london tech listing considerations

TRANSCRIPT

LONDON TECH LISTING CONSIDERATIONS MARCH 2017

EXECUTIVE SUMMARYWhy London?

LARGE APPETITE FOR UK TECH STOCKS

— Relative scarcity of UK-listed technology stocks makes large tech companies a must own for UK investors – Sophos marketed solely against US comps and achieved valuation premium

— Just Eat provides a case study in how VCs can use public markets for monetisation and growth

— London has lead the way with jumbo IPOs like Worldpay – the largest tech IPO globally in 2015

— Small cap successes such as Blue Prism demonstrate unique differentiation through AIM.

ENHANCED DEAL STRUCTURE AND PROCESS IN THE UK

— UK more receptive to small and micro cap deals— Less share price volatility observed in the UK due to long term orientation

of investors— UK IPO process provide more certainty in pricing and valuation— UK investors superior appetite to absorb secondary selldown at IPO than

US counterparts.

VASTLY REDUCED REGULATORY BURDEN AND COST

— London much more cost-effective for IPO underwriting and transaction costs

— Insurance far more expensive in US due to legal environment / track record of shareholder activism

— Annual Sarbanes Oxley compliance estimated at $1.5m / SEC review process longer than UKLA

— Quarterly reporting not mandatory in UK further reducing cost and time burden.

UK MARKETS PROVING RESILIENT AND IPOs ARE OUTPERFORMING

— London in the top five global exchanges for issuance despite political backdrop

— London IPOs have outperformed their US counterparts in 2015 and impressive performance continued in 2016 with technology companies leading the way

— UK indices continue to perform well post-Brexit – best major market performers in the local currency terms – driven by large overseas revenue exposure of UK-listed firms.

LONDON IS THE MOST INTERNATIONAL MARKET

— London is the most international stock market globally in terms of international listed companies

— International shareholders represent almost half the ownership in UK stocks

— North American shareholders alone own c.30% and UK IPOs routinely offered to most US institutions

— US IPO market remains essentially domestic with limited relative international investor representation

— US investors’ holding of “non-domestic” companies tends to be more volatile.

01

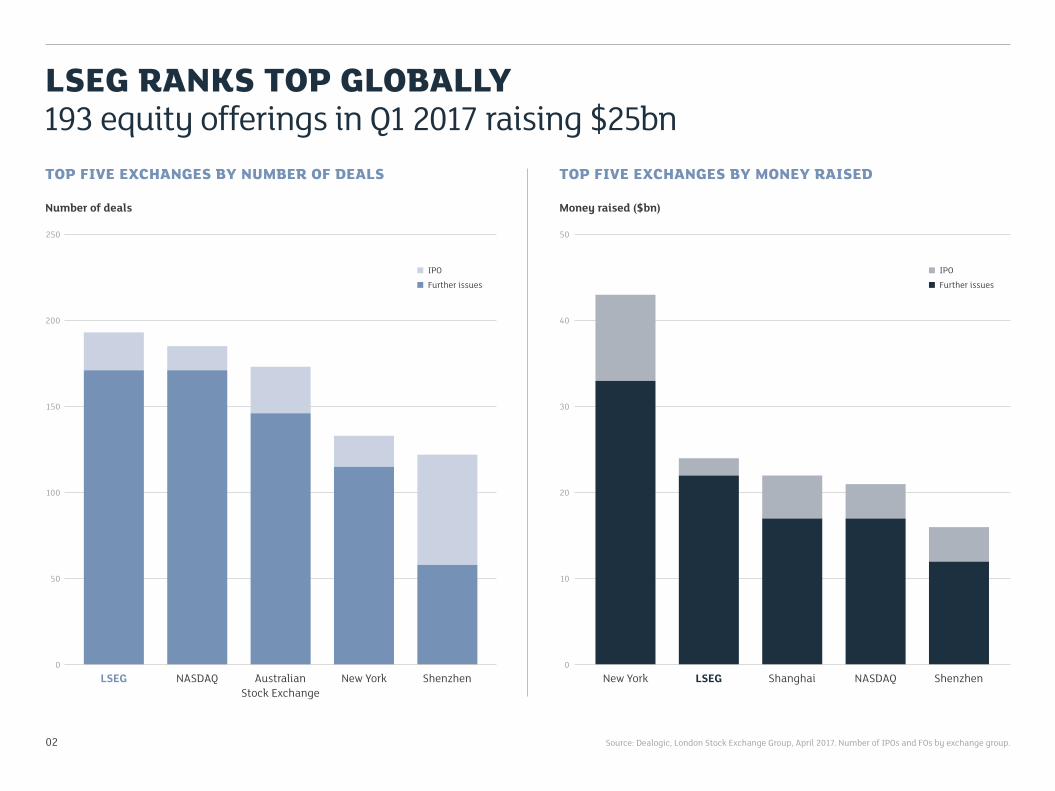

LSEG RANKS TOP GLOBALLY 193 equity offerings in Q1 2017 raising $25bn

Source: Dealogic, London Stock Exchange Group, April 2017. Number of IPOs and FOs by exchange group.

TOP FIVE EXCHANGES BY NUMBER OF DEALS

Number of deals

LSEG NASDAQ

250

0

200

150

100

50

IPO

Further issues

02

ShenzhenAustralian Stock Exchange

New York

TOP FIVE EXCHANGES BY MONEY RAISED

Money raised ($bn)

50

40

30

20

10

0New York LSEG ShenzhenShanghai NASDAQ

IPO

Further issues

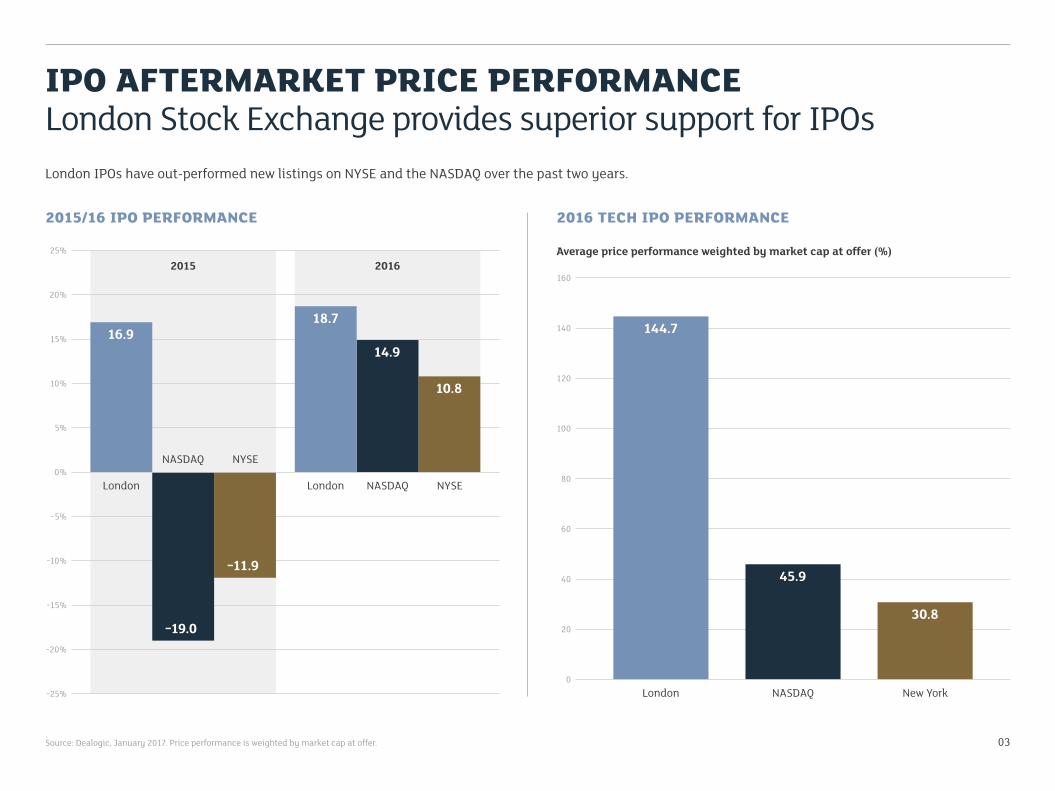

IPO AFTERMARKET PRICE PERFORMANCELondon Stock Exchange provides superior support for IPOsLondon IPOs have out-performed new listings on NYSE and the NASDAQ over the past two years.

2016 TECH IPO PERFORMANCE2015/16 IPO PERFORMANCE

25%

20%

15%

10%

5%

0%

−5%

−10%

−15%

−20%

−25%

16.918.7

14.9

10.8

−19.0

−11.9

2015 2016

London London NASDAQ NYSE

NASDAQ NYSE

Source: Dealogic, January 2017. Price performance is weighted by market cap at offer. 03

Average price performance weighted by market cap at offer (%)

160

140

120

100

80

60

40

20

0London NASDAQ New York

144.7

45.9

30.8

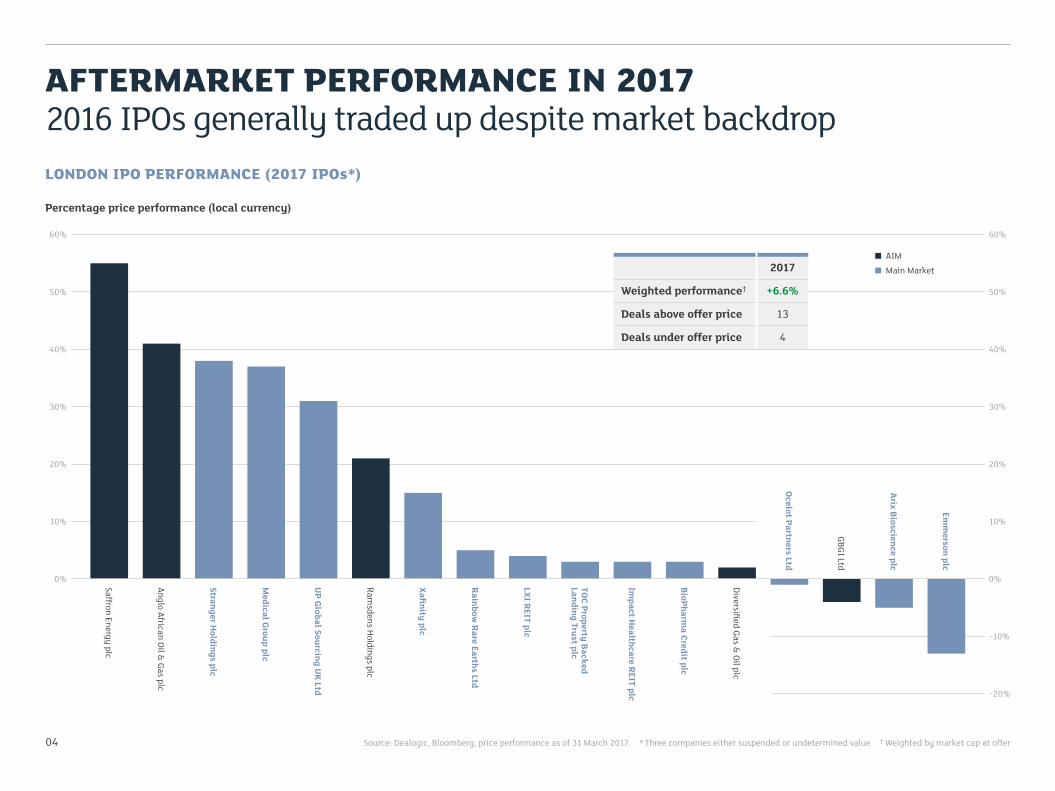

LONDON IPO PERFORMANCE (2017 IPOs*)

Percentage price performance (local currency)

60%

Source: Dealogic, Bloomberg, price performance as of 31 March 2017. * Three companies either suspended or undetermined value † Weighted by market cap at offer

Saffron Energy plc

Anglo African Oil & Gas plc

Stranger Holdings plc

Medical Group plc

UP Global Sourcing U

K Ltd

Ramsdens Holdings plc

Xafinity plc

Rainbow Rare Earths Ltd

LXI REIT plc

TOC Property Backed Landing Trust plc

Impact H

ealthcare REIT plc

BioPharma Credit plc

Diversified Gas & Oil plc

Ocelot Partners Ltd

GBGI Ltd

Arix Bioscience plc

Emm

erson plc

40%

30%

20%

10%

0%

60%

50%

40%

30%

20%

0%

−10%

−20%

2017

Weighted performance† +6.6%

Deals above offer price 13

Deals under offer price 4

AFTERMARKET PERFORMANCE IN 20172016 IPOs generally traded up despite market backdrop

AIM

Main Market

04

50%

10%

Index Constituents’ Overseas Revenue

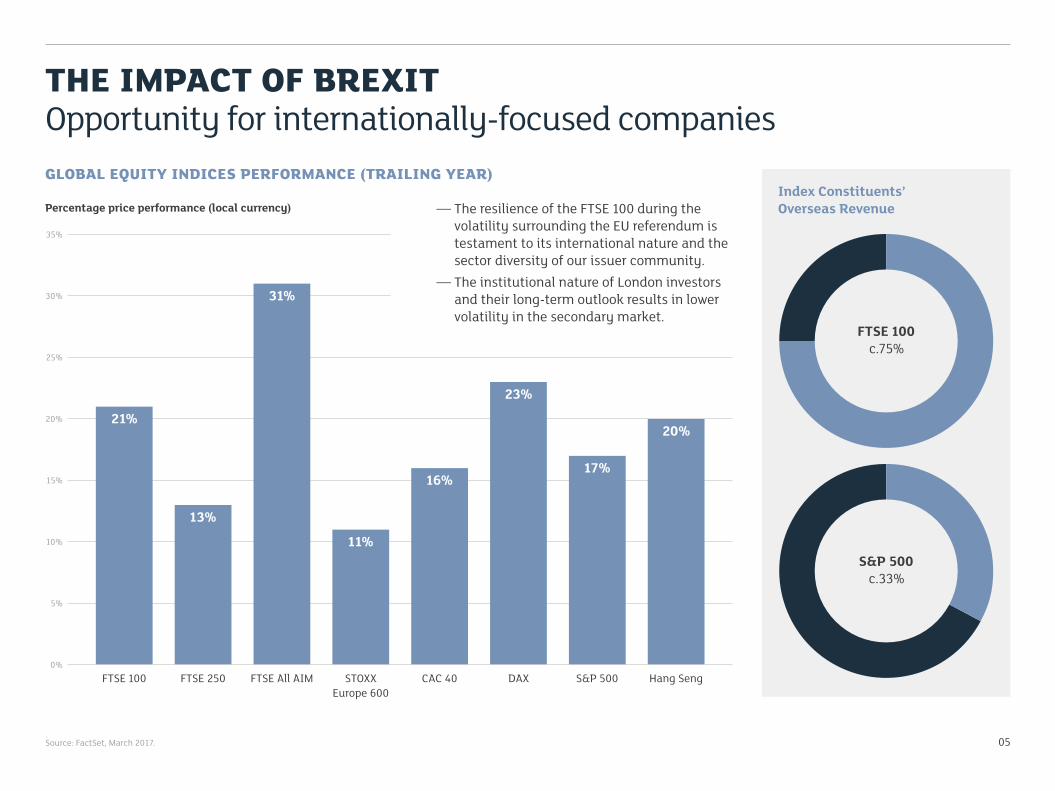

THE IMPACT OF BREXITOpportunity for internationally-focused companies

— The resilience of the FTSE 100 during the volatility surrounding the EU referendum is testament to its international nature and the sector diversity of our issuer community.

— The institutional nature of London investors and their long-term outlook results in lower volatility in the secondary market.

Source: FactSet, March 2017.

GLOBAL EQUITY INDICES PERFORMANCE (TRAILING YEAR)

FTSE 100

Percentage price performance (local currency)

0%

35%

30%

25%

20%

15%

10%

5%

Hang SengFTSE 250 FTSE All AIM STOXX Europe 600

CAC 40 DAX S&P 500

FTSE 100c.75%

S&P 500c.33%

05

21%

13%

31%

11%

16%

23%

17%

20%

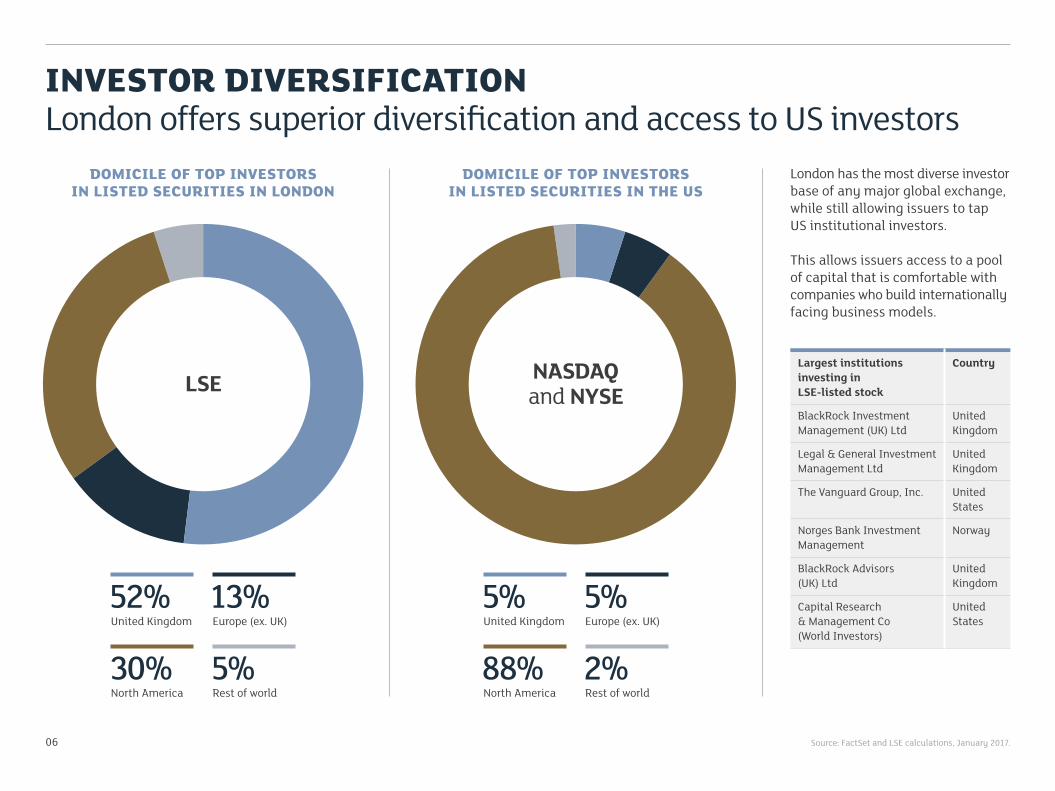

INVESTOR DIVERSIFICATIONLondon offers superior diversification and access to US investors

06

London has the most diverse investor base of any major global exchange, while still allowing issuers to tap US institutional investors.

This allows issuers access to a pool of capital that is comfortable with companies who build internationally facing business models.

Source: FactSet and LSE calculations, January 2017.

Largest institutions investing in LSE-listed stock

Country

BlackRock Investment Management (UK) Ltd

United Kingdom

Legal & General Investment Management Ltd

United Kingdom

The Vanguard Group, Inc. United States

Norges Bank Investment Management

Norway

BlackRock Advisors (UK) Ltd

United Kingdom

Capital Research & Management Co (World Investors)

United States

DOMICILE OF TOP INVESTORS IN LISTED SECURITIES IN LONDON

DOMICILE OF TOP INVESTORS IN LISTED SECURITIES IN THE US

52%United Kingdom

30%North America

13%Europe (ex. UK)

5%Rest of world

5%United Kingdom

88%North America

5%Europe (ex. UK)

2%Rest of world

LSE NASDAQ and NYSE

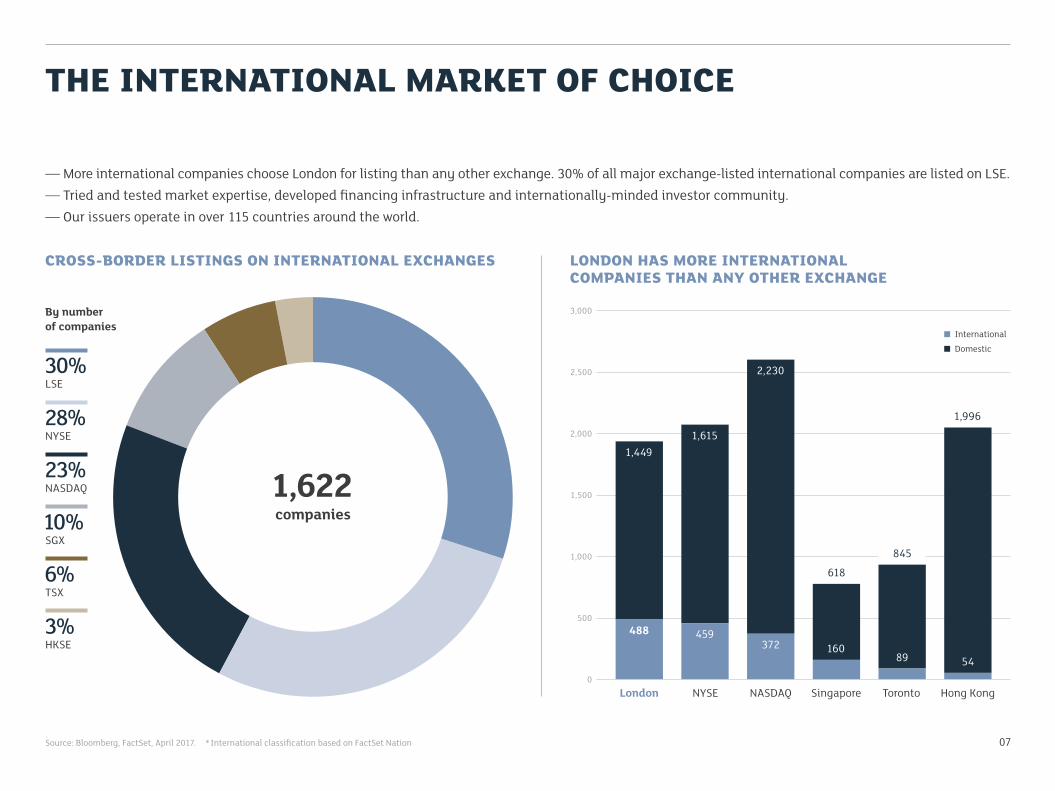

THE INTERNATIONAL MARKET OF CHOICE

07

— More international companies choose London for listing than any other exchange. 30% of all major exchange-listed international companies are listed on LSE.— Tried and tested market expertise, developed financing infrastructure and internationally-minded investor community.— Our issuers operate in over 115 countries around the world.

LONDON HAS MORE INTERNATIONAL COMPANIES THAN ANY OTHER EXCHANGE

CROSS-BORDER LISTINGS ON INTERNATIONAL EXCHANGES

Source: Bloomberg, FactSet, April 2017. * International classification based on FactSet Nation

30%LSE

28%NYSE

23%NASDAQ

10%SGX

6%TSX

3%HKSE

1,622 companies

By number of companies

London0

3,000

2,500

2,000

1,500

1,000

500

NYSE NASDAQ Singapore Toronto Hong Kong

International

Domestic

488

1,449

459

1,615

372

2,230

160

618

89

845

1,996

54

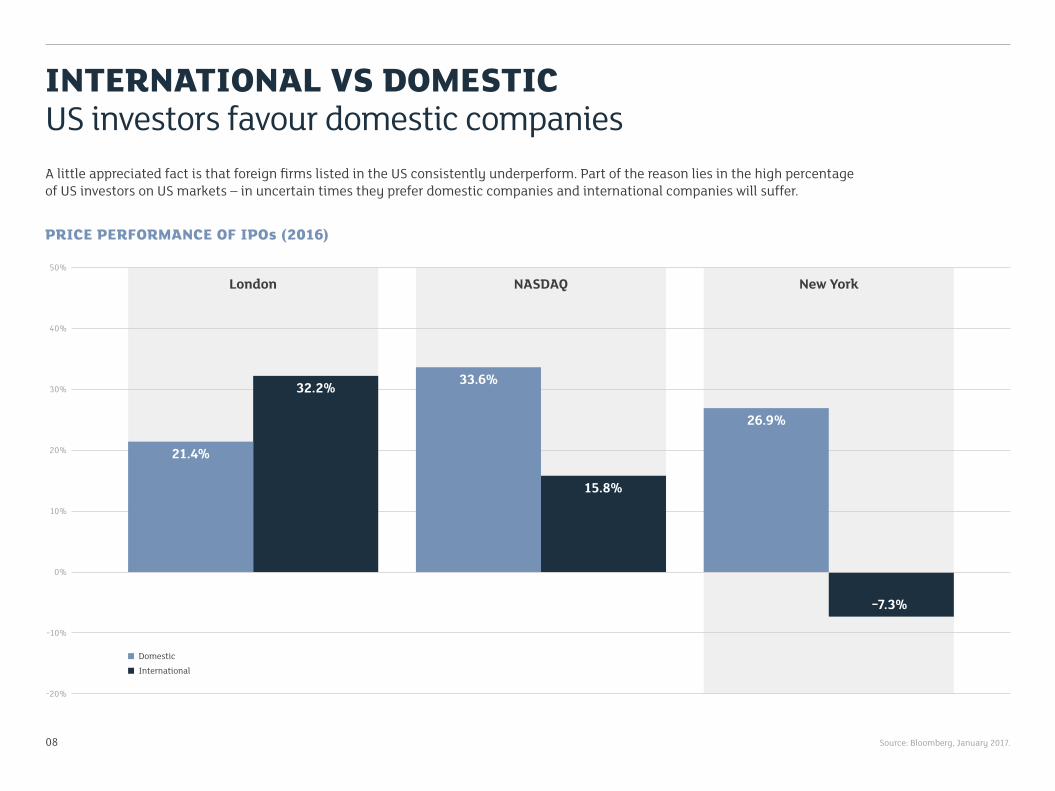

INTERNATIONAL VS DOMESTICUS investors favour domestic companies

08

A little appreciated fact is that foreign firms listed in the US consistently underperform. Part of the reason lies in the high percentage of US investors on US markets – in uncertain times they prefer domestic companies and international companies will suffer.

PRICE PERFORMANCE OF IPOs (2016)

50%

40%

30%

20%

10%

0%

−10%

−20%

London NASDAQ New York

21.4%

32.2% 33.6%

15.8%

26.9%

−7.3%

Domestic

International

Source: Bloomberg, January 2017.

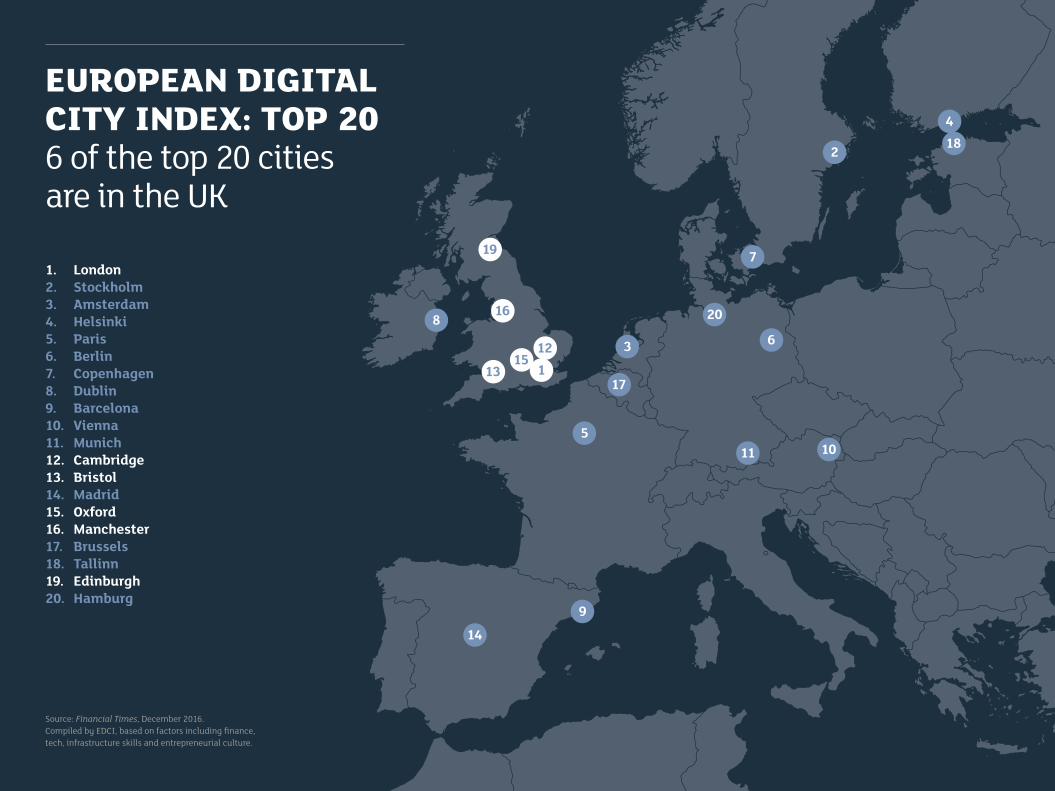

EUROPEAN DIGITAL CITY INDEX: TOP 20 6 of the top 20 cities are in the UK

1. London2. Stockholm3. Amsterdam4. Helsinki5. Paris6. Berlin7. Copenhagen8. Dublin9. Barcelona10. Vienna11. Munich12. Cambridge13. Bristol14. Madrid15. Oxford16. Manchester17. Brussels18. Tallinn19. Edinburgh20. Hamburg

Source: Financial Times, December 2016. Compiled by EDCI, based on factors including finance, tech, infrastructure skills and entrepreneurial culture.

1

2

3

4

5

6

7

8

9

1011

12

13

14

15

16

17

18

19

20

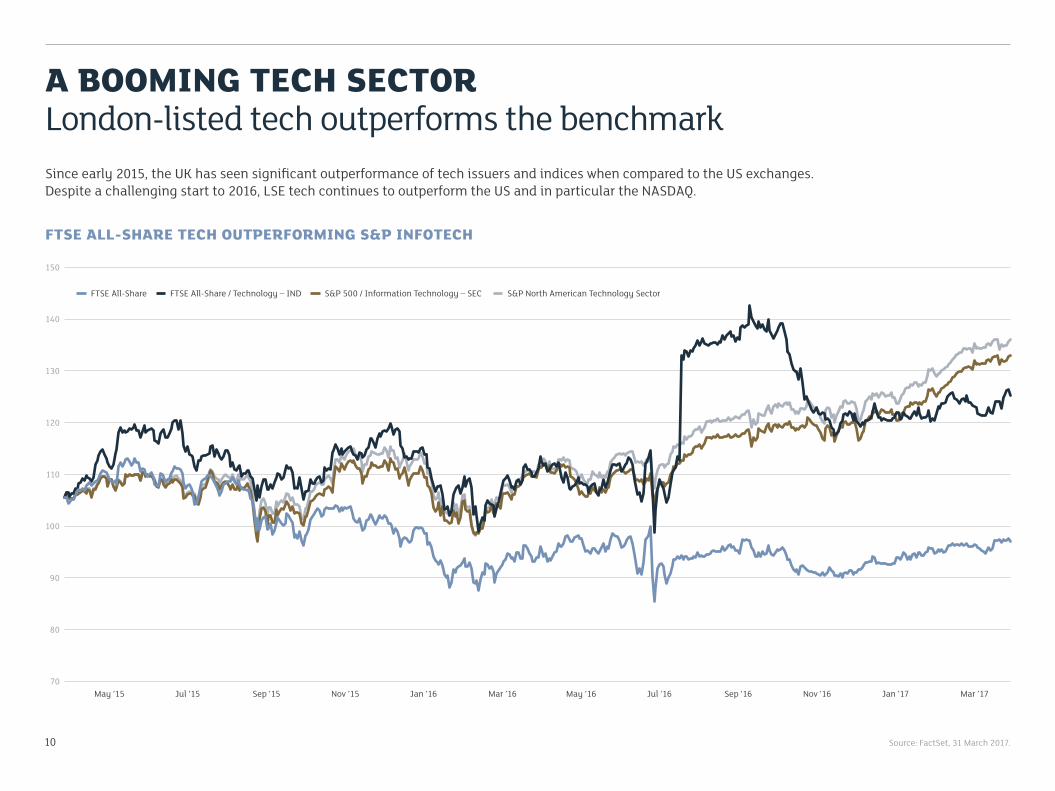

A BOOMING TECH SECTORLondon-listed tech outperforms the benchmark

10

Since early 2015, the UK has seen significant outperformance of tech issuers and indices when compared to the US exchanges. Despite a challenging start to 2016, LSE tech continues to outperform the US and in particular the NASDAQ.

Source: FactSet, 31 March 2017.

FTSE ALL-SHARE TECH OUTPERFORMING S&P INFOTECH

150

70

140

130

120

110

100

90

80

Mar ’17May ’15 Mar ’16 May ’16 Jul ’16 Sep ’16

FTSE All-Share FTSE All-Share / Technology – IND S&P 500 / Information Technology – SEC S&P North American Technology Sector

Nov ’16Jul ’15 Sep ’15 Nov ’15 Jan ’16 Jan ’17

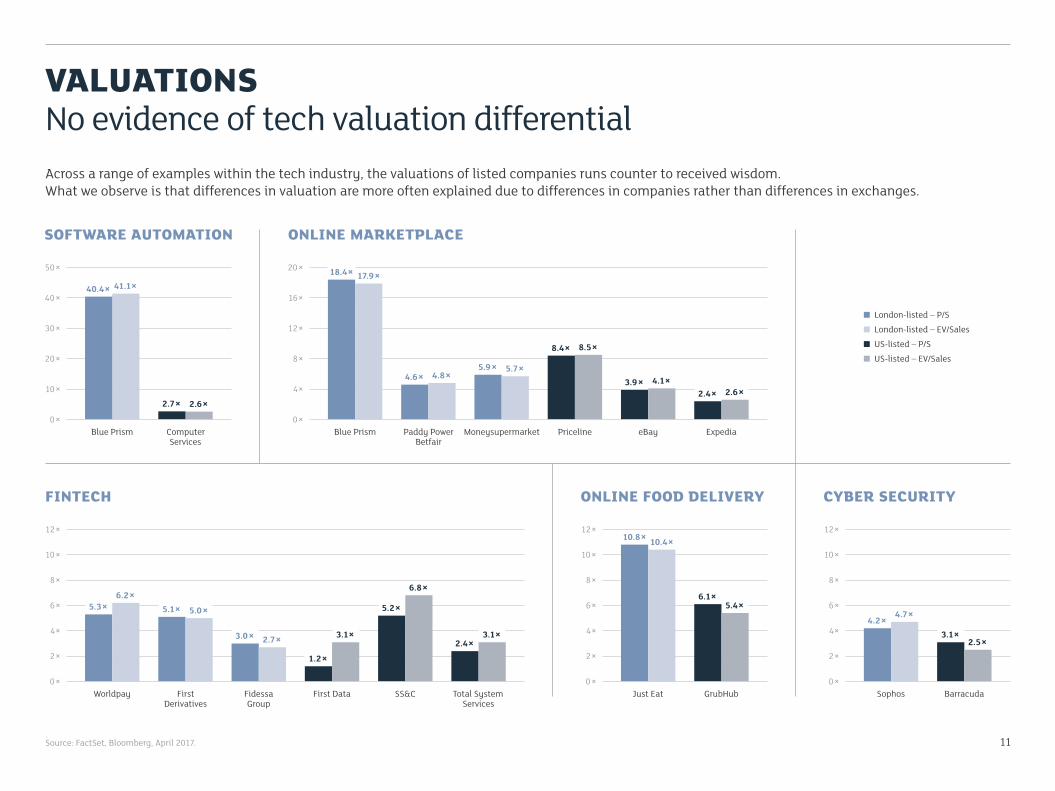

VALUATIONSNo evidence of tech valuation differentialAcross a range of examples within the tech industry, the valuations of listed companies runs counter to received wisdom.What we observe is that differences in valuation are more often explained due to differences in companies rather than differences in exchanges.

SOFTWARE AUTOMATION

11Source: FactSet, Bloomberg, April 2017.

ONLINE MARKETPLACE

FINTECH ONLINE FOOD DELIVERY CYBER SECURITY

Blue Prism

50×

0×

40×

30×

20×

10×

Computer Services

Blue Prism

20×

0×

12×

8×

4×

16×

Moneysupermarket Priceline eBayPaddy Power Betfair

Expedia

Worldpay

12×

0×

10×

6×

4×

2×

8×

First Derivatives

Fidessa Group

Total System Services

First Data SS&C0×

12×

10×

6×

4×

2×

8×

0×

12×

10×

6×

4×

2×

8×

BarracudaSophosGrubHubJust Eat

5.3×6.2×

5.1× 5.0×

3.0× 2.7×1.2×

3.1×

5.2×6.8×

2.4×3.1×

10.8× 10.4×

6.1×5.4×

4.2× 4.7×3.1×

2.5×

40.4× 41.1×

2.7× 2.6×

18.4× 17.9×

4.6× 4.8×5.9× 5.7×

8.4× 8.5×

3.9× 4.1×2.4× 2.6×

London-listed – P/S

London-listed – EV/Sales

US-listed – P/S

US-listed – EV/Sales

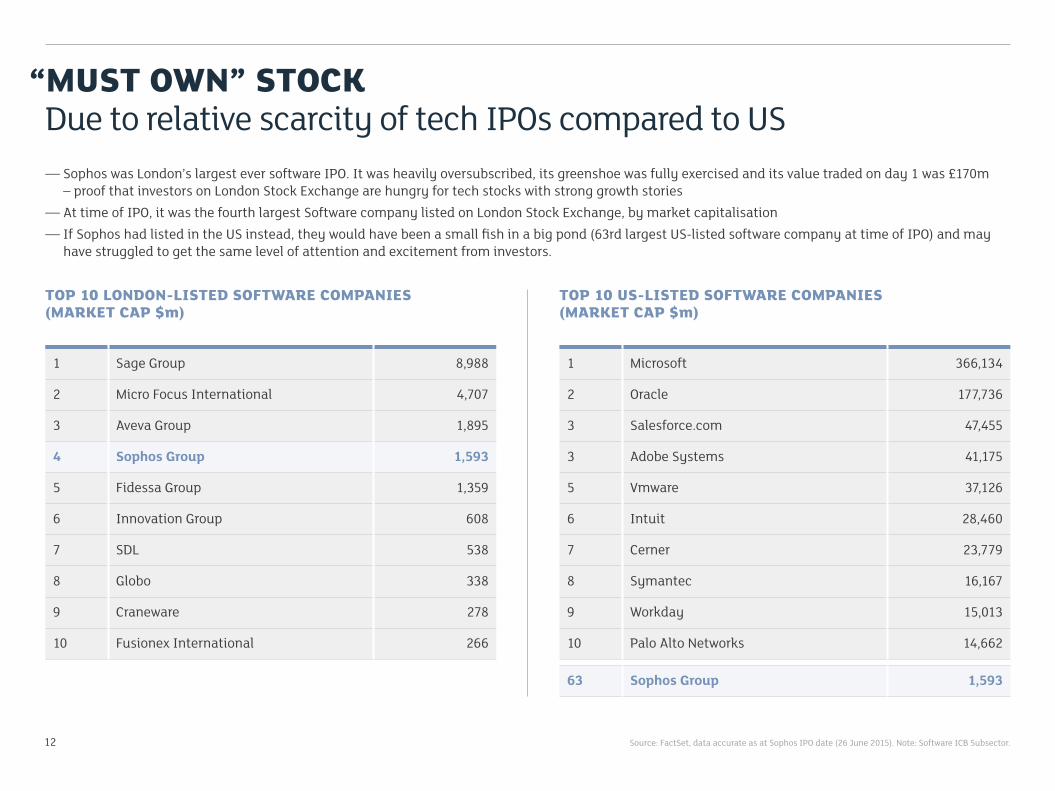

“MUST OWN” STOCKDue to relative scarcity of tech IPOs compared to US

12 Source: FactSet, data accurate as at Sophos IPO date (26 June 2015). Note: Software ICB Subsector.

— Sophos was London’s largest ever software IPO. It was heavily oversubscribed, its greenshoe was fully exercised and its value traded on day 1 was £170m – proof that investors on London Stock Exchange are hungry for tech stocks with strong growth stories

— At time of IPO, it was the fourth largest Software company listed on London Stock Exchange, by market capitalisation— If Sophos had listed in the US instead, they would have been a small fish in a big pond (63rd largest US-listed software company at time of IPO) and may

have struggled to get the same level of attention and excitement from investors.

TOP 10 LONDON-LISTED SOFTWARE COMPANIES(MARKET CAP $m)

TOP 10 US-LISTED SOFTWARE COMPANIES(MARKET CAP $m)

1 Sage Group 8,988

2 Micro Focus International 4,707

3 Aveva Group 1,895

4 Sophos Group 1,593

5 Fidessa Group 1,359

6 Innovation Group 608

7 SDL 538

8 Globo 338

9 Craneware 278

10 Fusionex International 266

1 Microsoft 366,134

2 Oracle 177,736

3 Salesforce.com 47,455

3 Adobe Systems 41,175

5 Vmware 37,126

6 Intuit 28,460

7 Cerner 23,779

8 Symantec 16,167

9 Workday 15,013

10 Palo Alto Networks 14,662

63 Sophos Group 1,593

13

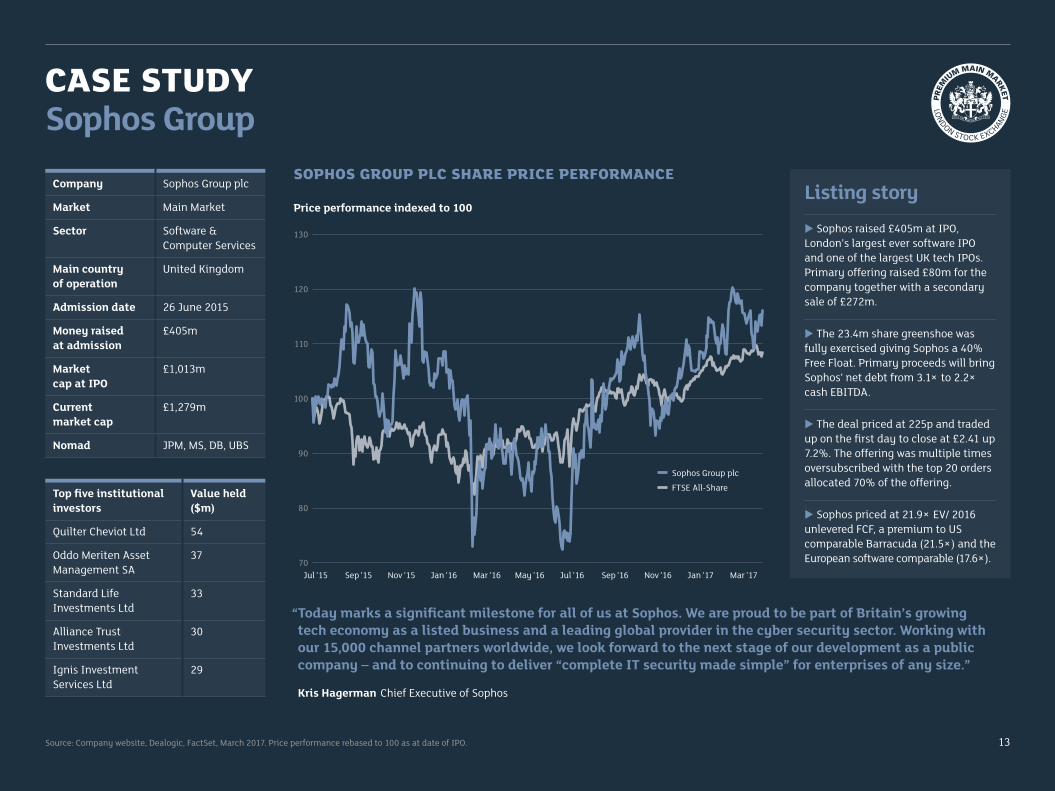

CASE STUDYSophos Group

Source: Company website, Dealogic, FactSet, March 2017. Price performance rebased to 100 as at date of IPO.

Company Sophos Group plc

Market Main Market

Sector Software & Computer Services

Main country of operation

United Kingdom

Admission date 26 June 2015

Money raised at admission

£405m

Market cap at IPO

£1,013m

Current market cap

£1,279m

Nomad JPM, MS, DB, UBS

Listing storyu Sophos raised £405m at IPO, London’s largest ever software IPO and one of the largest UK tech IPOs.Primary offering raised £80m for the company together with a secondary sale of £272m.

u The 23.4m share greenshoe was fully exercised giving Sophos a 40% Free Float. Primary proceeds will bring Sophos’ net debt from 3.1× to 2.2× cash EBITDA.

u The deal priced at 225p and traded up on the first day to close at £2.41 up 7.2%. The offering was multiple times oversubscribed with the top 20 orders allocated 70% of the offering.

u Sophos priced at 21.9× EV/ 2016 unlevered FCF, a premium to US comparable Barracuda (21.5×) and the European software comparable (17.6×).

Top five institutional investors

Value held ($m)

Quilter Cheviot Ltd 54

Oddo Meriten Asset Management SA

37

Standard Life Investments Ltd

33

Alliance Trust Investments Ltd

30

Ignis Investment Services Ltd

29

SOPHOS GROUP PLC SHARE PRICE PERFORMANCE

Price performance indexed to 100

130

120

110

100

90

80

“Today marks a significant milestone for all of us at Sophos. We are proud to be part of Britain’s growing tech economy as a listed business and a leading global provider in the cyber security sector. Working with our 15,000 channel partners worldwide, we look forward to the next stage of our development as a public company – and to continuing to deliver “complete IT security made simple” for enterprises of any size.”

Kris Hagerman Chief Executive of Sophos

70Jul ’15 Mar ’17Jul ’16 Sep ’16 Nov ’16 Jan ’17

Sophos Group plc

FTSE All-Share

Sep ’15 Nov ’15 Jan ’16 Mar ’16 May ’16

IPO detailsAdmission date 3 April 2014Money raised $600mPrimary $167mSecondary $433mMarket cap at IPO $2,438m

Sponsors exit at IPOIndex VenturesRedpoint VenturesSM TrustVitruvian PartnersGreylock Partners

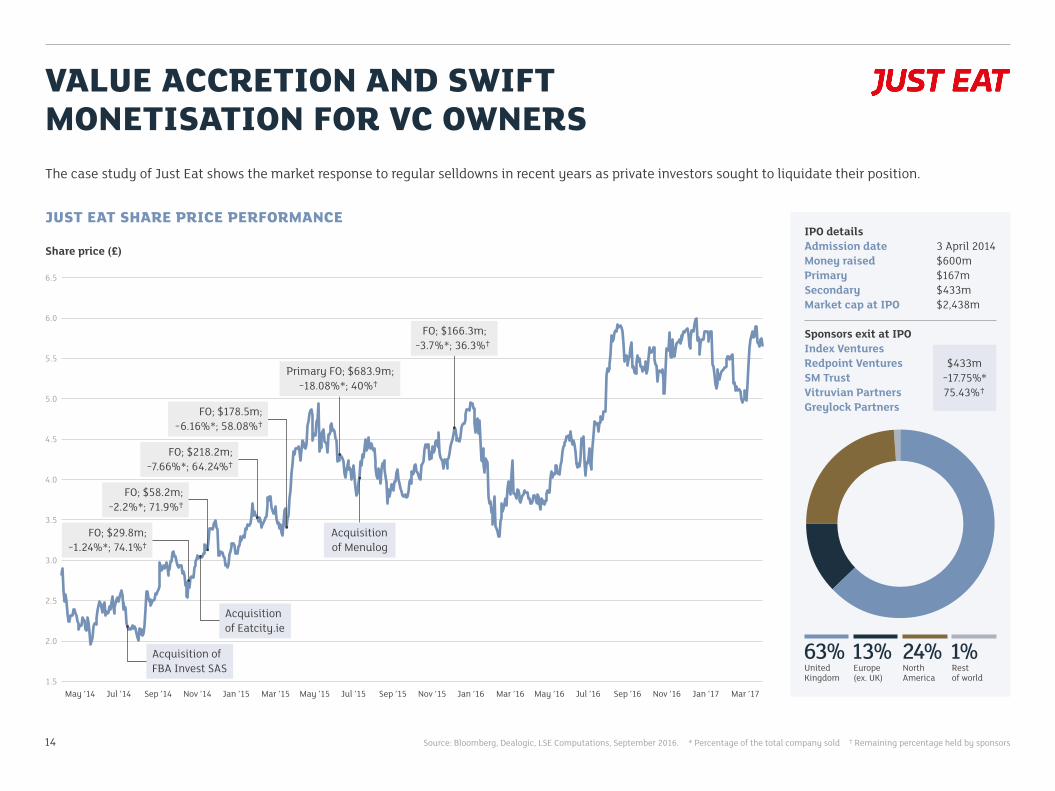

VALUE ACCRETION AND SWIFT MONETISATION FOR VC OWNERS

14

The case study of Just Eat shows the market response to regular selldowns in recent years as private investors sought to liquidate their position.

JUST EAT SHARE PRICE PERFORMANCE

Share price (£)

6.5

1.5Mar ’17

5.5

5.0

4.5

4.0

3.5

3.0

2.5

2.0

Source: Bloomberg, Dealogic, LSE Computations, September 2016. * Percentage of the total company sold † Remaining percentage held by sponsors

$433m−17.75%*75.43%†

63%United Kingdom

1%Rest of world

13%Europe (ex. UK)

24%North America

Acquisition of FBA Invest SAS

FO; $29.8m; −1.24%*; 74.1%†

Acquisition of Eatcity.ie

FO; $58.2m; −2.2%*; 71.9%†

FO; $218.2m; −7.66%*; 64.24%†

FO; $178.5m; −6.16%*; 58.08%†

Primary FO; $683.9m; −18.08%*; 40%†

FO; $166.3m; −3.7%*; 36.3%†

Acquisition of Menulog

6.0

May ’14 Jul ’14 Sep ’14 Nov ’14 Jan ’15 Mar ’15 May ’15 Jul ’15 Sep ’15 Nov ’15 Jan ’16 Mar ’16 May ’16 Jul ’16 Sep ’16 Nov ’16 Jan ’17

15

COMPARISON OF JUST EAT AND GRUBHUB

Source: FactSet, Dealogic, March 2017.

Stock exchange London New York

Pricing date 3 April 2014 3 April 2014

IPO size $599m $221m

Pricing vs range Top Above

Price range £2.10–£2.60 $23.00–$25.00

Priced £2.60 $26.00

Market cap at admission

$2.4bn $2.0bn

Current market cap $4.7bn $2.9bn

% offered at IPO 24.6% 10.9%

Primary/secondary split at IPO

28%:72% 47%:53%

Current to offer price 91.4% 34.1%

Selling shareholders Redpoint Ventures, SM Trust, Vitruvian Partners

GS Capital Partners Spectrum Equity, Thomas H Lee, Warburg Pincus

JUST EAT SHARE PRICE PERFORMANCE

Price performance indexed to 100

240

40

220

200

180

160

140

120

100

80

60

Mar ’17

Just Eat plc

GrubHub Inc.

Jun ’14 Sep ’14 Dec ’14 Mar ’15 Jun ’15 Sep ’15 Dec ’15 Mar ’16 Jun ’16 Sep ’16 Dec ’16

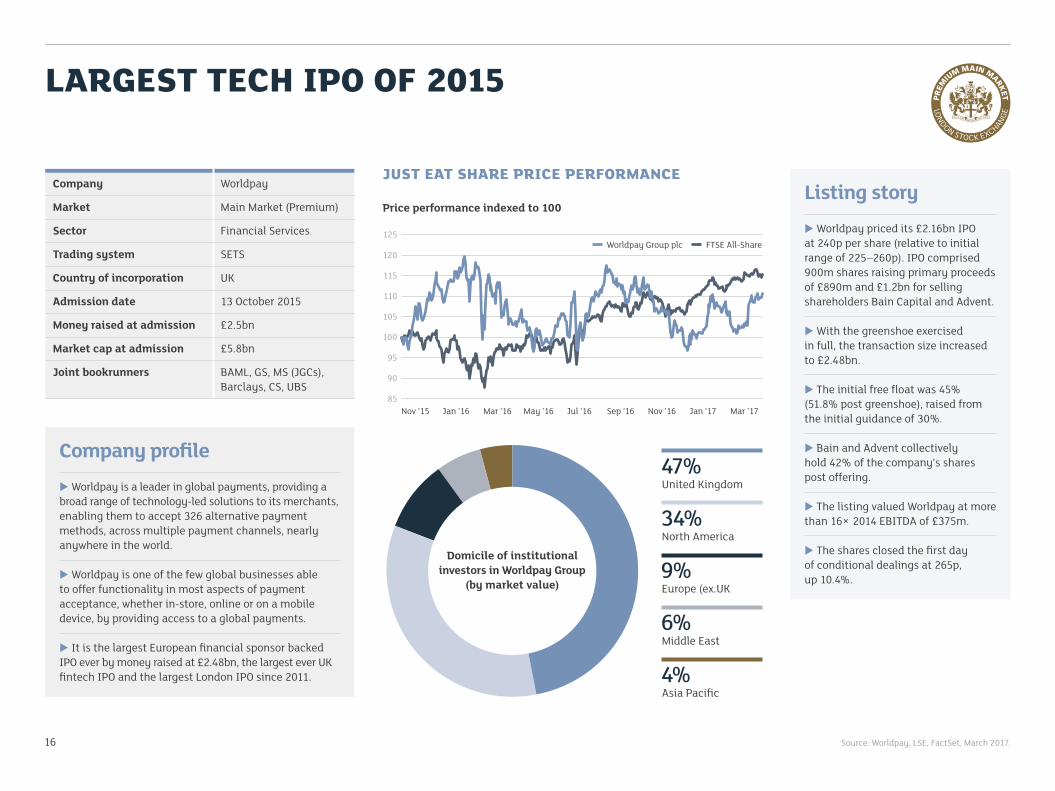

LARGEST TECH IPO OF 2015

Source: Worldpay, LSE, FactSet, March 2017.16

Company Worldpay

Market Main Market (Premium)

Sector Financial Services

Trading system SETS

Country of incorporation UK

Admission date 13 October 2015

Money raised at admission £2.5bn

Market cap at admission £5.8bn

Joint bookrunners BAML, GS, MS (JGCs), Barclays, CS, UBS

Listing storyu Worldpay priced its £2.16bn IPO at 240p per share (relative to initial range of 225–260p). IPO comprised 900m shares raising primary proceeds of £890m and £1.2bn for selling shareholders Bain Capital and Advent.

u With the greenshoe exercised in full, the transaction size increased to £2.48bn.

u The initial free float was 45% (51.8% post greenshoe), raised from the initial guidance of 30%.

u Bain and Advent collectively hold 42% of the company’s shares post offering.

u The listing valued Worldpay at more than 16× 2014 EBITDA of £375m.

u The shares closed the first day of conditional dealings at 265p, up 10.4%.

Company profileu Worldpay is a leader in global payments, providing a broad range of technology-led solutions to its merchants, enabling them to accept 326 alternative payment methods, across multiple payment channels, nearly anywhere in the world.

u Worldpay is one of the few global businesses able to offer functionality in most aspects of payment acceptance, whether in-store, online or on a mobile device, by providing access to a global payments.

u It is the largest European financial sponsor backed IPO ever by money raised at £2.48bn, the largest ever UK fintech IPO and the largest London IPO since 2011.

47%United Kingdom

34%North America

9%Europe (ex.UK

6%Middle East

4%Asia Pacific

JUST EAT SHARE PRICE PERFORMANCE

Price performance indexed to 100

Nov ’15 Mar ’17

125

85

120

115

110

105

100

95

90

Domicile of institutional investors in Worldpay Group

(by market value)

Worldpay Group plc FTSE All-Share

Jan ’16 Mar ’16 May ’16 Jul ’16 Sep ’16 Nov ’16 Jan ’17

WORLDPAY VS FIRST DATA COMPARISON

17

Worldpay and First Data listed within a day of each other. Worldpay was the largest IPO by deal size, First Data the largest IPO by valuation. Worldpay outperformed First Data on opening, and subsequently has continued to outperform the US-listed company despite challenging market conditions.

Source: FactSet, Dealogic, March 2017.

Price performance indexed to 100

Nov ’15

130

50

120

110

100

90

80

70

60

Jan ’16 May ’16 Jul ’16 Sep ’16 Mar ’17

Worldpay Group plc

First Data Corporation Class A

Mar ’16

WORLDPAY GROUP PLC VS FIRST DATA CORPORATION CLASS A

Stock exchange London New York

Pricing date 13 October 2015 14 October 2015

IPO size $3.81m $2.82m

Pricing vs range Mid range Below

Price range £2.25–£2.60 $18.00–$20.00

Priced £2.40 $16.00

Market cap at admission $4.8bn/$7.4bn $14.1bn

Current market cap $5.8bn/$7.2bn $14.4bn

Valuation at IPO 16 ’14 EBITDA 13 ’14 EBITDA

% offered at IPO 51.8% 19.7%

Primary/secondary split at IPO

44%:56% 100%:0%

Greenshoe exercised In shoe Partial

First day performance 10.42% 1.46%

Private equity sponsor(s) Advent International, Bain Capital

KKR

Nov ’16 Jan ’17

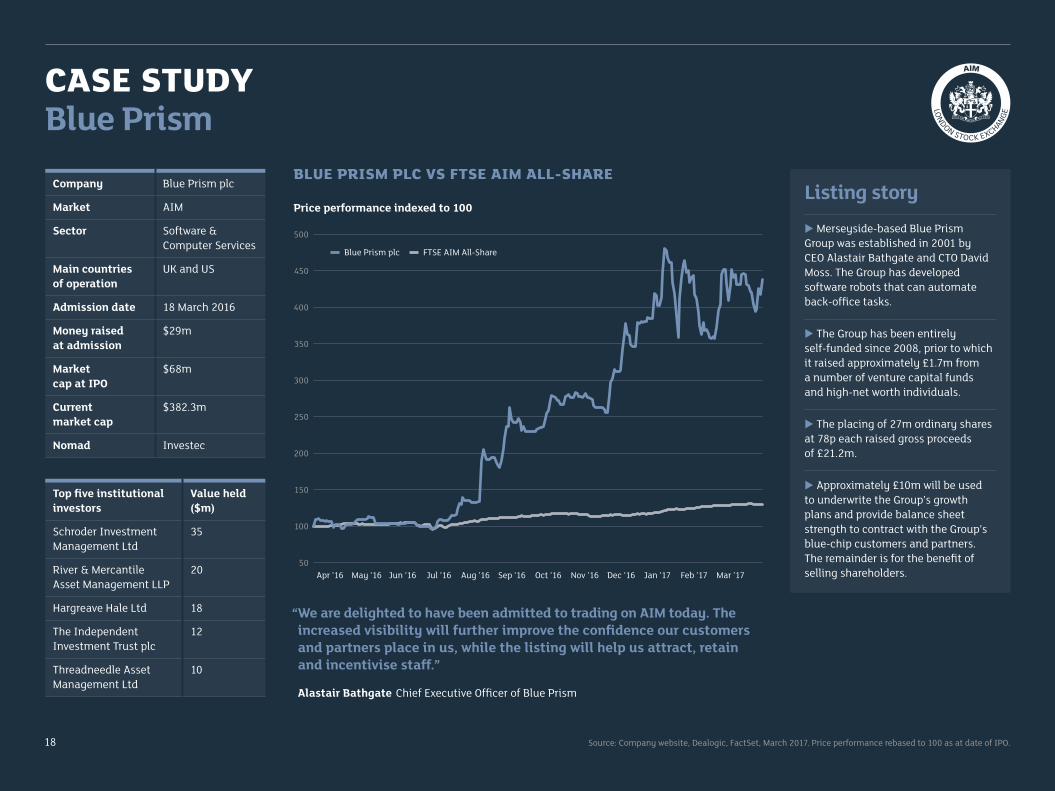

CASE STUDYBlue Prism

18

Company Blue Prism plc

Market AIM

Sector Software & Computer Services

Main countries of operation

UK and US

Admission date 18 March 2016

Money raised at admission

$29m

Market cap at IPO

$68m

Current market cap

$382.3m

Nomad Investec

Top five institutional investors

Value held ($m)

Schroder Investment Management Ltd

35

River & Mercantile Asset Management LLP

20

Hargreave Hale Ltd 18

The Independent Investment Trust plc

12

Threadneedle Asset Management Ltd

10

Listing storyu Merseyside-based Blue Prism Group was established in 2001 by CEO Alastair Bathgate and CTO David Moss. The Group has developed software robots that can automate back-office tasks.

u The Group has been entirely self-funded since 2008, prior to which it raised approximately £1.7m from a number of venture capital funds and high-net worth individuals.

u The placing of 27m ordinary shares at 78p each raised gross proceeds of £21.2m.

u Approximately £10m will be used to underwrite the Group’s growth plans and provide balance sheet strength to contract with the Group’s blue-chip customers and partners. The remainder is for the benefit of selling shareholders.

“We are delighted to have been admitted to trading on AIM today. The increased visibility will further improve the confidence our customers and partners place in us, while the listing will help us attract, retain and incentivise staff.”

Alastair Bathgate Chief Executive Officer of Blue Prism

BLUE PRISM PLC VS FTSE AIM ALL-SHARE

Price performance indexed to 100

Apr ’16 Mar ’17

Blue Prism plc FTSE AIM All-Share

500

400

250

200

150

100

50

350

300

450

Source: Company website, Dealogic, FactSet, March 2017. Price performance rebased to 100 as at date of IPO.

May ’16 Jun ’16 Jul ’16 Aug ’16 Sep ’16 Oct ’16 Nov ’16 Dec ’16 Jan ’17 Feb ’17

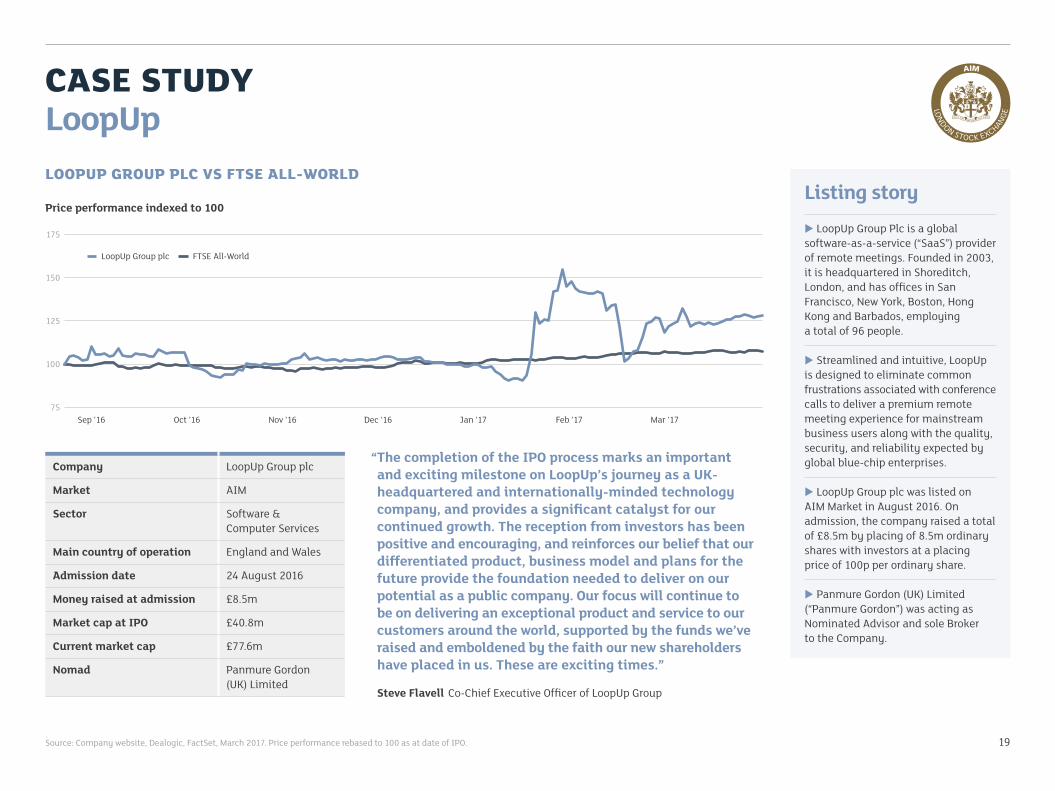

CASE STUDYLoopUp

19

Company LoopUp Group plc

Market AIM

Sector Software & Computer Services

Main country of operation England and Wales

Admission date 24 August 2016

Money raised at admission £8.5m

Market cap at IPO £40.8m

Current market cap £77.6m

Nomad Panmure Gordon (UK) Limited

Source: Company website, Dealogic, FactSet, March 2017. Price performance rebased to 100 as at date of IPO.

Listing storyu LoopUp Group Plc is a global software-as-a-service (“SaaS”) provider of remote meetings. Founded in 2003, it is headquartered in Shoreditch, London, and has offices in San Francisco, New York, Boston, Hong Kong and Barbados, employing a total of 96 people.

u Streamlined and intuitive, LoopUp is designed to eliminate common frustrations associated with conference calls to deliver a premium remote meeting experience for mainstream business users along with the quality, security, and reliability expected by global blue-chip enterprises.

u LoopUp Group plc was listed on AIM Market in August 2016. On admission, the company raised a total of £8.5m by placing of 8.5m ordinary shares with investors at a placing price of 100p per ordinary share.

u Panmure Gordon (UK) Limited (“Panmure Gordon”) was acting as Nominated Advisor and sole Broker to the Company.

“The completion of the IPO process marks an important and exciting milestone on LoopUp’s journey as a UK-headquartered and internationally-minded technology company, and provides a significant catalyst for our continued growth. The reception from investors has been positive and encouraging, and reinforces our belief that our differentiated product, business model and plans for the future provide the foundation needed to deliver on our potential as a public company. Our focus will continue to be on delivering an exceptional product and service to our customers around the world, supported by the funds we’ve raised and emboldened by the faith our new shareholders have placed in us. These are exciting times.”

Steve Flavell Co-Chief Executive Officer of LoopUp Group

LOOPUP GROUP PLC VS FTSE ALL-WORLD

Price performance indexed to 100

175

Sep ’16 Mar ’1775

150

100

125

Oct ’16 Nov ’16 Dec ’16 Jan ’17 Feb ’17

LoopUp Group plc FTSE All-World

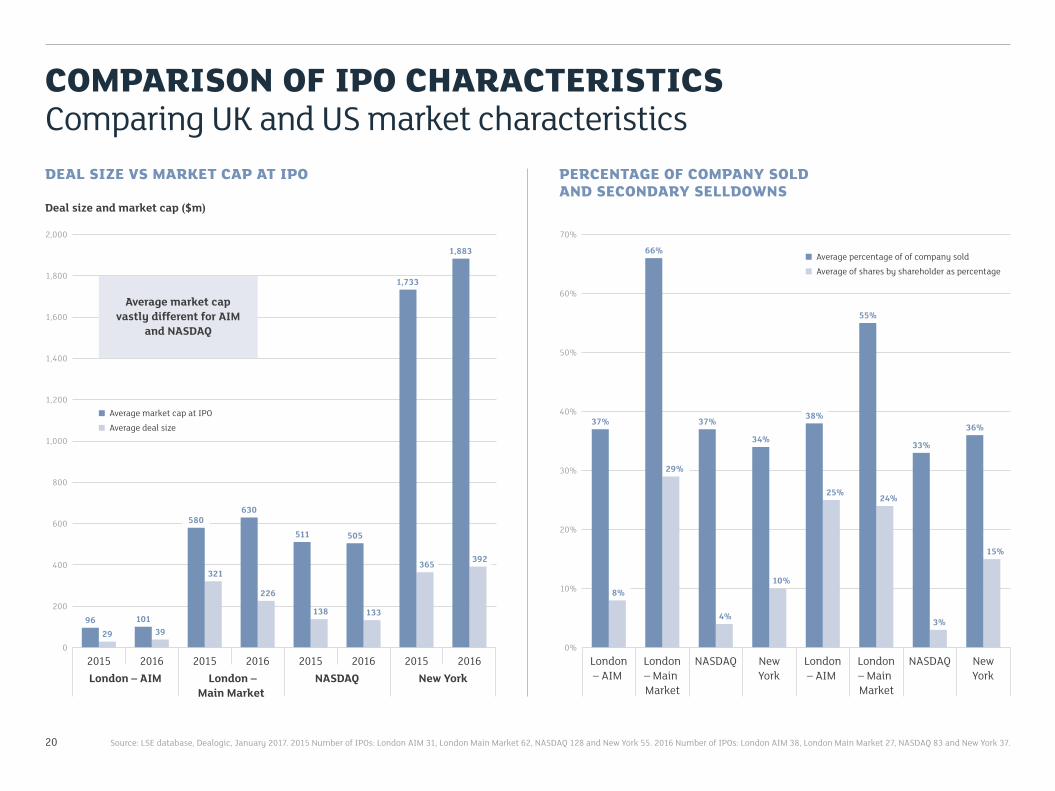

COMPARISON OF IPO CHARACTERISTICSComparing UK and US market characteristics

20

DEAL SIZE VS MARKET CAP AT IPO

Deal size and market cap ($m)

2,000

PERCENTAGE OF COMPANY SOLD AND SECONDARY SELLDOWNS

70%

London – AIM2015

020162016 2015 2016 2015 2016 2015

New YorkLondon – Main Market

NASDAQ

1,800

1,600

1,400

1,200

1,000

800

600

400

200

Source: LSE database, Dealogic, January 2017. 2015 Number of IPOs: London AIM 31, London Main Market 62, NASDAQ 128 and New York 55. 2016 Number of IPOs: London AIM 38, London Main Market 27, NASDAQ 83 and New York 37.

9629

10139

580

321

630

226

511

138

505

133

1,733

365

1,883

392

Average market cap at IPO

Average deal size

Average market cap vastly different for AIM

and NASDAQ

0%London – AIM

New York

London – Main Market

NASDAQ New York

London – AIM

London – Main Market

NASDAQ

60%

50%

40%

30%

20%

10%

Average percentage of of company sold

Average of shares by shareholder as percentage

37%

66%

37%

34%

38%

55%

33%

36%

8%

29%

4%

10%

25%24%

3%

15%

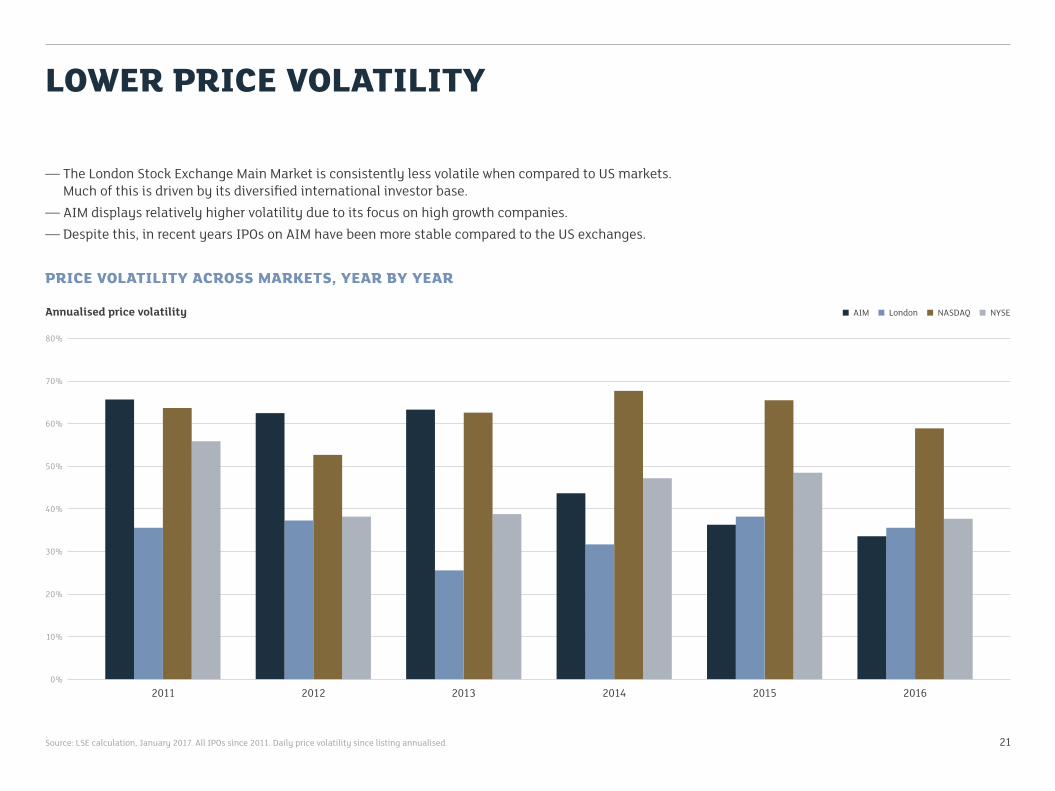

LOWER PRICE VOLATILITY

21

— The London Stock Exchange Main Market is consistently less volatile when compared to US markets. Much of this is driven by its diversified international investor base.

— AIM displays relatively higher volatility due to its focus on high growth companies.— Despite this, in recent years IPOs on AIM have been more stable compared to the US exchanges.

PRICE VOLATILITY ACROSS MARKETS, YEAR BY YEAR

Annualised price volatility

80%

20110%

70%

60%

50%

40%

30%

20%

10%

20162012 2013 2014 2015

AIM London NASDAQ NYSE

Source: LSE calculation, January 2017. All IPOs since 2011. Daily price volatility since listing annualised.

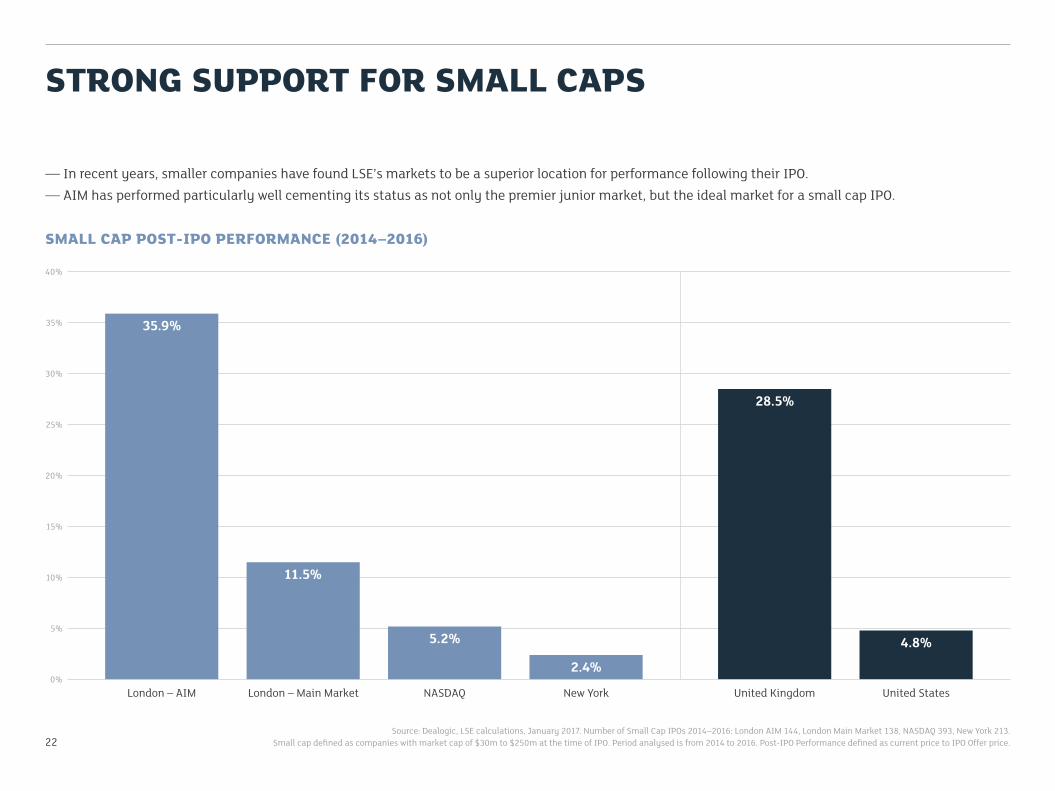

STRONG SUPPORT FOR SMALL CAPS

22

— In recent years, smaller companies have found LSE’s markets to be a superior location for performance following their IPO.— AIM has performed particularly well cementing its status as not only the premier junior market, but the ideal market for a small cap IPO.

Source: Dealogic, LSE calculations, January 2017. Number of Small Cap IPOs 2014–2016: London AIM 144, London Main Market 138, NASDAQ 393, New York 213.Small cap defined as companies with market cap of $30m to $250m at the time of IPO. Period analysed is from 2014 to 2016. Post-IPO Performance defined as current price to IPO Offer price.

SMALL CAP POST-IPO PERFORMANCE (2014–2016)

40%

0%

35%

30%

25%

20%

15%

10%

5%

London – AIM United StatesLondon – Main Market NASDAQ New York United Kingdom

35.9%

11.5%

5.2%

2.4%

28.5%

4.8%

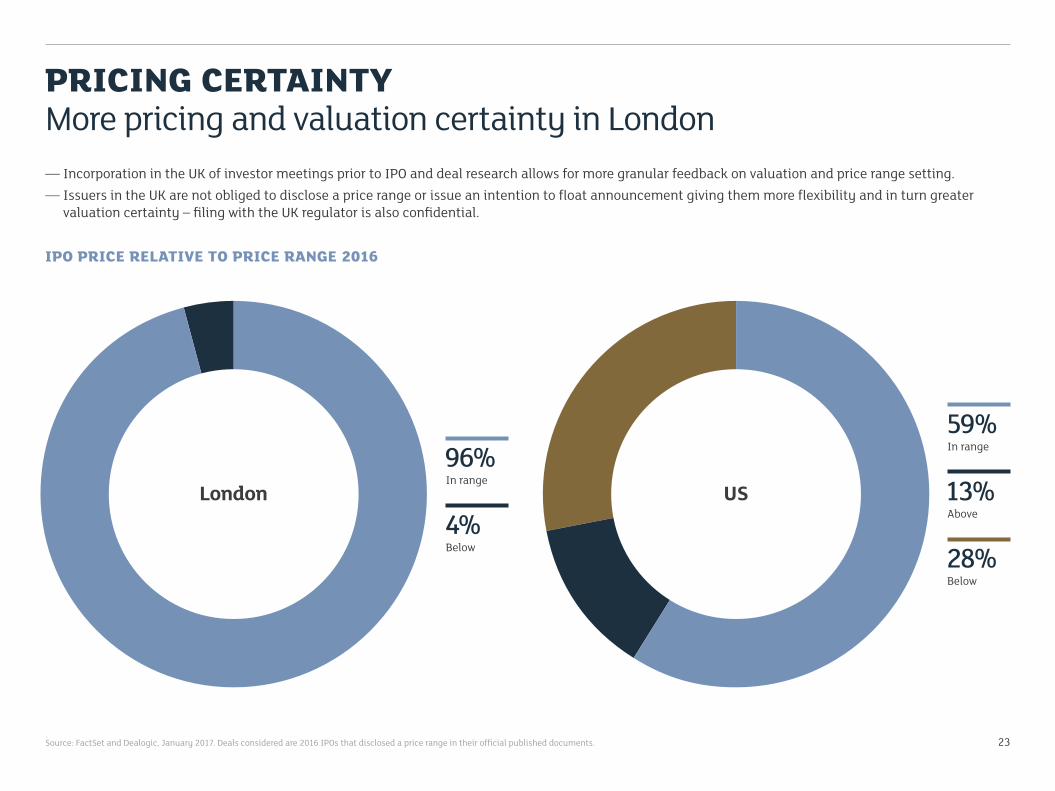

PRICING CERTAINTYMore pricing and valuation certainty in London

23Source: FactSet and Dealogic, January 2017. Deals considered are 2016 IPOs that disclosed a price range in their official published documents.

— Incorporation in the UK of investor meetings prior to IPO and deal research allows for more granular feedback on valuation and price range setting.— Issuers in the UK are not obliged to disclose a price range or issue an intention to float announcement giving them more flexibility and in turn greater

valuation certainty – filing with the UK regulator is also confidential.

IPO PRICE RELATIVE TO PRICE RANGE 2016

96%In range

4%Below

59%In range

13%Above

28%Below

London US

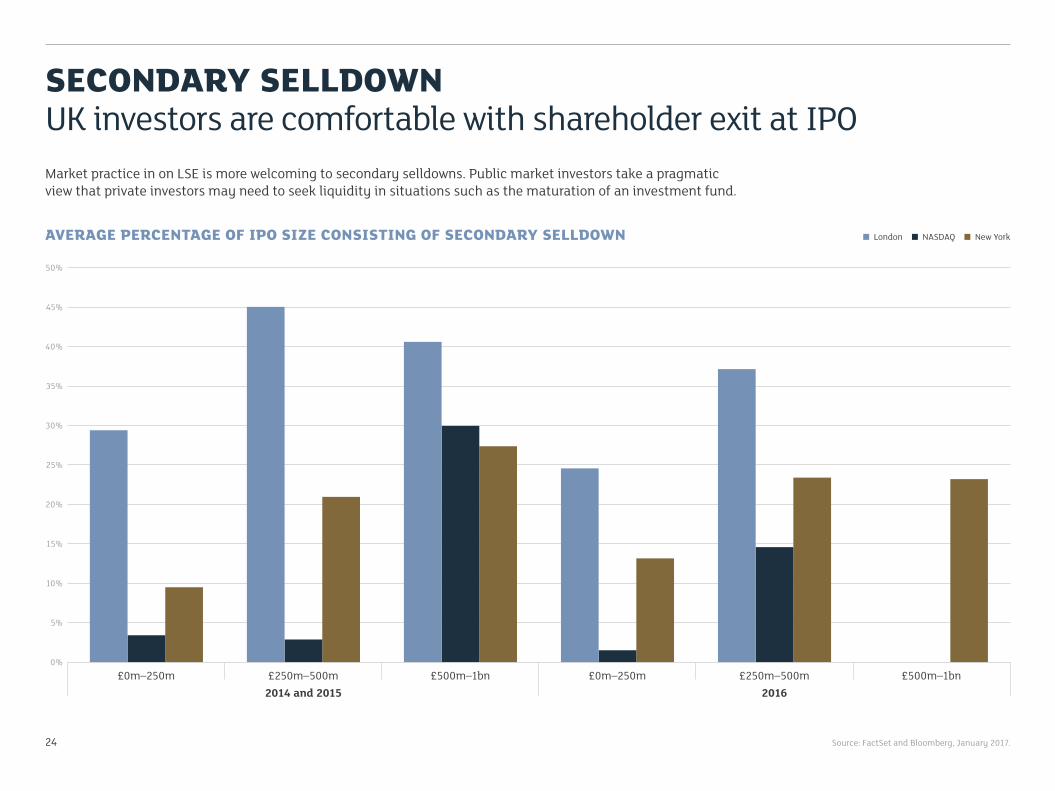

SECONDARY SELLDOWNUK investors are comfortable with shareholder exit at IPO

24

Market practice in on LSE is more welcoming to secondary selldowns. Public market investors take a pragmatic view that private investors may need to seek liquidity in situations such as the maturation of an investment fund.

Source: FactSet and Bloomberg, January 2017.

AVERAGE PERCENTAGE OF IPO SIZE CONSISTING OF SECONDARY SELLDOWN

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

2014 and 2015£0m–250m

0%

2016£500m–1bn£250m–500m £500m–1bn £0m–250m £250m–500m

London NASDAQ New York

25

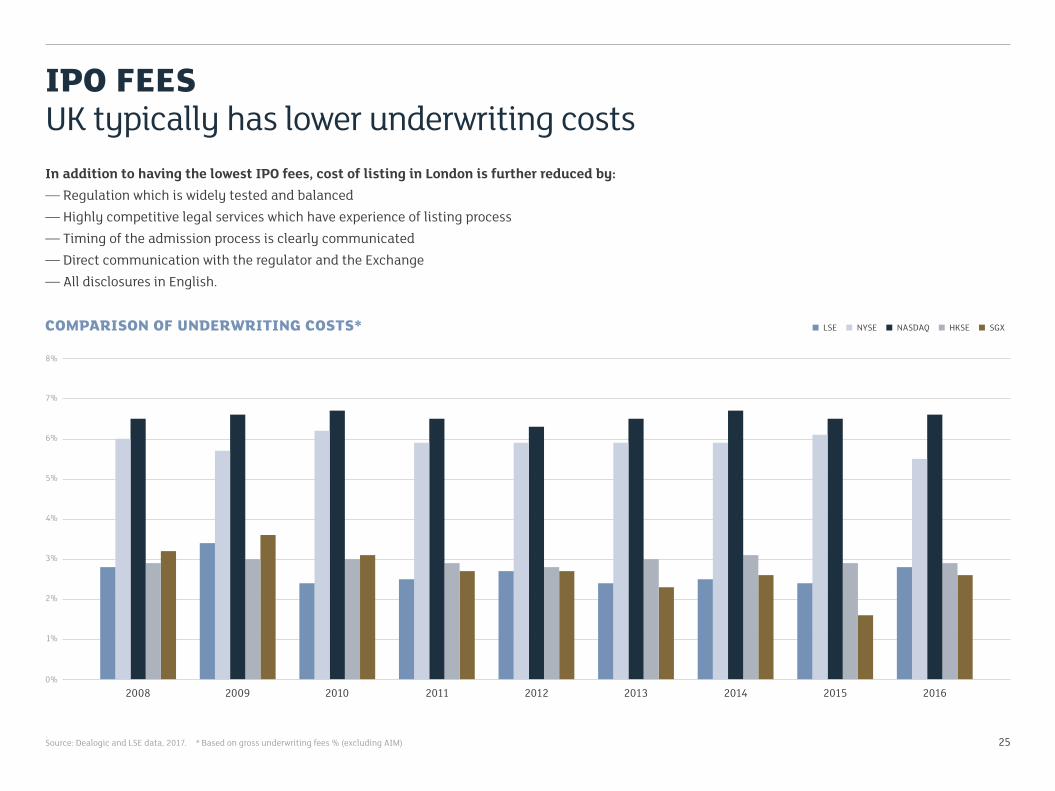

IPO FEESUK typically has lower underwriting costs

Source: Dealogic and LSE data, 2017. * Based on gross underwriting fees % (excluding AIM)

In addition to having the lowest IPO fees, cost of listing in London is further reduced by:— Regulation which is widely tested and balanced— Highly competitive legal services which have experience of listing process— Timing of the admission process is clearly communicated— Direct communication with the regulator and the Exchange— All disclosures in English.

COMPARISON OF UNDERWRITING COSTS* LSE NYSE NASDAQ HKSE SGX

2008 2009 2010 2011 2012 2013 2014 2015 2016

7%

6%

5%

4%

3%

2%

1%

8%

0%

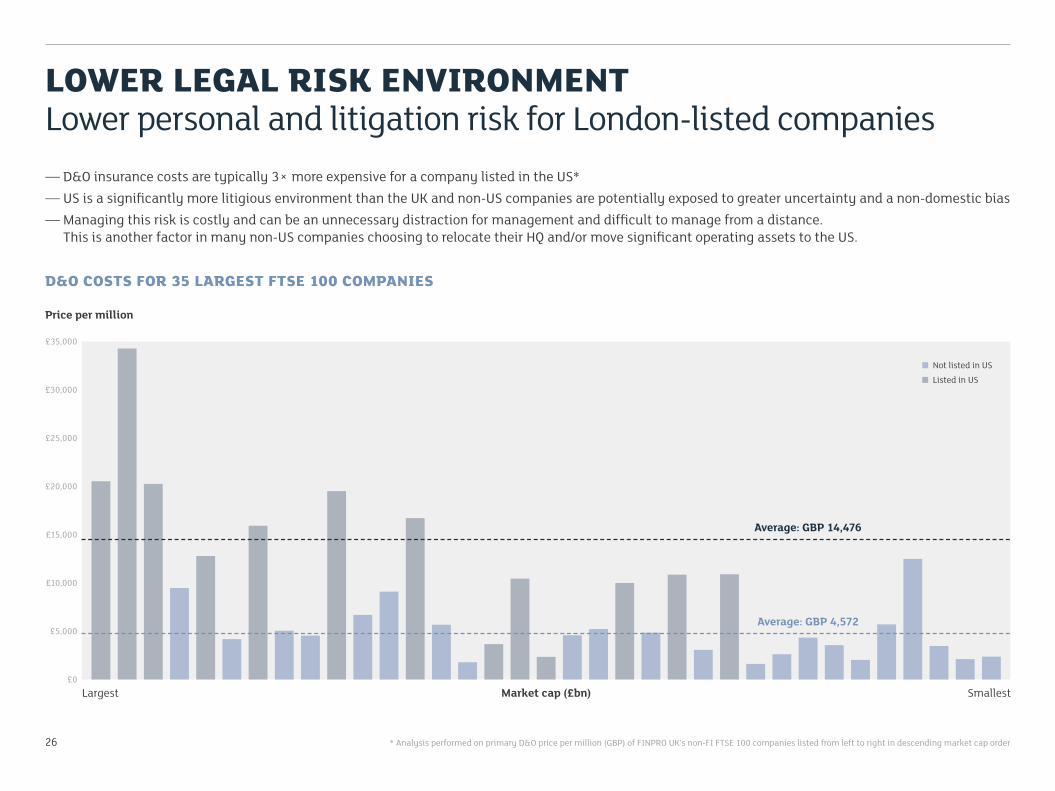

* Analysis performed on primary D&O price per million (GBP) of FINPRO UK’s non-FI FTSE 100 companies listed from left to right in descending market cap order

D&O COSTS FOR 35 LARGEST FTSE 100 COMPANIES

Price per million

Not listed in US

Listed in US

Average: GBP 14,476

Average: GBP 4,572

26

LOWER LEGAL RISK ENVIRONMENTLower personal and litigation risk for London-listed companies— D&O insurance costs are typically 3× more expensive for a company listed in the US*— US is a significantly more litigious environment than the UK and non-US companies are potentially exposed to greater uncertainty and a non-domestic bias— Managing this risk is costly and can be an unnecessary distraction for management and difficult to manage from a distance.

This is another factor in many non-US companies choosing to relocate their HQ and/or move significant operating assets to the US.

Largest Market cap (£bn) Smallest

£35,000

£30,000

£25,000

£20,000

£15,000

£10,000

£5,000

£0

LONDON STOCK EXCHANGE TECH CONTACTSUK

James ClarkTelephone +44 20 7797 [email protected]

Tom AttenboroughTelephone +44 20 7797 [email protected]

RUSSIA & CIS

Ayuna Nechaeva (London)Telephone +44 20 7797 [email protected]

ASIA PACIFIC

Jon Edwards (Beijing)Telephone +44 20 7797 [email protected]

INTERNATIONAL

Tom AttenboroughTelephone +44 20 7797 [email protected]

AMERICAS

Chris Mayo (Chicago)Telephone +1 646 925 [email protected]

CONTINENTAL EUROPE

Axel KalinowskiTelephone +44 20 7797 [email protected]

ISRAEL

Justine Zwerling (Tel Aviv)Telephone +97 [email protected]

For further information refer to www.lseg.com 27

NOTES

28

This document has been compiled by the London Stock Exchange plc (the “Exchange”). The Exchange has attempted to ensure that the information in this document is accurate, however the information is provided “AS IS” and on an “AS AVAILABLE” basis and may not be accurate or up to date. The Exchange does not guarantee the accuracy, timeliness, completeness, performance or fitness for a particular purpose of the document or any of the information in it. The Exchange is not responsible for any third party content which is set out in this document. No responsibility is accepted by or on behalf of the Exchange for any errors, omissions, or inaccurate information in the document. No action should be taken or omitted to be taken in reliance upon information in this document. The Exchange accepts no liability for the results of any action taken on the basis of the information in this document. All implied warranties, including but not limited to the implied warranties of satisfactory quality, fitness for a particular purpose, non-infringement, compatibility, security and accuracy are excluded by the Exchange to the extent that they may be excluded as a matter of law. Further, the Exchange does not warrant that the document is error free or that any defects will be corrected. To the extent permitted by applicable law, the Exchange expressly disclaims all liability howsoever arising whether in contract, tort (or deceit) or otherwise (including, but not limited to, liability for any negligent act or omissions) to any person in respect of any claims or losses of any nature, arising directly or indirectly from: (i) anything done or the consequences of anything done or omitted to be done wholly or partly in reliance upon the whole or any part of the contents of this document, and (ii) the use of any data or materials in this document. Information in this document is not offered as advice on any particular matter and must not be treated as a substitute for specific advice. In particular information in the document does not constitute professional, financial or investment advice and must not be used as a basis for making investment decisions and is in no way intended, directly or indirectly, as an attempt to market or sell any type of financial instrument. Advice from a suitably qualified professional should always be sought in relation to any particular matter or circumstances. The contents of this document do not constitute an invitation to invest in shares of the Exchange, or constitute or form a part of any offer for the sale or subscription of, or any invitation to offer to buy or subscribe for, any securities or other financial instruments, nor should it or any part of it form the basis of, or be relied upon in any connection with any contract or commitment whatsoever. London Stock Exchange and the London Stock Exchange coat of arms device are registered trade marks of London Stock Exchange plc. Other logos, organisations and company names referred to may be the trade marks of their respective owners.

© March 2017London Stock Exchange plc, 10 Paternoster Square, London EC4M 7LSTelephone +44 (0)20 7797 1000www.lseg.com