logistics real estate investing for supply chain managersjjb/classes/6340/talk/idi-g.pdf ·...

TRANSCRIPT

Logistics Real Estate Investing for Supply Chain Managers

March 15th, 2017

Derrick Perkins

Vice President, Investments

(404)479-4121

2

Logistics Real Estate Investing for Supply Chain Managers

• About IDI Gazeley

• Real Estate from the Investors Point of View

• Real Estate Fundamentals

• Case Study: Developing a Building

• Global Differences

Presentation Outline

3

Growing Together

https://www.youtube.com/watch?v=EjQLgbZH8gY

4

30BROOKFIELD PORT TERMINALS IN OUR MARKETS

13MARKET OFFICES

A truly global logistics real estate platform

50 MSFOPERATING PORTFOLIO

(4.6 MILLION SQ M)

45 MSFDEVELOPMENT LAND

(4.2 MILLION SQ M)

Map of Holdings

UNITED STATESHeadquartered in Atlanta

185 MSF (17 million SQ M) developed

750 facilities developed and acquired

30 MSF (2.8 million SQ M) land bank

CHINAHeadquartered in Shanghai

3.0 MSF (282,400 SQ M) developed

8 facilities developed

500,000 SF (46,000 SQ M) land bank

FRANCEHeadquartered in Paris

6.2 MSF (576,000 SQ M) developed

39 facilities developed and acquired

6 MSF (557,000 SQ M) land bank

UNITED KINGDOMHeadquartered in London

56 MSF (5.2 million SQ M)

developed

130 facilities developed and acquired

3.8 MSF (357,000 SQ M) land bank

GERMANYHeadquartered in Frankfurt

7.1 MSF (660,000 SQ M) developed

28 facilities developed and acquired

2.3 MSF (213,000 SQ M) land bank

NETHERLANDS15 facilities totaling 2.3 MSF (2.1 million SQ M)

5

Brookfield is a global alternative asset manager with $250 billion in assets under management.

They have four main businesses: property, infrastructure, renewable power and private equity.

As a portfolio company of Brookfield, we are part of one of the world's largest and most

sophisticated owners, operators, and investors in real estate.

Brookfield Asset Management

Brookfield Property

Partners 1

Private Institutional

Funds

Brookfield Property

Group

Brookfield Renewable

Energy Group

Brookfield Renewable

Energy Partners

(“BREP”) 1

Private Institutional

Funds

Brookfield

Infrastructure Group

Brookfield Infrastructure

Partners (“BIP”) 1

Private Institutional

Funds

Brookfield

Capital Group

(1) Flagship publicly listed entities

Brookfield

Brookfield Business Partners (“BBP”) 1

Private Institutional

Funds

6

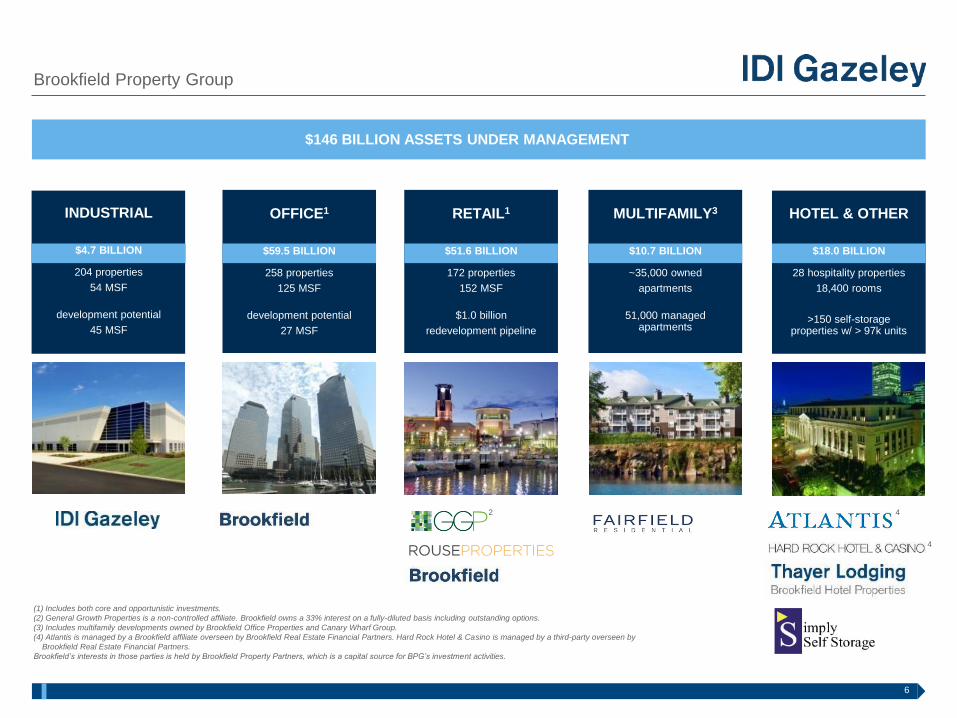

Brookfield Property Group

$146 BILLION ASSETS UNDER MANAGEMENT

OFFICE1

$59.5 BILLION

258 properties

125 MSF

development potential

27 MSF

RETAIL1

$51.6 BILLION

172 properties

152 MSF

$1.0 billion

redevelopment pipeline

MULTIFAMILY3

$10.7 BILLION

~35,000 owned

apartments

51,000 managed apartments

INDUSTRIAL

$4.7 BILLION

204 properties

54 MSF

development potential

45 MSF

HOTEL & OTHER

$18.0 BILLION

28 hospitality properties

18,400 rooms

>150 self-storage properties w/ > 97k units

(1) Includes both core and opportunistic investments.

(2) General Growth Properties is a non-controlled affiliate. Brookfield owns a 33% interest on a fully-diluted basis including outstanding options.

(3) Includes multifamily developments owned by Brookfield Office Properties and Canary Wharf Group.

(4) Atlantis is managed by a Brookfield affiliate overseen by Brookfield Real Estate Financial Partners. Hard Rock Hotel & Casino is managed by a third-party overseen by

Brookfield Real Estate Financial Partners.

Brookfield’s interests in those parties is held by Brookfield Property Partners, which is a capital source for BPG’s investment activities.

2

4

4

7

The Brookfield Advantage

BROOKFIELD LOGISTICS PROPERTIES60 MSF global operating portfolio

PORTS30 Brookfield port terminals

worldwide

GENERAL GROWTH PROPERTIES

(RETAIL)154 MSF portfolio

FAIRFIELD RESIDENTIAL50,000 managed and owned apartments

Being part of Brookfield ties all parts of IDI Gazeley’s business together

and leverages global relationships with local expertise.

8

E-commerce

Retail +

Consumer Goods

3PL

Healthcare +

Food

Automotive

More than 60% of our projects are with repeat customers from all major industries

Repeat Customers

Real Estate from the Investors Point of View

10

Who?

– Individuals through Public REITS (Prologis, Duke, First Industrial East Group)

– Institutional

• Pension Funds

• Retirement Funds

• Sovereign Wealth

– High Net Worth / Family Office

Why?

– Alternative / Hard Assets

– Bond Like Performance

– Inflation Hedge

Investing in Real Estate

1.8% 2.4%1.4%

0.7%2.1%

-1.2%

3.9%

9.2%

12.9%

9.6%

3.3%

10.1%

20.9%

7.8%7.2%

9.5%

14.2%

6.4% 6.0% 6.4%7.2%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

NPI LeveragedNPI

NCREIFFarmland

NCREIFTimberland

NFI-ODCE -gross of

fees

NAREITEquity REIT

Index

S&P 500Index

3Q 2016 1-Year 10-Year

11

Why Industrial?

– Unique demand drivers from other property types (Office, Retail, Multifamily, Hotel)

– Lower Investment (Initial, CapEx)

– Different Size Buildings = Different Demand Drivers

Investing in Real Estate

Super Bulk

Home Depot 657,000 SF Williams-Sonoma 1,350,000 SF

Light Industrial Bulk Distribution

12

Key: Maximum Flexibility to Meet Changing Market Demand

– Sizes: 50,000 SF to 1,000,000 SF

– Height: 28’ to 36’+

– Depth: 120’ to 650’

– Construction

• Wall type

• Column & bay spacing

– Loading (Docks, Space)

– Trailer and auto parking

• Impact on Rentable Area

– Expansion

• Land is Not Free

Investing in Real Estate

More than Just a Box!

13

The Site Plan

Investing in Real Estate

14

Construction Design

Investing in Real Estate

15

Investing Options

• Highest Risk (Uncertainty) usually has highest reward

• Core Investment – Buying Existing Asset - Safest

o Long-term leases to good credit tenants

o Established markets

o Traditional design features

o Return = Initial Yield + Rental Increases + Appreciation, 7-10%

• Speculative Development is Riskiest

o Empty land > Hopefully occupied building

o First Rents 2 to 3 years after investment decision

o Return = Development Profit + Rental Increases, 12-14%

Investing in Real Estate

16

Development ProForma

Investing in Real Estate

Raw Land Cost: $ 5.00 / BSF

Site Improvement Cost: $ 5.00

Base Building Cost: $20.00

Tenant Improvements (TI): $ 5.00

Design, Permits & Soft Costs: $ 4.00 / BSF

Finance Cost: $ 2.00

Leasing Commissions: $ 2.00

Total Cost $43.00 / BSF

Rent $3.25 / SF

Yield 7.55%

Cap Rate 6.00%

Sale Price (Rent/Cap) $54.00

Margin 25.6%

9 Month Construction, ~12 Month Lease-Up – Time Risk!

17

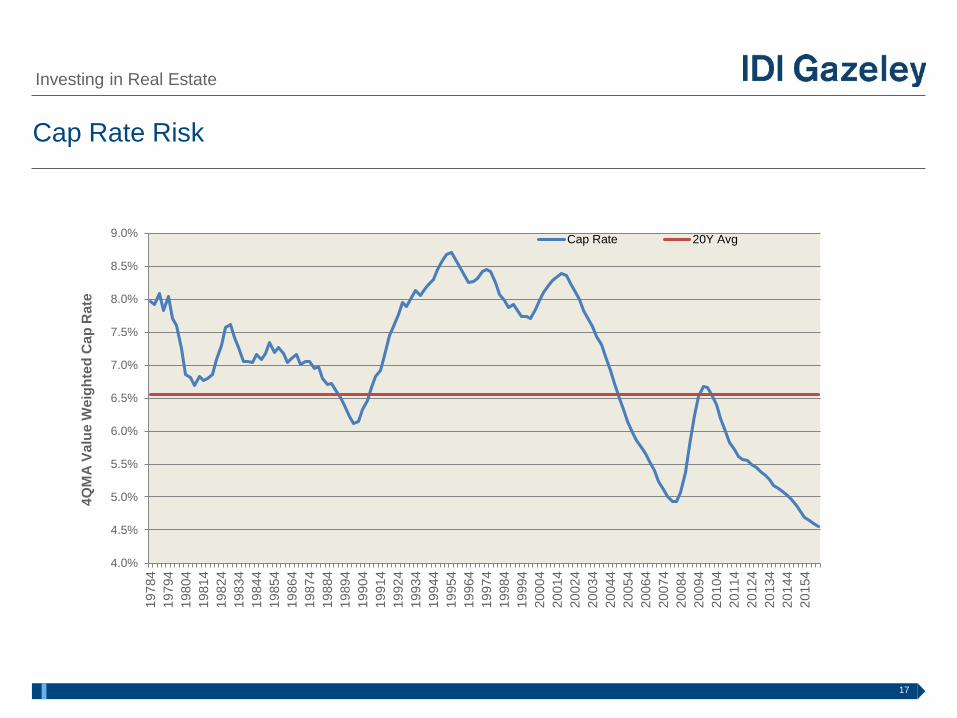

Cap Rate Risk

Investing in Real Estate

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

19

784

19

794

19

804

19

814

19

824

19

834

19

844

19

854

19

864

19

874

19

884

19

894

19

904

19

914

19

924

19

934

19

944

19

954

19

964

19

974

19

984

19

994

20

004

20

014

20

024

20

034

20

044

20

054

20

064

20

074

20

084

20

094

20

104

20

114

20

124

20

134

20

144

20

154

4Q

MA

Va

lue

We

igh

ted

Ca

p R

ate

Cap Rate 20Y Avg

18

NCREIF NPI “Core” Return

Investing in Real Estate

2.40%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

19

78

Q1

19

79

Q1

19

80

Q1

19

81

Q1

19

82

Q1

19

83

Q1

19

84

Q1

19

85

Q1

19

86

Q1

19

87

Q1

19

88

Q1

19

89

Q1

19

90

Q1

19

91

Q1

19

92

Q1

19

93

Q1

19

94

Q1

19

95

Q1

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

Qu

art

erl

y R

etu

rn

Total Return 20Y Average

NCREIF Average Annual Return = 9.95% (Unlevered)

Real Estate Fundamentals

20

Distribution Centers – Take Costs & Time of Supply Chain

Real Estate Fundamentals

21

Population Weighted Map of the US

Real Estate Fundamentals

- 80% of the US population lives in a metropolitan area -

22

Logistics is Balancing Services Levels with Cost Drivers

Real Estate Fundamentals

Source: Establish Inc., Herbert W. Davis and Company, Grubb and Ellis

50%

22%

10%

8%

4%

3%

2%

1%

0%

10%

20%

30%

40%

50%

60%

Tra

nsport

ation

Invento

ry

Lab

or

Custo

me

r S

erv

ice

Ren

t

Adm

in

Sup

plie

s

Oth

er

23

Superior Logistics Infrastructure Drives (Floats) demand for Modern Logistics

Real Estate Fundamentals

24

IDI / Georgia Tech Logistics Infrastructure Index

Real Estate Fundamentals

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

AustinPittsburghLas VegasRichmond

Salt Lake CityHartford

NashvilleSan Antonio

PhoenixNorfolk

CharlotteBoston

PortlandSan DiegoCleveland

DenverCentral Florida

St. LouisJacksonville

HoustonColumbus

MinneapolisSeattleAtlanta

Baltimore / WashingtonKansas City

DetroitPhiladelphia

New Jersey TurnpikeSouth Florida

IndianapolisNorthern California

New York MetroCincinnati

Dallas - Ft. WorthInland Empire

Los AngelesMemphisChicago

Rail Intermodal Index Airport Index Interstate Index

25

Top Logistics Markets in the US

Real Estate Fundamentals

Source: CBRE-EA, IDI Gazeley Research

Focus Market Classification Market Size (Modern Logistics)

Super Regional 20 MSF

Logistics Infrastructure 40 MSF

Highly Constrained

100 MSF

Regional Plus

Large Stabilized

200 MSF

Other

26

Real Estate Fundamentals

Source: IDI Gazeley Research, Costar

Retail E-Commerce Sales Worldwide, 2014-2019

$1.34

$1.67

$2.05

$2.50

$3.02

$3.58

6.3%

8.6%

12.8%

0%

2%

4%

6%

8%

10%

12%

14%

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

2014 2015 2016P 2017F 2018F 2019F

E-C

om

me

rce

Sa

les

(T

rill

ion

s)

Asia North America

Europe Latin America, Middle East, Asia

E-Comm. % of Total Retail Sales

27

Real Estate Fundamentals

Source: IDI Gazeley Research, Costar

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014 2015 2016

Nu

mb

er

of

Fa

cil

itie

s in

No

rth

Am

eri

ca

Fulfillment Sortation Depot

17

191

Amazon Distribution Center Growth in the US

28

Real Estate Fundamentals

Source: IDI Gazeley Research, Federal Reserve Bank

DepotFulfillment Sortation / Distribution

FF

F F

S

F

D

D

15mi /

24km

F S D

DEPOTS

Varies, Vintage (1970|1998), 25’ clear

70-100 KSF

FULFILLMENT CENTERS

Cross Dock, Modern 32’ clear

400-600 KSF

Last Mile Logistics – Amazon Distribution Center Network

29

North America Real Estate Fundamentals

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2007 2010 2013 2016

Mil

lio

ns

SF

Completions Net Absorption Vacancy

• 2016 ended the year with record absorption – 155% of the

historical average.

• Despite new construction, Vacancy continues to fall – down

to 5.5% for total industrial – a record low.

• Continued strength for the larger Super Bulk segment, also

where development is concentrated.

• Light Industrial healthy, but not out performing

• Rents growth healthy, investor demand and pricing remain

high

Source: IDI Gazeley Research, CoStar as of 3q16

MSFCurrent

Ask RentAvail. Vacancy

Trailing 4Q

Abs. MSF

Hist. Avg.

Abs. MSFYears Supply % Normal Abs.

Under Const.

MSF

LI (50-250 KSF) 877.9 $5.76 8.1% 8.1% 36.4 37.4 -0.44 97% 38.4

Bulk (250-600

KSF)729.6 $4.29 12.7% 10.2% 45.0 30.5 0.05 148% 50.7

SB (600 KSF +) 587.9 $3.64 8.9% 8.2% 56.9 24.7 -0.43 230% 69.7

Total Logistics 2,195.4 $4.88 11.1% 8.8% 139.4 90.0 -0.29 155% 158.7

Total Industrial 15,277.5 $6.62 7.8% 5.5% 254.1 251.1 -2.75 101% 203.0

MODERN LOGISTICS SUPPLY AND DEMAND

• Modern Logistics – 1995 and Newer, Warehouses for Rent, 50,000 SF +

• Percent Normal Absorption – Compares the trailing for quarters of absorption of a market or segment to its historical average (2003-2007)

• Years Excess Supply – Calculated as the vacancy over 10% divided by the normal absorption as defined above

HIGHLIGHTS

30

Modern Logistics Construction vs. Net Absorption

• After leveling off, 158.6 MSF currently under construction; 39% pre-lased according to CoStar

• Despite new supply, absorption has tracked well

• Super Bulk Strength – 230% absorption, 8.8% vacancy

• Development limited to institutional investors

-

20

40

60

80

100

120

140

160

180

Mil

lio

ns

SF

Under Construction Trailing 4Q Absorption Historical Average Absorption

31

Net Absorption vs Historic Market Average (Trailing 4Q)

Inland Empire

+ 170%

Dallas

+ 275%

Houston

+ 130%

Fort Lauderdale

+ 153%

Atlanta

+ 150%

Memphis

+ 85%

Chicago

+ 115%

Indianapolis

+ 141%Cincinnati

+ 70%

Central NJ

+ 117%Eastern PA

+ 339%

32

Real Estate Fundamentals

Choosing our Markets

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Market Penetration and Scalability Barriers to New Supply Business Environment Capital Markets

Demographic/Economic Demand and Rent Growth Logistics/Infrastructure

Model Output - Logistics

Case Study – Developing a Building

34

Case Study

• 2/3 of industrial space users in US Lease vs. Own

• Reasons to lease:

o Invest capital in primary business not real estate

o Flexibility to adapt to changing business needs

o Lease Payments align to Operating Income

o Simple Economics - DCF

• Reasons to own:

o Specialized Building / Control

o RE Returns higher than core business

o Simple Economics – DCF

o Sometimes emotional

Leasing versus Owning

35

Development Strategies

Case Study

• Speculative – “Inventory”

• Construct a building empty and lease it up

• Build-to-Suit

• Construct a building for a specific user

• Developer finances – short and long-term

• Owned Land or Neutral Site

• Build-to-Own / Fee Development

• Construct a building for a specific user

• Tenant owns & finances

• Sell land sites to users / other developers

36

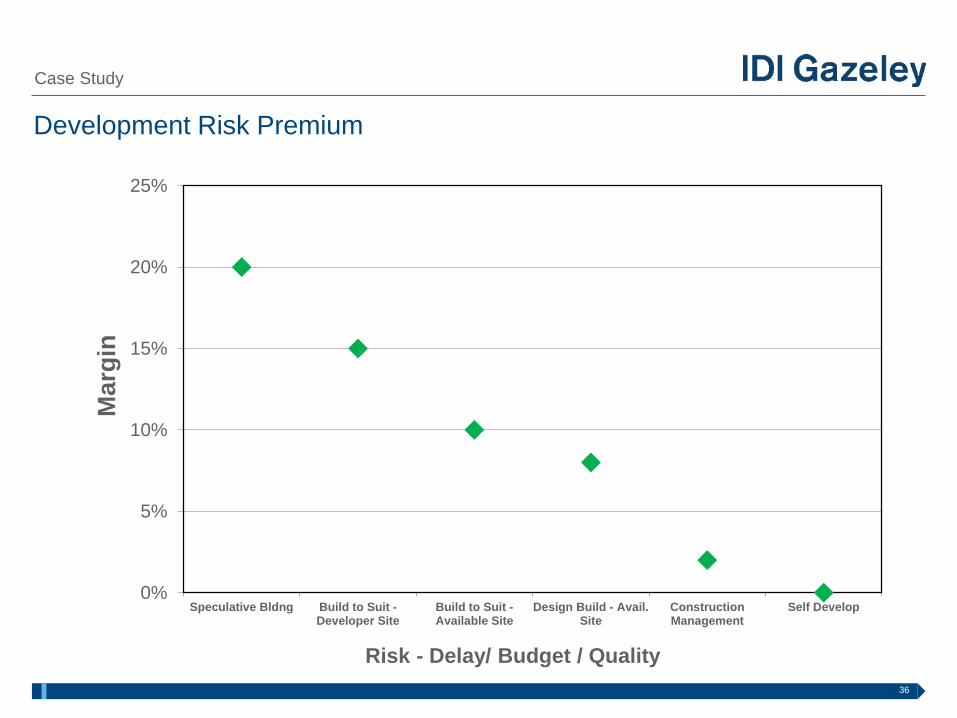

Development Risk Premium

Case Study

0%

5%

10%

15%

20%

25%

Speculative Bldng Build to Suit -Developer Site

Build to Suit -Available Site

Design Build - Avail.Site

ConstructionManagement

Self Develop

Ma

rgin

Risk - Delay/ Budget / Quality

37

Key Players: Who does What

Case Study

Tenant – Occupies space pays “rent” thru either direct monthly rental payment to landlord

or as a cost of capital if building is owned by tenant

Landlord – Building Owner / Investor

• Large institutional investors

o Pension funds sovereign wealth, university endowment

• Real Estate Operating Company and REITs

• Private Investors

• Often held in complicated partnerships and trusts

Developer – Coordinate the activities that convert ideas on paper into real

property. Development, is a multi-faceted business, encompassing activities that range

from the renovation and re-lease of existing buildings to the purchase of raw land and the

sale of improved land or parcels.

38

Key Players: Who does What

Case Study

Government – Regulates land use and approves design including variances. Also critical in

awarding tax incentives and administering municipal infrastructure. Numerous departments

and levels – primarily local, but also state and federal.

Attorneys – Documents purchase & sale, land use and lease agreements, also title review.

Architect & Engineers – Design site and facilities

General Contractor – Coordinates construction activities

Banker – Provides construction / development financing as well as long term debt

Investor – Provides equity investment typically 20 to 50% of project cost

Brokers – Paid a fee to represent tenants or landlords

Property Management – Collects rent, complying with laws and regulations, and maintaining

the property on behalf of the property owner.

39

Eastpoint at Exit 8A

South Brunswick, NJ

• IDI Gazeley’s History in New Jersey

• Site History

• Evaluation Process to go Spec

– Why not Build-to-suit?

– Market Intel – Fundamentals, Competitive Set, Lease Comps, Sale Comps

• Design Process and Consideration

– Rail Easement

– 36’ or 40’ Clear?

– Build trailer storage now or later?

– Access Improvements.

• Project Economics

• Site Plan Approval Process

• Brokerage Team Selection

• Current Status

Case Study

40

• Former Polymer manufacturing plant decommissioned by BASF in 2005. “Brownfield”.

• 2006 IDI Placed Under Contract

– BASF to demolish buildings, handle soil remediation and groundwater contamination.

– BASF to draft a Remedial Action Workplan based upon findings and submit to NJDEP.

– IDI to receive a No Further Action / Covenant Not to Sue from NJDEP as condition of closing.

– Soil remediation can be done quickly, groundwater monitored over time.

• Closing Occurred July of 2008

Case Study

41

Exit 8A Supply and Demand

Case Study

0%

5%

10%

15%

20%

25%

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016ytd.

Mill

ion

s S

F

Completions Net Absorption Vacancy

42

Site Plan

Case Study

43

Access Improvements

Case Study

44

Rendering

Case Study

45

Eastpoint at Exit 8A

South Brunswick, NJ

• IDI Gazeley’s History in New Jersey

• Site History

• Evaluation Process to go Spec

– Why not Build-to-suit?

– Market Intel – Fundamentals, Competitive Set, Lease Comps, Sale Comps

• Design Process and Consideration

– Rail Easement

– 36’ or 40’ Clear?

– Build trailer storage now or later?

– Access Improvements.

• Project Economics

• Site Plan Approval Process

• Brokerage Team Selection

• Current Marketing Status – Economics, ASTI, Etc.

Case Study

Global Differences

47

Milton Keynes Park

48

Milton Keynes, UK

49

Lutterworth, UK

50

Pre-Cast, Sealed Pour, Concrete MFL walls

51

Wooden Timbers (France, Scandanavia, Germany)

52

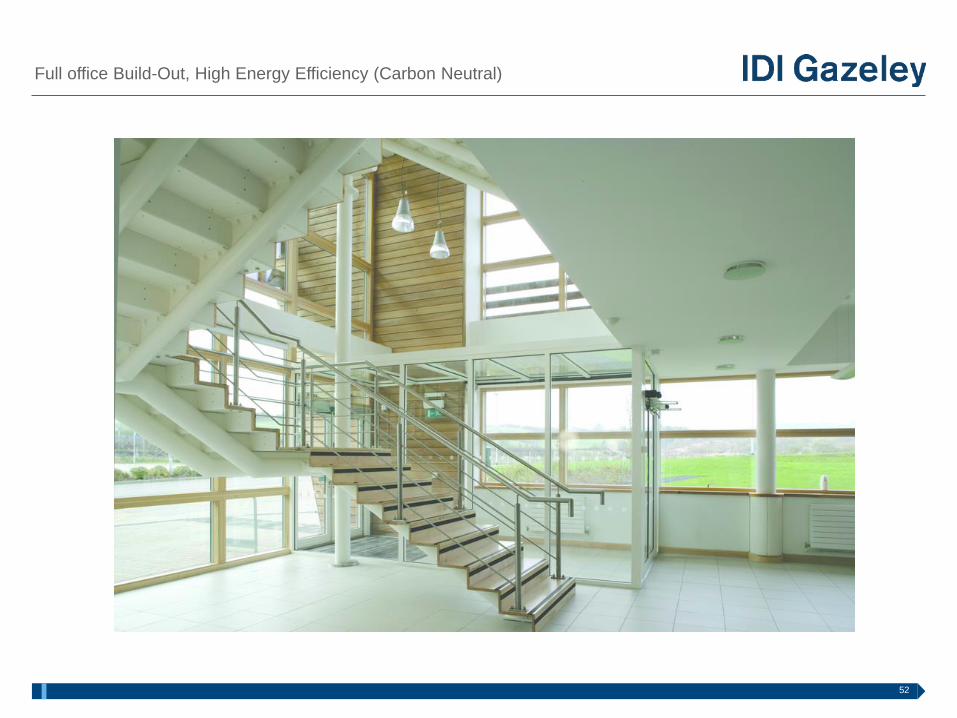

Full office Build-Out, High Energy Efficiency (Carbon Neutral)

53

Wuxi, China (75 West of Shanghai)

54

Wuxi, China

55

Wuxi, China

56

BTS in Dongguan, China (52M NW of Hong Kong)