lq budget 2017

TRANSCRIPT

UNION BUDGET 2017

ANALYSIS

1

LEGAL QUOTIENTCONSULTANTS

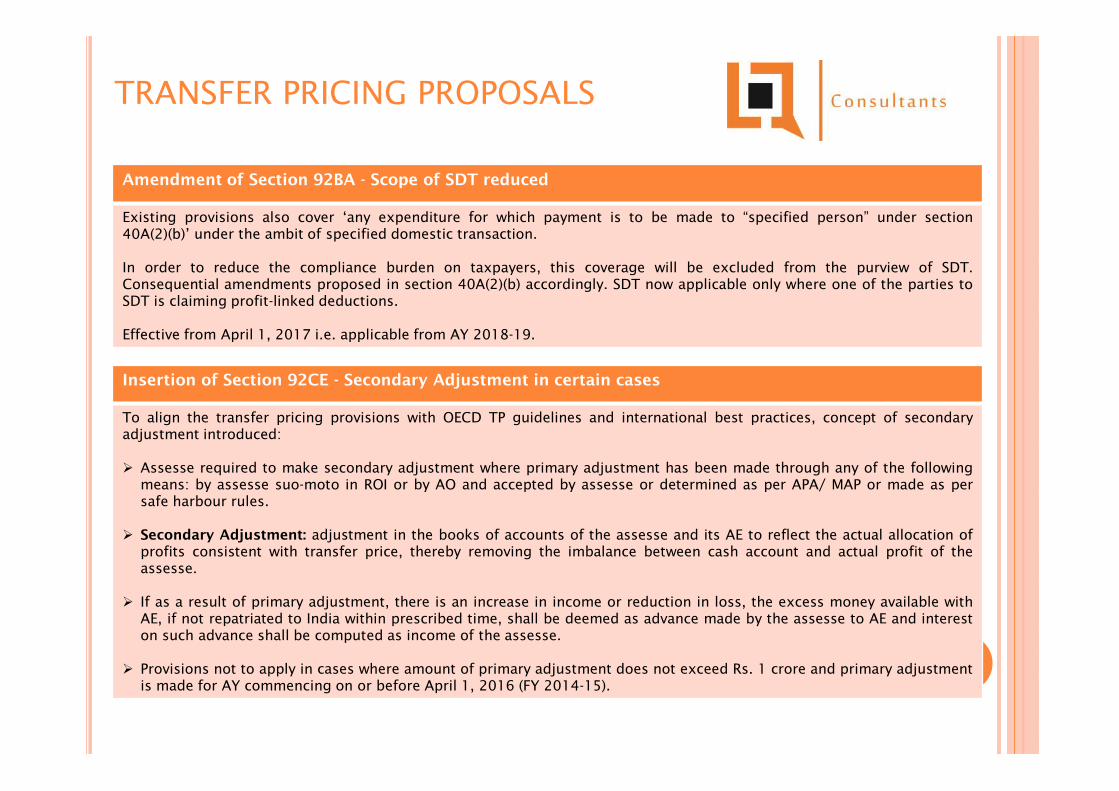

Amendment of Section 92BA - Scope of SDT reduced

Existing provisions also cover ‘any expenditure for which payment is to be made to “specified person” under section40A(2)(b)’ under the ambit of specified domestic transaction.

In order to reduce the compliance burden on taxpayers, this coverage will be excluded from the purview of SDT.Consequential amendments proposed in section 40A(2)(b) accordingly. SDT now applicable only where one of the parties toSDT is claiming profit-linked deductions.

Effective from April 1, 2017 i.e. applicable from AY 2018-19.

Insertion of Section 92CE - Secondary Adjustment in certain cases

To align the transfer pricing provisions with OECD TP guidelines and international best practices, concept of secondaryadjustment introduced:

Assesse required to make secondary adjustment where primary adjustment has been made through any of the followingmeans: by assesse suo-moto in ROI or by AO and accepted by assesse or determined as per APA/ MAP or made as persafe harbour rules.

Secondary Adjustment: adjustment in the books of accounts of the assesse and its AE to reflect the actual allocation ofprofits consistent with transfer price, thereby removing the imbalance between cash account and actual profit of theassesse.

If as a result of primary adjustment, there is an increase in income or reduction in loss, the excess money available withAE, if not repatriated to India within prescribed time, shall be deemed as advance made by the assesse to AE and intereston such advance shall be computed as income of the assesse.

Provisions not to apply in cases where amount of primary adjustment does not exceed Rs. 1 crore and primary adjustmentis made for AY commencing on or before April 1, 2016 (FY 2014-15).

TRANSFER PRICING PROPOSALS

Insertion of Section 94B - Thin Capitalization Rules: Limitation of interest deduction in certain cases

To align with the recommendations of OECD BEPS Action Plan 4 to counter cross-border shifting of profits through excessiveinterest payments and to protect country’s tax base, new section 94B has been introduced:

Provisions shall be applicable to an Indian company or permanent establishment of a foreign company in India, being theborrowers, paying interest or other similar consideration to its non-resident AE for which deduction is claimed forcomputing income under PGBP.

Interest expense deduction shall be restricted to 30% of EBITDA of borroweror interest paid / payable to AE, whichever isless.

In case debt is issued by non-AE lender, but AE provides guarantee or deposits equivalent to debt amount with such non-AE lender, such debt shall be deemed to have been issued by AE.

Interest expenditure not deducted in relevant FY, shall be carried forward and set-off as per prescribed limits forsubsequent 8 AYs subject to the 30% limit.

Provisions shall not be applicable to taxpayers engaged in the business of insurance or banking.

Provisions shall be applicable only if interest expenditure exceeds Rs. 1 crore.

Debt defined: loan, financial instrument, finance lease, financial derivative or any arrangement giving rise to interest,discount or other finance charges that are deductible for computing income under PGBP.

Effective fromApril 1, 2018 i.e. applicable fromAY 2018-19

OTHER DIRECT TAX PROPOSALS

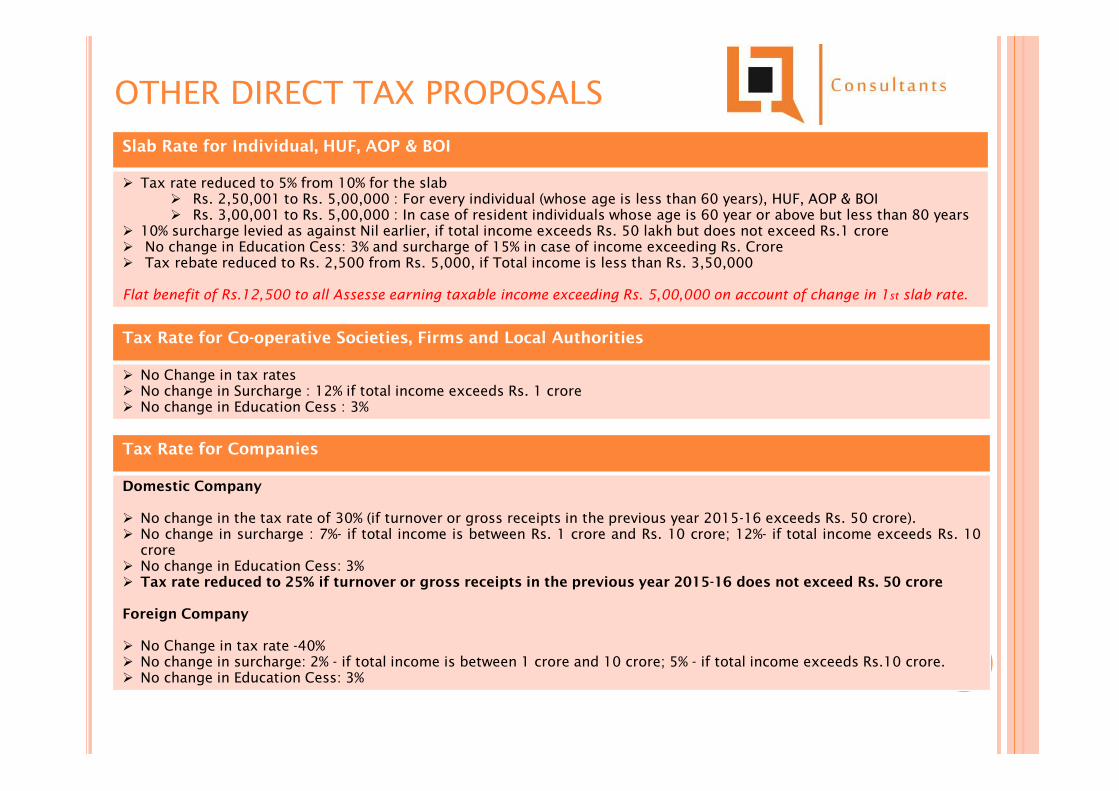

Slab Rate for Individual, HUF, AOP & BOI

Tax rate reduced to 5% from 10% for the slab Rs. 2,50,001 to Rs. 5,00,000 : For every individual (whose age is less than 60 years), HUF, AOP & BOI Rs. 3,00,001 to Rs. 5,00,000 : In case of resident individuals whose age is 60 year or above but less than 80 years

10% surcharge levied as against Nil earlier, if total income exceeds Rs. 50 lakh but does not exceed Rs.1 crore No change in Education Cess: 3% and surcharge of 15% in case of income exceeding Rs. Crore Tax rebate reduced to Rs. 2,500 from Rs. 5,000, if Total income is less than Rs. 3,50,000

Flat benefit of Rs.12,500 to all Assesse earning taxable income exceeding Rs. 5,00,000 on account of change in 1st slab rate.

Tax Rate for Co-operative Societies, Firms and Local Authorities

No Change in tax rates No change in Surcharge : 12% if total income exceeds Rs. 1 crore No change in Education Cess : 3%

Tax Rate for Companies

Domestic Company

No change in the tax rate of 30% (if turnover or gross receipts in the previous year 2015-16 exceeds Rs. 50 crore). No change in surcharge : 7%- if total income is between Rs. 1 crore and Rs. 10 crore; 12%- if total income exceeds Rs. 10

crore No change in Education Cess: 3% Tax rate reduced to 25% if turnover or gross receipts in the previous year 2015-16 does not exceed Rs. 50 crore

Foreign Company

No Change in tax rate -40% No change in surcharge: 2% - if total income is between 1 crore and 10 crore; 5% - if total income exceeds Rs.10 crore. No change in Education Cess: 3%

Nature Existing Provisions Proposed

Section 2(42A): Period ofholding for long term assets

(Effective date: AY 2018-19)

Section 2(42A) provides long termcapital asset as the capitalasset held by Assesse for morethan 36 months.

In case of immovable property, being landand building, the period of 36 months has beenreduced to 24 months.This should be a boost to Real Estatetransactions

Provision of Section 55:Base year for computation ofcapital gain.( Effective date: AY 2018-19)

For computing capital gains inrespect of an asset acquired before01.04.1981, the Assesse has beenallowed an option of either to takethe fair market value of the asset ason 01.04.1981 or the actual costof the asset as cost ofacquisition.

Base year for computation of capital gain isproposed to be amended as 01.04.2001.Consequential amendment is also proposedin section 48 and Cost Inflation Indexon1.4.2001 would be the base year forindexation purposes.This should be a boost to Real Estatetransactions

Section 54EC (Effective date :AY 2018-19)

Investment in bond issued by NHAIand REC is eligible for exemptionunder this section.

Investment in any bond redeemable after threeyears which has been notified by the CentralGovernment in this behalf shall also be eligiblefor exemption.Govt hopes to mop up funds for otherinfrastructure development projects through thisroute

Section 23 : Determiningthe annual value of houseproperty held as stock intrade.(Effective date: AY 2018-19)

If the property is not let out duringthe year, the annual value of anyproperty shall be deemed to be thesum for which theproperty might reasonably beexpected to let from year to year.

If the property is not let during the year, annualvalue of the property shall be taken as nil for aperiod of one year from the end of financial yearin which the certificate of completion ofproperty is received.This provision is introduced to afford realestate players an opportunity to liquidatetheir inventory within a specified time and notsuffer tax on notional income.

Special provisions for computation of capital gains in case of Joint Development Agreement (Effectivefrom April 1, 2018)

New sub-section (5A) in section 45 inserted in the Act. Where an individual/ HUF enters into a specified agreement for development of a project, capital gains shall be chargeable

in the year in which the certificate of completion for the whole or part of the project is issued by the competent authority. Full value of consideration shall be the stamp duty value of his share, being land or building or both, as on the date of

certificate of completion as increased by any consideration received in cash. However, the above benefit shall not not apply to an assesse who transfers his share in the project to any other person on

or before the date of issue of said certificate of completion It is proposed to amend section 49 that cost of acquisition in the hands of the transferee shall be the amount which is

deemed as full value of consideration under the said proposed provision.This is a welcome amendment for the real estate sector considering that tax had to be paid even though the transferor didnot receive any money on transfer date.

Tax deducted at source in case of joint development agreement (Effective from April 1, 2017)

New section 194-IC inserted in the Act to provide that In case any monetary consideration is payable under the specified agreement TDS at the rate of 10% shall be deductible from such payment

Nature Existing Provision Proposed

Section 80-IBA topromoteAffordableHousing(Effectivedate: AY2018-19)

100 % deduction in respectof the profits and gainsderived from developingand building certainhousing projects subject tocertain conditions.

Conditions are proposed to be relaxed as under:

Size of residential unit shall be based on “carpet area”not on “built-up area”Project on plot of land measuring at least 1,000 sq. mtrs and restriction ofsize of 30 sq. mtrs residential unit applies in Chennai, Delhi, Kolkata andMumbai;

For other places, plot of land should measure at least 2,000 sq. mtrs andrestriction in size of residential unit is 60 sq. mtrs

Period of completion of project increasedfromexisting three years to fiveyears.

More real estate players would be able to avail the tax holiday benefit and is astep in the direction of Government’s commitment to make availableaffordable housing to all.

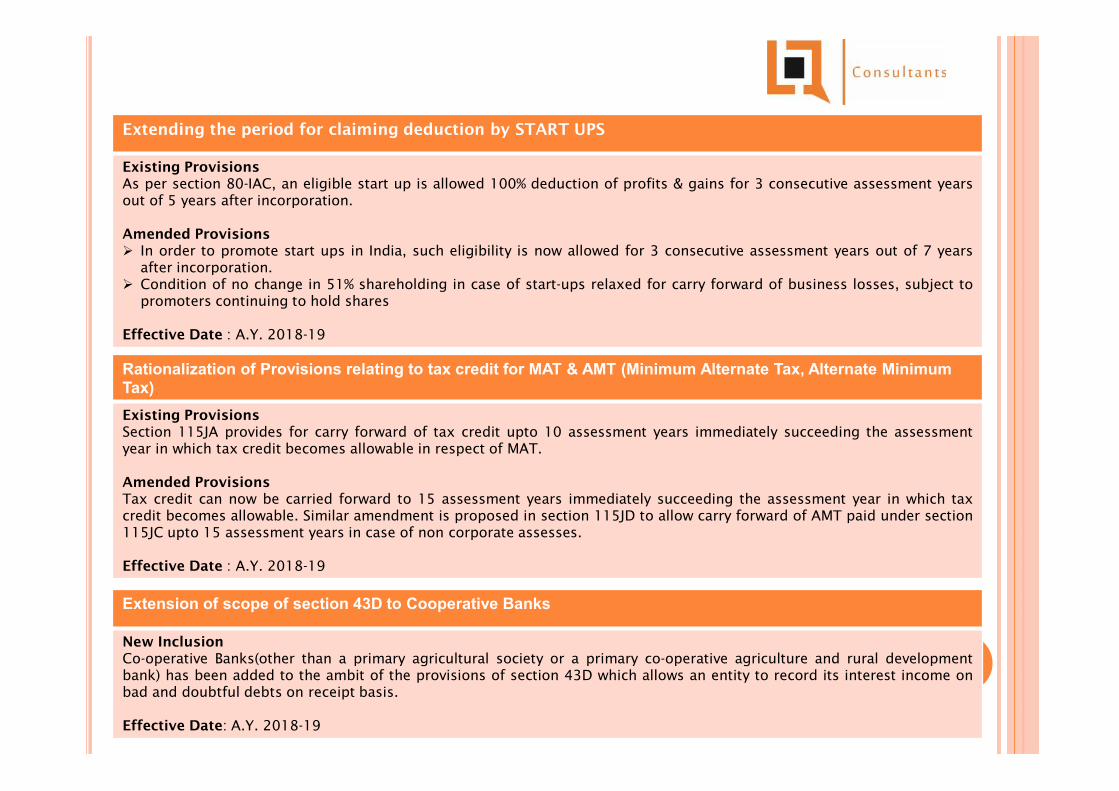

Extending the period for claiming deduction by START UPS

Existing ProvisionsAs per section 80-IAC, an eligible start up is allowed 100% deduction of profits & gains for 3 consecutive assessment yearsout of 5 years after incorporation.

Amended Provisions In order to promote start ups in India, such eligibility is now allowed for 3 consecutive assessment years out of 7 years

after incorporation. Condition of no change in 51% shareholding in case of start-ups relaxed for carry forward of business losses, subject to

promoters continuing to hold shares

Effective Date : A.Y. 2018-19

Rationalization of Provisions relating to tax credit for MAT & AMT (Minimum Alternate Tax, Alternate MinimumTax)Existing ProvisionsSection 115JA provides for carry forward of tax credit upto 10 assessment years immediately succeeding the assessmentyear in which tax credit becomes allowable in respect of MAT.

Amended ProvisionsTax credit can now be carried forward to 15 assessment years immediately succeeding the assessment year in which taxcredit becomes allowable. Similar amendment is proposed in section 115JD to allow carry forward of AMT paid under section115JC upto 15 assessment years in case of non corporate assesses.

Effective Date : A.Y. 2018-19

Extension of scope of section 43D to Cooperative Banks

New InclusionCo-operative Banks(other than a primary agricultural society or a primary co-operative agriculture and rural developmentbank) has been added to the ambit of the provisions of section 43D which allows an entity to record its interest income onbad and doubtful debts on receipt basis.

Effective Date: A.Y. 2018-19

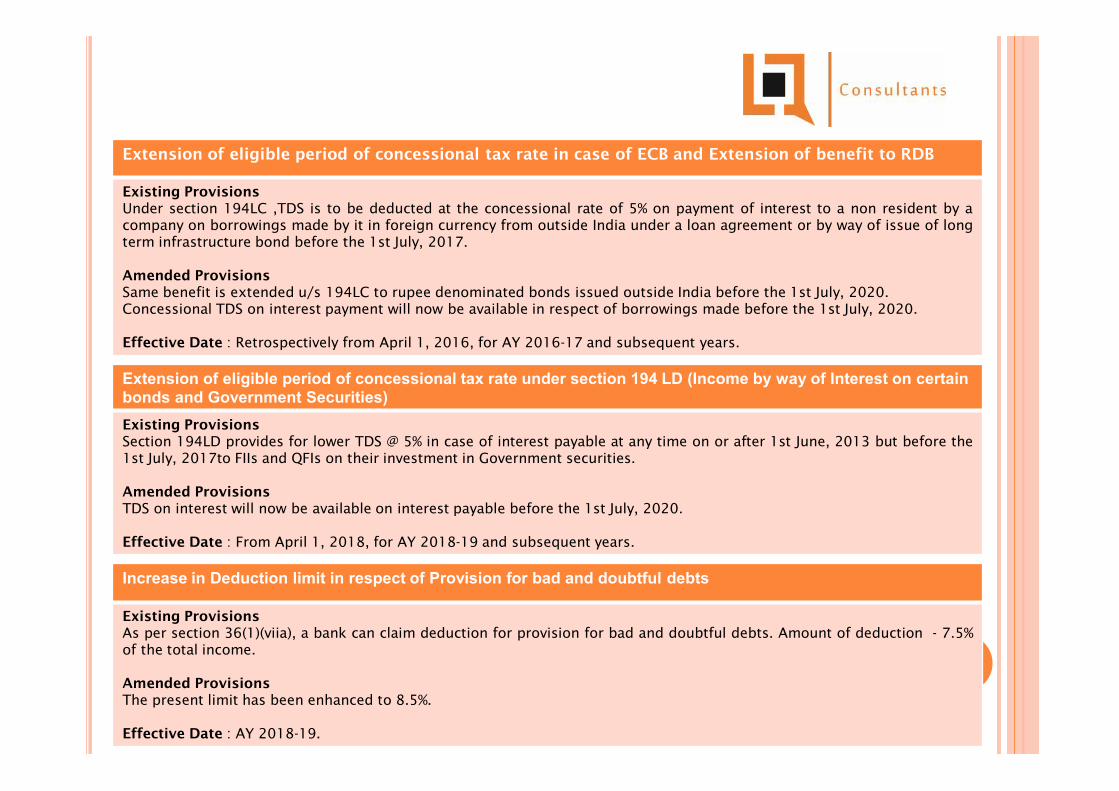

Extension of eligible period of concessional tax rate in case of ECB and Extension of benefit to RDB

Existing ProvisionsUnder section 194LC ,TDS is to be deducted at the concessional rate of 5% on payment of interest to a non resident by acompany on borrowings made by it in foreign currency from outside India under a loan agreement or by way of issue of longterm infrastructure bond before the 1st July, 2017.

Amended ProvisionsSame benefit is extended u/s 194LC to rupee denominated bonds issued outside India before the 1st July, 2020.Concessional TDS on interest payment will now be available in respect of borrowings made before the 1st July, 2020.

Effective Date : Retrospectively from April 1, 2016, for AY 2016-17 and subsequent years.

Extension of eligible period of concessional tax rate under section 194 LD (Income by way of Interest on certainbonds and Government Securities)Existing ProvisionsSection 194LD provides for lower TDS @ 5% in case of interest payable at any time on or after 1st June, 2013 but before the1st July, 2017to FIIs and QFIs on their investment in Government securities.

Amended ProvisionsTDS on interest will now be available on interest payable before the 1st July, 2020.

Effective Date : From April 1, 2018, for AY 2018-19 and subsequent years.

Increase in Deduction limit in respect of Provision for bad and doubtful debts

Existing ProvisionsAs per section 36(1)(viia), a bank can claim deduction for provision for bad and doubtful debts. Amount of deduction - 7.5%of the total income.

Amended ProvisionsThe present limit has been enhanced to 8.5%.

Effective Date : AY 2018-19.

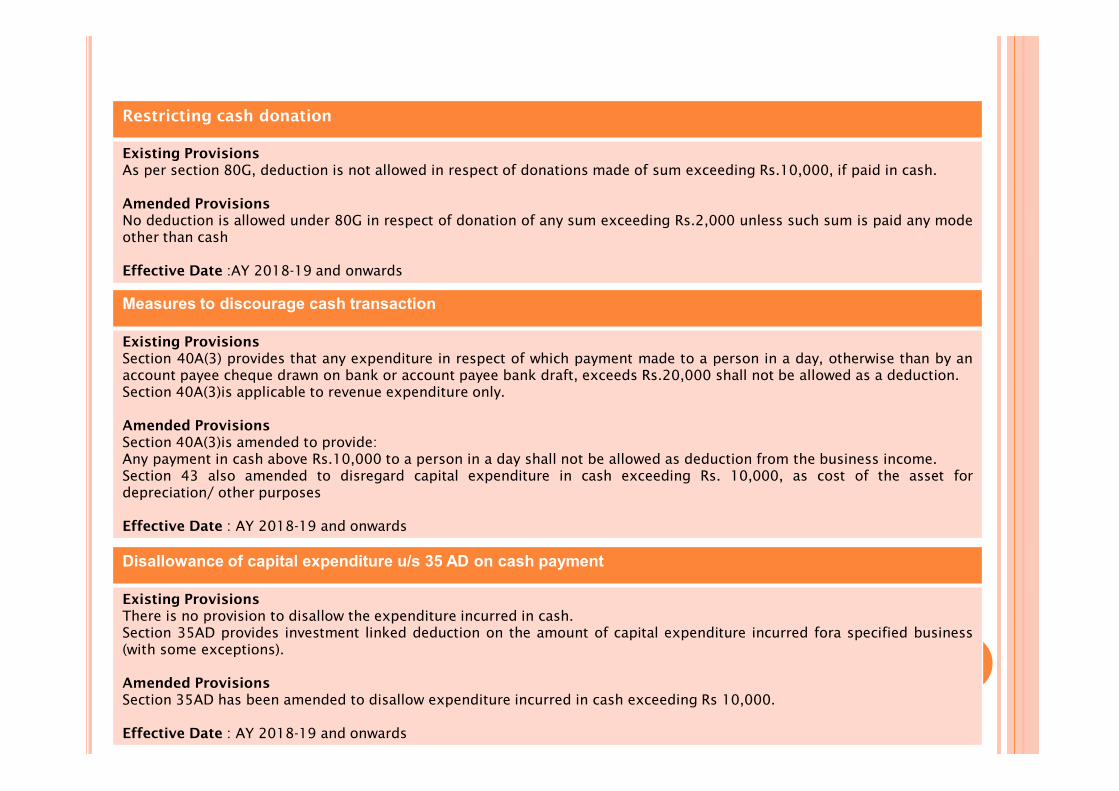

Restricting cash donation

Existing ProvisionsAs per section 80G, deduction is not allowed in respect of donations made of sum exceeding Rs.10,000, if paid in cash.

Amended ProvisionsNo deduction is allowed under 80G in respect of donation of any sum exceeding Rs.2,000 unless such sum is paid any modeother than cash

Effective Date :AY 2018-19 and onwards

Measures to discourage cash transaction

Existing ProvisionsSection 40A(3) provides that any expenditure in respect of which payment made to a person in a day, otherwise than by anaccount payee cheque drawn on bank or account payee bank draft, exceeds Rs.20,000 shall not be allowed as a deduction.Section 40A(3)is applicable to revenue expenditure only.

Amended ProvisionsSection 40A(3)is amended to provide:Any payment in cash above Rs.10,000 to a person in a day shall not be allowed as deduction from the business income.Section 43 also amended to disregard capital expenditure in cash exceeding Rs. 10,000, as cost of the asset fordepreciation/ other purposes

Effective Date : AY 2018-19 and onwards

Disallowance of capital expenditure u/s 35 AD on cash payment

Existing ProvisionsThere is no provision to disallow the expenditure incurred in cash.Section 35AD provides investment linked deduction on the amount of capital expenditure incurred fora specified business(with some exceptions).

Amended ProvisionsSection 35AD has been amended to disallow expenditure incurred in cash exceeding Rs 10,000.

Effective Date : AY 2018-19 and onwards

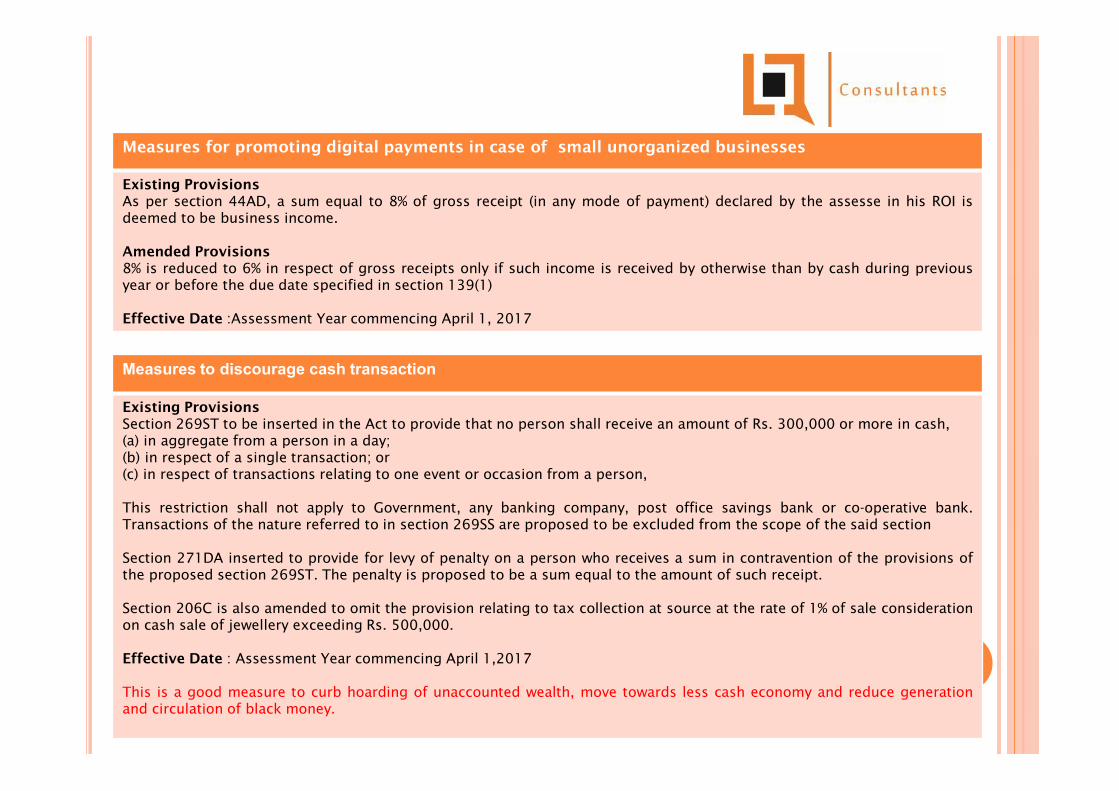

Measures for promoting digital payments in case of small unorganized businesses

Existing ProvisionsAs per section 44AD, a sum equal to 8% of gross receipt (in any mode of payment) declared by the assesse in his ROI isdeemed to be business income.

Amended Provisions8% is reduced to 6% in respect of gross receipts only if such income is received by otherwise than by cash during previousyear or before the due date specified in section 139(1)

Effective Date :Assessment Year commencing April 1, 2017

Measures to discourage cash transaction

Existing ProvisionsSection 269ST to be inserted in the Act to provide that no person shall receive an amount of Rs. 300,000 or more in cash,(a) in aggregate from a person in a day;(b) in respect of a single transaction; or(c) in respect of transactions relating to one event or occasion from a person,

This restriction shall not apply to Government, any banking company, post office savings bank or co-operative bank.Transactions of the nature referred to in section 269SS are proposed to be excluded from the scope of the said section

Section 271DA inserted to provide for levy of penalty on a person who receives a sum in contravention of the provisions ofthe proposed section 269ST. The penalty is proposed to be a sum equal to the amount of such receipt.

Section 206C is also amended to omit the provision relating to tax collection at source at the rate of 1% of sale considerationon cash sale of jewellery exceeding Rs. 500,000.

Effective Date : Assessment Year commencing April 1,2017

This is a good measure to curb hoarding of unaccounted wealth, move towards less cash economy and reduce generationand circulation of black money.

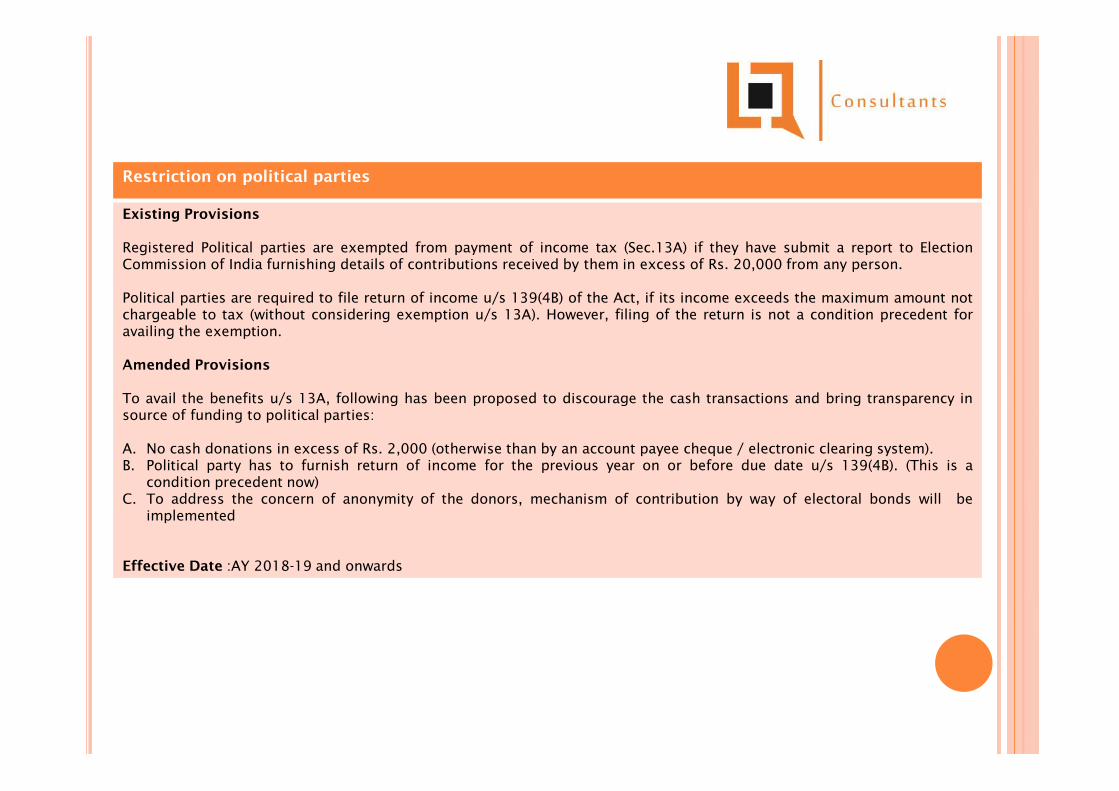

Restriction on political parties

Existing Provisions

Registered Political parties are exempted from payment of income tax (Sec.13A) if they have submit a report to ElectionCommission of India furnishing details of contributions received by them in excess of Rs. 20,000 from any person.

Political parties are required to file return of income u/s 139(4B) of the Act, if its income exceeds the maximum amount notchargeable to tax (without considering exemption u/s 13A). However, filing of the return is not a condition precedent foravailing the exemption.

Amended Provisions

To avail the benefits u/s 13A, following has been proposed to discourage the cash transactions and bring transparency insource of funding to political parties:

A. No cash donations in excess of Rs. 2,000 (otherwise than by an account payee cheque / electronic clearing system).B. Political party has to furnish return of income for the previous year on or before due date u/s 139(4B). (This is a

condition precedent now)C. To address the concern of anonymity of the donors, mechanism of contribution by way of electoral bonds will be

implemented

Effective Date :AY 2018-19 and onwards

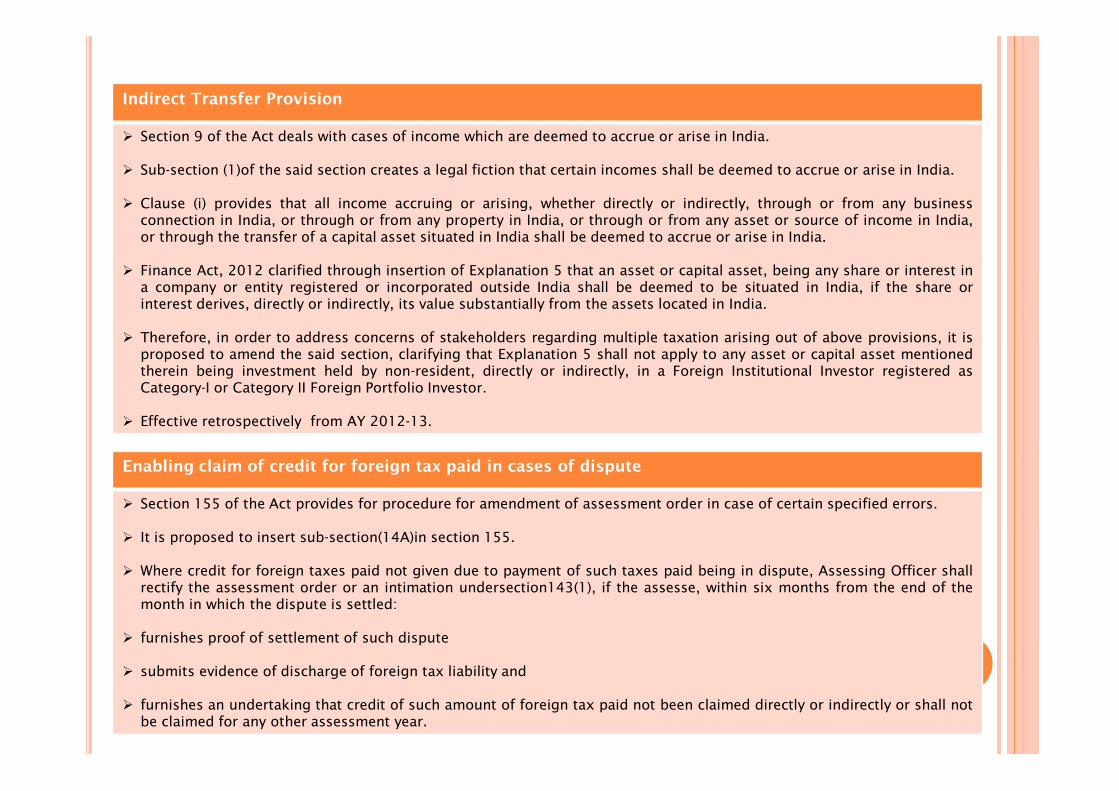

Indirect Transfer Provision

Section 9 of the Act deals with cases of income which are deemed to accrue or arise in India.

Sub-section (1)of the said section creates a legal fiction that certain incomes shall be deemed to accrue or arise in India.

Clause (i) provides that all income accruing or arising, whether directly or indirectly, through or from any businessconnection in India, or through or from any property in India, or through or from any asset or source of income in India,or through the transfer of a capital asset situated in India shall be deemed to accrue or arise in India.

Finance Act, 2012 clarified through insertion of Explanation 5 that an asset or capital asset, being any share or interest ina company or entity registered or incorporated outside India shall be deemed to be situated in India, if the share orinterest derives, directly or indirectly, its value substantially from the assets located in India.

Therefore, in order to address concerns of stakeholders regarding multiple taxation arising out of above provisions, it isproposed to amend the said section, clarifying that Explanation 5 shall not apply to any asset or capital asset mentionedtherein being investment held by non-resident, directly or indirectly, in a Foreign Institutional Investor registered asCategory-I or Category II Foreign Portfolio Investor.

Effective retrospectively from AY 2012-13.

Enabling claim of credit for foreign tax paid in cases of dispute

Section 155 of the Act provides for procedure for amendment of assessment order in case of certain specified errors.

It is proposed to insert sub-section(14A)in section 155.

Where credit for foreign taxes paid not given due to payment of such taxes paid being in dispute, Assessing Officer shallrectify the assessment order or an intimation undersection143(1), if the assesse, within six months from the end of themonth in which the dispute is settled:

furnishes proof of settlement of such dispute

submits evidence of discharge of foreign tax liability and

furnishes an undertaking that credit of such amount of foreign tax paid not been claimed directly or indirectly or shall notbe claimed for any other assessment year.

Section Existing Provision Proposed Adjustment

Amendment inSection 153(1) inrespect of timelimit for makingan assessmentorder undersection 143 and144

21 months from the end of the relevant AY For AY 2018-19 18 months

For AY 2019-20 and onwards 12 months

Amendment inSection 153(2) inrespect of timelimit for makingan order ofassessment,reassessment orre-computationunder section 147

9 months from the end of the financial year inwhich the notice under section 148 was issuedfor assessment, re-assessment and re-computation under section 147

12 months from the end of the financial year inwhich the notice under section 148 is served inrespect of notices served on or after April 1,2019

Amendment inSection 153(3) inrespect of timelimit for makingan order for freshassessment, inpursuance oforder undersection 254, 263or 264

Fresh assessment order in pursuance of anorder under section 254 or section 263 orsection 264, setting aside or cancelling anassessment, may be made at any time beforethe expiry of nine months from the end of thefinancial year in which the order under section254 is received/ passed.

Fresh assessment order in pursuance of anorder under section 254 or section 263 orsection 264, setting aside or cancelling anassessment, may be made at any time beforethe expiry of twelvemonths from the end of thefinancial year in whichthe order under section 254 is received/ passed.

Amendment inSection 139(5)

Revised return to be filed before the expiry of1 year from the end of the relevant assessmentyear or before the completion of assessment,whichever is earlier.

Revised return to be filed before the expiry ofthe relevant assessment year or before thecompletion of assessment, whichever is earlier.

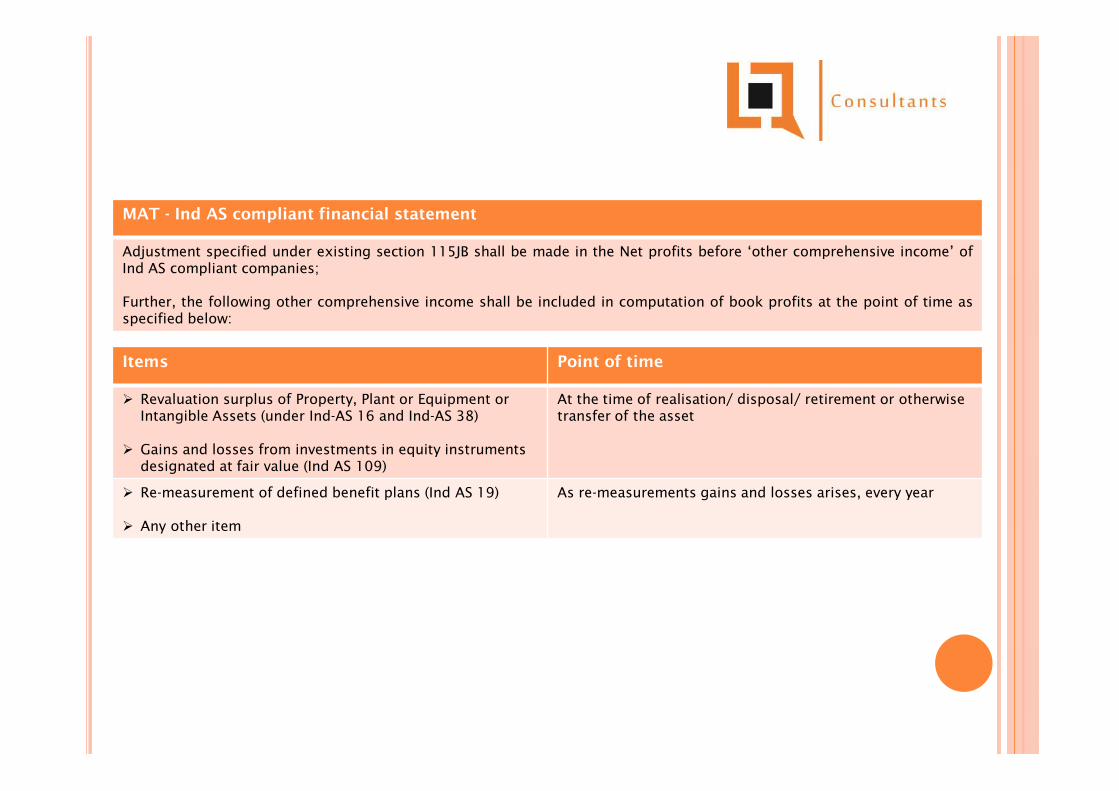

MAT - Ind AS compliant financial statement

Adjustment specified under existing section 115JB shall be made in the Net profits before ‘other comprehensive income’ ofInd AS compliant companies;

Further, the following other comprehensive income shall be included in computation of book profits at the point of time asspecified below:

Items Point of time

Revaluation surplus of Property, Plant or Equipment orIntangible Assets (under Ind-AS 16 and Ind-AS 38)

Gains and losses from investments in equity instrumentsdesignated at fair value (Ind AS 109)

At the time of realisation/ disposal/ retirement or otherwisetransfer of the asset

Re-measurement of defined benefit plans (Ind AS 19)

Any other item

As re-measurements gains and losses arises, every year

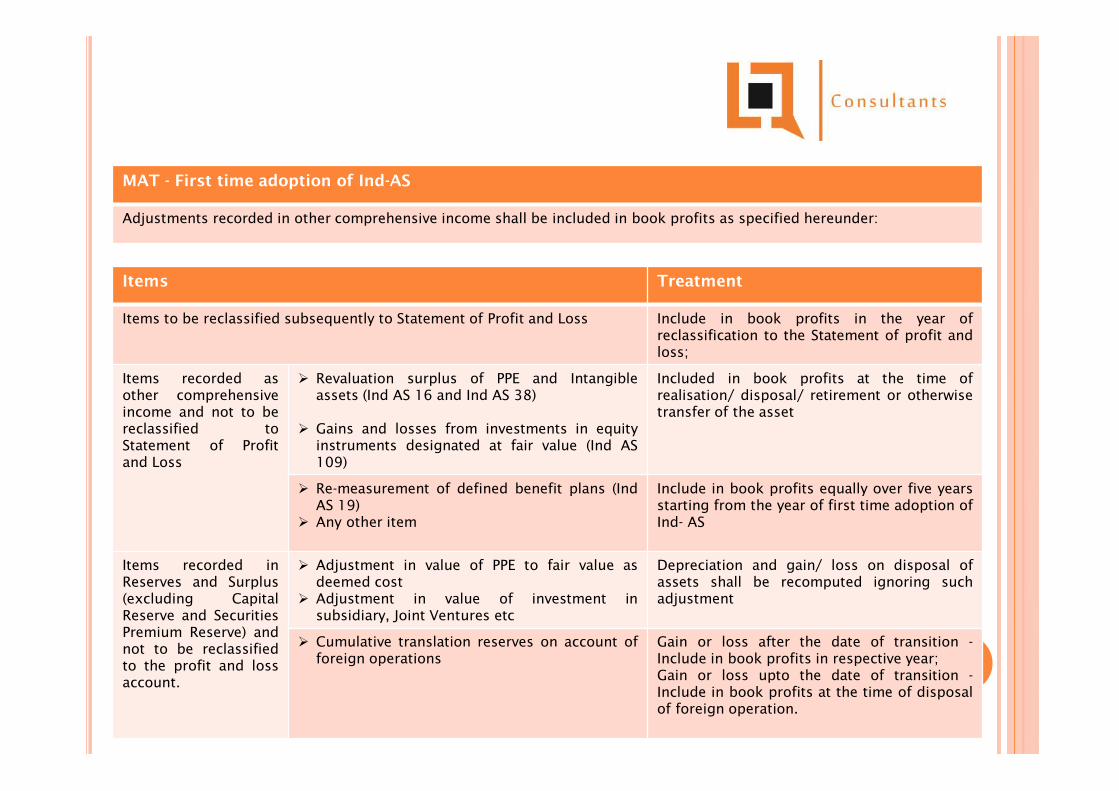

MAT - First time adoption of Ind-AS

Adjustments recorded in other comprehensive income shall be included in book profits as specified hereunder:

Items Treatment

Items to be reclassified subsequently to Statement of Profit and Loss Include in book profits in the year ofreclassification to the Statement of profit andloss;

Items recorded asother comprehensiveincome and not to bereclassified toStatement of Profitand Loss

Revaluation surplus of PPE and Intangibleassets (Ind AS 16 and Ind AS 38)

Gains and losses from investments in equityinstruments designated at fair value (Ind AS109)

Included in book profits at the time ofrealisation/ disposal/ retirement or otherwisetransfer of the asset

Re-measurement of defined benefit plans (IndAS 19)

Any other item

Include in book profits equally over five yearsstarting from the year of first time adoption ofInd- AS

Items recorded inReserves and Surplus(excluding CapitalReserve and SecuritiesPremium Reserve) andnot to be reclassifiedto the profit and lossaccount.

Adjustment in value of PPE to fair value asdeemed cost

Adjustment in value of investment insubsidiary, Joint Ventures etc

Depreciation and gain/ loss on disposal ofassets shall be recomputed ignoring suchadjustment

Cumulative translation reserves on account offoreign operations

Gain or loss after the date of transition -Include in book profits in respective year;Gain or loss upto the date of transition -Include in book profits at the time of disposalof foreign operation.

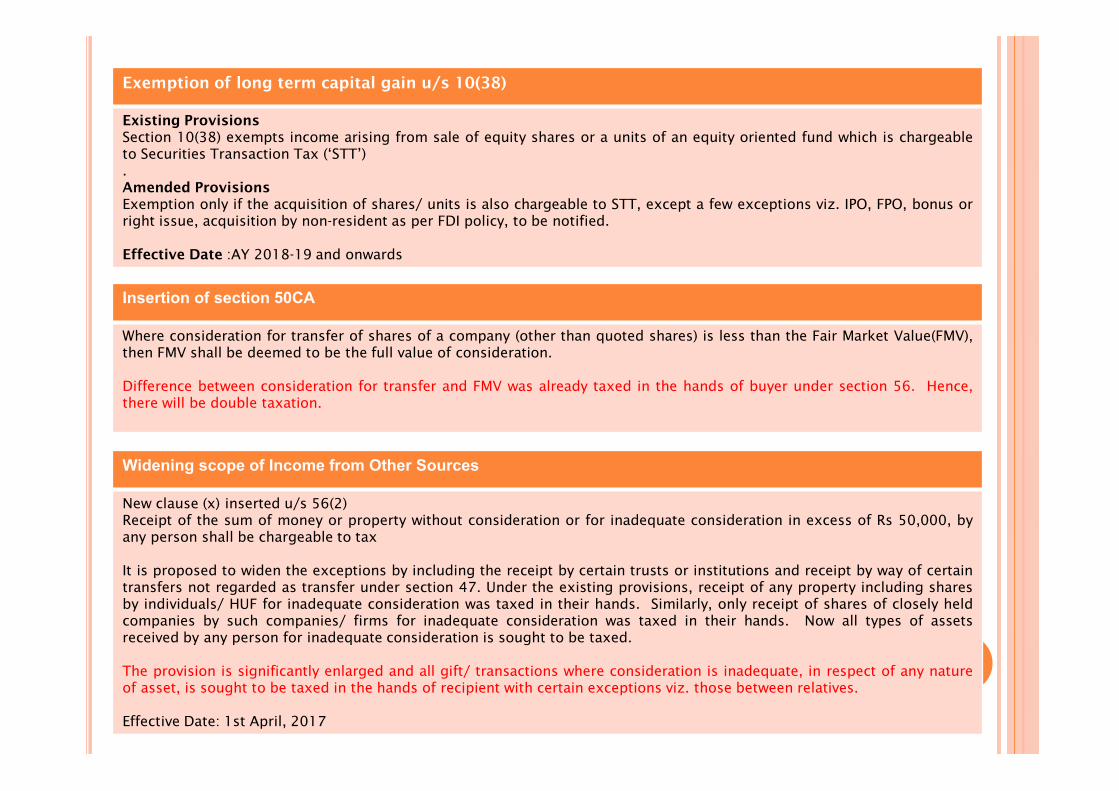

Exemption of long term capital gain u/s 10(38)

Existing ProvisionsSection 10(38) exempts income arising from sale of equity shares or a units of an equity oriented fund which is chargeableto Securities Transaction Tax (‘STT’).Amended ProvisionsExemption only if the acquisition of shares/ units is also chargeable to STT, except a few exceptions viz. IPO, FPO, bonus orright issue, acquisition by non-resident as per FDI policy, to be notified.

Effective Date :AY 2018-19 and onwards

Insertion of section 50CA

Where consideration for transfer of shares of a company (other than quoted shares) is less than the Fair Market Value(FMV),then FMV shall be deemed to be the full value of consideration.

Difference between consideration for transfer and FMV was already taxed in the hands of buyer under section 56. Hence,there will be double taxation.

Widening scope of Income from Other Sources

New clause (x) inserted u/s 56(2)Receipt of the sum of money or property without consideration or for inadequate consideration in excess of Rs 50,000, byany person shall be chargeable to tax

It is proposed to widen the exceptions by including the receipt by certain trusts or institutions and receipt by way of certaintransfers not regarded as transfer under section 47. Under the existing provisions, receipt of any property including sharesby individuals/ HUF for inadequate consideration was taxed in their hands. Similarly, only receipt of shares of closely heldcompanies by such companies/ firms for inadequate consideration was taxed in their hands. Now all types of assetsreceived by any person for inadequate consideration is sought to be taxed.

The provision is significantly enlarged and all gift/ transactions where consideration is inadequate, in respect of any natureof asset, is sought to be taxed in the hands of recipient with certain exceptions viz. those between relatives.

Effective Date: 1st April, 2017

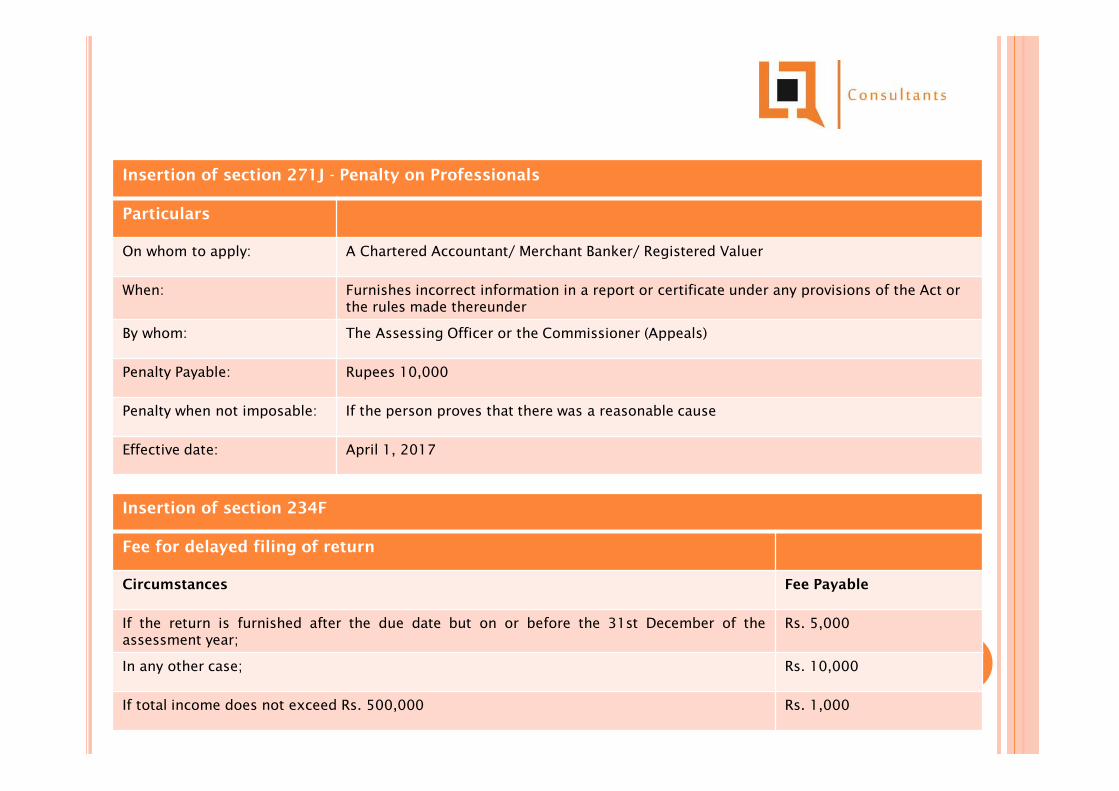

Insertion of section 271J - Penalty on Professionals

Particulars

On whom to apply: A Chartered Accountant/ Merchant Banker/ Registered Valuer

When: Furnishes incorrect information in a report or certificate under any provisions of the Act orthe rules made thereunder

By whom: The Assessing Officer or the Commissioner (Appeals)

Penalty Payable: Rupees 10,000

Penalty when not imposable: If the person proves that there was a reasonable cause

Effective date: April 1, 2017

Insertion of section 234F

Fee for delayed filing of return

Circumstances Fee Payable

If the return is furnished after the due date but on or before the 31st December of theassessment year;

Rs. 5,000

In any other case; Rs. 10,000

If total income does not exceed Rs. 500,000 Rs. 1,000

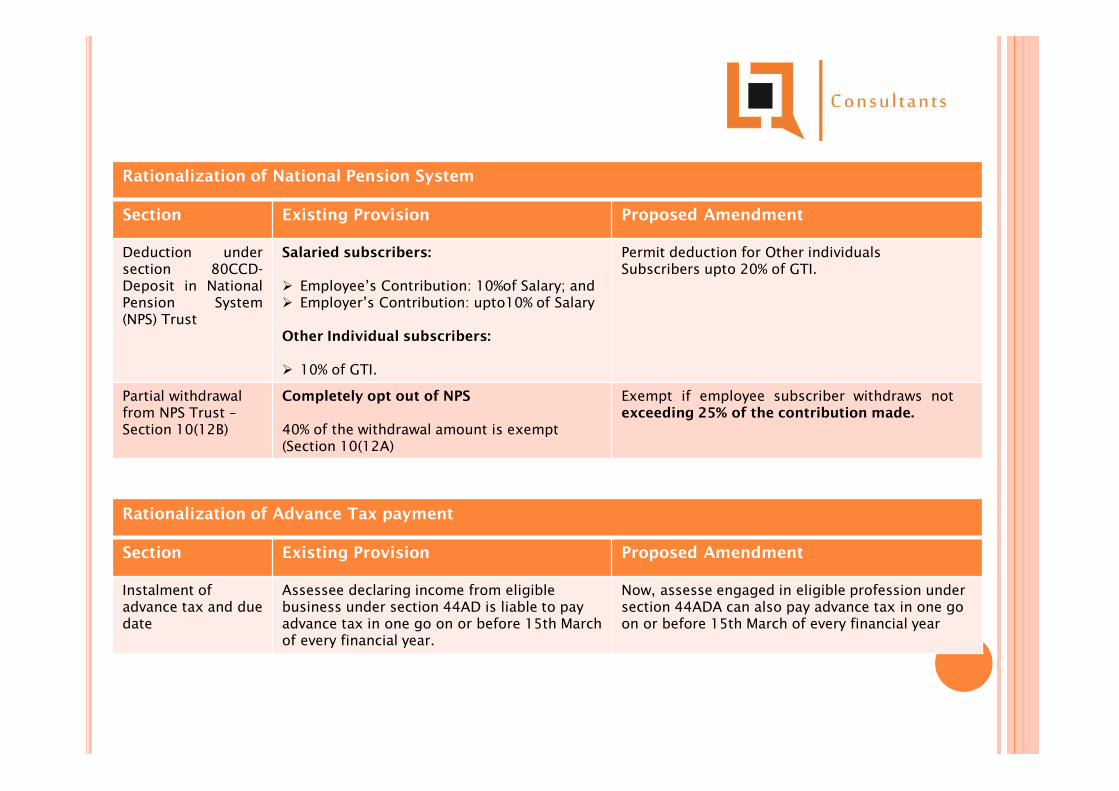

Rationalization of National Pension System

Section Existing Provision Proposed Amendment

Deduction undersection 80CCD-Deposit in NationalPension System(NPS) Trust

Salaried subscribers:

Employee’s Contribution: 10%of Salary; and Employer’s Contribution: upto10% of Salary

Other Individual subscribers:

10% of GTI.

Permit deduction for Other individualsSubscribers upto 20% of GTI.

Partial withdrawalfrom NPS Trust –Section 10(12B)

Completely opt out of NPS

40% of the withdrawal amount is exempt(Section 10(12A)

Exempt if employee subscriber withdraws notexceeding 25% of the contribution made.

Rationalization of Advance Tax payment

Section Existing Provision Proposed Amendment

Instalment ofadvance tax and duedate

Assessee declaring income from eligiblebusiness under section 44AD is liable to payadvance tax in one go on or before 15th Marchof every financial year.

Now, assesse engaged in eligible profession undersection 44ADA can also pay advance tax in one goon or before 15th March of every financial year

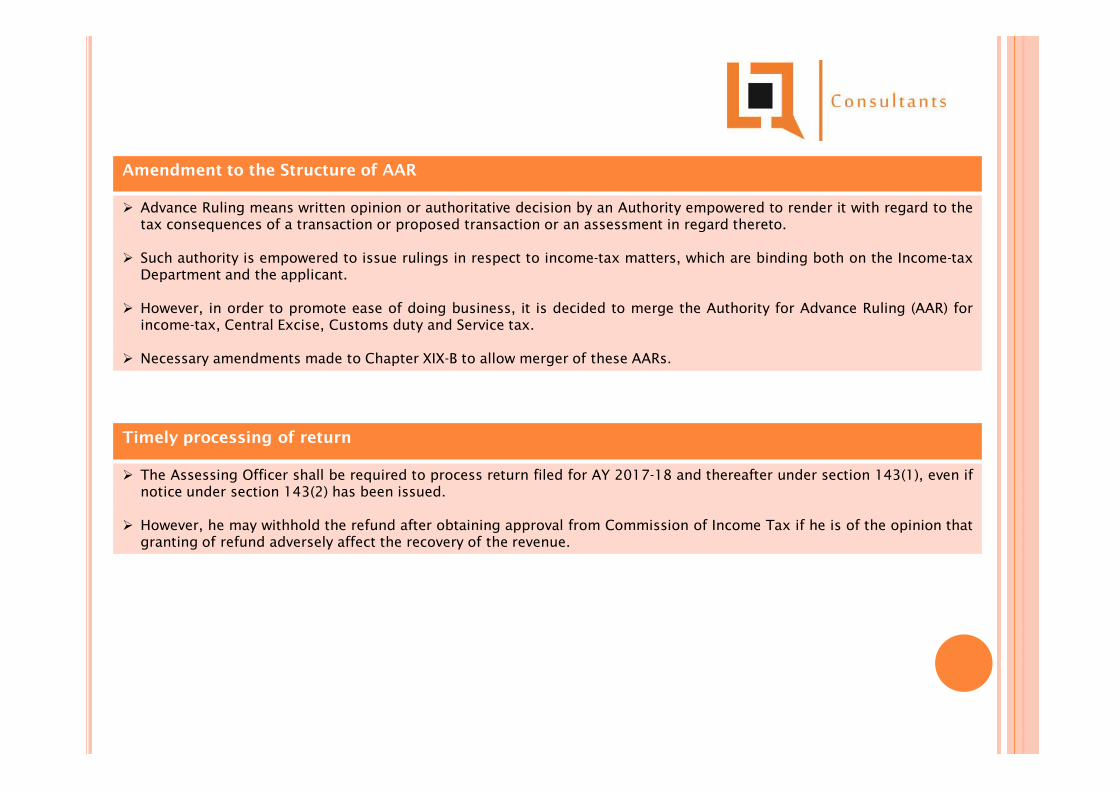

Amendment to the Structure of AAR

Advance Ruling means written opinion or authoritative decision by an Authority empowered to render it with regard to thetax consequences of a transaction or proposed transaction or an assessment in regard thereto.

Such authority is empowered to issue rulings in respect to income-tax matters, which are binding both on the Income-taxDepartment and the applicant.

However, in order to promote ease of doing business, it is decided to merge the Authority for Advance Ruling (AAR) forincome-tax, Central Excise, Customs duty and Service tax.

Necessary amendments made to Chapter XIX-B to allow merger of these AARs.

Timely processing of return

The Assessing Officer shall be required to process return filed for AY 2017-18 and thereafter under section 143(1), even ifnotice under section 143(2) has been issued.

However, he may withhold the refund after obtaining approval from Commission of Income Tax if he is of the opinion thatgranting of refund adversely affect the recovery of the revenue.

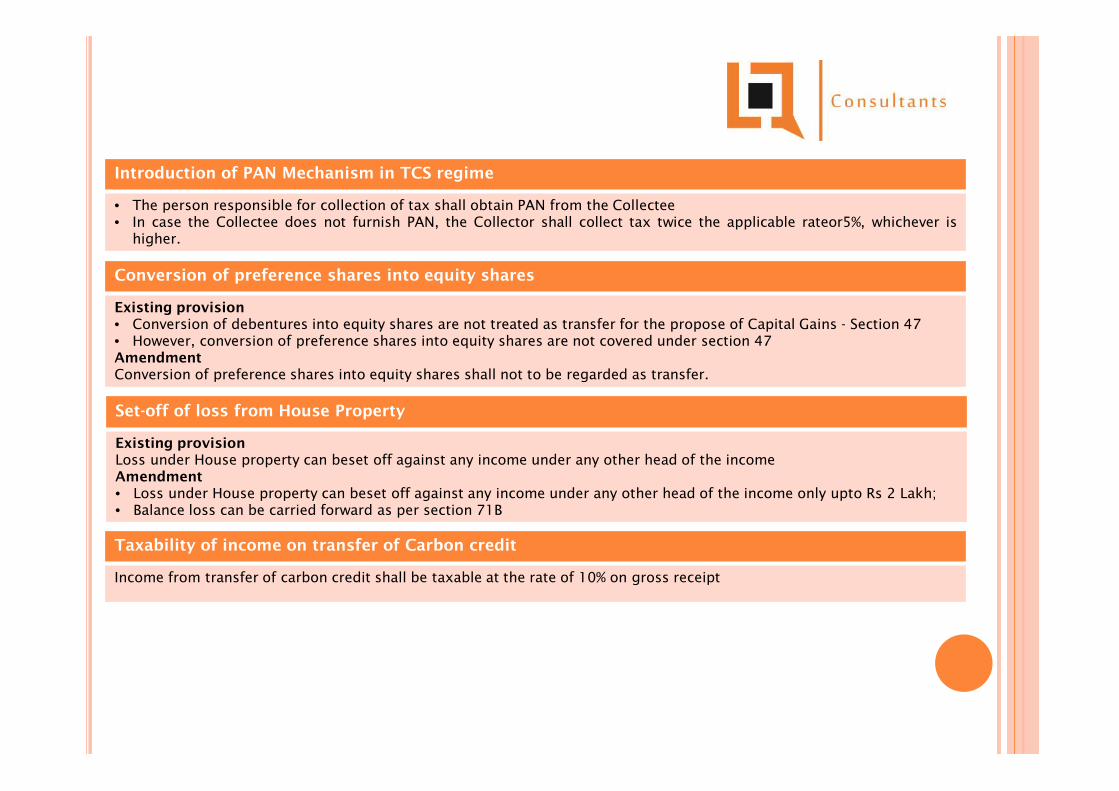

Introduction of PAN Mechanism in TCS regime

• The person responsible for collection of tax shall obtain PAN from the Collectee• In case the Collectee does not furnish PAN, the Collector shall collect tax twice the applicable rateor5%, whichever is

higher.

Conversion of preference shares into equity shares

Existing provision• Conversion of debentures into equity shares are not treated as transfer for the propose of Capital Gains - Section 47• However, conversion of preference shares into equity shares are not covered under section 47AmendmentConversion of preference shares into equity shares shall not to be regarded as transfer.

Set-off of loss from House Property

Existing provisionLoss under House property can beset off against any income under any other head of the incomeAmendment• Loss under House property can beset off against any income under any other head of the income only upto Rs 2 Lakh;• Balance loss can be carried forward as per section 71B

Taxability of income on transfer of Carbon credit

Income from transfer of carbon credit shall be taxable at the rate of 10% on gross receipt

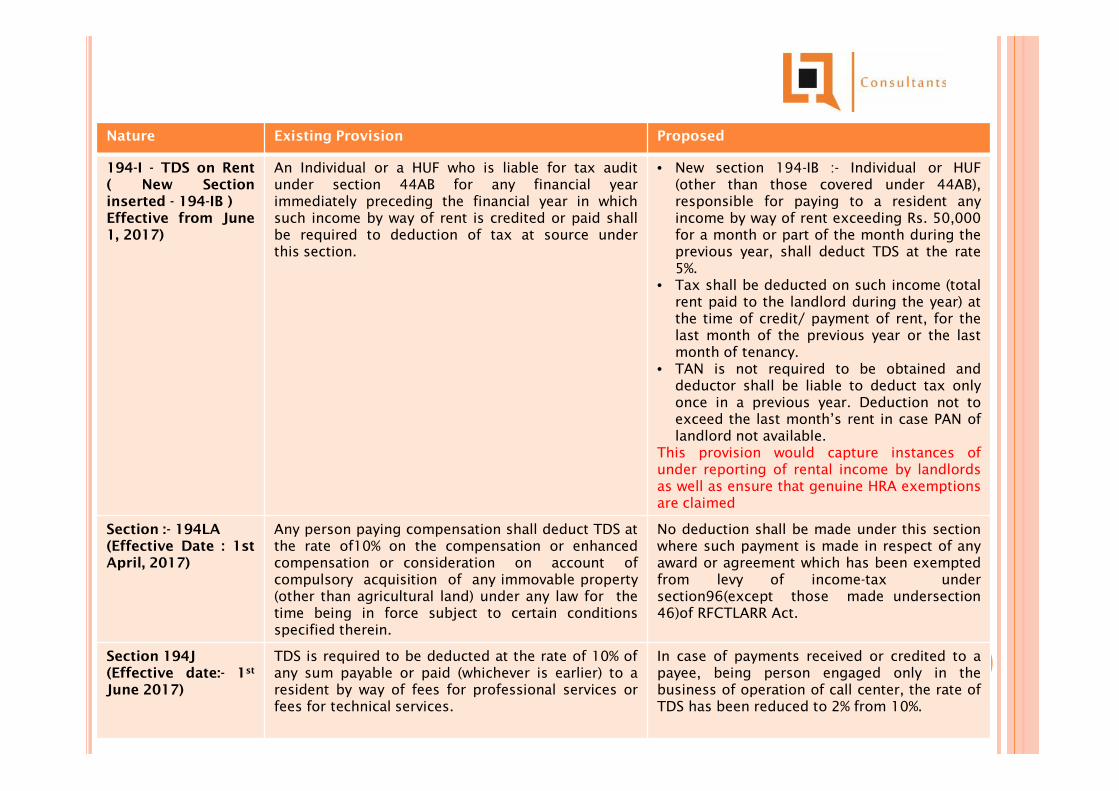

Nature Existing Provision Proposed

194-I - TDS on Rent( New Sectioninserted - 194-IB )Effective from June1, 2017)

An Individual or a HUF who is liable for tax auditunder section 44AB for any financial yearimmediately preceding the financial year in whichsuch income by way of rent is credited or paid shallbe required to deduction of tax at source underthis section.

• New section 194-IB :- Individual or HUF(other than those covered under 44AB),responsible for paying to a resident anyincome by way of rent exceeding Rs. 50,000for a month or part of the month during theprevious year, shall deduct TDS at the rate5%.

• Tax shall be deducted on such income (totalrent paid to the landlord during the year) atthe time of credit/ payment of rent, for thelast month of the previous year or the lastmonth of tenancy.

• TAN is not required to be obtained anddeductor shall be liable to deduct tax onlyonce in a previous year. Deduction not toexceed the last month’s rent in case PAN oflandlord not available.

This provision would capture instances ofunder reporting of rental income by landlordsas well as ensure that genuine HRA exemptionsare claimed

Section :- 194LA(Effective Date : 1stApril, 2017)

Any person paying compensation shall deduct TDS atthe rate of10% on the compensation or enhancedcompensation or consideration on account ofcompulsory acquisition of any immovable property(other than agricultural land) under any law for thetime being in force subject to certain conditionsspecified therein.

No deduction shall be made under this sectionwhere such payment is made in respect of anyaward or agreement which has been exemptedfrom levy of income-tax undersection96(except those made undersection46)of RFCTLARR Act.

Section 194J(Effective date:- 1st

June 2017)

TDS is required to be deducted at the rate of 10% ofany sum payable or paid (whichever is earlier) to aresident by way of fees for professional services orfees for technical services.

In case of payments received or credited to apayee, being person engaged only in thebusiness of operation of call center, the rate ofTDS has been reduced to 2% from 10%.

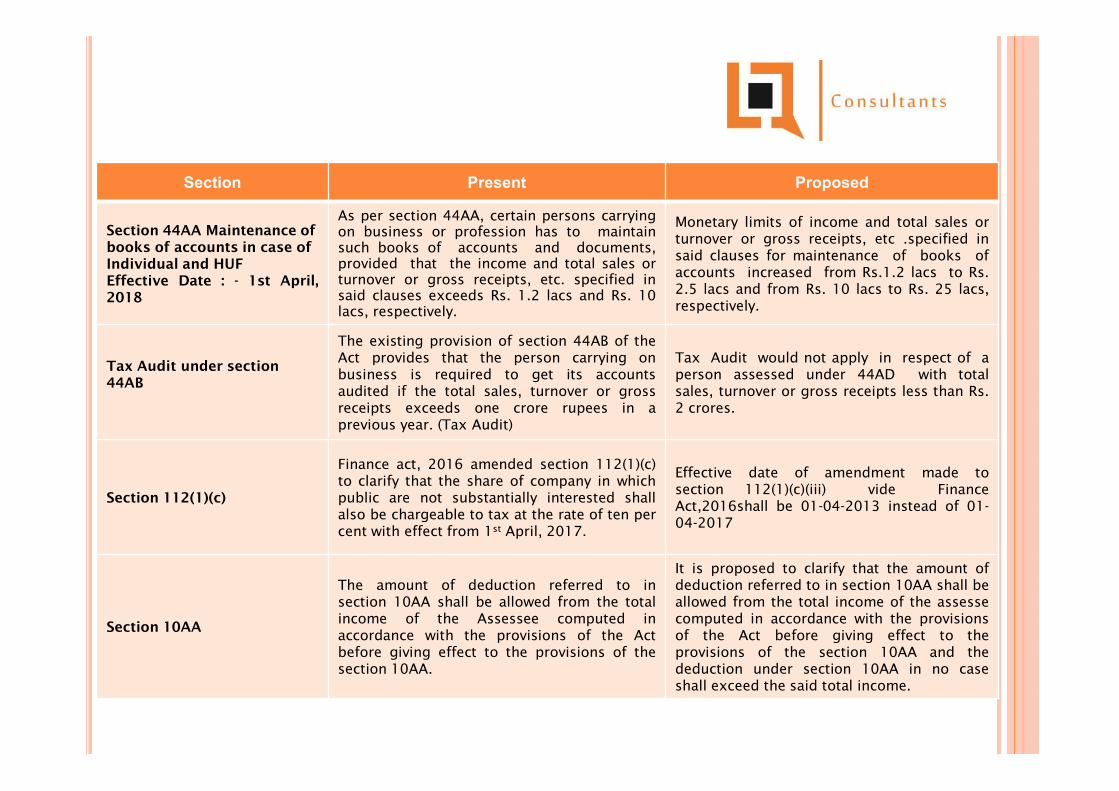

Section Present Proposed

Section 44AA Maintenance ofbooks of accounts in case ofIndividual and HUFEffective Date : - 1st April,2018

As per section 44AA, certain persons carryingon business or profession has to maintainsuch books of accounts and documents,provided that the income and total sales orturnover or gross receipts, etc. specified insaid clauses exceeds Rs. 1.2 lacs and Rs. 10lacs, respectively.

Monetary limits of income and total sales orturnover or gross receipts, etc .specified insaid clauses for maintenance of books ofaccounts increased from Rs.1.2 lacs to Rs.2.5 lacs and from Rs. 10 lacs to Rs. 25 lacs,respectively.

Tax Audit under section44AB

The existing provision of section 44AB of theAct provides that the person carrying onbusiness is required to get its accountsaudited if the total sales, turnover or grossreceipts exceeds one crore rupees in aprevious year. (Tax Audit)

Tax Audit would not apply in respect of aperson assessed under 44AD with totalsales, turnover or gross receipts less than Rs.2 crores.

Section 112(1)(c)

Finance act, 2016 amended section 112(1)(c)to clarify that the share of company in whichpublic are not substantially interested shallalso be chargeable to tax at the rate of ten percent with effect from 1st April, 2017.

Effective date of amendment made tosection 112(1)(c)(iii) vide FinanceAct,2016shall be 01-04-2013 instead of 01-04-2017

Section 10AA

The amount of deduction referred to insection 10AA shall be allowed from the totalincome of the Assessee computed inaccordance with the provisions of the Actbefore giving effect to the provisions of thesection 10AA.

It is proposed to clarify that the amount ofdeduction referred to in section 10AA shall beallowed from the total income of the assessecomputed in accordance with the provisionsof the Act before giving effect to theprovisions of the section 10AA and thededuction under section 10AA in no caseshall exceed the said total income.

Section:- 197A(Amendment) (Effective

date: 1st June 2017)

TDS is not required to be deducted, if therecipient of certain payments on which tax isdeductible furnishes to the payer a self-declaration in prescribed form no. 15G/15Hdeclaring that the tax on his estimated totalincome of the relevant previous year would be nil.

Insurance commission payment as referredin section 194D is now being coveredwithin the ambit of section 197A.

Nature Existing Provision Proposed

115BBDA - Tax onDividend received from

Domestic Company(Effective from April 1,

2018)

Dividend in excess of Rs. 10 lacs is chargeable totax at the rate of 10%.:- Section Applicable toresident individual, HUF or firm.

Provision extended to all residentassesses except domestic company andcertain funds, trusts, Institution.

24

LEGAL QUOTIENT CONSULTANTSTransfer Pricing | International Taxation

ABOUT US

We are a Delhi based consulting firm founded by Big4 alumnus and are focused to offer servicesin the field of Transfer Pricing. We aim to provide supreme, effective and unparalleled solutionsfor the Assessees who are involved in International/ Specified Domestic Transactions (“SDT”) asper the provisions of Income Tax laws in India. We assist our clients in the computation of Arm’sLength Price(ALP) and preparation of reports/documentations (Transfer pricing study and form3CEB).

We are a group of professionals, combining unmatched experience in issues / cases relatedto Transfer Pricing across various industries namely manufacturing, ITES, Software development,hospitality, tours and travel, consumer goods, heavy engineering goods etc;

Our services include:

•Transfer Pricing compliance and Documentation;

•Structuring the Business Model of the company (Transfer Pricing);

•Transfer Pricing Advisory as per the Global Arrangements;

•Representation before the Tax Authorities/Dispute Resolution Panel;

•Advance Pricing Agreement (“APA”)/ Mutual Agreement Procedure;

•Transfer Pricing risk evaluation;

•Safe Harbour Rules / Thin Capitalization; and

•FIN 48 Assistance (“USA Compliance”)

Legal Quotient Consultants

Add: B-19, Shakti Nagar Extn., Ashok Vihar Phase – 3, Delhi – 110052

Ph: 011- 65909030 | +91-9873681488 | +91-989909930 | +91-9999934558

Email: [email protected]

Web: www.LQconsultants.com