luxury goods capstone

TRANSCRIPT

Foreward

This research project was conducted as a part of a Georgetown University Executive MBA program. We would like to dedicate this work to our extraordinary learning journey and our fearless leader, Professor Dong. He has provided remarkable guidance, and more importantly, inspired us to think differently.

Sincerely,

Alison Elk, Robert Goodman, Dan Meyers, Nathan Ruiz, Damola St.Daniels, Deanna Siller, and Oneza Sohel

OUR FEARLESS ADVISOR

ARTHUR DONG

PROFESSOR

OUR TEAM

DEANNA SILLER ONEZA SOHEL

DAN MEYERS NATHAN RUIZ

DAMOLA ST.DANIELS

ROBERT GOODMAN ALISON ELK

Alison Elk, International Program Manager, United States NavyMs. Elk successfully manages a portfolio of Standard Missile Navy programs in excess of $50M. She has built a strong reputation for consistently delivering outstanding results in which she most recently was instrumental in securing $640M for a new program for Japan.

A goal-driven leader with a proven work ethic, Ms. Elk has completed over 20 trips to Asia in the past four years while earning her graduate degrees. It was her global business acumen, team leadership, and executive stakeholder management that secured the Department of Defense approval for the first international ballistic missile interceptor maintenance facility. Ms. Elk is highly equipped to resolve problems with great efficiency across multiple domains. She attributes her professional success to making smart, empathetic decisions while resolving conflict, and evolving her emotional agility. Ms. Elk believes that success in any market can be achieved through leadership, skill alignment, and teamwork.

In addition to her professional accomplishments, Ms. Elk is a board member advisor on the Tewaaraton Foundation. This non-profit organization annually recognizes the most outstanding men’s and women’s NCAA lacrosse players; honors the Native American historical and contemporary contributions to the game; and provides scholarships to Native American students who play lacrosse.

Robert Goodman, Director of Business Intelligence & Analytics, Georgetown UniversityMr. Goodman leads service delivery of Business Intelligence & Analytics solutions across Georgetown University’s enterprise. His team contributed to technology modernization efforts which were awarded CIO 100 by CIO Magazine in 2014 and Elite 100 Winners by InformationWeek in 2015. Working across multiple campuses and thousands of end-users, his team supports projects related to data governance, data quality, enterprise application integration, analytics, and reporting capabilities. At present, he is working on a finance/HR-centric BI project using the Workday ERP system and IBM Cognos.

Mr. Goodman consults regularly with KPMG and Bain & Co. on matters of business intelligence and enterprise application integration. He is also a frequent speaker at industry-related events. Most recently, he led a conference workshop in Austin, TX, where he discussed the “People Dilemma of Analytics.” Prior to Georgetown, Mr. Goodman worked as a Microsoft® Gold Certified partner and led a large global delivery practice.

Mr. Goodman is known for his unflappable demeanor and ability to relate to his team, both of which allow him to effectively lead his teams through the many challenges of change management and find creative solutions to complex issues.

Mr. Goodman holds an advanced degree in business administration, is an experienced IT and Project Management Professional (PMP)®, and has been formally trained as a computer and data scientist.

Dan Meyers, Vice President, DCI Group LLCDan Meyers is a communications, crisis, and public affairs consultant with experience managing local, federal, and global public affairs challenges. Dan consults for clients ranging from small and mid-cap enterprises to Fortune 100 companies. His strengths are strategy and integrated management. Dan’s experiences include overseeing every aspect of large- scale projects and campaigns from strategy, polling, and message development to day-to-day execution.

Dan has experience in developing winning solutions that involve grassroots outreach, national coalition building, third party engagement, and government relations strategies. He has managed federal and state legislative, regulatory, and ballot efforts including one of the largest statewide gaming ballot initiatives in 2012 and a successful local ballot initiative in 2009. Recently, Dan led the brand redevelopment of his public affairs firm’s online presence in 2015.

Dan’s political expertise hails from the most local levels to presidential politics. He was one of NYC Mayor Rudy Giuliani’s presidential campaign’s first employees, serving in various capacities including special assistant to campaign manager, Mike DuHaime and a personal aide to the Mayor and his wife. Dan worked at the Republican National Committee during the 2006 midterms and served President George W. Bush in foreign and domestic venues as a communications advance representative.

He is a member of the Board of Trustees for the Miss America Organization and President of the Board of Directors of Project Right Side.

Nathan Ruiz, Senior Consultant, IntelliwareMr. Ruiz is a strategic ambassador with a wide range of work experience, including industrial and physical security, inter-agency cooperation, counterintelligence, counterterrorism, and foreign liaison. Mr. Ruiz is at his finest when bringing leaders together to collaborate and work through highly complex, sensitive issues.

In his transition to the private sector, Mr. Ruiz built a relationship management program as part of a strategic relaunch of the FBI’s partnership with Fortune 500 companies. He helped grow the current membership from 297 to 387 companies, and he regularly interfaces with chief security officers from Fortune 100 companies such as Boeing, Disney, United, and Microsoft. Mr. Ruiz planned and facilitated four strategic off-site meetings with key leaders, laying the foundation for the new program’s governance and implementation. His ongoing relationship cultivation with executive leadership in business provides critical voice of the customer data, driving government decisions.

A 10-year veteran of the U.S. Air Force, he served as a Federal Agent with the Air Force Office of Special Investigations (AFOSI), leading the high-profile office at the U.S. Embassy in Paris, where he increased national-level liaison efforts with French law enforcement, intelligence, and military forces. Mr. Ruiz was hand-selected as head of the elite security protection detail assigned to the Chief of Staff, USAF and has deployment experience in the Middle East, Southwest Asia and Africa. He lived and worked abroad for 10 years and has deep expertise forming and leading teams on all seven continents.

Damola St.Daniels, Managing Director, DBSMr. St.Daniels currently heads several departments within the bureau of consular affairs, consular systems and technology on behalf of Vistronix, Inc. at the U.S. Department of State. As a leader in the federal government space, he oversees diverse technology projects and advises federal government agencies on IT security practices. His broad and deep knowledge of IT coupled with his prowess in problem solving ensures that critical applications, systems, and infrastructure are constantly maintained at optimum levels. Federal government agencies and private companies alike rely on Mr. St.Daniels for his leadership and expertise concerning all things IT from application development, testing, vendor management, IT strategy, disaster planning and recovery, penetration testing, and database management to independent verification and validation (IV&V).

Mr. St.Daniels cultivates key partnerships that help drive current development and implementation agendas. His entrepreneurial spirit and direct attention to detail deliver impressive results such as 99% application and product defect free rate and 100% performance to SLA standards. Mr. St.Daniels was privileged to serve active duty in the U.S. Navy as a project manager for a sea-deployed strike fighter attack squadron (VFA-146). He was responsible for ensuring 12 FA-18C fighter aircraft were mission ready alone with the avionics and maintenance divisions. His strategic planning and tactical execution directly contributed to his squadron’s receipt of multiple LTJG Bruce Carrier awards for maintenance excellence as well as many campaign medals.

Deanna Siller, Partner, GenslerMs. Siller is a partner at Gensler, one of the world’s leading architecture and interior design firms. One of Gensler’s top global brand design leaders, Ms. Siller brings strategic insights that result in innovative and unique user experiences that foster the human connection. She immerses herself in her clients’ business in order to unleash the hidden potential of a place, an idea, or an experience. As an expert storyteller, she helps companies develop differentiated, compelling, and cohesive brand strategies. As a member of the management committee, she works closely with Gensler’s board in the development of hospitality, retail, sports, and brand practice areas.

Ms. Siller is a sought after speaker. Whether speaking at L’Oreal’s Inspiration Day, SATE conference for Themed Entertainment Association, as guest lecture at the University of Pennsylvania, or a panelist at ULI’s Washington Real Estate Trends Conference, she brings a unique point of view that challenges the status quo.

Her work has earned numerous awards from the American Institute of Graphic Arts, International Interior Design Association, American Institute of Architects, Society of Environmental Graphic Design, and Washington Building Congress.

Ms. Siller served as chairman of the board at Dance Place and believes in using her expertise to impact her local community. She is a USGBC LEED Accredited Professional and a member of the Society of Environmental Graphic Design.

Oneza Sohel, RAN Optimization Manager, AT&TMs. Sohel is a proven leader domestically and internationally, across different verticals, and impacting different business processes. She is known for her problem solving skills and vision that demonstrate her ability to lead strategy from concept to implementation. She brings 13 years of experience in global business development, operational excellence, delivering strategic solutions, and team building.

She is highly skilled in leading global organizations through the optimization of business operations to take full advantage of technology innovation, streamlining procedures to provide cost efficient processes and technological innovations.

Currently, in her role with AT&T Mobility, Ms. Sohel handles the day-to-day pressures of keeping the network running, with key partners and collaborators. Her ability to keep calm under high-profile events like the presidential inauguration and Pope’s visit and her ability to influence people from senior levels to a new hire has made her a success.

From supporting mobile world congress in Barcelona to designing the China mobile network, Ms. Sohel has been collaborating with telecom experts across the world and leveraging the best practices in order to enhance productivity, identify opportunities, and provide recommended solutions for continuous improvement.

TABLE OF CONTENTS

TEAM HYPOTHESIS WHAT IS LUXURY THE POWER OF LUXURY US COMPARISON AND ANALYSIS FINDINGS AND KEY ANALYSIS INDUSTRY EXPERT INSIGHTS CHINESE CULTURE GLOBAL LUXURY MARKET CHINESE LUXURY MARKET EVOLUTION OF THE ASIAN

LUXURY CONSUMER MARKET SEGMENT OVERVIEWS

WINE & SPIRITS LUXURY AUTOS HOSPITALITY COSEMETICS

FINAL THOUGHTS

PRESENTATION EXECUTIVE SUMMARY HYPOTHESIS OVERVIEW WHY STUDY THE CHINESE

LUXURY MARKET? GLOBAL LUXURY MARKET EVOLUTION OF THE ASIAN

LUXURY CONSUMER MARKET SEGMENT OVERVIEWS

WINE & SPIRITS LUXURY AUTOS HOSPITALITY COSEMETICS

SUMMARY OF FIELD RESEARCH FINDINGS AND KEY ANALYSIS US COMPARISON AND ANALYSIS CONCLUSIONS ADDENDA

PAPER

OUR HYPOTHESIS The continued growth of the Chinese economy and China’s voracious appetite for luxury goods

will provide the impetus for further growth in luxury good consumption.

SCARCITY

DESIRE

AUTHENTIC

TELLS A STORY

SUPERIOR CRAFTMANSHIP

WHAT IS LUXURY?

ALL THINGS PEOPLE

WANT… AND NOTHING

THEY NEED.

WORLDWIDE LUXURY MARKETS COLLECTIVELY SURPASSING ONE TRILLION IN 2015

POWER & INFLUENCE

The luxury industry surpassed €1 trillion in retail sales value in 2015 and delivered healthy growth of 5% year over year (at constant exchange rates), driven primarily by luxury cars (8%), luxury hospitality (7%) and Þne arts (6%).

MARKET GROWTH

Global currency fluctuations and continued purchases by “borderless consumers,” the personal luxury goods market—the “core of the core” of luxury – grew more than €250 billion in 2015. That represents 13% growth over 2014 at current exchange rates, while real growth (at constant exchange rates) has eased to only 1% to 2%. The slowdown conÞrms a shift to a “new normal” of lower sales growth in the personal luxury goods market.

NEW NORMAL

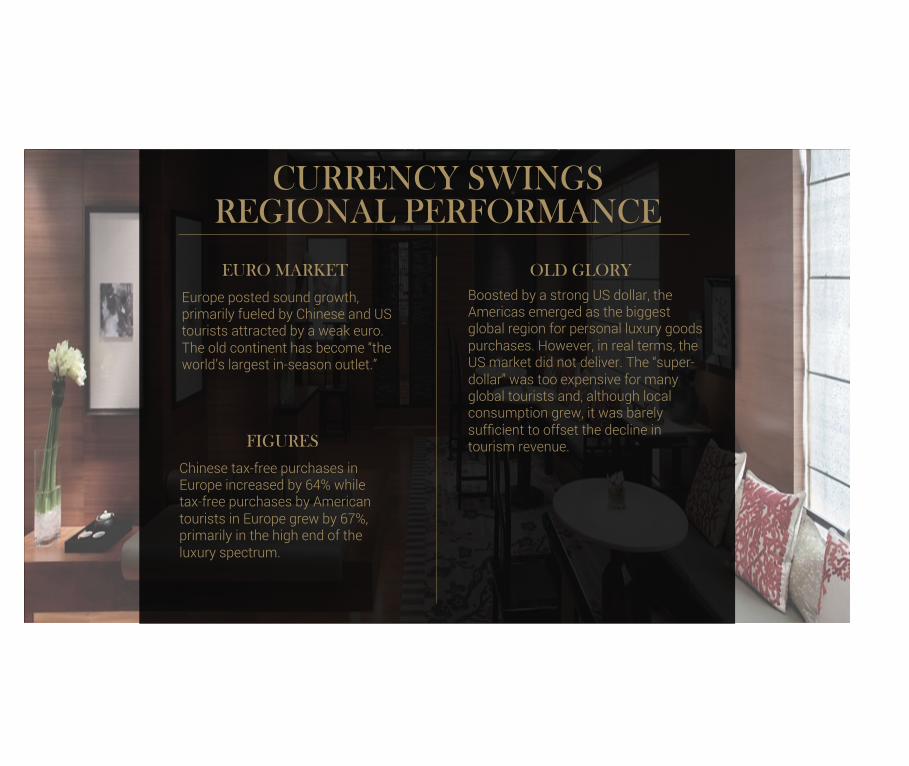

CURRENCY SWINGS REGIONAL PERFORMANCE

Europe posted sound growth, primarily fueled by Chinese and US tourists attracted by a weak euro. The old continent has become “the world’s largest in-season outlet.”

EURO MARKET Boosted by a strong US dollar, the Americas emerged as the biggest global region for personal luxury goods purchases. However, in real terms, the US market did not deliver. The “super-dollar” was too expensive for many global tourists and, although local consumption grew, it was barely sufÞcient to offset the decline in tourism revenue.

OLD GLORY

Chinese tax-free purchases in Europe increased by 64% while tax-free purchases by American tourists in Europe grew by 67%, primarily in the high end of the luxury spectrum.

FIGURES

• Mainland Chinese tourists buying power impacted.

• Luxury goods market is less impacted by currency fluctuations.

• Lower-end luxury consumers consider other destinations with more favorable currency exchange rates.

CURRENCY DEPRECIATION

ANTI-CORRUPTION MOVEMENT

LUXURY ONLINE SALES

GLOBE-TROTTERS

• The government’s anti-corruption drive has greatly affected gift giving in China

• A survey by Hurun shows that gift giving among China’s wealthiest individuals fell by 5% yoy in 2014*

• According to Bain’s report, cross-border and overseas websites are taking about 12% of all Chinese luxury goods spending

• Luxury globe-trotters have fueled the performance of airport retail, which posted a 29% growth rate in current exchange rates (18% in constant exchange rates) and now accounts for 6% of the global luxury market.

01 02 03 04 SHIFTS IN THE CHINESE LUXURY MARKET

NEW GEOGRAPHIC MARKETS

With rapidly rising incomes, widely available luxury products, and shifting attitudes toward the display of wealth, more Chinese consumers than ever feel comfortable buying luxury goods.

Rapid urbanization and growing wealth beyond China’s largest cities are creating a number of geographic markets with sizable pools of luxury-goods consumers who are able to afford luxury goods in less expensive areas of the world.

SHIFTING ATTITUDES

GREATER SOPHISTICATION

Instead of buying luxury goods at department stores, shopping malls, or arranging a deal with a daigou merchant, Chinese shoppers are making purchases through websites like JD, Tmall, Net-A Porter.com, ShopBop, and Harrods.

With the surge in the number of luxury stores, fashion magazines, and websites and the use of social media, Chinese consumers are now familiar with nearly twice as many brands as they were in 2008.

ONLINE SHOPPING

RESULT OF LUXURY SHIFTS

Source:McKinsey

DEPRECIATION OF THE EURO

Source: Bain & Co.

CHINESE CONSUMERS: ONE-THIRD OF THE GLOBAL MARKET

Source: Bain & Co.

LUXURY GOODS SPENDING

Source: Bain & Co.

ASIA UNITED STATES

mature luxury market

.

$2,400 avg. spend

per shopping trip

24% global luxury share

CHINA AND UNITED STATES: LUXURY COMPARISON

emerging luxury market

$7,200 avg. spend

per shopping trip

31% global luxury share

frequent ritual

occasional indulgence

80% luxury

shopping abroad

30% luxury

shopping abroad

AMERICAS EMERGED AS THE BIGGEST GLOBAL REGION FOR PERSONAL LUXURY GOODS PURCHASES

23.1

7.9

4.8 4.1 3.8 3.8

2.7 2.0

1.0 0.7 0.1

US China UK South Korea France Hong Kong Germany Middle East Italy Japan Russia

Personal luxury goods: growth contribution, by market, in absolute value, 2009-2-14E (€billions)

3X €15.0B

CHINA LUXURY GOODS SALES

2014

€64.9B US LUXURY

GOODS SALES 2014

Sources: Euromonitor International and Bain & Co.

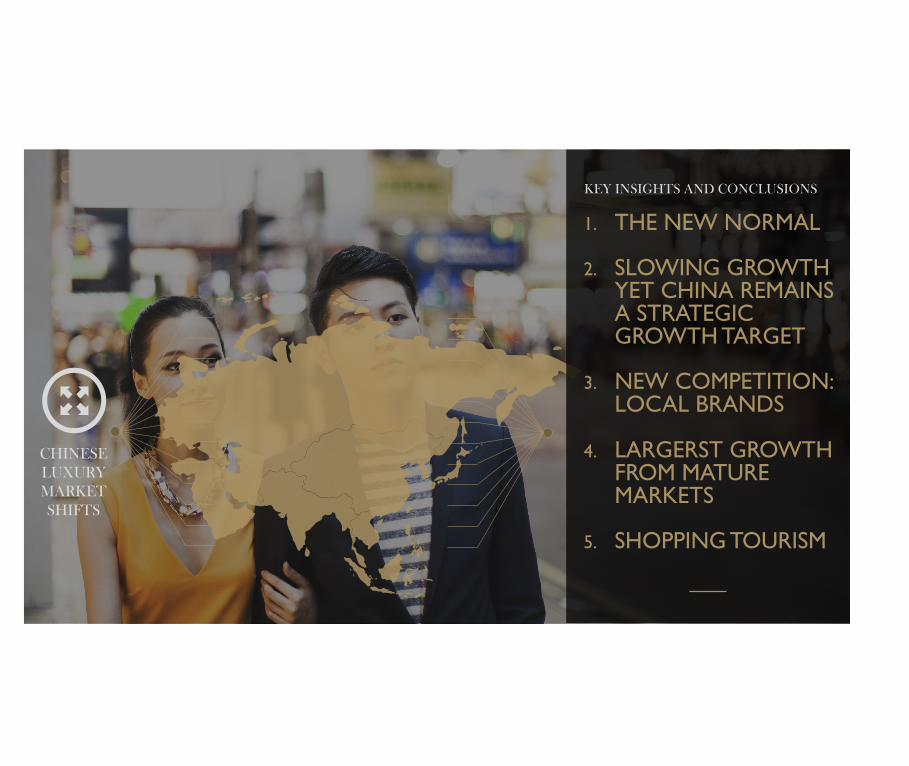

CHINESE LUXURY MARKET SHIFTS

1. THE NEW NORMAL

2. SLOWING GROWTH YET CHINA REMAINS A STRATEGIC GROWTH TARGET

3. NEW COMPETITION: LOCAL BRANDS

4. LARGERST GROWTH FROM MATURE MARKETS

5. SHOPPING TOURISM

KEY INSIGHTS AND CONCLUSIONS

• Global luxury market • Global trends in luxury shopping • Luxury consumer: buying behaviors • Chinese and US comparison

RESEARCH

HOW WE GOT THERE: OUR APPROACH

• Chinese luxury market: Hong Kong and Macau

IMMERSE

• 5 luxury segments • 9 industry experts

DISCOVER • Key Findings • Conclusions

STRATEGIZE

INDUSTRY EXPERT INSIGHTS

“Only 7% of Chinese have passports.

Imagine the spending power as this grows.”

Bill Weidner Chairman and CEO

Global Gaming Asset Management

“The luxury consumer is still buying; however, they are buying

differently.”

Chris Exline CEO, Asia PaciÞc Home Essentials

“The world is the luxury consumers

shopping experience.”

Kevin Roche Senior Vice President, Global Design

DFS Group Ltd.

“Think about it in terms of desire.

Never compete on price. Compete

on desire.”

Mark del Rosso Executive Vice President

Audi

“Economic downturn, price competition from

e-commerce, and oversea purchase are

the main challenges for luxury market.”

Mr. JianHua Qian CEO

JZ motors

“While there is normal fluctuation in the

luxury market, the recent market growth is not sustainable. There

is a new normal.”

Edward Cheung CEO Greater China

Cushman & WakeÞeld

“We offer the highest view. This is luxury too… not just

goods.”

Pierre Perusset General Manager

Ritz Carlton, Hong Kong

“Asia-Pacific region is projected to contain

60% of the world’s 4.3 billion middle class. 1.4

of the 4.3 billion are contributed to China.”

Fabrice Weber President APAC

Estée Lauder

“Once the only portal for foreign businesses in China, Hong Kong must now evolve and adapt to political and economic reforms.”

Andrew Shaw Chief Economic/Political Section

Consulate General of the United States

Chinese culture

CULTURAL

CONTEXT

In the 18th Century China had the richest land and was the most urbanized country in the world. Political reforms closed boarders and isolationism took hold.

SHEER SIZE

Given history, Chinese are skeptical of the future compared to the US. They save a staggering 40%-50% compared to 3%-5% in the US.

CULTURE OF SAVING

1978 Chinese Economic Reforms introduced market principles. This decentralized agriculture, opened up FDI, loosened price controls and brought 600 million out of poverty.

ECONOMIC REFORMS

LUXURY MARKET

CHINESE GLOBAL LUXURY

MARKET

LUXURY GOODS POWER ON

-8

-6

-4

-2

0

2

4

6

8

10

12

14

0

50

100

150

200

250

300

350

400

450

500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Global Luxury Sales (US $ Billion) and Growth 2008 -‐2018

$ Billion % Y-‐O-‐Y Value Growth

Source: Euromonitor International

PERFORMANCE BY COUNTRY 8.

2%

3.4%

2.9%

4.3%

0.1%

5.4%

11.1

%

9.4%

6.6%

10.3

%

8.5%

11.5

%

7.3%

10.5

%

20.7

%

11.8

%

7.4%

7.3%

8.6%

13.9

%

6.5%

8.6%

10.6

%

14.3

%

10.8

%

7.5%

8.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Top 100 China/Hong Kong France Italy Spain Switzerland United Kingdom United States Other Countries Axis Title

FY13 luxury goods sales growth FY13 net profit margin FY13 return on assets FY11-13 net sales CAGR

Source: Bain & Co.

LUXURY MARKET

€850 b 7%

growth

10% LUXURY

CARS

9% LUXURY

HOSPITALITY

Source: Bain & Co.

7% 2013

NEW NORMAL

SLOWER STEADY GROWTH

5% 2014

Source: Bain & Company

218 223

250-265

2013 2014 E 2017 F at constant rate of exchange

Market forecast for personal luxury goods ( € billions)

+2% (+5% at constant exchange rates)

+4%-6% at constant

exchange rates

CAGR, 204E-2017F

(%)

CHINA UNITED STATES

.

By 2031 $33.66 trillion

GDP By 2031

$35.26 trillion GDP

ROLE REVERSAL: CHINA AS THE LARGEST ECONOMY

Source: Bain & Co.

Deanna to design

TOP TEN LUXURY GOODS COMPANIES

Luxury goods sales rank FY13 Company Name Country of Origin

FY13 luxury goods sales

(US $mil)

FY13 total revenue

(US $mil)

FY13 luxury goods sales

growth* FY13 net

profit margin** FY13 return on assets*

FY11-13 luxury goods sales CAGR* ***

1 LVMH Moët Hennessy - Louis Vuitton SA France 21,761 387,171 0.0% 13.5% 7.1% 8.7%

2 Compagnie Financlere Richemont SA Switzerland 13,429 14,275 4.2% 19.4% 13.0% 8.9%

3 The Estée Lauder Companies Inc. United States 10,969 10,969 7.7% 11.0% 15.4% 6.3%

4 Chow Tai Fook Jewellery Group Limited Hong Kong 9,979 9,979 34.8% 9.6% 12.1% 17.0%

5 Luxottica Group SpA Italy 9,713 9,713 3.2% 7.5% 6.8% 8.4%

6 The Swatch Group Ltd. Switzerland 8,822 9,128 8.8% 22.8% 16.6% 9.9%

7 Kerling SA France 8,594 12,948 4.2% 0.4% 0.2% 14.7%

8 L'Oréal Luxe France 7,791 7,791 5.3% 14.7% 19.6% 10.5%

9 Ralph Lauren Corporation United States 7,459 7,450 7.3% 10.4% 12.7% 4.2%

10 PVH Corp. United States 6,200 8,186 42.0% 1.8% 1.2% 22.7%

Top 10 104,707 129,157 8.4% 11.7% 8.0% 10.2%

Top 100 214,231 247,624 8.2% 10.3% 8.6% 9.8%

Economic Concentration of Top 10 48.9% 29.5%

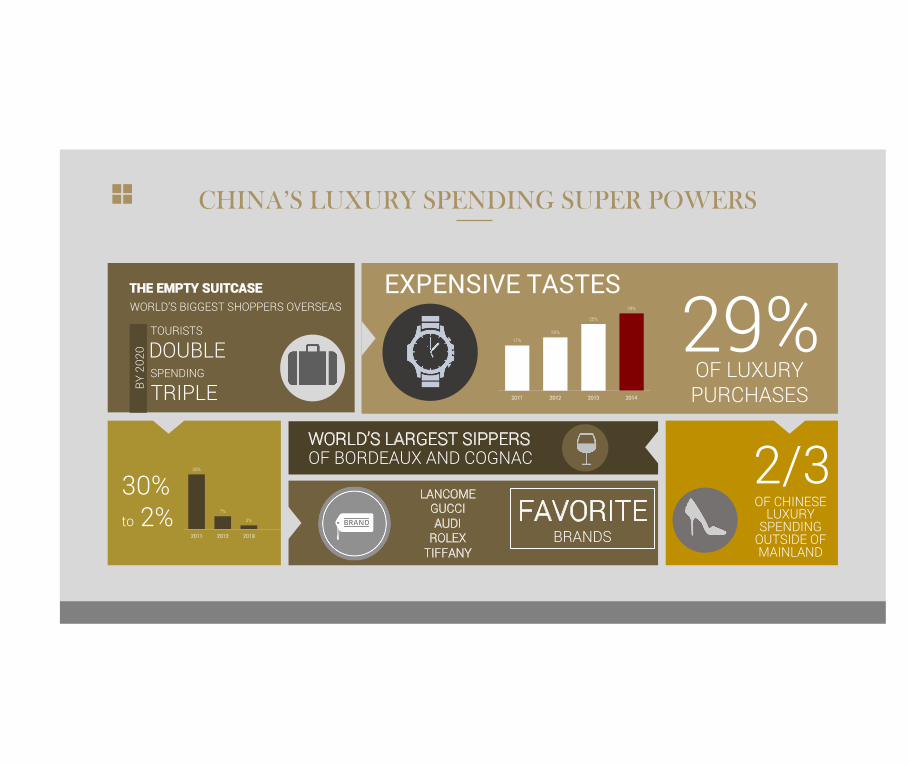

29% OF LUXURY PURCHASES

17%

20%

25%

29%

2011 2012 2013 2014

30% to 2%

THE EMPTY SUITCASE

WORLD’S LARGEST SIPPERS OF BORDEAUX AND COGNAC

LANCOME GUCCI AUDI

ROLEX TIFFANY

FAVORITE BRANDS

2/3

WORLD’S BIGGEST SHOPPERS OVERSEAS EXPENSIVE TASTES

DOUBLE TOURISTS

TRIPLE SPENDING

BY 2

020

30%

7%

2%

2011 2012 2013

OF CHINESE LUXURY

SPENDING OUTSIDE OF MAINLAND

CHINA’S LUXURY SPENDING SUPER POWERS

CHINA’S GROWTH SLOWS . 01

BRANDS SLOW EXPANSION 02

FROM HONG KONG TO JAPAN 03

TOP GIVE GROWTH MARKETS 04

LUXURY MARKET: 2016 FORECAST

Source: Euromonitor International

Shift in Asian consumption power from Hong Kong to Japan, as growing numbers of Chinese shoppers head to Japan.

US will be the biggest market, followed by Japan, South Korea, France and the UK.

Economic growth slows, consumers cautious about spending

Leading global brands such as LVMH, Gucci and Prada have

expanded rapidly but will slow their expansion plans..

BUYING ABROAD WHY ARE TWO-THIRDS OF THE LUXURY PRODUCTS BOUGHT ABROAD?

PRICE DISCREPANCY

INCREASE OF PERSONAL WEALTH

LIMITED PRODUCT SELECTION

IMPORTANCE OF THE COUNTRY OF ORIGIN

GIFT TRADITION

AUTHENTICITY OF THE PRODUCTS

GREATER EASE OF OBTAINING A VISA

OF THE ASIAN CONSUMER

EVOLUTION

ATTITUDES, LIFESTYLES AND BRAND PREFERENCE DIFFER

SEGMENT THE AFICIONADO THE EPICUREAN THE BLING KING THE BRAND SKEPTIC THE ASPIRANT

GENDER M:52% F:48% M: 54% F:40% M: 54% F:40% M: 51% F:49% M: 61% F:39%

DEMOGRAPHY

AVG Age : 32.3 MMI: ¥23,367 LUXURY SPEND: ¥32,981 SINGLE: 22% MARRIED: 78%

AVG Age : 32.6 MMI: ¥193,891 LUXURY SPEND: ¥28,631 SINGLE: 20% MARRIED: 80%

AVG Age : 32.4 MMI: ¥181,855 LUXURY SPEND: ¥23,367 SINGLE: 20% MARRIED: 80%

AVG Age : 33 MMI: ¥161,127 LUXURY SPEND: ¥19,066 SINGLE: 20% MARRIED: 80%

AVG Age : 31.9 MMI: ¥155,288 LUXURY SPEND: ¥16,525 SINGLE: 23% MARRIED: 77%

SOCIAL #1 99% POST ON WECHAT #2 98% POST ON

WECHAT #3 96% POST ON WECHAT #5 94% POST ON

WECHAT #4 95% POST ON WECHAT

LUXURY ECOMMERCE #1 18% HAVE BOUGHT LUXURY ONLINE

#3 15% HAVE BOUGHT LUXURY ONLINE

#2 17% HAVE BOUGHT LUXURY ONLINE

#2 17% HAVE BOUGHT LUXURY ONLINE

#3 15% HAVE BOUGHT LUXURY ONLINE

OS TRAVEL LOCAL #3 55% HAVE BOUGHT LUXURY IN HK, M, OR TW

#4 53% HAVE BOUGHT LUXURY IN HK, M, OR TW

#1 66% HAVE BOUGHT LUXURY IN HK, M, OR TW

#2 56% HAVE BOUGHT LUXURY IN HK, M, OR TW

#5 17% HAVE BOUGHT LUXURY IN HK, M, OR TW

OS TRAVEL LOCAL #1 40% HAVE BOUGHT LUXURY OS OTHERS

#2 31% HAVE BOUGHT LUXURY OS OTHERS

#3 26% HAVE BOUGHT LUXURY OS OTHERS

#4 23% HAVE BOUGHT LUXURY OS OTHERS

#5 6% HAVE BOUGHT LUXURY OS OTHERS

SCREEN MEDIA TIME #3 70% SCREEN-TIME CONSUMPTION #2 73% SCREEN-TIME

CONSUMPTION #1 76% SCREEN-TIME CONSUMPTION #3 70% SCREEN-TIME

CONSUMPTION #4 65% SCREEN-TIME CONSUMPTION

DIGITAL MEDIA TIME #1 50%DIGITAL0MEDIA CONSUMPTION TIME #1 50%DIGITAL0MEDIA

CONSUMPTION TIME #2 48%DIGITAL0MEDIA CONSUMPTION TIME #3 47%DIGITAL0MEDIA

CONSUMPTION TIME #4 45%DIGITAL0MEDIA CONSUMPTION TIME

FASHION ACUMEN #1 FASHION ACUMEN, INTEREST #2 FASHION

ACUMEN, INTEREST #3 FASHION ACUMEN, INTEREST #5 FASHION

ACUMEN, INTEREST #4 FASHION ACUMEN, INTEREST

LUXURY ATTITUDE

• HIGH KNOWLEDGE & SOPHISTICATION

• HAVE DEVELOPED OWN STYLE &TASTE

• ARE TREND-SETTERS & OPIN ION SHAPERS

• OBSESSED WITH LUXURY

• NOT BRAND-LOYAL

• FAD-LED & WANT TO TRY SOMETHING • ARE SOCIAL SHARERS

• LOW KNOWLEDGE BUT STRONG DESIRE TO IMPRESS

• PERCEIVE LUXURY AS A SYMBOL OF STATUS & ARE CONSPICUOUS

• PERCEIVED LUXURY AS OVERRATED

• WHEN THEY DO PURCHASE LUXURY, IT IS BECAUSE IT IS A REFLECTION OF QUALITY & CRAFTMANSHIP

• THE EMERGING SEGMENT

• LOVE LUXURY BUT HAVE VERY LITTLE KNOWLEDGE

• ARE STRONGLY INFLUENCED BY ADS, KOHL'S, & WOM

Source: Jing Daily | The Business of Luxury in China

TOP SPENDERS IN LUXURY AND FASHION-FORWARD IN OUTLOOK

THE AFICIONADO

SECOND HIGHEST PURCHASING POWER AND FASHION-CENTRIC LIFESTYLE

THE EPICUREAN

LIVING A FLAMBOYANT AND CONSUMPTION-DRIVEN LIFESTYLE

THE BLING KING

LOWER LEVEL LUXURY SPENDERS THAT PLACE LITTLE VALUE ON BRANDS

THE BRAND SKEPTICS

LOWEST PURCHASING POWER BUT HIGH FASHION FOCUS & DESIRE

THE ASPIRANT

WINE & SPIRITS LUXURY AUTOS COSMETICS HOSPITALITY

LUXURY SEGMENTS STUDIED

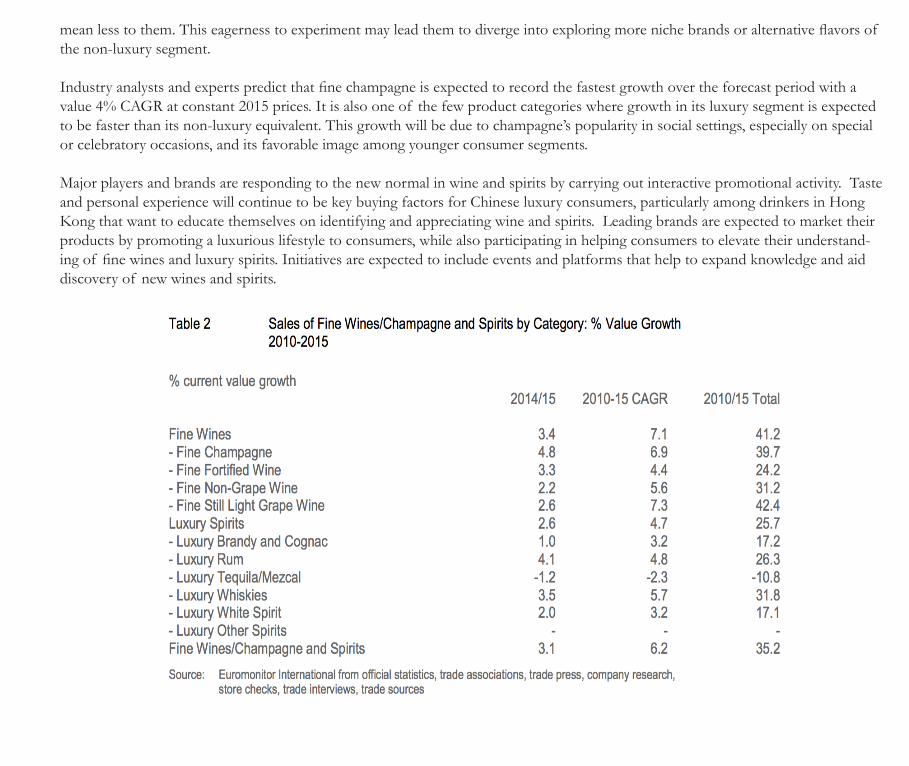

Asia’s wine cellar. Champagne craze.

WINE & SPIRITS

Slowing growth.

SLOWING GROWTH

2012 2013 2014 2015

3% 4% 6% 9%

Source: Euromonitor InternaOonal

The Occupy movement in 2014 and 2015 led to signiÞcant unrest in the Central district of Hong Kong.

Anti-corruption practices impacted wine and spirits due to lavish gift giving which was common throughout upper tiers of Chinese society.

TWO PRIMARY VARIABLES

1 2

SLOWDOWN

PREFERENCES & PALATES

WINE & SPIRITS

Red wine dominates the market at a staggering 37% of sales. Popular due to its appealing

taste to Asian consumers palate. Also, popular choice for gifting.

RED WINE

White wine accounts for about 7% of sales. Acidic taste does not

pair well with Asian cuisine. White wine has seen more growth than red in 2015 due to increased

consumer sophistication.

WHITE WINE

Champagne is the fastest growing, rising 5% in 2015. Considered

“aspirational” and associated with luxury and living “the high life.”

Opened only at special occasions, it has not experienced the same

slowdown as red and white wines.

CHAMPAGNE

Source: Euromonitor InternaOonal

WINE & SPIRITS

Led Þne wines, champagne and spirits in 2014 with Dom Perignon,

Veuve Clicquot, Hennessy XO, and Glenmorangie.

LOUIS VUITTON MOET HENNESSY LEADS

Developing consumer tastes and education have led to exploration and looking beyond brands and

bottle labels.

EDUCATED CONSUMERS

Cognac is enjoyed at business dinners. Cognac makers have been

hit hard by the stock market instability and luxury crackdown.

LUXURY COGNAC HIT HARD

Brands advertise in luxury lifestyle magazines and department stores/wine retailers. Travel retail plays key

role especially duty free.

MAGAZINES, DEPT STORES STILL ADVERTISING KEY

COMPETITIVE LANDSCAPE

Source: Euromonitor International

DISTRIBUTION

97%

2.1% ONLINE

NO IMPORT DUTY: Hong Kong as

primary sales

COUNTERFEIT IMPACT

RETAILERS

Source: Euromonitor Interna0onal

BOTTOMS UP

64%

36%

FINE WINE

LUXURY SPIRITS

2015 SALES Source: Euromonitor International

23.19%

0.55%

0.30%

40.05%

11.24%

0.07%

0.01%

21.78%

2.80%

Champagne

FortiÞed Wine

Non-Grape Wine

Still Light Grape Wine

Brandy & Cognac

Rum

Tequila/Mezcal

Whiskies

White Spirits

WINE & SPIRITS 2015 MARKET COMPOSITION

Source: Euromonitor InternaOonal

WINE & SPIRITS GROWTH WINNERS

FINE WINE 12.4%

SPIRITS 3.2%

CHAMPAGNE 18.9%

WHITE WINE

8.9% WHISKIES

7.8% 2015-2020 Source: Euromonitor International

THREATS TO THE FUTURE

Consumer education and sophistication changes preferences. As their wine and spirit knowledge grows, they seek more unique choices, diverse selections, and variable flavors. This is especially true for young consumers in Hong Kong.

WINE & SPIRITS FUTURE

TASTE INTERACTIVE EXPERIENCE

LIFESTYLE

Leading brands are expected to market their products by promoting

a luxurious lifestyle including events and platforms to expand knowledge and aid discovery of

new wines and spirits.

WHAT’S NEXT

Demand for luxury cars in Hong Kong. Market Overview.

LUXURY AUTOS

Disruptors.

Customers desire: EXOTIC-NESS

ELEGANCE POWER

COMFORT PERFORMANCE

LUXURY HISTORY

STATUS SYMBOL

DEMAND FOR LUXURY AUTOS

PASSENGER VEHICLES

PREMIUM CARS

26%

Market growth per year for 10 years

1.25 million

2012 PREMIUM CAR SALES

2nd LAREGEST IN THE WORLD

36%

Expected grow at a compound annual rate of 16 percent between now and 2020.

80% of Chinese premium car owners have annual disposable household income of more than RMB 200,0004.

NEW GENERATION OF LUXURY CAR CONSUMERS

1 2

LUXURY CARS

McKinsey’s consumer research

300 cities in China will have consumers with sufÞcient household income to buy premium vehicles by 2020.

By 2020, there will be 23 million affluent urban households in China Ð 7% of the population. 3 4

LUXURY CARS NEW GENERATION OF LUXURY CAR CONSUMERS

McKinsey’s consumer research

STRONG GROWTH WILL BE DRIVEN BY AN EXTRAORDINARY BOOM IN AFFLUENT AND NEW MAINSTREAM MIDDLE CLASS FAMILIES IN CHINA

Number of urban households by annual disposable income bracket, million households

Affluent (more than USD 34,000)

New Mainstream (USD 16,000-34,000)

7

37

23

171

82

33

14

19

13

10

9

10

12

12

7

14

25

24

2012 2020 Other premium car markets

PREMIUM CAR SALES

SHARE OF MAJOR BRANDS IN CHINA 2013

China 31%

Germany 10% United

States 10%

Other 43%

China 20%

Germany 10%

United States

10%

Other 52%

China 15%

Germany 10%

United States

10%

Other 45%

492k units

391k units

218k units

GLOBAL SALES

1.57M units

1.96M units

1.46M units

LUXURY AUTOS DISRUPTOR: TESLA

0

200

400

600

800

1000

1200

1400

1600

1800

2009 2010 2011 2012 2013 2014 2015

Electric vehicle registrations in Hong Kong

TESLA’S HONG KONG BOOM MIGHT BE SHORT-LIVED

3% New vehicle

registrations

2,279 Evs on

the road 70%

TESLAS

Business or Pleasure. Service and Amenities.

HOSPITALITY

BENCHMARK LIVING.

HOSPITALITY Luxury hospitality is the history, reputation,

location, views, brand value, star employees, infrastructure, furnishings, crystal ware, silverware,

and the Þnest Þttings. In reality, the luxury world of hospitality is all this and more.

HOSPITALITY

Luxury hotels typically have a lower guest-to-staff ratio which leads to personalized service.

SERVICE

Spas, swimming pools, gyms with trainers, golf courses, poolside

drink service, dry-cleaning services, and shoe shines are major distinguishing factors.

AMENITIES

Guests are pampered, from plush lobbies, furniture, bedding to higher quality F&B and concierge service.

INDULGENCE

Award-winning and high-quality meals showcasing local cultures and

ingredients giving guests an opportunity to pamper their palate.

RESTAURANTS

GROWING TRAVEL FUELS LUXURY HOTELS

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

16,000.00

18,000.00

20,000.00 Outbound Trips

Source: Euromonitor

Hotel brands would need to focus their efforts on affluent and independent Chinese travelers especially Chinese female travelers.

One of the trends in hospitality is “more bang for your buck”. Chinese expect to get good service included due to the premium price.

1 2

LUXURY LIVING SAVY CHINESE CONSUMER

Attract AÞcionados to Aspirants with location,

ecommerce Ð social media reviews, and specialized

services for each consumer segment.

MAINTAINING APPEAL

Its eminent for Chinese consumer to maintain their socioeconomic stature and

the only differentiating factor is the purchase of

luxury brands.

LUXURY DEMANDS

Perception is everything for Chinese consumer.

PERCEPTION

SOURCE: PIERRE PERUSSET, GM, RITZ CARLTON HONG KONG

HOSPITALITY INSIGHT

DESIGN AROUND

THE LUXURY BRANDS

Godiva high tea BlancPain watches Caviar bar Luxury towels and sheets Rolls Royce for airport transfer Chateau Petrus wine

THE POWER OF LUXURY COBRANDING

15%

10%

10%

9%

7% 4% 4%

3% 3%

2%

33%

Holiday Inn

Sangri-‐La

Sheraton

Hilton

MarrioV

HyaV

InternaOonal

Sofitel

Kempinski

Macro Polo

HOTELS ARE PROVIDING UNIQUE EXPERIENCES

Percentage of Chinese travelers staying at top 4 and 5 star hotel

Chinese hotel industry competes with travel destinations like Venice, Hawaii and Cambodia. These top 3 travel destination have unparalleled

history, culture and views. China travel has a probability of being over crowded. Luxury hotels

risk a less than 70% occupancy rate.

SUSTAINABLITY

Once A New Market. Evolving Opportunity.

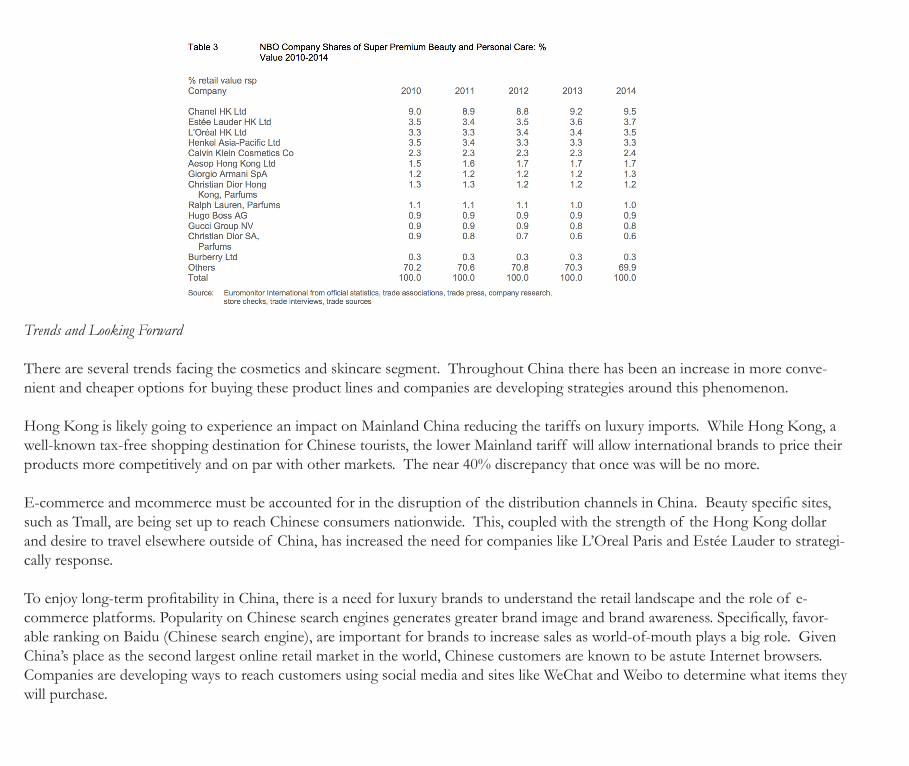

COSMETICS

BEAUTY.

Multinational companies turned their focus to China with the rise in income and developed two-part strategies.

For decades, Chinese viewed cosmetics as “counter-revolutionary.” The void in the segment after economic reforms meant an open playing Þeld.

A SORTED HISTORY

1 2

COSMETICS

SEGMENT SNAPSHOT • Global beauty industry worth over US$55 billion • Luxury beauty and personal care grew 4% to HK$2.6B in 2015 • Growth is slowing • Distribution channels disruption

COSMETIC GROWTH

DECLINING

2011 2012 2013 2014

5% 6% 6% 8% 3%

2015 Source: Euromonitor InternaOonal

THE MEANS TO THE CONSUMER

DISTRIBUTION

Tier one Chinese cities, like others worldwide, rent space

to premium brands to, in essence, create stores

within stores.

DEPARTMENT STORES

In smaller cities in China, mid-sized beauty product chain stores have brand-

speciÞc beauty assistants to assist customers in

their experience.

BEAUTY CHAINS

Throughout rural China and smaller cities, brand

assistants are non-existent and local retailers typically

sell lesser-known, Asian product lines.

LOCAL RETAIL

TRAVEL CHANGES

43

72

3

5

2

6

60

51

20

19

7

7

Hong Kong/Taiwan/Macao

Mainland China

Europe

Japan/Korea

South East Asia

Other overseas countries

PURCHASE LOCATIONS 2012 2009

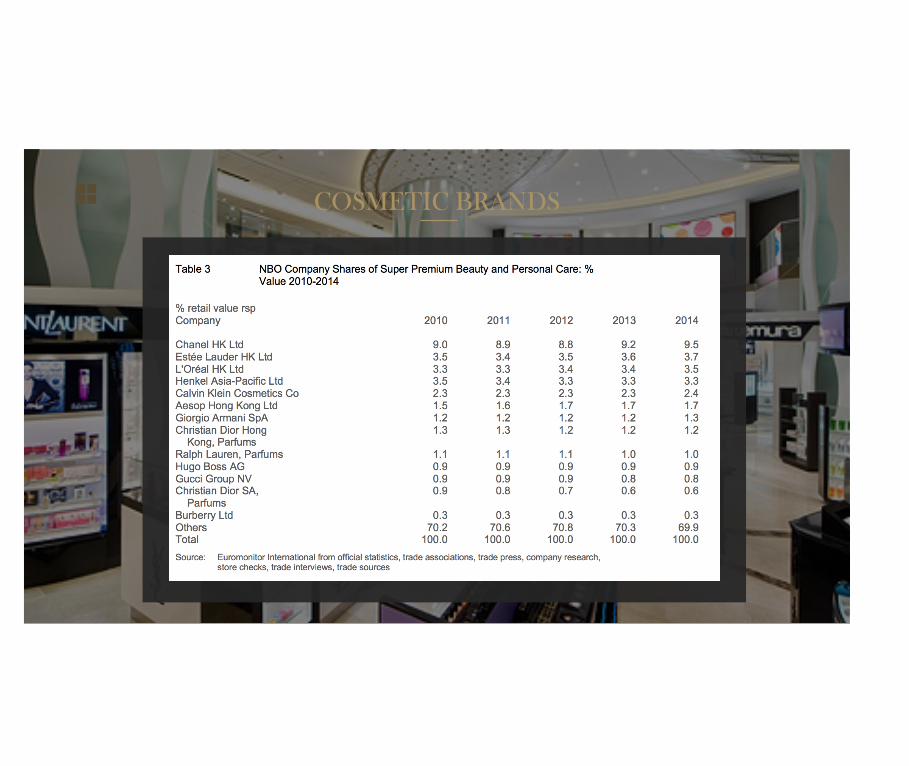

TOP COSMETIC BRANDS

CHANEL. • French • 9.5% Share • Diverse Product Line • Entered China in 1998

ESTEE LAUDER • American • 3.7% Share • Focused on co-Branding • Entered China in 2002

L ‘OREAL PARIS • French • 3.5% Share • Refocused on skincare • Entered China in 1997

COSMETIC BRANDS

COSMETICS AND SKINCARE TOMORROW

TRENDS

Reduced tariffs on luxury imports will boost Mainland domestic consumption. A

40% discrepancy is disappearing.

LOWER TARIFFS

Shopping destinations other than Hong Kong are

becoming more attractive to the Chinese consumer due to the strength of the Hong

Kong dollar.

HKD AND TRAVEL

Internet retailing (ecommerce) and

mcommerce have changed the landscape of distribution.

International platforms are on the rise.

INTERNET RETAIL

PERSONAL NATURAL

EXPERIENCE REGIONAL

Estée Lauder and other leading companies are tailoring their brands to be more personal,

natural, and create an experience in order to remain dominant.

FINAL THOUGHTS

IMAGINE LUXURY IN 2030 TODAY ONLY 7% OF CHINESE HAVE PASSPORTS. IMAGINE LUXURY TOURISM WITH 20%, 50% OR 70% TRAVELERS. AS APPETITES INCREASE FOR LUXURY, CONSUMERS DEMAND LUXURY EVERYTHING. HIGH-TOUCH AND HIGH-TECH: FROM MOBIL TO PERSONAL SHOPPERS. ONLINE SALES WILL OUT-PACE IN-STORE SALES. LESS SEGMENTATION; MORE CO-CREATION, CO-BRANDING, CO-HABITATION, CO-EVERYTHING LUXURY RENTAL AND SHARING LUXURY AUTO: MOTORING DRIVERLESS FOR MAINSTREAM

CHINESE LUXURY: THE NEW NORMAL

TEAM DONG

THANK YOU

CAPSTONE PAPER RESEARCH AND KEY FINDINGS

Executive Summary

Our team embarked on a journey of exploring and comparing the luxury markets in Asia and the United States. We specifically focused our attention on Hong Kong and Macau. Our research involved testing a hypothesis that examined the dip in consumption abroad and if this was a new normal for the industry or if it would rebound.

Throughout the process we explored the history and political evolution of opening up China and attempted to understand the mindset of these new con-sumers. Once we soundly understood the lens in which we felt Chinese luxury consumers approached the market we analyzed the evolution of these consum-ers. What is their varying desires, wants, and needs? We posed questions of how were leading industry players are adapting to meet them in the areas of wine and spirits, cosmetics, hospitality, and automotive sectors. After spending nearly a week in Hong Kong and Macau, meeting with execu-tives and comparing academic research we reached the conclusion that there is, in fact, a new normal in China. The slowdown is likely permanent compared to the staggering, explosive growth in the last decade. Business is responding well to this reality but also looking forward to the growth of China’s middle class – an ongoing phenomenon.

We conclude our research with several themes we heard form nearly every interview in one form or another. These themes help tell the story and explain why this “new normal” has come to be. They include significant currency fluctuation, which is causing Mainland Chinese to both travel elsewhere and view Hong Kong as too expensive for luxury travel and expense. What was once the premier destination for Chinese upper class is now being replaced by direct travel to places like Paris or London. Another theme is a shift in culture away from corrupt practices that were once commonplace. With a keener eye on gift giving and overspending, there are now reins in place on lavish spending causing all four of our segments to react accordingly. Lastly, there is a boon in the future of vacation travelers. As the middle class grows and more Mainland Chinese obtain passports, they will travel outside of China, far beyond Hong Kong and Macau. While abroad they will make their luxury purchases else-where and enjoy this new, shopping experience.

Throughout our journey we discovered and developed insights previously unknown, shared and laughed in the company of each other and amazing business leaders, and our advisor, Professor Arthur Dong. We hope you enjoy our findings as much as we did discovering them.

Hypothesis

The continued growth of the Chinese economy and China’s voracious appetite for luxury goods will provide the impetus for further growth in luxury good consumption both in China and other parts of Asia.

Our research explores the following questions:

• What is the market size of luxury goods in Hong Kong, China?• What trends and drivers are shaping the Asian luxury goods market?• What business factors are transforming the luxury goods shopping experience?• What are luxury good consumer preferences, motivators and demands?• Which brands are exploring alternative sales channels and innovative partnerships?• How dynamic is the growth of luxury goods Internet sales?• What is driving growth? What is slowing growth?

Throughout our journey we discovered and developed insights previously unknown, shared and laughed in the company of each other and amazing business leaders, and our advisor, Professor Arthur Dong. We hope you enjoy our findings as much as we did discovering them.

Overview

According to Bain & Company, Inc.’s Luxury Goods Worldwide Market Study, the overall luxury industry comprises nine segments: luxury cars, private jets, yachts, luxury hospitality, luxury cruises, luxury wines and spirits, fine food, designer furniture, and personal luxury goods. Factoring all segments, the overall luxury market exceeded €850 billion in 2014, showing healthy growth of 7% overall, driven primarily by luxury cars (10%) and luxury hospitality (9%).

Bain’s research found that international travel and tourism is fueling an appetite for 360-degree luxury experiences, such as high-end transportation, that includes highly customized “super cars” and yachts, as well as luxury hotels and cruises.Personal luxury goods, the “core of the core” of luxury, continue to buoy the market. The overall global market is on target to reach €223 billion in 2014, triple its size 20 years ago. Yet that growth is slowing: in 2013, luxury goods grew 7%, and in 2014, growth slowed to 5% at constant exchange rates (2% at current rates). That slower pace is, however, more sustainable, and it reflects the “new normal” for luxury goods, particularly as the global economy continues its sluggish recovery from the financial crisis of 2008. Demand from Chinese consumers, mature consumers in the US, and Japanese shoppers returning to luxury goods have all helped shore up growth.

Luxury spending doesn’t always take place at home. Touristic spending now drives the luxury-goods industry in most markets, which means that who the buyers are matters more than where they buy. Chinese consumers, for the last three to five years, represent the top and fastest-growing nationality for luxury, spending abroad more than three times what they spend locally.

Wealth creation within Asia has led to a super-cycle of demand for luxury goods. However in 2014, luxury goods recorded the smallest growth in five years. The softening growth was largely attributed to the strong growth rates occurring in previous years, the anti-graft campaign and flagging economic growth in Mainland China. Consequently, Mainland Chinese tourist flows in Hong Kong, were significantly reduced in 2014 and 2015, after having registered a record high in tourist numbers in 2013.

With the present slow down in the China economy as well as other parts of Asia, will the growth in luxury goods sales in Asia likely to persist? Is the slower growth pace more sustainable and reflective of a new normal for luxury goods? What impact does this slowdown have on other markets, business, people, and generations? And how does the luxury market in Hong Kong and Macau compare to the United States?

History & Background

In order to better understand how the luxury market evolved in China and specifically Hong Kong and Macau, we discovered the importance of understanding the Chinese cultural history. This involved studying the past and opening up of China from a strangle-hold communist government’s grip.

Interview with Mr. Bill Weidner

On January 29, 2016 we interviewed Mr. William (Bill) Weidner. Bill Weidner is the Chairman and CEO of Global Gaming Asset Management, LLC and Principal of Weidner Holdings and its subsidiaries Weidner Resorts China and Taiwan. GGAM, which is a joint venture between Cantor Fitzgerald and former members of the Las Vegas Sands management team, was formed to advise, in-vest in, acquire and manage hospitality and gaming assets globally. GGAM recently built one of four integrated resorts in the Philip-pines Entertainment City Manila project with Bloomberry Resort called Solaire. Weidner Resorts specializes in developing boutique hotels and integrated 5-star residential resorts around the world in cooperation with Discovery Land Co. of Scottsdale, Arizona.

Mr. Weidner served as the President and Chief Operating Officer of Las Vegas Sands (LVS) from 1995 to 2009. While at LVS, Mr. Weidner lead the LVS team in developing and managing the 64-acre Sands Hotel site into the world’s largest integrated resort. He led the LVS team in opening the 4,000 room Venetian Las Vegas in 1999 and the 3,000 room Palazzo in 2007. He spearheaded LVS’ international expansion in Macau by opening the Sands Macau in 2004, winning the right to develop the first western-style casino in China. Following the opening of the Sands Macau, Mr. Weidner led the LVS team to open the 3,000 suite Venetian Macau in 2007 and the Four Seasons Macau in 2008 and also won the right to open Singapore’s first integrated casino resort (opened in April 2010) which is now generating over $1.7 billion of EBITDA annually.

Mr. Weidner started by encouraging us to “step out of the US mindset” and really try and understand how the Chinese got to the point where luxury goods and the market was even attainable. He talked about the perspective of what the size of the Chinese economy was in the 16th century, the evolution of the rest of the world surpassing them, the consequential isolationism and resent-ment, and the resurgence.

Prior to the nineteenth century, China had one of the worlds most advanced and largest economies. Adam Smith, in the eighteenth century wrote of China having had one the richest (meaning fertile), best cultivated, industrious, prosperous, and urbanized countries in the world. Unfortunately, for China, the economy stagnated and declines in absolute terms for much of the nineteenth and twenti-eth centuries – with a brief recovery in 1930. The primary economic reforms began after Deng Xiaoping and his reformist allies managed to displace the Gang of Four Maoist faction in China. By the time Deng took power, there was widespread support among the elite for economic reforms. As the de facto leader, Deng’s policies faced opposition from party conservatives but were extremely successful in increasing the country’s wealth. The economic reforms in 1978, known as “The Chinese Economic Reform” began to introduce market principles into China in two

phases. The first included the decentralization or decollectivization of agriculture, the opening up of China to foreign direct invest-ment (FDI), and permission for Chinese entrepreneur’s to start their won companies and businesses. Large industries like manufac-turing still remained state-owned and operated. The second phase, in the late 1980’s and 1990’s involved relinquishing some of that state-owned industry through privatization or contract outsourcing. The Chinese government also lifted price controls and loosened protectionist policies and regulations.

As a result of these reforms, the private sector in China began to boom, accounting for as much of 70% of China’s GDP by 2005. As a whole, from when these reforms started to take place in the late 1970’s to date, China experienced unprecedented growth and an economy that was growing at nearly 10% annually. In actual terms, the reforms in the 1980’s and 1990’s brought nearly 600 million people out of poverty and into a growing middle class. This new group of consumers shook industries of all sorts around the globe. But how do these consumers think and act?

A Culture of Savings

Suddenly exposed to nominal wealth and a better life, given their past, the Chinese consumers are still skeptical of the future. They come to the table with a mindset of the government being able to change the environment very rapidly and much of their life will be out of their control. This top-down controlled environment is very different that that of what consumers in the United States are accustom to. The United States middle class worries less about the future and thinks about social security, for example, as a safety net. As a result, the Chinese typically save a staggering 40-50% of their earnings compared to 3-5% in the United States.

No one can say for sure how much the Chinese people save. Data based on national income is incomplete and does not accord with international standards. The most credible estimate places China’s household saving rate for 2007 at nearly 26%. This is extraordi-narily high, although in line with rates in Japan, South Korea and Italy in previous decades.

Common explanations of why Chinese save have been less than satisfying. Most popular are invocations of “culture” — just as we’ve seen elsewhere in Asia. More often than not, Chinese leaders trace the nation’s thriftiness back to Confucian values. Com-pared to Americans who became accustomed to overspending, observed the official China Daily, the Chinese people have developed a “tradition of savings since ancient times.” Zhou Xiaochuan, governor of China’s central bank, recently defended his country’s high saving rate as in large part the product of Confucianism, which values thrift, self-discipline, moderation, and an aversion to extrava-gance.

There is something rather forced about these claims. In the 1960s, Chairman Mao Zedong denounced Confucius as a “stinking corpse.” Only in the last 20 years has the Chinese Community Party conveniently rediscovered the sage’s age-old influence on popular behavior. Ironically, the inspiration came primarily from abroad, from Confucian revivalists in Singapore and Taiwan and from West-erners who write about the development of “Confucian capitalism” in Japan and the rest of East Asia.Cultural explanations are all the more dubious when we consider the following: Not so long ago, the Chinese people were terrible savers. Under Maoism from 1952 to 1978, household saving rates did not exceed 2% or 3% and often sunk to less than 1%. If Chi-nese saved at impressive rates thereafter, surely other factors rank higher than Confucianism.

Another explanation favored by American economists and journalists is that Chinese save excessively in the absence of adequate welfare programs. It is an argument sustained by constant repetition, and little evidence. This analysis comes complete with its own policy recommendation. In the words of the influential economist Stephen Roach, China should build an institutionalized safety net necessary to temper the “fear-driven precautionary saving that inhibits the development of a more dynamic consumer culture.”

Uncertainty, it is true, may motivate people to save, but so do many other factors. Globally, the correlation between high saving and inadequate social benefits is a weak one. Scores of poor nations provide little in the way of social welfare, yet their saving rates are minuscule. Among advanced economies, high-saving nations in continental Europe all provide comprehensive welfare benefits. Americans, who aside from the elderly lack sturdy safety nets, conversely saved little in recent decades.

There are, however, better explanations. In China, household saving rates have risen in tandem with rapid economic growth. We have observed this pattern in Asia’s other success stories, as well as in Western Europe after World War II. Following Mao’s death and the advent of Deng Xiaoping in 1978, the party-state fundamentally transformed the Communist economy into one based on global trade, foreign investment, and the partial embrace of market principles. The Chinese economy leaped into high growth, the GDP surging 10% annually from 1980 to the present. As elsewhere, household savings rose as consumption lagged behind increases in incomes.

Second, Chinese save more because of poor access to credit. Saving tends to be inversely related to borrowing. American journal-ists glory in the story of Chinese conspicuous consumption and the spread of credit cards. Most of these “credit cards” are, in fact, debit cards tied to bank accounts. A small fraction of the cards offer revolving credit. The heavily regulated banks have been miserly in extending consumer credit, and they generally require stiff down payments before lending money to homebuyers.

This is in sharp contrast to the United States, but not so different from several Asian and European countries where consumer and housing credit is subject to significant regulation. In a fast growing economy like China’s, people want to buy cars and other durables, but in lieu of easy credit they need to save in order to consume.

Curiously, few observers consider the possibility that the Chinese party-state might have had a hand in directly encouraging popular saving. Indeed, China represents one of the most compelling cases of the efficacy of aggressive savings promotion.

Under Maoist rule, Chinese households saved almost nothing. They had little money, it is true, but they also lacked safe, convenient banking facilities. In the three years following the Communist Revolution of 1949, the regime eliminated all public and private banks, transferring their assets to the central People’s Bank of China. The dissolved banks included the Republic of China’s fledgling postal savings bank, established in 1919. Although families under Maoism may have saved by hoarding goods and a little cash, they had little incentive to save in lieu of accessible institutions for small savings.

All this changed in the wake of the regime’s decision to reform and open the Chinese economy in 1978. Leaders recognized the pressing need to mobilize domestic savings to remedy capital shortages. One year later the state established the Agricultural Bank

of China, the Bank of China, and the People’s Construction Bank of China. The creation of the Industrial and Commercial Bank of China in 1983 completed the formation of what today constitute the four big state-owned commercial banks.The year 1986 ushered in the next phase, the relentless pursuit of small savers nationwide. The Agricultural Bank and the Industrial and Commercial Bank set up nearly 30,000 new branches that year. The Agricultural Bank alone doubled the number of its branches, reaching villagers who likely had never before had a savings account.

Institutions bear heavily on savings behavior. In 1986, savings deposits increased at a faster clip than at any time since the founding of the People’s Republic of China. It was not simply that branches opened and customers streamed in. Bank employees ran nation-ally coordinated campaigns to persuade the locals to entrust their savings to the new institutions. Including its joint savings projects with the authorities, associations, and cooperatives, in 1991 the Industrial and Commercial Bank claimed one million staff members engaged in “savings mobilization.”

Joining the big banks in 1986 was the new—or rather improved—Chinese postal savings system. For all the recent insistence on Chi-nese exceptionalism, officials methodically emulated the savings-promotion policies of Japan and other thriving Asian economies.

Once the regime committed itself to reviving postal savings, Chinese bureaucrats visited Japan’s Postal Savings Bureau and Central Council for Savings Promotion. Cooperative relationships between savings officials of the two nations developed. During the 1990s, Japan’s Ministry of Posts and Telecommunications assisted the Chinese in computerizing the postal savings system. Officials from the People’s Bank of China, moreover, actively participated in the Bank of Japan’s meetings for Asian central bankers, reporting on Chinese programs to boost savings deposits.

Postal savings became immensely popular among Chinese for much the same reasons we have seen elsewhere. In many rural and remote areas of China, it is one of the few institutions that serve small savers. The number of branches mushroomed from less than 2,500 in 1986 to 37,000 in 2009. Its popularity also rested on more than two decades of promotional campaigns by postal employees and the local authorities.

As a share of total deposits, postal savings appears small compared to deposits the four big state-owned commercial banks—only 8.1% in 2002. But of course we’re talking about the world’s largest country. The number of households with postal accounts that year came to a mind-boggling 104 million.

Chinese leaders today speak less openly about their efforts to promote saving. Instead, officials increasingly pledge to stimulate con-sumption as a vital prop of the Chinese economy. As in Singapore, the party-state recognizes that its continued legitimacy depends on improvements in the people’s material lives. In view of decreased demand from sluggish Western economies, the planners are also aware that domestic consumers may need to buy more if the Chinese economy is to continue high growth.

However, the Communist Party’s pronouncements on consumption have their tactical side. They aim to reassure American observers, many of whom take any pledge as evidence that China will soon embrace an American-style consumer society.

Unquestionably consumption is rising in China, yet the Asian giant will likely remain a high-saving society for many years to come. The consumption levels enjoyed by Westerners, Japanese, Koreans, and Singaporeans are well beyond the reach of hundreds of mil-lions of Chinese. Consumption as a share of GDP stands at 35–36%, half that of the United States. Contrary to many media stories, China’s high growth relies overwhelmingly on investment, exports, and government consumption — and relatively little on domestic consumption.

Finally, the regime has a powerful stake in promoting household saving for the foreseeable future. Chinese authorities learned a great deal from the Japanese and Singaporean models, in which the state manages and invests large pools of small savings. The Chinese government similarly captures the people’s savings at low cost from the state-owned banks and postal savings system. This capital finances companies and infrastructure at home. It also flows into the Singaporean-style sovereign wealth fund that China invests stra-tegically in such things as U.S. Treasury securities and the exploitation of African minerals.

China, the newest savings superpower, now enjoys influence in international relations it could scarcely imagine three decades ago. When then-Treasury Secretary Henry Paulson blamed the China’s “superabundant savings” for causing a global credit bubble, the Chinese turned the tables just as the Japanese had done 20 years earlier. The United States, declared Premier Wen Jiabao, should be held most accountable for the global economic crisis. America had pursued an “unsustainable model of development characterized by prolonged low savings and high consumption,” the “blind pursuit of profit,” and “the failure of financial supervision.”

Make no mistake about it. Chinese leaders have few plans to jettison the policies of savings promotion that have served them so well.

Why Study the Chinese Luxury Market?

Much of luxury’s allure comes from the opportunity to share in the rich cultural heritage associated with a brand. This concept is rapidly catching on with Chinese luxury consumers, and many leading brands are promoting their history and craftsmanship. But the picture isn’t totally straightforward: one-third of luxury consumers in China said they would prefer to buy products that were designed specifically for the country and incorporated Chinese imagery. - McKinsey and Co

Chinese consumers now represent about one-third of the global market, up from only 1% in 2000; Japanese consumers, who ac-counted for a quarter of the market in 2000, now make up 10% of global purchases.

According to The Guardian the global luxury goods market exceeds €1tn. The Guardian attributed strong sales of luxury cars and fine art as luxury segments that have helped push the global luxury goods market higher than €1tn (£700bn) for the first time, ac-cording to a new report, despite slowing demand for personal luxuries such as jewelry and handbags.

The Guardian further notes that the personal luxury market has been hit by weaker demand in China and Hong Kong, said the an-nual report from consultancy Bain & Co. Chinese consumers account for 31% of global luxury sales, followed by US consumers at 24% and Europeans at 18%.

Chinese consumers are still spending, but they are now heading to Europe and Japan – attracted by the weak euro and yen – rather than their traditional shopping destinations of Hong Kong and Macau. About 80% of Chinese luxury goods shopping is done abroad. The findings echo recent comments from British luxury fashion house Burberry, which has blamed a sharp sales slowdown on weaker demand among shoppers in China.

The fastest growth was for sales of luxury cars, up 8% year on year, and fine art, up 6% - with postwar and contemporary work par-ticularly strong.

In China, household disposable income has been growing consistently over recent years, and is expected to continue in coming years. McKinsey & Company predicts the number of “upper middle-class” Chinese (those with an annual income between 106,000 and 229,000 yuan) will increase tremendously in the coming decade - 54% of China’s urban consumers will be regarded as “upper middle-class” by 2022, up from 14% in 2012. According to Hurun Wealthy Report 2014, there were 1.09 million millionaires and 67,000 super-rich individuals in China in 2013, an increase of 3.8% yoy and 3.7% yoy, respectively from 2012. The growth rates were much slower than that in 2010 and 2011, due largely to the relatively slow recovery of the world economy and slower economic growth in China.

Shifts in Attitudes

The luxury market in China seemed to be recession proof, as the luxury goods markets defied the global recession in 2009 as sales of luxury goods in the mainland rose by 16 percent, to about 64 billion renminbi—down from the 20% growth of previous years but far better than the performance of many other major luxury markets. To get a better idea of the dynamics, McKinsey surveyed more than 1,500 luxury consumers in 17 Chinese cities in spring 2010. According to Yuval Atsmon and Cathy Wu of McKinsey, three factors in particular, accounted for the Chinese demand for luxury goods, namely shifting attitudes, greater sophistication, and new geographic markets.

McKinsey research notes that given rapidly rising incomes, widely available luxury products (and information about them), and shift-ing attitudes toward the display of wealth, more Chinese consumers than ever feel comfortable buying luxury goods. As a result, China’s love for them is moving down the economic ladder, creating opportunities and challenges for marketers accustomed to serv-ing only the very rich. While wealthy consumers (with incomes above 300,000 renminbi, or about $46,000) will continue to account for a majority of luxury consumption, McKinsey research shows that the 13 million households in China’s upper middle class (in-comes between 100,000 and 200,000 renminbi) offer the biggest new growth opportunity. They already account for about 12 percent of the market, and their numbers are growing rapidly: McKinsey expects to see 76 million households in this income range by 2015, accounting for 22 percent of luxury-goods purchases.

According to McKinsey, interest in luxury goods is moving beyond handbags, jewelry, fashion, and the like. A growing number of Chinese luxury consumers are also splurging on spas and other wellness activities. Consumption is growing faster for such luxury services than for luxury goods: 20% of these consumers said they were spending more on experiences, only 13% on products.

Greater Sophistication

McKinsey’s research further elucidates the Chinese are increasingly exposed to luxury goods through the Internet, overseas travel, and first-hand experience. As a result, they have become more discerning.

With the surge in the number of luxury stores, fashion magazines, and websites and the use of social media, Chinese consumers are now familiar with nearly twice as many brands as they were in 2008. Half of the consumers McKinsey surveyed in 2010, for instance, could name more than three ready-to-wear brands, compared with only 23% two years before. As Chinese consumers become more familiar with luxury goods, they are becoming savvier about the relationship between quality and price. In 2010, only about half of consumers equated the most expensive products with the best ones, down from 66% in 2008.

Price transparency contributes to this dynamic. More than half of luxury consumers check product details and prices online, com-pared with 13% of all urban dwellers. Since two out of three luxury consumers have made at least one trip overseas, they have access to external benchmarks for comparing prices back home. In 2008, only two of five people in China realized that in the mainland, prices were at least 20% higher than they were in places such as Hong Kong. By 2010, 66% did.

Luxury-goods companies have long waged a battle against counterfeit goods in China. However: McKinsey’s research shows that consumers increasingly want the real thing. The percentage of those who said they would buy fake jewelry, for example, dropped to 12%, from 31%, in 2008. Some luxury buyers told us they felt sure that their friends would spot a counterfeit. A woman who used her first salary check to reward herself with a luxury handbag said, “it would be meaningless if it was fake.” What’s more, an interna-tionally well-known brand has become one of the most important factors in making a purchase.

New Geographic Markets

McKinsey states that rapid urbanization and growing wealth beyond China’s largest cities are creating a number of geographic mar-kets with sizable pools of luxury-goods consumers. More small cities will become large enough to justify the presence of stores cater-ing to them; McKinsey expects luxury sales in urban areas such as Qingdao and Wuxi, for instance, to triple over the next five years. By 2015, consumption in such cities will approach today’s levels in Hangzhou and Nanjing—now two of China’s most developed luxury-goods markets—and luxury consumption could pass 500 million renminbi in more than 60 cities, compared with 30 today. But the luxury-goods market will remain concentrated in the top 36, which will account for 74% of the market’s growth and 76% of total luxury sales by 2015.

McKinsey observes - most of the world’s luxury-goods companies are already in China or contemplating increased investment there. They must tackle several big issues before making their next moves. First, delivering exceptional service in stores is critical; two out of three consumers are disappointed with the indifferent attitudes of salespeople.

Overseas Shopping

According to Bain, daigou, or overseas personal shoppers who buy and send luxury goods to customers in China, has grown to an es-timated market value of RMB 55-75 billion in 2014, concentrated in cosmetics, followed by leather goods, watches and jewelry. This is nearly 50% of the store sales in China.

Seventy pecent of luxury brands bought by Chinese is now bought abroad or through daigou agencies; in terms of travel destina-tions, Korea and Japan have been the big winners in 2014.

According to technode, Japan was a particularly popular destination, as sales of luxury items are up an estimated 251% since 2014. South Korea was second with an increase of 33%, followed by Europe with an increase of 31%. In contrast, sales in Hong Kong and Macau decreased by about 25%. The sharp increase in luxury items purchased by Chinese shoppers in Japan is attributed to a more open visa policy, which also explains the increasing number of Chinese tourists who visit Japan.

Chinese consumers have strong preferences for shopping luxury goods overseas. China’s outbound tourists amounted to 116 million yuan in 2014, up 18.2% yoy according to the Chinese Tourism Academy. Touristic spending has become a strong driver of luxury spending Bain & Company estimates that Chinese visitors spent as much as 209 million yuan on luxury goods overseas in 2014.

E-Commerce / Web Strategies

According to Bain’s report, cross-border and overseas websites are taking about 12% of all Chinese luxury goods spending. Tech-node reveals that Instead of buying luxury goods at department stores, shopping malls, or arranging a deal with a daigou merchant, Chinese shoppers are making purchases through websites like JD, Tmall, Net-A-Porter.com, ShopBop (acquired by Amazon in 2006), and Harrods.

The Chinese government has also been helping to move luxury brand purchases online. For example, in January 2015, limits on cross-country online payments increased from $10,000 USD to $50,000 USD. The expansion of free trade zones in China also offers tax benefits to companies that conduct cross-border e-commerce.

Furthermore, McKinsey discloses that while the in-store experience is by far the most important factor driving purchasing decisions, the Internet has rapidly become the second-most-important consumer touch point for luxury categories such as fashion. Market-ers will need increasingly sophisticated Web strategies; for example, they can work with social-media agencies to monitor and shape online conversations among consumers or to identify influential bloggers and help educate them about brands.

Global Luxury Market

In the 1950s and 1960s, the world economy was transformed by the emergence of the American consumer. Now China is poised to become the next consumption superpower, having overtaken Japan as the second-biggest consumer economy. With roughly $3.3 tril-lion in private consumption, China has about 8% of the world total, and it has only just begun.

According to Global Powers of Luxury Goods 2015, a report by Deloitte, a UK consulting firm, the economic climate for makers of luxury goods is positive, but there are risks. On the positive side, the economies of the U.S., Europe, and Japan appear to be recover-ing. On the negative side, economic growth in three of the four BRIC economies has stalled, the exception being India which the IMF predicts will grow at 7.3% in 2016. Although currency market volatility also contributes to the challenges, luxury goods compa-nies should be pleased that, after years of stagnation, the global economy is generally on the rise.

Luxury Goods Industry

The global luxury goods industry, which includes drinks, fashion, cosmetics, fragrances, watches, jewelry, luggage and handbags, has been growing for several years. Luxury goods are considered to be goods at the highest end of the market in terms of quality and price, and meet consumer demand by delivering on design, quality materials, superior craftsmanship and pricing. Luxury goods trans-form everyday objects into status symbols. As a rule, the industry rises and falls with the gross domestic product (GDP), climbing in times of economic stability and falling in unfavorable economic climates. The United States has long been the largest market for luxury goods.

Over the past 20 years the number of luxury-goods consumers worldwide has more than trebled to 330m, according to Bain & Company, a global management consultancy based in Toronto. Spending on luxury consumer goods has risen by double the rate of growth in global GDP. Most new buyers are not the super-rich, or even the very rich, but the prosperous, with incomes of up to €150,000 ($188,000).

In 2014, the 13th edition of the Bain Luxury Study, a global market report, analyzed recent developments in the global luxury-goods industry. It sees slower, steadier growth for luxury goods for the immediate future. The overall luxury industry comprises nine seg-ments in total, one of which is personal luxury goods.

For 2015, the overall luxury market exceeded €850 billion, showed healthy growth of 5% overall, and was driven primarily by luxury cars (8%) and luxury hospitality (7%).

Bain research found that international travel and tourism was fueling an appetite for 360-degree luxury experiences, such as high-end transportation that includes highly customized “super cars” and yachts, as well as luxury hotels and cruises. Not to be outdone, personal luxury goods — luxury’s “core of the core” — continue to sustain the market, which in 2014 was three times the size it was 20 years ago.

Yet growth is slowing. In 2013, luxury goods grew by 7% and in 2014 by 5% at constant exchange rates (2% at current rates). The slower pace is more sustainable, reflecting a “new normal” for luxury goods. Helping to bolster growth is demand from Chinese consumers, mature consumers in the US, and Japanese shoppers returning to luxury goods.

Not all luxury spending takes place at home. Tourist spending drives the luxury-goods industry in most markets. Chinese shoppers are the fastest-growing luxury consumer, spending more than three times abroad than they spend locally. With such cross-pollination of luxury spending, it makes little sense to think only in terms of location. This new mindset has considerable consequences for luxury brands, requiring new thinking from a global perspective.

Bain’s study predicts the following trends:

• Americas — The Americas were the undisputed growth engine in 2014, delivering a 6% increase at constant exchange rates. Brazil posted disappointing results due to local currency devaluation, but Mexico and Canada maintained positive performance.

• Europe — Growth across the continent was up 2%, despite persistent economic challenges, socio-political tensions in Eastern Europe, and less dynamic tourism.

• Japan — Japan regained a growth leadership position in 2014, increasing by 10% at constant exchange rates that made it the best-performing market in real terms.

• China — Luxury spending in China fell for the first time: –1% growth this year at constant exchange rates (–2% at current rates), due to greater controls on luxury spending and changing consumption patterns. Concurrently, less established and younger brands have commended themselves to the growing upper-middle-class “wannabe” consumer segment, which is expected to double by 2017.

LVMH (Louis Vuitton Moet Hennessy), the most valuable luxury brand in the world, is valued at about US$25.87 billion. For the 2014 fiscal year, LVMH Group’s total revenue was about €30.64 billion. Three of the top 10 companies are luxury companies with in multiple luxury brands; two are cosmetics and fragrance companies; two are jewelry and watch companies; two are apparel compa-nies; and one, Luxottica, is an accessories company. LVMH, Richemont and Estée Lauder maintained their positions as the top three luxury companies. Of the top ten companies, six have headquarters in the United States and France (three each), Switzerland has two, and Italy and Hong Kong each have one.

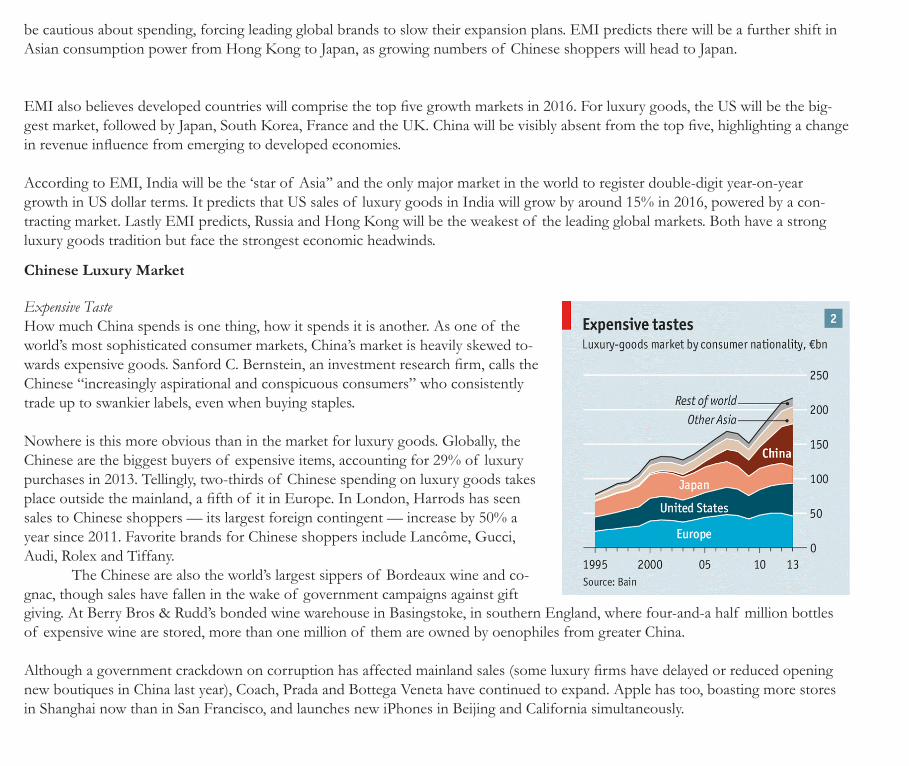

How will 2016 shape up for the global luxury goods industry? According to Euromonitor International (EMI), rising instabil-ity in emerging market economies poses the biggest threat. However, the prospect of slightly stronger growth in Western Europe and North America could offer some respite for global brands. Even so, 2016 is set to be another challenging year. Over the past decade, LVMH, Gucci and Prada have expanded rapidly into China, but as the country’s economic growth slows, consumers will

be cautious about spending, forcing leading global brands to slow their expansion plans. EMI predicts there will be a further shift in Asian consumption power from Hong Kong to Japan, as growing numbers of Chinese shoppers will head to Japan.

EMI also believes developed countries will comprise the top five growth markets in 2016. For luxury goods, the US will be the big-gest market, followed by Japan, South Korea, France and the UK. China will be visibly absent from the top five, highlighting a change in revenue influence from emerging to developed economies.