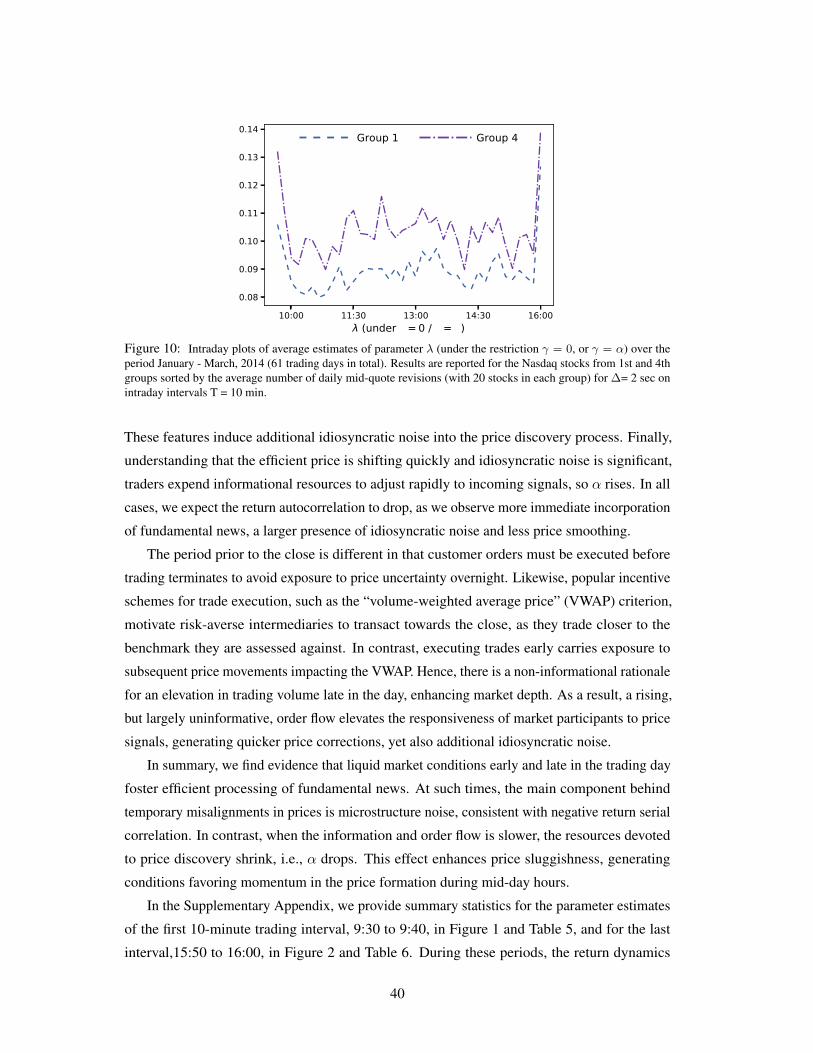

local mispricing and microstructural noise: a parametric

TRANSCRIPT

Local Mispricing and Microstructural Noise:

A Parametric Perspective∗

Torben G. Andersen† Ilya Archakov‡

Gokhan Cebiroglu§ Nikolaus Hautsch¶

This Version: October 2019

Abstract

We extend the classic ”martingale-plus-noise” model for high-frequency returns to accom-

modate an error correction mechanism and endogenous pricing errors. It is motivated by (i)

novel empirical evidence documenting that microstructure noise is interwoven with innova-

tions to the efficient price; (ii) building a bridge between high-frequency econometrics and

market microstructure models. We identify temporal pricing error corrections and noise

endogeneity as complementary components driving high-frequency dynamics and inducing

two separate regimes, characterized by the sign of the return serial correlation and an im-

plied bias in realized variance estimates. We document frequent fluctuations between these

regimes, which we associate with price discovery in a setting with incomplete information

and learning. The model links critical concepts from high-frequency statistics and market

microstructure theory, opening up new paths for volatility estimation.

Keywords: volatility estimation; market microstructure noise; price reversal; momentum;

contrarian trading; JEL classification: C58, C32, G14

∗We thank participants of the ”Jan Mossin Symposium,” Bergen, 2016; FERM, Guangzhou, 2016; SoFiE,

Aarhus, 2016; ”New Developments in Measuring and Forecasting Financial Volatility,” Durham, NC, 2016; MFA

Meeting, Chicago, 2017; Stevanovich Conference, University of Chicago, 2018; IAAE Conference, Nicosia, 2019;

and seminars at Aarhus University, Humboldt University, Universitat Pompeu Fabra, UNC at Chapel Hill, Vienna

University of Economics and Business, the U.S. Commodity Futures Trading Commission, and the University of

Giessen for comments and discussions. We are grateful to Peter R. Hansen for valuable comments. Andersen

acknowledges support from CREATES (DNRF78), funded by the Danish National Research Foundation. Hautsch

acknowledges financial support from the Wiener Wissenschafts-, Forschungs- und Technologiefonds (WWTF).†Kellogg School of Management, Northwestern University and NBER. Email: [email protected].‡Department of Statistics and Operations Research, University of Vienna. Email: [email protected].§Credit Suisse, London. Email: [email protected]. The views, thoughts, and opinions expressed in this

article belong solely to the author, and are not necessarily shared by the author’s employer.¶Department of Statistics and Operations Research, and the Research Platform ”Data Science @ Uni Vi-

enna,” University of Vienna, Vienna Graduate School of Finance and Center for Financial Studies. Email: niko-

1 Introduction

The increasing availability of high-frequency asset price data has spurred two largely separate

literatures. One focuses on model-free ex-post measurement of features concerning the realized

return path, with the main attribute of interest being the realized volatility, representing the

empirical quadratic return variation. The premise is that asset prices reflect an underlying

arbitrage-free “efficient” or “fundamental” return process polluted by microstructure noise

(MMN), due to rounding to a price grid, varying transaction and quote intensities, private

information, bid-ask spreads, and other trading costs. Hence, the fundamental log-price process

is a semimartingale, while MMN is viewed as a nuisance factor. Implicitly, this literature

presumes that all relevant information is impounded instantaneously so that, at all times,

transaction prices and quotes embed the latent efficient equilibrium price, bracketed by the bid-

ask spread. Consequently, at the micro level, the fundamental price is “hidden” through a MMN

distortion which, locally, are of non-trivial order. As a result, much work has been devoted

to MMN-robust inference for realized components of the efficient price process, see, e.g., the

classic articles in Andersen and Bollerslev (2018b), the survey by Andersen and Bollerslev

(2018a), and the book treatment of Ait-Sahalia and Jacod (2014).

Whereas the realized volatility literature generally treats the fundamental price innovations

as exogenous, a central topic in the market microstructure literature is price discovery. This

literature explores a variety of complications, including asymmetric information, heterogeneous

trading motives, and market design features. Here, learning, price impact, and strategic trading

arise as natural phenomena. The interaction of such features generates a complex environment,

so most theoretical microstructure models are fairly stylized, allowing for specific aspects of the

price discovery process to be explored in isolation. For example, Kyle (1985) analyzes strategic

trading of a risk-neutral agent with monopolistic private information, finding information to be

incorporated into the price slowly, as the informed agent spreads trades over time to manage

price impact. In contrast, Holden and Subrahmanyam (1992) show that information revelation

occurs rapidly if there are multiple informed agents. Likewise, both information acquisition

and risk aversion can have similar effects, see, e.g., Holden and Subrahmanyam (1996). Vives

(1995) also demonstrates that the speed of information revelation is negatively correlated with

the degree of risk aversion among informed agents and the amount of noise trading. Finally, in a

stylized setting, Glosten and Milgrom (1985) show that the bid (ask) prices represent conditional

expectations of the efficient price conditional on a sell (buy) transaction, so the “noise” in the

realized volatility literature is literally intertwined with innovations to the fundamental price.

In summary, typical microstructure models imply that noise is endogenous because inno-

vations to the transaction prices and quotes interact with the efficient price process through

1

learning and temporal feedback mechanisms. At the same time, microstructure theory is largely

void of the return dynamics of primary interest in the econometric work focusing on realized

volatility. In this paper, we build bridges between these strands of the literature. In particular,

as a methodological contribution, we suggest estimating the fundamental volatility over short

intraday windows from our microstructure model in a manner that corrects realized volatility

measures for MMN effects. By cumulating the former estimators, we obtain an alternative return

variation measure that generally is consistent with the RV measures, but deviates systematically

under specific market conditions, reflecting the relative strength of different MMN distortions.

As an initial step, we document, empirically, the presence of persistent time-varying return

autocorrelation, inconsistent with a noise process that is orthogonal to the fundamental price.

At the same time, the return correlation pattern displays pronounced fluctuations. As a vivid

illustration, Figure 1 provides volatility signature plots for four different stocks on selected days.

The upward sloping curves (as one approaches the origin) in the left panels are similar to the

biases induced by i.i.d. noise, which generate an MA(1) structure and negative return serial

correlation, as noted by Roll (1984).1 However, our sample of Nasdaq stocks contains many

examples of the exact opposite behavior. This is exemplified by the right panels, where the

signatures drop sharply as we approach the highest sampling frequencies, reflecting pronounced

positive serial correlation. Consistent with such findings, studies–going back at least as far as

Hansen and Lunde (2006)–show that the high-frequency return dynamics is inconsistent with

an MA(1) representation, as also touched on by Hasbrouck and Ho (1987). In-and-of-itself,

positive serial dependence may be rationalized by a more general specification of the noise

process. However, if noise is uncorrelated with the efficient price, it will only augment the

overall return variation, implying that signature plots will be increasing at high frequencies,

where the noise is dominant. That is, a declining return variation at high frequencies is only

feasible, if the noise and fundamental return innovations are (negatively) correlated, i.e., the

noise is endogenous. Hence, such MMN features leave a distinct footprint in the data.

The above evidence points towards time-varying return dependencies that are at odds with

the semimartingale paradigm and are not readily accommodated through the infill asymptotic

inference procedures commonplace within the high-frequency econometrics literature. More-

over, the presence of endogenous noise raises fundamental questions regarding our ability to

separately identify the return volatility associated with the efficient price versus noise innova-

tions. These considerations lead us to adapt a simple discrete-time parametric framework that

allows for rapidly shifting regimes, yet also provides a tractable and economically interpretable

setting, highlighting the impact of microstructural traits on the high-frequency dynamics.

1In a fully parametric setting, this property can be exploited to construct estimators of both the “fundamental” andMMN variance, see, e.g., Zhang et al. (2005).

2

Figure 1: The figure depicts signature plots for the Realized Variances (RV) computed for 4 stocks (Facebook,Apple, Ebay and Amazon) on selected trading days. The left and right panels illustrate cases with downwardand upward sloping signature plots, respectively. For each sampling frequency ∆ (from 1sec to 120sec with aone-second step), we compute the RV measure for multiple ”grids” obtained by shifting the initial price observationup by one second to ∆ seconds (thus, for ∆=1sec we have one grid and for ∆=120sec, we obtain 120 grids).Blue dots correspond to daily RV estimates computed from different underlying sampling frequencies and all gridconfigurations. The red solid lines represent the average values of RV across all grids (the so-called sub-sampledRV).

To ensure a transparent setup, we extend the classic ”martingale-plus-noise” model by

components accommodating an error correction mechanism and price endogeneity. These

features arise naturally once one recognizes that the investors’ information set is imperfect

and subject to acquisition and processing delays. Under these circumstances, investors cannot

determine, with certainty, whether a given price increase is due to the arrival of positive (private)

news or random net buying orders from liquidity traders (noise). In the former case, the price is

likely to continue its upward trajectory while, in the second case, the price tends to revert to its

prior level. Even if astute traders avoid systematic mispricing, the valuation is only unbiased

on average. During episodes with sustained imbalances in net liquidity demand or an unusual

intensity of privately informed trading, rational agents tend to err in their instantaneous valuation

in the same direction. At the same time, rationality does imply that simple momentum and

contrarian strategies cannot earn significant profits. The fact that we find positive and negative

3

return autocorrelation patterns about equally common is consistent with the latter hypothesis.

The ingredients of our model are not new to the MMN literature, but no existing tractable

framework simultaneously accommodates noise endogeneity and pronounced variation in the

return autocorrelation pattern. We retain tractability by stipulating that our model applies only

locally, and thus allow the model parameters to vary across intraday intervals. This flexible

approach is aligned with our empirical evidence, showing that momentum and contrarian

regimes, and thus the sign of return autocorrelations, may alternate frequently across the trading

day. It effectively allows the shifting market environment to guide the evolution of the system.

Moreover, the use of a local approximating model with constant volatility enables us to sidestep

the difficult task of jointly modeling the intraday patterns and the persistent activity dynamics.

Our model mimics features associated with learning via an error correction mechanism,

reminiscent of the partial adjustment dynamics introduced by Amihud and Mendelson (1987). It

includes four parameters; (i) the volatility of the random walk process (“fundamental volatility”);

(ii) the “magnitude of the noise,” or noise-to-signal ratio; (iii) the speed of reversal from

mispricing, which is closely related to the persistent autocorrelation or momentum effects; and

(iv) the instantaneous response to efficient price innovations, capturing the extent of mispricing

due to informational frictions. These parameters allow for both dynamic error correction

and price endogeneity features with differential implications for the return autocorrelation

pattern. Furthermore, the specification enables us to separate these components and render them

statistically identifiable and economically interpretable.

This parsimonious representation captures various return dependencies implied by existing

microstructure models. In particular, the classical “martingale-plus-noise” model as well as

variants, allowing the noise to be correlated with the efficient returns, emerge as special cases.

Combined with our ability to accommodate heterogeneity across intraday intervals, we obtain

a setting reminiscent of the endogenous noise representation analyzed by Kalnina and Linton

(2008).2 Our approach is also related to prior studies that link the properties of noise more

explicitly to the process of trading and the underlying microstructure, see, e.g., Madhavan et al.

(1997), Diebold and Strasser (2013), Chaker (2013) and Li et al. (2016). However, none of these

studies consider the type of high-frequency variation in the mispricing and temporal feedback

effects that we deem crucial in explaining the return dynamics observed in Figure 1.

In our model, the speed of price reversion interacts with the noise-to-signal ratio to determine

the sign of the return autocorrelation. We classify the market environment accordingly as

belonging to one of two regimes. In one, the impact of “mispricing” is dominated by the

strength of the price reversal, induced by idiosyncratic noise shocks, so the returns display

negative serial correlation, or “contrarian” traits. In the other regime, the feedback from

2See also Sheppard (2013) for a related notion intended to measure market “speed.”

4

mispricing generates “momentum,” or positive return autocorrelation.

The irregular alternation between such return dependency regimes have important implica-

tions for standard volatility measures based on high-frequency returns, see, e.g., Andersen et al.

(2003). In the contrarian regime, realized volatility tends to exaggerate the quadratic variation

of the efficient price, inducing the well-known upward-shaped volatility signature plots. In

the other regime, high-frequency sampling causes downward-shaped signature plots. Even

more fundamentally, prolonged periods of nontrivial return autocorrelation renders the standard

infill asymptotic approach problematic, because the associated finite-sample approximations

assume that the return dependencies are negligible beyond short (calendar) time windows. The

latter assumption, however, is not compatible with market microstructure approaches featuring

learning and pricing error corrections, as such mechanisms make return dependencies persist for

extended periods and are naturally cast in discrete time. In fact, the difficulty to align temporal

feedback effects in market microstructure models with infill asymptotics, where pricing errors

(in the limit) should be corrected instantaneously, is one of the major reasons why there is no

straightforward connection between common approaches for high-frequency based volatility

estimation and market microstructure models. For these reasons, we turn towards a discrete-time

representation and employ more traditional methods of inference.

Conveniently, our model may be cast in a linear state-space form, enabling estimation via

the Kalman filter. This facilitates consistent estimation of the (locally constant) volatility, albeit

with non-negligible error for short horizons. The setting encompasses several alternative models,

including the i.i.d. martingale-plus-noise and Amihud and Mendelson (1987) specifications,

allowing us to test their relative merits. In addition, we analyze identification issues arising from

mispricing and noise endogeneity. We find that the fundamental return volatility is identified,

even if the signal-to-noise ratio and the degree of noise endogeneity are only partially identified.

As such, our approach represents a step towards the development of high-frequency volatility

estimators that retain a link to the existing market microstructure literature and allow for a more

structural treatment of the impact due to noise shocks.

We estimate the model over intraday intervals using mid-quote returns sampled at different

frequencies. The analysis points towards a high degree of informational efficiency, although

the price discovery process also involves a non-trivial element of sluggishness. We identify

strong intraday periodicities in the speed of price discovery and, strikingly, find that fundamental

volatility is highly elevated at the market open and flat through the remainder of the trading day.

The dramatic increase in market activity towards the market close is, in contrast, driven by a spike

in uninformed trading and idiosyncratic noise. This illustrates the potential of our approach

to build a foundation for new quantitative measures of market efficiency and fundamental

volatility. Formal econometric tests favor our flexible parameter approach, involving a lagged

5

price adjustment mechanism, relative to popular stylized microstructure models.

The rest of the paper is structured as follows. Section 2 provides comprehensive evidence

for locally significant return autocorrelation of varying sign. Section 3 introduces the model,

explores its dynamic properties, and its relation to existing models. Section 4 focuses on

identification issues in our general specification and reviews our estimation strategy. Section

5 present our detailed empirical findings, and Section 6 concludes. Auxiliary materials are

deferred to a Supplementary Appendix, including also a large-scale Monte Carlo study.

2 Local Regimes of Significant Return Autocorrelation

This section provides novel empirical evidence for the existence of short-lived regimes, charac-

terized by distinct levels of return autocorrelation. That is, the return series vacillates between

periods with significantly positive, insignificant, and significantly negative return dependence.

We quantify the return serial dependence over consecutive short intervals using high-frequency

mid-quote prices of the Nasdaq 100 equity index constituents, obtained from LOBSTER.3 To

keep the analysis manageable, we restrict our sample to the first three months of 2014 yielding

a total of 61 trading days. For each day, we consider the full 6.5 hour trading period.

Since we focus on the properties of mid-quote returns across short intervals, spanning 10-20

minutes, we split our sample into quintiles based on the average daily number of mid-quote

revisions, with Group 1 being the 20% of stocks with most frequent revisions and Group 5 being

the 20% with the fewest. While we concentrate our discussion on the most liquid groups, we

convey a sense of robustness by reporting results for the full spectrum of stocks.

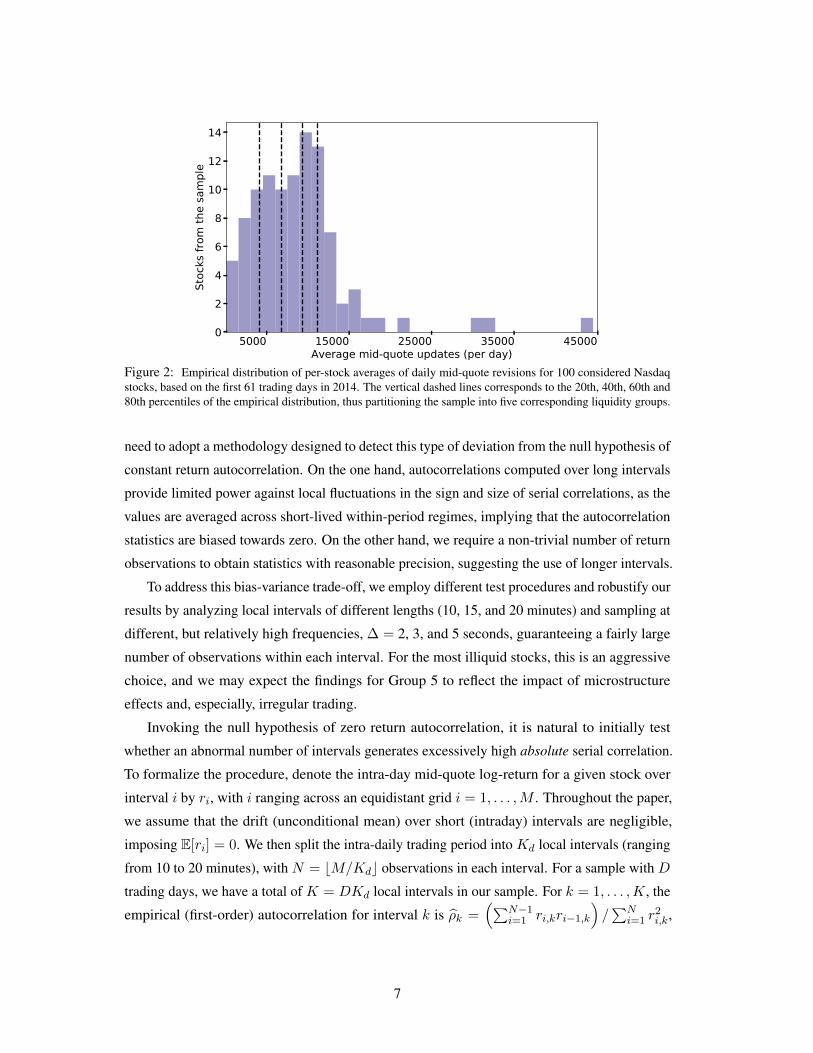

Figure 2 displays the distribution of daily mid-quote revisions, with the vertical lines

providing the partitioning into five liquidity groupings. The corresponding quintiles amount

to 17,485, 10,365, 8,166, 5,531 and 2,497 average daily mid-quote revisions, respectively. If

we sample every 5 seconds (over 6.5 hours of trading), we have 4,680 return observations per

day. Consequently, for a typical stock in Group 5, we usually have fewer quote revisions than

intra-day returns, whereas this ratio is much more favorable for stocks in Groups 1 to 4.

2.1 Significance of Return Autocorrelations in Local Intervals

We face the challenge of identifying return autocorrelations over local intervals of unknown (and

possibly) time-varying lengths. If individual stocks truly do undergo alternating periods with

different degrees of return autocorrelation – ranging from significantly negative to significantly

positive – but such episodes are fairly short, of varying duration and not directly observed, we

3The LOBSTER database (https://lobsterdata.com) builds on Nasdaq’s historical TotalView-ITCH data. It providesinformation on all trade and quote activity on Nasdaq at nano-second time stamp precision.

6

5000 15000 25000 35000 45000Average mid-quote updates (per day)

0

2

4

6

8

10

12

14

Stoc

ks from

the sa

mple

Figure 2: Empirical distribution of per-stock averages of daily mid-quote revisions for 100 considered Nasdaqstocks, based on the first 61 trading days in 2014. The vertical dashed lines corresponds to the 20th, 40th, 60th and80th percentiles of the empirical distribution, thus partitioning the sample into five corresponding liquidity groups.

need to adopt a methodology designed to detect this type of deviation from the null hypothesis of

constant return autocorrelation. On the one hand, autocorrelations computed over long intervals

provide limited power against local fluctuations in the sign and size of serial correlations, as the

values are averaged across short-lived within-period regimes, implying that the autocorrelation

statistics are biased towards zero. On the other hand, we require a non-trivial number of return

observations to obtain statistics with reasonable precision, suggesting the use of longer intervals.

To address this bias-variance trade-off, we employ different test procedures and robustify our

results by analyzing local intervals of different lengths (10, 15, and 20 minutes) and sampling at

different, but relatively high frequencies, ∆ = 2, 3, and 5 seconds, guaranteeing a fairly large

number of observations within each interval. For the most illiquid stocks, this is an aggressive

choice, and we may expect the findings for Group 5 to reflect the impact of microstructure

effects and, especially, irregular trading.

Invoking the null hypothesis of zero return autocorrelation, it is natural to initially test

whether an abnormal number of intervals generates excessively high absolute serial correlation.

To formalize the procedure, denote the intra-day mid-quote log-return for a given stock over

interval i by ri, with i ranging across an equidistant grid i = 1, . . . ,M . Throughout the paper,

we assume that the drift (unconditional mean) over short (intraday) intervals are negligible,

imposing E[ri] = 0. We then split the intra-daily trading period into Kd local intervals (ranging

from 10 to 20 minutes), with N = bM/Kdc observations in each interval. For a sample with D

trading days, we have a total of K = DKd local intervals in our sample. For k = 1, . . . ,K, the

empirical (first-order) autocorrelation for interval k is ρk =(∑N−1

i=1 ri,kri−1,k

)/∑N

i=1 r2i,k,

7

where ri,k denotes the i-th midquote return in interval k.4

For inference robust to heteroskedasticity and volatility clustering in high-frequency returns,

stemming from stochastic volatility and intraday periodicity effects, we apply asymptotic limit

results by Kokoszka and Politis (2011). Under mild assumptions on the return moments and the

dependence in the squared return process, they demonstrate that,

√N (ρk − ρk)

d→ N (0, Vk) ,

where the asymptotic variance Vk can be consistently estimated by

Vk =(N − 1)−1

∑N−1i=1 r2

i,kr2i−1,k

(N−1∑N

i=1 r2i,k)

2.

Under the null hypothesis H0 : ρk = 0, for all k, the local estimates ρk are noisy estimates

of zero, stemming from asymptotically independent, non-identical Gaussian distributions. To

gain power, we do not aim at testing the significance of local autocorrelations for each individual

interval, but focus on averages of absolute (local) autocorrelations. Given the results above, the

absolute autocorrelations |ρk| are asymptotically distributed as a half-normal random variate

with E[|ρk|] =√

2Vk/(Nπ) and V[|ρk|] = (1 − 2/π)Vk/N for all k. Then, by a standard

central limit theorem, under H0, the average absolute autocorrelation ρ = K−1∑

k |ρk|,asymptotically follows the distribution,

ρa∼ N

(1

K

∑k

√2VkNπ

,1

K2N

(1− 2

π

)∑k

Vk

). (1)

Hence, by constructing a test for ρ using the quantiles associated with the distribution in

equation (1), we obtain a test with power against the alternative of local autocorrelations of

varying signs. To test separately for positive and negative autocorrelations, we split the sample

of K intervals into the subsamples I− and I+, consisting of intervals where ρk is positive

or negative, respectively. Accordingly, one-sided average absolute autocorrelations are given

by ρ+ = K−1+

∑k∈I+ |ρk| and ρ− = K−1

−∑

k∈I− |ρk|, respectively, where K+ = |I+| and

K− = |I−|. The asymptotic distributions of ρ+ and ρ− are readily derived as for ρ above.

Hence, this test has power to separate average empirical autocorrelation estimates of a given

sign from random realizations of the same sign generated by the null distribution.

Table 1 reports the corresponding test results. The choice of T and ∆ trades off estimation

efficiency (increasing for low ∆ and large T ), biases due to the possible impact of market

4In unreported results, we find qualitatively similar autocorrelation results for the corresponding transaction returns.

8

T = 10 min T = 15 min T = 20 min

(I) (I+) (I−) (I) (I+) (I−) (I) (I+) (I−)

∆ #5%#1%#5%#1%#5%#1% π+ #5%#1%#5%#1%#5%#1% π+ #5%#1%#5%#1%#5%#1% π+

Liquidity group 1 (20 most liquid assets from NASDAQ 100)

2 sec 20 20 20 20 14 13 0.57 20 20 20 20 14 12 0.58 20 20 20 20 14 12 0.593 sec 20 20 20 20 11 10 0.58 20 20 20 20 12 10 0.59 20 20 20 20 12 9 0.605 sec 20 20 20 20 11 9 0.59 20 20 20 20 11 10 0.60 20 20 19 19 10 9 0.62

Liquidity group 2

2 sec 20 20 20 20 17 17 0.53 20 20 20 19 17 17 0.54 20 20 20 20 17 16 0.543 sec 20 20 20 20 16 15 0.55 20 20 20 20 15 14 0.55 20 20 20 20 15 15 0.565 sec 20 20 20 20 15 12 0.57 20 20 20 20 14 11 0.58 20 20 20 20 11 10 0.59

Liquidity group 3

2 sec 20 20 18 18 20 19 0.49 20 20 18 18 18 18 0.49 20 20 18 18 18 16 0.503 sec 20 20 18 18 20 15 0.52 20 20 18 18 18 16 0.52 20 20 18 18 14 11 0.535 sec 20 20 19 19 16 12 0.55 20 20 18 18 14 10 0.56 20 20 18 18 9 7 0.57

Liquidity group 4

2 sec 20 20 18 18 20 19 0.44 20 20 18 17 19 19 0.45 20 20 18 15 19 19 0.453 sec 20 20 18 17 20 19 0.48 20 20 18 17 18 18 0.48 20 20 17 17 18 17 0.485 sec 20 20 19 19 17 17 0.51 20 20 19 18 16 16 0.52 20 20 20 19 17 14 0.53

Liquidity group 5 (20 least liquid assets from NASDAQ 100)

2 sec 20 20 19 14 20 19 0.27 20 20 14 10 20 19 0.30 20 20 11 8 20 19 0.313 sec 20 20 18 15 20 20 0.29 20 20 14 11 20 20 0.32 20 20 11 10 20 19 0.335 sec 20 20 18 14 20 19 0.32 20 20 17 11 20 19 0.35 20 20 14 7 20 18 0.36

K = 2379 K = 1586 K = 1159

Table 1: Significance of first order return autocorrelations calculated for local intra-daily intervals of length T =10, 15, and 20 minutes. Columns #5% and #1% report the number of stocks (out of 20 in each liquidity group) forwhich the null hypothesis is rejected at 5% and 1% significance level, respectively. Columns marked by (I) referto the results of the test which is based on all intervals in the sample, while columns under (I+) and (I−) refer toresults based on intervals with only positive or only negative autocorrelations, respectively. Columns π+ provide theaverage (across stocks) fraction of intervals with positive return autocorrelations over the full sample of K intra-dailyintervals (K is reported in the bottom of the table). The tests are conducted for local intervals observed during 61consecutive trading days spanning the first three month of 2014. Results are reported separately for five groups ofstocks sorted by the average number of daily mid-quote revisions.

microstructure noise (worsens for small ∆) and the superposition of local autocorrelation

regimes (problematic for large T ) versus the resulting power of the test. We report inference

based on local intervals of T = 10, 15, and 20 minutes, computed at sampling frequencies ∆ =

2, 3, and 5 seconds. The results are based on the first 61 trading days of 2014 and are reported

separately for stocks from the five liquidity groups defined above.

We report on the test for absolute autocorrelation ρ in the columns marked by (I), while

those marked (I+) and (I−) concern ρk for k ∈ I+ and k ∈ I−, respectively. We indicate the

number of stocks (out of 20 in each liquidity class) for which we reject the null at 1% and 5%

confidence levels, together with the relative proportions of intervals belonging to I+ (or I−).

First, for every single stock, we reject the null hypothesis of constant first-order return

9

autocorrelation of zero. For a vast majority of stocks, we also reject the null for most configura-

tions of T and ∆, when positive and negative autocorrelations are considered separately. The

fraction of intervals with positive serial correlation ranges between 27% and 62%, depending on

the liquidity group, sampling frequency ∆ and interval length T . Hence, the evidence clearly

supports the hypothesis of significant local return serial correlation of varying signs.

Secondly, for most liquid stocks (group 1 and 2), we reject the null more often for regimes

of positive than negative autocorrelation. This pattern reverses for the low-liquidity groups 4

and 5, revealing asymmetries with respect to the intensity of the quote revisions. For longer

intervals, T , rejections of the null are slightly less frequent, likely due to a loss of power caused

by variations in the return dynamics within the intervals. Conversely, the proportion of rejections

is largely independent of the sampling frequency, ∆.

Finally, we generally observe more intervals with positive than negative autocorrelations

(K+ > K−) for the stocks from the first three liquidity groups. This suggests that a form of

“momentum” is a major driver of the local return dependence structure.

2.2 Persistence of Return Autocorrelations

We now explore the persistence of the regimes. Predictability of the sign of the return autocorre-

lation across local windows is inconsistent with the hypothesis of zero return dependencies and

suggests the existence of local regimes with shifting autocorrelation structures.

By defining the indicator variable

θk = 1{ρk≥0

}, k = 1, . . . ,Km

we apply a standard nonparametric Wald–Wolfowitz runs test to assess whether θk is purely

random. A ”run” is defined as a string of identical elements in the indicator sequence. Assuming

independent elements, the number of runs, Rθ, follows the asymptotic distribution,

Rθ ∼ N

(2π+π−K + 1, 4π2

+π2−K

2 − 2π+π−K

K − 1

),

where π+ = 1K

∑k θk = K+/K and π− = 1−π+ = K−/K denote the proportions of positive

and negative autocorrelation regimes, respectively. Table 2 reports results for different choices

of T and ∆. The null is rejected for a clear majority of stocks, even at the 99% confidence level.

Moreover, the rejections fall consistently in the left tail, indicating (positive) persistence.

To explore the underlying dependence structure, we implement a test based on the serial

correlation in the local return autocorrelation regime. We define {θk} as a homogeneous Markov

chain of order one with transition probability pij = Prob(θk+1 = j∣∣θk = i), with i, j ∈ {0, 1}.

10

T = 10 min T = 15 min T = 20 min∆ #2.5 #97.5 #0.5 #99.5 π+ #2.5 #97.5 #0.5 #99.5 π+ #2.5 #97.5 #0.5 #99.5 π+

Liquidity group 1 (20 most liquid assets from NASDAQ 100)

2 sec 19 0 19 0 0.57 19 0 17 0 0.58 19 0 17 0 0.593 sec 19 0 18 0 0.58 20 0 18 0 0.59 19 0 17 0 0.605 sec 20 0 17 0 0.59 19 0 18 0 0.60 19 0 15 0 0.62

Liquidity group 2

2 sec 20 0 20 0 0.53 18 0 16 0 0.54 14 0 14 0 0.543 sec 18 0 18 0 0.55 17 0 14 0 0.55 19 0 16 0 0.565 sec 19 0 17 0 0.57 19 0 18 0 0.58 17 0 17 0 0.59

Liquidity group 3

2 sec 17 0 14 0 0.49 17 0 14 0 0.49 15 0 11 0 0.503 sec 15 0 15 0 0.52 18 0 16 0 0.52 18 0 15 0 0.535 sec 16 0 15 0 0.55 18 0 16 0 0.56 16 0 14 0 0.57

Liquidity group 4

2 sec 20 0 14 0 0.44 16 0 14 0 0.45 13 0 12 0 0.453 sec 19 0 16 0 0.48 15 0 12 0 0.48 17 0 12 0 0.485 sec 18 0 17 0 0.51 16 0 13 0 0.52 16 0 11 0 0.53

Liquidity group 5 (20 least liquid assets from NASDAQ 100)

2 sec 18 0 15 0 0.27 15 0 13 0 0.30 16 0 12 0 0.313 sec 19 0 17 0 0.29 17 0 13 0 0.32 15 0 10 0 0.335 sec 18 0 15 0 0.32 17 0 10 0 0.35 14 0 11 0 0.36

K = 2379 K = 1586 K = 1159

Table 2: The table reports on Wald–Wolfowitz run tests for intervals of T = 10, 15, and 20 minutes. The nullhypothesis asserts that positive vs. negative return autocorrelation regimes follow an independent random sequence.The number of stocks (out of 20), for which we reject the null, are given in columns labeled %2.5, %0.5 (left tailrejections) and %97.5, %99.5 (right tail rejections). Columns π+ provide the average (across stocks) fraction ofintervals with positive return autocorrelation in the full sample of K intraday intervals. The sample covers 61 tradingdays spanning the first three month of 2014. Results are reported separately for stocks sorted by the intensity ofmid-quote revisions, with the highest in Group 1 and the lowest in Group 5.

The null hypothesis stipulates that θk is an i.i.d. Bernoulli process, i.e., p00 = p10 = p and

p01 = p11 = 1− p, so θk should be Bernoulli distributed with E[θk] = p and V[θk] = p(1− p),

∀k. A natural estimator for pij , pij , is the proportion of transitions from state i to state j relative

to the total number of observations for state i. Under the null, letting π+ denote the sample

estimate of p and K →∞, pij is asymptotically distributed as

pij ∼ N

(1{

i=1}(2π+ − 1) + π−,

π+π−K

).

Table 3 reports results for different values of T and ∆. The null hypothesis of random

variation in the sign of the autocorrelation is rejected in most cases. Notably, the rejections are

associated exclusively with extreme right tail realizations of the test statistic, indicating that both

positive and negative autocorrelation regimes display persistence across adjacent local intervals.

11

Persistence of positive regimes (H0: p11 = p) Persistence of negative regimes (H0: p00 = 1− p)

10 min 15 min 20 min 10 min 15 min 20 min∆ #2.5 #97.5 π+ #2.5 #97.5 π+ #2.5 #97.5 π+ #2.5 #97.5 π− #2.5 #97.5 π− #2.5 #97.5 π−

Liquidity group 1 (20 most liquid assets from NASDAQ 100)

2 sec 0 20 0.57 0 19 0.58 0 16 0.59 0 19 0.43 0 19 0.42 0 19 0.413 sec 0 18 0.58 0 18 0.59 0 17 0.60 0 19 0.42 0 20 0.41 0 18 0.405 sec 0 18 0.59 0 18 0.60 0 15 0.62 0 20 0.41 0 20 0.40 0 19 0.38

Liquidity group 2

2 sec 0 20 0.53 0 17 0.54 0 13 0.54 0 20 0.47 0 18 0.46 0 16 0.463 sec 0 18 0.55 0 14 0.55 0 16 0.56 0 18 0.45 0 19 0.45 0 20 0.445 sec 0 18 0.57 0 18 0.58 0 15 0.59 0 20 0.43 0 19 0.42 0 17 0.41

Liquidity group 3

2 sec 0 16 0.49 0 17 0.49 0 14 0.50 0 15 0.51 0 17 0.51 0 14 0.503 sec 0 16 0.52 0 17 0.52 0 18 0.53 0 15 0.48 0 18 0.48 0 16 0.475 sec 0 16 0.55 0 17 0.56 0 15 0.57 0 16 0.45 0 17 0.44 0 17 0.43

Liquidity group 4

2 sec 0 20 0.44 0 16 0.45 0 15 0.45 0 15 0.56 0 15 0.55 0 13 0.553 sec 0 17 0.48 0 15 0.48 0 16 0.48 0 18 0.52 0 14 0.52 0 16 0.525 sec 0 17 0.51 0 15 0.52 0 14 0.53 0 19 0.49 0 17 0.48 0 16 0.47

Liquidity group 5 (20 least liquid assets from NASDAQ 100)

2 sec 0 19 0.27 1 18 0.30 0 19 0.31 0 12 0.73 0 9 0.70 0 9 0.693 sec 0 20 0.29 1 18 0.32 0 16 0.33 0 16 0.71 0 10 0.68 0 8 0.675 sec 0 19 0.32 0 18 0.35 0 16 0.36 0 14 0.68 0 12 0.65 0 10 0.64

K = 2379 K = 1586 K = 1159 K = 2379 K = 1586 K = 1159

Table 3: The table reports the number of stocks for which the null hypothesis of independent transitions betweenlocal autocorrelation regimes is rejected. On the left side, we report the results of the test for the persistence ofregimes with positive return autocorrelation underH0: p11 = p. On the right side, we test the presence of persistenceof regimes with non-positive return autocorrelation under H0: p00 = 1− p. We reject the null hypothesis for theleft tail at the 2.5% and for the right tail at the 97.5% level. The corresponding number of stocks for which wereject the null hypothesis is given in columns marked by #2.5 and #97.5. Columns π+ and π− provide average(across stocks) fractions of intervals with positive and non-positive return autocorrelations in the total sample ofK intra-daily intervals, respectively (K are reported in the bottom of the table). The tests are conducted for localintervals observed during 61 consecutive trading days spanning the first three month of 2014. The results are reportedseparately for five groups of stocks sorted by the average daily mid-quote revisions.

Section 1 of the Supplementary Appendix explores the small-sample properties of our tests

and their robustness to noise and jumps via simulations from a stochastic volatility model

used by, e.g., Huang and Tauchen (2005), Barndorff-Nielsen et al. (2008b), and Goncalves

and Meddahi (2009). Even for small samples mimicking our local intervals and prices subject

to MMN and jumps, the size distortions identified in our simulations differ by an order of

magnitude from the test outcomes reported above. These findings confirm that our evidence

concerning the variability, significance and persistence of local autocorrelation regimes is not

spurious, but rather appear to be driven by structural features of the price formation process.

12

3 A Model for High-Frequency Asset Price Dynamics

This section introduces a parsimonious parametric model that can accommodate the salient

features of the short-term price dynamics documented in Section 2. The objective is to assist in

the identification and interpretation of the drivers behind the time-variation in the shape of the

volatility signature plots and the return serial correlation patterns. The aspiration is to provide

a starting point for building more realistic models of real-time price discovery and market

fluctuations in which we can gauge the relative impact of learning, information heterogeneity

and elements of market microstructure frictions.

3.1 The Discrete-Time Local Regime Model

We consider a model in discrete time, i ∈ {0, 1, 2, . . . , T}, defined over an equidistant time

grid. At each point in time, we observe the logarithm of the quote midpoint for a given asset, pi ,

yielding a total of T log-returns, ri = pi − pi−1, i = 1, . . . , T . We focus on the salient features

of the intraday return dynamics and typically think of each return covering a short interval, on

the order of multiple seconds, but not fractions of a second.

An important consideration for our model design is the identification of channels for price

discovery, as opposed to MMN, allowing for significant return autocorrelation over non-trivial

time intervals. Generally, we cannot disentangle such features by nonparametric techniques, so

we impose identifying structure through parametric assumptions, subject to empirical scrutiny.

The ”efficient” (full information and frictionless) log price at time i, p∗i, follows a random

walk, consistent with a no-arbitrage representation for the return over short intraday intervals,

p∗i = p∗i−1 + ε∗i and ε∗i = r∗i = p∗i − p∗i−1 , (2)

where r∗i = ε∗i is the “efficient” return with E[ε∗i ] ∼ i.i.d.(0, σ2∗).

The evidence in Section 2 suggests that the mid-quote price dynamics deviates from that of

the efficient price in significant ways. We propose a simple representation that accommodates

both price endogeneity and correlation in the pricing errors via readily identifiable components.

Specifically, the return dynamics, locally, evolves according to the scheme,

ri = pi − pi−1 = −α (pi−1 − p∗i−1) + (γ ε∗i + εi) , 0 < α < 2, (3)

where εi is an i.i.d. component, uncorrelated with ε∗i , E[εi ] = E[εi ε∗i ] = 0 and V[εi] = σ2

ε .

It is convenient to introduce an explicit notation for the noise-to-signal ratio,

λ = σ2ε/σ

2∗ .

13

In the “classic” martingale plus noise model, this ratio directly impacts the optimal sampling

frequency, see Ait-Sahalia et al. (2005) and Bandi and Russell (2006), and it remains critical for

the short-run price dynamics in our general framework.

For α = γ = 1, our model reduces to this classical representation, pi = p∗i + ε∗i . In

contrast, if γ 6= 1 or α 6= 1, we introduce endogeneity and error correction into the price

dynamics, potentially generating downward-sloped volatility signatures and persistent return

autocorrelation.

Uncorrelated Endogenous Pricing Errors

For α = 1, we eliminate persistent return serial dependence. Specifically,

pi = p∗i + (γ − 1) ε∗i + εi , (4)

so the system features i.i.d. noise but, in general, there is endogeneity, as the error term is

correlated with the fundamental price innovation ε∗i , whenever γ 6= 1.

Letting γ differ across local intervals is one way to mimic intertemporal heterogeneity in the

information environment. Traders with incomplete information seek to infer the fundamental

value from the concurrent market dynamics, including signals derived from price innovations,

evolving order book imbalances, consummated trades, and incoming news items. At a point in

time, rational agents with incomplete information tend to draw similar conclusions from avail-

able public signals. Hence, cumulative random shocks in either direction generate correlated,

albeit short-lived, pricing errors. Even if investors price assets correctly on average, they will,

for short intervals, induce γ > 1 in some scenarios and γ < 1 in others. Such temporary periods

of over- or under-reaction to latent news impact the price dynamics. To formalize the discussion,

we explicitly characterize the return variation and first-order return dependence in the system.

Direct computations exploiting equation (4) demonstrate that the return variance equals

V[ri] = V[pi − pi−1] = σ2∗ + 2 [ γ(γ − 1) + λ ]σ2

∗ , (5)

while the first-order return auto-covariance takes the form

Cov[ri, ri−1] = [ γ(1− γ) − λ ]σ2∗ , (6)

and all higher order return autocorrelation coefficients (h > 1) are zero.

The return variation depends on the quadratic term γ (γ − 1). If γ = 1, we obtain the

traditional expression for the noise-induced inflation of the return variation. If γ < 1, the

14

concurrent return innovation fails to fully incorporate the efficient price innovation. This

smoothes the price path, counteracting the effect of the idiosyncratic noise, so the return variation

may even drop below the value associated with the fundamental return, i.e., V[ri] < σ2∗ . Note

further that, because α = 1, the adjustment to the fundamental price innovation will be fully

completed by the subsequent interval. Consequently, the impact of the cumulative squared

returns are minimized, when the price change is distributed evenly across the current and

following interval, i.e., the smoothing effect is maximized at γ = 1/2. In other words, for

γ < 1/2, a disproportionate share of the adjustment occurs in the interval following the efficient

price innovation, generating a more irregular price path. Finally, for γ > 1, the price overreacts

to fundamental news, reinforcing the excess volatility stemming from i.i.d. noise.

The effect of γ on the return autocovariance is simply the reverse, as it depends on γ (1−γ). Accordingly, the return autocovariance attains its maximum at γ = 1/2 and is positive

for γ (1 − γ) > λ, i.e., for moderate noise. In these cases, endogeneity, i.e., correlation

between the fundamental returns and the pricing errors, induces momentum which outweighs

the idiosyncratic noise and generates positive return serial dependence. For γ > 1 the price

overshoots, exacerbating the negative return correlation induced by idiosyncratic noise.

The above discussion reflects the fact that the effect of γ on the second order return moments

is symmetric around 1/2. All else equal, two distinct γ values that imply the same value for

|γ − 1/2| induce the same degree of price smoothing and lead to identical return variances

and auto-covariances. This helps explain why we later establish an equivalence among two

benchmark cases, γ = 1 and γ = 0. Hence, for α = 1, not only γ = 1 but also γ = 0 generates

the classic martingale plus noise model, annihilating the issue of endogeneity. This equivalence

induces a statistical identification problem that will be analyzed in some detail below.

Error Correction Dynamics

Focusing instead on the error correction mechanism, the scenario γ = 1 and α 6= 1 yields

pi = pi−1 − α (pi−1 − p∗i−1) + ε∗i + εi = p∗i + (1 − α) (pi−1 − p∗i−1) + εi . (7)

Now, the i.i.d. error term is independent of the fundamental return innovation, but for 0 < α < 1,

the observed price responds sluggishly to current and past pricing errors, inducing longer-run

return autocorrelation. The latter is, empirically, a relevant feature, as documented in Section 2.

This error correction mechanism is motivated by the intuition that risk-averse agents with in-

complete information form (unconditionally) unbiased, yet not error-free, expectations about the

efficient price. The agents are aware that temporary mispricing is likely, creating opportunities

15

for (risky) speculative trading that generates a pull back towards efficiency. As such, the model

captures temporal feedback effects through a minimalistic reduced-form approach. Earlier

contributions, including Kyle (1985) and Vives (1995), discuss various settings and economic

factors, that render prolonged price reaction patterns consistent with sequential learning models.

More formally, it is straightforward in this case to establish that

V[ri] = σ2∗ +

2λ

2 − ασ2∗ , (8)

and the hth-order return auto-covariance is

Cov[ri, ri−h] = − (1 − α)h−1 αλ

2 − ασ2∗ . (9)

Absent endogeneity, the error term inflates the return variation and the autocorrelation in

Equation (9) is negative. For a small α, the information transmission is slow, i.e., pricing

errors induce more protracted corrections, implying more return smoothing and lower the price

variation. Likewise, if α > 1, price reactions imply overshooting and increased return variation.

0 20 40 60 80 100time

−6

−4

−2

0

2

4

6

8

10

p an

d p*

p *

p :α=0.05α=0.90

Figure 3: Simulated trajectories for p∗i and pi from model (2) - (3) given two different values of α. The remainingparameters take the values σ2

∗ = 1, γ = 0 and λ = 0.1.

The ”Random-Walk-plus-Noise” Representation

To facilitate comparisons to the extant literature, we couch our model (2)-(3) in a random-walk-

16

plus-noise format by labeling the mispricing component, its innovation, and its variance,

µi = pi − p∗i , εµi = (γ− 1) ε∗i + εi and V[εµi ] = σ2µ = (γ− 1)2σ2

∗ + σ2ε . (10)

The system (2)–(3) now implies,

pi = p∗i + µi, (11)

µi = (1− α)µi−1 + εµi . (12)

Equation (11) highlights the role of µi as a MMN type component, creating a wedge between

pi and p∗i . However, correlation between the innovations in Equation (2) and (3) along with

the temporal feedback imply that the pricing error is affected by shocks to both the efficient

price and noise process. Econometrically, αµi−1 serves as an error correction term, pushing the

mid-quote back towards the ”equilibrium” level, pi = p∗i .

The role of ε∗i in the error εµi resembles features discussed in the case of uncorrelated

endogenous errors. If γ = 1, the efficient price innovation is fully incorporated in pi and has

no impact on εµi . In contrast, if γ = 0, new information has no immediate impact, implying a

lagged price response, and ε∗i is fully embedded in εµi . We review this scenario in Section 3.4.5.

Figure 3 displays a simulated efficient price path along with a few price series generated by

the model, given specific parametric configurations. γ = 0 reflects a short (one-period) delay

associated with information retrieval and processing, while the value of α controls the degree of

adherence to the efficient price.5 The feedback generated by error correction induces short-term

serial correlation, as evident from the α = 0.05 and α = 0.90 scenarios. Both series constitute

smoothed and lagged variants of the jagged efficient price path, as is particularly evident for

α = 0.05. In the extreme case, α = 0, the efficient and observed prices are entirely decoupled.

In contrast, for α = 1, all current mispricing is eliminated in the subsequent period.

The mispricing component in Equations (11)-(12) takes the form of a mean-zero AR(1)

process. It is stationary for 0 < α < 2 with unconditional variance

V[µi] =σ2µ

α (2− α)=

(γ − 1)2 + λ

α (2− α)σ2∗ . (13)

Expression (13) may be interpreted as a measure of (average) mispricing, or market in-

efficiency. The mid-quote price equals the efficient price in expectation, i.e., E[µi] = 0 and

E[pi] = E[p∗i ], so the average squared pricing error is determined by the variance, V[µi]. It is

evident that V[µi] is minimized for α = 1 implying, rather intuitively, that rapid error correction

enhances price efficiency.

5As we establish later, if α 6= 1, the case γ = 0 is empirically relevant, and a canonical case of particular interest.

17

The second factor controlling the degree of inefficiency is the pricing error innovation in

the numerator of Equation (13). This term is small if, all else equal, there is no (local) over- or

under-reaction to latent news (γ = 1), and the idiosyncratic error is minimal (low λ).

In summary, the price dynamics reflects the covariance structure of the innovations to the

mispricing component and the fundamental price, and how these shocks are propagated through

the temporal adjustment process. The covariance structure takes the form,

Σ =

[E[(εµi )2] E[εµi ε

∗i ]

E[εµi ε∗i ] E[(ε∗i )

2]

]=

[(γ − 1)2 + λ γ − 1

γ − 1 1

]σ2∗ . (14)

Equation (14) shows that the off-diagonal entries are non-zero, if and only if γ 6= 1. This point

is discussed further below in our review of the extant literature.

We reiterate that our model, deliberately, is of reduced form and focuses on specific channels

behind salient features of the return dynamics. It is intended as an approximation for short

intraday periods, like 10-30 minutes, for which the factors governing the return dynamics

remain stable. Over longer horizons, the size of the volatility innovation is clearly not constant.

Allowing model parameters to shift across adjacent short intervals, indicating a transition from

one informational regime to another, is in line with the findings of significant time-varying

return autocorrelations in Section 2. We may move from a period of under-reaction to one

of over-reaction due to the shifting nature of the information flow and the broader market

environment.6

3.2 Second Order Return Moments

This section provides model-implied conditions for excess volatility and return serial correlation.

These features are closely related and reflect the impact of MMN versus smoothing in the return

variation process. The latter also affects our ability to identify the drivers behind the price

dynamics from the observed return moments in the absence of auxiliary assumptions.

3.2.1 Excess Return Variation

We recall that the log-return in Equation (3) may be stated as ri = −αµi−1 + (ε∗i + εµi ) . The

following lemma provides an explicit expression for the return variation in this general case.

6The spirit of this approach mimics the assumptions often invoked for developing inference techniques with high-frequency data, see, e.g., Mykland and Zhang (2009) and Bibinger et al. (2014), who explicitly rely on localwindows in which the quantity of interest, in their case return volatility, may be assumed to remain fixed.

18

Lemma 1 (Return Variance). Assume σ2ε > 0, 0 < α ≤ 1, 0 ≤ γ < 2. Then,

V[ri] = α2 V[µi] + (γ2 + λ)σ2∗ (15)

= σ2∗ +

2

2 − αFα(γ, λ) σ2

∗ , (16)

where, for later convenience, for given α, we define Fα(γ, λ) as a function of γ and λ,

Fα(γ, λ) = γ2 + ( 1 − γ ) α + λ − 1.

Proof. Follows by a sequence of straightforward calculations from equation (13).

Equation (15) implies that the return volatility is increasing in σ2∗ and λ. Likewise, due

to the “smoothing” of the price path for low α, the volatility increases with α (for γ < 1).

Finally, as before, the return variation is minimized for γ = α/2, increasing for γ > α/2, and

decreasing for γ < α/2, generalizing the result for the uncorrelated endogenous noise setting

(α = 1).

The following corollary summarizes the conditions for excess volatility in our general

setting, featuring both error correction and endogeneity.

Corollary 1. Assume σ2ε > 0, and 0 < α ≤ 1.

V[ri] ≤ V[r∗i ] if Fα(γ, λ) ≤ 0 , (17)

V[ri] > V[r∗i ] otherwise. (18)

Consequently, the return volatility is lower than the fundamental volatility if price updating

is slow, the extent of noise is low (i.e., α and λ are small), and γ is close to α/2, implying a

variance-minimizing degree of smoothing. The condition Fα(γ, λ) < 0, alternatively, can be

stated as γ2 + λ < 1− α(1− γ). Hence, the two regimes are governed by the relative size of

the effective return smoothing, 1− α(1− γ), and the size of the return innovations, γ2 + λ.

Thus, we have two distinct regimes. In the classical model, γ = 1, the presence of noise,

λ > 0, trivially leads to excess volatility. In contrast, in the presence of partial price adjustments,

the volatility may drop below the level associated with the fundamental innovation process and

generate inverted volatility signature plots.

3.3 Return Auto-Covariances

The determinants of whether returns display excess volatility are also critical for the sign of the

return auto-covariances. This is a consequence of the following lemma and corollary.

19

Lemma 2 (Return Auto-Covariances). Assume σ2ε > 0, 0 < α ≤ 1, , h ≥ 1. Then,

Cov[ri, ri−h] = ψ(h− 1) σ2∗[1 − α (1− γ) − (γ2 + λ)

](19)

= − Fα(γ, λ) ψ(h− 1) σ2∗ , (20)

with ψ(h− 1) = α2−α (1− α)h−1 and ψ(0) = 1, if α = 1.

Proof. See the Supplementary Appendix.

Hence, the relation between 1 − α (1 − γ) and γ2 + λ also governs the sign of the auto-

covariance for the observed returns. We summarize this result in the form of a corollary.

Corollary 2. Assume σ2ε > 0, 0 < α ≤ 1, and h ≥ 1.

Cov[ri, ri−h] ≥ 0 if Fα(γ, λ) ≤ 0 , (21)

Cov[ri, ri−h] ≤ 0 otherwise. (22)

We note that, for 0 < α < 1, the sign of the auto-correlation is identical for all h ≥ 1, so both

”contrarian” and ”momentum” regimes display persistent return dependence. In Section 5, we

seek to identify this feature empirically over short trading intervals.7

For models without endogeneity, γ = 1, return momentum is ruled out, as the necessary

condition, λ < 0, is infeasible – a point further discussed in Section 3.4.1. In contrast, for

γ < 1, momentum regimes are attainable and, contrary to the pure price endogeneity setting of

Section 3.1, this is now possible, e.g., for γ = 0 (as long as λ < 1− α).

It is useful to relate these model implications to our prior empirical evidence. Section 2.1

finds that the returns, on average, display only limited serial dependence. For low values of γ,

this is possible only if 1−α ≈ λ. This is plausible, if the MMN component is small, while prices

impound information swiftly, i.e., 1−α is small as well. More generally, zero return correlation

is consistent with MMN, as long as the impact is mitigated by a certain sluggishness in market

prices. Nonetheless, a large noise component, λ ≥ 1, always induces negative serial correlation

and excess return volatility due to the reversal needed to correct idiosyncratic mispricing.

A natural application of these results is to realized volatility estimation. Traditional realized

variance measures, obtained from cumulative high-frequency squared returns, will be biased

and inconsistent unless the market environment generates a return dynamic that satisfies the

condition for zero excess volatility or, equivalently, for no (significant) return serial correlation,

namely, γ2 + λ ≈ 1 − α (1− γ) or Fα(γ, λ) ≈ 0.

7In contrast, α > 1 implies that the signs alternate for h > 1. Such cycles may be plausible over longer horizons,but abrupt alterations in the return dependencies across short intraday intervals are counterfactual.

20

Finally, note that for given α and λ, scenarios for which |γ − α/2| are identical, e.g., the

cases γ = 0 and γ = α, yield the same return variances and autocovariances. We will discuss

these aspects in more detail in the context of statistical identification in Section 4.1.

3.4 Nested Models

Our model captures basic structural mechanisms from alternative market microstructure ap-

proaches within a uniform setting, providing a starting point for identifying strengths and

limitations of existing paradigms. Because we nest several important special cases, our em-

pirical work should help shed light on which models best approximate salient features of the

high-frequency return process. A second objective is to highlight the identification issues that

arise in microstructure models with a latent endogenous noise component. This often-overlooked

feature becomes evident, as we summarize the empirical implications of various models below.

3.4.1 The Classical Model with Idiosyncratic Noise Autocorrelation

A critical feature of our model (2)–(3) is the allowance for noise endogeneity by having γ 6= 1.

In fact, if γ = 1 then, independently of the noise dynamics, we obtain,

Σ =

[E[(εµi )2] E[εµi ε

∗i ]

E[εµi ε∗i ] E[(ε∗i )

2]

]=

[λ 0

0 1

]σ2∗ .

The absence of correlation among the innovations has important ramifications. Letting ∆µi =

µi − µi−1, for any stationary noise dynamics and integers i, j, we have E[ ε∗i ∆µj ] = 0 and,

ri = pi − pi−1 = ε∗i + ∆µi . (23)

It follows that the actual return variation always exceeds the efficient return variation,

E[ r 2i ] = σ2

∗ + E[ (∆µi)2 ] ≥ σ 2

∗ ,

and the return variance and autocovariances take the form in equations (8) –(9). It implies that,

uniformly, the volatility signature plots should lie above the efficient variance. This is at odds

with the evidence in Section 2, as the signature plots often drop sharply at higher frequencies.

We reiterate that this feature arises, even with dependence in the return series induced by

serial correlation in the noise process. Our model specification (11) and (12) now implies

pi = p∗i + µi , (24)

µi = (1− α)µi−1 + εi , (25)

21

with E[εi ε∗i ] = 0 and E[ εi µj ] = 0 for all integers i, j. Hence, in our parametric setting, the

mispricing component, µi , follows an AR(1) process, inducing return dependence for α 6= 1.

This has empirical relevance for measures using high-frequency features, such as the bid-ask

spread, the price grid and order splitting induce serial dependence in both transaction and

quote returns. Recognizing this issue, the original realized volatility estimation procedures

employ sparse sampling, e.g., Andersen and Bollerslev (1998). Subsequently, a variety of robust

statistical approaches were proposed, including realized kernels, pre-averaging, multi-scale,

or spectral procedures, e.g., Barndorff-Nielsen et al. (2008b), Jacod et al. (2009), Zhang et al.

(2005), and Bibinger et al. (2014). A recent development of simple procedures attaining the

same objective is given by Da and Xiu (2019).

3.4.2 The Classical Model

The i.i.d. noise model is obtained from the model in the preceding section by, in addition,

imposing α = 1, so we have E[εi ε∗i ] = 0 and,

pi = p∗i + εi . (26)

Thus, fundamental news is embodied instantaneously and past pricing errors are corrected

without delay, so shocks fully dissipate by the next observation, yielding V[ri] = σ2∗(1 + 2λ)

and Cov[ri , ri−1] = −λσ2∗ . That is, instant error correction implies negative first-order serial

correlation, but also no return correlation beyond lag one.

This scenario corresponds to the “classic” random-walk-plus-iid-noise model, see, e.g.,

Zhou (1996), Ait-Sahalia et al. (2005) and Bandi and Russell (2008). It still provides the

basic reference for empirical microstructure effects, yet it rules out both feedback effects and

noise endogeneity. The model is rejected, if we find significant evidence of 0 < α < 1, and,

secondarily, γ 6= 1. In fact, these conditions apply for a large set of subintervals in Section 5.2,

pointing towards serious empirical shortcomings of the classic model.

3.4.3 The Uncorrelated Endogenous Noise Model

As discussed in Section 3.4.2, imposing α = 1 generates a scenario with endogenous, but

serially uncorrelated noise, where pi = p∗i + (γ− 1) ε∗i + εi , and the first-order autocovariance

equals Cov(ri , ri−1) = [(1 − γ) γ − λ] σ 2∗ . The specification is consistent with positive

return dependence if γ < 1 , i.e., the concurrent return innovation does not fully incorporate the

efficient price innovation. In this setting, the fundamental return variation may be estimated

consistently through a simple first-order lag adjustment to the realized volatility estimator, as

originally suggested by Zhou (1996).

22

The general point is that noise endogeneity and information feedback are distinct features

and have different implications. The endogeneity can alter the sign of the first-order return

autocorrelation, while the noise correlation generates longer lasting correlation effects. One

objective of this paper is to determine conditions under which we can identify the underlying

source of noise from the observed high-frequency return dependencies.

3.4.4 The Amihud-Mendelson Model

Our model (2)–(3) modifies the standard representation to allow for economic mechanisms

that generate longer-run return dependence. Meanwhile, the finance literature contains several

models designed to accommodate low-frequency serial correlation. Prominent models include

Amihud and Mendelson (1987) and Hasbrouck and Ho (1987). Specifically, the model by

Amihud and Mendelson (1987) emerges as a special case by setting γ = α, implying,

pi = (1 − α) pi−1 + αp∗i + εi . (27)

In this scenario, the mid-quote price is a weighted average of the past price and the current

efficient price, with an innovation term, that is uncorrelated with the efficient price innovation.

The price dynamics in Equation (27) mimics the one in Equation (3), with the notable

difference that the price adjustment in the latter is based on the discrepancy between the lagged

observed and past efficient price. Importantly, the model allows for both noise endogeneity

and feedback effects through an error correction mechanism, while providing a parsimonious

and readily identifiable model. The main drawback is the tight link between the strength of

endogeneity and speed of error correction via the condition γ = α.

Note that Amihud and Mendelson (1987) seek to capture daily return dynamics. In that

context, updating based on the current efficient price (established over a full trading day) is

sensible relative to one-day-old information. In a high-frequency setting, featuring incessant

order book revisions, multiple trades per second, and nearly continuous news feeds, it is less

plausible that traders have the capability, and all relevant information, to gauge the efficient

price every instant. Instead, updates may occur with a delay of a few seconds. As such, Equation

(3) seems more suitable at high frequencies.

3.4.5 The Information Delay Model

An alternative specification, yielding the identical first- and second-order return moments as the

Amihud and Mendelson (1987) model, may be obtained via a different economic mechanism.

As noted in Section 3.2, γ = 0 implies that even well-informed agents respond to newly arriving

information with a minor delay. This leads to a lagged price response and feedback – features

23

that appear empirically relevant. Moreover, the delay and feedback effects can be stronger

or weaker depending on the information and market environment at the time, motivating our

approach of keeping model parameters fixed only over short intraday intervals.

In this “information processing delay” representation, the only contemporaneous shock

impacting the price is idiosyncratic noise. Simultaneously, the price adjusts to past pricing

errors, enabling the efficient price innovations to govern the intermediate return dynamics, as

the market disentangles the noise and fundamental shocks to prices.

Letting γ = 0, Equations (2)–(3) generate the following price dynamic,

pi = (1 − α) pi−1 + αp∗i−1 + εi . (28)

A few comments are in order. First, since ε∗i is latent and uncorrelated with εi, we obtain

an equivalent representation by relabeling p∗i−1 as p∗i . But this renders Equations (27) and (28)

identical. In other words, we cannot separately identify the two models – they generate the

identical process for the observed returns. This point was briefly mentioned in Section 3. It

complicates identification and inference in general – an issue we discuss in depth in Section 4.1.

Second, the covariance structure for the innovations now takes the simple form

Σ =

[E[(εµi )2] E[εµi ε

∗i ]

E[εµi ε∗i ] E[(ε∗i )

2]

]= σ2

∗

[1 + λ −1

−1 1

].

This result reflects that efficient innovations are incorporated into prices with a delay, so the

mispricing component must absorb the full impact of any concurrent ε∗i shock, rendering the

noise process endogenous. In this scenario, the return dynamics, reflecting the error correction

mechanism, is the only source of coherence between market and efficient prices. Hence, the

market is in a perpetual state of transition, driven by an ongoing process of price discovery.

Conceptually, this separates our specification from standard microstructure models in which

prices are in equilibrium, except for short-lived distortions induced by exogenous noise shocks.

Third, the “information delay” model differs from the high-frequency Amihud and Mendel-

son (1987) model, as the latter has a covariance structure identical to the general representation

(14), but with γ = α. For either model, once information processing is initiated, it proceeds at

a rate governed by α. The latency of the efficient innovation means that we cannot determine

if this occurs with a temporal delay or not. This notwithstanding, the incomplete and delayed

price adjustment renders the noise endogenous. Typically, such endogeneity is imposed through

explicit statistical assumptions, see, e.g., Kalnina and Linton (2008), but it is endowed with a

more structural interpretation in our specification.

In summary, our information delay model – or high-frequency reinterpretation of Amihud

24

and Mendelson (1987) – featuring just three free parameters, (α, λ, σ∗), endows the asset pricing

process with dynamic properties reflecting distinct underlying economic factors. The empirical

evidence in Section 5 illustrates how this fully identifiable variant of our model captures salient

features of the short-run dynamics, providing a superior framework for assessing the separate

economic forces at play relative to traditional microstructure representations.

3.5 Realized Volatility Measures

This section reviews the implications of the preceding results for realized volatility measures

computed from return data generated by model (2)–(3). The realized volatility for interval [0, T ],

using equidistant log-price observations, pi∆ , i = 0, . . . , n = n(∆) = bT/∆c, is obtained as

RVT (∆) =

n(∆)∑i=1

(pi∆ − p(i−1)∆

) 2=

n(∆)∑i=1

( ri∆ ) 2 , (29)

where we have chosen the notation n(∆) to make the dependence of n on ∆ explicit.

In the frictionless variant of our model with α = γ = 1 and λ = 0, we have

E [RVT (∆) ] = T σ2∗ . (30)

In the case of general exogenous noise, ri = ε∗i + ∆µi , as discussed in Section 3.4.1, we

find, in analogy to the result established there, that,

E [RVT (∆) ] = T[σ2∗ + E[ (∆µi)

2]≥ T σ2

∗ . (31)

This result reiterates a point stressed by Hansen and Lunde (2006) – the realized volatility

measure, absent endogenous noise, cannot be downward biased. Moreover, the extent of any

upward bias is determined by the properties of the noise process. The usual assumption is that

every price observation contains a noise component unrelated to the sampling interval, so ∆µi

constitutes an Op(1) term which, for ∆→ 0, dominates the Op(√

∆) term stemming from the

efficient price innovation. This generates an increasing upward bias with sampling frequency,

and a positively sloped volatility signature plot for ∆→ 0.

As noted previously, the above is, generally, not factual. The illustrations in Figure 1 show

that, as the sampling frequency increases, the volatility signature plot is sharply upward sloping

in some periods and sharply downward sloping in other periods. The discussion in Section

3.4.1 reminds us that the latter is possible only if the noise is endogenous. Specifically, for our

25

parametric model (2)–(3), but imposing exogenous noise, γ = 1, we obtain

E [RVT (∆) ] = T [ 1 + 2λ ] σ2∗ . (32)

In contrast, for the full parametric model with γ 6= 1,

E [RVT (∆) ] = T

[1 +

2

2 − αFα(γ, λ)

]σ2∗ . (33)

As before, the sign of Fα(γ, λ) determines whether the return volatility measure is upward or

downward biased. Both cases are empirically important, as they each occur with regularity,

showing that a (time-varying) degree of exogenous and endogenous noise is required to capture

the observed features of the volatility process for individual large capitalization equity returns.

4 Statistical Inference

4.1 Identification

Section 3 shows that our general model (2)–(3) is not uniquely identified from the second-order

return moments. This type of identification issue is well recognized. There are two distinct

sets of assumptions regarding the noise, leading to starkly different procedures. One approach

casts the model in continuous time and conducts inference via an in-fill asymptotic scheme,

where the number of observations (ticks) diverges within a fixed interval. In this case, the noise

dependence can generally be identified, because the size of the tick-by-tick innovations in the

efficient price shrinks in line with the interval, while the magnitude of the noise shocks are

invariant with respect to sampling frequency, so the noise is asymptotically “big,” allowing for

nonparametric identification. A thorough development of this approach is provided by Jacod

et al. (2017); see also the discussion in Li and Linton (2016). Likewise, Da and Xiu (2019)

obtain consistent inference from a tick-time MA(q) noise process in a continuous-time setting

with independence between noise and efficient price, but otherwise very general assumptions.

In contrast, if the noise dependence is fixed in calendar time, asymptotic inference requires an

increasing time horizon. In this case, identification hinges on the stipulation that the fundamental

price process is a (semi-)martingale, while the noise is stationary. The latter implies an element

of mean reversion but, without auxiliary assumptions, this can only be ascertained with precision

over longer time intervals. Moreover, dependence between the noise and fundamental price

process complicates identification even further, as noted in Ait-Sahalia et al. (2006). Typically,

one can only accomplish this task via careful parametric modeling.

Our general discrete-time model illustrates the latter point. Without endogeneity (γ = 1),

26

the system is identified through the parametric specification, but once such dependence is

introduced, we have only partial identification. We can estimate the key parameter determining

the fundamental price volatility, namely σ2∗ , but the finer details of the noise dynamics are elusive,

as the second-order moments of observed returns cannot disentangle the delay with which the

observed price incorporates the fundamental innovation from the relative size (variance) of the

noise component. Specifically, the issue revolves around separate identification of λ and γ.

Both impact the return variation and autocovariances, (15) and (20), only through the function

Fα(γ, λ) = γ2 − αγ + α+ λ− 1. Thus, any combinations of γ and λ yielding the same value

for Fα(γ, λ) imply identical second-order moments. In contrast, it is readily shown that α and

σ2∗ are identifiable. Henceforth, in this section, we often abbreviate Fα(γ, λ) by Fα.

We may exploit additional information by imposing natural constraints on γ and λ, such

as non-negativity. Yet, whenever they are not on the boundary, any small shift in γ may be

offset by a compensatory shift in λ, leaving Fα unaltered. Since Fα is linear in λ and quadratic

in γ, fixing γ identifies λ but, as illustrated in Section 3, fixing λ does not generally uniquely

identify γ, as the implied second-order polynomial in γ has two roots. Accordingly, scenarios

with identical values for |γ − α/2| are observationally equivalent. When estimating the general

model, we therefore focus on the lower-dimensional vector (α, σ2∗ , Fα), with values for Fα

consistent with a range of (γ, λ) combinations for given return dynamics.

To illustrate the geometry of non-identification regions for (γ, λ), we consider two scenarios

associated with positive and negative return autocorrelations, respectively. In Regime I, we

choose the parameter values α = 0.835, σ2∗ = 0.986 · 10−8 and Fα = −0.100 producing a

positive first-order autocorrelation of 0.087. In Regime II, we set α = 0.976, σ2∗ = 0.524 · 10−8

and Fα = 0.091, resulting in a negative first-order autocorrelation of −0.074. These values for

α, σ2∗ and Fα correspond to the median estimates α, σ2

∗ and Fα obtained across local 10-minute

intervals with positive and negative return autocorrelations, respectively, in Section 5.

27

0.0 0.2 0.4 0.6 0.8 1.0 1.2γ

0.0

0.1

0.2

0.3

0.4λ

F<0

F>0

Regime Iλ= λ(γ)Fα(γ, λ) = 0

0.0 0.2 0.4 0.6 0.8 1.0 1.2γ

0.0

0.1

0.2

0.3

0.4

λ

γ<1 γ>1

F<0

F>0

Regime II

Figure 4: The dashed blue lines describe admissible values of (γ, λ), corresponding to Regime I (left plot) andRegime II (right plot). Regime I has α = 0.835, σ2

∗ = 0.986 · 10−8 and Fα = −0.100 and generates positivereturn autocorrelation. Regime II has α = 0.976, σ2

∗ = 0.524 · 10−8 and Fα = 0.091 and generates negativeautocorrelation. The solid black lines represent values of (γ, λ) which solve equation Fα(γ, λ) = 0 for a given α.