loan portfolio management – year 1 - graduate … · loan portfolio management – year 1 ......

TRANSCRIPT

Lecture Materials

LOAN PORTFOLIO MANAGEMENT – YEAR 1

Thomas A. Farin Chairman of the Board

FARIN Financial Risk Management Fitchburg, Wisconsin

[email protected] 608-661-4219

August 10, 2016

CREATE SYNERGY. DRIVE PROFITABILITY1

GSB Credit TrackEffective Loan Pricing

Thomas FarinPresident

CREATE SYNERGY. DRIVE PROFITABILITY

Effective Loan Pricing• At school

– Whatweneedtoknowtopricealoan

– Fourdifferentmodelsformakingloanpricingdecisions

• Second two parts when you are working on your intersession project– Session2‐ Pricingindividualloans

– Session3– Pricingdealsandrelationships

2

CREATE SYNERGY. DRIVE PROFITABILITY

Challenges in Asset Selection• Common fear of available

assets– Fixedrate,longerterm

• Interestraterisk– Cappedearnings– Variablefundingcosts

• Creditquality– Borrowerstability migration

• Liquidity

• Concerns with current market– Balloons

• Creditriskatrenewal– Variablerates

• Interestraterisk floors,caps• Creditrisk paymentshock• Prepaymentrisk refinancerisk• Caps?

• Role of Loan Pricing tool in ALCO– Dowesettherateorevaluatetheabilitytooffertheproductatall?

– Attheloanofficerleveltakeallowedassetsandensuresprofitability.

• Loan Pricing options in this section– 1‐4Family– CRE– Ag– Consumer

• Funding options– Funding“gap”– Coredepositvalueinassetselection

– Useofwholesalein“efficientfrontier” model

3

CREATE SYNERGY. DRIVE PROFITABILITY

Optimal Earning Asset Matrix• Every balance

sheet mix carries maximum return\volatility combinations

• Finding your optimal earnings frontier is key to strategic\capital plan– Whatstrategyhashigherearningspotentialandless“risk”

4

Where is your current and projected performance vs. actual?Given your “risk appetite” what is your “domain” of optimal return?

Volatilityofearnings

ROE

CREATE SYNERGY. DRIVE PROFITABILITY

Funds Transfer Pricing Curve• Requires a cost curve for funding costs

• Penalizeslendingfunctionifinefficientatpricingfunds,maycauseoutofmarketratesetting

• Doesnotrewardfundingprovidersforgatheringwellpricedfunding

• FHLB,Jumbo/Brokered/Internet/CDARS/SWAP• Pickclosestmatchtocurveyouwoulduse,andallowedforbyliquidity/fundingpolicies&strategies

5

CREATE SYNERGY. DRIVE PROFITABILITY

6

Non-Rate SettersUse of Pricing Models

• Given others set market rates– Identifywellpricedloans

– Identifypoorlypricedloans

– Aggressivelycompeteforwellpricedloans

– Donotaggressivelycompeteforpoorlypricedloans

• Loan pricing models– MarketView

• Investmentbenchmarks

• Valuation– Balancesheetview

• RAROC– RiskAdjustedReturnonCapital

• ROA‐ Netincomeproduced

CREATE SYNERGY. DRIVE PROFITABILITY

Factors in Pricing Loans• Cash flows, not

maturity– DoyouviewaMortgageBackedsecuritythesamewayasaMunicipalbond?

• Funding costs– Doesyourcurrentcostoffundsmatter?

– Isthatwhatkeepsyoufrommakinglongertermloanswhenratesarelow?

– Potentialfundingcostsarewhatmatters

• Risks to consider– Interestraterisk– cashflows– Creditrisk ALLLandlosses– Servicingcosts

• Origination• Incrementalcostofadditionalservicing

• Directorgeneraloverheadallocations?

– Optionrisk– cashflowvolatility• Prepayment• Caps/floors

– Marketrates?• Competitorsthataremakingbaddecisionsshouldnotbefollowedoverthecliff! 7

CREATE SYNERGY. DRIVE PROFITABILITY

8

Cash Flow and Repricing Characteristics

• Fixed or Variable– OriginationRate– FirstReprice– RepricingRate– RepricingFrequency

• Term or Revolving– Amortizing?– Term– Balloon?

• AmortizationTerm– PrepaymentSpeed

60MonthBulletLoan

CREATE SYNERGY. DRIVE PROFITABILITY9

Loan Pricing – Cash Flows

0

0.5

1

1.5

2

2.5

3

3.5

1 2 3 4 5

Funding Cost

Rates

Match

60 Month Bullet

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

1 6 11 16 21 26 31 36 41 46 51 56

Cum Prin CF

Series1Series2

Considers Interest Cash Flows

60 Month Bullet Loan

CREATE SYNERGY. DRIVE PROFITABILITY10

Loan Pricing – Cash Flows

Match

Considers Interest Cash Flows

60 Month New Car - 20% PP

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

1 6 11 16 21 26 31 36 41 46 51 56

Cum Prin CF

60 Month Amortizing Loanwith 25% annual prepayments

CREATE SYNERGY. DRIVE PROFITABILITY11

Loan Pricing – Cash Flows

Match

Considers Interest Cash Flows& Repricin

5 Year Ballon Mtg - 8% PP

$0$5,000

$10,000$15,000$20,000$25,000$30,000$35,000$40,000$45,000$50,000

1 6 11 16 21 26 31 36 41 46 51 56

Cum Prin CF

0.84

CREATE SYNERGY. DRIVE PROFITABILITY

12

Loan Pricing – Interest Rate Risk

• Interest Rate Risk– Whenyouarepricingloansyouarepricingcashflowsnotmaturities.

– Withfixed‐rateloans,piecesrepriceascashflowscomein.Fewrepriceatmaturity.

– Principalcashflowsareoftenuncertain• Prepaymentoptions

– Variablerateloansreprice• Whencashflowpiecescomein• Whencontractualrepricingoccurs,but…• Variablerateloansmaynotrespondimmediatelyorcompletelyatresetpoints

• Resetfrequency• Restrictionsonadjustments caps

• To manage interest rate risk, institutions need to match funding to the repricing of the loans of loans. Two approaches:– Simplistic– matchbasedonduration– Morecomplex– Matchfundindividualrepricingflows.

– Whileintherealworldyoumaynotmatch,inmakingpricingdecision,weshouldassumematching.x

x

X– Approachtakeninthiscourse

CREATE SYNERGY. DRIVE PROFITABILITY

13

Market Curve UsageCurveNo CurveName

1 US Treasury5 Prime6 Fed Funds9 Balloon MBS

10 Libor14 FHLMC FR MBS16 UST Strip20 FNMA FR MBS21 GNMA FR MBS29 Interest Rate Swap37 Indexed AAA Corporate Bon40 AAA Auto Index66 11th District COFI84 Average FHLB ADV87 Cost of Savings Index90 Indexed AAA MUNI Bond91 Indexed Agency Bond95 National COFI98 REPO (Overnight)99 Retail CD Avg

100 US CMT (H.15)119 AAA Commercial Equipmen126 Indexed A Corporate Bond127 Indexed B Corporate Bond128 Indexed A- MUNI Bond134 FR MBS137 Balloon MBS Synthetic138 GNMA II ARMS

• Curves Used for– RiskFreeCurves– InvestmentBenchmarks– WholesaleFundingCurves

• Requirements– Broadrangeofbenchmarks.– Updatedveryfrequently

CREATE SYNERGY. DRIVE PROFITABILITY14

Cash Flow Matching Example

60 Month Auto loan – 1st 12 months of amortization

Weighted averageinvestment benchmarksand funding costs arecalculated from thesematches.

CREATE SYNERGY. DRIVE PROFITABILITY15

Loan Pricing – The Basics

Interest Rate Risk – Conclusions• Interest rate risk driven by the cash flow and repricing

characteristics of the loan rather than the term of the loan• To model most accurately, each cash flow and repricing

point is matched• The loan can be matched up to an appropriate point of:

– Afundingcurvewhenmatchingfunding• FundsTransferPricing FTP

– Aninvestmentcurvewhenlookingatinvestmentalternatives.• Pricingloansoffinvestmentalternatives• Valuingloans

CREATE SYNERGY. DRIVE PROFITABILITY

Which History to Use?• Was history from 2005-2007 a legitimate predictor

of recent credit losses?• Are 2008-2010 losses a legitimate predictor of

losses of newly originated loans in 2011?• Do we even have legitimate loss history for loans

originated today?– Changesincollateralcoverage– Changesinunderwritingstandards– Changesinkindsofloansoriginated

16

CREATE SYNERGY. DRIVE PROFITABILITY

17

Loan Pricing – ServicingServicing Cost

– MarginalOriginationCost• Costoforiginatingthenextloan

– MarginalServicingCost• Costofservicingthenextloan

– DirectOverheadAllocation• Fixedcostsdirectlyrelatedtoloanproduction

– GeneralOverheadAllocation• President’ssalary,humanresources,etc.

Arguments– Economist– Continuetoproducewidgetsuntilmarginalrevenueequalsmarginalcost.

– Accountant– Withoutoverheadallocation,youendupwithprofitableloansandanunprofitableinstitution.

OTS Cost Assumptions– 0.20%‐ FRMortgages– 0.38%‐ ARMs– 0.20%‐ Multi&Non‐Res– 0.20%‐ Const&Land– 0.20%‐ SecondMtg.– 0.20%‐ Commercial– 0.20%‐ Consumer– 1.00%‐ CreditCard

• Is there a better source for generic servicing costs

CREATE SYNERGY. DRIVE PROFITABILITY18

Servicing Example

• Differential pricing on A, B, C credits should reflect both additional charge offs, and additional servicing costs due to legal and collection fees.

CREATE SYNERGY. DRIVE PROFITABILITY19

Loan Pricing – The BasicsOption Risk – Dealing with uncertain cash flows• We imbed options in loan contracts that allow

customers to modify cash flow characteristics of loans when they consider it to their advantage to do so.– Prepayments

• Basicprepaymentlevels– death,divorce,transfer,upgrades,etc.

• Incentivedrivenprepayments– Customerprepaystorefinanceatalowerrate– Customercan’taffordtomoveorupgradebecauseofinterestratejump.

– Uptothecustomertoexecutetheoption– Insomecases,subjecttopenalty– primarilycommercialcontracts

– Adjustableratemortgagecaps• Annualcaps,lifetimecaps• Automaticallyexecutedbytheinstitution.• Loanfloors

• Ideally the institution is compensated with rate for making the option available.

CREATE SYNERGY. DRIVE PROFITABILITY

20

Option Risk – What Is It• 15 year FRM example showing remaining principal under different

rate environments– Falling– 25%CPR– 2.75yearduration– Flat– 8%CPR– 4.64Yearduration– Rising– 5%CPR– 5.21YearDuration

15 Year FRM

-

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

1 14 27 40 53 66 79 92 105 118 131 144 157 170

Month

Rem

aini

ng P

rinci

pal

5% CPR8% CPR25% CPR

CREATE SYNERGY. DRIVE PROFITABILITY

21

Consider Option Risk in Pricing Loans?

• Against– Notatruecostlikechargeoffs,servicingcosts,orcostsofmatchingfunding.

– Consideringoptionriskwillcauseloanstobeunprofitable.

– Nottheloanofficer’sproblem.– Verydifficulttocalculate– Maybeinherentlyhedgedinbalancesheetofretailfinancialinstitution.

• For– Optionriskcandamagetheperformanceofun‐hedgedinstitutions.Itcostsmoneytohedgeoptionrisk

– Price/yieldofsecuritiesreflectsoptionrisk.Securitiesaresecuritizedloans

– Ifloanofficersarenot‘charged’foroptions,theywillgiveawayoptionsinexchangeforrate

– Canbederivedfromsecuritiesmarket.

• Source– SecuritiesMarkets

CREATE SYNERGY. DRIVE PROFITABILITY22

Sample Loan – 5/20 Balloon

•Cash Flows•Pricing•Expenses•Risk Assum

CREATE SYNERGY. DRIVE PROFITABILITY

23

Investment Benchmark• Market rather than internal

benchmark• Compares performance of loan to

closest investment benchmark after adjusting for risk and cost differences.

• Most relevant when– Youaretryingtodecidehowtoinvestcashalreadyraised.

– Anytimeinvestinginasecurityisanalternativetomakingaloan

– Youaretryingtoderivemarketadjustmentsfor• Interestraterisk• Optionrisk

• Required inputs– Cashflowcharacteristics– Riskfreecurve– Investmentbenchmarkcurve– Pricing– Ratesandfees– Operatingexpenses– Creditriskadjustment– Additionaloptionriskadjustments

• Calculated adjustments– Interestrateriskadjustment– Optionriskadjustment– Loan’sspreadtoinvestmentbenchmarkafteradjustments

– Test– Isspreadpositive good ornegative bad ?

• Not considered– Fundingcostcurve– Capitalrequirement– RAROCGoal– InstitutionTaxRate

CREATE SYNERGY. DRIVE PROFITABILITY

Investment Benchmark Comparison - CRE • 20 Yr FR amortizing

loan only 6 bp less profitable than 5/20 balloon

• Longer cash flows requires more IRR coverage

• Can a 50bp premium be collected from customer in exchange for certainty?

• Duration extends < 2 years

24

Investment Benchmarks 5/20 Balloon CRE20 Yr FR CRE

@4.5%Risk Free Rate 0.460% 0.460%

+ Int Rate Risk Adjust 0.937% 1.518%= Risk Free Match 1.397% 1.978%

+ Option Risk Adjust 0.750% 0.750%= Investment Benchmark 2.147% 2.728%

+ Credit Risk Adjust 0.250% 0.250%+ Expense Adjust 0.795% 0.775%

= Retail Equiv Benchmark 3.192% 3.753%Wtd Loan Yield 4.000% 4.500%

Spread to Benchmark 0.808% 0.747%-0.060%

Duration 3.42 5.31

Conclusion: 20 Yr FR fully amortizing CRE loan can be a profitable loan when compared

to investment alternatives. Covers the inherent risks and costs!

CREATE SYNERGY. DRIVE PROFITABILITY

25

Valuation• Market rather than internal

benchmark• Compares market value of loan as

compared to book at time of origination.

• Most relevant when– Youaregoingtosellloanafterorigination.

– Whenyouaretryingtoimprovethefranchisevalueofyourinstitutionbyholdingwellpricedloans

• Required inputs– Cashflowcharacteristics– Riskfreecurve– Investmentbenchmarkcurve– Discountratecurve– Pricing– Ratesandfees– Operatingexpenses– Creditriskadjustment– Additionaloptionriskadjustments

• Calculated outputs– Marketvaluevsbookvalueofloan– Price– Withandwithoutoriginationfees– Test– Ispriceatorabove100 good orbelow100 bad ?

• Not considered– Fundingcostcurve– Capitalrequirement– RAROCGoal– InstitutionTaxRate

CREATE SYNERGY. DRIVE PROFITABILITY26

Valuation - Steps• Value Cash flows

– Projectamountandtimingofcashflows– Usediscountratestomarkcashflowstomarket.

n PVFVi

PV1 FV1 / 1 i n 9126.26/ 1 1.31%/12 1 9152.32

Note:Cashflowscontinueforanadditional48months

DiscountRate InvestmentBenchmark Adjustmentsnotincludingexpense

Thesumofthemarketvaluesofindividualcashflowsisthemarketvalueoftheinstrument.

CREATE SYNERGY. DRIVE PROFITABILITY27

Valuation - Steps

Book Amount of LoanWith FeesSum of Cash Flow Market Values100 * MV / BVWithout FeesSum of Cash Flow Market Values100 * MV / BV

Note: By Valuation standards, this is a well priced loan as its market value exceeds book at the time of origination.

CREATE SYNERGY. DRIVE PROFITABILITY

28

Internal Profitability Measures• How institutions make

money– LoanYield 6.0%– FundingCost 2.0%– Spread 4.0%

• Who owns the spread?– LoanOfficer?– FundingProvider?– TreasuryFunction?

CREATE SYNERGY. DRIVE PROFITABILITY

29

Funds Transfer Pricing• Internal profitability benchmark• Evaluates whether a loan is profitable

within context of balance sheet• Most relevant when

– Youaretryingtodecidewhetheryoucanmakemoneyoriginatingaloan

– Anytimeyouaretryingtoassestheprofitabilityofarelationship,productorprofitcenter

• Can focus on:– Dollarcontributiontoprofit ROA– Returnonrequiredcapital RAROC

• Required inputs– Cashflowcharacteristics– CostCurve– Pricing– Ratesandfees– Operatingexpenses– Creditriskadjustment– Additionaloptionriskadjustments– CapitalRequirement RAROC– CapitalGoal RAROC– InstitutionTaxRate

• Calculated adjustments– PretaxSpread $or%– Aftertaxspread $or%– RAROC– SpreadtoRAROCGoal– Test– Isspreadpositive good ornegative

bad ?• Not considered

– Riskfreecurve– Investmentbenchmarkcurve– CapitalRequirement ROA

CREATE SYNERGY. DRIVE PROFITABILITY

30

Selecting a FTP Curve •Not Recommended - Your Cost of Funds Curve

–Penalizesloanfunctionforinefficientfundsgathering,rewardsforefficientfundsgathering.Couldforceyoutopriceoutofthemarket.–Failstorewardandprovideanincentiveforfundsproviderstogatherfundsefficiently.–Historybasedcurveisusedtopricenewlyoriginatedinstruments.

•Recommended - Your true wholesale funding alternative

• FHLBAdvance• Jumbo/Brokered/I‐netCD• AAAcorporate• SwapCurve

–Usetheonethatcomesclosesttoyourtruewholesalefundingcost.–Creditsdepositgatheringfunctionsforsub‐wholesaledeposits.Levelstheplayingfieldforlendingfunctions.

CREATE SYNERGY. DRIVE PROFITABILITY

31

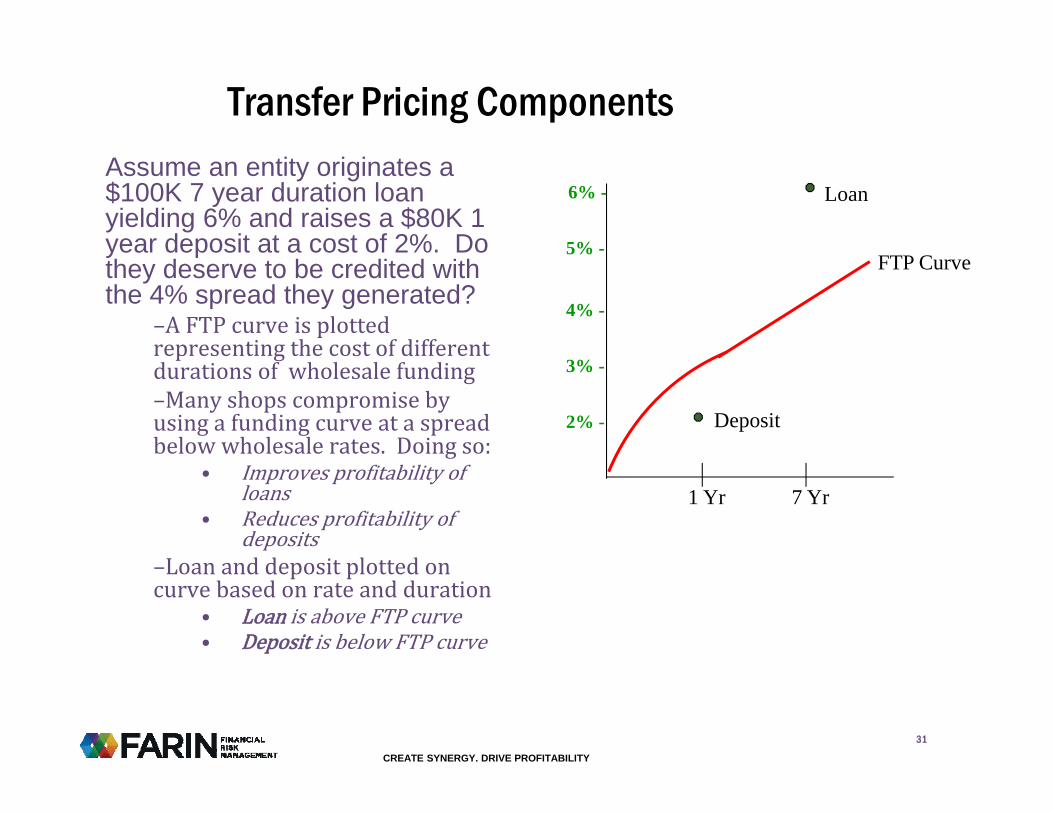

Transfer Pricing ComponentsAssume an entity originates a $100K 7 year duration loan yielding 6% and raises a $80K 1 year deposit at a cost of 2%. Do they deserve to be credited with the 4% spread they generated?

–AFTPcurveisplottedrepresentingthecostofdifferentdurationsofwholesalefunding–Manyshopscompromisebyusingafundingcurveataspreadbelowwholesalerates.Doingso:

• Improvesprofitabilityofloans

• Reducesprofitabilityofdeposits

–Loananddepositplottedoncurvebasedonrateandduration

• Loan isaboveFTPcurve• Deposit isbelowFTPcurve

FTP Curve

Loan

2% -

3% -

4% -

5% -

6% -

1 Yr 7 Yr

Deposit

CREATE SYNERGY. DRIVE PROFITABILITY

32

Transfer Pricing Components

•Spread - Deposit is credited to the entity. In this example:

–Depositratefor1yeardepositis2.0%–FTPratefor1yeardepositis3.0%.–Aspreadof1.0%on$80Kisallocatedtothedepositgatheringunit.

FTP Curve

Deposit

Loan

Spread - Deposit

2% -

3% -

4% -

5% -

6% -

1 Yr 7 Yr

CREATE SYNERGY. DRIVE PROFITABILITY

33

Transfer Pricing Components

•Spread – Rate Riskdue to mismatch is transferred to Treasury.

–OnlytheTreasurycanmanagethisriskandtheyneedthemargincontributiontodoso.–Inthisexample,theslopeintheyieldcurvebetweenthe1and7yearpointsis1% 4%‐3% .

FTP Curve

Deposit

Spread - Deposit

Spread – Rate Risk

2% -

3% -

4% -

5% -

6% -

1 Yr 7 Yr

Loan

CREATE SYNERGY. DRIVE PROFITABILITY

34

Transfer Pricing Components

•Spread – Option Risk is transferred to Treasury

–MostFTPsystemsignorethisrisk,butitisbecomingamoreandmoresubstantialportionoftheriskonfinancialinstitutionbalancesheets.–Tonottransferthisriskadjustmentwouldencouragelenderstograntoptionsinexchangeforhigherratesand/orvolumes.–Lenderscannotmanageoptionrisk.ThiscanonlybedonebyTreasuryandthespreadneedstobeavailabletobuytheriskprotection.

FTP Curve

Deposit

Loan

Spread - Deposit

Spread – Rate Risk

Spread – Option Risk

2% -

3% -

4% -

5% -

6% -

1 Yr 7 Yr

Inthisexample,spread‐optionriskof1%istransferredtotheTreasury.

CREATE SYNERGY. DRIVE PROFITABILITY

35

Transfer Pricing Components

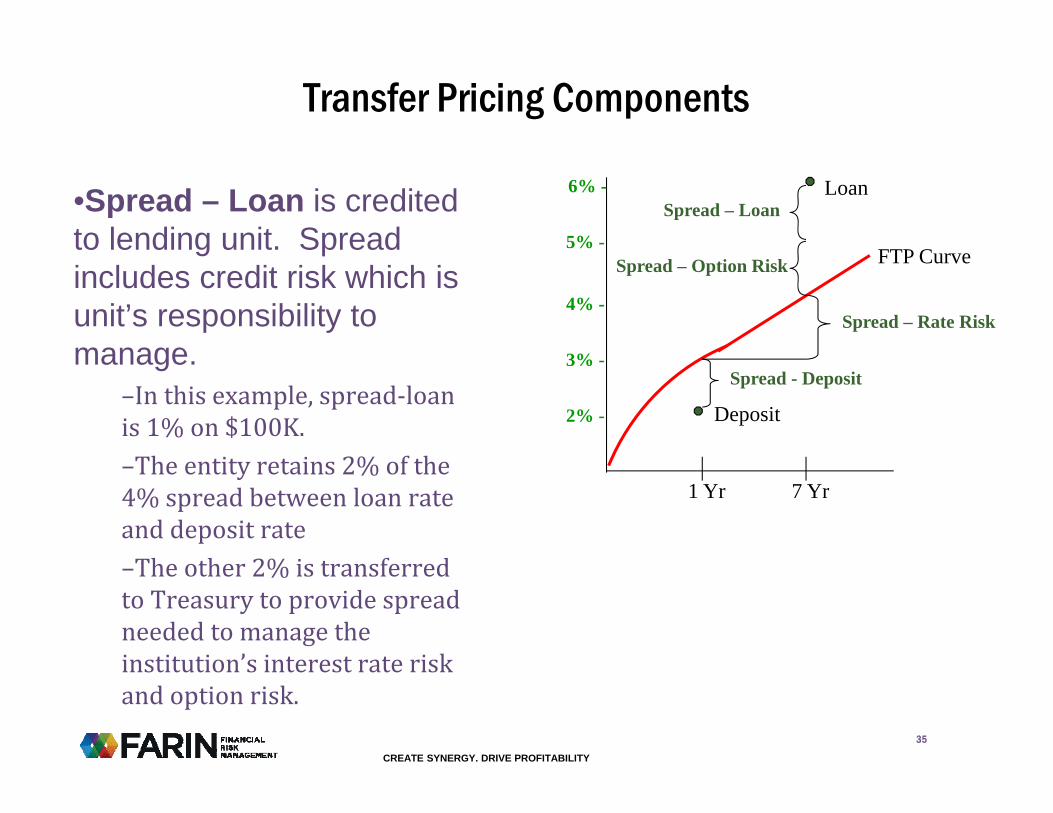

•Spread – Loan is credited to lending unit. Spread includes credit risk which is unit’s responsibility to manage.

–Inthisexample,spread‐loanis1%on$100K.–Theentityretains2%ofthe4%spreadbetweenloanrateanddepositrate–Theother2%istransferredtoTreasurytoprovidespreadneededtomanagetheinstitution’sinterestrateriskandoptionrisk.

FTP Curve

Deposit

Loan

Spread - Deposit

Spread – Rate Risk

Spread – Loan

Spread – Option Risk

2% -

3% -

4% -

5% -

6% -

1 Yr 7 Yr

CREATE SYNERGY. DRIVE PROFITABILITY

36

Transfer Pricing Components

•Return on Equity(RAROC) for the transaction -is calculated by:

–Summingnetinterestincomecontributionfromloanandinvestment–Addingfeesandsubtractingallocatedoperatingexpenses.–NetincomeisdividedbycapitalrequiredtocalculateReturnonCapital ROE

•So FTP income can be measured with

–NetIncome ROA–RAROC

FTP Curve

Deposit

Loan

Spread - Deposit

Spread – Rate Risk

Spread – Loan

Spread – Option Risk

2% -

3% -

4% -

5% -

6% -

1 Yr 7 YrBalance Rate FTP Rate Spread Net Int Inc

Loan 100,000 6.00% 5.00% 1.00% 1,000 Deposit 80,000 2.00% 3.00% 1.00% 800 Total 1,800 Fees 500 Expenses 1,000 Net 1,300 Capital Requirement (8%) 8,000 ROE 16.25%

CREATE SYNERGY. DRIVE PROFITABILITY

Capital Allocation•Why assign a capital requirement to a loan?

–Relatesprofitabilityofanentityloan toaprimaryearningsmeasurementratio.–Allowsforadjustmentsinreturnbasedondifferentialcapitalneedsfordifferentloansandinvestments.

•Should you bother with a capital allocation model?

–Willaddingthislevelofcomplexityhaveamaterialeffectonanalysisordecisions?–Iscapitalaconstraint

• Regulatoryrequirements• Self‐imposedrequirements

•What capital allocation model should I use?

–LeverageRequirement•Corecapitalrequirement•Internalcapitalgoals

–RiskBasedRequirement•BaselIII•InternalModel

–Isuspectwe’llseeamovementtowardinternalmodels

37

CREATE SYNERGY. DRIVE PROFITABILITY

38

FTP Analysis - RAROCBalance weighted costs

Decision – Don’t make the loan !!!

RAROC GoalRAROC (ROE)

Assumed tax rate of 35%

Horizon

Lifetime

CREATE SYNERGY. DRIVE PROFITABILITY

39

FTP Analysis - Income

Decision ToolMake the loan !!!Note: The net incomefigure is converted into ROA

Ratio analysisrestated indollars

CREATE SYNERGY. DRIVE PROFITABILITY

RAROC (Lifetime) 5/20 Balloon CRE20 Yr FR CRE

@4.5%20 Yr FR CRE

@5%20 Yr FR CRE @4.5% w\fee

Wtd Loan Yield 4.000% 4.500% 5.000% 4.500%+Wtd Fees 0.000% 0.000% 0.000% 0.250%- Wtd Fund Bench 1.642% 2.330% 2.330% 2.330%- Option Risk 0.375% 0.375% 0.375% 0.375%- Credit Risk 0.250% 0.250% 0.250% 0.250%- Expense 0.792% 0.775% 0.775% 0.775%= Spread 0.941% 0.770% 1.270% 1.020%- Tax Adjust 0.000% 0.000% 0.000% 0.000%= After Tax Spread 0.941% 0.770% 1.270% 1.020%/ Capital Req. 10.000% 10.000% 10.000% 10.000%= ROE (RAROC) 9.413% 7.704% 12.70% 10.20%ROE Target 10.000% 10.000% 10.000% 10.000%ROE Spread -0.587% -2.296% 2.704% 0.204%

RAROC Comparison - CRE

• How can we make this loan more profitable for ROE?– OriginationfeeOrhigherrate?– Additionalrelationships?

• Finding options brings loan to a 10% ROE to meet target– Canyousellit?

40

CREATE SYNERGY. DRIVE PROFITABILITY

41

Decision Rules Summary

Which model do you use? In this case, three lights are green and one is red?

CREATE SYNERGY. DRIVE PROFITABILITY

42

Decision TreeLoan New A 48 Mo

Initial Reprice Is the spread to Investment Rate 6.500% 0.000% Benchmark positive? 0.851%Reprice 0 0 Better off putting moneyAmortize in investments.Mature 48Balance 1,000 CapitalOption 0.00% Constraint?Credit 0.15% Decision based on ROE (RAROC)Servicing 0.15% Don't make the

Decision based on loan. income contribution

Is the FTP loan profitadequate? 4.82

Does the FTP ROE beatthe target? -7.70%

Originate for Is the loan price sufficientlyportfolio. above book? 101.82

Don't make the Originate and loan. Sell.

No

NoYes

Yes

YesNo

No

No

Yes

Yes

CREATE SYNERGY. DRIVE PROFITABILITY

Session 2• Recorded Webinar

• Reviewof4decisionmodels• Modelingandtweakingexamples• iPriceInstruction– iPriceisbrowserbased– resultsonourservers.

– Loggingon– Buildingarelationship– Modelingaloan– Tweakingaloan

43

CREATE SYNERGY. DRIVE PROFITABILITY

Session 3• Recorded Webinar

• Modelingandtweakingexamples• iPriceInstruction

– Buildingarelationship– Modelingaloan– Addingloansanddepositstotherelationship– Tweakingtherelationship– Evaluatingrelationshipprofitability

44

CREATE SYNERGY. DRIVE PROFITABILITY

What We Will Provide• Student Resource

Page– RegistrationLink giveusoneworkingdaytoapproveyou

– LinkstotwoWebExon‐demandrecordings• Session3• Session4

– LinktodownloadGettingStartedGuide pdf totheLoanEdge software

• Software and project support from our support staff during normal business hours.

• You will need:– RelativelyfastPCwithinternetaccessandareasonablyuptodateoperatingsystemandbrowser

– SeeGettingStartedGuidefordetails.

45