lpc answered part i - sample chapter (blp, litigation & conduct)

DESCRIPTION

ÂTRANSCRIPT

www.lpcanswered.com

LPC ANSWERED

SAMPLE NOTES FROM OUR PART I GUIDE

From Civil Litigation: Settlement and Part 36 Offers

From Conduct: Restrictions on Financial Promotions

From Business: Substantial Property Transactions

LPC Answered is a comprehensive set of revision notes for the Legal Practice Course. Part I covers the core modules of the LPC:

o Civil Litigation

o Criminal Litigation

o Property Law and Practice

o Business Law and Practice

o Tax

o Wills and the Administration of Estates

o Conduct

We have also written a number of individual guides to cover as many of the electives on the LPC as possible. Our Part II guides cover ten elective modules, including all of the Accelerated LPC modules. Please visit www.lpcanswered.com if you wish to purchase a copy.

This chapter is provided by way of sample only. It is provided for marketing purposes and does not

constitute legal advice. It is intended solely for prospective customers who are students or prospective students of the law of England and Wales. All information contained within is correct to

the best of the author’s knowledge.

ALL RIGHTS RESERVED. COPYRIGHT © 2014 LAW ANSWERED

www.lpcanswered.com

CIVIL LITIGATION SAMPLE

SETTLEMENT AND PART 36 OFFERS

The purpose of Part 36 offers is to give financial incentives to the other side to encourage them to settle at any time, even prior to commencement of proceedings. The principle behind Part 36 is that a party who tries to be reasonable but is dragged to trial should be compensated, and a party who unreasonably insists on trial in the face of a reasonable offer should be penalised. A Part 36 offer does not prevent parties making other attempts to settle (such as without prejudice negotiations, or Alternative Dispute Resolution). It must be certain whether something is a Part 36 offer or not. A Part 36 offer must: (1) be in writing, (2) state that it is intended to have the consequences of Part 36, (3) give a relevant period of at least 21 days, and (4) state whether it relates to all or part of the claim and includes any counterclaims (CPR 36.2). The party making the offer can use Form N242A or draft a bespoke letter for this. If these formalities have not been fully complied with, the offer might not have Part 36 consequences (PHI v Robert West). Must be made 21 days or more before trial, otherwise it is actually an ordinary settlement offer rather than a Part 36 offer. Settlement offers are governed by CPR 44.3. A Part 36 offer cannot be time limited – so if you wish to make an offer to settle which is time limited, your only options therefore are:

1) To make a Part 36 offer and then withdraw it (withdrawing before the relevant period

requires the permission of the court (CPR 36.3(5)); withdrawing after the relevant

period has expired does not require court permission, but a Notice of Withdrawal is

needed (CPR 363(6)&(7))); or

2) To make a Calderbank offer (which means an offer to settle headed “without

prejudice, save as to costs”).

Both withdrawal and acceptance of a Part 36 offer require a Notice to be served. Note that ordinary contractual rules (e.g. lapse, counter-offer rejection, postal rule) do not apply (Gibbon v Manchester CC), so do not apply any rules about acceptance and withdrawal of offers that you may have learnt elsewhere. Accepting a Part 36 offer brings the case to an end (the action is stayed (CPR 36.11(1))). Other negotiated settlements are effectively contracts between the parties and will need a court order to bring the proceedings to an end. Acceptance of a Part 36 offer must be in writing (CPR 36.9(1)). Acceptance must be served on the offeror and filed with the court (PD 36A para 3.1). If the offer is accepted outside of the relevant period, the parties must agree liability for costs between themselves and if they cannot do so the court will make an order (CPR 36.10(4)).

www.lpcanswered.com

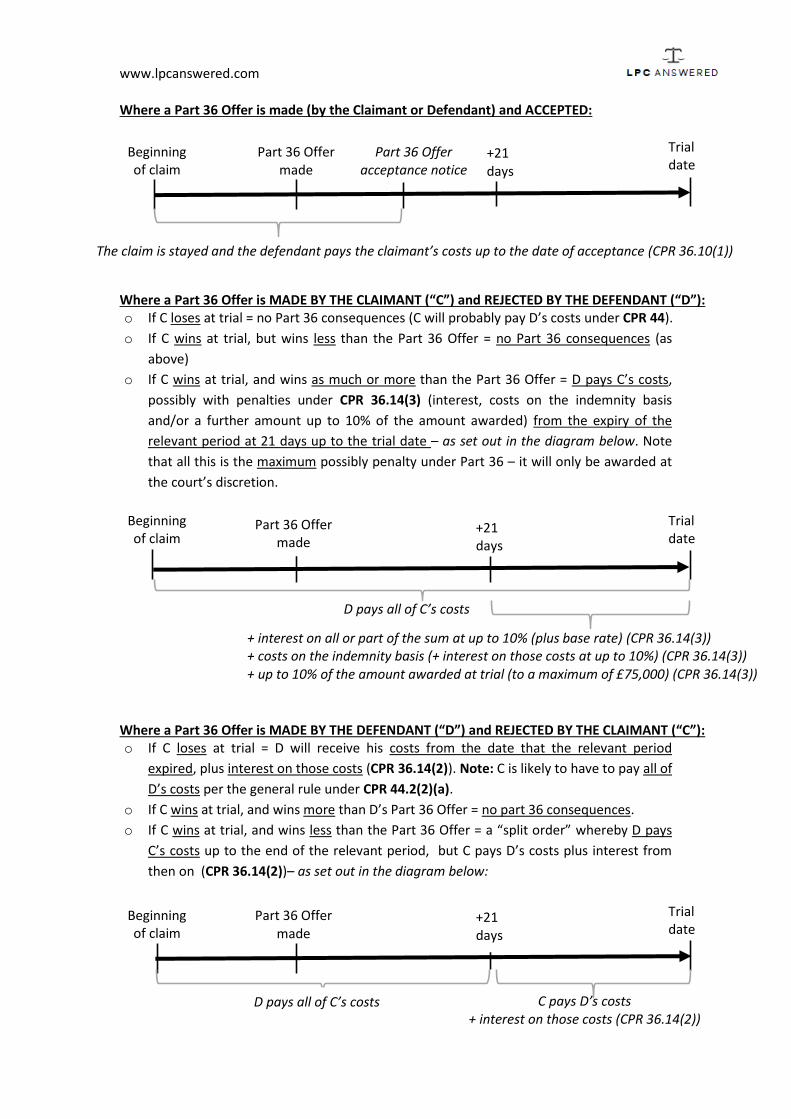

Where a Part 36 Offer is made (by the Claimant or Defendant) and ACCEPTED:

Where a Part 36 Offer is MADE BY THE CLAIMANT (“C”) and REJECTED BY THE DEFENDANT (“D”): o If C loses at trial = no Part 36 consequences (C will probably pay D’s costs under CPR 44).

o If C wins at trial, but wins less than the Part 36 Offer = no Part 36 consequences (as

above)

o If C wins at trial, and wins as much or more than the Part 36 Offer = D pays C’s costs,

possibly with penalties under CPR 36.14(3) (interest, costs on the indemnity basis

and/or a further amount up to 10% of the amount awarded) from the expiry of the

relevant period at 21 days up to the trial date – as set out in the diagram below. Note

that all this is the maximum possibly penalty under Part 36 – it will only be awarded at

the court’s discretion.

. Where a Part 36 Offer is MADE BY THE DEFENDANT (“D”) and REJECTED BY THE CLAIMANT (“C”): o If C loses at trial = D will receive his costs from the date that the relevant period

expired, plus interest on those costs (CPR 36.14(2)). Note: C is likely to have to pay all of

D’s costs per the general rule under CPR 44.2(2)(a).

o If C wins at trial, and wins more than D’s Part 36 Offer = no part 36 consequences.

o If C wins at trial, and wins less than the Part 36 Offer = a “split order” whereby D pays

C’s costs up to the end of the relevant period, but C pays D’s costs plus interest from

then on (CPR 36.14(2))– as set out in the diagram below:

.

+ interest on all or part of the sum at up to 10% (plus base rate) (CPR 36.14(3)) + costs on the indemnity basis (+ interest on those costs at up to 10%) (CPR 36.14(3)) + up to 10% of the amount awarded at trial (to a maximum of £75,000) (CPR 36.14(3))

The claim is stayed and the defendant pays the claimant’s costs up to the date of acceptance (CPR 36.10(1))

Beginning of claim

Part 36 Offer made

Beginning of claim

Part 36 Offer made

Trial date

Part 36 Offer acceptance notice

+21 days

Trial date

D pays all of C’s costs

Beginning of claim

Part 36 Offer made

Trial date

+21 days

C pays D’s costs + interest on those costs (CPR 36.14(2))

D pays all of C’s costs

+21 days

www.lpcanswered.com

ENFORCING A SETTLEMENT

Accepting a Part 36 Offer will bring the claim to an end by means of a stay. Otherwise, to enforce a settlement which is not a Part 36 Offer, the settlement must be on the face of a court order (which will generally be a consent order). This is because ordinary settlements are effectively contracts between the parties – to enforce such a settlement the innocent party would have to commence further proceedings for breach of contract and then apply for summary judgment. Court orders make any enforcement issues easier and formally bring court proceedings to an end. Possible court orders following a non-Part 36 settlement:

1. Stay of proceedings – until such time as the court may direct.

2. Dismissal – the claim is dismissed and the claimant can never bring proceedings

again on the issue. There are no automatic costs consequences, as costs may be

agreed beforehand between the parties.

3. Consent order/Judgment – either simply an order laying out the terms of the

contract between the parties for evidential purposes, or an order drawn up by the

court with terms that the parties agree to. Only the latter can be varied by the court.

4. Discontinuance – not really a court order, as it is the claimant who discontinues his

claim. This is an advantage for the claimant, as the claimant could later bring fresh

proceedings. It is presumed that the claimant pays the defendant’s costs, but costs

are agreed beforehand between the parties.

www.lpcanswered.com

CONDUCT SAMPLE

FINANCIAL PROMOTIONS – SECTION 21 FSMA

Law firms must comply with both ss. 19(1) & 21 FSMA. Section 21 FSMA states that firms

must not make financial promotions in the course of business unless they are authorised, or

the content of their communications is authorised. “Financial promotions” involve making

communications which invite or induce others to engage in certain investment activities.

Doing so is a crime (s. 25).

Parts of s. 21 are extracted in the box below – key elements are underlined:

21 Restrictions on financial promotion.

(1) A person (“A”) must not, in the course of business, communicate an invitation

or inducement to engage in investment activity.

(2) But subsection (1) does not apply if—

(a) A is an authorised person; or

(b) the content of the communication is approved for the purposes of this

section by an authorised person.

(3) In the case of a communication originating outside the United Kingdom,

subsection (1) applies only if the communication is capable of having an effect

in the United Kingdom.

(4) The Treasury may by order specify circumstances in which a person is to be

regarded for the purposes of subsection (1) as—

(a) acting in the course of business;

(b) not acting in the course of business.

(5) The Treasury may by order specify circumstances (which may include

compliance with financial promotion rules) in which subsection (1) does not

apply.

(8) “Engaging in investment activity” means—

(a) entering or offering to enter into an agreement the making or

performance of which by either party constitutes a controlled activity;

or

(b) exercising any rights conferred by a controlled investment to acquire,

dispose of, underwrite or convert a controlled investment.

(9) An activity is a controlled activity if—

(a) it is an activity of a specified kind or one which falls within a specified

class of activity; and

(b) it relates to an investment of a specified kind, or to one which falls within

www.lpcanswered.com

a specified class of investment.

(10) An investment is a controlled investment if it is an investment of a specified

kind or one which falls within a specified class of investment.

(13) “Communicate” includes causing a communication to be made.

(14) “Investment” includes any asset, right or interest.

(15) “Specified” means specified in an order made by the Treasury.

Note: this is not the full text of s. 21 – always refer to the statute in preference to this

extract.

You will notice that many sections refer to the contents of an order made by the Treasury

– this is The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005

(the “FPO”).

“Financial promotions” cover a wide range of activities under s. 21 – clearly offering

investments and providing opportunities for people to invest would be financial promotions,

but so too would circulating offer documents to shareholders in a company takeover, for

example.

Exam technique: Follow these steps

STEP 1: Is there a communication? Is it made in the course of business? Does it originate

from the UK, or is it capable of having an effect in the UK? What type of communication is

it?

A communication must be made by someone to someone else. “Communicate” includes

directly making a communication to another person in the ordinary sense of the word, as

well as causing a communication to be made by another person (s. 21(13)).

Communications must be made in the course of business (s. 21(1)).

Communications are broadly defined – they must be made by a person in the UK, or by

someone outside the UK where they are simply “capable” of having any effect in the UK (s.

21(3)).

The FPO has a very broad definition of “communication” – it includes “real time”

communications (face-to-face meetings and phone calls), “non-real time” communications

(letters, emails, etc), “solicited” communications (communications initiated or invited by

the other party) and “unsolicited” communications (any communication which is not

solicited).

So, for example, a phone call to a client made in response to a message left by them asking

for the solicitor to phone back would be a solicited real time communication. If the solicitor

responded by email that would be a solicited non-real time communication. An email sent

out the blue by a fund manager would be an unsolicited non-real time communication. A

knock on the door by a door-to-door salesman would be an unsolicited real time

www.lpcanswered.com

communication.

It is important to understand the type of communication being made because this will

affect the available exemptions see Step 4.

STEP 2: Does the communication relate to a controlled investment?

The “controlled investments” are listed in Schedule I Part II FPO. Among others, they

include:

Rights under a contract of insurance

Shares

Instruments creating or acknowledging indebtedness

Government securities

Options, futures and contracts for difference

You may have noticed that a “controlled investment” under s. 21(10) and the FPO is very

similar to a “specified investment” under s. 19.

STEP 3: Does the communication invite someone to engage in investment activity?

Section 21(8) states that “engaging in investment activity” means: (1) entering into an

agreement the performance of which would mean carrying out a “controlled activity” in

relation to a “controlled investment”; or (2) a person exercising their rights to buy or sell a

“controlled investment.”

“Controlled activities” are very widely defined in Schedule I Part I FPO – they are

like the “specified activities” under s. 19 but wider, as none of the RAO exclusions

apply. Among others, they include:

o Effecting contracts of insurance

o Dealing in securities

o Arranging deals in investments

o Managing investments

“Controlled investments” are listed in Schedule I Part II FPO see Step 2 above.

The communication must invite or induce someone to do either or both of these:

Invitations directly invite someone to engage in investment activity – e.g.

advertisements in newspapers and prospectuses with application forms to

subscribe for shares.

Inducements are less direct and involve an element of persuasion – e.g.

www.lpcanswered.com

advertisements by fund managers that declare that they make investors wealthy.

STEP 4: Is the communication exempt?

Paragraphs 16 – 73 of the FPO list the exempt communications. Roughly speaking, non-real

time communications, solicited real time communications or communications made by an

exempt person will be exempt, but check the specifics of the FPO in each case.

STEP 5: Has an authorised person drafted or approved the content of the

communication?

The “authorised person” must be a person authorised to do so by the FCA or PRA. Note that

it is only ever possible for an authorised person to draft or approve a non-real time

communication.

STEP 6: Conclude

Has there been a communication relating to engaging in investment activity? Is it exempt?

Has an authorised person approved it? What are the consequences? In other words, has

there been a criminal financial promotion?

www.lpcanswered.com

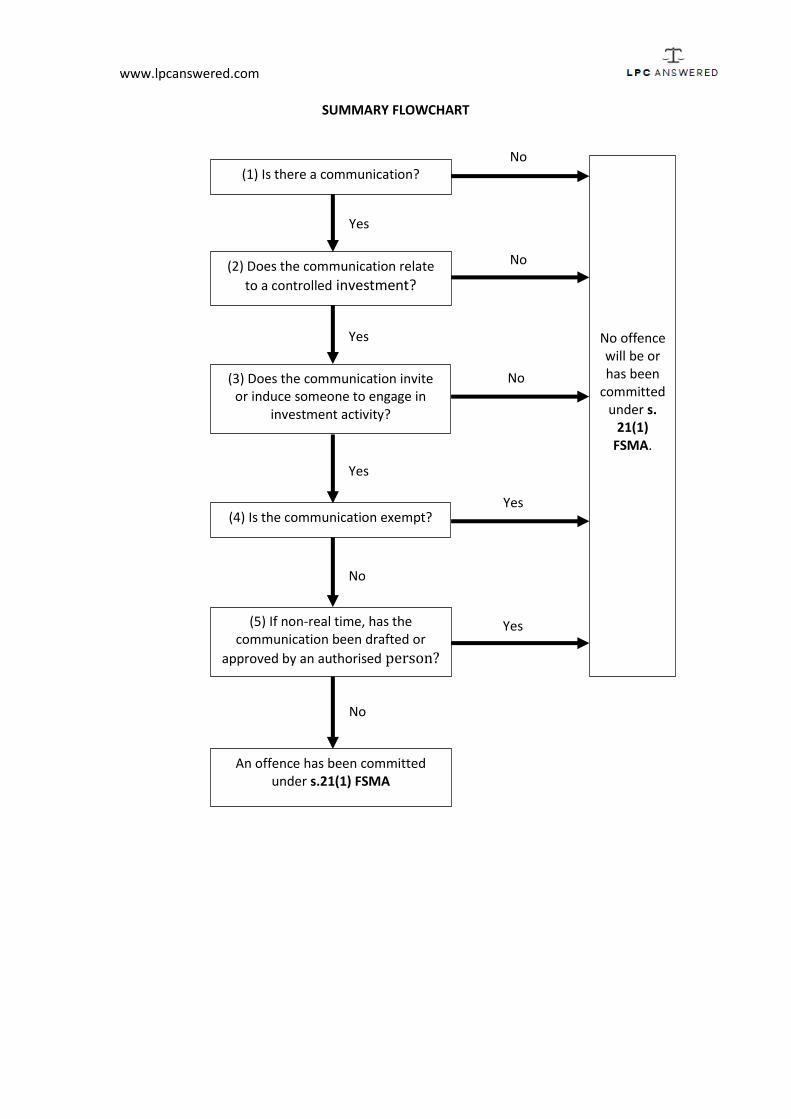

SUMMARY FLOWCHART

Yes

(1) Is there a communication?

(2) Does the communication relate

to a controlled investment?

(3) Does the communication invite or induce someone to engage in

investment activity?

(4) Is the communication exempt?

(5) If non-real time, has the communication been drafted or

approved by an authorised person?

An offence has been committed under s.21(1) FSMA

No offence will be or has been

committed under s.

21(1) FSMA.

Yes

Yes

Yes

Yes

No

No

No

No

No

www.lpcanswered.com

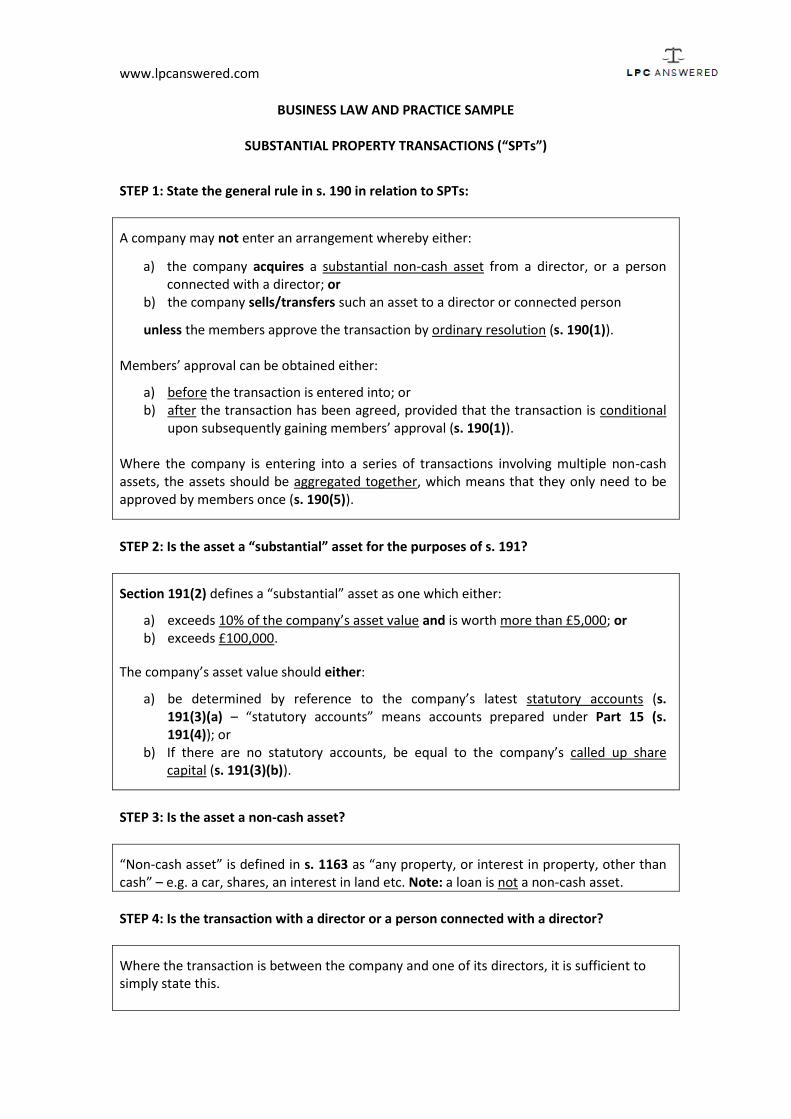

BUSINESS LAW AND PRACTICE SAMPLE

SUBSTANTIAL PROPERTY TRANSACTIONS (“SPTs”)

STEP 1: State the general rule in s. 190 in relation to SPTs:

A company may not enter an arrangement whereby either:

a) the company acquires a substantial non-cash asset from a director, or a person connected with a director; or

b) the company sells/transfers such an asset to a director or connected person

unless the members approve the transaction by ordinary resolution (s. 190(1)). Members’ approval can be obtained either:

a) before the transaction is entered into; or b) after the transaction has been agreed, provided that the transaction is conditional

upon subsequently gaining members’ approval (s. 190(1)). Where the company is entering into a series of transactions involving multiple non-cash assets, the assets should be aggregated together, which means that they only need to be approved by members once (s. 190(5)).

STEP 2: Is the asset a “substantial” asset for the purposes of s. 191?

Section 191(2) defines a “substantial” asset as one which either:

a) exceeds 10% of the company’s asset value and is worth more than £5,000; or b) exceeds £100,000.

The company’s asset value should either:

a) be determined by reference to the company’s latest statutory accounts (s. 191(3)(a) – “statutory accounts” means accounts prepared under Part 15 (s. 191(4)); or

b) If there are no statutory accounts, be equal to the company’s called up share capital (s. 191(3)(b)).

STEP 3: Is the asset a non-cash asset?

“Non-cash asset” is defined in s. 1163 as “any property, or interest in property, other than cash” – e.g. a car, shares, an interest in land etc. Note: a loan is not a non-cash asset.

STEP 4: Is the transaction with a director or a person connected with a director?

Where the transaction is between the company and one of its directors, it is sufficient to simply state this.

www.lpcanswered.com

Where the transaction is between the company and a person connected with a director, you must consider the definition of a connected person in ss. 252-255. According to s. 252(2)(a)-(e), a person is connected with a director if they are:

a) A member of the director’s family. This is defined in s. 253 as the director’s: i) spouse or civil partner; ii) children and step-children; iii) parents; and iv) any person with whom the director lives as partner in an enduring family

relationship, and any children or step children of that person who live with the director and are under 18;

b) A body corporate with which the director is connected – defined in ss. 254-256; c) The trustee of a trust of which the director or persons connected to him are

beneficiaries; d) A (business) partner of either the director or a person connected with him; and e) A firm with legal personality in which the director is a partner or in which any

partner is connected to the director by virtue of the above.

STEP 5: Do any exceptions apply?

The company does not need to gain members’ approval under s. 190 if:

The director or connected person is acting in their capacity as a shareholder of the company (s. 192(a));

The contract is between a holding company and its subsidiary, or between two wholly owned subsidiaries of the same holding company (s. 192(b));

The company is in administration (s. 193(2)); The transaction relates to something to which the director is entitled under their

service contract (s. 190(6)(a)); or The company is not UK-registered (s. 190(4)(a)).

STEP 6: What will be the effect of failing to gain shareholder approval?

If the company fails to gain the required shareholder approval, the transaction will be voidable at the election of the company (s. 195(2)).

However, the shareholders can instead choose to affirm the transaction by ordinary resolution, after it has been entered into. Where they choose to do so within a reasonable period, the transaction cannot then be avoided (s. 196).

In addition, whether or not the transaction is avoided:

any director of the company or of its holding company, or a person connected with them, with whom the company entered into the transaction; and

any other director who authorised the transaction

must account to the company for any gain they make, and must jointly and severally indemnify the company for any loss it suffers, as a result of the transaction (ss. 195(3)&(4)).

www.lpcanswered.com

SUGGESTED PROCEDURE PLAN FOR SPT APPROVAL

First Board Meeting

Notice Any director can call (MA 9) on “reasonable notice” (Browne v La Trinidad).

Quorum 2 (MA 11(2)).

Agenda

Board must agree to call GM using their powers in s. 302. They should approve

notice of the GM – call GM on 14 clear days notice (ss. 307 & 360). Notice of a

GM should contain:

i. Time, date and place of meeting (s. 311(1)); and ii. Proxy notice (s. 325(1)).

Should also draft an ordinary resolution for the shareholders approving the SPT.

Voting Unanimous or by a simple majority on a show of hands (MAs 7 & 8).

General Meeting

Notice

Notice period is 14 clear days (ss. 307, 360), but if there is insufficient time:

Written Resolution procedure is a possibility (ss. 289 – 291, 296, 297,

300) – circulate to all eligible members immediately – there are no

abstentions, as non-votes count as votes against – votes in favour

cannot be revoked – will lapse if threshold of votes is not met by a set

date – all votes on written resolutions are on a poll.

Short Notice procedure reduces notice time to the time it takes to

acquire necessary consent – needs at least 90% of shareholders to

agree (s. 307(4)-(6)).

Quorum 2 (s. 318(2)), unless a single member company, then 1 (s. 318(1)).

Agenda The shareholders must vote to approve the SPT (s. 190).

Voting Ordinary resolutions require 50%+ votes in favour (s. 282) – voting is on a show of hands, unless a poll vote is demanded (MA 42).

Second Board Meeting

Notice Any director can call (MA 9) on “reasonable notice” (Browne v La Trinidad).

Quorum 2 (MA 11(2)), but remember: the interested director will not count towards the

quorum (MA 14(1)).

Agenda

Chairman reports what resolutions were passed at the GM.

Unless an exception applies, the director involved in the proposed SPT must declare it (s. 177) by making a written declaration under s. 184 (unless general notice has already been given to the board under s. 185).

The board can now enter into the SPT contract using their general power under

www.lpcanswered.com

MA 3. They could have done so at the first BM, but to do so the contract would

have had to have been conditional upon subsequently gaining the members’

approval (s. 190(1)).

Secretary instructed (or a director if no secretary) to file documents set out under post meeting matters.

Voting

Unanimous or by a simple majority show of hands (MAs 7 & 8). Remember: the interested director cannot vote unless the company has voted to disapply MA 14(1) (MA 14(3)).

Post Meeting Matters

Update internal records:

1. Draw up minutes of BMs and GM, and enter them into the company’s minute books where they must be kept for at least 10 years (ss. 248 & 355)

2. Keep a copy of all meetings and resolutions (s. 355), even if a sole member company (s. 357).