m a and fundraising activity and trends 2014

TRANSCRIPT

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 112

Global

Advertisingand MarketingTechnology

MampA and FundraisingActivity and Trends

September 2014

Julie Langley Partner UK

+44 (0) 207 514 8247 jlangleyresultsigcom

Pierre-Georges Roy Partner United States +1 646 747 6505pgroyresultsigcom

Maurice Watkins Partner United States +1 646 747 6510

mwatkinsresultsigcom

Mark Williams Director UK +44 (0) 207 514 8242mwilliamsresultsigcom

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 212

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends2

Our predictions983161 Enterprise software vendors will continue to move not just into marketing technology but more squarely into the media end of the

advertising technology sector

983161 The largest and fastest growing US AdTech players will move more aggressively into Europe making strategic acquisitions not just fortechnology but for geographic scale and revenue

983161 The online and offline worlds will further converge as large offline players seek to leverage their increasingly valuable offline datasets andexpertise Partnerships and MampA will occur as digital marketing stacks seek to inform media buying with integration of offline data

983161 The buyer universe for AdTech and MarTech companies will continue to diversify Telcos publishers broadcasters tech infrastructurevendors and traditional data companies will become active acquirers

983161 Pan-European winners with a presence in the main European media markets will emerge

983161 The European Private Equity community will become more active in the sector as European champions reach greater scale

The advertising and marketing technologymarkets continue to evolve at paceWhilst the public markets have beenunfavourable for many AdTech andMarTech businesses so far in 2014 MampAactivity continues to flourish and if dealactivity continues at the current pace2014 will see twice the number of deals as2013 The level of MampA activity has beendriven by a number of trends

Innovation in technology and channels

Constant innovation in technology and the way consumers engagewith media has driven vast amounts of MampA as buyers seek to stayahead of a rapidly changing market Particularly hot areas haveincluded video mobile social multi-screening and online to offline

where the large digital media players such as Yahoo AOL Facebook Twitter and Google have been very active

New entrants

Interest in the sector is coming from an increasingly diverse groupof buyers Amongst the telcos Telefonica SingTel and Telstra have allmade significant acquisitions in AdTech Also broadcasters such asRTL and Comcast have made bold moves into video advertising withan eye to establishing a presence in the online as well as offline (TV)market

Emergence of pure-play buyers of scale

The rapid growth of businesses like AppNexus MediaMath and Turnwhich have raised substantial sums of growth capital has created a

pool of sizeable private buyers able to make significant acquisitionsdriven by technology geographic expansion and scale

Continued integration between enterprise software and AdTech

For a couple of years now enterprise software vendors such as Oracleand Salesforce have been very acquisitive in areas such as marketingautomation as they extend their CRM business into a broadermarketing and customer engagement suite In 2014 we have seen theenterprise software vendors move much more squarely into AdTechfor example Oraclersquos acquisition of BlueKai and we expect much moreof this kind of deal activity to occur in the future as other vendors makesimilar moves

The battle for data

Access to data to improve targeting and better understand the

customer journey has driven substantial deal activity Particularly hotthemes have included the role of offline data in closing the loop forin-store purchases omni-channel attribution as a means of betterunderstanding customer journeys and various applications of bigdata whether across mobile search or social We have also seen bothadvertisers and publishers thinking more strategically about thevalue of their first party data and how that should be leveraged (andprotected) as the eco-system evolves

All eyes on Europe

From a European perspective an exciting development has been thenumber of US and overseas players looking to Europe for technologyand innovation whether that rsquos Google buying Spiderio Twitter buyingSecondSync or Rakuten buying DC Storm Europe is well and truly

front of mind for the large US players right now and we expect 2014and beyond to see an uptick in the level of activity amongst US playerslooking to expand in Europe whether via acquisition or organically

International fundraising strengthens

Fundraising activity is strong and showing no signs of slowing oneither side of the Atlantic Investors remain committed to fundinginnovation and disruption as well as supporting successful investmentsthrough to international scale Over $3 billion of investment was madein the first half of 2014 The stage of investing reflects the fact thatparts of the market are now well established with international marketleaders and yet other areas continue to be disrupted by innovativenew entrants Hence there were several $60 million-plus late-stage pre-IPO rounds as well as over 160 seed and series A investments made

into earlier-stage disruptive entrants all within the first half of 2014 The level of funding in Europe particularly at seed series A and seriesB stage is also encouraging as is the growing interest amongst USinvestors in Europe attracted by the level of innovation ambition andtalent of founders and management teams

Itrsquos an exciting time to be working in the sector and we look forward tocontinued high levels of activity in the rest of 2014 and beyond

ForewordBy Julie Langley Partner

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 312

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 3

Global deal volume in 2014 set to double over 2013 levels

Global MampA activity in the sector has seen a huge uplift in 2014 as theindustry has continued to grow and mature (Figure 1)

Across the spectrum of deals that have occurred the nature of MampAactivity has visibly evolved Deals are increasingly driven by the needfor scale geographic expansion access to data and new channels asthe race to be the leading global vendors in the sector heats up

Key observations

983161 The number of deals completed in H1 alone was nearly as high asin the whole of 2013 If deal activity continues at this pace ndash andactivity through July and August suggests it will ndash then deal volumein 2014 will be close to double that of 2013

983161 MarTech companies represent about 70 of overall deal volumeboth in 2013 and H1 2014 This in part reflects the high level of dealactivity undertaken by the large enterprise software vendors as theybuild out their cloud marketing suites

Part 1

MampA Activity

983161 In addition competition in the battle for client ad spend continuesto grow as new buyers ranging from social media networks(eg Twitter and LinkedIn) to telcos (eg SingTel and Telefonica)seek to enter the AdTech and MarTech sector through strategicacquisitions

983161 Deal value for AdTech is on track to double in 2014 over 2013with average deal value remaining broadly constant Deal valuefor MarTech is down on an annualised basis compared to 2013however this reflects a handful of very large deals which took placein 2013 including Oraclersquos $15 billion acquisition of Responsys andSalesforcersquos $26 billion acquisition of ExactTarget

50

40

30

20

10

0

N u m b e r o f d e a l s

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

2013 Number Value

MarTech 162 $85b

AdTech 61 $18b

Total 223 $103b

H1 2014 Number Value

MarTech 152 $22b

AdTech 57 $20b

Total 209 $42b

Global deal volume (January 2013 to June 2014) Figure 1

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 412

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends4

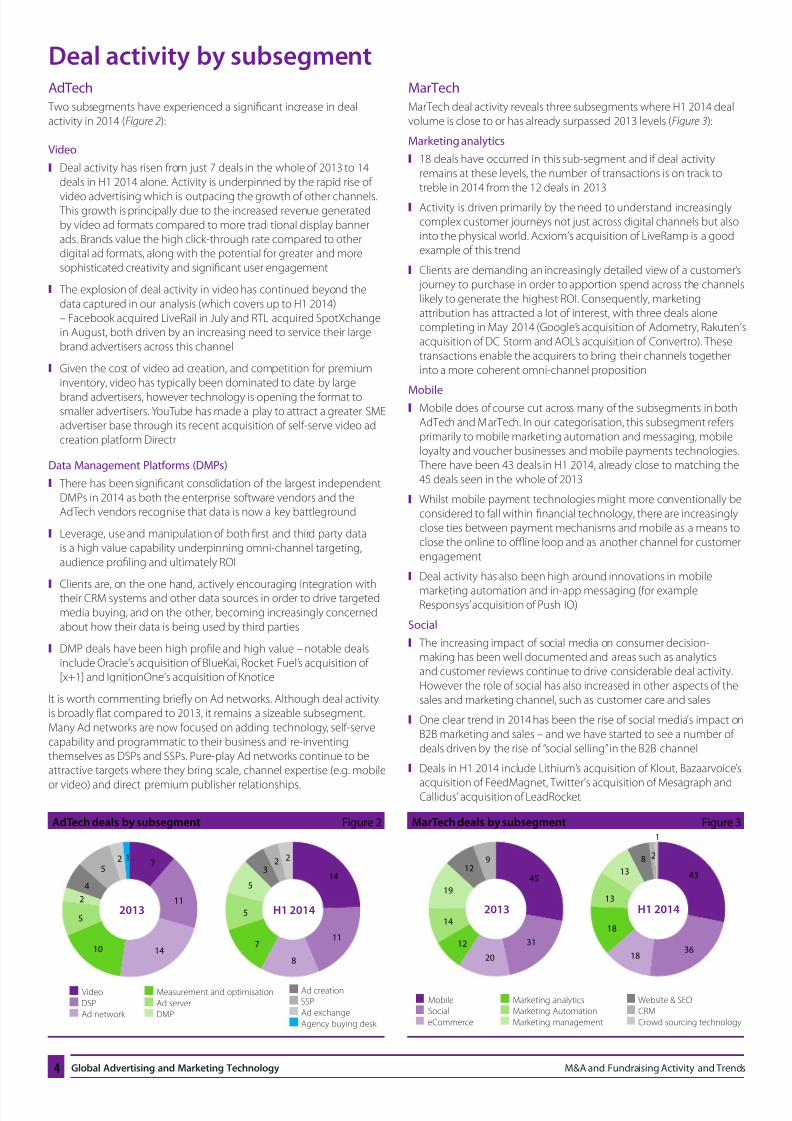

Deal activity by subsegmentAdTech

Two subsegments have experienced a significant increase in dealactivity in 2014 (Figure 2)

Video

983161 Deal activity has risen from just 7 deals in the whole of 2013 to 14deals in H1 2014 alone Activity is underpinned by the rapid rise of

video advertising which is outpacing the growth of other channels This growth is principally due to the increased revenue generatedby video ad formats compared to more traditional display bannerads Brands value the high click-through rate compared to otherdigital ad formats along with the potential for greater and moresophisticated creativity and significant user engagement

983161 The explosion of deal activity in video has continued beyond thedata captured in our analysis (which covers up to H1 2014)ndash Facebook acquired LiveRail in July and RTL acquired SpotXchangein August both driven by an increasing need to service their largebrand advertisers across this channel

983161 Given the cost of video ad creation and competition for premiuminventory video has typically been dominated to date by large

brand advertisers however technology is opening the format tosmaller advertisers YouTube has made a play to attract a greater SMEadvertiser base through its recent acquisition of self-serve video adcreation platform Directr

Data Management Platforms (DMPs)

983161 There has been significant consolidation of the largest independentDMPs in 2014 as both the enterprise software vendors and theAdTech vendors recognise that data is now a key battleground

983161 Leverage use and manipulation of both first and third party datais a high value capability underpinning omni-channel targetingaudience profiling and ultimately ROI

983161 Clients are on the one hand actively encouraging integration withtheir CRM systems and other data sources in order to drive targeted

media buying and on the other becoming increasingly concernedabout how their data is being used by third parties

983161 DMP deals have been high profile and high value ndash notable dealsinclude Oraclersquos acquisition of BlueKai Rocket Fuelrsquos acquisition of[x+1] and IgnitionOnersquos acquisition of Knotice

It is worth commenting briefly on Ad networks Although deal activityis broadly flat compared to 2013 it remains a sizeable subsegmentMany Ad networks are now focused on adding technology self-servecapability and programmatic to their business and re-inventingthemselves as DSPs and SSPs Pure-play Ad networks continue to beattractive targets where they bring scale channel expertise (eg mobile

or video) and direct premium publisher relationships

MarTech

MarTech deal activity reveals three subsegments where H1 2014 dealvolume is close to or has already surpassed 2013 levels (Figure 3)

Marketing analytics

983161 18 deals have occurred in this sub-segment and if deal activityremains at these levels the number of transactions is on track totreble in 2014 from the 12 deals in 2013

983161 Activity is driven primarily by the need to understand increasinglycomplex customer journeys not just across digital channels but alsointo the physical world Acxiomrsquos acquisition of LiveRamp is a goodexample of this trend

983161 Clients are demanding an increasingly detailed view of a customerrsquos journey to purchase in order to apportion spend across the channelslikely to generate the highest ROI Consequently marketingattribution has attracted a lot of interest with three deals alonecompleting in May 2014 (Googlersquos acquisition of Adometry Rakutenrsquosacquisition of DC Storm and AOLrsquos acquisition of Convertro) Thesetransactions enable the acquirers to bring their channels togetherinto a more coherent omni-channel proposition

Mobile983161 Mobile does of course cut across many of the subsegments in both

AdTech and MarTech In our categorisation this subsegment refersprimarily to mobile marketing automation and messaging mobileloyalty and voucher businesses and mobile payments technologies There have been 43 deals in H1 2014 already close to matching the45 deals seen in the whole of 2013

983161 Whilst mobile payment technologies might more conventionally beconsidered to fall within financial technology there are increasinglyclose ties between payment mechanisms and mobile as a means toclose the online to offline loop and as another channel for customerengagement

983161 Deal activity has also been high around innovations in mobile

marketing automation and in-app messaging (for exampleResponsysrsquo acquisition of Push IO)

Social

983161 The increasing impact of social media on consumer decision-making has been well documented and areas such as analyticsand customer reviews continue to drive considerable deal activityHowever the role of social has also increased in other aspects of thesales and marketing channel such as customer care and sales

983161 One clear trend in 2014 has been the rise of social mediarsquos impact onB2B marketing and sales ndash and we have started to see a number ofdeals driven by the rise of ldquosocial sellingrdquo in the B2B channel

983161 Deals in H1 2014 include Lithiumrsquos acquisition of Klout Bazaarvoicersquos

acquisition of FeedMagnet Twitterrsquos acquisition of Mesagraph andCallidusrsquo acquisition of LeadRocket

Video

DSP Ad network

AdTech deals by subsegment Figure 2

Measurement and optimisation

Ad server DMP

Ad creation SSP

Ad exchange

Agency buying desk

7

11

1410

5

2

4

52 1

2013

14

11

8

7

5

5

32 2

H1 2014

MarTech deals by subsegment Figure 3

Mobile Social

eCommerce

Marketing analytics Marketing Automation

Marketing management

Website amp SEO CRM

Crowd sourcing technology

45

31

20

12

14

19

129

2013

43

3618

18

13

13

8 2

1

H1 2014

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 512

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 5

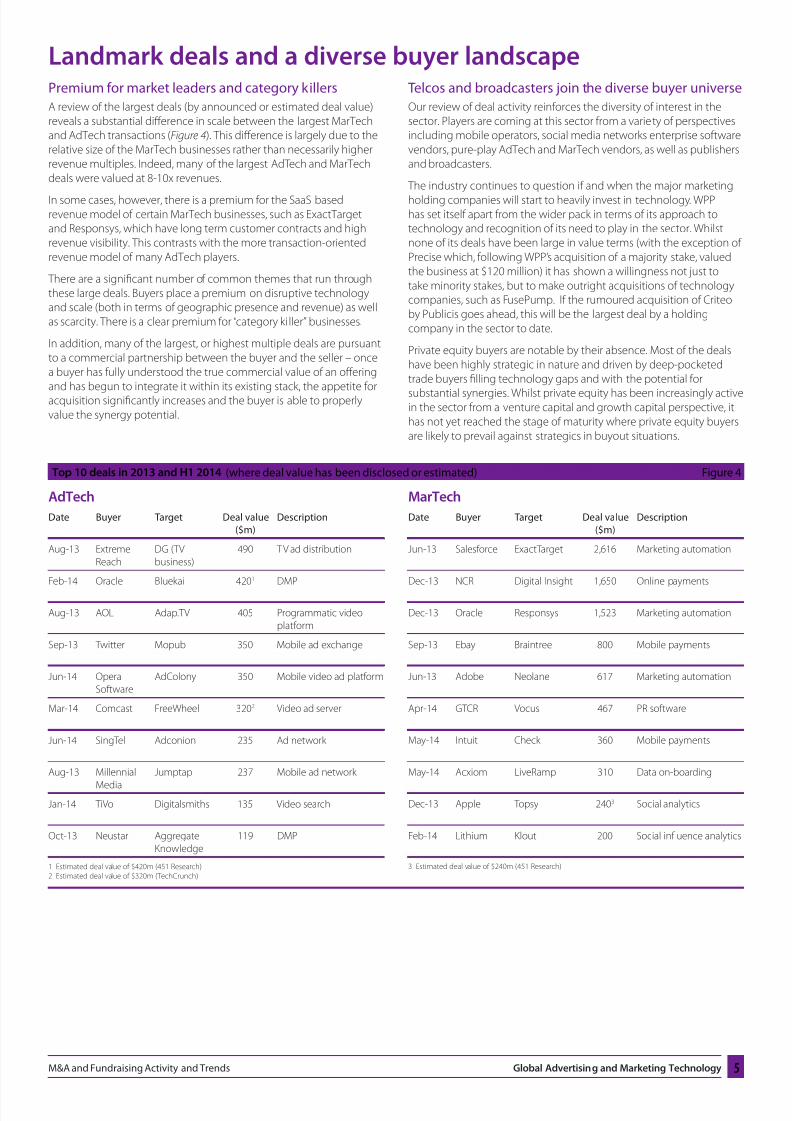

Landmark deals and a diverse buyer landscape

AdTech

Date Buyer Target Deal value($m)

Description

Aug-13 ExtremeReach

DG (TVbusiness)

490 T V ad distribution

Feb-14 Oracle Bluekai 4201 DMP

Aug-13 AOL AdapTV 405 Programmatic videoplatform

Sep-13 Twitter Mopub 350 Mobile ad exchange

Jun-14 OperaSoftware

AdColony 350 Mobile video ad platform

Mar-14 Comcast FreeWheel 3202 Video ad server

Jun-14 SingTel Adconion 235 Ad network

Aug-13 Millennial

Media

Jumptap 237 Mobile ad network

Jan-14 TiVo Digitalsmiths 135 Video search

Oct-13 Neustar AggregateKnowledge

119 DMP

1 Estimated deal value of $420m (451 Research)2 Estimated deal value of $320m (TechCrunch)

MarTech

Date Buyer Target Deal value($m)

Description

Jun-13 Salesforce ExactTarget 2616 Marketing automation

Dec-13 NCR Digital Insight 1650 Online payments

Dec-13 Oracle Responsys 1523 Marketing automation

Sep-13 Ebay Braintree 800 Mobile payments

Jun-13 Adobe Neolane 617 Marketing automation

Apr-14 GTCR Vocus 467 PR software

May-14 Intuit Check 360 Mobile payments

May-14 Acxiom LiveRamp 310 Data on-boarding

Dec-13 Apple Topsy 2403 Social analytics

Feb-14 Lithium Klout 200 Social influence analytics

3 Estimated deal value of $240m (451 Research)

Premium for market leaders and category killers

A review of the largest deals (by announced or estimated deal value)reveals a substantial difference in scale between the largest MarTechand AdTech transactions (Figure 4) This difference is largely due to therelative size of the MarTech businesses rather than necessarily higherrevenue multiples Indeed many of the largest AdTech and MarTechdeals were valued at 8-10x revenues

In some cases however there is a premium for the SaaS basedrevenue model of certain MarTech businesses such as ExactTargetand Responsys which have long term customer contracts and highrevenue visibility This contrasts with the more transaction-orientedrevenue model of many AdTech players

There are a significant number of common themes that run throughthese large deals Buyers place a premium on disruptive technologyand scale (both in terms of geographic presence and revenue) as wellas scarcity There is a clear premium for ldquocategory ki llerrdquo businesses

In addition many of the largest or highest multiple deals are pursuantto a commercial partnership between the buyer and the seller ndash oncea buyer has fully understood the true commercial value of an offeringand has begun to integrate it within its existing stack the appetite foracquisition significantly increases and the buyer is able to properlyvalue the synergy potential

Top 10 deals in 2013 and H1 2014 (where deal value has been disclosed or estimated) Figure 4

Telcos and broadcasters join the diverse buyer universe

Our review of deal activity reinforces the diversity of interest in thesector Players are coming at this sector from a variety of perspectivesincluding mobile operators social media networks enterprise softwarevendors pure-play AdTech and MarTech vendors as well as publishersand broadcasters

The industry continues to question if and when the major marketing

holding companies will start to heavily invest in technology WPPhas set itself apart from the wider pack in terms of its approach totechnology and recognition of its need to play in the sector Whilstnone of its deals have been large in value terms (with the exception ofPrecise which following WPPrsquos acquisition of a majority stake valuedthe business at $120 million) it has shown a willingness not just totake minority stakes but to make outright acquisitions of technologycompanies such as FusePump If the rumoured acquisition of Criteoby Publicis goes ahead this will be the largest deal by a holdingcompany in the sector to date

Private equity buyers are notable by their absence Most of the dealshave been highly strategic in nature and driven by deep-pocketedtrade buyers filling technology gaps and with the potential for

substantial synergies Whilst private equity has been increasingly activein the sector from a venture capital and growth capital perspective ithas not yet reached the stage of maturity where private equity buyersare likely to prevail against strategics in buyout situations

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 612

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends6

International buyers are looking to Europe for innovationCountry of target H1 2014 Figure 5

16

6

22913

139

4

APAC

Middle East

Eastern Europe

Western EuropeUK

North America

South America

As the market has matured in Europe and a large number of US playershave reached substantial scale in their domestic market we expect awave of more sizeable acquisitions over the next 18 months driven byinternational expansion

European landscape dominated by smaller companies

than US

It is interesting to note that only one of the 20 deals in Figure 4 on theprevious page involved a European-headquartered target the sale ofNeolane to Adobe Adconion was founded in the UK but had relocatedits headquarters to the US

There is an evident difference in scale between the leading US andEuropean players although this does of course mirror the broader techand software market However specifically in AdTech the ability ofEuropean players to scale as quickly as their US counterparts has in partbeen impacted by the nature of the European media buying marketbuilt on an ecosystem of national buying and national publishingCompanies that are able to build a true pan-European presence willbecome prime acquisition targets

US actively looking to Europe for innovation

European sellers accounted for 44 of the total of 209 transactions inH1 2014 (Figure 5) broadly comparable as a percentage to 2013 Ofthose 44 transactions 17 were acquired by US buyers Many of thesetransactions were primarily technology buys (Figure 6) focused on

the addition of talent and point technology rather than a strategicimperative for scale or geographic expansion

Recent acquisitions by US and Asian buyers in Europe ndash selected deals Figure 6

Date Buyer Target Buyer Region Target Region Description

Jul-14 Netsuite Venda US UK eCommerce platform

Jun-14 AppNexus Alenty US France Ad viewability measurement

Jun-14 Facebook Pryte US Finland Mobile data access

May-14 Microsoft Capptain US France Mobile app management platform

May-14 Rakuten DC Storm Japan UK Tag management and attribution

Apr-14 MediaMath Tactads US France Cookieless targeting

Apr-14 Twitter SecondSync US UK Social analytics for TV

Apr-14 Twitter Mesagraph US France Social TV analytics

Mar-14 Ensighten TagMan US UK Tag management

Feb-14 Google Spiderio US UK Ad fraud identification

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 712

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 7

Part 2

Fundraising Activity

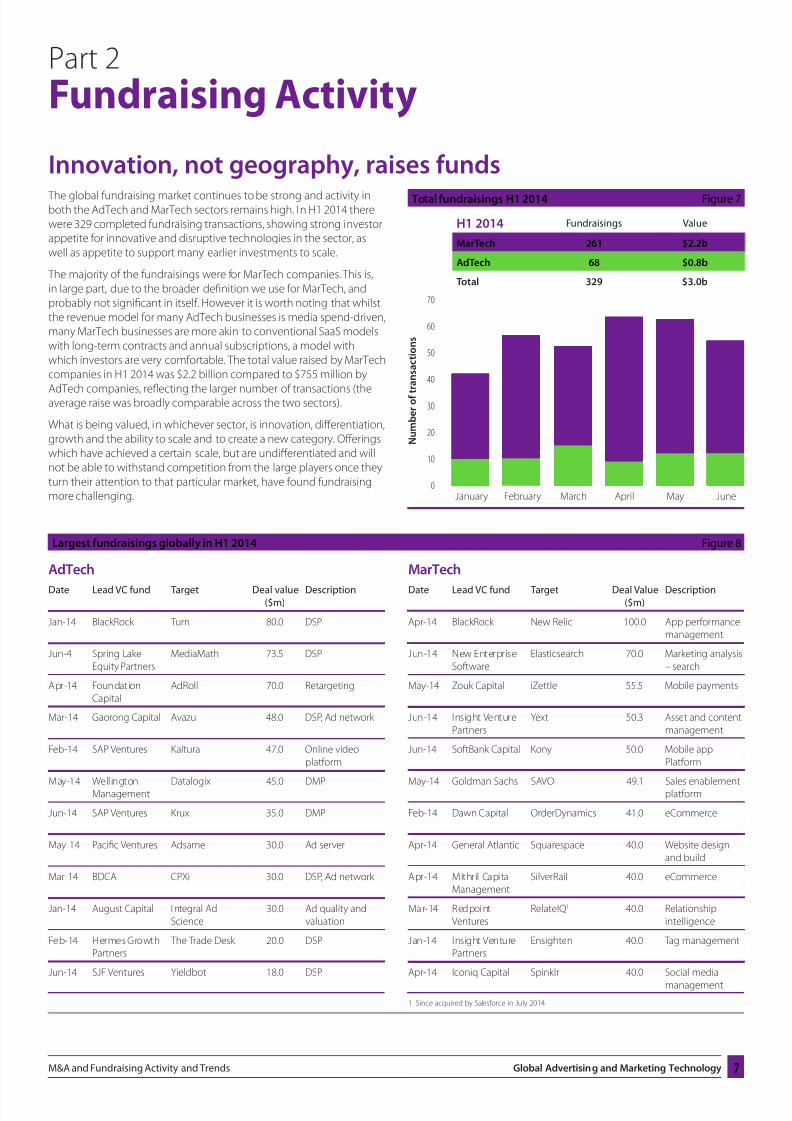

Innovation not geography raises funds

The global fundraising market continues to be strong and activity inboth the AdTech and MarTech sectors remains high In H1 2014 therewere 329 completed fundraising transactions showing strong investorappetite for innovative and disruptive technologies in the sector aswell as appetite to support many earlier investments to scale

The majority of the fundraisings were for MarTech companies This isin large part due to the broader definition we use for MarTech andprobably not significant in itself However it is worth noting that whilstthe revenue model for many AdTech businesses is media spend-drivenmany MarTech businesses are more akin to conventional SaaS modelswith long-term contracts and annual subscriptions a model withwhich investors are very comfortable The total value raised by MarTechcompanies in H1 2014 was $22 billion compared to $755 million by

AdTech companies reflecting the larger number of transactions (theaverage raise was broadly comparable across the two sectors)

What is being valued in whichever sector is innovation differentiationgrowth and the ability to scale and to create a new category Offeringswhich have achieved a certain scale but are undifferentiated and willnot be able to withstand competition from the large players once theyturn their attention to that particular market have found fundraisingmore challenging

Largest fundraisings globally in H1 2014 Figure 8

AdTech

Date Lead VC fund Target Deal value($m)

Description

Jan-14 BlackRock Turn 800 DSP

Jun-4 Spring LakeEquity Partners

MediaMath 735 DSP

Apr-14 FoundationCapital

AdRoll 700 Retargeting

Mar-14 Gaorong Capital Avazu 480 DSP Ad network

Feb-14 SAP Ventures Kaltura 470 Online videoplatform

May-14 WellingtonManagement Datalogix 450 DMP

Jun-14 SAP Ventures Krux 350 DMP

May-14 Pacific Ventures Adsame 300 Ad server

Mar-14 BDCA CPXi 300 DSP Ad network

Jan-14 August Capital Integral AdScience

300 Ad quality andvaluation

Feb-14 Hermes GrowthPartners

The Trade Desk 200 DSP

Jun-14 SJF Ventures Yieldbot 180 DSP

MarTech

Date Lead VC fund Target Deal Value($m)

Description

Apr-14 BlackRock New Relic 1000 App performancemanagement

Jun-14 New EnterpriseSoftware

Elasticsearch 700 Marketing analysisndash search

May-14 Zouk Capital iZettle 555 Mobile payments

Jun-14 Insight VenturePartners

Yext 503 Asset and contentmanagement

Jun-14 SoftBank Capital Kony 500 Mobile appPlatform

May-14 Goldman Sachs SAVO 491 Sales enablementplatform

Feb-14 Dawn Capital OrderDynamics 410 eCommerce

Apr-14 General Atlantic Squarespace 400 Website designand build

Apr-14 Mithril CapitalManagement

SilverRail 400 eCommerce

Mar-14 RedpointVentures

RelateIQ1 400 Relationshipintelligence

Jan-14 Insight VenturePartners

Ensighten 400 Tag management

Apr-14 Iconiq Capital Spinklr 400 Social media

management

1 Since acquired by Salesforce in July 2014

70

60

50

40

30

20

10

0

N u m b e r o f t

r a n s a c t i o n s

January February March April May June

H1 2014 Fundraisings Value

MarTech 261 $22b

AdTech 68 $08b

Total 329 $30b

Total fundraisings H1 2014 Figure 7

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 812

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends8

Fundraising activity by subsegmentMarTech

49

48

46

37

36

19

1212

2

eCommerce

Social

Mobile

Marketing analytics

CRM

Marketing automation

Marketingmanagement

Website amp SEO

Crowd sourcing technology

MarTech fundraisings H1 2014 Figure 10

eCommerce

983161 As the global adoption of online shopping continues to drive

double-digit growth in eCommerce there has been considerableinnovation both in core eCommerce platforms but also acrossanalytics personalisation payments curation and online to offline

983161 Fundraisings have ranged from large series C investmentsinto companies including OrderDynamics (formerly known aseCommera in omnichannel order management) and SilverRail (rai l-ticketing) to earlier stage rounds for companies including Sweden-based Tictail (eCommerce platform for boutique and smaller highstreet retailers) Peerius (personalisation and recommendations) andSpree Commerce (Open source eCommerce platform)

Social

983161 Mirroring the trend in MampA investors too are cognisant of the rising

influence that social media has on the decision-path to purchaseand significant amounts have been invested in the US and Europe inofferings designed to use social to enhance the sales and marketingprocess

983161 Sprinklr was the largest pure social investment in H1 raising $40million for its social software platform and Spredfast raised $325million for its social marketing platform

983161 In Europe TrustPilot an online review platform and Brandwatch asocial media monitoring and analytics solution both raised in excessof $20 million in H1 2014

AdTech

AdTech fundraisings H1 2014 Figure 9

20

10

9

6

6

5

6

42

DSP

Video

Measurement and

optimisation

DMP

SSP

Ad creation

Ad network

Ad exchange

Ad server

Video

983161 Video is the fastest growing advertising channel but has not until

now been able to provide the same level of targeting data andanalytics as display advertising and therefore itrsquos not surprising tosee the high level of investment in the sector Investment is goinginto solutions which improve data collection and analytics audienceprofiling and targeting and measurement and tracking as well asinfrastructure-based video solutions and self-serve offerings

983161 With the exception of Kaltura (an open source online videoplatform) which raised $47 million fundraisings in video have beenpredominantly earlier stage smaller funding rounds The secondlargest fundraise in the space was by Vungle a mobile video adplatform which raised $17 million

DSP

983161 Established DSPs have been responsible for some of the largestfundraisings in H1 including Turn (which raised $80 million) and

MediaMath (which raised $735 million in equity as well as putting inplace a substantial credit facility)

983161 These two companies have raised financing to continue to fundinnovation but also to fuel expansion into new geographies andmarkets MediaMath has publicly stated that one use of funds willbe to pursue international MampA and Turn is also building out itsinternational footprint

983161 With a number of large DSPs such as MediaMath Turn and DataXualready well established in the market newer entrants need to beclearly differentiated to attract funding Yieldbot and Trade Deskhave both successfully raised significant rounds ($18 million and

$20 million respectively) Yieldbot focuses on capturing real-timeconsumer intent through search keywords and Trade Desk hasdemonstrated rapid international growth

983161 The majority of investments into DSPs and certainly the largest havebeen in the US Many of the largest European DSPs have been self-financing

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 912

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 9

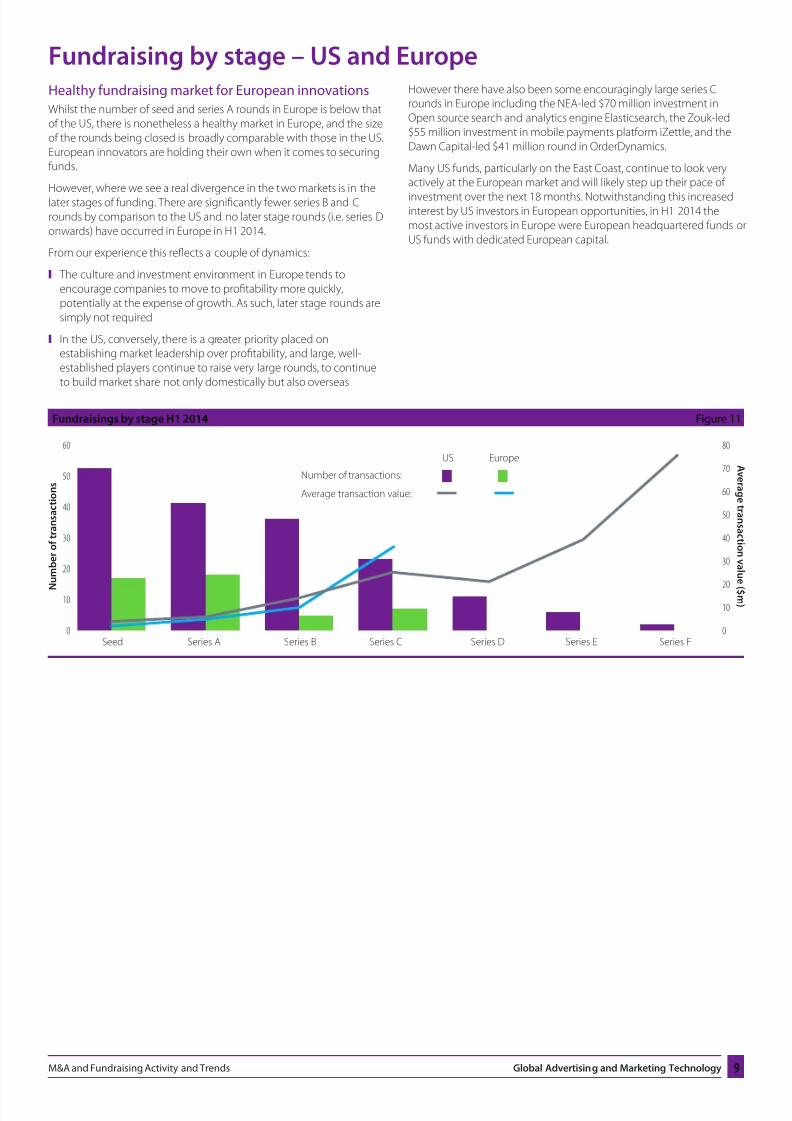

Fundraising by stage ndash US and EuropeHealthy fundraising market for European innovations

Whilst the number of seed and series A rounds in Europe is below thatof the US there is nonetheless a healthy market in Europe and the sizeof the rounds being closed is broadly comparable with those in the USEuropean innovators are holding their own when it comes to securingfunds

However where we see a real divergence in the two markets is in thelater stages of funding There are significantly fewer series B and Crounds by comparison to the US and no later stage rounds (ie series Donwards) have occurred in Europe in H1 2014

From our experience this reflects a couple of dynamics

983161 The culture and investment environment in Europe tends toencourage companies to move to profitability more quicklypotentially at the expense of growth As such later stage rounds aresimply not required

983161 In the US conversely there is a greater priority placed onestablishing market leadership over profitability and large well-established players continue to raise very large rounds to continueto build market share not only domestically but also overseas

However there have also been some encouragingly large series Crounds in Europe including the NEA-led $70 million investment inOpen source search and analytics engine Elasticsearch the Zouk-led$55 million investment in mobile payments platform iZettle and theDawn Capital-led $41 million round in OrderDynamics

Many US funds particularly on the East Coast continue to look veryactively at the European market and will likely step up their pace of

investment over the next 18 months Notwithstanding this increasedinterest by US investors in European opportunities in H1 2014 themost active investors in Europe were European headquartered funds orUS funds with dedicated European capital

60

50

40

30

20

10

0

80

70

60

50

40

30

20

10

0

N

u m b e r o f t r a n s a c t i o n s

A v er a g e t r an s a c t i onv al u e

( $ m )

Seed Series A Series B Series C Series D Series E Series F

US Europe

Number of transactions

Average transaction value

Fundraisings by stage H1 2014 Figure 11

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 1012

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends10

Appendix

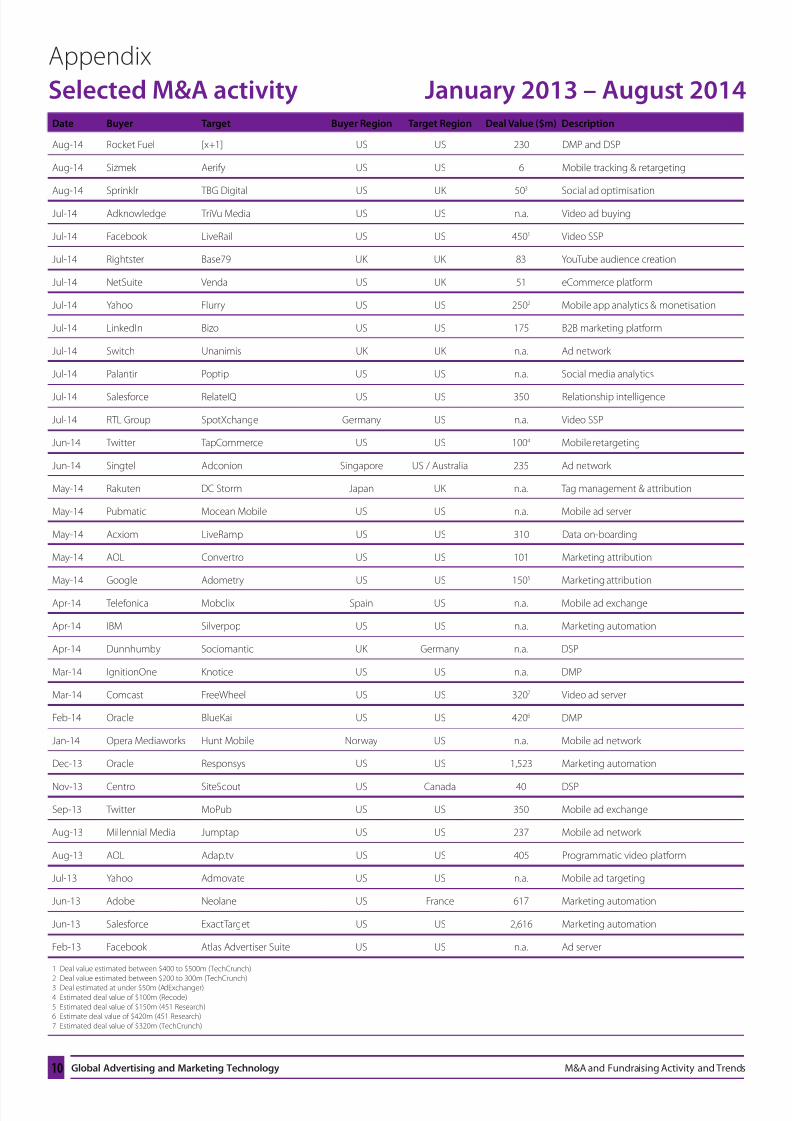

Selected MampA activity January 2013 ndash August 2014Date Buyer Target Buyer Region Target Region Deal Value ($m) Description

Aug-14 Rocket Fuel [x+1] US US 230 DMP and DSP

Aug-14 Sizmek Aerify US US 6 Mobile tracking amp retargeting

Aug-14 Sprinklr TBG Digital US UK 503 Social ad optimisation

Jul-14 Adknowledge TriVu Media US US na Video ad buying

Jul-14 Facebook LiveRail US US 4501 Video SSP

Jul-14 Rightster Base79 UK UK 83 YouTube audience creation

Jul-14 NetSuite Venda US UK 51 eCommerce platform

Jul-14 Yahoo Flurry US US 2502 Mobile app analytics amp monetisation

Jul-14 LinkedIn Bizo US US 175 B2B marketing platform

Jul-14 Switch Unanimis UK UK na Ad network

Jul-14 Palantir Poptip US US na Social media analytics

Jul-14 Salesforce RelateIQ US US 350 Relationship intelligence

Jul-14 RTL Group SpotXchange Germany US na Video SSP

Jun-14 Twitter TapCommerce US US 1004 Mobile retargeting

Jun-14 Singtel Adconion Singapore US Australia 235 Ad network

May-14 Rakuten DC Storm Japan UK na Tag management amp attribution

May-14 Pubmatic Mocean Mobile US US na Mobile ad server

May-14 Acxiom LiveRamp US US 310 Data on-boarding

May-14 AOL Convertro US US 101 Marketing attribution

May-14 Google Adometry US US 1505 Marketing attribution

Apr-14 Telefonica Mobclix Spain US na Mobile ad exchange

Apr-14 IBM Silverpop US US na Marketing automation

Apr-14 Dunnhumby Sociomantic UK Germany na DSP

Mar-14 IgnitionOne Knotice US US na DMP

Mar-14 Comcast FreeWheel US US 3207 Video ad server

Feb-14 Oracle BlueKai US US 4206 DMP

Jan-14 Opera Mediaworks Hunt Mobile Norway US na Mobile ad network

Dec-13 Oracle Responsys US US 1523 Marketing automation

Nov-13 Centro SiteScout US Canada 40 DSP

Sep-13 Twitter MoPub US US 350 Mobile ad exchange

Aug-13 Millennial Media Jumptap US US 237 Mobile ad network

Aug-13 AOL Adaptv US US 405 Programmatic video platform

Jul-13 Yahoo Admovate US US na Mobile ad targeting

Jun-13 Adobe Neolane US France 617 Marketing automation

Jun-13 Salesforce ExactTarget US US 2616 Marketing automation

Feb-13 Facebook Atlas Advertiser Suite US US na Ad server

1 Deal value estimated between $400 to $500m (TechCrunch)

2 Deal value estimated between $200 to 300m (TechCrunch)3 Deal estimated at under $50m (AdExchanger)

4 Estimated deal value of $100m (Recode)

5 Estimated deal value of $150m (451 Research)6 Estimate deal value of $420m (451 Research)

7 Estimated deal value of $320m (TechCrunch)

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 1112

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 11

Appendix

Selected Fundraising activity 2014 YTDDate Lead VC fund Target Target HQ Deal Value ($m) Description

Aug-14 Ignition Partners Xamarin USA 540 Moble app development

Aug-14 Private investors AppNexus USA 600 Ad exchange

Jul-14 Hony Capital Deem USA 500 Customer acquisition and engagement

Jul-14 Comerica mBlox USA 435 Mobile messaging

Jun-14 Softbank Capital IgnitionOne USA 300 Digital marketing suite

Jun-14 SoftBank Capital InsightVenture Partners

Kony USA 500 Moble app development

Jun-14 Deutsche Private Equity Webtrekk Germany 339 Web analytics

Jun-14 Tiger Global Management Freshdesk USA 310 Customer support software

Jun-14 DFJ SiSense Israel 300 Market analysis and business intelligence

Jun-14 SAP Ventures krux digital USA 350 DMP

Jun-14 New Enterprise Associates Elasticsearch Netherlands 700 Marketing analysis ndash search analytics

Jun-14 Insight Venture Partners Yext USA 503 Digital asset and content management

Jun-14 Spring Lake Equity Partners MediaMath USA 735 DSP

May-14 Goldman Sachs The SAVO Group USA 491 Sales enablement platform

May-14 Wellington ManagementCompany

DataLogix Holdings USA 450 DMP

May-14 Index Ventures BitPay USA 300 Bitcoin eCommerce payment

May-14 Pacific Venture Partners ampDream Capital Group

AdSame China 300 Ad server

May-14 Zouk Capital iZettle Sweden 555 Mobile payments

Apr-14 BlackRock New Relic USA 1000 App performance management

Apr-14 Tencent Sequoia Capital Weebly USA 350 Website design amp build

Apr-14 Foundation Capital Adroll USA 700 Retargeting

Apr-14 General Atlantic Squarespace USA 400 Website design amp buildApr-14 Mithril Capital Management SilverRail USA 400 eCommerce platform

Apr-14 Iconiq Capital Sprinklr USA 400 Social media management

Mar-14 Business DevelopmentCorporation of America

CPX Interactive USA 300 DSP Ad network

Mar-14 Redpoint Ventures RelateIQ1 USA 400 Relationship intelligence

Mar-14 FirstHand Technology ValueFund

Phunware USA 307 Mobile app development

Mar-14 Gaorang Capital Avazu China 480 DSP Ad network

Feb-14 Dawn Capital OrderDynamics UK 410 eCommerce platform

Feb-14 Institutional Venture Partners ZEFR USA 300 Brand and content management

Feb-14 SAP Ventures Nokia GrowthPartners Commonfund CapitalGera Ventures

Kaltura USA 470 Online video platform

Jan-14 Insight Venture Partners Ensighten USA 400 Tag management

Jan-14 BlackRock Turn USA 800 DSP

Jan-14 Lead Edge Capital Spredfast USA 325 Social media management

Jan-14 August Capital Integral Ad Science USA 300 Ad quality and valuation

1 Since acquired by Salesforce in July 2014

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 1212

Results International is a leading corporate finance advisor to marketing technology and healthcarecompanies in Europe and has advised on over 250 transactions The Company employs over 40 peopleglobally across offices in London New York and Asia and has a strong track record advising on cross-border

transactions winning MampA Cross Border Deal of the Year in the 2014 MampA Awards

Results Internationalrsquos 2014 AdTech and MarTech Deals

Disclaimer

Results International has compiled this report using data sourced from publicly availablesources and third-party tools to which it holds licensed access Results International doesnot accept any responsibility for the accuracy of the information provided Nor does ResultsInternational accept any liability for any use of the information provided in this report or anyconsequence from its use thereof

Keith Hunt

Managing Partner +44 (0) 207 514 8232keithhuntresultsigcom

Pierre-Georges Roy

Partner +1 646 747 6505pgroyresultsigcom

Mark Williams Director +44 (0) 207 514 8242mwilliamsresultsigcom

Julie Langley Partner +44 (0) 207 514 8247 jlangleyresultsigcom

Maurice Watkins

Partner +1 646 747 6510mwatkinsresultsigcom

Julia Crawley-Boevey Director +44 (0) 207 514 8239 jcrawley-boeveyresultsigcom

Jim Houghton

Partner +44 (0) 207 514 8234 jhoughtonresultsigcom

Chris Lewis Managing Director +44 (0) 207 514 8236clewisresultsigcom

has been acquired by

Results International acted forDC Storm

has been acquired by

Results International acted forWe Are Social

is joining

Results International served as

an exclusive financial adviserto Hunt

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 212

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends2

Our predictions983161 Enterprise software vendors will continue to move not just into marketing technology but more squarely into the media end of the

advertising technology sector

983161 The largest and fastest growing US AdTech players will move more aggressively into Europe making strategic acquisitions not just fortechnology but for geographic scale and revenue

983161 The online and offline worlds will further converge as large offline players seek to leverage their increasingly valuable offline datasets andexpertise Partnerships and MampA will occur as digital marketing stacks seek to inform media buying with integration of offline data

983161 The buyer universe for AdTech and MarTech companies will continue to diversify Telcos publishers broadcasters tech infrastructurevendors and traditional data companies will become active acquirers

983161 Pan-European winners with a presence in the main European media markets will emerge

983161 The European Private Equity community will become more active in the sector as European champions reach greater scale

The advertising and marketing technologymarkets continue to evolve at paceWhilst the public markets have beenunfavourable for many AdTech andMarTech businesses so far in 2014 MampAactivity continues to flourish and if dealactivity continues at the current pace2014 will see twice the number of deals as2013 The level of MampA activity has beendriven by a number of trends

Innovation in technology and channels

Constant innovation in technology and the way consumers engagewith media has driven vast amounts of MampA as buyers seek to stayahead of a rapidly changing market Particularly hot areas haveincluded video mobile social multi-screening and online to offline

where the large digital media players such as Yahoo AOL Facebook Twitter and Google have been very active

New entrants

Interest in the sector is coming from an increasingly diverse groupof buyers Amongst the telcos Telefonica SingTel and Telstra have allmade significant acquisitions in AdTech Also broadcasters such asRTL and Comcast have made bold moves into video advertising withan eye to establishing a presence in the online as well as offline (TV)market

Emergence of pure-play buyers of scale

The rapid growth of businesses like AppNexus MediaMath and Turnwhich have raised substantial sums of growth capital has created a

pool of sizeable private buyers able to make significant acquisitionsdriven by technology geographic expansion and scale

Continued integration between enterprise software and AdTech

For a couple of years now enterprise software vendors such as Oracleand Salesforce have been very acquisitive in areas such as marketingautomation as they extend their CRM business into a broadermarketing and customer engagement suite In 2014 we have seen theenterprise software vendors move much more squarely into AdTechfor example Oraclersquos acquisition of BlueKai and we expect much moreof this kind of deal activity to occur in the future as other vendors makesimilar moves

The battle for data

Access to data to improve targeting and better understand the

customer journey has driven substantial deal activity Particularly hotthemes have included the role of offline data in closing the loop forin-store purchases omni-channel attribution as a means of betterunderstanding customer journeys and various applications of bigdata whether across mobile search or social We have also seen bothadvertisers and publishers thinking more strategically about thevalue of their first party data and how that should be leveraged (andprotected) as the eco-system evolves

All eyes on Europe

From a European perspective an exciting development has been thenumber of US and overseas players looking to Europe for technologyand innovation whether that rsquos Google buying Spiderio Twitter buyingSecondSync or Rakuten buying DC Storm Europe is well and truly

front of mind for the large US players right now and we expect 2014and beyond to see an uptick in the level of activity amongst US playerslooking to expand in Europe whether via acquisition or organically

International fundraising strengthens

Fundraising activity is strong and showing no signs of slowing oneither side of the Atlantic Investors remain committed to fundinginnovation and disruption as well as supporting successful investmentsthrough to international scale Over $3 billion of investment was madein the first half of 2014 The stage of investing reflects the fact thatparts of the market are now well established with international marketleaders and yet other areas continue to be disrupted by innovativenew entrants Hence there were several $60 million-plus late-stage pre-IPO rounds as well as over 160 seed and series A investments made

into earlier-stage disruptive entrants all within the first half of 2014 The level of funding in Europe particularly at seed series A and seriesB stage is also encouraging as is the growing interest amongst USinvestors in Europe attracted by the level of innovation ambition andtalent of founders and management teams

Itrsquos an exciting time to be working in the sector and we look forward tocontinued high levels of activity in the rest of 2014 and beyond

ForewordBy Julie Langley Partner

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 312

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 3

Global deal volume in 2014 set to double over 2013 levels

Global MampA activity in the sector has seen a huge uplift in 2014 as theindustry has continued to grow and mature (Figure 1)

Across the spectrum of deals that have occurred the nature of MampAactivity has visibly evolved Deals are increasingly driven by the needfor scale geographic expansion access to data and new channels asthe race to be the leading global vendors in the sector heats up

Key observations

983161 The number of deals completed in H1 alone was nearly as high asin the whole of 2013 If deal activity continues at this pace ndash andactivity through July and August suggests it will ndash then deal volumein 2014 will be close to double that of 2013

983161 MarTech companies represent about 70 of overall deal volumeboth in 2013 and H1 2014 This in part reflects the high level of dealactivity undertaken by the large enterprise software vendors as theybuild out their cloud marketing suites

Part 1

MampA Activity

983161 In addition competition in the battle for client ad spend continuesto grow as new buyers ranging from social media networks(eg Twitter and LinkedIn) to telcos (eg SingTel and Telefonica)seek to enter the AdTech and MarTech sector through strategicacquisitions

983161 Deal value for AdTech is on track to double in 2014 over 2013with average deal value remaining broadly constant Deal valuefor MarTech is down on an annualised basis compared to 2013however this reflects a handful of very large deals which took placein 2013 including Oraclersquos $15 billion acquisition of Responsys andSalesforcersquos $26 billion acquisition of ExactTarget

50

40

30

20

10

0

N u m b e r o f d e a l s

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

2013 Number Value

MarTech 162 $85b

AdTech 61 $18b

Total 223 $103b

H1 2014 Number Value

MarTech 152 $22b

AdTech 57 $20b

Total 209 $42b

Global deal volume (January 2013 to June 2014) Figure 1

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 412

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends4

Deal activity by subsegmentAdTech

Two subsegments have experienced a significant increase in dealactivity in 2014 (Figure 2)

Video

983161 Deal activity has risen from just 7 deals in the whole of 2013 to 14deals in H1 2014 alone Activity is underpinned by the rapid rise of

video advertising which is outpacing the growth of other channels This growth is principally due to the increased revenue generatedby video ad formats compared to more traditional display bannerads Brands value the high click-through rate compared to otherdigital ad formats along with the potential for greater and moresophisticated creativity and significant user engagement

983161 The explosion of deal activity in video has continued beyond thedata captured in our analysis (which covers up to H1 2014)ndash Facebook acquired LiveRail in July and RTL acquired SpotXchangein August both driven by an increasing need to service their largebrand advertisers across this channel

983161 Given the cost of video ad creation and competition for premiuminventory video has typically been dominated to date by large

brand advertisers however technology is opening the format tosmaller advertisers YouTube has made a play to attract a greater SMEadvertiser base through its recent acquisition of self-serve video adcreation platform Directr

Data Management Platforms (DMPs)

983161 There has been significant consolidation of the largest independentDMPs in 2014 as both the enterprise software vendors and theAdTech vendors recognise that data is now a key battleground

983161 Leverage use and manipulation of both first and third party datais a high value capability underpinning omni-channel targetingaudience profiling and ultimately ROI

983161 Clients are on the one hand actively encouraging integration withtheir CRM systems and other data sources in order to drive targeted

media buying and on the other becoming increasingly concernedabout how their data is being used by third parties

983161 DMP deals have been high profile and high value ndash notable dealsinclude Oraclersquos acquisition of BlueKai Rocket Fuelrsquos acquisition of[x+1] and IgnitionOnersquos acquisition of Knotice

It is worth commenting briefly on Ad networks Although deal activityis broadly flat compared to 2013 it remains a sizeable subsegmentMany Ad networks are now focused on adding technology self-servecapability and programmatic to their business and re-inventingthemselves as DSPs and SSPs Pure-play Ad networks continue to beattractive targets where they bring scale channel expertise (eg mobile

or video) and direct premium publisher relationships

MarTech

MarTech deal activity reveals three subsegments where H1 2014 dealvolume is close to or has already surpassed 2013 levels (Figure 3)

Marketing analytics

983161 18 deals have occurred in this sub-segment and if deal activityremains at these levels the number of transactions is on track totreble in 2014 from the 12 deals in 2013

983161 Activity is driven primarily by the need to understand increasinglycomplex customer journeys not just across digital channels but alsointo the physical world Acxiomrsquos acquisition of LiveRamp is a goodexample of this trend

983161 Clients are demanding an increasingly detailed view of a customerrsquos journey to purchase in order to apportion spend across the channelslikely to generate the highest ROI Consequently marketingattribution has attracted a lot of interest with three deals alonecompleting in May 2014 (Googlersquos acquisition of Adometry Rakutenrsquosacquisition of DC Storm and AOLrsquos acquisition of Convertro) Thesetransactions enable the acquirers to bring their channels togetherinto a more coherent omni-channel proposition

Mobile983161 Mobile does of course cut across many of the subsegments in both

AdTech and MarTech In our categorisation this subsegment refersprimarily to mobile marketing automation and messaging mobileloyalty and voucher businesses and mobile payments technologies There have been 43 deals in H1 2014 already close to matching the45 deals seen in the whole of 2013

983161 Whilst mobile payment technologies might more conventionally beconsidered to fall within financial technology there are increasinglyclose ties between payment mechanisms and mobile as a means toclose the online to offline loop and as another channel for customerengagement

983161 Deal activity has also been high around innovations in mobile

marketing automation and in-app messaging (for exampleResponsysrsquo acquisition of Push IO)

Social

983161 The increasing impact of social media on consumer decision-making has been well documented and areas such as analyticsand customer reviews continue to drive considerable deal activityHowever the role of social has also increased in other aspects of thesales and marketing channel such as customer care and sales

983161 One clear trend in 2014 has been the rise of social mediarsquos impact onB2B marketing and sales ndash and we have started to see a number ofdeals driven by the rise of ldquosocial sellingrdquo in the B2B channel

983161 Deals in H1 2014 include Lithiumrsquos acquisition of Klout Bazaarvoicersquos

acquisition of FeedMagnet Twitterrsquos acquisition of Mesagraph andCallidusrsquo acquisition of LeadRocket

Video

DSP Ad network

AdTech deals by subsegment Figure 2

Measurement and optimisation

Ad server DMP

Ad creation SSP

Ad exchange

Agency buying desk

7

11

1410

5

2

4

52 1

2013

14

11

8

7

5

5

32 2

H1 2014

MarTech deals by subsegment Figure 3

Mobile Social

eCommerce

Marketing analytics Marketing Automation

Marketing management

Website amp SEO CRM

Crowd sourcing technology

45

31

20

12

14

19

129

2013

43

3618

18

13

13

8 2

1

H1 2014

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 512

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 5

Landmark deals and a diverse buyer landscape

AdTech

Date Buyer Target Deal value($m)

Description

Aug-13 ExtremeReach

DG (TVbusiness)

490 T V ad distribution

Feb-14 Oracle Bluekai 4201 DMP

Aug-13 AOL AdapTV 405 Programmatic videoplatform

Sep-13 Twitter Mopub 350 Mobile ad exchange

Jun-14 OperaSoftware

AdColony 350 Mobile video ad platform

Mar-14 Comcast FreeWheel 3202 Video ad server

Jun-14 SingTel Adconion 235 Ad network

Aug-13 Millennial

Media

Jumptap 237 Mobile ad network

Jan-14 TiVo Digitalsmiths 135 Video search

Oct-13 Neustar AggregateKnowledge

119 DMP

1 Estimated deal value of $420m (451 Research)2 Estimated deal value of $320m (TechCrunch)

MarTech

Date Buyer Target Deal value($m)

Description

Jun-13 Salesforce ExactTarget 2616 Marketing automation

Dec-13 NCR Digital Insight 1650 Online payments

Dec-13 Oracle Responsys 1523 Marketing automation

Sep-13 Ebay Braintree 800 Mobile payments

Jun-13 Adobe Neolane 617 Marketing automation

Apr-14 GTCR Vocus 467 PR software

May-14 Intuit Check 360 Mobile payments

May-14 Acxiom LiveRamp 310 Data on-boarding

Dec-13 Apple Topsy 2403 Social analytics

Feb-14 Lithium Klout 200 Social influence analytics

3 Estimated deal value of $240m (451 Research)

Premium for market leaders and category killers

A review of the largest deals (by announced or estimated deal value)reveals a substantial difference in scale between the largest MarTechand AdTech transactions (Figure 4) This difference is largely due to therelative size of the MarTech businesses rather than necessarily higherrevenue multiples Indeed many of the largest AdTech and MarTechdeals were valued at 8-10x revenues

In some cases however there is a premium for the SaaS basedrevenue model of certain MarTech businesses such as ExactTargetand Responsys which have long term customer contracts and highrevenue visibility This contrasts with the more transaction-orientedrevenue model of many AdTech players

There are a significant number of common themes that run throughthese large deals Buyers place a premium on disruptive technologyand scale (both in terms of geographic presence and revenue) as wellas scarcity There is a clear premium for ldquocategory ki llerrdquo businesses

In addition many of the largest or highest multiple deals are pursuantto a commercial partnership between the buyer and the seller ndash oncea buyer has fully understood the true commercial value of an offeringand has begun to integrate it within its existing stack the appetite foracquisition significantly increases and the buyer is able to properlyvalue the synergy potential

Top 10 deals in 2013 and H1 2014 (where deal value has been disclosed or estimated) Figure 4

Telcos and broadcasters join the diverse buyer universe

Our review of deal activity reinforces the diversity of interest in thesector Players are coming at this sector from a variety of perspectivesincluding mobile operators social media networks enterprise softwarevendors pure-play AdTech and MarTech vendors as well as publishersand broadcasters

The industry continues to question if and when the major marketing

holding companies will start to heavily invest in technology WPPhas set itself apart from the wider pack in terms of its approach totechnology and recognition of its need to play in the sector Whilstnone of its deals have been large in value terms (with the exception ofPrecise which following WPPrsquos acquisition of a majority stake valuedthe business at $120 million) it has shown a willingness not just totake minority stakes but to make outright acquisitions of technologycompanies such as FusePump If the rumoured acquisition of Criteoby Publicis goes ahead this will be the largest deal by a holdingcompany in the sector to date

Private equity buyers are notable by their absence Most of the dealshave been highly strategic in nature and driven by deep-pocketedtrade buyers filling technology gaps and with the potential for

substantial synergies Whilst private equity has been increasingly activein the sector from a venture capital and growth capital perspective ithas not yet reached the stage of maturity where private equity buyersare likely to prevail against strategics in buyout situations

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 612

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends6

International buyers are looking to Europe for innovationCountry of target H1 2014 Figure 5

16

6

22913

139

4

APAC

Middle East

Eastern Europe

Western EuropeUK

North America

South America

As the market has matured in Europe and a large number of US playershave reached substantial scale in their domestic market we expect awave of more sizeable acquisitions over the next 18 months driven byinternational expansion

European landscape dominated by smaller companies

than US

It is interesting to note that only one of the 20 deals in Figure 4 on theprevious page involved a European-headquartered target the sale ofNeolane to Adobe Adconion was founded in the UK but had relocatedits headquarters to the US

There is an evident difference in scale between the leading US andEuropean players although this does of course mirror the broader techand software market However specifically in AdTech the ability ofEuropean players to scale as quickly as their US counterparts has in partbeen impacted by the nature of the European media buying marketbuilt on an ecosystem of national buying and national publishingCompanies that are able to build a true pan-European presence willbecome prime acquisition targets

US actively looking to Europe for innovation

European sellers accounted for 44 of the total of 209 transactions inH1 2014 (Figure 5) broadly comparable as a percentage to 2013 Ofthose 44 transactions 17 were acquired by US buyers Many of thesetransactions were primarily technology buys (Figure 6) focused on

the addition of talent and point technology rather than a strategicimperative for scale or geographic expansion

Recent acquisitions by US and Asian buyers in Europe ndash selected deals Figure 6

Date Buyer Target Buyer Region Target Region Description

Jul-14 Netsuite Venda US UK eCommerce platform

Jun-14 AppNexus Alenty US France Ad viewability measurement

Jun-14 Facebook Pryte US Finland Mobile data access

May-14 Microsoft Capptain US France Mobile app management platform

May-14 Rakuten DC Storm Japan UK Tag management and attribution

Apr-14 MediaMath Tactads US France Cookieless targeting

Apr-14 Twitter SecondSync US UK Social analytics for TV

Apr-14 Twitter Mesagraph US France Social TV analytics

Mar-14 Ensighten TagMan US UK Tag management

Feb-14 Google Spiderio US UK Ad fraud identification

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 712

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 7

Part 2

Fundraising Activity

Innovation not geography raises funds

The global fundraising market continues to be strong and activity inboth the AdTech and MarTech sectors remains high In H1 2014 therewere 329 completed fundraising transactions showing strong investorappetite for innovative and disruptive technologies in the sector aswell as appetite to support many earlier investments to scale

The majority of the fundraisings were for MarTech companies This isin large part due to the broader definition we use for MarTech andprobably not significant in itself However it is worth noting that whilstthe revenue model for many AdTech businesses is media spend-drivenmany MarTech businesses are more akin to conventional SaaS modelswith long-term contracts and annual subscriptions a model withwhich investors are very comfortable The total value raised by MarTechcompanies in H1 2014 was $22 billion compared to $755 million by

AdTech companies reflecting the larger number of transactions (theaverage raise was broadly comparable across the two sectors)

What is being valued in whichever sector is innovation differentiationgrowth and the ability to scale and to create a new category Offeringswhich have achieved a certain scale but are undifferentiated and willnot be able to withstand competition from the large players once theyturn their attention to that particular market have found fundraisingmore challenging

Largest fundraisings globally in H1 2014 Figure 8

AdTech

Date Lead VC fund Target Deal value($m)

Description

Jan-14 BlackRock Turn 800 DSP

Jun-4 Spring LakeEquity Partners

MediaMath 735 DSP

Apr-14 FoundationCapital

AdRoll 700 Retargeting

Mar-14 Gaorong Capital Avazu 480 DSP Ad network

Feb-14 SAP Ventures Kaltura 470 Online videoplatform

May-14 WellingtonManagement Datalogix 450 DMP

Jun-14 SAP Ventures Krux 350 DMP

May-14 Pacific Ventures Adsame 300 Ad server

Mar-14 BDCA CPXi 300 DSP Ad network

Jan-14 August Capital Integral AdScience

300 Ad quality andvaluation

Feb-14 Hermes GrowthPartners

The Trade Desk 200 DSP

Jun-14 SJF Ventures Yieldbot 180 DSP

MarTech

Date Lead VC fund Target Deal Value($m)

Description

Apr-14 BlackRock New Relic 1000 App performancemanagement

Jun-14 New EnterpriseSoftware

Elasticsearch 700 Marketing analysisndash search

May-14 Zouk Capital iZettle 555 Mobile payments

Jun-14 Insight VenturePartners

Yext 503 Asset and contentmanagement

Jun-14 SoftBank Capital Kony 500 Mobile appPlatform

May-14 Goldman Sachs SAVO 491 Sales enablementplatform

Feb-14 Dawn Capital OrderDynamics 410 eCommerce

Apr-14 General Atlantic Squarespace 400 Website designand build

Apr-14 Mithril CapitalManagement

SilverRail 400 eCommerce

Mar-14 RedpointVentures

RelateIQ1 400 Relationshipintelligence

Jan-14 Insight VenturePartners

Ensighten 400 Tag management

Apr-14 Iconiq Capital Spinklr 400 Social media

management

1 Since acquired by Salesforce in July 2014

70

60

50

40

30

20

10

0

N u m b e r o f t

r a n s a c t i o n s

January February March April May June

H1 2014 Fundraisings Value

MarTech 261 $22b

AdTech 68 $08b

Total 329 $30b

Total fundraisings H1 2014 Figure 7

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 812

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends8

Fundraising activity by subsegmentMarTech

49

48

46

37

36

19

1212

2

eCommerce

Social

Mobile

Marketing analytics

CRM

Marketing automation

Marketingmanagement

Website amp SEO

Crowd sourcing technology

MarTech fundraisings H1 2014 Figure 10

eCommerce

983161 As the global adoption of online shopping continues to drive

double-digit growth in eCommerce there has been considerableinnovation both in core eCommerce platforms but also acrossanalytics personalisation payments curation and online to offline

983161 Fundraisings have ranged from large series C investmentsinto companies including OrderDynamics (formerly known aseCommera in omnichannel order management) and SilverRail (rai l-ticketing) to earlier stage rounds for companies including Sweden-based Tictail (eCommerce platform for boutique and smaller highstreet retailers) Peerius (personalisation and recommendations) andSpree Commerce (Open source eCommerce platform)

Social

983161 Mirroring the trend in MampA investors too are cognisant of the rising

influence that social media has on the decision-path to purchaseand significant amounts have been invested in the US and Europe inofferings designed to use social to enhance the sales and marketingprocess

983161 Sprinklr was the largest pure social investment in H1 raising $40million for its social software platform and Spredfast raised $325million for its social marketing platform

983161 In Europe TrustPilot an online review platform and Brandwatch asocial media monitoring and analytics solution both raised in excessof $20 million in H1 2014

AdTech

AdTech fundraisings H1 2014 Figure 9

20

10

9

6

6

5

6

42

DSP

Video

Measurement and

optimisation

DMP

SSP

Ad creation

Ad network

Ad exchange

Ad server

Video

983161 Video is the fastest growing advertising channel but has not until

now been able to provide the same level of targeting data andanalytics as display advertising and therefore itrsquos not surprising tosee the high level of investment in the sector Investment is goinginto solutions which improve data collection and analytics audienceprofiling and targeting and measurement and tracking as well asinfrastructure-based video solutions and self-serve offerings

983161 With the exception of Kaltura (an open source online videoplatform) which raised $47 million fundraisings in video have beenpredominantly earlier stage smaller funding rounds The secondlargest fundraise in the space was by Vungle a mobile video adplatform which raised $17 million

DSP

983161 Established DSPs have been responsible for some of the largestfundraisings in H1 including Turn (which raised $80 million) and

MediaMath (which raised $735 million in equity as well as putting inplace a substantial credit facility)

983161 These two companies have raised financing to continue to fundinnovation but also to fuel expansion into new geographies andmarkets MediaMath has publicly stated that one use of funds willbe to pursue international MampA and Turn is also building out itsinternational footprint

983161 With a number of large DSPs such as MediaMath Turn and DataXualready well established in the market newer entrants need to beclearly differentiated to attract funding Yieldbot and Trade Deskhave both successfully raised significant rounds ($18 million and

$20 million respectively) Yieldbot focuses on capturing real-timeconsumer intent through search keywords and Trade Desk hasdemonstrated rapid international growth

983161 The majority of investments into DSPs and certainly the largest havebeen in the US Many of the largest European DSPs have been self-financing

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 912

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 9

Fundraising by stage ndash US and EuropeHealthy fundraising market for European innovations

Whilst the number of seed and series A rounds in Europe is below thatof the US there is nonetheless a healthy market in Europe and the sizeof the rounds being closed is broadly comparable with those in the USEuropean innovators are holding their own when it comes to securingfunds

However where we see a real divergence in the two markets is in thelater stages of funding There are significantly fewer series B and Crounds by comparison to the US and no later stage rounds (ie series Donwards) have occurred in Europe in H1 2014

From our experience this reflects a couple of dynamics

983161 The culture and investment environment in Europe tends toencourage companies to move to profitability more quicklypotentially at the expense of growth As such later stage rounds aresimply not required

983161 In the US conversely there is a greater priority placed onestablishing market leadership over profitability and large well-established players continue to raise very large rounds to continueto build market share not only domestically but also overseas

However there have also been some encouragingly large series Crounds in Europe including the NEA-led $70 million investment inOpen source search and analytics engine Elasticsearch the Zouk-led$55 million investment in mobile payments platform iZettle and theDawn Capital-led $41 million round in OrderDynamics

Many US funds particularly on the East Coast continue to look veryactively at the European market and will likely step up their pace of

investment over the next 18 months Notwithstanding this increasedinterest by US investors in European opportunities in H1 2014 themost active investors in Europe were European headquartered funds orUS funds with dedicated European capital

60

50

40

30

20

10

0

80

70

60

50

40

30

20

10

0

N

u m b e r o f t r a n s a c t i o n s

A v er a g e t r an s a c t i onv al u e

( $ m )

Seed Series A Series B Series C Series D Series E Series F

US Europe

Number of transactions

Average transaction value

Fundraisings by stage H1 2014 Figure 11

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 1012

Global Advertising and Marketing Technology MampA and Fundraising Activity and Trends10

Appendix

Selected MampA activity January 2013 ndash August 2014Date Buyer Target Buyer Region Target Region Deal Value ($m) Description

Aug-14 Rocket Fuel [x+1] US US 230 DMP and DSP

Aug-14 Sizmek Aerify US US 6 Mobile tracking amp retargeting

Aug-14 Sprinklr TBG Digital US UK 503 Social ad optimisation

Jul-14 Adknowledge TriVu Media US US na Video ad buying

Jul-14 Facebook LiveRail US US 4501 Video SSP

Jul-14 Rightster Base79 UK UK 83 YouTube audience creation

Jul-14 NetSuite Venda US UK 51 eCommerce platform

Jul-14 Yahoo Flurry US US 2502 Mobile app analytics amp monetisation

Jul-14 LinkedIn Bizo US US 175 B2B marketing platform

Jul-14 Switch Unanimis UK UK na Ad network

Jul-14 Palantir Poptip US US na Social media analytics

Jul-14 Salesforce RelateIQ US US 350 Relationship intelligence

Jul-14 RTL Group SpotXchange Germany US na Video SSP

Jun-14 Twitter TapCommerce US US 1004 Mobile retargeting

Jun-14 Singtel Adconion Singapore US Australia 235 Ad network

May-14 Rakuten DC Storm Japan UK na Tag management amp attribution

May-14 Pubmatic Mocean Mobile US US na Mobile ad server

May-14 Acxiom LiveRamp US US 310 Data on-boarding

May-14 AOL Convertro US US 101 Marketing attribution

May-14 Google Adometry US US 1505 Marketing attribution

Apr-14 Telefonica Mobclix Spain US na Mobile ad exchange

Apr-14 IBM Silverpop US US na Marketing automation

Apr-14 Dunnhumby Sociomantic UK Germany na DSP

Mar-14 IgnitionOne Knotice US US na DMP

Mar-14 Comcast FreeWheel US US 3207 Video ad server

Feb-14 Oracle BlueKai US US 4206 DMP

Jan-14 Opera Mediaworks Hunt Mobile Norway US na Mobile ad network

Dec-13 Oracle Responsys US US 1523 Marketing automation

Nov-13 Centro SiteScout US Canada 40 DSP

Sep-13 Twitter MoPub US US 350 Mobile ad exchange

Aug-13 Millennial Media Jumptap US US 237 Mobile ad network

Aug-13 AOL Adaptv US US 405 Programmatic video platform

Jul-13 Yahoo Admovate US US na Mobile ad targeting

Jun-13 Adobe Neolane US France 617 Marketing automation

Jun-13 Salesforce ExactTarget US US 2616 Marketing automation

Feb-13 Facebook Atlas Advertiser Suite US US na Ad server

1 Deal value estimated between $400 to $500m (TechCrunch)

2 Deal value estimated between $200 to 300m (TechCrunch)3 Deal estimated at under $50m (AdExchanger)

4 Estimated deal value of $100m (Recode)

5 Estimated deal value of $150m (451 Research)6 Estimate deal value of $420m (451 Research)

7 Estimated deal value of $320m (TechCrunch)

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 1112

MampA and Fundraising Activity and Trends Global Advertising and Marketing Technology 11

Appendix

Selected Fundraising activity 2014 YTDDate Lead VC fund Target Target HQ Deal Value ($m) Description

Aug-14 Ignition Partners Xamarin USA 540 Moble app development

Aug-14 Private investors AppNexus USA 600 Ad exchange

Jul-14 Hony Capital Deem USA 500 Customer acquisition and engagement

Jul-14 Comerica mBlox USA 435 Mobile messaging

Jun-14 Softbank Capital IgnitionOne USA 300 Digital marketing suite

Jun-14 SoftBank Capital InsightVenture Partners

Kony USA 500 Moble app development

Jun-14 Deutsche Private Equity Webtrekk Germany 339 Web analytics

Jun-14 Tiger Global Management Freshdesk USA 310 Customer support software

Jun-14 DFJ SiSense Israel 300 Market analysis and business intelligence

Jun-14 SAP Ventures krux digital USA 350 DMP

Jun-14 New Enterprise Associates Elasticsearch Netherlands 700 Marketing analysis ndash search analytics

Jun-14 Insight Venture Partners Yext USA 503 Digital asset and content management

Jun-14 Spring Lake Equity Partners MediaMath USA 735 DSP

May-14 Goldman Sachs The SAVO Group USA 491 Sales enablement platform

May-14 Wellington ManagementCompany

DataLogix Holdings USA 450 DMP

May-14 Index Ventures BitPay USA 300 Bitcoin eCommerce payment

May-14 Pacific Venture Partners ampDream Capital Group

AdSame China 300 Ad server

May-14 Zouk Capital iZettle Sweden 555 Mobile payments

Apr-14 BlackRock New Relic USA 1000 App performance management

Apr-14 Tencent Sequoia Capital Weebly USA 350 Website design amp build

Apr-14 Foundation Capital Adroll USA 700 Retargeting

Apr-14 General Atlantic Squarespace USA 400 Website design amp buildApr-14 Mithril Capital Management SilverRail USA 400 eCommerce platform

Apr-14 Iconiq Capital Sprinklr USA 400 Social media management

Mar-14 Business DevelopmentCorporation of America

CPX Interactive USA 300 DSP Ad network

Mar-14 Redpoint Ventures RelateIQ1 USA 400 Relationship intelligence

Mar-14 FirstHand Technology ValueFund

Phunware USA 307 Mobile app development

Mar-14 Gaorang Capital Avazu China 480 DSP Ad network

Feb-14 Dawn Capital OrderDynamics UK 410 eCommerce platform

Feb-14 Institutional Venture Partners ZEFR USA 300 Brand and content management

Feb-14 SAP Ventures Nokia GrowthPartners Commonfund CapitalGera Ventures

Kaltura USA 470 Online video platform

Jan-14 Insight Venture Partners Ensighten USA 400 Tag management

Jan-14 BlackRock Turn USA 800 DSP

Jan-14 Lead Edge Capital Spredfast USA 325 Social media management

Jan-14 August Capital Integral Ad Science USA 300 Ad quality and valuation

1 Since acquired by Salesforce in July 2014

8102019 m a and Fundraising Activity and Trends 2014

httpslidepdfcomreaderfullm-a-and-fundraising-activity-and-trends-2014 1212

Results International is a leading corporate finance advisor to marketing technology and healthcarecompanies in Europe and has advised on over 250 transactions The Company employs over 40 peopleglobally across offices in London New York and Asia and has a strong track record advising on cross-border

transactions winning MampA Cross Border Deal of the Year in the 2014 MampA Awards

Results Internationalrsquos 2014 AdTech and MarTech Deals

Disclaimer

Results International has compiled this report using data sourced from publicly availablesources and third-party tools to which it holds licensed access Results International doesnot accept any responsibility for the accuracy of the information provided Nor does ResultsInternational accept any liability for any use of the information provided in this report or anyconsequence from its use thereof

Keith Hunt