long-term assets. types of long-term assets n property, plant, and equipment –long-term assets...

Post on 21-Dec-2015

218 views

TRANSCRIPT

Long-term AssetsLong-term Assets

Types of Long-Term AssetsTypes of Long-Term Assets

Property, plant, and equipmentProperty, plant, and equipment

– Long-term assets acquired for use in Long-term assets acquired for use in operationsoperations

Natural resourcesNatural resources

– Long-term assets with a value that Long-term assets with a value that decreases through use or saledecreases through use or sale

Types of Long-Term AssetsTypes of Long-Term Assets

Intangible assetsIntangible assets

– Long-term assets that do not have Long-term assets that do not have physical substancephysical substance

Plant Asset CostPlant Asset Cost

Purchase price (less cash Purchase price (less cash discount)discount)

Plant Asset CostPlant Asset Cost

Purchase price (less cash Purchase price (less cash discount) plus all other discount) plus all other reasonable and necessary reasonable and necessary expendituresexpenditures

Plant Asset CostPlant Asset Cost

Purchase price (less cash Purchase price (less cash discount) plus all other discount) plus all other reasonable and necessary reasonable and necessary expenditures to prepare the expenditures to prepare the asset for useasset for use

Examples of Items IncludedExamples of Items Included

Purchase price less any cash discountPurchase price less any cash discount Shipping costsShipping costs Installation costsInstallation costs Cost of modificationsCost of modifications Interest cost during constructionInterest cost during construction

DepreciationDepreciation

Allocation of the cost of an asset to the Allocation of the cost of an asset to the periods the asset benefitsperiods the asset benefits

Not a valuation processNot a valuation process

Factors in Estimating Factors in Estimating DepreciationDepreciation

Initial costInitial cost Estimated residual valueEstimated residual value Estimated Useful LifeEstimated Useful Life

Depreciation MethodsDepreciation Methods

Straight-lineStraight-line

– allocate an equal amount to each allocate an equal amount to each periodperiod

Production unitProduction unit

– depreciation based on volume of depreciation based on volume of outputoutput

Accelerated Accelerated Depreciation MethodsDepreciation Methods

Double Declining-balanceDouble Declining-balance

– apply a uniform rate to a declining apply a uniform rate to a declining amount (book value)amount (book value)

Sum-of-the-Years’-DigitsSum-of-the-Years’-Digits

– annual amount the decreases by a annual amount the decreases by a constant amountconstant amount

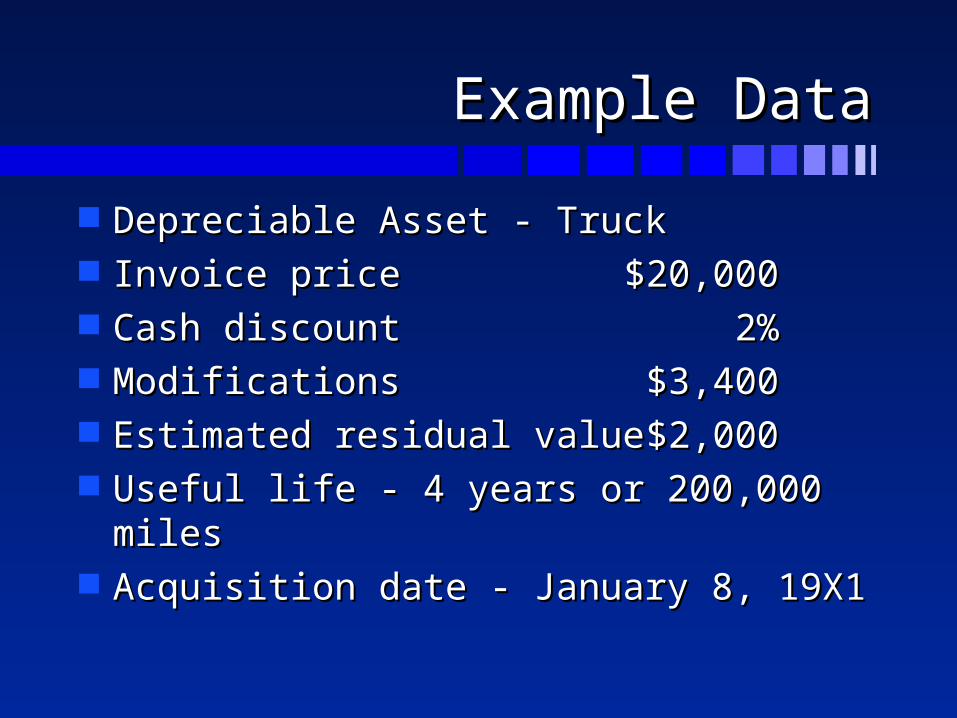

Example DataExample Data

Depreciable Asset - TruckDepreciable Asset - Truck Invoice priceInvoice price $20,000$20,000 Cash discountCash discount 2%2% ModificationsModifications $3,400 $3,400 Estimated residual valueEstimated residual value $2,000$2,000 Useful life - 4 years or 200,000 milesUseful life - 4 years or 200,000 miles Acquisition date - January 8, 19X1Acquisition date - January 8, 19X1

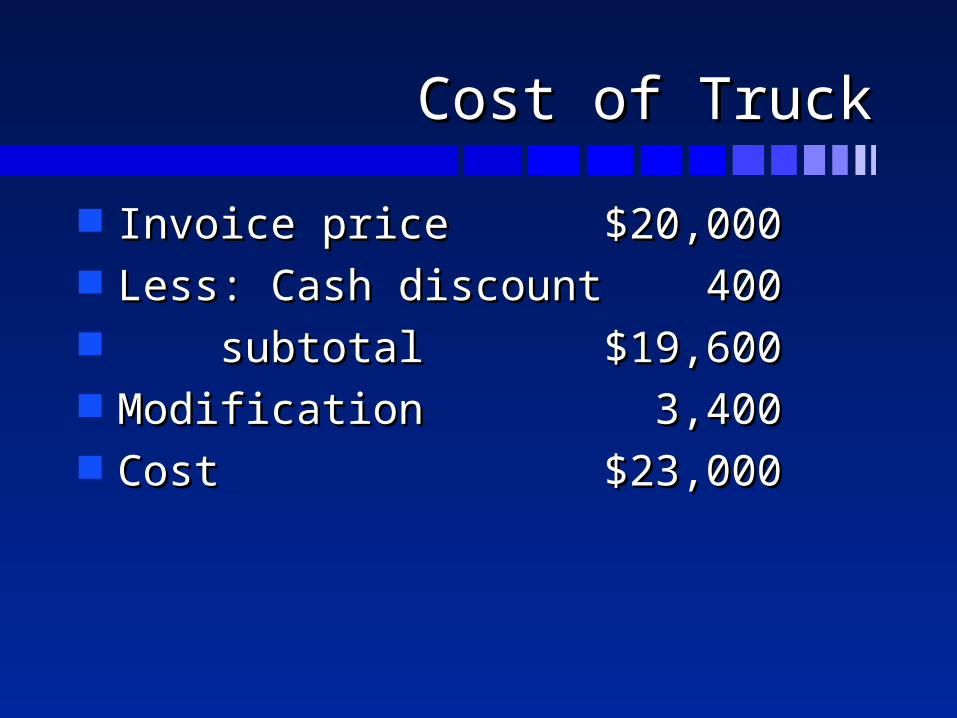

Cost of TruckCost of Truck

Invoice priceInvoice price $20,000$20,000 Less: Cash discountLess: Cash discount 400400 subtotalsubtotal $19,600$19,600 ModificationModification 3,4003,400 CostCost $23,000$23,000

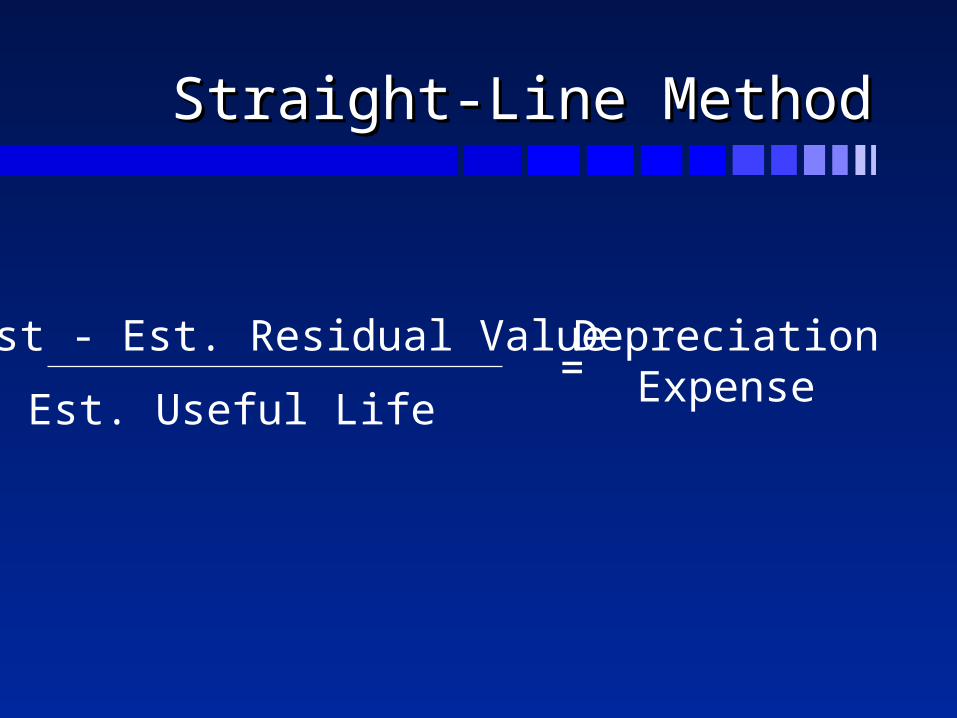

Straight-Line MethodStraight-Line Method

Cost - Est. Residual Value

Est. Useful Life=

DepreciationExpense

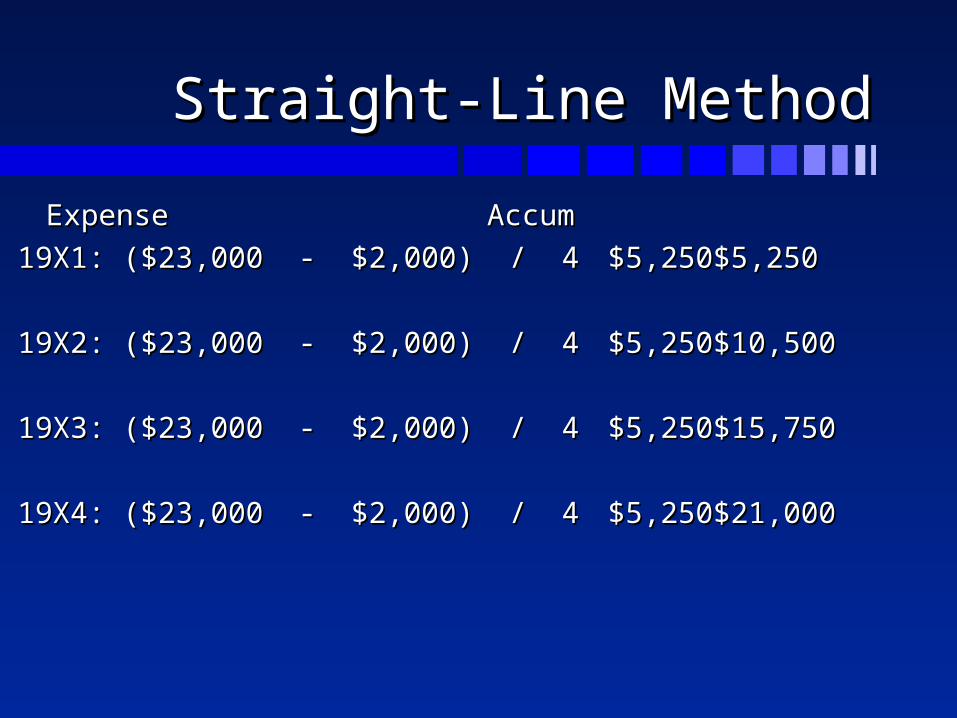

Straight-Line MethodStraight-Line Method

ExpenseExpense AccumAccum

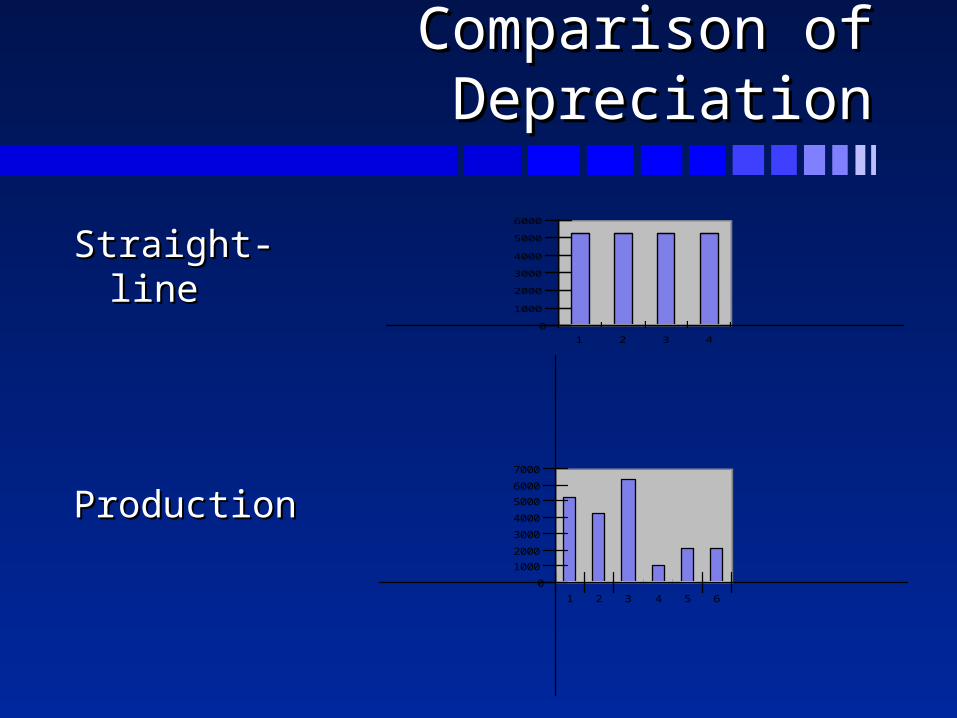

19X1: ($23,000 - $2,000) / 419X1: ($23,000 - $2,000) / 4 $5,250$5,250 $5,250$5,250

19X2: ($23,000 - $2,000) / 419X2: ($23,000 - $2,000) / 4 $5,250$5,250 $10,500$10,500

19X3: ($23,000 - $2,000) / 419X3: ($23,000 - $2,000) / 4 $5,250$5,250 $15,750$15,750

19X4: ($23,000 - $2,000) / 419X4: ($23,000 - $2,000) / 4 $5,250$5,250 $21,000$21,000

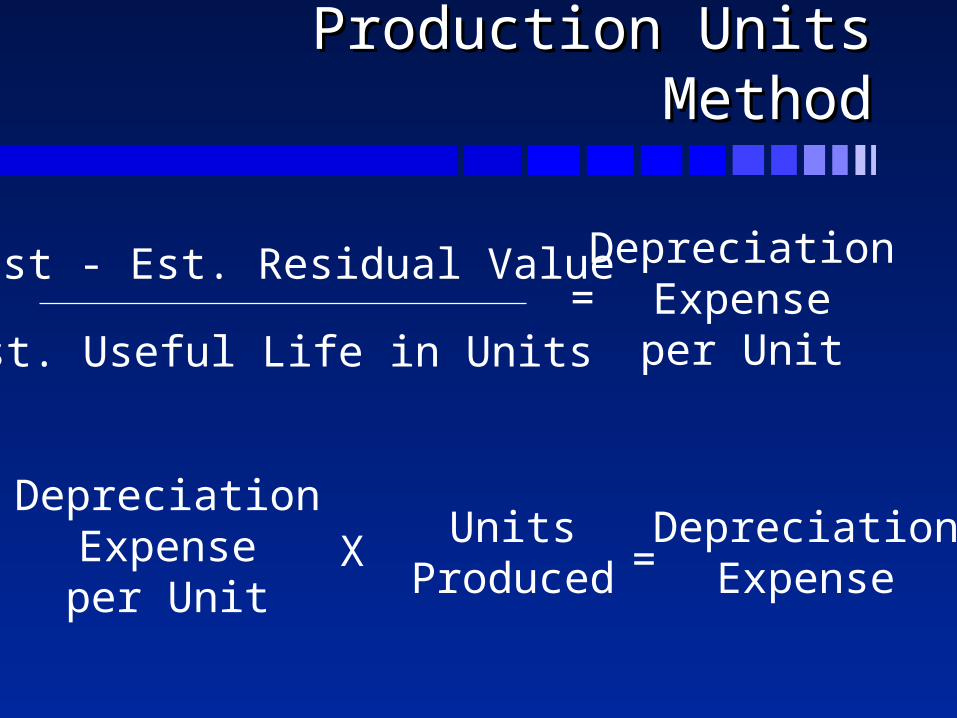

Production Units MethodProduction Units Method

Cost - Est. Residual Value

Est. Useful Life in Units=

DepreciationExpenseper Unit

DepreciationExpenseper Unit

XUnits

Produced =Depreciation

Expense

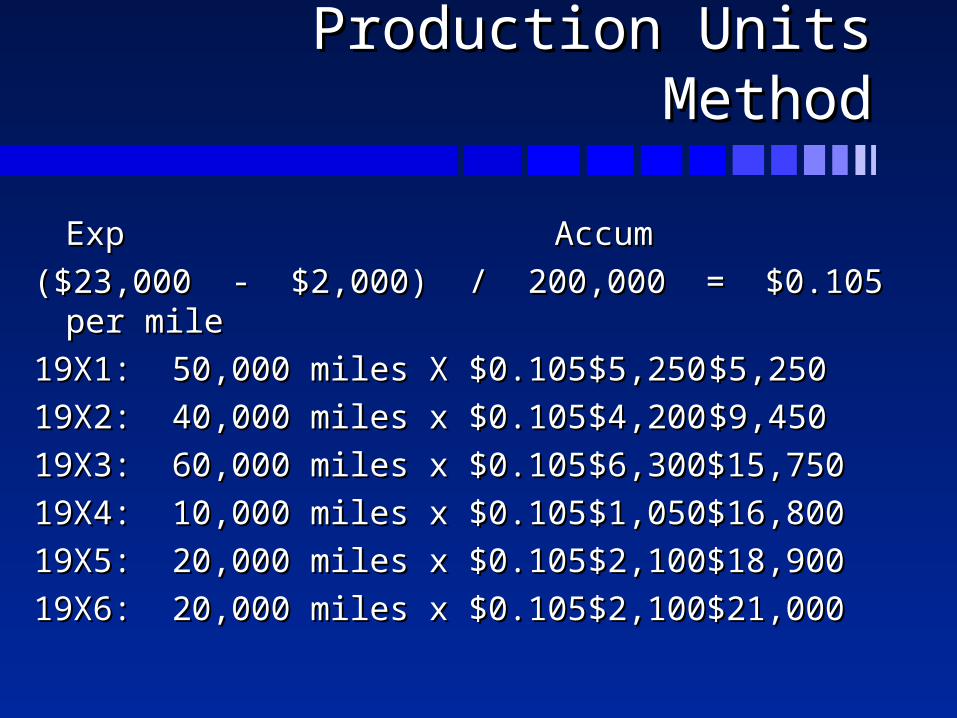

Production Units MethodProduction Units Method

Exp Exp Accum Accum

($23,000 - $2,000) / 200,000 = $0.105 per mile($23,000 - $2,000) / 200,000 = $0.105 per mile

19X1: 50,000 miles X $0.10519X1: 50,000 miles X $0.105 $5,250$5,250 $5,250$5,250

19X2: 40,000 miles x $0.10519X2: 40,000 miles x $0.105 $4,200$4,200 $9,450$9,450

19X3: 60,000 miles x $0.10519X3: 60,000 miles x $0.105 $6,300$6,300 $15,750$15,750

19X4: 10,000 miles x $0.10519X4: 10,000 miles x $0.105 $1,050$1,050 $16,800$16,800

19X5: 20,000 miles x $0.10519X5: 20,000 miles x $0.105 $2,100$2,100 $18,900$18,900

19X6: 20,000 miles x $0.10519X6: 20,000 miles x $0.105 $2,100$2,100 $21,000$21,000

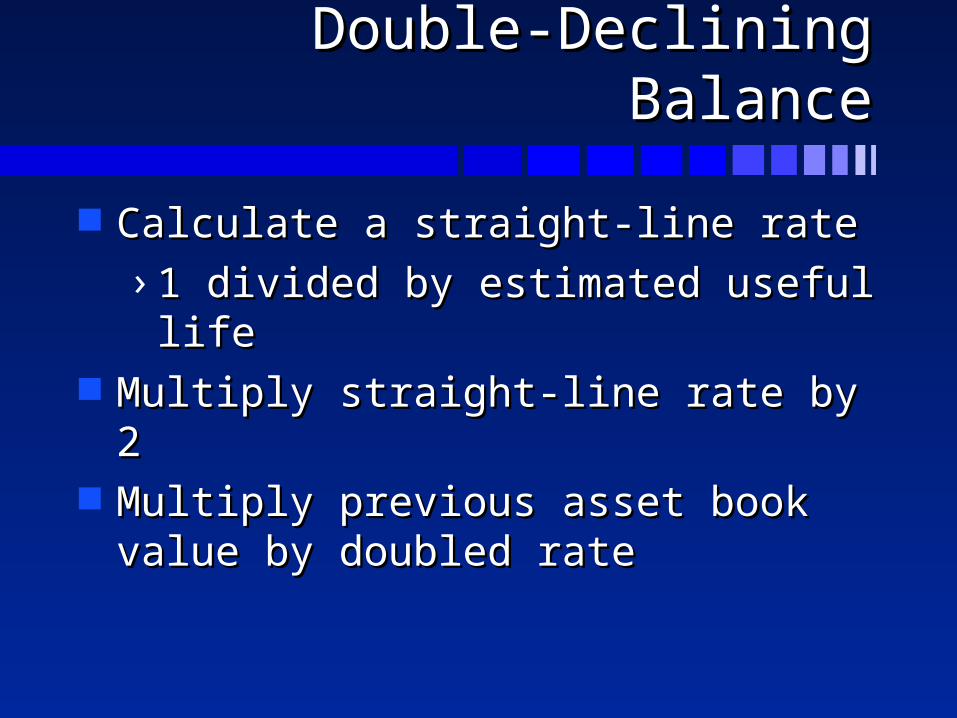

Double-Declining BalanceDouble-Declining Balance

Calculate a straight-line rateCalculate a straight-line rate

› 1 divided by estimated useful life1 divided by estimated useful life Multiply straight-line rate by 2Multiply straight-line rate by 2 Multiply previous asset book value by Multiply previous asset book value by

doubled ratedoubled rate

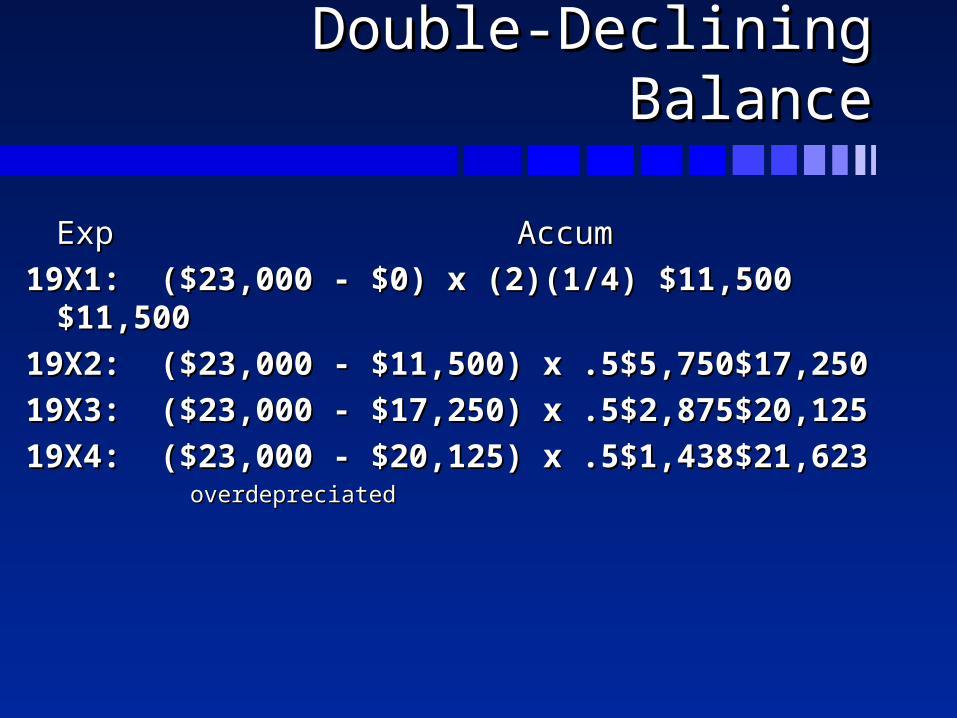

Double-Declining BalanceDouble-Declining Balance

Exp Exp Accum Accum

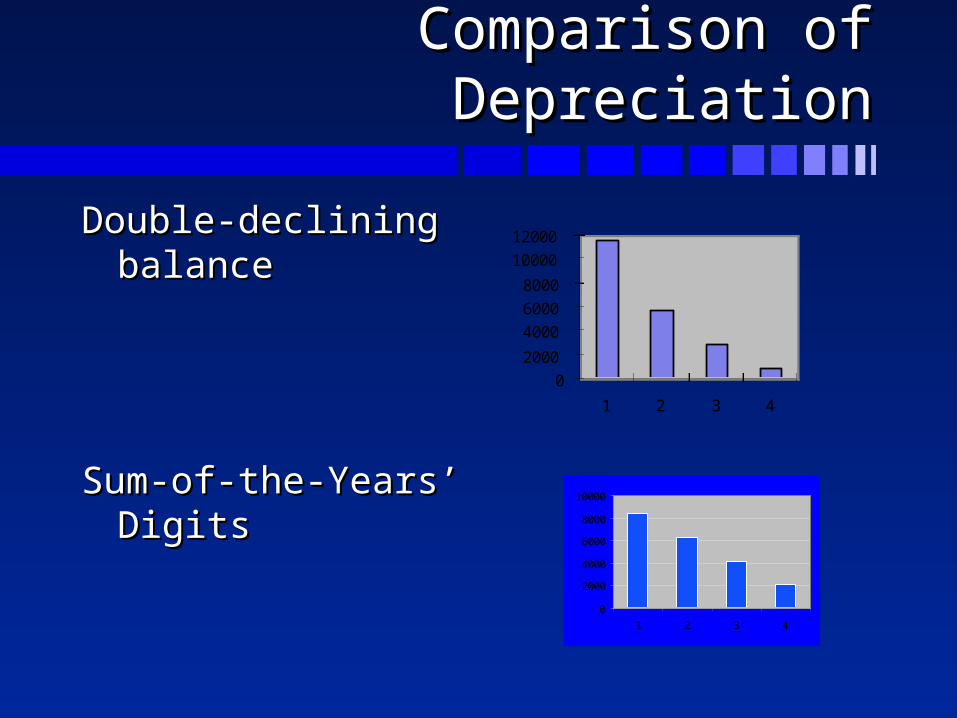

19X1: ($23,000 - $0) x (2)(1/4)19X1: ($23,000 - $0) x (2)(1/4) $11,500$11,500 $11,500$11,500

19X2: ($23,000 - $11,500) x .519X2: ($23,000 - $11,500) x .5 $5,750$5,750 $17,250$17,250

19X3: ($23,000 - $17,250) x .519X3: ($23,000 - $17,250) x .5 $2,875$2,875 $20,125$20,125

19X4: ($23,000 - $20,125) x .519X4: ($23,000 - $20,125) x .5 $1,438$1,438 $21,623$21,623overdepreciatedoverdepreciated

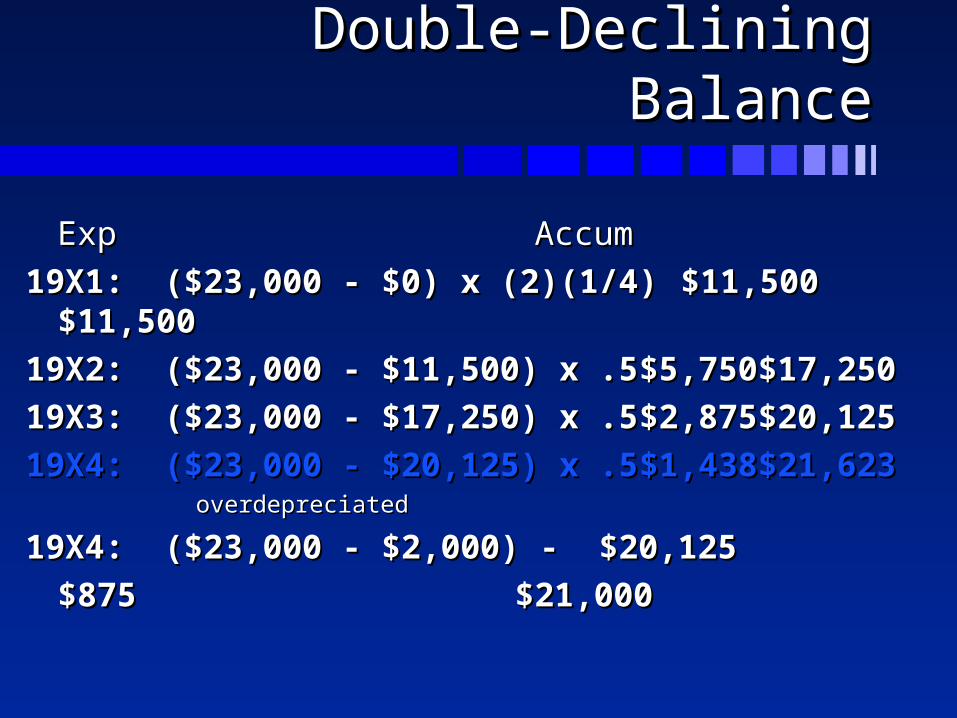

Double-Declining BalanceDouble-Declining Balance

Exp Exp Accum Accum

19X1: ($23,000 - $0) x (2)(1/4)19X1: ($23,000 - $0) x (2)(1/4) $11,500$11,500 $11,500$11,500

19X2: ($23,000 - $11,500) x .519X2: ($23,000 - $11,500) x .5 $5,750$5,750 $17,250$17,250

19X3: ($23,000 - $17,250) x .519X3: ($23,000 - $17,250) x .5 $2,875$2,875 $20,125$20,125

19X4: ($23,000 - $20,125) x .519X4: ($23,000 - $20,125) x .5 $1,438$1,438 $21,623$21,623overdepreciatedoverdepreciated

19X4: ($23,000 - $2,000) - $20,12519X4: ($23,000 - $2,000) - $20,125

$875$875 $21,000$21,000

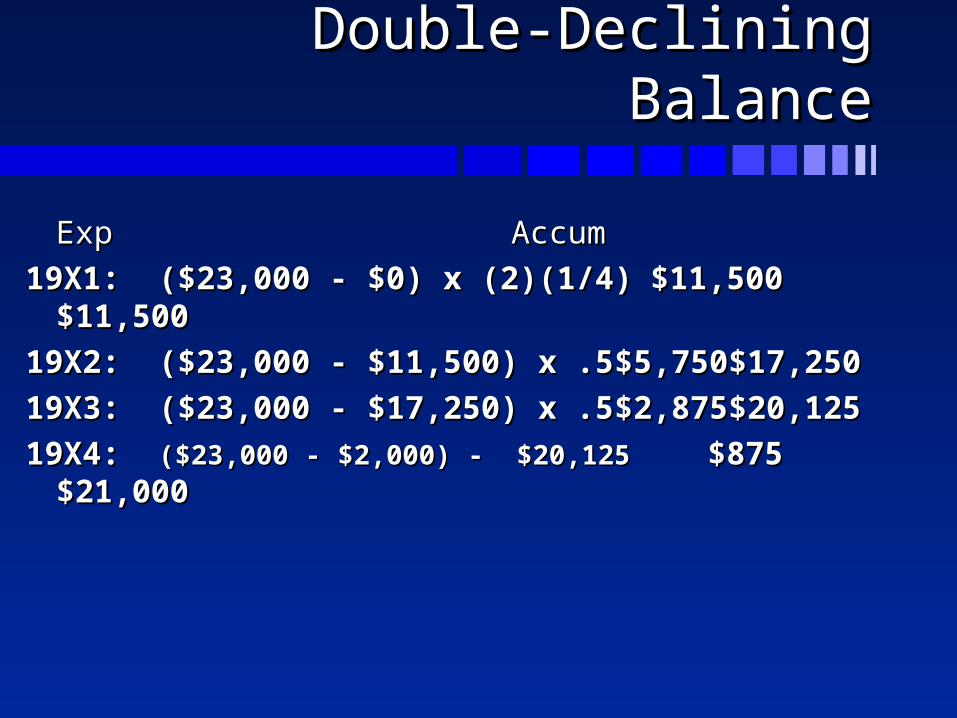

Double-Declining BalanceDouble-Declining Balance

Exp Exp Accum Accum

19X1: ($23,000 - $0) x (2)(1/4)19X1: ($23,000 - $0) x (2)(1/4) $11,500$11,500 $11,500$11,500

19X2: ($23,000 - $11,500) x .519X2: ($23,000 - $11,500) x .5 $5,750$5,750 $17,250$17,250

19X3: ($23,000 - $17,250) x .519X3: ($23,000 - $17,250) x .5 $2,875$2,875 $20,125$20,125

19X4: 19X4: ($23,000 - $2,000) - $20,125($23,000 - $2,000) - $20,125 $875$875 $21,000$21,000

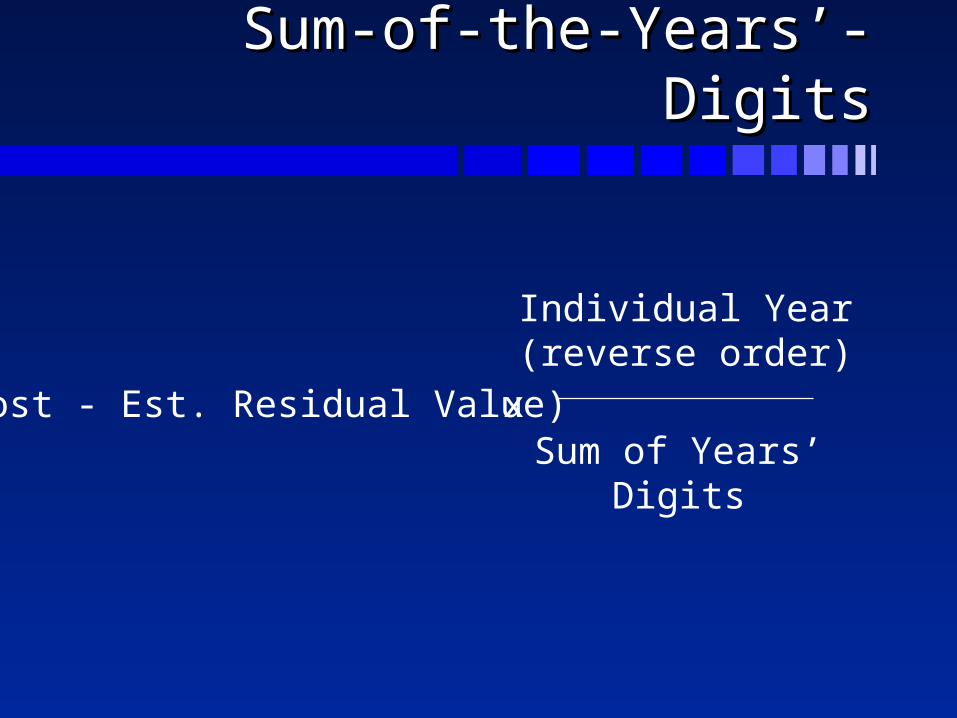

Sum-of-the-Years’-DigitsSum-of-the-Years’-Digits

(Cost - Est. Residual Value) x

Individual Year(reverse order)

Sum of Years’Digits

Sum-of-the-Years’-DigitsSum-of-the-Years’-Digits

Calculating sum of years’ digitsCalculating sum of years’ digits Add the numeric digits in useful lifeAdd the numeric digits in useful life ExampleExample

› 1 + 2 + 3 + 4 = 101 + 2 + 3 + 4 = 10

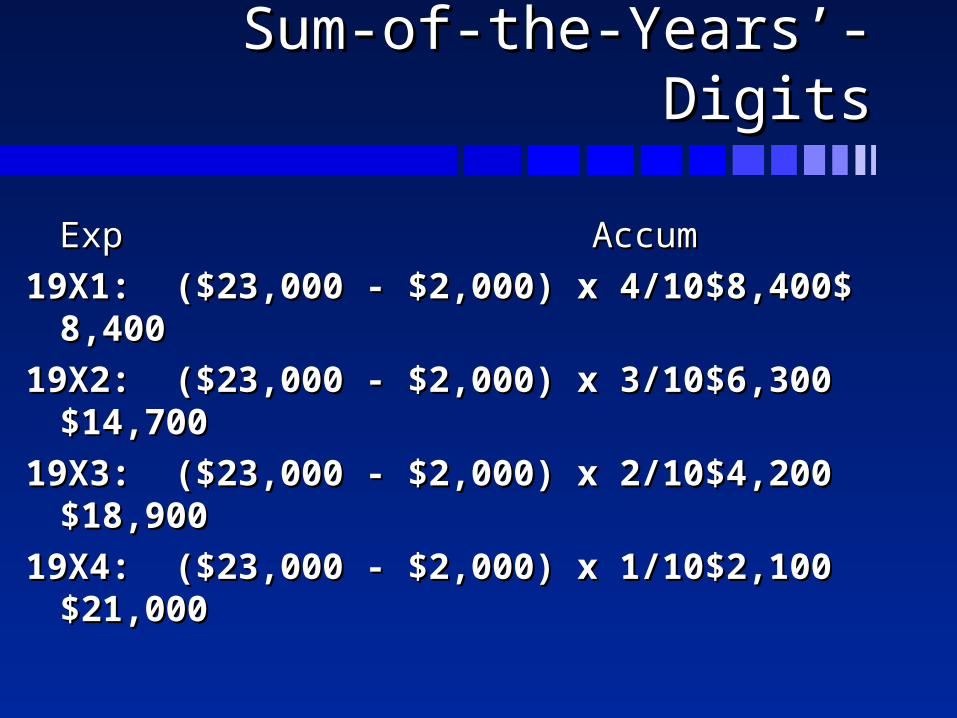

Sum-of-the-Years’-DigitsSum-of-the-Years’-Digits

Exp Exp Accum Accum

19X1: ($23,000 - $2,000) x 4/1019X1: ($23,000 - $2,000) x 4/10 $8,400$8,400 $ 8,400$ 8,400

19X2: ($23,000 - $2,000) x 3/1019X2: ($23,000 - $2,000) x 3/10 $6,300$6,300 $14,700$14,700

19X3: ($23,000 - $2,000) x 2/1019X3: ($23,000 - $2,000) x 2/10 $4,200$4,200 $18,900$18,900

19X4: ($23,000 - $2,000) x 1/1019X4: ($23,000 - $2,000) x 1/10 $2,100$2,100 $21,000$21,000

Pattern of depreciation expensePattern of depreciation expense

Straight-lineStraight-line

– Amount is constant and equalAmount is constant and equal ProductionProduction

– Amount varies depending on usageAmount varies depending on usage

Pattern of depreciation expensePattern of depreciation expense

Double decliningDouble declining

– Amount is decreasing by decreasing Amount is decreasing by decreasing amountsamounts

Sum-of-the-Year’s-DigitsSum-of-the-Year’s-Digits

– Amount is decreasing by constant Amount is decreasing by constant amountamount

Comparison of DepreciationComparison of Depreciation

Straight-lineStraight-line

ProductionProduction

0

1000

2000

3000

4000

5000

6000

1 2 3 4

0

1000

2000

3000

4000

5000

6000

7000

1 2 3 4 5 6

Comparison of DepreciationComparison of Depreciation

Double-declining Double-declining balancebalance

Sum-of-the-Years’ Sum-of-the-Years’ DigitsDigits

02000

400060008000

1000012000

1 2 3 4

0

2000

4000

6000

8000

10000

1 2 3 4

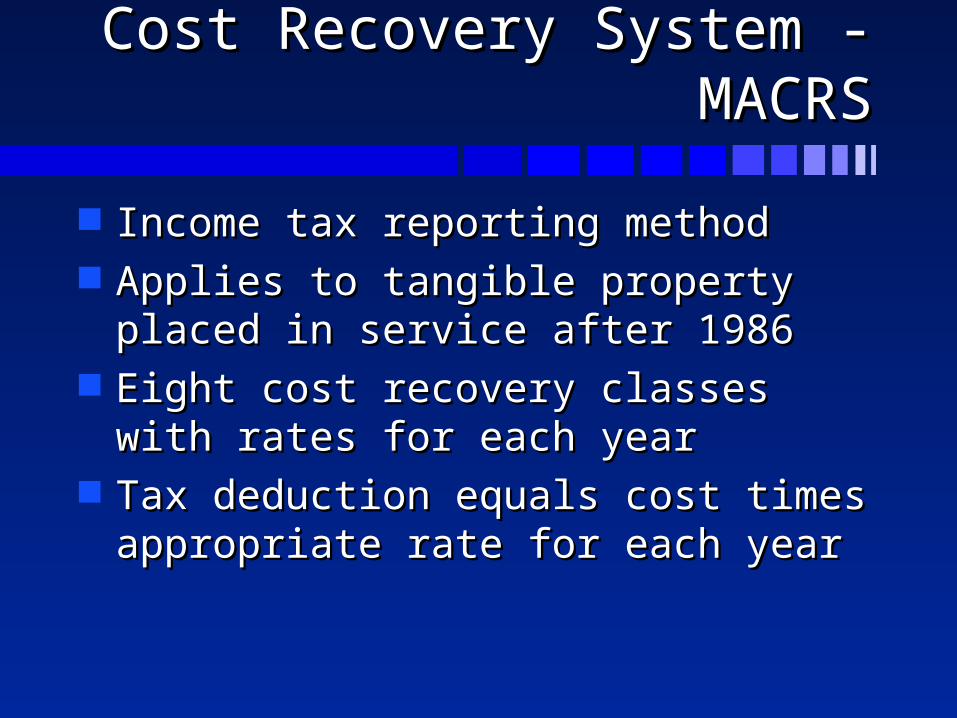

Modified Accelerated Cost Modified Accelerated Cost Recovery System - MACRSRecovery System - MACRS

Income tax reporting methodIncome tax reporting method Applies to tangible property placed in Applies to tangible property placed in

service after 1986service after 1986 Eight cost recovery classes with rates Eight cost recovery classes with rates

for each yearfor each year Tax deduction equals cost times Tax deduction equals cost times

appropriate rate for each yearappropriate rate for each year

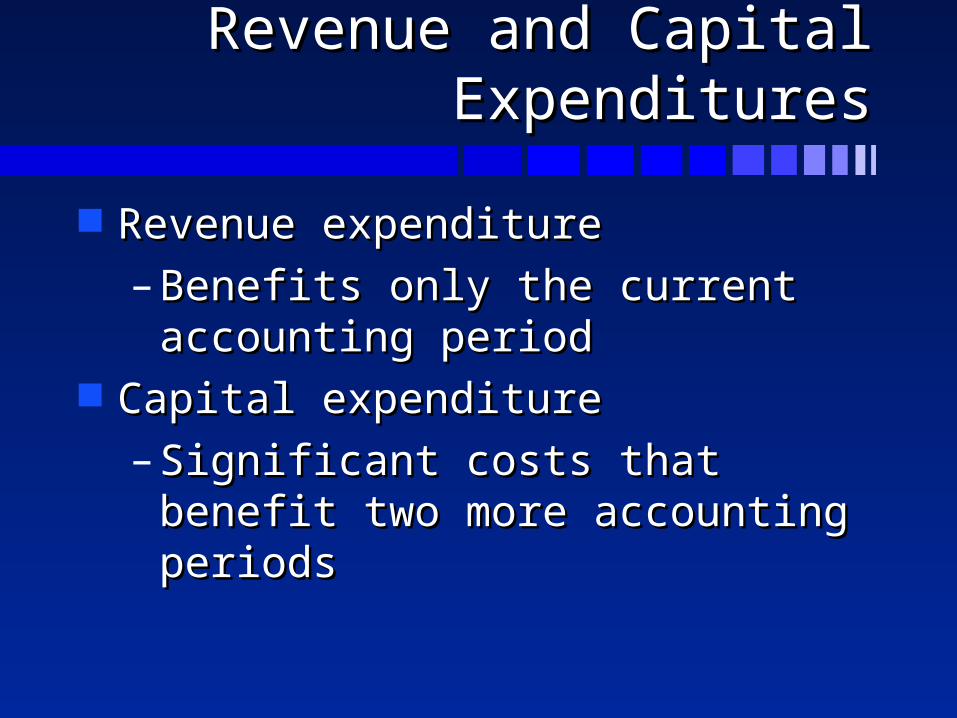

Revenue and Capital Revenue and Capital ExpendituresExpenditures

Revenue expenditureRevenue expenditure

– Benefits only the current accounting Benefits only the current accounting periodperiod

Capital expenditureCapital expenditure

– Significant costs that benefit two more Significant costs that benefit two more accounting periodsaccounting periods

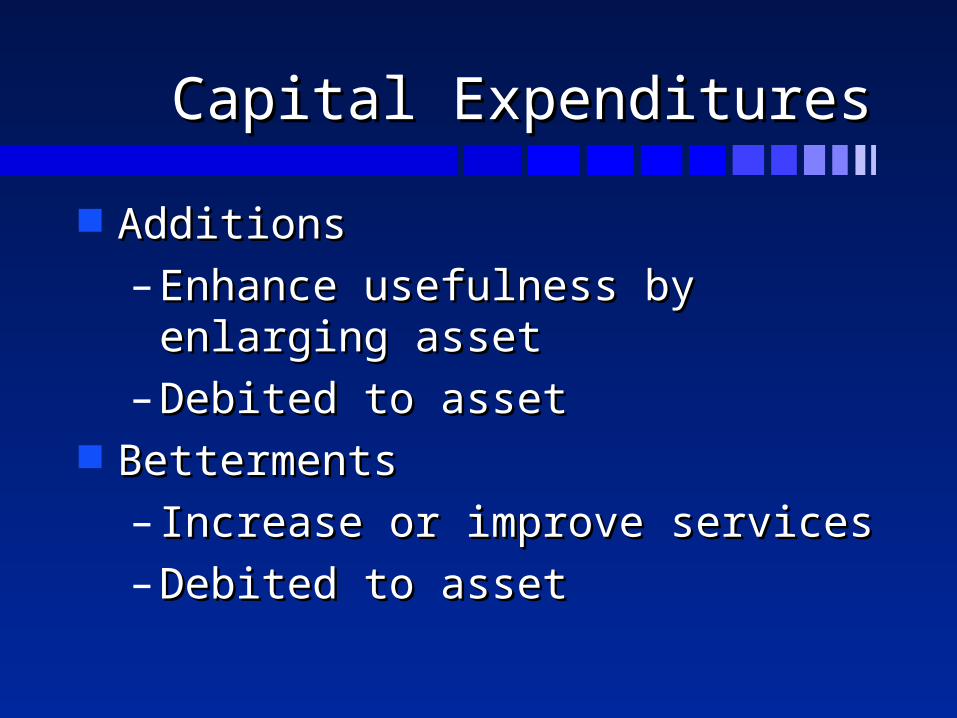

Capital ExpendituresCapital Expenditures

AdditionsAdditions

– Enhance usefulness by enlarging Enhance usefulness by enlarging assetasset

– Debited to assetDebited to asset BettermentsBetterments

– Increase or improve servicesIncrease or improve services

– Debited to assetDebited to asset

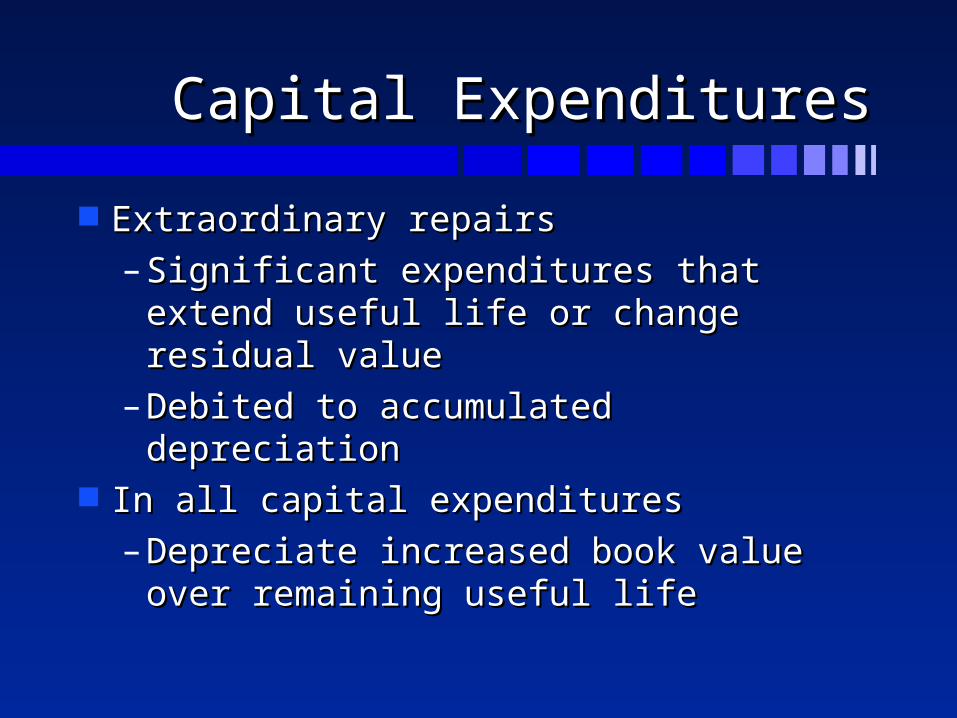

Capital ExpendituresCapital Expenditures

Extraordinary repairsExtraordinary repairs

– Significant expenditures that extend Significant expenditures that extend useful life or change residual valueuseful life or change residual value

– Debited to accumulated depreciationDebited to accumulated depreciation In all capital expendituresIn all capital expenditures

– Depreciate increased book value over Depreciate increased book value over remaining useful liferemaining useful life

Disposal of Plant AssetsDisposal of Plant Assets

SaleSale RetirementRetirement ExchangeExchange

Accounting for DisposalAccounting for Disposal

Remove asset cost and related Remove asset cost and related accumulated depreciation from the recordsaccumulated depreciation from the records

Book value is cost - accum deprecBook value is cost - accum deprec Determine gain or loss on disposalDetermine gain or loss on disposal GainGain

– Received more than book valueReceived more than book value LossLoss

– Received less than book valueReceived less than book value

Sales or RetirementsSales or Retirements

Always recognize any gain or lossAlways recognize any gain or loss

ExchangesExchanges

Always recognize lossAlways recognize loss Recognize gain only if exchange of Recognize gain only if exchange of

dissimilar assetsdissimilar assets If gain on exchange of similar assetsIf gain on exchange of similar assets

– Reduce cost of new asset by gainReduce cost of new asset by gain

Natural ResourcesNatural Resources

Mineral deposits, oil reserves, timber Mineral deposits, oil reserves, timber tractstracts

Consumption has a costConsumption has a cost

– Recognize depletion by production Recognize depletion by production methodmethod

Intangible AssetsIntangible Assets

Long-term rights that have future valueLong-term rights that have future value Patents, R&D, GoodwillPatents, R&D, Goodwill Consumption has a costConsumption has a cost

– Recognize amortization by straight-Recognize amortization by straight-line methodline method

Analyzing InformationAnalyzing Information

Are methods, asset lives, and residual values Are methods, asset lives, and residual values used reasonable?used reasonable?

If methods, lives, or residual values are If methods, lives, or residual values are changed during year, what is impact on net changed during year, what is impact on net income?income?

If some interest cost was capitalized, what is If some interest cost was capitalized, what is total interest cost for period?total interest cost for period?

– How would this change ratio “Times How would this change ratio “Times Interest Earned”?Interest Earned”?

Times Interest EarnedTimes Interest Earned

Net income + Income Tax Expense + Net income + Income Tax Expense + Total Interest CostTotal Interest Cost

divided bydivided by Total Interest CostTotal Interest Cost