loan% - michigan credit union · pdf fileloan% documentation%...

TRANSCRIPT

Loan Documentation Michigan Credit Union League – Lending & Marke5ng Conference February 11, 2015

Introduction

• Mostly, loan documents will never be needed.

• Borrower in financial crisis may lead to: • A line of creditors wan5ng to be paid • The necessity of following the leKer of the documents

• Collec5on vs. Charge Off • Loans documented by bank personnel may be tested by legal counsel who aKempt to expose deficiencies and challenge the lender’s posi5on

• The only strength the lender has is the efficiency and effec(veness of its documenta5on

• So, appropriate loan documenta5on is cri5cal to our success as lenders.

Ronn

ie L. B

oling -‐ 2

015

2

Balance Sheet

Ronnie L. Boling -‐ 2011 3

A Lending Ins(tu(on

Ronn

ie L. B

oling -‐ 2

015

3

Income Statement

Ronnie L. Boling -‐ 2011 4

Source of Income -‐ Lending

Ronn

ie L. B

oling -‐ 2

015

4

Lending – The Big E’s

• Effec(veness • Efficiency

Ronn

ie L. B

oling -‐ 2

015

5

The Bo'om Line

Given enhanced compe55on, shrinking margins, and a somewhat erra5c economy, success or failure of the financial ins5tu5on will greatly depend on its documenta5on of the loan porVolio. We must get it right!

Ronn

ie L. B

oling -‐ 2

015

6

Training Is Key

• Lending Officers • Loan Underwriters • Loan Processors • Credit Department Personnel • Senior Management …..We are all in the same boat!

Ronn

ie L. B

oling -‐ 2

015

7

The Uniform Commercial Code & Article 9 • The Uniform Commercial Code (UCC) is the result of an effort to harmonize the law of sales and other commercial transac5ons in all 50 states within the United States of America.

• Has been in effect since the early 1960’s • Ar5cle 9 -‐ Covers security interests in personal property and fixtures

• Adopted in all 50 states • The State of Michigan has adopted all major amendments

Ronn

ie L. B

oling -‐ 2

015

8

Security Interest

• Must be…. • In wri5ng • Authen5cated by the debtor (signed) • Grant a security interest • Describe the debt • Describe the collateral being offered. • AKached

• The Security Agreement must be valid • Secured party must give value (i.e. a loan) • The debtor must have rights to the collateral

• Perfected…

Ronn

ie L. B

oling -‐ 2

015

9

Ronn

ie L. B

oling -‐ 2

015

10

Security Interest – Perfection • Pledge • Automa5c Perfec5on • Purchase money security interest • Security interest in proceeds

• Lien Recording – Titled Goods • Control • Filing – UCC-‐1 Financing Statement

Ronn

ie L. B

oling -‐ 2

015

11

CONTRACTS USED IN COMMERCIAL LENDING

Ronn

ie L. B

oling -‐ 2

015

12

Contracts

• A promise or a set of promises for breach of which the law gives a remedy or the performance of which the law in some way recognizes a duty.

• May be wriKen or oral….wriKen is easier to prove.

• Must contain…. • An offer and an acceptance • Considera5on – established value • Must be legal Ro

nnie L. B

oling -‐ 2

015

13

Term Sheet

• A non-‐binding document incorpora5ng some of the material terms of the loan but not a binding document to lend money.

• Used to nego5ate in the early stages of the lending process.

Ronn

ie L. B

oling -‐ 2

015

14

This Proposal cons5tutes only a general, non-‐binding expression of interest on part of Bank. THIS PROPOSAL IS SUBJECT TO BANK’S CREDIT, LEGAL, AND INVESTMENT APPROVAL PROCESS AND IS NOT INTENDED TO AND DOES NOT CREATE A LEGALLY BINDING COMMITMENT OR OBLIGATION ON PART OF BANK. The crea5on of such a legally binding commitment or obliga5on is subject to, among other things, the comple5on by Bank of an in-‐depth inves5ga5on of the proposed investment, the results of which are deemed sa5sfactory by Bank and the nego5a5on, execu5on and delivery of defini5ve documents which are mutually agreed upon by borrow and Bank and no occurrence of a material adverse change in business, financial condi5on, or prospect of borrower or any guarantor. This proposal is provided solely for your benefit and shall not be reproduced, distributed, quoted, or otherwise made reference to except between the senior management, officers and legal counsel of the borrower. Please review and sign and send back to Bank.

Ronn

ie L. B

oling -‐ 2

015

15

Commitment Letter

• The purpose is to set forth the basic commitment of the financial ins5tu5on to lend money and the requirements of the borrower as far as repayment and security.

• Components • The par5es • Type and purpose of the loan • Amount of the lender’s commitment • Interest and other compensa5on to the lender • Repayment and prepayment provisions • Collateral (if any) • Condi5ons precedent to lending • Representa5ons and warran5es • Affirma5ve covenants • Nega5ve covenants • Financial covenants

• Every element of the loan must be set forth

Ronn

ie L. B

oling -‐ 2

015

16

Ronn

ie L. B

oling -‐ 2

015

17

Authority to Borrow

• Establishes who is authorized to borrow on behalf of the business en5ty.

• Components • Iden5fica5on of borrower • Name of person’s authorized to execute documents

• Signed by corporate officers • General or specific to a certain transac5on

Ronn

ie L. B

oling -‐ 2

015

18

Corporate Resolu(on RESOLVED, that the of the Corpora5on is authorized, for the account of this Corpora5on, and on such terms and condi5ons as he/she/they may deem proper, to borrow from (Financial Ins5tu5on) sums of money; and to sign, execute, and endorse all such documents as may be required by said bank to evidence such indebtedness; to discount or rediscount with said bank any of the bills receivable owned by this Corpora5on; to apply for and obtain from said bank leKers of credit, and to execute agreements to secure said bank in connec5on therewith, to pledge and/or mortgage any moneys on deposit or any moneys otherwise in the possession of said band, and/or any bonds, stocks, receivables, or other property of this Corpora5on, to secure the payment of any indebtedness, liability, or obliga5on of this Corpora5on to said bank whether now due or to become due and whether exis5ng or hereaper incurred, to withdraw and/or subs5tute any property held at any 5me by said bank as collateral, and to sign and execute trust receipts for the withdrawal of same when required; and generally to do and perform all acts and sign all agreements, obliga5ons, pledges, and/or other instruments necessary or required by said bank. The undersigned hereby cer5fies that he/she is the duly elected and qualified Secretary and the custodian of the books and records and seal of ,a corpora5on duly formed pursuant to the laws of the state of and that the foregoing is a true record of a resolu5on duly adopted at a mee5ng of the and that said mee5ng was held in accordance with state law and the Bylaws of the above-‐named Corpora5on on ,and that said resolu5on is now in full force and effect without modifica5on or rescission. IN WITNESS WHEREOF, I have executed my name as Secretary and have hereunto affixed the corporate seal of the above-‐named Corpora5on this ____ , of ___________________., 2015 Secretary ________________________________

Ronn

ie L. B

oling -‐ 2

015

19

Promissory Note

• The primary document that evidences the borrower’s indebtedness to the financial ins5tu5on.

• Components • Iden5fica5on of borrower • Amount of the loan / credit line • Iden5fica5on of payee • Interest rate provisions • Repayment agreement • Defini5on of events of default and remedies Ro

nnie L. B

oling -‐ 2

015

20

Loan Agreement

• A detailed statement of the borrower’s obliga5on to repay the loan, provide security for repayment and to perform its opera5ons during the term of the loan in specific ways as requested by the financial ins5tu5on and agreed to by the borrower.

• Components • Amount of the loan, repayment terms and interest rate

• Collateral • Condi5ons precedent – things that must be accomplished before the loan or advanced sre made

• Borrower’s representa5ons and warran5es • Environmental covenants • Affirma5ve and nega5ve covenants • Financial covenants • Default provisions and remedies • Jurisdic5on provisions

Ronn

ie L. B

oling -‐ 2

015

21

Security Agreement

• Gives the lender a security interest in the collateral described in the agreement.

• Components: • In wri5ng • Authen5cated by the debtor • Describe the collateral • Specifically grants a security interest • Describes the obliga5on being secured • Date of execu5on • Representa5ons and warran5es • Events of default • Remedies of the lender • Loca5on of the collateral • Insurance requirements • Environmental provisions

Ronn

ie L. B

oling -‐ 2

015

22

Guaranty Agreement

• Creates a binding contract whereby the guarantor is obligated to repay the loan in the event the debtor defaults on the obliga5on

• Components: • Descrip5on of the debt to be paid • Iden5fica5on of the party whose debt is being paid

• Iden5fies the party receiving payment in the event of default Ro

nnie L. B

oling -‐ 2

015

23

Pledge / Security Agreement • Creates a perfected security interest in collateral possessed by the financial ins5tu5on

• Components: • Descrip5on of the collateral • Iden5fica5on of party holding collateral (financial insitu5on)

• Financial ins5tu5on’s commitment to preserve the collateral

• Lender’s right to sell or dispose of the collateral

Ronn

ie L. B

oling -‐ 2

015

24

The Financing Statement – UCC1 • Exists as a means of perfec5ng a security interest in collateral

• Must contain: • Name of debtor • Name of secured party • Descrip5on of collateral • Date of execu5on

• UCC11 • Search for exis5ng liens

• UCC3 • Con5nua5on • Amendment • Release

Ronn

ie L. B

oling -‐ 2

015

25

Ronn

ie L. B

oling -‐ 2

015

26

Ronn

ie L. B

oling -‐ 2

015

27

Ronn

ie L. B

oling -‐ 2

015

28

Deed of Trust / Mortgage • Secure a lien on real estate • Components: • Mortgagor • Mortgagee • Grant of security interest in trust • Descrip5on of real estate • Descrip5on of debt • Representa5ons and warran5es • Events of default and remedies of mortgagee • Environmental covenants

Ronn

ie L. B

oling -‐ 2

015

29

Assignment of Life Insurance • Assigns proceeds from life insurance as collateral to secure a debt

• Lender holds policy and has assignment acknowledged by life insurance company.

Ronn

ie L. B

oling -‐ 2

015

30

Trust Receipt

• Lender agrees to release collateral “in trust” to the borrower for some specific purpose and the borrower agrees to return it by a specified period of 5me.

Ronn

ie L. B

oling -‐ 2

015

31

Ronn

ie L. B

oling -‐ 2

015

32

Delivery Agreement

• Borrower agrees to deliver collateral to lender at a specified 5me.

Ronn

ie L. B

oling -‐ 2

015

33

REGULATIONS

Ronn

ie L. B

oling -‐ 2

015

34

The Fences: Regulations • The Equal Credit Opportunity Act (ECOA) is a United States law (codified

at 15 U.S.C. § 1691 et seq.), enacted in 1974, that makes it unlawful for any creditor to discriminate against any applicant, with respect to any aspect of a credit transaction, on the basis of race, color, religion, national origin, sex, marital status, or age (provided the applicant has the capacity to contract);[1] to the fact that all or part of the applicant’s income derives from a public assistance program; or to the fact that the applicant has in good faith exercised any right under the Consumer Credit Protection Act. The law applies to any person who, in the ordinary course of business, regularly participates in a credit decision, including banks, retailers, bankcard companies, finance companies, and credit unions.

• Failure to comply with the Equal Credit Opportunity Act's Regulation B can subject a financial institution to civil liability for actual and punitive damages in individual or class actions. Liability for punitive damages can be as much as $10,000 in individual actions and the lesser of $500,000 or 1 percent of the creditor’s net worth in class actions.[2]

• The Truth in Lending Act (TILA) of 1968 is a United States federal law designed to promote the informed use of consumer credit, by requiring disclosures about its terms and cost to standardize the manner in which costs associated with borrowing are calculated and disclosed. [1]

• TILA also gives consumers the right to cancel certain credit transactions that involve a lien on a consumer's principal dwelling, regulates certain credit card practices, and provides a means for fair and timely resolution of credit billing disputes. With the exception of certain high-cost mortgage loans, TILA does not regulate the charges that may be imposed for consumer credit. Rather, it requires uniform or standardized disclosure of costs and charges so that consumers can shop. It also imposes limitations on home equity plans that are subject to the requirements of Sec. 226.5b and certain higher-cost mortgages that are subject to the requirements of Sec. 226.32. The regulation prohibits certain acts or practices in connection with credit secured by a consumer's principal dwelling.

Ronn

ie L. B

oling -‐ 2

015

35

Regulations (cont’d.) • The Fair Credit Reporting Act (FCRA) is a United States federal law

(codified at 15 U.S.C. § 1681 et seq.) that regulates the collection, dissemination, and use of consumer information, including consumer credit information.[1] (Full Statute (PDF).) Along with the Fair Debt Collection Practices Act (FDCPA), it forms the base of consumer credit rights in the United States. It was originally passed in 1970,[2] and is enforced by the US Federal Trade Commission and private litigants.

• he Community Reinvestment Act (CRA, Pub.L. 95-128, title VIII of the Housing and Community Development Act of 1977, 91 Stat. 1147, 12 U.S.C. § 2901 et seq.) is a United States federal law designed to encourage commercial banks and savings associations to help meet the needs of borrowers in all segments of their communities, including low- and moderate-income neighborhoods.[1][2][3] Congress passed the Act in 1977 to reduce discriminatory credit practices against low-income neighborhoods, a practice known as redlining.[4][5]

• The Act requires the appropriate federal financial supervisory agencies to encourage regulated financial institutions to help meet the credit needs of the local communities in which they are chartered, consistent with safe and sound operation (Section 802.) To enforce the statute, federal regulatory agencies examine banking institutions for CRA compliance, and take this information into consideration when approving applications for new bank branches or for mergers or acquisitions (Section 804.)[6]

• The Real Estate Settlement Procedures Act (RESPA) was created because various companies associated with the buying and selling of real estate, such as lenders, real estate agents, construction companies and title insurance companies were often engaging in providing undisclosed kickbacks to each other, inflating the costs of real estate transactions and obscuring price competition by facilitating bait-and-switch tactics. It requires lenders to provide a good faith estimate (GFE) for all the approximate costs of a particular loan and finally a HUD-1 (for purchase real estate loans) or a HUD-1A (for refinances of real estate loans) at the closing of the real estate loan. The final HUD-1 or HUD-1A allows the borrower to know specifically the costs of the loan and to whom the fees are being allotted.

Ronn

ie L. B

oling -‐ 2

015

36

Regulations (cont’d.) • The United States Home Mortgage Disclosure Act (or HMDA, pronounced

HUM-duh) was passed in 1975. It requires financial institutions to maintain and annually disclose data about home purchases, home purchase pre-approvals, home improvement, and refinance applications involving 1 to 4 unit and multifamily dwellings. It also requires branches and loan centers to display a HMDA poster.[1]

• HMDA was designed by the Federal Reserve Board in order to:

• Help public officials to distribute public-sector investments• Discover if financial institutions are serving housing needs of communities• Identify where there are discriminatory lending practices• Home Ownership Equity Protection Act: n July 14, 2008 the Board of

Governors of the Federal Reserve (Fed) released new rules under the Truth in Lending Act (TILA) - Regulation Z. The rule seeks to protect consumers from unfair and deceptive acts and practices.

• The rule provides protections by establishing a new category of "higher-priced mortgage loans" defined as closed-end consumer credit transactions secured by the consumer's principal dwelling where the Annual Percentage Rate (APR) on the loan exceeds the rate on a Treasury security with a comparable maturity by 3%. This would include purchase loans, refinancings of such loans, and home equity loans, but would exclude loans for vacation properties, open-end home-equity plans, reverse mortgages, or construction-only loans.

• Additionally, the rule requires earlier consumer disclosures for closed end mortgages secured by a principal dwelling and prohibits: certain acts of or practices for "higher priced" or subprime mortgage loans and loans that meet HOEPA's cost triggers; other acts or practices for all closed-end credit transactions secured by a consumer's principal dwelling; and certain misleading or deceptive advertising practices in connection with closed-end mortgages.

Ronn

ie L. B

oling -‐ 2

015

37

Regulations (cont’d.) • The United States Home Mortgage Disclosure Act (or HMDA, pronounced

HUM-duh) was passed in 1975. It requires financial institutions to maintain and annually disclose data about home purchases, home purchase pre-approvals, home improvement, and refinance applications involving 1 to 4 unit and multifamily dwellings. It also requires branches and loan centers to display a HMDA poster.[1]

• HMDA was designed by the Federal Reserve Board in order to:

• Help public officials to distribute public-sector investments• Discover if financial institutions are serving housing needs of communities• Identify where there are discriminatory lending practices• Home Ownership Equity Protection Act: n July 14, 2008 the Board of

Governors of the Federal Reserve (Fed) released new rules under the Truth in Lending Act (TILA) - Regulation Z. The rule seeks to protect consumers from unfair and deceptive acts and practices.

• The rule provides protections by establishing a new category of "higher-priced mortgage loans" defined as closed-end consumer credit transactions secured by the consumer's principal dwelling where the Annual Percentage Rate (APR) on the loan exceeds the rate on a Treasury security with a comparable maturity by 3%. This would include purchase loans, refinancings of such loans, and home equity loans, but would exclude loans for vacation properties, open-end home-equity plans, reverse mortgages, or construction-only loans.

• Additionally, the rule requires earlier consumer disclosures for closed end mortgages secured by a principal dwelling and prohibits: certain acts of or practices for "higher priced" or subprime mortgage loans and loans that meet HOEPA's cost triggers; other acts or practices for all closed-end credit transactions secured by a consumer's principal dwelling; and certain misleading or deceptive advertising practices in connection with closed-end mortgages.

Ronn

ie L. B

oling -‐ 2

015

38

Consumer Loans

• Personal • Automobile • Home equity line of credit • Boat • Equipment • Securi5es porVolio • Mortgage

Ronn

ie L. B

oling -‐ 2

015

39

Documentation

• Note, Disclosure and Security Agreement • Perfec5on of Lien • Personal Unsecured • Automobile • Home equity line of credit • Boat • Equipment • Securi5es porVolio • Mortgage

Ronn

ie L. B

oling -‐ 2

015

40

Ronn

ie L. B

oling -‐ 2

015

41

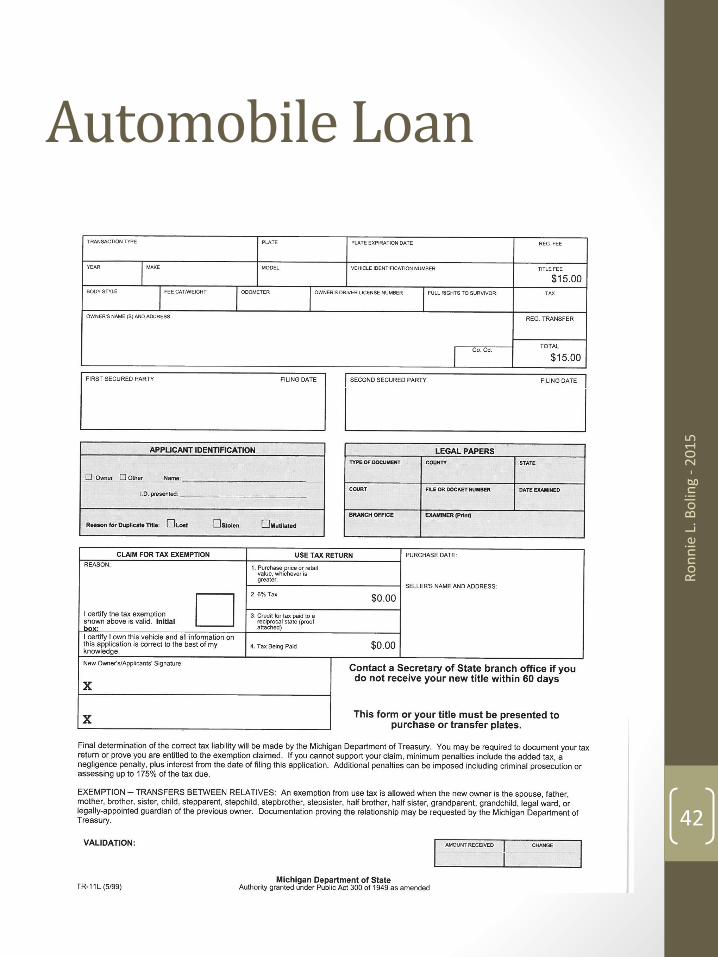

Automobile Loan

Ronn

ie L. B

oling -‐ 2

015

42

Home Equity Line of Credit – Deed of Trust

Ronn

ie L. B

oling -‐ 2

015

43

Boat Loan

• Greater than 25’ is considered a yacht • Lien recorded using a Ships Mortgage via the United States Coast Guard

• Boat and trailer are 5tled vehicles • Motor – file UCC1

Ronn

ie L. B

oling -‐ 2

015

44

Ronn

ie L. B

oling -‐ 2

015

45

Equipment Loan

• Lien perfected by filing a UCC1 • File with Secretary of State • File with County Recorder • File in debtors first name, last name, DBA name, etc.

Ronn

ie L. B

oling -‐ 2

015

46

Securities / Portfolio

Ronn

ie L. B

oling -‐ 2

015

47

Real Estate

• Deed of Trust • Open End vs. Closed End • Title Search to guarantee clear 5tle

Ronn

ie L. B

oling -‐ 2

015

48

Loan Checklist

Ronn

ie L. B

oling -‐ 2

015

49

Be prepared for the worst….leave no room for error!

Ronn

ie L. B

oling -‐ 2

015

50