lloyd’s ils investor presentation/media/files/lloyds/investor...c t u a l 2 0 1 4 a c t u a l 2 0...

TRANSCRIPT

Lloyd’s ILS Investor Presentation

© Lloyd’s

February 2018

John Parry, Chief Financial Officer

2

Disclaimer

© Lloyd’s

This information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. It is the responsibility of any person publishing, downloading or communicating the contents of this document or communication, or any part thereof, to ensure compliance with all applicable legal and regulatory requirements.

The content of this presentation does not represent a prospectus or invitation in connection with any solicitation of capital. Nor does it constitute an offer to sell securities or insurance, a solicitation or an offer to buy securities or insurance, or a distribution of securities in the United States or to a U.S. person, or in any other jurisdiction where it is contrary to local law. Such persons should inform themselves about and observe any applicable legal requirement.

3© Lloyd’s

Strategy 5

Brexit 8

Oversight 11

Capital 15

Central Fund – ILS opportunity 28

Agenda

Strategy

© Lloyd’s

5

The benefits of placing business and operating at Lloyd’s

© Lloyd’s

The advantages of operating at Lloyd’s remain strong

Customers & distribution Capital Operations & services

• Access to business brought to Lloyd’s

• A broad and expanding licence network in over 200 territories

• Delegated authority and subscription models

• All policies underpinned by the Central Fund

• Efficient and Flexible

• Single Financial Strength Rating

• Economies of scale from central services

Talent Brand Market oversight

• The Lloyd’s market is a recognised centre of specialist underwriting, claims and analytics expertise

• Lloyd’s has a globally recognisable brand

• Reputation for paying all valid claims in a timely and efficient manner

• Corporation oversees risks written at Lloyd’s

• Proportionate and robust market oversight regime consistent with an entrepreneurial and innovative culture

6

New entrants

© Lloyd’s

7

6

8

5

3

2

4

3

2

4

3

3

2

1

4

2

3

4

4

4

1

1

1

1 1

4

3

1

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Approved Managing Agents

Approved SPA

Approved Syndicates

Interest in business joining the Lloyd’s

Market remains strong.

The SPA structure remains attractive for the

development of new businesses.

Groups are continuing to access the market

initially at member level, supporting third

party syndicates.

Brexit

© Lloyd’s

8

Why do we need the Lloyd’s Brussels subsidiary?GWP(1) (EUR MN)

© Lloyd’s

1,445

1,447

1,202

2,891

1,202

Note: (1) based on 2016 EEA GWP, excluding Life

Accessible

Reverse solicitation

Prohibited

Accessible via LIC

Do nothing – World Trade Organisation Rules Lloyd’s Insurance Company

9

.

• Lloyd’s Brexit lobbying position: continued trade with Single Market. No ‘hard Brexit’, transitional arrangements instead. Ongoing engagement with UK Government

• Brussels Subsidiary will be a fully fledged Insurance Company, fully regulatory and tax compliant

• Allows continued trading under the Lloyd’s brand and benefiting from Lloyd’s robust financial ratings

• Maximum Reinsurance back to syndicates (100%)

• Initial capital injection from Society of Lloyd’s

Timeline of the Lloyd’s Brussels subsidiary

Lloyd’s

October 2017Regulatory application submitted

July 2018Operationally ready

and regulatory authorisation

received

Q2 2018Market onboarding

Q4 2017Company set-up 1 Jan 2019

March 2019UK exits EU

Timeline:

Live Trading Q3 2018Business

processing

© Lloyd’s

Oversight

© Lloyd’s

11

Risk Appetite Framework

Key Corporation risk Market oversight risk

Corporation purpose:

Board level Tier 1 metrics

Pillar: Sustainability

Strategic, Group, Insurance, Credit

Pillar: Solvency

Market, Liquidity

Pillar: Operational

Reputation, Legal & Reg, Conduct

Under our trusted name, the Corporation acts to create and maintain a competitive, innovative and secure market. Our dedicated people serve to protect and promote the interests of the market and its policyholders, provide valued services to market participants and advance the interests of

capital providers over the long term

Delivery metrics

Monitoring metrics

Attractiveness of Lloyd’s Market

Underwritingprofitability

Syndicate capability

Liquidity

Reinsurance failure

Catastrophe exposure

Reserve deterioration

Central Fund investment

Operational effectiveness

Financial crime and sanctions

Regulatory, legal & tax compliance

Conduct

Cyber (data protection and

theft)

Risk objective: Management of financial risks ensures that Lloyd’s is not exposed to undue

concentration and is able to withstand an extreme event & trade forward

Risk objective: Risk of operational and other events is managed to ensure Lloyd’s

maintains its strong reputation

Risk objective: Lloyd’s strategy must deliver a sustainable business model over the

medium term

Board reporting dashboard = 13 key metricsLloyd’s has redeveloped the risk appetite framework

© Lloyd’s

12

Performance Management – four priorities

© Lloyd’s

Operating expenses

Market facilities

Acquisition costs

Catastrophe cover

13

Approach to business planning

© Lloyd’s

Focus on combined ratio

20

13

act

ua

l

20

14

act

ua

l

20

15

act

ua

l

20

16

act

ua

l

20

17

pla

n

20

18

pre

HIM

pla

n

20

18

po

stH

IM p

lan

Entry = closing a performance gap

High-level plan

New timetable: staggered deadlines

Direct presentations to CPG

Pre HIM

Post HIM

Rate vs exposure changes

Capital

© Lloyd’s

15

Lloyd’s capital base is diversifying in line with our strategy

© Lloyd’s

US Insurance Industry

2011 – 23.1%2017 – 18.8%

UK Insurance Industry 2011 – 22.6%2017 – 13.0%

Japan Insurance Industry

2011 – 5.5%2017 – 13.7%

Bermuda Insurance Industry

2011 – 18.2%2017 – 15.9%

European Insurance Industry 2011 – 4.7%2017 – 11.5%

Middle/Far East Insurance Industry

2011– 0.4%2017 – 2.8%

Private Capital 2011 – 12%2017 – 10.2%

Worldwide Non-Insurance 2011 – 8.1%2017 – 4.2%

Rest of World Insurance Industry 2011 – 5.5%2017 – 9.8%

Other Capital Sources:

16

Strong and Flexible Capital Structure:

All premiums received by a syndicate are held in its premium trust funds and are the first resource for paying policyholder claims from that syndicate.

Each member provides Capital to support its underwriting at Lloyd’s. Each managing agent produces its own capital assessment in respect of each managed syndicate stating how much capital it considers is needed to cover its underlying business risks with a 99.5% confidence level.

The central assets are available at the discretion of the Council of Lloyd’s to meet any valid claim that cannot be met by the resources of any member. It is funded by members’ annual contributions and subordinated debt issued by the Society in 2014 and 2017.

3

2

1severalAssets

Syndicate level Assets£52,983m

Callable layer(≤ 3%) 2

£875m

Subordinated Debt/Securities £792m

Central Fund £2,030mCorporation Net assets1

Members Funds at Lloyd’s (FAL)£22,291m

SecondLink

Firstlink

ThirdLink

mutualAssets

Lloyd’s “Chain of Security”

Cla

ims/ Losses

1) Corporation net assets: Corporation Reserves, Associates Reserve, Revaluation Reserve, Translation Reserve; 2) Callable layer: Central Fund assets may be supplemented by a ‘callable layer’ of up to 3% of members’ overall premium limits in any one calendar year. These funds would be drawn from premium trust funds. Source: Lloyd’s pro forma financial statements, 30 June 2017

£83m

17

Balance sheet

Balance sheet

£m December 2014 December 2015 December 2016 June 2017

Cash and investments 54,889 56,900 67,646 65,941

Reinsurers’ share of unearned premiums 1,976 2,368 3,110 4,422

Reinsurers’ share of claims outstanding 8,785 8,610 11,310 11,963

Other assets 14,063 15,751 19,536 23,122

Total assets 79,713 83,629 101,602 105,448

Gross unearned premiums (12,652) (13,723) (16,548) (19,212)

Gross claims outstanding (38,134) (38,833) (47,747) (47,373)

Other liabilities (5,514) (5,975) (8,710) (10,884)

Net resources 23,413 25,098 28,597 27,979

Member assets 20,835 22,453 25,718 25,074

Central assets1 2,578 2,645 2,879 2,905

Source: Lloyd’s pro forma financial statements, 30 June 2017. 1Central assets are the net assets of the Society including the Central Fund, excluding subordinated debt liabilities and the callable layer.

December 2014 – HY 2017

18

Lloyd’s financial strength ratings are strong

© Lloyd’s

Source: S&P Research update October 2017, S&P Full Rating Report September 2017, Fitch Ratings Press Release October 2017, Fitch Ratings Full Rating Report July 2017, A.M. Best press release July 2017, Best’s Rating of Lloyd’s 2017, September 2017

Ratings Standard & Poor’s Fitch Ratings A.M. Best

Insurer financial strength (IFS)

Affirmed October 2017Negative outlook

Affirmed October 2017Negative outlook

Affirmed July 2017Stable outlook

Subordinated debt rating

A- A- a-

Key strengthsquoted by the rating agency

• Very strong competitive position with wide geographic and product coverage

• Very strong capital and earnings and strong financial flexibility

• Strong risk controls, risk culture and risk management

• Very strong business profile and strong market performance

• Strong and well structured risk management framework

• Strong member and central capital

• Strong and stable risk-adjusted capitalisation

• Good financial flexibility

• Strong underwriting performance

• Excellent business profile

IFS Ratings

AA-

A+

A

A-

BBB+

S&P

2011 2012 2013 2014 2015 2016 2017

Fitch

AM Best

A+(Strong)

AA-(Very strong)

A(Excellent)

19

500300

0

100

200

300

400

500

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Nominal value (£m)

Lloyd’s Tier 2 subordinated debt outstanding

Debt Profile

Issue Date Issuer StatusBond Rating (S&P/Fitch)

CurrencyAmount Issued (£m)

Amount Outstanding

(£m)

Coupon (%)

First Call Date

Maturity Date

07 Feb ‘17Society of

Lloyd’sTier 2 A-/A- GBP 300 300 4.875 07 Feb ‘27 07 Feb ‘47

30 Oct ‘14Society of

Lloyd’sTier 2 A-/A- GBP 500 500 4.750 N/A 30 Oct ‘24

N.B.: Chart shows bonds at the earlier of maturity and first call date

© Lloyd’s

20

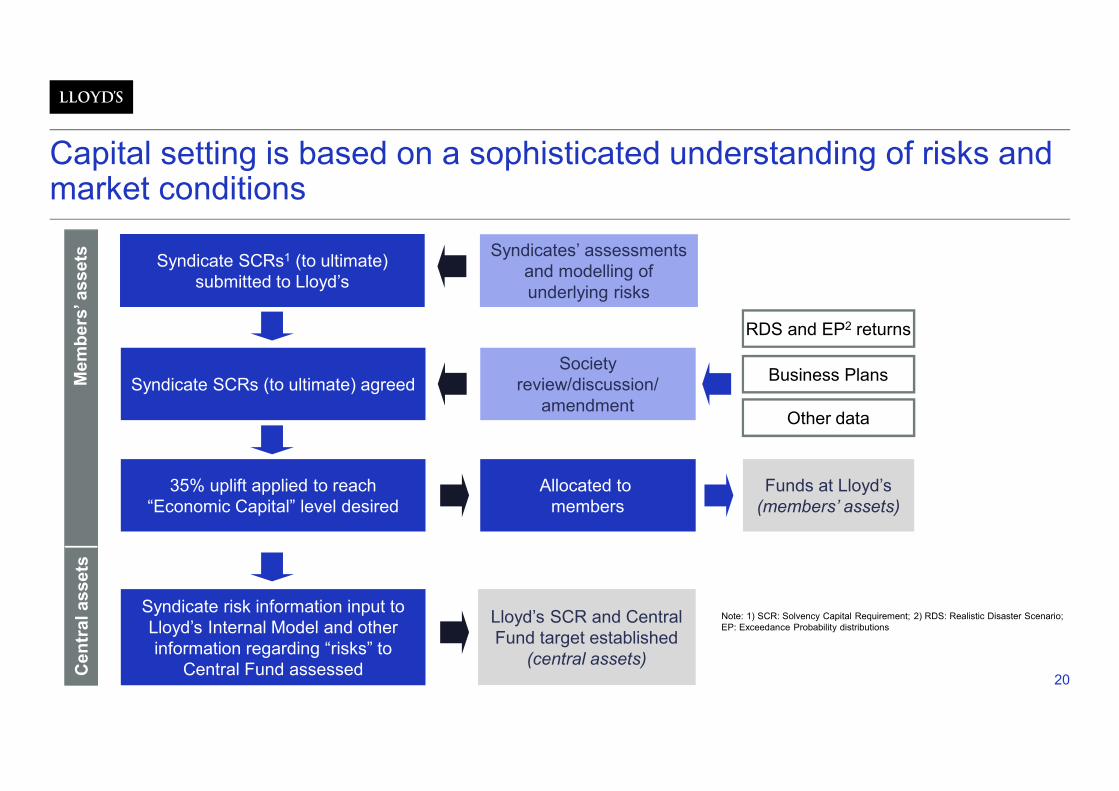

Capital setting is based on a sophisticated understanding of risks and market conditions

Syndicate risk information input toLloyd’s Internal Model and other information regarding “risks” to

Central Fund assessed

35% uplift applied to reach“Economic Capital” level desired

Syndicate SCRs (to ultimate) agreed

Syndicate SCRs1 (to ultimate) submitted to Lloyd’s

Allocated to members

Lloyd’s SCR and Central Fund target established

(central assets)

Funds at Lloyd’s(members’ assets)

Societyreview/discussion/

amendment

RDS and EP2 returns

Business Plans

Other data

Syndicates’ assessments and modelling of underlying risks

Mem

bers

’ assets

Cen

tral assets

Note: 1) SCR: Solvency Capital Requirement; 2) RDS: Realistic Disaster Scenario; EP: Exceedance Probability distributions

21

How does Lloyd’s calculate and cover solvency?

© Lloyd’s

Under Solvency II the Solvency Capital Requirement (SCR) must be calculated

Sufficient capital to cover a 1 in 200 year loss event for the entity over a one year time period

Lloyd’s calculates two SCRs

Both the Lloyd’s MWSCR and CSCR are calculated using Lloyd’s Internal Model

Solvency also assessed at the member level

SCR Scope of calculation Capital available to cover SCR

Lloyd’s Market Wide SCR (MWSCR)

Covers whole Lloyd’s market All capital held at Lloyd’s including syndicate assets, member level capital and central capital

Lloyd’s Central SCR (CSCR) Covers central risks only, in particular risk that members may not have enough capital to meet losses (and thus hit Central Fund)

Central capital – mainly the Central Fund

22

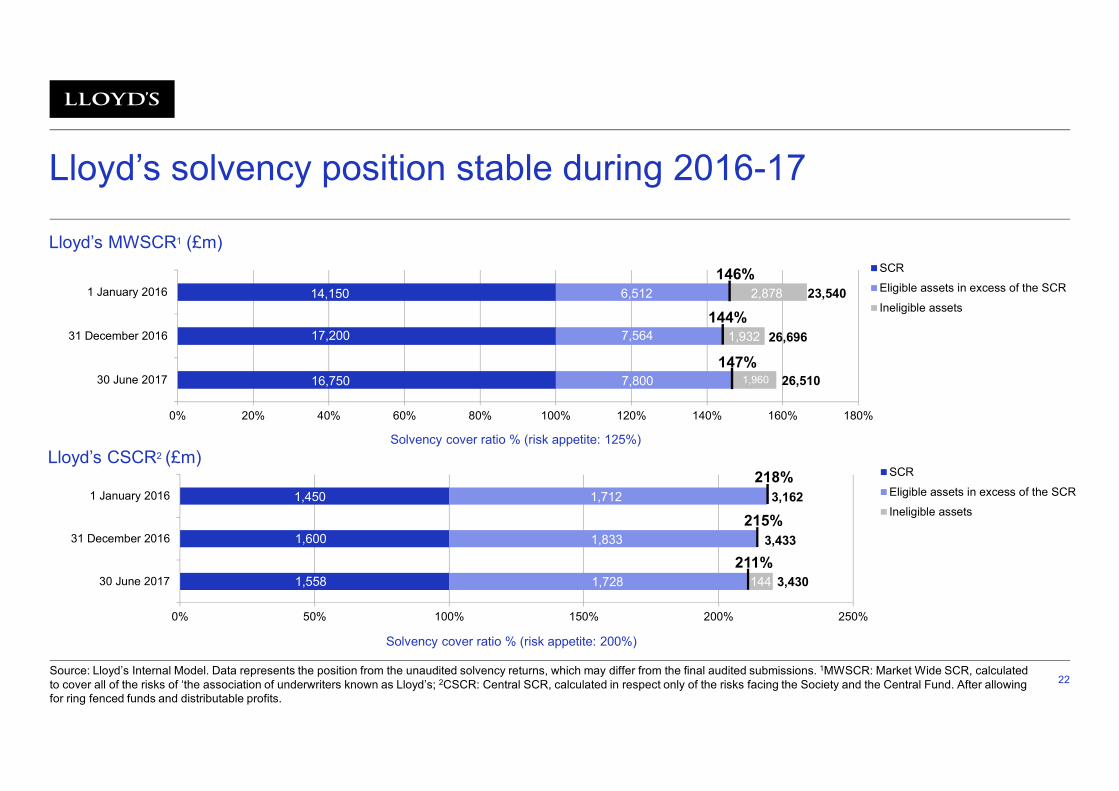

Lloyd’s solvency position stable during 2016-17

Source: Lloyd’s Internal Model. Data represents the position from the unaudited solvency returns, which may differ from the final audited submissions. 1MWSCR: Market Wide SCR, calculated to cover all of the risks of ‘the association of underwriters known as Lloyd’s; 2CSCR: Central SCR, calculated in respect only of the risks facing the Society and the Central Fund. After allowing for ring fenced funds and distributable profits.

0% 20% 40% 60% 80% 100% 120% 140% 160% 180%

30 June 2017

31 December 2016

1 January 2016

SCR

Eligible assets in excess of the SCR

Ineligible assets

Lloyd’s MWSCR1 (£m)

147%

144%

0% 50% 100% 150% 200% 250%

30 June 2017

31 December 2016

1 January 2016

SCR

Eligible assets in excess of the SCR

Ineligible assets

Lloyd’s CSCR2 (£m)218%

211%

26,510

1,932

7,800

7,564

1,558 3,430

1,600

1,960

3,4331,833

1,728

17,200

16,750

26,696

Solvency cover ratio % (risk appetite: 125%)

Solvency cover ratio % (risk appetite: 200%)

144

146%14,150 6,512 2,878 23,540

1,450 1,712 3,162

215%

23

Industry wide insured catastrophe losses Lloyd’s major claims1

Major claims < 5% of industry wide insured cat losses (to June)

GBP bnUSD bn

Note: 1) Indexed for inflation to 2016. Claims in other currencies translated at the exchange rate prevailing at the date of loss. Source: Swiss Re Sigma Report 2016, Lloyd’s Annual Report 2016 & Lloyd’s Interim Report 2017

0

1

2

3

4

5

6

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017H1

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

24

Impact of natural catastrophes in H2

© Lloyd’s

Industry estimates still vary widely

Significant industry losses

Market-turning event?

Earnings event?

Capital event?

It’s not only Harvey, Irma and Maria

USD Billions Industry loss estimates

EventLloyd’s net

claims estimatesLow range estimate

High range estimate

Harvey 1.8 7.5 35

Irma 2.1 32 55

Maria 0.9 15 40

Total 4.8 54.5 130

25

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

All othersyndicates

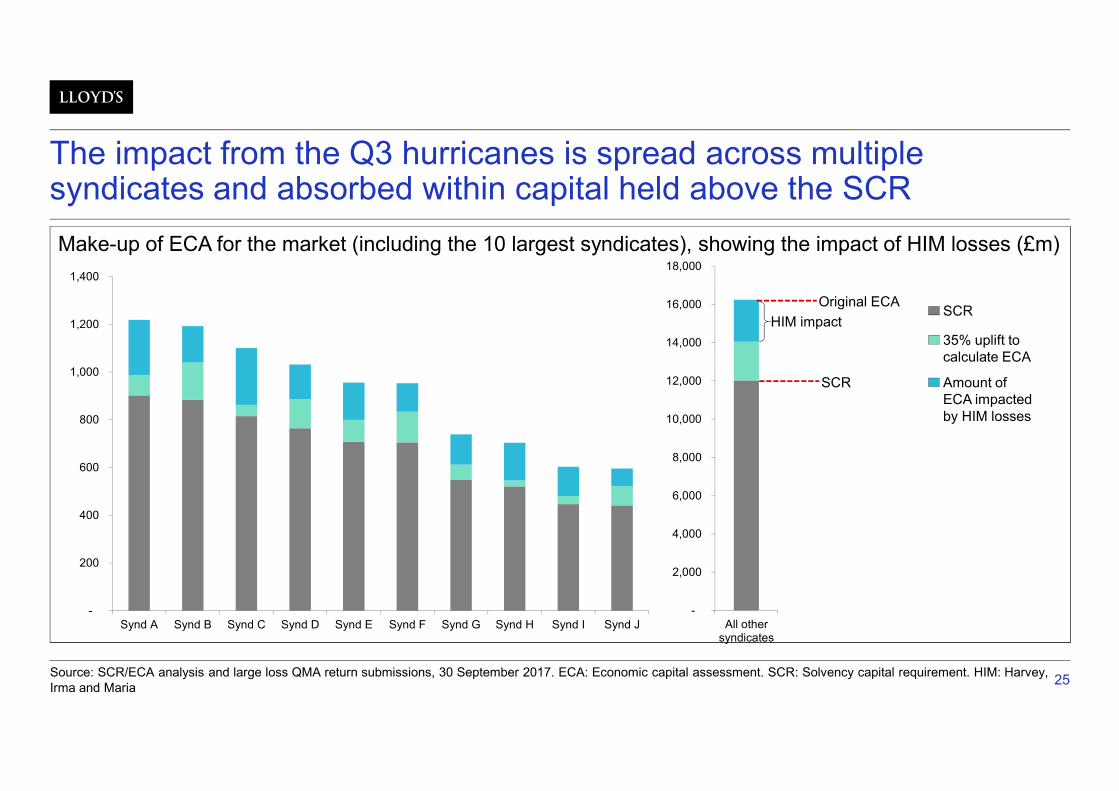

The impact from the Q3 hurricanes is spread across multiple syndicates and absorbed within capital held above the SCR

Make-up of ECA for the market (including the 10 largest syndicates), showing the impact of HIM losses (£m)

Source: SCR/ECA analysis and large loss QMA return submissions, 30 September 2017. ECA: Economic capital assessment. SCR: Solvency capital requirement. HIM: Harvey, Irma and Maria

SCR

SCR

Original ECA

35% uplift to calculate ECA

Amount of ECA impacted by HIM losses

HIM impact

-

200

400

600

800

1,000

1,200

1,400

Synd A Synd B Synd C Synd D Synd E Synd F Synd G Synd H Synd I Synd J

26

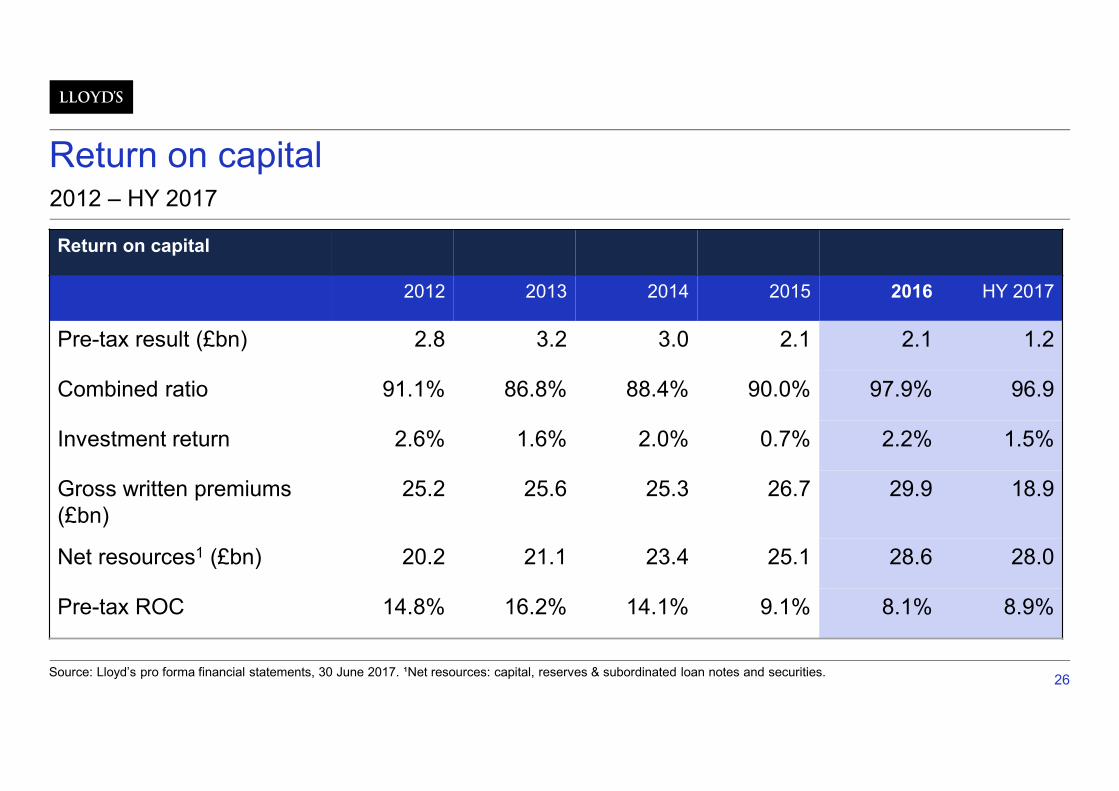

Return on capital

Return on capital

2012 2013 2014 2015 2016 HY 2017

Pre-tax result (£bn) 2.8 3.2 3.0 2.1 2.1 1.2

Combined ratio 91.1% 86.8% 88.4% 90.0% 97.9% 96.9

Investment return 2.6% 1.6% 2.0% 0.7% 2.2% 1.5%

Gross written premiums (£bn)

25.2 25.6 25.3 26.7 29.9 18.9

Net resources1 (£bn) 20.2 21.1 23.4 25.1 28.6 28.0

Pre-tax ROC 14.8% 16.2% 14.1% 9.1% 8.1% 8.9%

Source: Lloyd’s pro forma financial statements, 30 June 2017. ¹Net resources: capital, reserves & subordinated loan notes and securities.

2012 – HY 2017

ILS Opportunity (?)

© Lloyd’s

28

Current Lloyd’s capital structure

© Lloyd’s

Reminder

Central Fund (Discretionary) – Use requires cessation of Lloyd’s underwriting

SCR(U) as ECU: +35%

SCR(U): 100%

(Graphic represents the notional syndicate level stack)

29

Where would an ILS sit in Lloyd’s capital structure?

© Lloyd’s

Central Fund (Discretionary)

SCR(U) as ECU: +35%

SCR(U): 100%

(Graphic represents the notional syndicate level stack)

Potential ILS layers?

30

Insurance Risk dominates Lloyd’s SCR

Catastrophe risk30%

Non-Cat Premium risk37%

Reserving risk22%

Market risk2%

RI credit risk5%

Additional Central Fund risk2%

Operational risk2%

2017 SCR

Insurance risk 89% of total

© Lloyd’s

31

Lloyd’s solvency Q2 2017; current Central Assets Central solvency ratio

Tier 1 Tier 2 Tier 3 Total

£m £m £m £m

Society assets:- Subordinated debt (valued at fair value)1

- Deferred tax- Balance of net assets (net of Lloyd’s China provision)

Callable layer (available at the 1:200 year stress level)

1,827

680

88835

88835

1,827

680

Total central own funds available to meet the central SCR 2,507 888 35 3,430

Lloyd’s central SCR 1,558

‘Excess’ central own funds not eligible to meet central SCR - 109 35 144

Total central own funds eligible to meet the central SCR(Tier 2 and 3 assets can only cover up to 50% of central SCR)

2,507 779 - 3,286

Lloyd’s central solvency ratio 211%

(1) The 2014 and 2017 dated debt is Tier 2

32

Historical experience shows cash requirements lag declaration of losses to Central Fund…

0

200

400

600

800

1,000

1,200

1,400

1,600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

£m

Net Paid Forecast drawdowns

Improved £578m

Source: Central Fund Accounts Dec 10 / Central Fund Modelling System

33

… and recent experience has minimal Central Fund losses

© Lloyd’s

-10

-5

0

5

10

15

20

25

2011 2012 2013 2014 2015 2016 2017

Ne

t lo

sse

s to

Ce

ntr

al F

un

d (

£m

)

All relates to 2007 & prior. No new hits 2008 to date

Nil Nil

34

Some rebuttable assumptions…

Central Fund solvency coverage meets risk appetite and supports the target Ratings

Central Fund exposure / concern is insurance risk…

…and is split roughly equally across natural catastrophe, other premium risk and reserve risk

Tier 2 allowance is maxed out

Restricted Tier 1 debt issue an option…

…to weigh against an ILS issue

Gearing and coupon / premium cover not a concern

© Lloyd’s

35

Key considerations for supplementing Central Assets

Cash v solvency

Post loss adequacy – second loss response?

Actual hit to CF or to benefit of members who trade forward?

Cat cover only or all insurance risks?

Multi year…run-off / collateral retention?

© Lloyd’s