(lon:ptro) pelatro plc 27 july 2020 pelatro: big data, big

TRANSCRIPT

PELATRO PLC(LON:PTRO)

27 July 2020

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 1

Software & Services

52-WEEK HIGH 79.00p

52-WEEK LOW 25.25p

PRICE 57.00p

MARKET CAP MLN £18.54

Share Price

Major Shareholders

Bannix Management LLP - 39.9%Chelverton Asset Management - 6.6%Rathbones IM - 5.0%Shares in issue 32,532,431Avg Three-month tradingvolume

96,868

Primary IndexNext Key Announcement August 2020

Company Information

Address: 49 Queen Victoria St., London EC4N4SA

Website: /www.pelatro.com

Analyst Details

Pelatro: Big Data, big growth drivers

Revenue enhancing software for the telecom industry

Pelatro PLC (LON:PTRO) is a software provider focussed on the telecomsector, offering telecom operators solutions for increasing revenue persubscriber, retaining subscribers, and monetising data.

The customer base includes major global telecom operators, with the biggestgeographies being Southeast Asia and South Asia. The company has achieveda compounded annual growth rate (CAGR) in revenue of 78% since 2016 withconsistent profitability (2019 EBITDA margin 43%).

The growing need for Pelatro’s software-based solutions is driven by thematuration of the global telecom industry. Telecom operators can no longerrely on growth in the subscriber base and need to focus instead on averagerevenue per user (ARPU) and customer retention. Pelatro’s suite of solutionsaddresses these needs.

Competitive position:

Pelatro has a customer base of 19 major telecom operators. This hasgrown every year since inception in 2015 and now covers about one billionunderlying mobile phone users. The company has won business away from thebig software companies as well as from other telecom specialists. Some ofPelatro’s competitive advantages include:

• Big Data enabled solutions that can handle data from billions ofcustomer transactions to tailor and target offers from the telco(telecommunications company) to the customer at an individual level in acontextual, relevant, personalised and real-time manner

• Domain expertise and specialisation in the telecom space• A strong customer service capability

We expect growth in the customer base to continue in 2020, and the companyhas reported that the COVID crisis is not leading to customers cancelling theirinvestment plans. We examine the business drivers in this report.

Financials and valuation

Pelatro has begun the transition of its business towards a multi-year subscriptionmodel, and this is a very important aspect of the investment thesis. Thissubscription model offers Pelatro increased value per contract, increasedrevenue visibility and a deeper level of customer engagement. Among thefinancial benefits, the company has an objective, within the next two years, toensure that the recurring revenue run-rate at the start of each year is equal to orhigher than the cost base for that full year.

In profit & loss terms in the short-term, the business model transition createsa lag in revenue recognition, as there is less upfront licence fee income beingbooked. We expect to see a significant re-acceleration in reported revenuegrowth starting in 2021.

We argue that what looks at first glance like a slowdown in revenue growth hashit the Pelatro share price. We examine this valuation discount in this report, andwe argue that this represents an opportunity for investors.

Year end Dec 31 Current 2019 2020 2021

Revenue (US$M) 6.1 6.7 7.3 9.1EBITDA (US$M) 3.8 2.9 3.0 4.3Net Cash 1.8 0.5 1.4 2.1

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 2

Subash Menon – chief executive officer (CEO)

Menon co-founded Pelatro in April 2013. Priorto Pelatro, he was the CEO and founder ofSubex – a company he transformed into aglobal leader in telecoms software for businessoptimisation. He guided Subex through asuccessful flotation in 1999 and through sevenacquisitions in the UK, US, and Canada

Nicholos Hellyer – finance director

Hellyer is a chartered accountant and formerinvestment banker with more than 25 years ofexperience primarily at UBS and HSBC. He hasalso spent time in industry as chief financialofficer of Buddi Limited and as a partner atOpus Corporate Finance

Investment summary

Pelatro is a specialist in the telecom marketing space, providing enterprise-classcustomer engagement software solutions to help telecom operators increaserevenue and reduce churn.

As the telecom service industry has become mature, telcos can no longer rely onmarket growth to drive revenue and profit growth. Instead, they become morefocussed on:

• Increasing average revenue per user• Customer retention• Increasing share of wallet.

Pelatro offers a suite of solutions called mViva, which consists of fourcomponents, summarised in the following table:

The Pelatro Product offering

Source: Proactive Research

Enabling telcos to target offers at anindividual level

mViva Contextual Marketing Solution (CMS)

The CMS allows telcos to target offers to a customer using a detailed individualcustomer profile based on analysis of that individual’s transactions. The CMSincludes cutting edge AI/ML (artificial intelligence / machine learning) features inthe form of descriptive, predictive and prescriptive analytics and provides end-to-end capability of segmentation, campaign design, configuration, execution,fulfilment, provisioning, reporting and analytics.

mViva Data Monetisation Platform (DMP)

The DMP organises customer data into an individual profile detailing thebehaviour and demography of each customer. This allows telcos to monetisethis asset through targeted third-party advertisements, while remaining withinrelevant data protection laws, for consenting subscribers. For enterprises thatpartner with telcos, this allows them to get better value for money from theiradvertising. The DMP offers a complete solution with partner management,portal, offer design, execution and reporting.

mViva Loyalty Management Solution (LMS)

The LMS is a tool for customer retention. It rewards each customer with pointsbased on various activities such as revenue generation, early bill payment,referral etc. and these points can then be exchanged for various rewards.

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 3

It is a comprehensive solution that provides for points earning, redemption,segmentation, tiering, campaigning, fulfilment, provisioning and reporting.

mViva Unified Communication Manager

The telco customer may be targeted with numerous different types of messages,such as emergency messages, informational messages, offers for third partyproducts etc. The telco must, therefore, employ a policy governing the number ofsuch messages together with priority for each type of message. The mViva UCMensures that telcos have centralised control of their messaging policy and privacysettings of customers.

The four software solutions are integrated with various elements of the telecomprovider’s network to allow them to gather information on every transaction thateach end customer generates.

Pelatro’s customer base:

Pelatro has achieved strong growth in its customer base since signing its firstcustomer in 2015, and now serves 19 major telcos globally. This encompassessome 850 million underlying individual subscribers, with its strongest positionsin Southeast Asia and South Asia. The following map shows the current customerbase.

19 customers across a range ofgeographies

Pelatro customer base

Source: Pelatro

Pelatro is differentiated from some of its larger rivals (details p6) because it hasalways had a pure focus on the telco customer base. It, therefore, offers deepdomain expertise and a product which is built around the demands of Big Datain order to handle the billions of customer data points generated by telecomoperators.

The company has achieved market share gains in each year 2015-2019.

The financial outlook and valuation

Pelatro has achieved a revenue CAGR of 78% since 2016, and delivers strongprofitability with an earnings before interest, tax, depreciation and amortisation(EBITDA) margin of 43% (2019 actual).

The subscription model is a key part of theinvestment thesis

As Pelatro has established significant market positions across its initial targetregions, the company has made a strategic decision to shift its business modelfrom a one-off licence model to a subscription model. This is a crucial factor inunderstanding the financial model and the valuation case.

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 4

Under the subscription model, Pelatro offers a multi-year contract encompassingsoftware provision and support services. Under the licence model it was a one-off software licence fee followed by separate payments for services.

The subscription model offers:

• A higher net present value per contract for Pelatro• Greater visibility over revenue and earnings• A deeper level of engagement with the customer, cementing the relationship

and allowing Pelatro to offer additional solutions as the Pelatro productoffering expands

The subscription model does, however, mean that some revenue recognition isdeferred. This led to slower revenue growth in 2019, at 9% versus 95% reportedin 2018.

We examine the financial implications of the change in business model on page7-8. We conclude that the subscription model enables greater value creation forPelatro, albeit at the expense of deferral in revenue recognition.

Valuation multiple does not reflectPelatro's ongoing growth trajectory

The shares are now trading on an enterprise value (EV)/EBITDA ratio of 5.7x. Incomparison with the wider speciality software space; we argue that this is a lowvaluation multiple particularly in light of Pelatro’s prospective EBITDA growthin 2021 and onwards. We believe that during the next six-24 months the marketwill have an opportunity to better understand the business model transitionand to see proof of the financial benefit to Pelatro. We argue that this couldpotentially trigger a re-rating in terms of the valuation.

Mobile telephony is now a mature marketThe market need

The mobile telephone industry is now a mature market globally. This meansthat telcos can no longer rely on growth in subscriber numbers to drive revenuegrowth. Furthermore, in a commoditised market for mobile phone services,providers contend with aggressive competition for their existing customers.

The following diagram illustrates the approaching saturation of the mobile phonemarket.

Mobile phone users globally

Source: Proactive Research, composite of market sources

In this environment, the telecom operators must focus on:

• Retention of existing customers• Maximising the revenue from their existing customer base• Seeking additional ways to monetise their position, such as third party

advertising

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 5

These imperatives play exactly to the strengths of Pelatro’s mViva suite ofproducts.

In terms of the specific geographic markets addressed by Pelatro, the biggestgeographies are South Asia and Southeast Asia. The following chart showsPelatro’s customer geographic profile for 2019:

A high degree of emerging marketexposure

Pelatro customer base, FY 2019

Source: Pelatro data

Although Pelatro’s customer base has a more emerging market focussed endsubscriber base they are experiencing the same issues as European or NorthAmerican telecom operators in terms of markets maturing and customer baseapproaching saturation. They do, however, have more headroom in terms ofrevenue per customer.

Monthly revenue per mobile user

Source: Proactive Research, composite of market sources

A suite of products fulfilling an essentialneed in any geographic market

We argue that the mViva suite of solutions offers essential utility for telecomoperators across any geographic region or customer demographic. Pelatro addedadditional sales resource for the Latin America and Caribbean region during 2019and added to its Asian sales force. We expect the company to continue growingboth within its existing geographies and by adding additional geographies.

The company increased its underlying subscriber base (the customers of Pelatro’scustomers) to about 1 billion in 2020 from 325mln at the end of 2018. We expect

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 6

Pelatro’s growth to continue in the coming years, and we expect this to come frommarket share gain as more telecom operators switch to the mViva solutions.

Telecom companies continue to become more focussed on maximising valuecapture from their existing customer base, and mViva has now proven itself to bea valuable tool in facilitating this value capture.

Pelatro market position

The space that Pelatro plays into is populated by specialist software providersfocussed on the telecom market as well as the big software generalists. Thefollowing diagram shows some examples of competitors.

Pelatro and the competitor base - illustrative positioning, not to

scale

Source: Proactive Research

Pelatro has been winning market sharefrom the big software generalists and alsothe telco specialists

In recent years Pelatro has won customers from the big generalists as well as fromsome of its specialist peers.

These market share gains are driven by the value-added capabilities that themViva suite of products offers to the telco customer. These have been shown togenerate up to 5% incremental revenue for the customer while reducing churn.

We highlight three differentiating features of Pelatro’s customer offering:

Big Data is a fundamental characteristic ofthe telecom industry

Telecom-specific products – Big Data enabled

Pelatro has only ever focussed on the telecom customer base. As a result thecompany has produced a suite of products that are specifically evolved to meetthe needs of telecom operators. In particular, the mViva solutions employ astateless computer architecture that is inherently suited to handling Big Data.

Pelatro’s biggest customer has 350+ million subscribers. A customer base ofthis size generates tens of billions of transactions per day. The systems thatPelatro offers can handle and analyse this volume of data and enable marketingcampaigns to be targeted at various levels of granularity right down to a singleuser.

Flexible solutions that can be tailored to the customers’ need

The mViva suite is built on a modular platform, meaning that once a customer hashad the system installed it is easy to add further modules to meet the customer’sevolving requirements.

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 7

Furthermore, the analytical system itself is designed to provide the customerwith a flexible tool for designing and implementing new campaigns. Users mayconfigure complex flows with hundreds of symbols and connectors depicting atypical customer journey with branches, conditional logic, splits and regroupingincluding timers and waits for customer events in isolation or in combination.

Customer Service

Based on its deep domain expertise in the telecom space, Pelatro understandsthe complex needs of the customer base and the importance of a responsivecustomer service capability. The company cites the quality of its customer servicepersonnel as the biggest differentiating factor leading customers to choosePelatro over its competitors.

Market share gains have driven continual growth in Pelatro’s customer base. Thefollowing chart illustrates this in terms of the number of enterprises using mViva.

The strength of the product offeringdrives continual growth in the customerbase

Pelatro customer numbers

Source: Pelatro data

Pelatro continues to gain new customers on the strength of its product offering.We expect this to continue in the coming year and for this to be reflected inrevenue and earnings growth.

Revenues are driven by both software andthe service element

Changing revenue mix

Pelatro’s offering to the customer comprises the provision of software togetherwith a service element. The services provided can be broken down as follows:

Implementation and support services. These encompass the installation ofthe software within the customer’s network, and technical support servicesthereafter.

Managed services. These go beyond product support and include campaigndesign and implementation and 24/7 information technology (IT) support, as wellas business consulting. Managed services are provided by a dedicated team forthe customer offering a fully outsourced solution.

Change requests. Customer can request bespoke configurations andcustomisation that are provided for a fee.

Under the licence model, which has historically been the main type of contractfor Pelatro, software is sold under a one-off perpetual licence, with additionalservices under a separate contract.

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 8

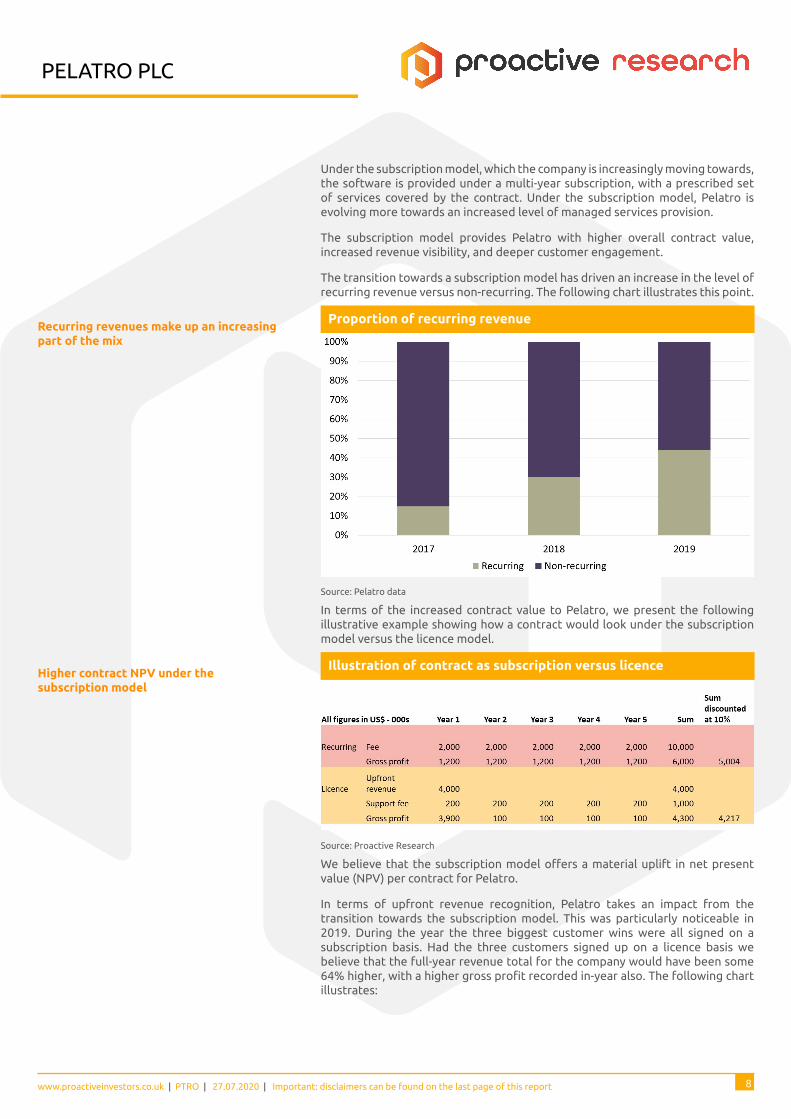

Under the subscription model, which the company is increasingly moving towards,the software is provided under a multi-year subscription, with a prescribed setof services covered by the contract. Under the subscription model, Pelatro isevolving more towards an increased level of managed services provision.

The subscription model provides Pelatro with higher overall contract value,increased revenue visibility, and deeper customer engagement.

The transition towards a subscription model has driven an increase in the level ofrecurring revenue versus non-recurring. The following chart illustrates this point.

Recurring revenues make up an increasingpart of the mix

Proportion of recurring revenue

Source: Pelatro data

In terms of the increased contract value to Pelatro, we present the followingillustrative example showing how a contract would look under the subscriptionmodel versus the licence model.

Higher contract NPV under thesubscription model

Illustration of contract as subscription versus licence

Source: Proactive Research

We believe that the subscription model offers a material uplift in net presentvalue (NPV) per contract for Pelatro.

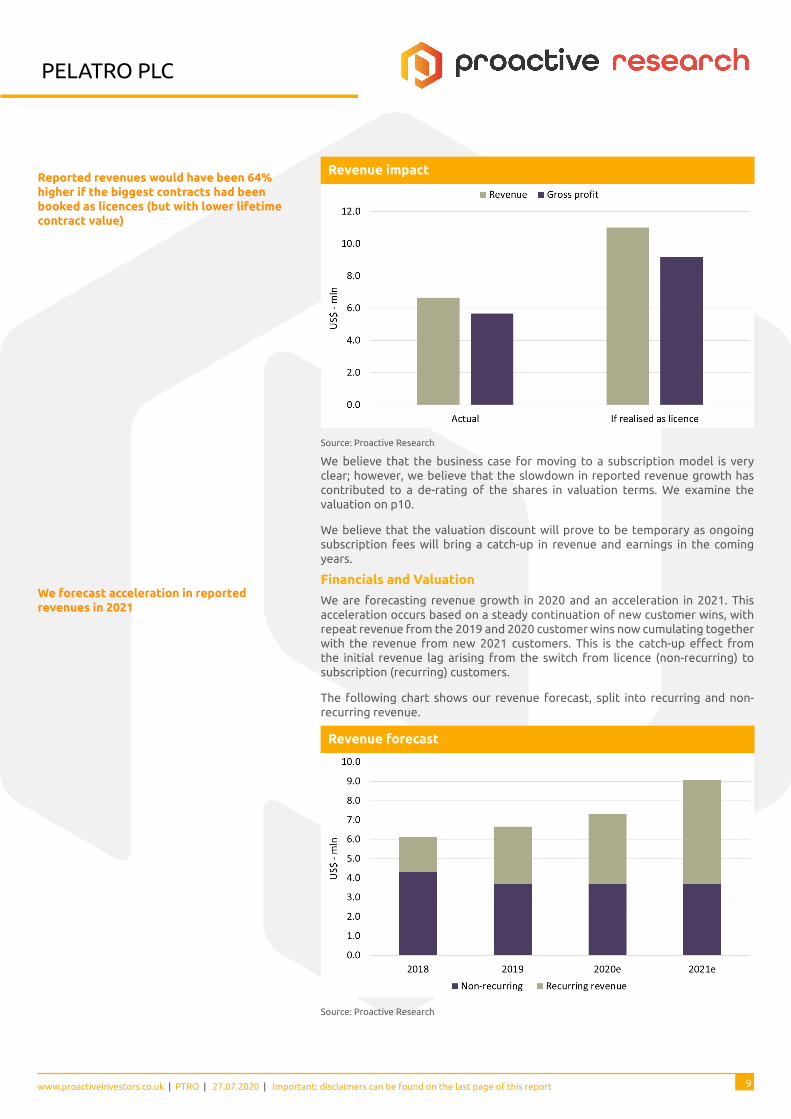

In terms of upfront revenue recognition, Pelatro takes an impact from thetransition towards the subscription model. This was particularly noticeable in2019. During the year the three biggest customer wins were all signed on asubscription basis. Had the three customers signed up on a licence basis webelieve that the full-year revenue total for the company would have been some64% higher, with a higher gross profit recorded in-year also. The following chartillustrates:

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 9

Reported revenues would have been 64%higher if the biggest contracts had beenbooked as licences (but with lower lifetimecontract value)

Revenue impact

Source: Proactive Research

We believe that the business case for moving to a subscription model is veryclear; however, we believe that the slowdown in reported revenue growth hascontributed to a de-rating of the shares in valuation terms. We examine thevaluation on p10.

We believe that the valuation discount will prove to be temporary as ongoingsubscription fees will bring a catch-up in revenue and earnings in the comingyears.

We forecast acceleration in reportedrevenues in 2021

Financials and Valuation

We are forecasting revenue growth in 2020 and an acceleration in 2021. Thisacceleration occurs based on a steady continuation of new customer wins, withrepeat revenue from the 2019 and 2020 customer wins now cumulating togetherwith the revenue from new 2021 customers. This is the catch-up effect fromthe initial revenue lag arising from the switch from licence (non-recurring) tosubscription (recurring) customers.

The following chart shows our revenue forecast, split into recurring and non-recurring revenue.

Revenue forecast

Source: Proactive Research

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 10

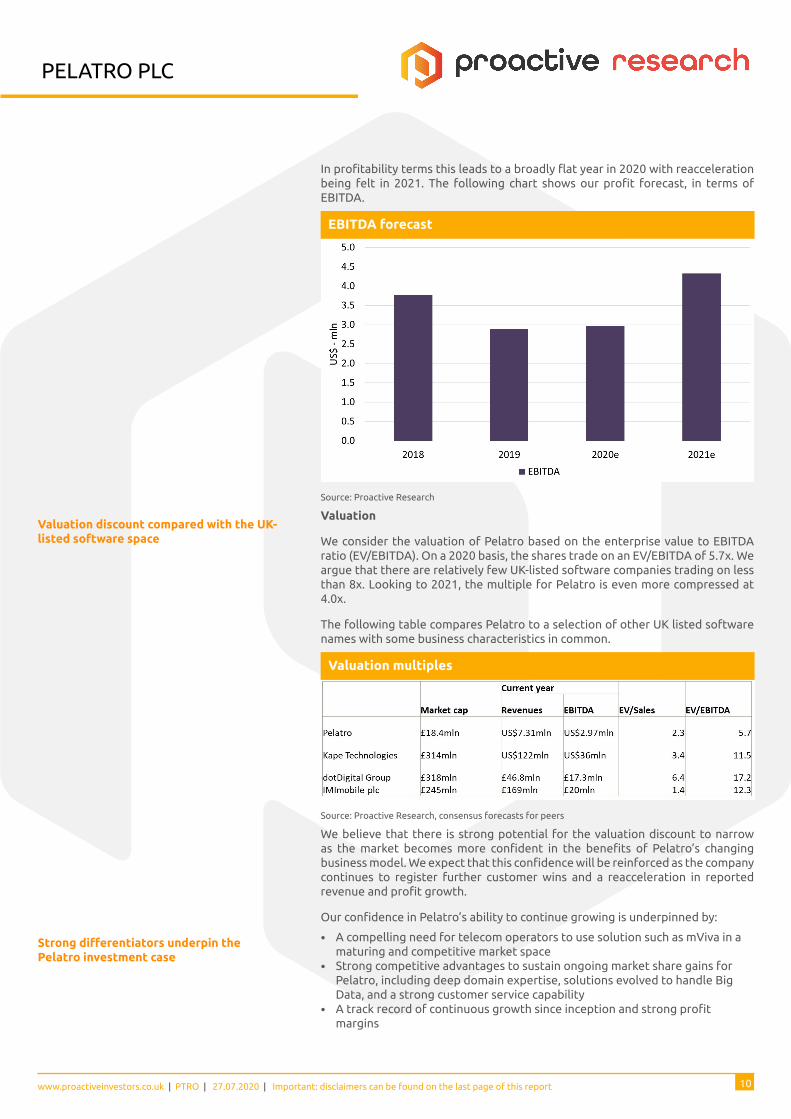

In profitability terms this leads to a broadly flat year in 2020 with reaccelerationbeing felt in 2021. The following chart shows our profit forecast, in terms ofEBITDA.

EBITDA forecast

Source: Proactive Research

Valuation discount compared with the UK-listed software space

Valuation

We consider the valuation of Pelatro based on the enterprise value to EBITDAratio (EV/EBITDA). On a 2020 basis, the shares trade on an EV/EBITDA of 5.7x. Weargue that there are relatively few UK-listed software companies trading on lessthan 8x. Looking to 2021, the multiple for Pelatro is even more compressed at4.0x.

The following table compares Pelatro to a selection of other UK listed softwarenames with some business characteristics in common.

Valuation multiples

Source: Proactive Research, consensus forecasts for peers

We believe that there is strong potential for the valuation discount to narrowas the market becomes more confident in the benefits of Pelatro’s changingbusiness model. We expect that this confidence will be reinforced as the companycontinues to register further customer wins and a reacceleration in reportedrevenue and profit growth.

Our confidence in Pelatro’s ability to continue growing is underpinned by:

Strong differentiators underpin thePelatro investment case

• A compelling need for telecom operators to use solution such as mViva in amaturing and competitive market space

• Strong competitive advantages to sustain ongoing market share gains forPelatro, including deep domain expertise, solutions evolved to handle BigData, and a strong customer service capability

• A track record of continuous growth since inception and strong profitmargins

PELATRO PLC

www.proactiveinvestors.co.uk | PTRO | 27.07.2020 | Important: disclaimers can be found on the last page of this report 11

General Disclaimer and copyrightLEGAL NOTICE – IMPORTANT – PLEASE READ

Proactive Research is a trading name of Proactive Investors Limited which is regulated and authorised by the Financial ConductAuthority (FCA) under firm registration number 559082. This document is published by Proactive Research and its contents have notbeen approved as a financial promotion by Proactive Investors Limited or any other FCA authorised person. This communication ismade on the basis of the 'journalist exemption' provide for in Article 20 of The Financial Services and Markets Act 2000 (FinancialPromotion) Order 2005 and having regard to the FCA Rules, and in particular PERG 8.12.

This communication has been commissioned and paid for by the company and prepared and issued by Proactive Research forpublication. All information used in the preparation of this communication has been compiled from publicly available sources thatwe believe to be reliable, however, we cannot, and do not, guarantee the accuracy or completeness of this communication.

The information and opinions expressed in this communication were produced by Proactive Research as at the date of writing andare subject to change without notice. This communication is intended for information purposes only and does not constitute anoffer, recommendation, solicitation, inducement or an invitation by, or on behalf of, Proactive Research to make any investmentswhatsoever. Opinions of and commentary by the authors reflect their current views, but not necessarily of other affiliates ofProactive Research or any other third party. Services and/or products mentioned in this communication may not be suitable for allrecipients and may not be available in all countries.

This communication has been prepared without taking account of the objectives, financial situation or needs of any particularinvestor. Before entering into any transaction, investors should consider the suitability of the transaction to their individualcircumstance and objectives. Any investment or other decision should only be made by an investor after a thorough reading of therelevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating tothe issue of securities or other financial instruments.

Nothing in this communication constitutes investment, legal accounting or tax advice, or a representation that any investment orstrategy is suitable or appropriate for individual circumstances or otherwise constitutes a personal recommendation for any specificinvestor. Proactive Research recommends that investors independently assess with an appropriately qualified professional adviser,the specific financial risks as well as legal, regulatory, credit, tax and accounting consequences.

Past performance is not a reliable indicator of future results. Performance forecasts are not a reliable indicator of futureperformance. The investor may not get back the amount invested or may be required to pay more.

Although the information and date in this communication are obtained from sources believed to be reliable, no representation ismade that such information is accurate or complete. Proactive Research, its affiliates and subsidiaries do not accept liability for lossarising from the use of this communication. This communication is not directed to any person in any jurisdiction where, by reason ofthat person's nationality, residence or otherwise, such communications are prohibited.

This communication may contain information obtained from third parties, including ratings from rating agencies such as Standard& Poor's, Moody's, Fitch and other similar rating agencies. Reproduction and distribution of third-party content in any form isprohibited except with the prior written consent of the related third-party. Credit ratings are statements of opinion and are notstatements of fact or recommendations to purchase, hold or sell securities. Such credit ratings do not address the market value ofsecurities or the suitability of securities for investment purposes, and should not be relied upon as investment advice.

Persons dealing with Proactive Research or members of the Proactive Investors Limited group outside the UK are not covered by therules and regulations made for the protection of investors in the UK.

Notwithstanding the foregoing, where this communication constitutes a financial promotion issued in the UK that is not exemptunder the Financial Services and Markets Act 2000 or the Orders made thereunder or the rules of the FCA, it is issued or approvedfor distribution in the UK by Proactive Investors Limited.

London

+44 207 989 0813

The Business Centre

6 Wool House

74 Back Church Lane

London E1 1AF

New York

+1 347 449 0879

767 Third Avenue

Floor 17

New York

NY 10017

Vancouver

+1 604-688-8158

Suite 965

1055 West Georgia Street

Vancouver, B.C. Canada

V6E 3P3

Sydney

+61 (0) 2 9280 0700

Suite 102

55 Mountain Street

Ultimo, NSW 2007