lonmin presentation

TRANSCRIPT

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 1/18

Lonmin Plc

Ian Farmer CEO1 March 2011

BMO GLOBAL METALS & MINING CONFERENCE

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 2/18

2

The Platinum Investment Case

2Medium to long term investment case remains compelling

Platinum demand has grown by 3% per annum on average since 1990

3.5

4.5

5.5

6.5

7.5

8.5

9.5

90 95 00 05 10 15

Millionou

nces

0200

400

600

800

1000

1200

1400

1600

1800

2000

US$/o

z

Demand Off-Road Diesel An Avg Price (right)

US recession

Source: Historical - JM, Forecast - Lonmin

"Credit

Crunch"

3.1% per year

average growth(180 koz pa)

Jewellery contracts

due to high price

Forecast

2011

Y-t-D

Avg

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 3/18

3

Automotive Demand

China, pent-up demand and access to credit supporting unit sales 3

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

Quarterly vehicle sales*

and platinum supply(rhs '000 oz; lhs '000 units)

Vehicle Sales

Pt Supply

Source: SFA (Oxford) from Oxford Economics, ACEA, JAMA, Ward's Auto, CAAM, Bloomberg* Include all vehicle sales in W.Europe, Japan, China and light vehicle sales in the United States

10 quarter downturn

12 quarter downturn

5 quarterdownturn

Scrappageschemes

Recovery & emergingmarket growth

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 4/18

Platinum Demand in HDD and Off-road

Legislative requirements in Heavy Duty diesel engines and off-roaddiesel remains on track 4

523

484286

369

507618

677 668 68440

188

290

443 456 472

0

200

400

600

800

1,000

1,200

1,400

2007 2008 2009 2010 2011 2012 2013 2014 2015

Heavy Commercial Vehicles Off-road engines

Pt demand in on-road heavy commercial vehicles and off-road engines, koz

+870 koz

Source: SFA

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 5/18

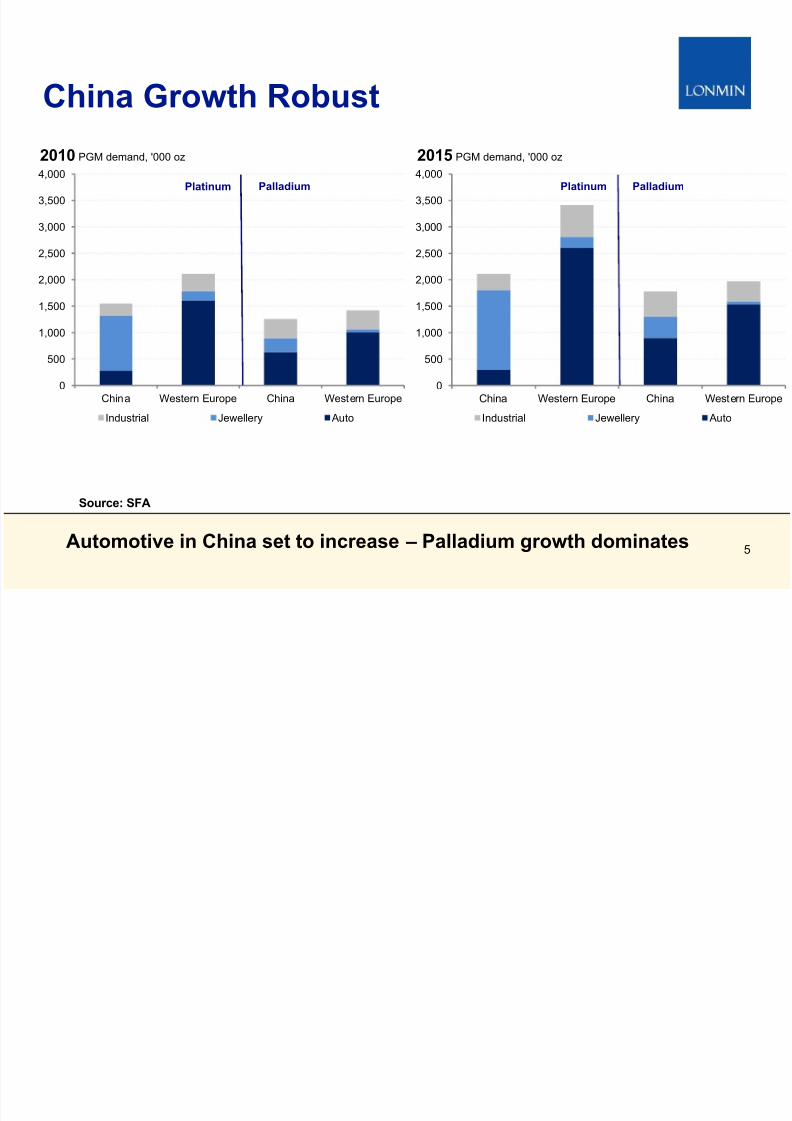

China Growth Robust

5Automotive in China set to increase – Palladium growth dominates

Source: SFA

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

China Western Europe China Western Europe

2010 PGM demand, '000 oz

Industrial Jewellery Auto

Platinum Palladium

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

China Western Europe China Western Europe

2015 PGM demand, '000 oz

Industrial Jewellery Auto

Platinum Palladium

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 6/18

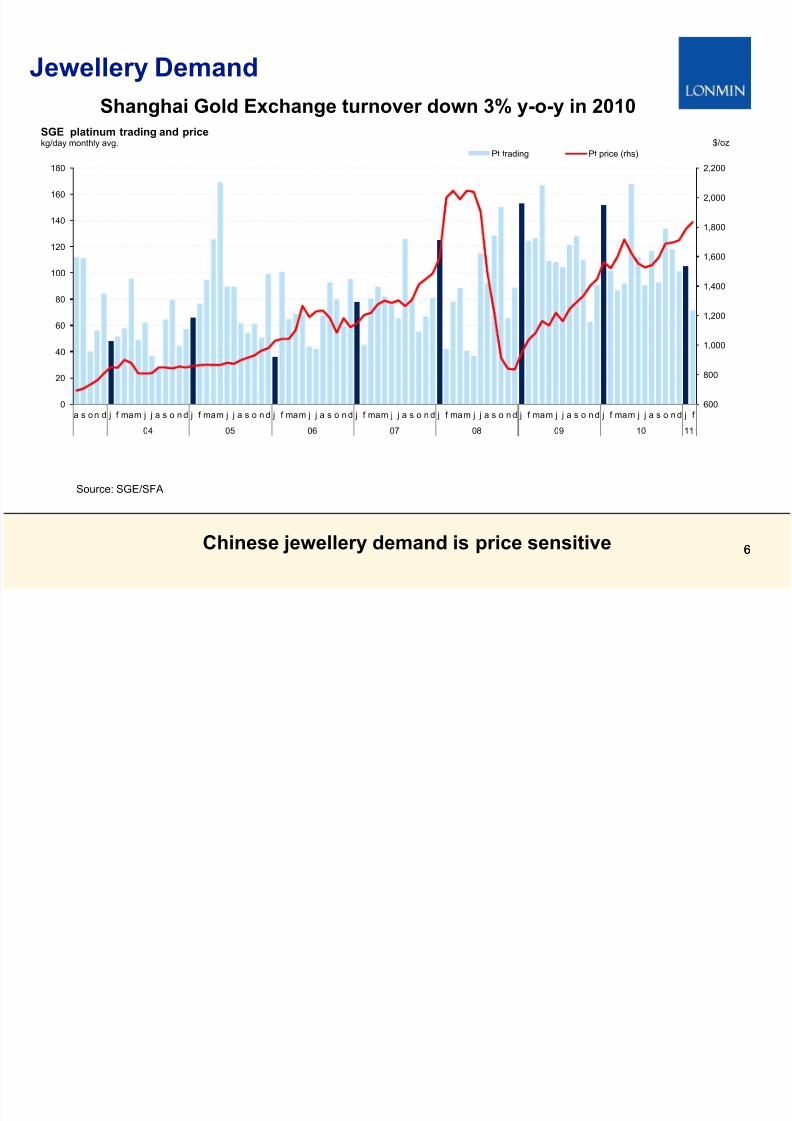

66Chinese jewellery demand is price sensitive

Jewellery Demand

Source: SGE/SFA

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

0

20

40

60

80

100

120

140

160

180

a s o n d j f mam j j a s o n d j f mam j j a s o n d j f mam j j a s o n d j f mam j j a s o n d j f mam j j a s o n d j f mam j j a s o n d j f mam j j a s o n d j f

04 05 06 07 08 09 10 11

SGE platinum trading and pricekg/day monthly avg.

Pt trading Pt price (rhs)

$/oz

Shanghai Gold Exchange turnover down 3% y-o-y in 2010

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 7/18

Impact of Auto Trends on PGM Demand

Extra >15 million passenger cars p.a. forecast by 2020 outweighsnegative impacts on PGMs from powertrain developments 7

Unit SalesVolumes

EngineSize

PGM demand trend

Drive-train &Diesel vs Gas

EmissionLegislation

Substitution& thrifting

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 8/18

8

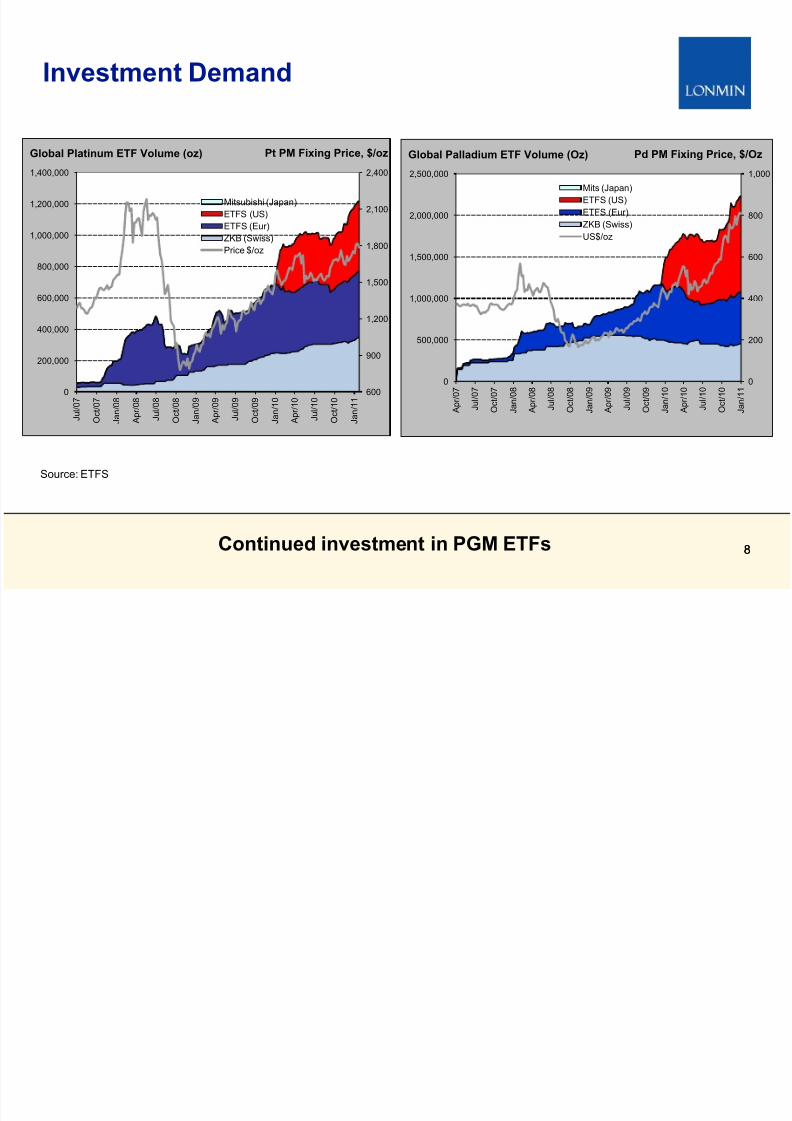

Investment Demand

8

Source: ETFS

Continued investment in PGM ETFs

600

900

1,200

1,500

1,800

2,100

2,400

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

J u

l / 0 7

O c

t / 0 7

J a n / 0 8

A p

r / 0 8

J u

l / 0 8

O c

t / 0 8

J a n / 0 9

A p

r / 0 9

J u

l / 0 9

O c

t / 0 9

J a n / 1 0

A p

r / 1 0

J u

l / 1 0

O c

t / 1 0

J a n / 1 1

Mitsubishi (Japan)

ETFS (US)

ETFS (Eur)

ZKB (Swiss)

Price $/oz

Global Platinum ETF Volume (oz) Pt PM Fixing Price, $/oz

0

200

400

600

800

1,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

A p r / 0 7

J u l / 0 7

O c t / 0 7

J a n / 0 8

A p r / 0 8

J u l / 0 8

O c t / 0 8

J a n / 0 9

A p r / 0 9

J u l / 0 9

O c t / 0 9

J a n / 1 0

A p r / 1 0

J u l / 1 0

O c t / 1 0

J a n / 1 1

Mits (Japan)

ETFS (US)

ETFS (Eur)

ZKB (Swiss)

US$/oz

Global Palladium ETF Volume (Oz) Pd PM Fixing Price, $/Oz

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 9/18

9

Platinum Supply Constraints and InducementPricing

Source: Lonmin

Incentive price between $1,850 and $2,000/Pt oz. Supply side

response expected to be muted while risks remain

0

500

1,000

1,500

2,000

2,500

3,000

4.0 5.0 6.0 7.0 8.0 9.0 10.0 11.0 12.0 13.0

W e i g h t e d a v e r a g e p l a t i n u m p r i c e ( $ / o z )

ZAR:$

Project incentive pricing (real, 2010)

December 2010

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 10/18

1010

Lonmin

View

Opportunities

•

Industrial and auto demand recovery from 2011• Small deficit in 2011

• Supply incapable of keeping up – growing deficits

__ in 2012 – 2014 period

• Stronger demand upswing

• Supply surprising on the downside

• Even tighter market & even higher prices

PGM Market Outlook

Risks

• Euro zone deteriorates

• China slowdown

• Substitution

Overall positive medium and long term market fundamentals

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 11/18

11

Lonmin’s Safety Record

11

Source: Department of Mineral Resources

Lonmin

AngloplatsPt industry

Impala

Comparison of Platinum Industry – Fatality Rate

12 Month Rolling

Aquarius

Committed to safety improvement

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

J a n - 0 5

M a y - 0 5 S e

p - 0 5 J a n - 0 6

M a y - 0 6 S e

p - 0 6 J a n - 0 7

M a y - 0 7 S e

p - 0 7 J a n - 0 8

M a y - 0 8 S e

p - 0 8 J a n - 0 9

M a y - 0 9 S e

p - 0 9 J a n - 1 0

M a y - 1 0 S e

p - 1 0

Permillion

hours

Impala Angloplats Lonmin Aquarius Pt Indus try

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 12/18

1212

• Continued progress in mining with tonnes mined and milled increasing

• Underground milled head grade down 0.19g/t from 4.74g/t in prior period to

4.55g/t

• Impacted by mix change and poor ground conditions

• Remains within our grade banding and down 0.08g/t from 2010Q4 - closely monitored by management

• Positive trend in underground concentrator recoveries maintained - from

84.5% in prior period to 85.1%

• Platinum sales in Q1 down 39.1% to 66,426 Platinum oz

• Impacted by unexpected adverse weather conditions in the northern hemisphere and Number One

furnace rebuild

• Number One furnace ramping up successfully following its scheduled rebuild

and modification

Q1 2011 – Operational Performance Update

A solid start to the year

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 13/18

-

400

800

1,200

1,600

2,000

2,400

2,800

3,200

Q109 Q110 Q111 Q209 Q210 Q309 Q310 Q409 Q410

T o n n e s

H o i s t e

d

( ' 0 0 0 s )

Westerns Middelkraal Easterns Karee

13

Marikana MiningUnderground production overview

13An encouraging trend

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 14/18

14

SA Industry Challenges

Operational

• Cost pressures

• Labour - wage agreements well aboveCPI

• Power - high tariff increases

• Resource constraints

• Lack of security over supply of powerand water may impact on new projects

• Shortage of experienced people

• Rand strength

• Has eroded margins and free cash flow

Regulatory

• Nationalisation

• An issue of national debate

• Security of tenure of mining rights• Associated minerals largely resolved

• Keysha issue outstanding

• Revised Mining Charter

• Collaborative approach by the DMR andindustry participants

• Increasing evidence of spot visits by mineinspectors

South Africa’s government acknowledges the need for a competitive

mining industry

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 15/18

15

2011 Focus and Guidance

Key deliverables for 2011

• Platinum sales of around 750,000 safe ounces

• Unit cost percentage increase of less than wage settlement

• Capital expenditure of up to $380 million, mostly Rand based

Key focus areas for 2011

• Continue to improve on safety to achieve zero harm

• Accelerate transformation and sustainability delivery

• Invest in further growth in our Marikana asset

•Focus on improving daily productivity

• Consider options beyond 2013 delivery of 850,000 Platinum ounces atMarikana

Building on a healthy operational platform

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 16/18

1616

• Delivering on the target of 850,000 safe Platinum ounces by 2013

• Considering options beyond this including Akanani and Limpopo

• Driving productivity through efficiencies and strict cost control

• Enabling growth and an improved competitive position

• Achieving our BEE ownership and transformation targets

Medium to Long Term Value Creation ReviewOutlook beyond 2011

Delivering growth into a market with robust fundamentals

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 17/18

Lonmin Plc

Questions

8/12/2019 lonmin Presentation

http://slidepdf.com/reader/full/lonmin-presentation 18/18

18

Disclaimer

This presentation, which is personal to the recipient, has been issued by Lonmin. This presentation includes forward-looking statements. All statements other than statements ofhistorical fact included in this announcement, including without limitation those regarding Lonmin's plans, objectives and expected performance, are forward-looking statements.Lonmin has based these forward-looking statements on its current expectations and projections about future events, including numerous assumptions regarding its present and futurebusiness strategies, operations, and the environment in which it will operate in the future. Forward-looking statements generally can be identified by the use of forward-lookingterminology such as 'ambition', 'may', 'will', 'could', 'would', 'expect', 'intend', 'estimate', 'anticipate', 'believe', 'plan', 'seek' or 'continue', or negative forms or variations of similarterminology. Such forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors related to Lonmin, including, among other factors: (1)material adverse changes in economic conditions generally or in relevant markets or industries in particular; (2) fluctuations in demand and pricing in the mineral resource industryand fluctuations in exchange rates; (3) future regulatory and legislative actions and conditions affecting Lonmin's operating areas; (4) obtaining and retaining skilled workers and keyexecutives; and (5) acts of war and terrorism. By their nature, forward-looking statements involve risks, uncertainties and assumptions and many relate to factors which are beyondLonmin‘ control, such as future market conditions and the behaviour of other market participants. Actual results may differ materially from those expressed in forward-lookingstatements. Given these risks, uncertainties, and assumptions, you are cautioned not to put undue reliance on any forward-looking statements. In addition, the inclusion of suchforward-looking statements should under no circumstances be regarded as a representation by Lonmin that Lonmin will achieve any results set out in such statements or that theunderlying assumptions used will in fact be the case. Other than as required by applicable law or the applicable rules of any exchange on which Lonmin's securities may be listed,Lonmin has no intention or obligation to update or revise any forward-looking statements included in this presentation after the publication of this presentation. This presentation is forinformation only and does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase, any shares in Lonmin or any other securities, nor shallit or any part of it nor the fact of its distribution form the basis of, or be relied upon in connection with, any contract or investment decision related thereto. Information supplied by host

presenters may not be used, referenced or published without the prior written consent of the author of the presentations.

18