london november 20, 2003 aesc european conference new leadership for a changing europe why ceos fall...

TRANSCRIPT

LondonLondonNovember 20, 2003November 20, 2003

AESC European ConferenceAESC European ConferenceNew Leadership for a Changing EuropeNew Leadership for a Changing Europe

Why CEOs FallWhy CEOs FallA Global Perspective on CEO TurnoverA Global Perspective on CEO Turnover

2

Today’s Agenda: Addressing Three Key QuestionsToday’s Agenda: Addressing Three Key Questions

Why has leadership become so difficult Why has leadership become so difficult and risky?and risky?

Why has life at the top become nasty, Why has life at the top become nasty, brutish and short?brutish and short?

So, what do we do about this mess?So, what do we do about this mess?

The Leadership ChallengeThe Leadership Challenge

4

Today’s management challengesToday’s management challenges

Growth (innovation, technology evolution, new shape of growth in developed Growth (innovation, technology evolution, new shape of growth in developed economies, etc.)economies, etc.)

Demanding customers (audience fragmentation, CRM, smart customization, etc.)Demanding customers (audience fragmentation, CRM, smart customization, etc.)

ROI (marketing and sales effectiveness)ROI (marketing and sales effectiveness)

New Competition (disaggregating value chains, Innovator’s dilemma, emerging New Competition (disaggregating value chains, Innovator’s dilemma, emerging markets, etc.)markets, etc.)

‘‘Glocalisation’ (linking economies of scale and scope with local execution)Glocalisation’ (linking economies of scale and scope with local execution)

The Human Factor (labor mobility, war for talent, how do values create value, The Human Factor (labor mobility, war for talent, how do values create value, alignment, etc.)alignment, etc.)

5

… but also… but also

Discontinuities (9/11, X-rates, capital markets, etc.)Discontinuities (9/11, X-rates, capital markets, etc.)

Wayward CEOs and Corporate scandalsWayward CEOs and Corporate scandals

Corporate GovernanceCorporate Governance

Shareholder activismShareholder activism

6

One big theme that underlies these trends…One big theme that underlies these trends…

Meta-networks

Complex options

Competition

Transparency

Asymmetric Risk

““Managing Managing complexity in a complexity in a

world of continual, world of continual, discontinuous discontinuous

change”change”

Life at the TopLife at the Top

8

Booz Allen’s 2002 CEO Succession StudyBooz Allen’s 2002 CEO Succession Study

Largest worldwide study to examine the causes of failure of Chief Executives

Annual study at the world’s largest (by market cap.) 2,500 public companies

– 65% in the US

– 23% in Europe

– 12% Japan and rest of APJ

Examined CEO succession events during 1995, 1998, 2000, 2001 and 2002

– Age and Tenure

– Insider/Outsider status

– Type of Succession (regular, merger driven, forced)

– Education and previous position

– Total company shareholder return rates during tenure

9

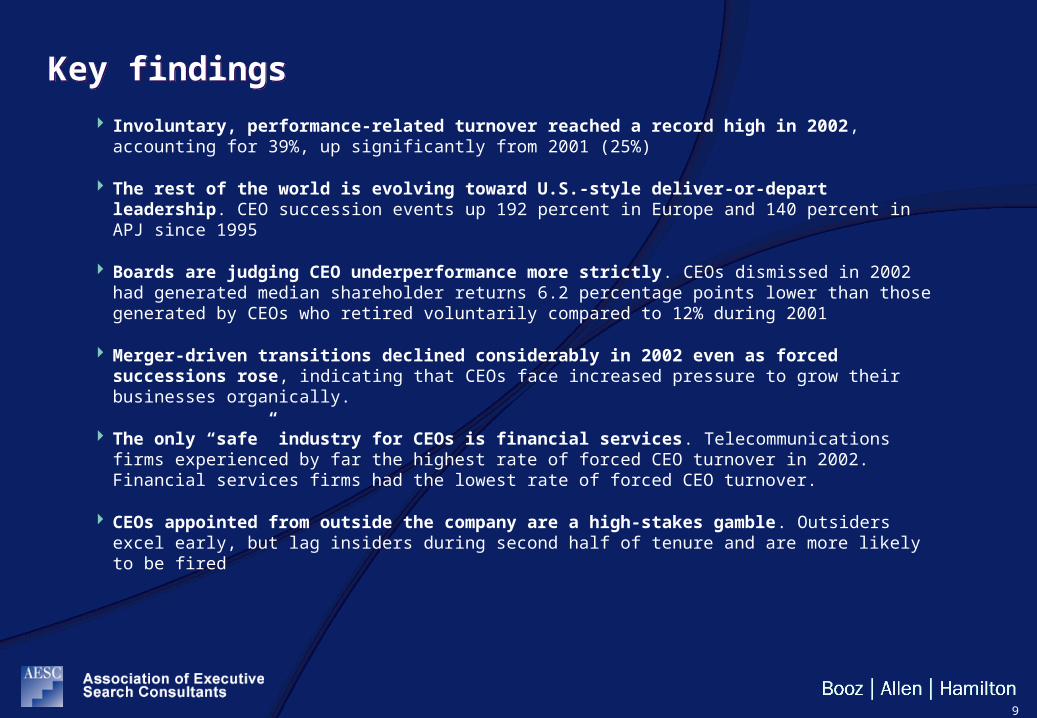

Key findingsKey findings

Involuntary, performance-related turnover reached a record high in 2002, accounting for 39%, up significantly from 2001 (25%)

The rest of the world is evolving toward U.S.-style deliver-or-depart leadership. CEO succession events up 192 percent in Europe and 140 percent in APJ since 1995

Boards are judging CEO underperformance more strictly. CEOs dismissed in 2002 had generated median shareholder returns 6.2 percentage points lower than those generated by CEOs who retired voluntarily compared to 12% during 2001

Merger-driven transitions declined considerably in 2002 even as forced successions rose, indicating that CEOs face increased pressure to grow their businesses organically.

The only “safe” industry for CEOs is financial services. Telecommunications firms experienced by far the highest rate of forced CEO turnover in 2002. Financial services firms had the lowest rate of forced CEO turnover.

CEOs appointed from outside the company are a high-stakes gamble. Outsiders excel early, but lag insiders during second half of tenure and are more likely to be fired

10

North America still leads in rate of CEO successionsNorth America still leads in rate of CEO successions

253 global succession events during 2002 (10.1%)

Succession rate in Europe is catching up.

Sharp increases also seen in Japan and rest of Asia.

3.5% 3.0%4.9%

6.2%4.3%

2.3%

9.8%

2.2%3.3%

8.4%

4.1%

1.9%

10.5% 10.2%8.5% 8.6%

10.3%10.6%

17.9%

13.5%

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

16.0%18.0%

20.0%

North America Europe Japan Rest of Asia/Pacific

1995 1998 2000 2001 2002

Regional Succession Rates Among Top CompaniesRegional Succession Rates Among Top Companies

11

Rate of performance-related successions rose 70% over 2001 Rate of performance-related successions rose 70% over 2001

Forced events made up 39 percent of the global total last year; in 2001, they accounted for one-quarter of all successions.

Mergers drove only 15 percent of succession events in 2002

– compared with 27 percent in 2001 and 29 percent in 2000

Global Results of CEO SuccessionGlobal Results of CEO Succession

Regular 4.2%

1995

3.6%

1998

4.8%

2000

4.4%

2001

4.7%

2002

Performance-Related 1.0% 1.9% 3.2% 2.3% 3.9%

Merger-Driven 0.8% 1.9% 3.2% 2.5% 1.5%

12

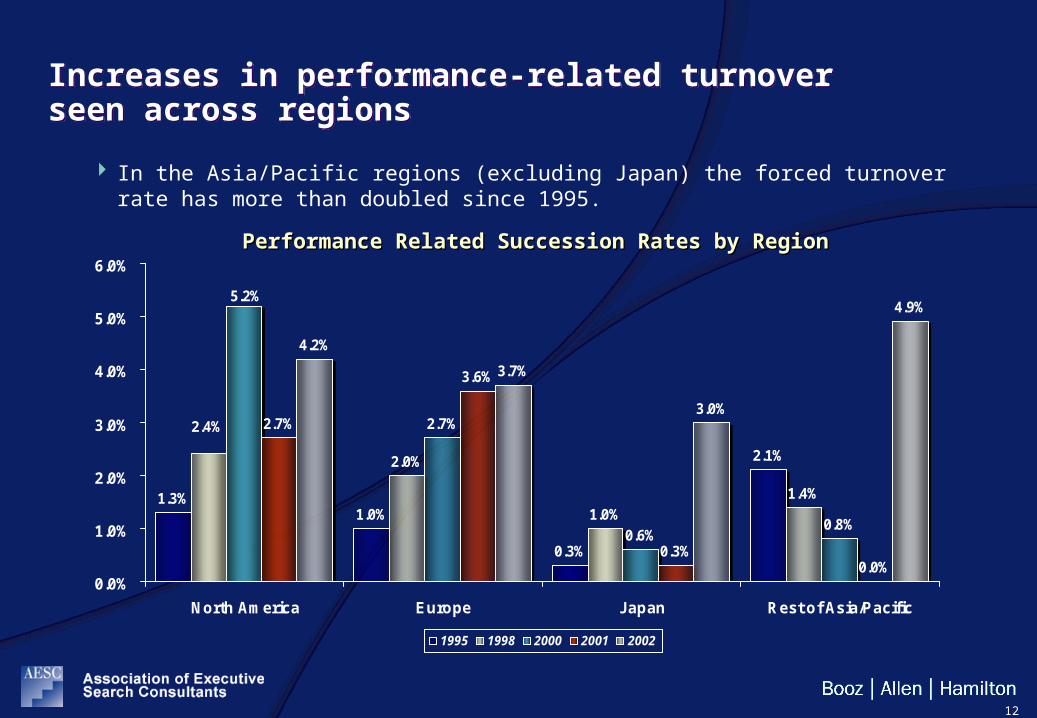

Increases in performance-related turnover seen across regions Increases in performance-related turnover seen across regions

In the Asia/Pacific regions (excluding Japan) the forced turnover rate has more than doubled since 1995.

1.3%1.0%

0.3%

2.1%2.0%

1.0%1.4%

2.7%

0.6%0.8%

2.7%

3.6%

0.3%0.0%

4.2%

3.7%

3.0%

4.9%

2.4%

5.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

North America Europe Japan Rest of Asia/Pacific

1995 1998 2000 2001 2002

Performance Related Succession Rates by RegionPerformance Related Succession Rates by Region

13

Performance mattersPerformance matters

Poor shareholder performance continues to drive forced turnover.

For departing “class of 2002” performance gap was 6.2 points, half of what prompted dismissal during 2001 (11.9%) and even less than in 2000 (13.5%)

Media Shareholder Returns, by Reason for SuccessionMedia Shareholder Returns, by Reason for Succession

Regular 2.1%

1995

0.8%

1998

-4.3%

2000

2.0%

2001

4.8%

2002

Performance-Related -3.1% -4.5% -17.8% -9.9% -1.4%

Return Gap 5.2 pts 5.3 pts 13.5 pts 11.9 pts 6.2 pts

14

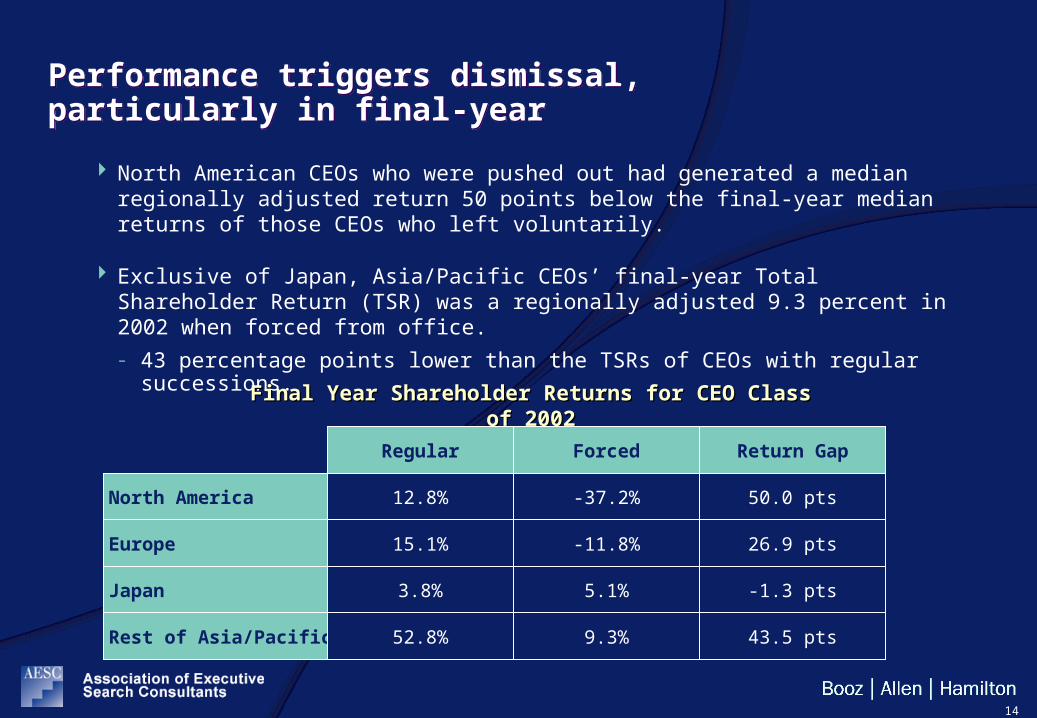

North American CEOs who were pushed out had generated a median regionally adjusted return 50 points below the final-year median returns of those CEOs who left voluntarily.

Exclusive of Japan, Asia/Pacific CEOs’ final-year Total Shareholder Return (TSR) was a regionally adjusted 9.3 percent in 2002 when forced from office.

– 43 percentage points lower than the TSRs of CEOs with regular successions.

Performance triggers dismissal, particularly in final-yearPerformance triggers dismissal, particularly in final-year

Final Year Shareholder Returns for CEO Class of 2002Final Year Shareholder Returns for CEO Class of 2002

North America

Europe

12.8%

Regular

-37.2%

Forced

50.0 pts

Return Gap

15.1% -11.8% 26.9 pts

Japan

Rest of Asia/Pacific

3.8% 5.1% -1.3 pts

52.8% 9.3% 43.5 pts

15

Performance gaps largest in North America and EuropePerformance gaps largest in North America and Europe

Shareholder returns not a driver for performance-related successions in Japan

6.3

13.3

4.26.4

13.3

2.3

-5.7

28.0

4.7

16.8

6.3

1.3

10.1

6.3

-3.7

4.55.1

15.3

-10

-5

0

5

10

15

20

25

30

North America Europe Japan Rest of Asia/Pacific

1995 1998 2000 2001 2002

Median Shareholder Returns, by Region Performance RelatedMedian Shareholder Returns, by Region Performance Related

n/an/a n/an/a

16

Two industries with high turnover in the five years studied stand out: telecommunications services and energyTwo industries with high turnover in the five years studied stand out: telecommunications services and energy

Financial services had the lowest CEO turnover in four of the previous years we studied and the second lowest turnover in 2002.

Across the five years, telecommunications services has the highest forced turnover.

Regular

Telecommunications Services

Energy

Information Technology

Materials

Consumer Staples

Consumer Discretionary

Utilities

Industrials

Financial Services

Average Across Industries

15.6% 12.1%

12.6% 11.3%

9.1% 9.7%

13.5% 9.3%

2002 All 5 Years

8.9% 9.2%

9.2% 8.9%

15.8% 8.9%

8.3% 8.5%

8.6% 6.6%

10.1% 8.8%

Health 9.7% 9.4%

Regular

Information Technology

Telecommunications Services

Consumer Discretionary

Utilities

Consumer Staples

Industrials

Materials

Energy

Financial Services

Average Across Industries

4.7% 4.3%

9.4% 4.2%

3.5% 3.1%

5.7% 2.2%

2002 All 5 Years

1.8% 2.2%

3.2% 2.0%

5.2% 1.9%

2.5% 1.7%

3.3% 1.5%

3.9% 2.5%

Health Care 3.8% 2.8%

Succession Rates, by IndustrySuccession Rates, by Industry Forced Succession Rates, by IndustryForced Succession Rates, by Industry

17

Outsider CEOs – a risky businessOutsider CEOs – a risky business

Outsiders face a much greater — and an increasing — probability of being fired.

Outsiders come on extremely strong, are unable to uphold their early promise, and are more likely to generate disaffection among shareholders and dismissals by boards.

Forced Succession Among Insider and Outsider CEOs, by RegionForced Succession Among Insider and Outsider CEOs, by Region

North America

Europe

Asia/Pacific

Global

49%

Insiders

57%

Outsiders

38% 64%

42% 0%

44% 53%

2002

31%

Insiders

38%

Outsiders

45% 54%

30% 40%

34% 43%

All 5 Years

18

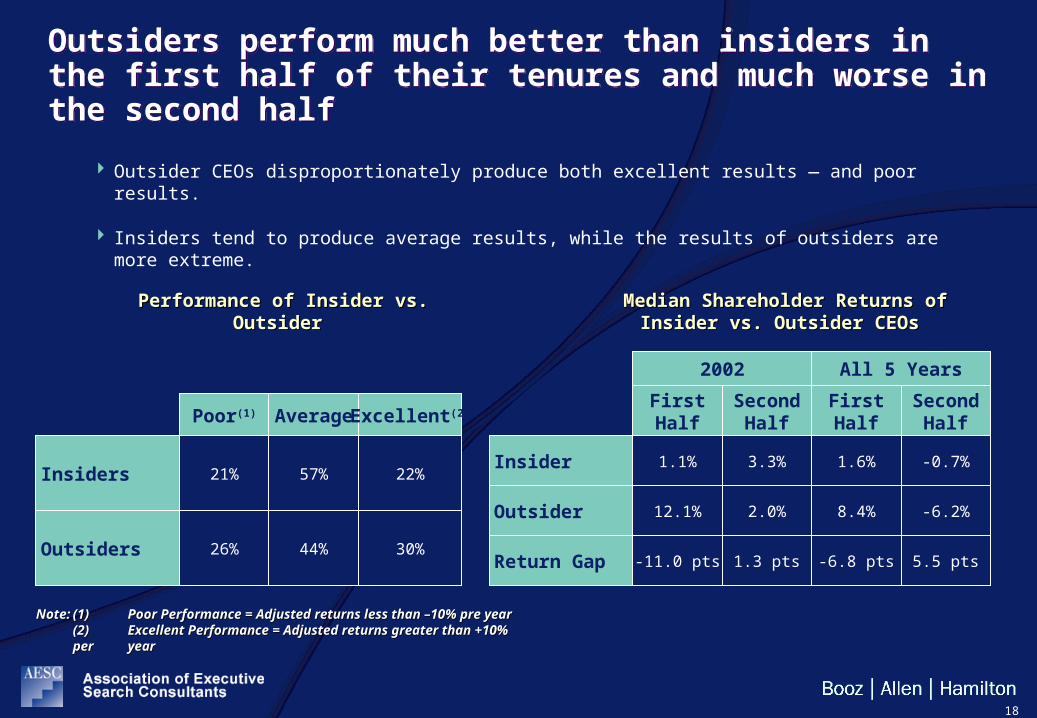

Outsiders perform much better than insiders in the first half of their tenures and much worse in the second halfOutsiders perform much better than insiders in the first half of their tenures and much worse in the second half

Outsider CEOs disproportionately produce both excellent results — and poor results.

Insiders tend to produce average results, while the results of outsiders are more extreme.

Insider 1.1%

FirstHalf

3.3%

SecondHalf

2002

1.6%

FirstHalf

-0.7%

SecondHalf

All 5 Years

Median Shareholder Returns of Median Shareholder Returns of Insider vs. Outsider CEOsInsider vs. Outsider CEOs

Poor(1) Average Excellent(2)

Performance of Insider vs. OutsiderPerformance of Insider vs. Outsider

Outsiders 26% 44% 30%

Insiders 21% 57% 22%

Outsider 12.1% 2.0% 8.4% -6.2%

Return Gap -11.0 pts 1.3 pts -6.8 pts 5.5 pts

Note:Note: (1)(1) Poor Performance = Adjusted returns less than –10% pre Poor Performance = Adjusted returns less than –10% pre yearyear(2)(2) Excellent Performance = Adjusted returns greater than +10% Excellent Performance = Adjusted returns greater than +10% per per yearyear

19

Life at the Top is getting shorter Life at the Top is getting shorter

The average tenure for CEOs forced from office across all regions has declined since 1995

2002 seems an exception. Both in the US and in Europe the mean tenure length for fired CEOs increased. 7.9 yrs in the US and 5.4 yrs in Europe – the longest since 1995

8.9

4.85.6

7.0

5.1

7.5

6.3

4.9

3.5

4.84.6 4.5

8.0

4.6

7.9

5.4

3.9

6.46.2

4.9 4.85.7

6.8

4.9

012345

6789

10

North America Europe Asia/Pacific Global

1995 1998 2000 2001 2002 All 5 Years

Average Tenure (in Years) of Departing CEOs, by Region Performance RelatedAverage Tenure (in Years) of Departing CEOs, by Region Performance Related

20

In conclusion …In conclusion …

Despite increases in CEO tenure and age, professional lives of CEOs resemble the Hobbesian man: nasty, brutish and short

Increased CEO ‘volatility’ is natural outcome of two-decade trend toward “celebritizing” of individual CEOs, especially in North America and Europe

Five observations:

1. Individual leadership still matters

2. Execution and vision cannot be divided

3. Hit the ground running – and then keep running

4. Board shouldn’t just be judge and jury; it must be coach and counselor

5. Help the board become more effective too

The Transformation ImperativeThe Transformation Imperative

22

The Need for Strategy Based TransformationThe Need for Strategy Based Transformation

Complexity is the challenge

Transformation is the path

Resilience is the goal

Meta-networks

Complex options

Competition

Transparency

Asymmetric Risk

23

Strategy Based Transformation

Strategy

“Establish the case for change”

Capabilities

“Define what to change“

Program Architecture

“Determine how to change“

Change Management

“Get it done“

Mission:“Booz Allen Hamilton works with clients to deliver results that endure”

A unique perspective on the dynamics of businesses and governments in today’s world…– Complexity is the

challenge– Transformation is

the path– Resilience is the goal

Fix problems/build capabilities by blending multi-functional expertise (Strategy, Oper-ations, Organization, IT) to address client priorities:– Channels, Customers and

Markets– Innovation– Supply Chain– People and Performance

(NOM)– One-time events– Enterprise Resilience

The design and execution of an objectives driven transformation effort to ensure results with speed, certainty and precision

Shaping the organisation by:– Engaging the top to

lead the change– Cascading down and

break barriers– Mobilizing the base

= + + +

Booz Allen’s response: Integrated approach to help clients change and develop the capabilities to adapt and grow through future uncertainties

Booz Allen’s Strategy Based Transformation ApproachBooz Allen’s Strategy Based Transformation Approach

24

Results are showingResults are showing

Booz Allen Hamilton Client ExamplesBooz Allen Hamilton Client Examples