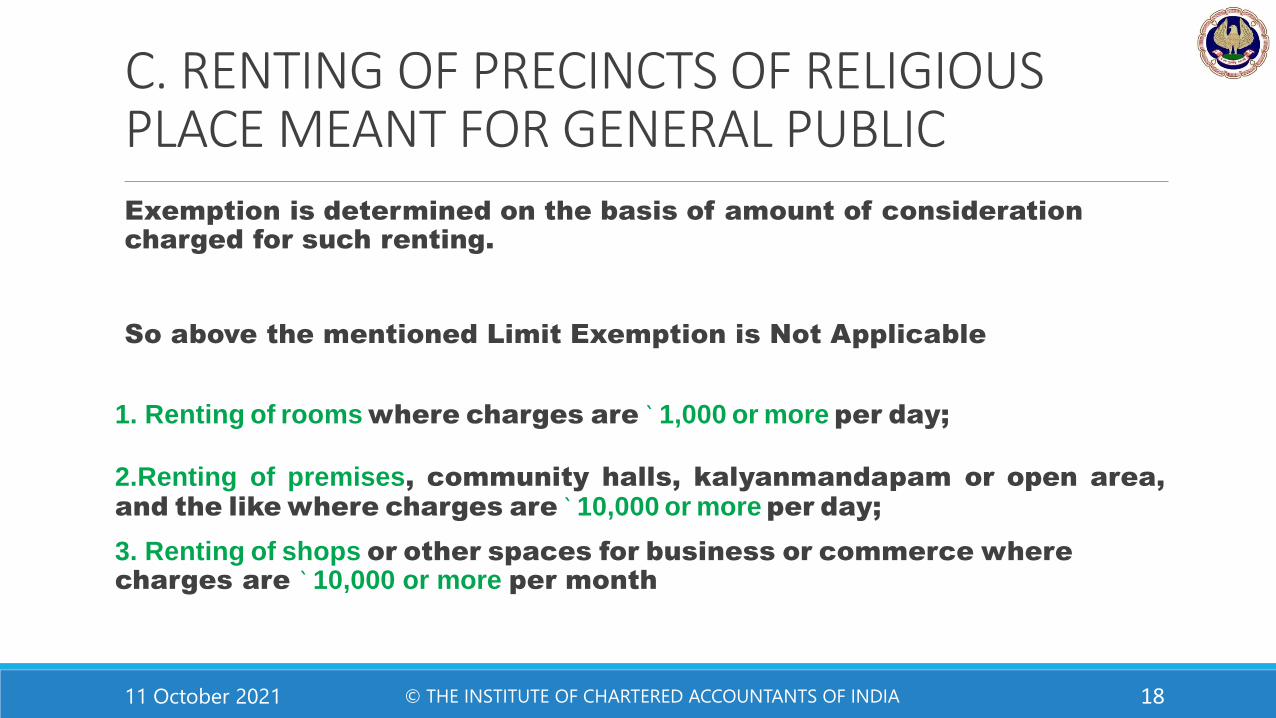

C. RENTING OF PRECINCTS OF RELIGIOUS PLACE MEANT FOR GENERAL PUBLIC

Exemption is determined on the basis of amount of consideration charged for such renting.

So above the mentioned Limit Exemption is Not Applicable

1. Renting of rooms where charges are ` 1,000 or more per day;

2.Renting of premises, community halls, kalyanmandapam or open area,and the like where charges are ` 10,000 or more per day;

3. Renting of shops or other spaces for business or commerce where charges are ` 10,000 or more per month

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 18

Question

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 19

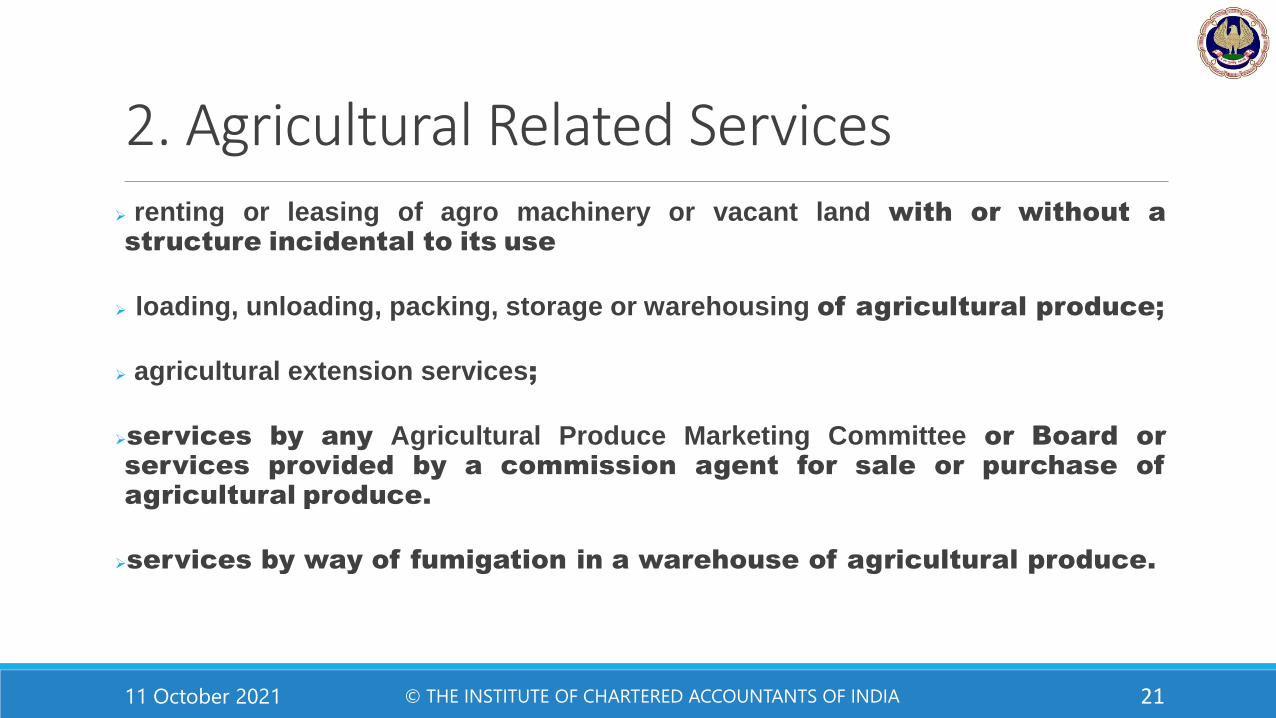

2. Agricultural Related Services

Entry 54 - Services relating to cultivation of plants and rearing of all life forms of animals, except the rearing of horses, for food, fibre, fuel, raw material orother similar products or agricultural produce by way of—

➢ Agricultural operations directly related to production of any agriculturalproduce including cultivation, harvesting, threshing, plant protection ortesting;

➢ Supply of farm labour;

➢ Processes carried out at an agricultural farm including tending, pruning, cutting,harvesting, drying, cleaning, trimming, sun drying, fumigating, curing, sorting,grading, cooling or bulk packaging and such like operations which do not alterthe essential characteristics of agricultural produce but make it onlymarketable for the primary market;

Agriculture Produce - On which either no further processing is done or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics, but makes it marketable for primary market

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 20

2. Agricultural Related Services➢ renting or leasing of agro machinery or vacant land with or without astructure incidental to its use

➢ loading, unloading, packing, storage or warehousing of agricultural produce;

➢ agricultural extension services;

➢services by any Agricultural Produce Marketing Committee or Board orservices provided by a commission agent for sale or purchase ofagricultural produce.

➢services by way of fumigation in a warehouse of agricultural produce.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 21

Renting or leasing of agro machinery or vacant land

Item (d) of the entry exempts renting or leasing of agro machinery or vacant land withor without a structure incidental to its use.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 22

Agricultural extension services

Application of scientific research and knowledge to agricultural practicesthrough farmer education or training.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 23

Agricultural Produce Marketing Committee services

Services by any Agricultural Produce Marketing Committee or Board or services provided by a commission agent for sale or purchase of agricultural produceare not liable to GST. APMCs collect market fees, license fees, rents etc.

Any other Services provided by APMC not relating to Agriculture , will be liable to tax e.g. renting of shops or other property for commercial purposes.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 24

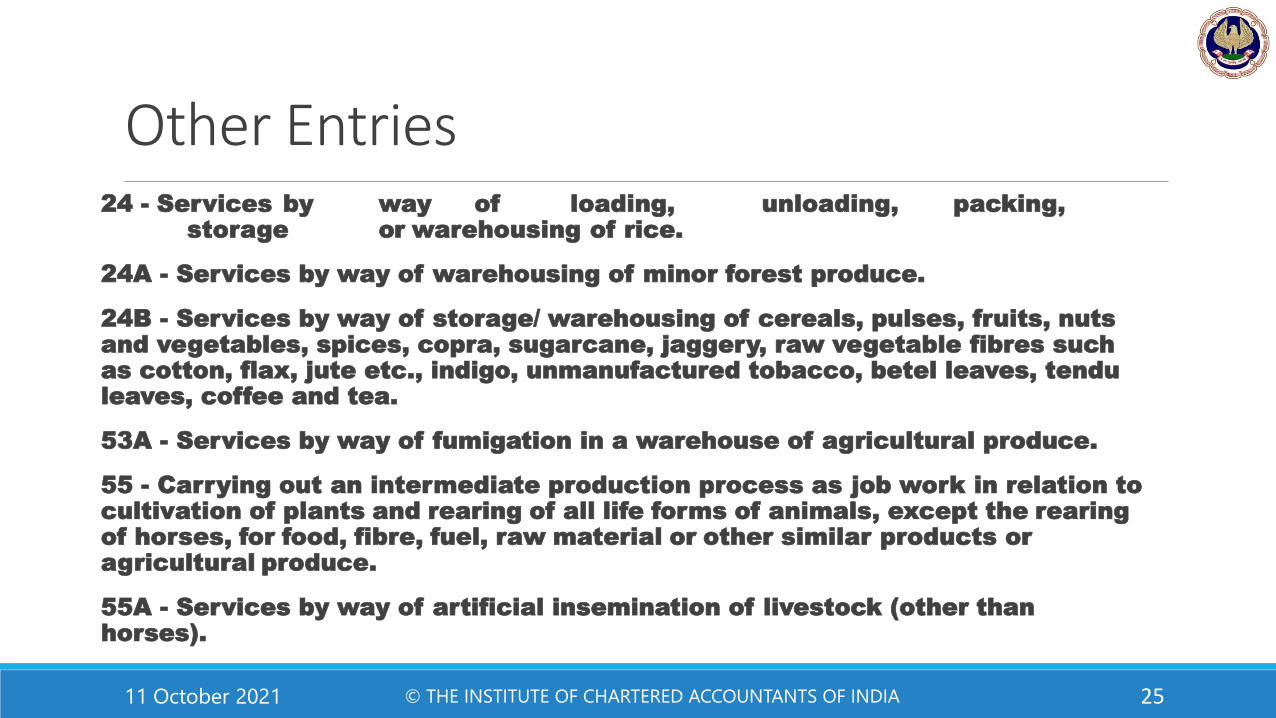

Other Entries24 - Services by way of loading, unloading, packing,

storage or warehousing of rice.

24A - Services by way of warehousing of minor forest produce.

24B - Services by way of storage/ warehousing of cereals, pulses, fruits, nuts and vegetables, spices, copra, sugarcane, jaggery, raw vegetable fibres such as cotton, flax, jute etc., indigo, unmanufactured tobacco, betel leaves, tendu leaves, coffee and tea.

53A - Services by way of fumigation in a warehouse of agricultural produce.

55 - Carrying out an intermediate production process as job work in relation tocultivation of plants and rearing of all life forms of animals, except the rearingof horses, for food, fibre, fuel, raw material or other similar products or agricultural produce.

55A - Services by way of artificial insemination of livestock (other than horses).

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 25

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 26

ILLUSTRATION 1

Dukhiya Das is enaged in providing following services. With the help of information

given below, determine which of the services provided by Dukhiya Das are exempt from

GST:

•Packaging of the onions purchased from village farmers into small packets of 1 kg each,

in Dukhiya Das warehouse, so that same can be sold in a nearby city mall.

•Warehousing of jaggery and tea.

•Renting of warehouse for storage of agricultural produce.

3. Educational Services – Entry 66

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 27

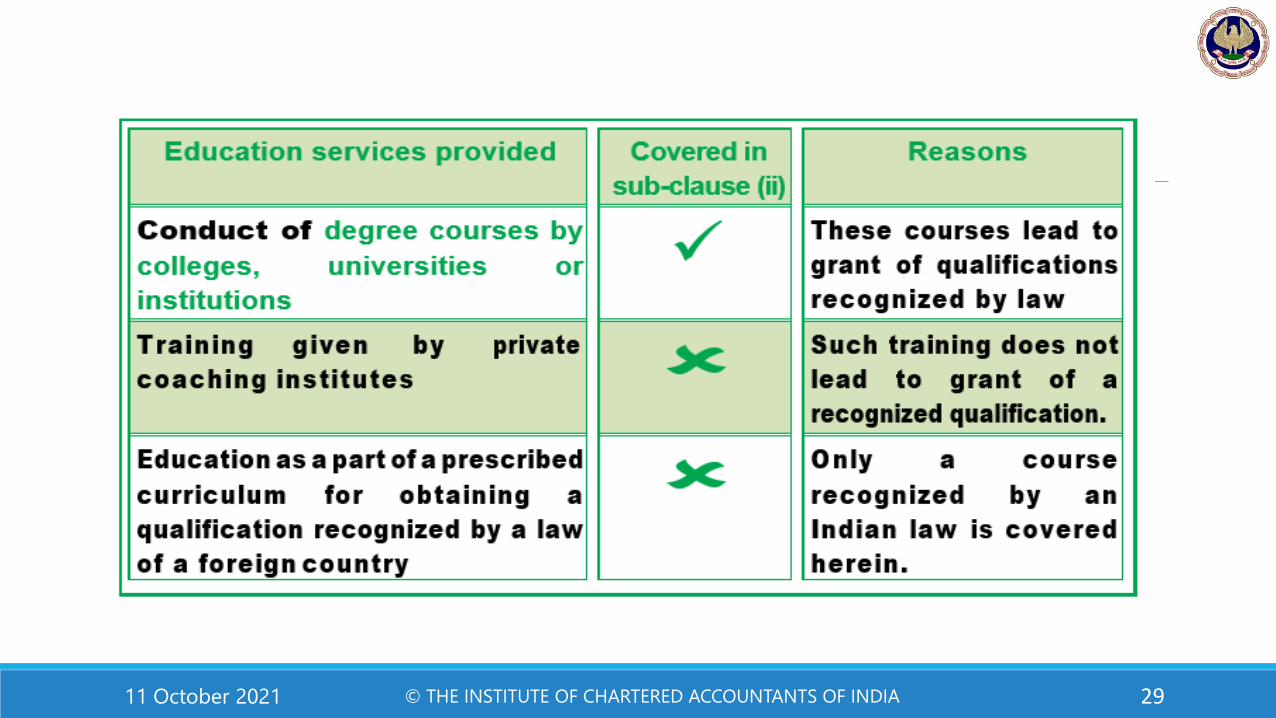

Services provided by an educational institution to its students, faculty and staff and by way of conduct of entrance examination against consideration in the formof entrance fee are exempt from GST.

Educational Institutionan institution providing services by way of,-

(i) pre-school education and education up to higher secondary school

or equivalent;

(i) education as a part of a curriculum for obtaining a qualification recognised byany law for the time being in force;

(ii) education as a part of an Approved vocational education course.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 28

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 29

Boarding Schools

In Boarding Schools service of education coupled with other services likeproviding dwelling units for residence and food. This may be a case of compositesupply if the charges for education and lodging and boarding are inseparable.

In this case since the predominant nature is determined by the service of education, the other service of providing residential dwelling will not be considered for the purpose of determining the tax liability and in this case theentire consideration for the supply will be exempt.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 30

Educational institutions providing qualification recognized by law - Exempt

Dual Qualification & only one of which is recognized by law

Two separate services Service in respect of each qualification would, therefore, be assessed separately

& if Not Separatable then will be treated as Mixed Supply

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 31

Incidental auxiliary courses provided by way of hobby classes or extra-curricular activities

will be an example of naturally bundled course, and therefore treated ascomposite supply

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 32

Indian Institutes of ManagementIIMs fall under purview of “educational institutions” as they provide education as a part of a curriculum for obtaining a qualification recognized by law for thetime being in force

Long Duration Course – Recognised by Law (1 Year or More) – Exempt

Short Duration Courses – Not Recognised by Law – Not Exempt

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 33

Supply of food in a mess or canteen

If the catering services is one of the services provided by an educational institution to itsstudents, faculty and staff and the said educational institution is covered by the definition of‘educational institution’ as given above, then the same is exempt

If the catering services, i.e., supply of food or drink in a mess or canteen, is provided by anyone other than the educational institution, i.e. the institution outsources thecatering activity to an outside contractor, then it is a supply of service to the concerned educational institution by such outside caterer and attracts GST.**

Note: Said services when provided to an educational institution providing pre- school education or education up to higher secondary school or equivalent are exempt from tax

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 34

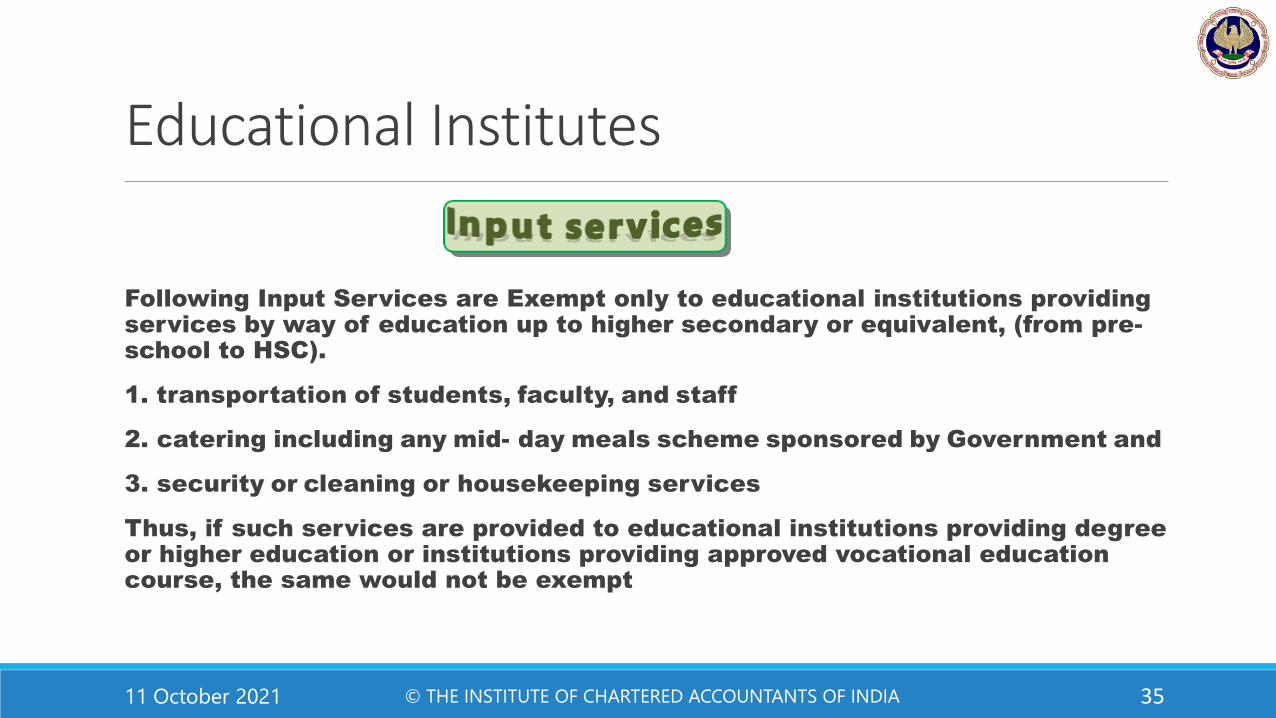

Educational Institutes

Following Input Services are Exempt only to educational institutions providing services by way of education up to higher secondary or equivalent, (from pre-school to HSC).

1. transportation of students, faculty, and staff

2. catering including any mid- day meals scheme sponsored by Government and

3. security or cleaning or housekeeping services

Thus, if such services are provided to educational institutions providing degree or higher education or institutions providing approved vocational education course, the same would not be exempt

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 35

4. Services relating to admission to, or conduct of examination by, such institution:

Is an Exempt Input Service to all Including Schools upto HSC and institutions providing qualification recognized by Law.

5. Supply of Online educational Journal or Periodicals will be Exempt to only Educational institution providing education as a part of a curriculum for obtaining a recognised qualification

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 36

Educational institution providing pre-school education and education up to higher secondary school or equivalent

Educational institution providing education as a part of a curriculum for obtaining a recognised qualification

Educational institution providing education as a part of approved vocational education course

Exempt Input Services 1. Transportation of students, faculty, amdstaff

2. Catering including any midday meals sponsored by Central Government, State or Union

3. Security or cleaning or house keeping services

4. Services relating to admission to, or Conduct of examination

1. Services relating to admission to, orconduct of examination by such institute2. Supply of Online Educational Journal

1. Services relating to admission to, orconduct of examination by such institute

Exempt Output Services Services provided by an educational institution -(a) to its students, faculty and staff;(aa) by way of conduct of entrance examination against consideration in the form of entrance fee.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 37

4. Health Care Services

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 38

Description of services

Services by a veterinary clinic in relation to health care of animals or birds.

Services by way of-

(a) health care services by a clinical establishment, an authorised medicalpractitioner or para-medics;

(b) services provided by way of transportation of a patient in an ambulance,other than those specified in (a)above.

Services provided by the cord blood banks by way of preservation of stem cells or any otherservice in relation to such preservation.

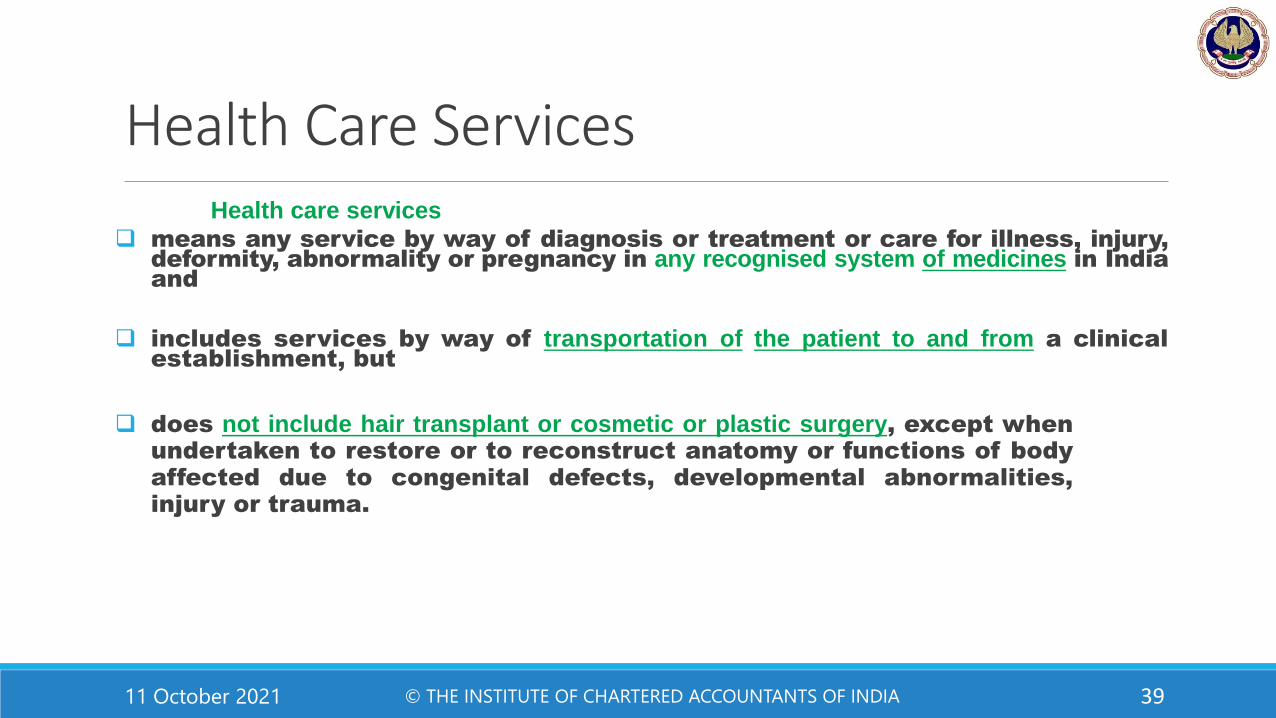

Health Care ServicesHealth care services

❑ means any service by way of diagnosis or treatment or care for illness, injury,deformity, abnormality or pregnancy in any recognised system of medicines in Indiaand

❑ includes services by way of transportation of the patient to and from a clinicalestablishment, but

❑ does not include hair transplant or cosmetic or plastic surgery, except whenundertaken to restore or to reconstruct anatomy or functions of bodyaffected due to congenital defects, developmental abnormalities,injury or trauma.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 39

Health Care ServicesAs it is apparent from the definition of health care services, onlyservices in recognized systems of medicines in India are exempt under thisentry.Following systems of medicines are the recognized systems of medicines in India15:-

❑ Allopathy

❑ Yoga

❑ Naturopathy

❑ Ayurveda

❑ Homeopathy

❑ Siddha

❑ Unani

❑ Any other system of medicine that may be recognized by Central Government

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 40

Services provided by senior doctors/ consultants/ technicians

Hospitals hire senior doctors/ consultants/ technicians independently. Such persons do not have any contract with the patient. Hospitals pay them consultancy charges and there is no employer-employee relationship between them.

It is clarified by CBIC that services provided by such senior doctors/ consultants/ technicians, whether employees or not, are healthcare services which are exempt from GST

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 41

Food supplied to the patients

➢Food supplied to the in-patients as advised by the doctor/nutritionists is a part of composite supply of healthcare and not separately taxable

➢When outsourced, there is no ambiguity that the suppliers shall charge tax as applicable and hospital will get no ITC.

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 42

ILLUSTRATION 2

Good Health Medical Centre, a clinical establishment, offers the following services:

(i) Reiki healing treatments.

(ii) Plastic surgeries. One such surgery was conducted to repair cleft lip of a new born

baby.

(iii) Air ambulance services to transport critically ill patients from distant locations to the

Medical Centre.

(iv) Palliative care for terminally ill patients. On request, such care is also provided to

patients at their homes. (Palliative care is given to improve the quality of life of

patients who have a serious or life-threatening disease but the goal of such care is

not to cure the disease).

(v) Alternative medical treatments by way of yoga

Good Health Medical Centre also operates a cord blood bank which provides services in

relation to preservation of stem cells.

Good Health Medical Centre is of the view that since it is a clinical establishment, all the

service provided by it as well as all the services provided to it are exempt from GST.

You are required to examine the situation in the light of relevant statutory provisions

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 43

11 October 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 44

THANK YOU