london accounting developments seminar - typepad accounting developments semin… · accounting...

TRANSCRIPT

London Accounting Developments seminar

www.pwc.co.uk/london

#ADS15 #PALDN

25 November 2015

PwC

Agenda

25 November 2015Accounting developments seminar

2

What’s happening in the economy?

1

Telling the story –Corporate reportingElaine Forrest 2

Accounting regulator activityPeter Hogarth 3

New UK GAAPJennifer Dickie

4

Cyber SecurityWilliam Rimington

5

Coffee Break

Tax reportingRay Farnan

6

Q&A Panel

8

IFRS UpdatePeter Hogarth

7

PwC

Accounting developments seminar

3

What’s happening inthe economy?

Simon O’Brien

125 November 2015

PwC

What’s happening in the economy?

Video available to watch here: http://www.pwc.co.uk/services/economics-policy/insights/uk-economic-outlook/ukeo-nov-15-summary.html

Accounting developments seminar

4

25 November 2015

PwC

Implications of the economy on financial reporting

5

Accounting developments seminar

Reporting of risks &

exposures

Impairment testing and sensitivities

FX, hedgingBusiness

combinations

25 November 2015

PwC

2015 Autumn statement 25 November at 1230pm

Accounting developments seminar

6

25 November 2015

Follow @PwC_UK for live commentary.

Hashtag #AutumnStatement and #SR2015

www.pwc.co.uk/autumnstatement

Topics we predict may be covered...

• More action on avoidance and evasion• Measures for Private Equity, Travel and

Subsistence• The Northern Powerhouse • Reform of business rates • BEPS (Base Erosion and Profit Shifting)

PwC

Upcoming eventshttp://www.pwc.co.uk/events/passionate-about-london-.html

Webcast – 15 December 2015

Accounting developments seminar

7

25 November 2015

Follow the hashtag #PALDN to find out more

One of the main issues for London business right now is talent, skills and finding the next generation of employees.

Our Passionate about London webcast will debate these issues.

PwC

Got a question for us?

Tweet your questions to our speakers throughout the event using hashtag:

#ADS15

Accounting developments seminar

8

25 November 2015

PwC 9

Telling the story –Corporate reporting

Elaine Forrest

225 November 2015Accounting developments seminar

PwC

Relevant risk reporting – Is your risk reporting specific and dynamic enough to bring to life your risk management?4

Telling an authentic story – Is your narrative consistent and coherent throughout?

Weighty tomes – has the continued increase in length of annual reports been at the expense of quality? 1

Measures that matter – Do your KPIs genuinely explain the progress being made?

2

3

What does your reporting say about you?Emerging themes from our review

10

Facing the future – Are you providing the reader with a forward-looking orientation that is clear and consistent?5

Accounting developments seminar

PwC

25 November 2015

PwC

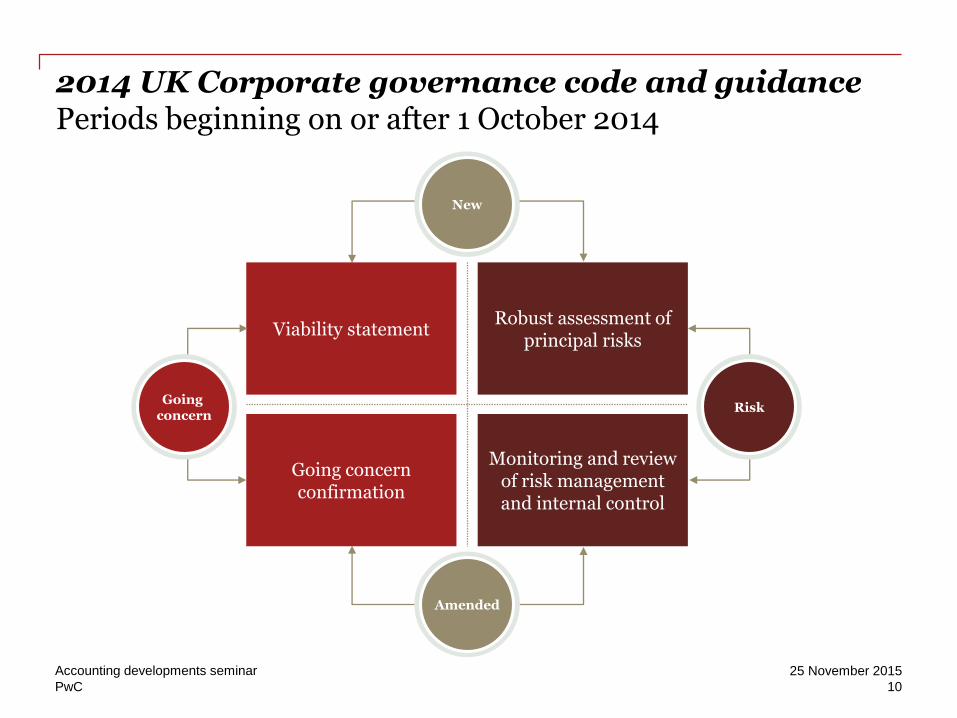

2014 UK Corporate governance code and guidancePeriods beginning on or after 1 October 2014

25 November 2015Accounting developments seminar

10

New

Viability statement

Going concern confirmation

Robust assessment of principal risks

Monitoring and review of risk management and internal control

Amended

Going concern

Risk

PwC

Viability statementsWhat we’ve seen in early examples

12

25 November 2015Accounting developments seminar

Periods chosen –

3 to 5 years

Business plan forecasts usedas basis

Occasional references to other factors

Explanation of process could be more insightful

Particular opportunities on stress testing

Lack of clarity on qualifications or assumptions

PwC

25 November 2015Accounting developments seminar

13

Accounting regulator activity

Peter Hogarth

3

PwC

Spotlight on the accounting regulator – CRRT

25 November 2015Accounting developments seminar

14

1Quality of reporting good, room for improvement for smaller companies

2Clear and concise continues to be a focus

330% of companies approached for further information and explanation; 3 Press Notices and 6 Committee References

4Company responses: good practice guidelines

5Changes to CRRT operating procedures

PwC

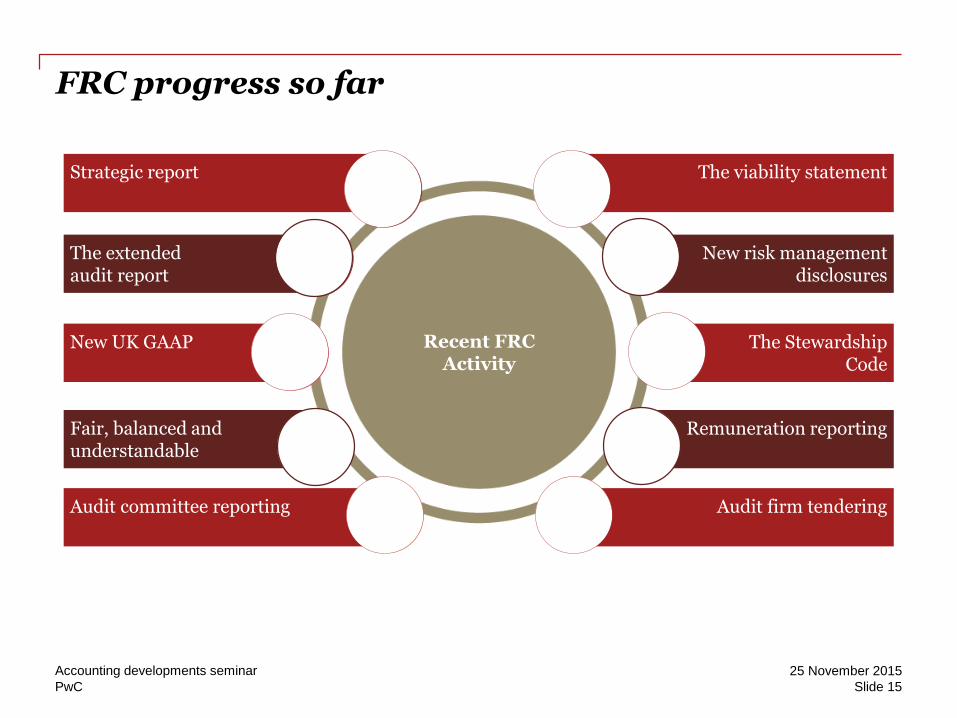

FRC progress so far

25 November 2015Accounting developments seminar

Slide 15

Audit committee reporting

Fair, balanced and understandable

New UK GAAP

The extendedaudit report

Strategic report

Audit firm tendering

Remuneration reporting

The StewardshipCode

New risk management disclosures

The viability statement

Recent FRCActivity

PwC

Development of prior years areas of focus

25 November 2015Accounting developments seminar

16

Involvement of professional expertise

Tax impacts

Clarity of specific nature of judgments applied

Include IAS 1 sensitivity analysis

Disclosed benefits vs intangibles recognised

Accounting policy needed

Auditors’ and Audit Committee reports used

Clear disclosure of significant estimates

Expect to see more intangibles

Items which enhance rather than distract

Exceptional items Significant judgements

Estimates and sensitivities

Business combinations and separate intangibles

PwC

Areas of focus for 2015/16

25 November 2015Accounting developments seminar

17

Applicationof materiality

judgements

Complex supplier

arrangementsPensions

Revenue Cash flow statements

Tax

PwC

FRC priority sectors

25 November 2015Accounting developments seminar

18

• Insurance

• Food, drink and consumer goods manufacturers and retailers

• Companies servicing the extractive industries

• Business services

• Support services

• IT (including software companies)

2014/15

2015/16

PwC

25 November 2015Accounting developments seminar

19

New UK GAAP

Jennifer Dickie

4

PwC

New UK GAAPTemperature test

20

Q: Have you started to look at New UK GAAP?

1. We’ve been working on it since last year’s ADS

2. We’ve started thinking about it

3. Not yet – we don’t need to think about it till we report next year

25 November 2015Accounting developments seminar

PwC

New UK GAAP is here!

21

25 November 2015Accounting developments seminar

PwC

PwC

• Qualifying entities

• Notify shareholders

FRS 101 – IFRS with disclosure exemptions

• FRS 100 – Application of financial reporting requirements

• FRS 103 – Insurance contracts

• FRS 104 – Interim financial reporting

• FRS 105 – Micro-entities

What else is there?

22

New UK GAAP frameworkRecap

25 November 2015Accounting developments seminar

FRS 102 – The ‘New UK GAAP’

• All entities except groups listed on an EU regulated market

• Notify shareholders of reduced disclosures

PwC

Changes to Company Law and new UK GAAP

• Effective date 1 January 2016 for most changes

• Main impact of changes on small and micro companies

• Consolidation exemption conditions changed

• A full list of related undertakings (direct and indirect) is required for accounts approved after 1 July 2015

• IFRS formats for P&L and balance sheet allowed

New EU Accounting Directive now implemented into Company Law (SI 2015/980)

1

New UK GAAP standards a moving target until recently2

23

25 November 2015Accounting developments seminar

PwC

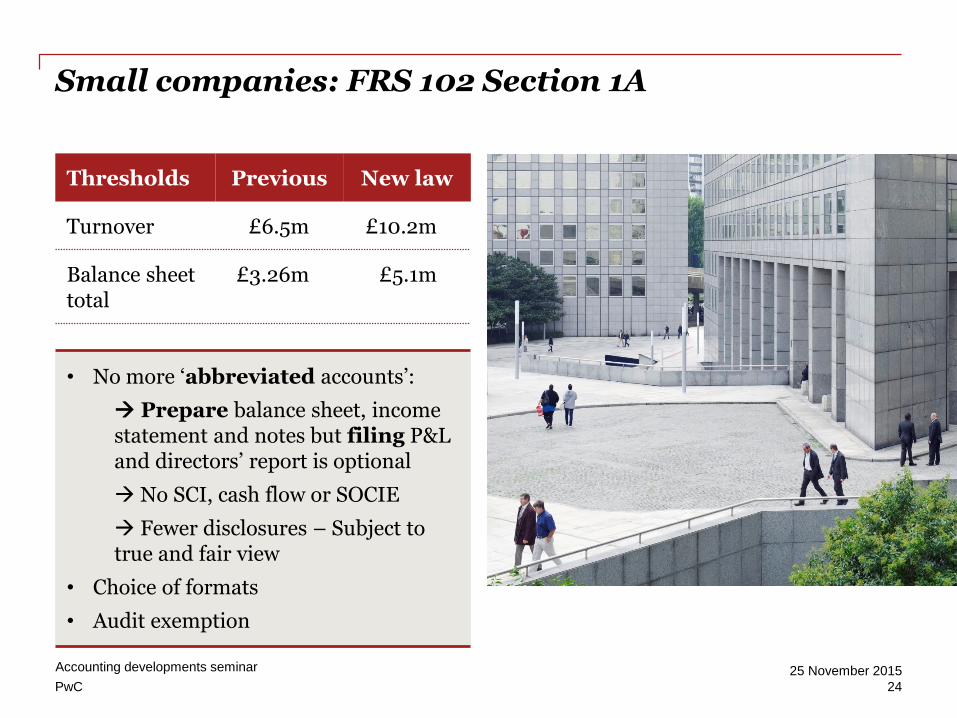

Small companies: FRS 102 Section 1A

24

Thresholds Previous New law

Turnover £6.5m £10.2m

Balance sheet total

£3.26m £5.1m

• No more ‘abbreviated accounts’:

Prepare balance sheet, income statement and notes but filing P&L and directors’ report is optional

No SCI, cash flow or SOCIE

Fewer disclosures – Subject to true and fair view

• Choice of formats

• Audit exemption

25 November 2015Accounting developments seminar

PwC

FRS 102Measurement changes vs. old UK GAAP

25 November 2015Accounting developments seminar

25

Ta

ng

ible

assets

Sh

are b

ased

pa

ym

ents

Leases

Post employment benefits

Intangible assets

Other employee benefits

Capitalisation of borrowing costs

Business combinations

Deferred tax

Investment propertiesFinancial instruments

Deriv

ativ

es

Hed

gin

gC

ash

an

d ca

sh eq

uiv

alen

ts

Comparative information

PwC

FRS 102Measurement changes vs. old UK GAAP

25 November 2015Accounting developments seminar

26

1. Off-market intercompany loans

2. Forward contract

3. Business combinations

4. Deferred tax

Areas we will cover

Debt restructuring

Investment property

Other key areas

PwC

FRS 102 Company background

New GAAP Limited

Parent Co

Sub 1 Sub 2 Sub 3

Sub 4

27

25 November 2015Accounting developments seminar

PwC

FRS 102 Scenario 1Off-market intercompany loans: Old UK GAAP

28

New GAAP Limited

Parent Co• £100m lent in 2012

• 10 year term, bears interest at fixed rate of 10%

• Market rate of interest 15%

£100m @ 10%

25 November 2015Accounting developments seminar

Sub 1 Sub 3

Old UK GAAP (FRS 4):

Net proceeds

PwC

FRS 102 Scenario 1Off-market intercompany loans: FRS 102

BasicAmortised cost (Section 11)

ComplexFair value P&L (Section 12)

• Basic – amortised cost

Basic or complex? 1

29

25 November 2015Accounting developments seminar

PwC

FRS 102 Scenario 1Off-market intercompany loans: FRS 102

• Recognise at face value

• Basic – amortised cost

Basic or complex? 1

• Initial measurement of basic loan at fair value

Is it a financing arrangement? 2

Is it repayable on demand?3

30

25 November 2015Accounting developments seminar

PwC

FRS 102 Scenario 2 Forward contract – Old UK GAAP

• Foreign currency debtor €100m

• Due in 3 months time

• Forward contract taken out to fix the price at £

• Revenue and debtor recorded at forward contract rate

31

25 November 2015Accounting developments seminar

New GAAP

LimitedBANK

In 3 months:• pay €100m

• receive £75m

Debtor €100m

Old UK GAAP:

Presented as £75m

PwC

FRS 102 Scenario 2Forward contract – FRS 102

32

25 November 2015Accounting developments seminar

• Translate sale and debtor at transaction spot rate

• Retranslate debtor over 3 month period, difference in P&L

• Derivative recognised on the balance sheet at fair value

New GAAP

LimitedBANK

In 3 months:• pay €100m

• receive £75m

Debtor €100m

PwC

FRS 102 Scenario 3Business combinations and intangibles – Old UK GAAP

Goodwill

• Acquired ABC Ltd in October 2014

• Consol b/s: £m

FV consideration x

FV net assets (x)

Goodwill x

• 20 year life

Acquired assets

• Computer software acquired = tangible asset

• No deferred tax recognised

New GAAP Limited

ABC Ltd

33

25 November 2015Accounting developments seminar

PwC

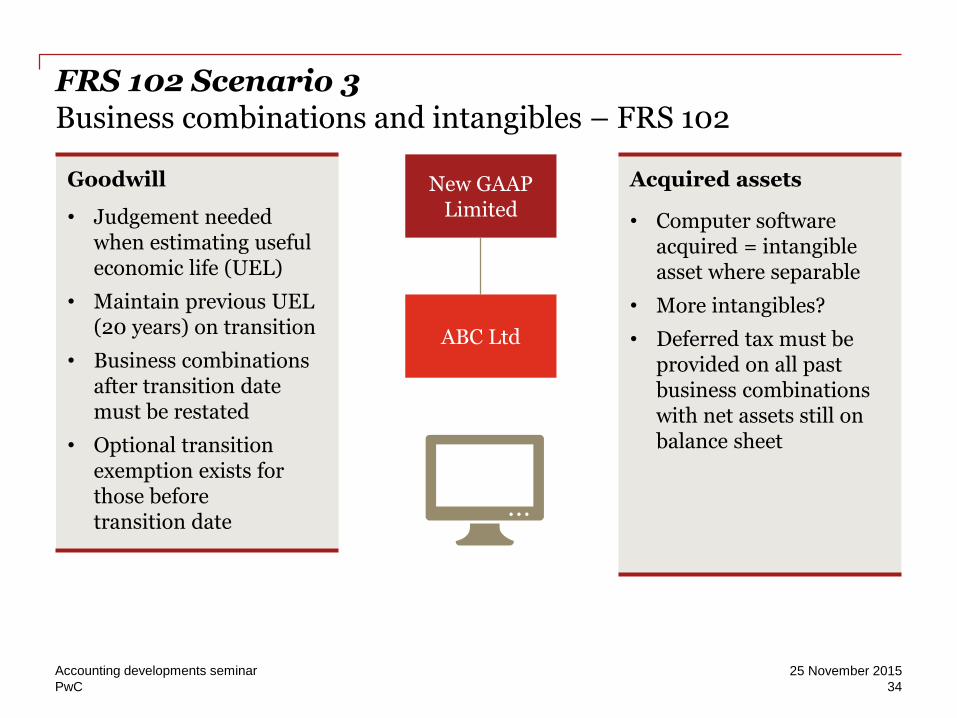

FRS 102 Scenario 3Business combinations and intangibles – FRS 102

34

25 November 2015Accounting developments seminar

Goodwill

• Judgement needed when estimating useful economic life (UEL)

• Maintain previous UEL (20 years) on transition

• Business combinations after transition date must be restated

• Optional transition exemption exists for those before transition date

Acquired assets

• Computer software acquired = intangible asset where separable

• More intangibles?

• Deferred tax must be provided on all past business combinations with net assets still on balance sheet

New GAAP Limited

ABC Ltd

PwC

FRS 102 Scenario 4 Deferred tax – Old UK GAAP

Revalued building

New GAAP

35

25 November 2015Accounting developments seminar

Deferred tax may be discounted

PwC

FRS 102 Scenario 4 Deferred tax – FRS 102

Timing differences ‘plus’ approach

Revalued building

Deferred tax provided on revaluation of non-monetary assets

Deferred tax is not discounted

36

25 November 2015Accounting developments seminar

PwC

Transition truth or myth?

Truth Myth

37

25 November 2015Accounting developments seminar

Business combinations1

Third balance sheet needed2

Shareholder notification FRS 1023

Shareholder notification on transition4

Transition date5

Dormant companies6

PwC

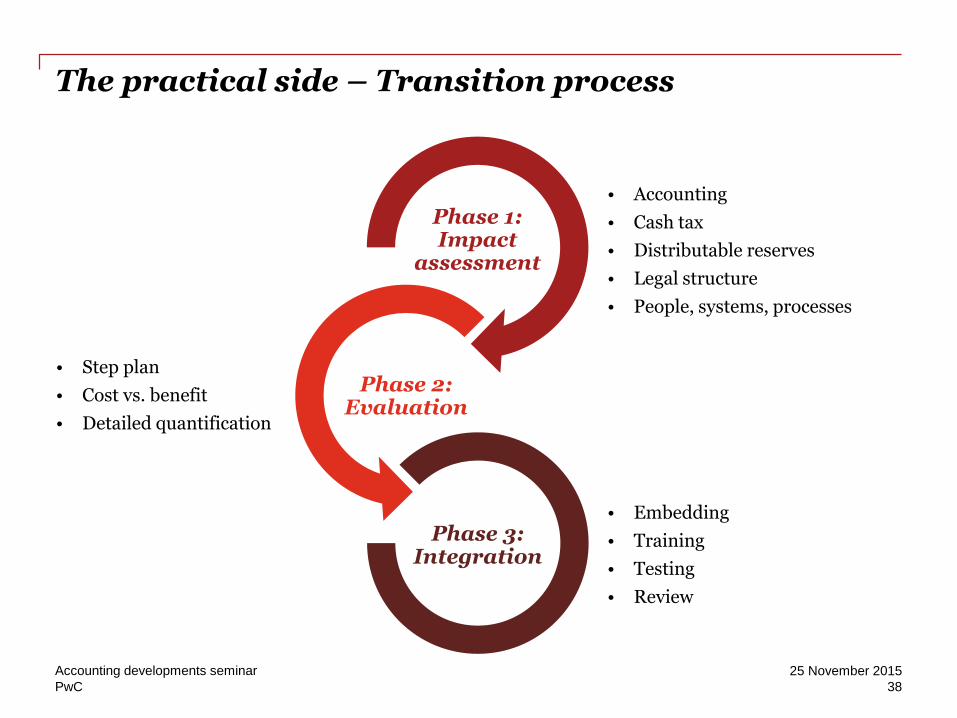

The practical side – Transition process

38

25 November 2015Accounting developments seminar

• Accounting

• Cash tax

• Distributable reserves

• Legal structure

• People, systems, processes

Phase 1: Impact

assessment

Phase 2: Evaluation

Phase 3: Integration

• Step plan

• Cost vs. benefit

• Detailed quantification

• Embedding

• Training

• Testing

• Review

PwC

The practical side – FRS 102 transition checklist

39

25 November 2015Accounting developments seminar

Restate comparatives Explain impact Balance sheet and P&L

reconciliations, including opening period

Other reconciliations as considered useful

Update policies Update notes

PwC

Disclosure when adopting FRS 102

All entities

Qualifying entity exemptions

(if applicable)

Primary statements

Transition

Judgements and

estimates

Statement of

compliance

40

25 November 2015Accounting developments seminar

PwC

Other possible disclosures

41

25 November 2015Accounting developments seminar

Financial instruments(including fair value)

1 Deferred tax2

Joint ventures3Investment properties (including FV)

4

Defined benefit plans5 Business combinations6

PwC

Help is available

• Practical guides

• Similarities and differences publication

• PwC ‘Manual of accounting – NewUK GAAP’ (2nd edition)

• FRS 102 and FRS 101 Illustrative accounts

• Reporting Impact Assessment

• FRS 102 roll forward

• PwC Treasury, Structuring, Tax, Accounting Advisory and Pensions

• PwC Inform – New UK GAAP branch

42

25 November 2015Accounting developments seminar

PwC

25 November 2015Accounting developments seminar

43

Cyber Security

William Rimington

5

PwC 44

25 November 2015Accounting developments Seminar

Sources of cyber attacks

INSIDER

Nation State Hacktivism

Organised Crime

Cyber Terrorists

45

25 November 2015Accounting Developments SeminarPwC

Our unique selling points

• Integrated services

• In-house legal expertise

• Ranked #1 by Gartner

• Access to clients and reach

• Breach aid

• CSIR certified to deal with cyber attacks

46

25 November 2015Accounting Developments seminarPwC

To help us service our clients, we’ve teamed up with a few

alliance partners

47

25 November 2015Accounting Developments Seminar

Building confidence in your digital future

Seize the advantageWe help you exploit digital opportunity with confidence

• Compliance with privacy and regulation• Digital trust is embedded in the strategy• Risk management and risk appetite

You can’t secure everythingWe help you set the right priorities

• Enterprise security architecture• Protect what matters• Strategy, organisation, governance• Threat intelligence

It’s not if but whenWe help you build an intelligence-led defence, enabling rapid cyber response

• Continuity and resilience• Crisis management• Incident response• Monitoring and detection

Fix the basicsWe help you use technology to your advantage, deriving maximum return from your technology investments

• Identity and access management• Information technology hygiene• Information technology, operations technology and

consumer technology• Security intelligence and analytics

Their risk is your riskWe help you understand and manage risk in your interconnected business ecosystem

• Digital channels• Partner and supplier management• Robust contracts

People matterWe help you build and maintain a secure culture, where people are aware of their critical security decisions

• Insider threat management• People and ‘Moments that Matter’• Security culture and awareness

48

25 November 2015Accounting Developments SeminarPwC

Our cyber security services

Build and assure

defences

Navigate legal and

regulatory landscape

Identify and respond

to attacks

We are unique in providing integrated, market-leading cyber security services

49

25 November 2015Accounting Developments SeminarPwC

PwC

25 November 2015Accounting developments seminar

50

Coffee break

Visit our stands…

Social media help desk

PwC Inform

The IPO Journey

My Taxpartner

PwC

25 November 2015Accounting developments seminar

51

Tax

Ray Farnan

6

PwC

Agenda

November 2015

Slide 52

Emerging tax issues

• EC State aid reviews

• OECD’s Base Erosion and Profit Shifting (BEPS) action plan

• Countries’ unilateral actions

Uncertainty over Income Tax Treatments – Draft IFRIC interpretation

1

Meet the experts

2

PwC

Emerging Tax issues

November 2015

Slide 53

Meet the experts

PwC

EU State aid

November 2015

Slide 54

Major European tax initiative

• EU law defines ‘State aid’ as an advantagein any form that is conferred on a selective basis to undertakings by national public authorities.

• The European Commission (EC) is using State aid laws to challenge corporate tax rulings.

• If State aid is determined to have been granted:

- EC can force country to collect from companies up to 10 years of tax savings (plus interest) based on benefit received.

- Expect adjustment or contingency to be accounted for under IAS 12 rules.

• Management’s accounting conclusion should be consistent with IAS 12 recognition and measurement principles for uncertain tax positions.

Recent EC’s investigations

• Challenges to several tax arrangements of large MNCs within European countries.

Meet the experts

PwC

EU State aid

November 2015

Slide 55

What are the next steps?

• Quantification of amounts to be repaid.

• Further litigation on the cases with final decisions?

• Further final rulings are expected in the near future.

• Tax authorities are to share ‘rulings’ with each other under the EU transparency initiatives. Which may lead to further investigations.

What should companies be doing?

• Understand if they have received any rulings or potentially preferential treatment from EU taxing authorities.

• Document with appropriate analyses/support any uncertain positions.

• Determine if any disclosure regarding State Aid risk is appropriate.

Meet the experts

PwC

EU State aid – US companies’ disclosures

November 2015

Slide 56

Location of disclosures

Income tax note

Directors report

Significant risks

Meet the experts

Examples

“If the European Commission were to conclude against Ireland, the European Commission could require Ireland to recover from the Company past taxes covering a period of up to 10 years reflective of the disallowed state aid. While such amount could be material, as of June 27, 2015 the Company is unable to estimate the impact.”

– (Apple)

“The outcome of the European Commission’s investigations could require changes to existing tax rulings that, in turn, could have an impact on the company’s taxes.”

– (Zoetis)

PwC

OECD’s BEPS actions

November 2015

Slide 57

Action 1Address the challenges of the digital economy

Action 2Neutralise the effect of hybrid mismatch arrangements

Action 3Strengthen CFC rules

Action 4Limit base erosion via interest deductions and other financial payments

Action 5Counter harmful tax practices more effectively

Action 6Prevent treaty abuse

Action 7Prevent the artificial avoidance of PE status

Action 8Assuring that TP outcomes are in line with value creation: Intangibles

Action 9Assuring that TP outcomes are in line with value creation: Risks and Capital

Action 10Assuring that TP outcomes are in line with value creation: Other high-risk transactions

Action 11Establish methodologies to collect and analyse data on BEPS and the actions to address it

Action 12Require taxpayers to disclose their aggressive tax planning arrangements

Action 13Re-examine transfer pricing documentation

Action 14Make dispute resolution mechanisms more effective

Action 15Develop a multilateral instrument

Actions that may have potential tax accounting implications, e.g. uncertain tax positions, outside basis implications, transparent entity accounting, increase in tax accounting compliance, etc.

Meet the experts

PwC

Practical challengesQuestions of definition vs. accounting

November 2015

Slide 58

Tax jurisdiction

Revenues Profit(loss) before income tax

Incometax paid (on cash basis)

Income taxes accrued –currentyear

Stated capital

Accumulatedearnings

Number of full time employees

Tangible assets (other than cash and cash equivalents)

Unrelated party

Related party

Total

Treatment of branches/pass

through entities?

CFC taxation?

Leases? Inventory?

Treatment of contractors?

Inclusion of dormant vs. liquidated entities?

What comprises net sales?

Clarification of PY adjustments?

Permanent establishments?

Additional non-share capital? Basis of calculation? (pre-acq included?)

Meet the experts

PwC

Unilateral actions

November 2015

Slide 59

Country Actions Tax accounting considerations

EU State aid, transparency packages UTPs, disclosures

United Kingdom Diverted profits tax, tax transparency proposals

UTPs, disclosures

Australia expansion of anti-avoidance rules, disclosure of certain tax information, tax transparency code proposal

UTPs, disclosures

Ireland elimination of a ‘double Irish’ structure UTPs

France anti-hybrid rules UTPs, transparent entity accounting

Meet the experts

PwC

Uncertainty over Income Tax Treatments – Draft IFRIC Interpretation

November 2015

Slide 60

Meet the experts

PwC

Uncertainty over Income Tax Treatments

November 2015

Slide 61

Now January 2016 June 2016 December 2016

Educate

Respond

Identify

Policy

Document

Disclosures

Controls

Monitor

Quantify

Action plan

Meet the experts

Key areas covered by the draft interpretation

• Scope

• Unit of account

• Detection risk

• Recognition and measurement

• Changes in recognition and measurement

• Disclosures

• Transition

What are the key implications

• Formal structure

• Potential measurement differences

• Impact on disclosures and expectations

PwC

25 November 2015Accounting developments seminar

62

IFRS accounting update

What’s new in 2015/16?

What’s in the pipeline after 2015/16?

Peter Hogarth 7

PwC

Not much!

What’s new in 2015?

63

25 November 2015Accounting developments seminar

PwC

Amendments effective this year

64

Standard Nature of amendment

IAS 19, ‘Employee benefits’ Employee contributions

Annual improvements Various

25 November 2015Accounting developments seminar

PwC

A little more change next year

65

Standard Nature of amendment

IFRS 14, ‘Regulatory deferral accounts’ Rate-regulated activities

Amendments to IFRSs 10, 11 and IAS 28 Acquisition of interests

IASs 16 and 38 Methods of depreciation

IAS 1 ‘Disclosure initiative’

IFRS 10 and IAS 28 Investment entities

Annual improvements Various

25 November 2015Accounting developments seminar

EU endorsement is still pending for most standard changes

PwC

What’s next? The ‘big three’

66

• Published July 2014

• Effective 2018

• EFRAG predict EU endorsement before end of 2015

25 November 2015Accounting developments seminar

IFRS 9 Financial instruments

IFRS 15 Revenue

Leases

• Published May 2014

• Effective 2018

• EFRAG predict EU endorsement soon

• IASB and FASB proposing amendments already

• May be published before end of 2015

• (Almost) all leases on-balance sheet

• IASB to treat all leases like finance leases; FASB to classify leases for P&L purposes

PwC

25 November 2015Accounting developments seminar

67

IFRS 15

PwC

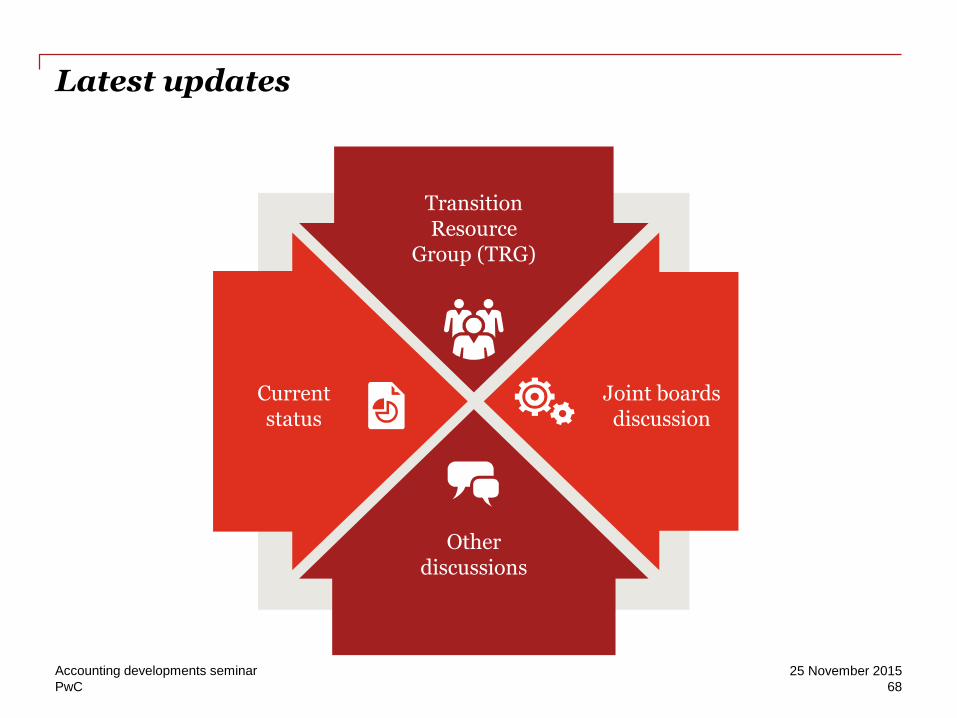

Latest updates

68

Current status

Joint boards discussion

Transition Resource

Group (TRG)

Other discussions

25 November 2015Accounting developments seminar

PwC

IFRS 15 - Practical considerations

There are likely to be many interested parties, in the implementation of this new standard, with impacts far outside the finance function:

Sales staff – How are they incentivised? Based on revenue? Will that change?

Licensing/legal –Opportunities to change contractual terms - can they or should they change given new rules?

Budgeting – how is this factored into budgets/5 year plans?

Investor relations – how and when is this communicated to the market?

IT – what new data needs to be collected for e.g. new estimates or disclosure, and will there be a requirement to change current systems?

Controls – New processes and controls required, including controls over the impact of estimation

25

Accounting developments seminar 25 November 2015

PwC

25 November 2015Accounting developments seminar

70

[IFRS 16] – Leasing

PwC

Timeline

71

ED Published

Aug 2010

New ED published

May 2013

Expected final standard

Q4 2015

Discussion paper issued

Re-deliberations began

Re-deliberations began

Mar 2009 Jan 2011 Mar 2014

Effective date: TBD EU Endorsement: TBD

25 November 2015Accounting developments seminar

PwC

Lessee accounting

72

• All leases on Balance Sheet as with finance leases under IAS 17

• Exemptions for short term leases and leases of low value assets ($5,000)

Single approach

• Right of use (ROU) asset

• Lease liabilityBalance sheet

• Amortisation expense

• Interest expense

Income statement

25 November 2015Accounting developments seminar

PwC

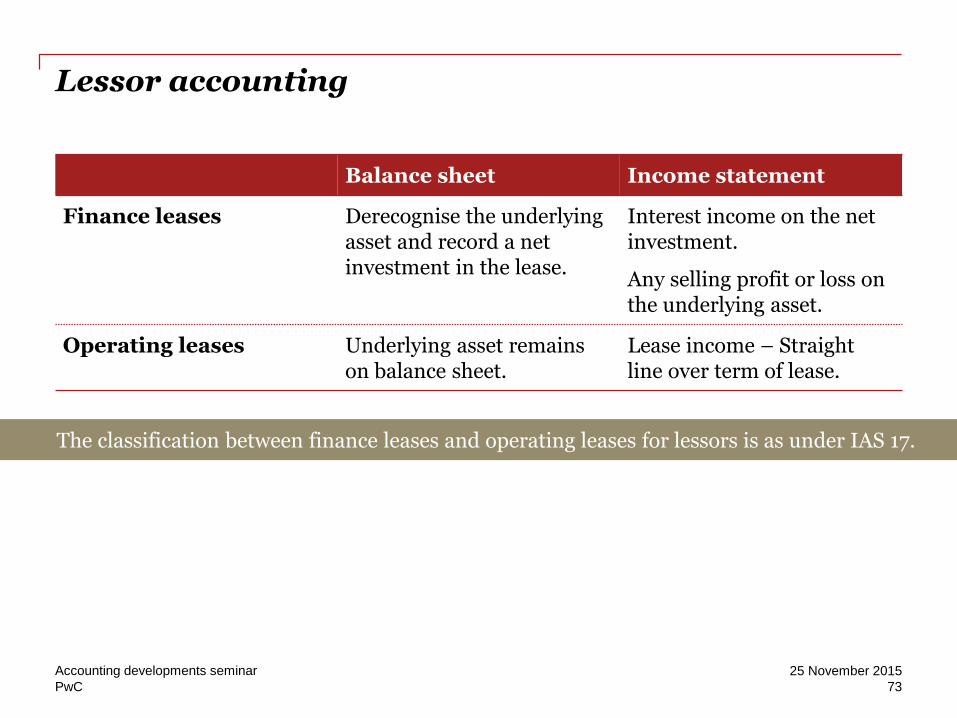

Lessor accounting

73

The classification between finance leases and operating leases for lessors is as under IAS 17.

Balance sheet Income statement

Finance leases Derecognise the underlying asset and record a net investment in the lease.

Interest income on the net investment.

Any selling profit or loss on the underlying asset.

Operating leases Underlying asset remains on balance sheet.

Lease income – Straight line over term of lease.

25 November 2015Accounting developments seminar

PwC

Help is available

• Practical guides and In Depths

• Similarities and differences publication

• PwC IFRS Manual of accounting

• IFRS Illustrative accounts

• PwC Treasury, Structuring, Tax, Accounting Advisory and Pensions

• PwC Inform

• Pocket guides

74

25 November 2015Accounting developments seminar

PwC

25 November 2015Accounting developments seminar

75

Q&A panel

9

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the

information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the

accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members,

employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to

act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to the UK member firm, and may sometimes refer to the PwC

network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

151008-184212-HH-OS

Thank you