m-pesa development, operational risk … · 2. m-pesa evolution to a complex and dynamic ecosystem...

TRANSCRIPT

M-PESA DEVELOPMENT, OPERATIONAL RISK MANAGEMENT AND CONSUMER PROTECTION

By Mrs. Anne Mariga

Head National Payments System, Central Bank of Kenya

Innovation on Retail Payment System: Issues, Policies & Challenges

Sheraton Mustika Resort & Spa,

Yogyakarta

November 13-17, 2017

1

Outline

1. Payments System Structure

2. M-Pesa Evolution to a Complex and Dynamic Ecosystem

3. Mobile Payments Landscape – 10 years of Transformation

4. M-Pesa Key Critical Success Factors, Risks & Mitigation Measures and

Consumer Protection

5. Key Outcomes & Lessons Learnt

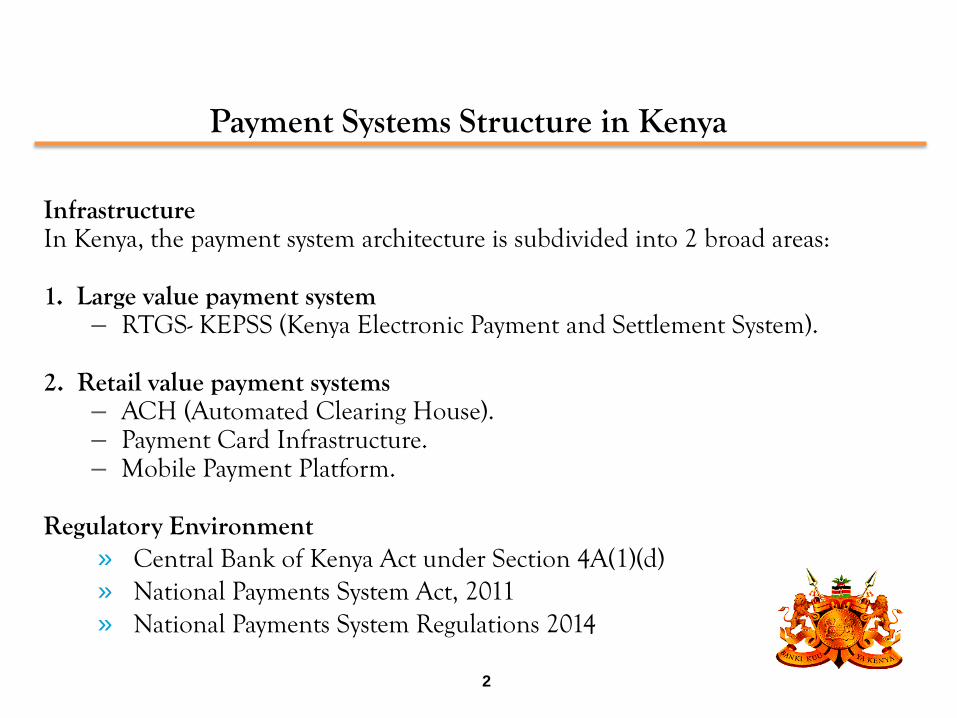

Payment Systems Structure in Kenya

InfrastructureIn Kenya, the payment system architecture is subdivided into 2 broad areas:

1. Large value payment system– RTGS- KEPSS (Kenya Electronic Payment and Settlement System).

2. Retail value payment systems– ACH (Automated Clearing House).– Payment Card Infrastructure.– Mobile Payment Platform.

Regulatory Environment» Central Bank of Kenya Act under Section 4A(1)(d)» National Payments System Act, 2011» National Payments System Regulations 2014

2

Payment systems Structure

Mobile Money moves the highest number of transactions with an average of 4.8 Million per day

KEPSS moves highest value of transactions average of Ksh. 105 Billion (USD 1.01 Billion) daily with a volume of 15, 000 transactions

3

M-PESAMOBILE MONEY TRANSFER SERVICE

4

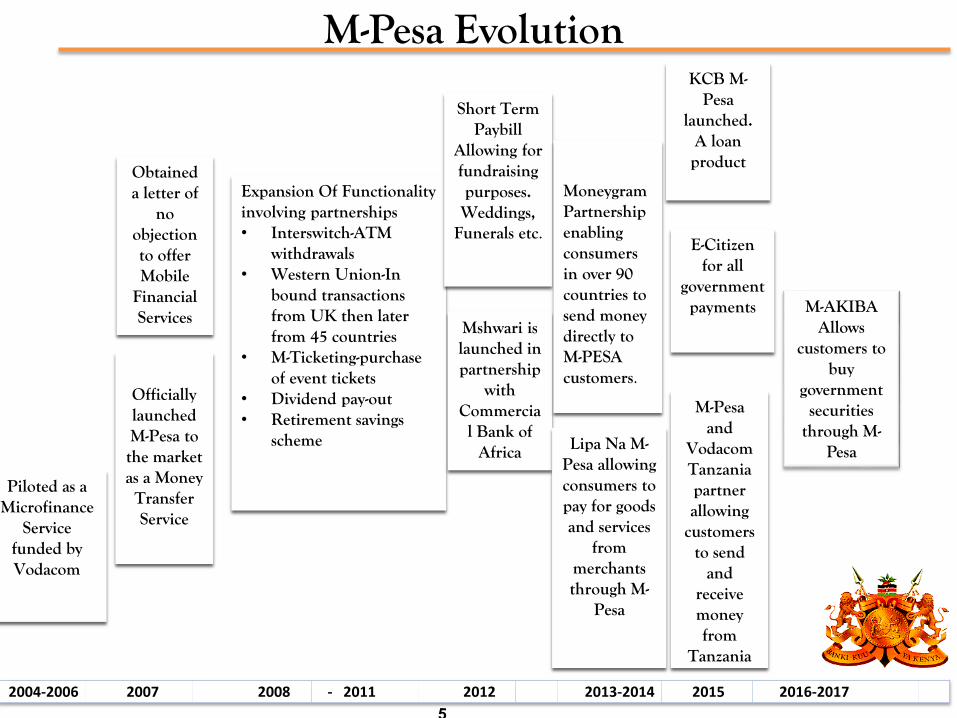

M-Pesa Evolution

2004-2006 2007 2008 - 2011 2012 2013-2014 2015 2016-2017

Piloted as a Microfinance

Service funded by Vodacom

Obtained a letter of

no objection to offer Mobile

Financial Services

Officially launched M-Pesa to the market as a Money

Transfer Service

Expansion Of Functionality involving partnerships• Interswitch-ATM

withdrawals• Western Union-In

bound transactions from UK then later from 45 countries

• M-Ticketing-purchase of event tickets

• Dividend pay-out• Retirement savings

scheme

Mshwari is launched in partnership

with Commercial Bank of

Africa

Short Term Paybill

Allowing for fundraising purposes. Weddings,

Funerals etc.

Lipa Na M-Pesa allowing consumers to pay for goods and services

from merchants through M-

Pesa

MoneygramPartnership enabling consumers in over 90 countries to send money directly to M-PESA customers.

M-Pesaand

Vodacom Tanzania partner allowing

customers to send

and receive money from

Tanzania

KCB M-Pesa

launched. A loan

product

E-Citizenfor all

government payments M-AKIBA

Allows customers to

buy government

securities through M-

Pesa

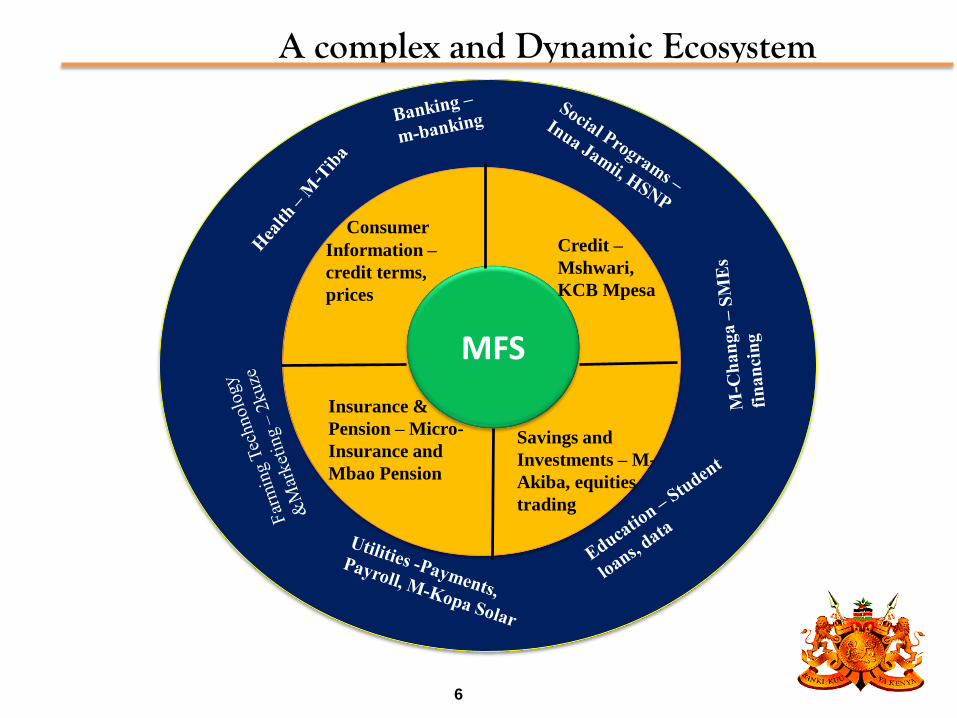

MFS

Credit –

Mshwari,

KCB Mpesa

Savings and

Investments – M-

Akiba, equities

trading

Consumer

Information –

credit terms,

prices

Insurance &

Pension – Micro-

Insurance and

Mbao Pension

A complex and Dynamic Ecosystem

6

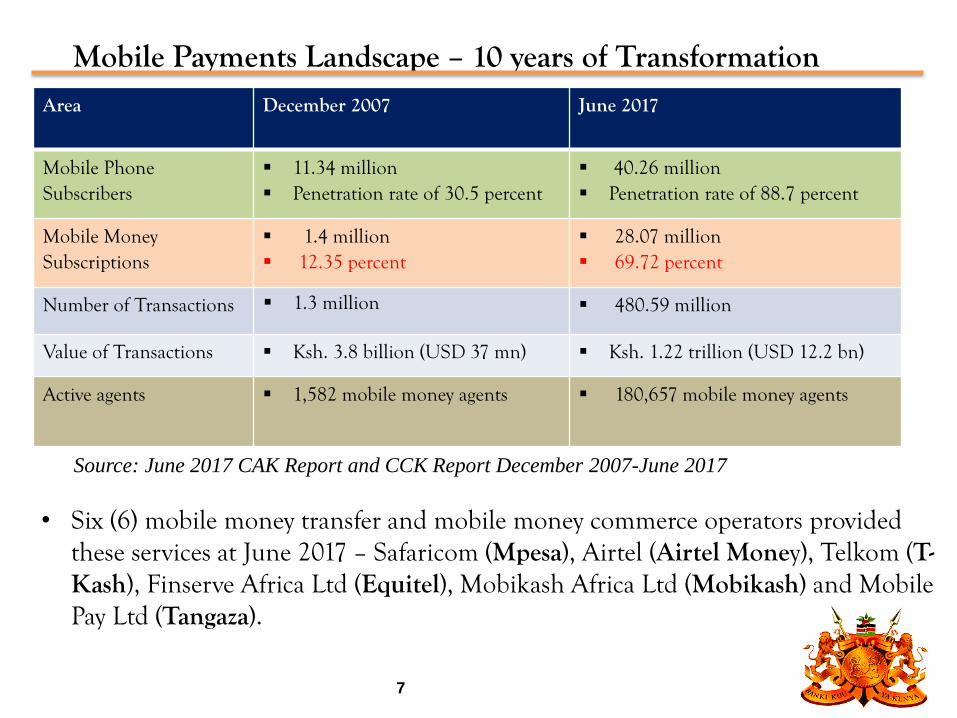

Mobile Payments Landscape – 10 years of Transformation

Source: June 2017 CAK Report and CCK Report December 2007-June 2017

• Six (6) mobile money transfer and mobile money commerce operators provided these services at June 2017 – Safaricom (Mpesa), Airtel (Airtel Money), Telkom (T-Kash), Finserve Africa Ltd (Equitel), Mobikash Africa Ltd (Mobikash) and Mobile Pay Ltd (Tangaza).

Area December 2007 June 2017

Mobile Phone Subscribers

11.34 million Penetration rate of 30.5 percent

40.26 million Penetration rate of 88.7 percent

Mobile Money Subscriptions

1.4 million 12.35 percent

28.07 million 69.72 percent

Number of Transactions 1.3 million 480.59 million

Value of Transactions Ksh. 3.8 billion (USD 37 mn) Ksh. 1.22 trillion (USD 12.2 bn)

Active agents 1,582 mobile money agents 180,657 mobile money agents

7

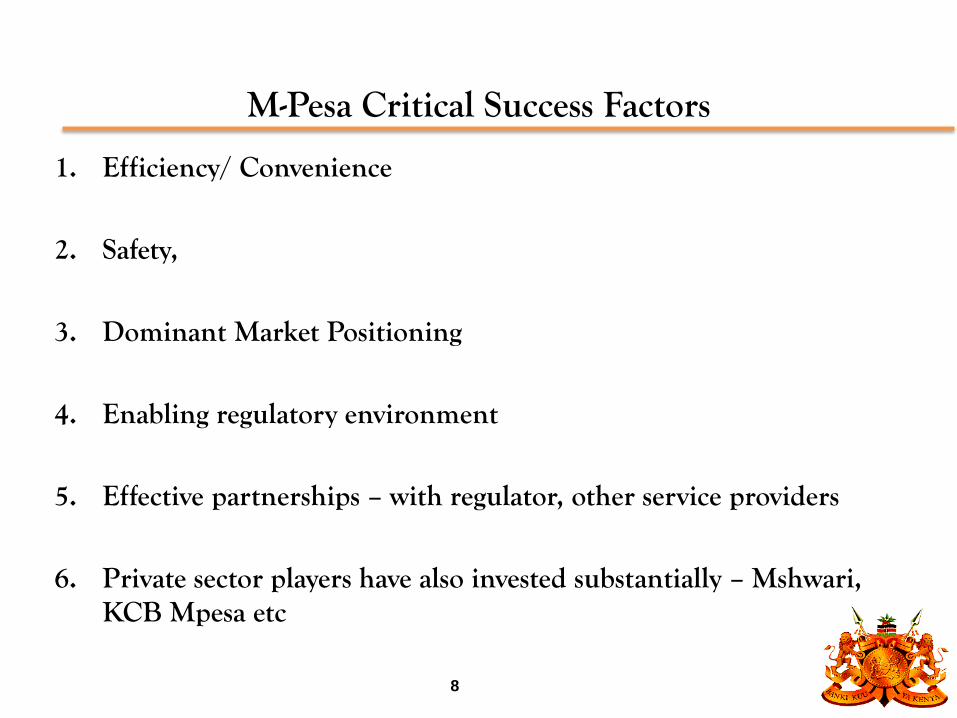

M-Pesa Critical Success Factors

1. Efficiency/ Convenience

2. Safety,

3. Dominant Market Positioning

4. Enabling regulatory environment

5. Effective partnerships – with regulator, other service providers

6. Private sector players have also invested substantially – Mshwari, KCB Mpesa etc

8

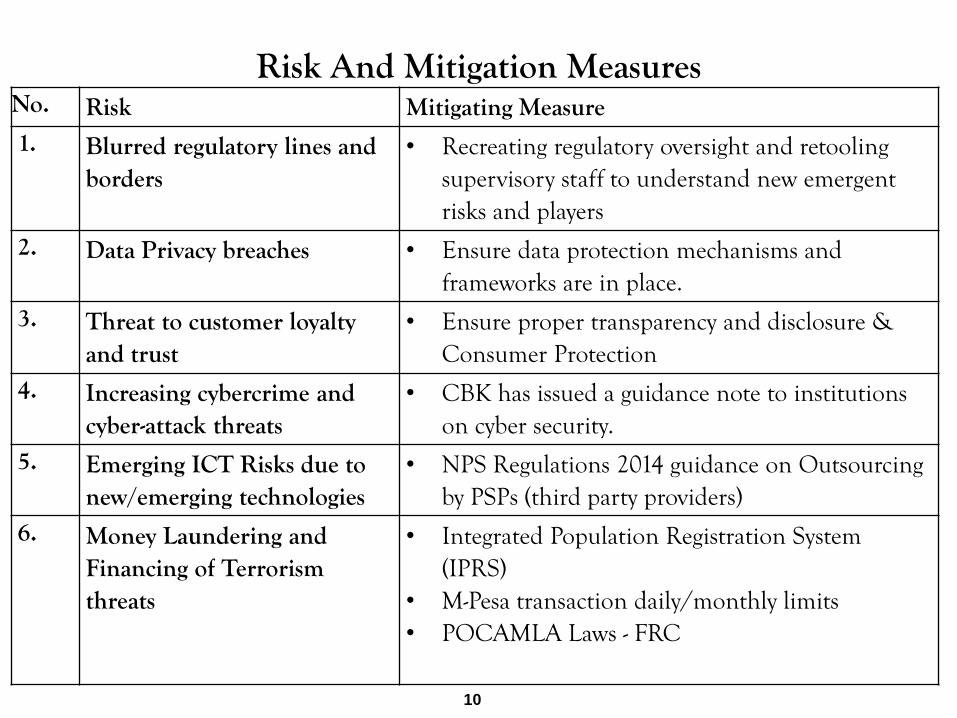

Risk And Mitigation Measures

10

No. Risk Mitigating Measure

1. Blurred regulatory lines and borders

• Recreating regulatory oversight and retooling supervisory staff to understand new emergent risks and players

2. Data Privacy breaches • Ensure data protection mechanisms and frameworks are in place.

3. Threat to customer loyalty and trust

• Ensure proper transparency and disclosure & Consumer Protection

4. Increasing cybercrime and cyber-attack threats

• CBK has issued a guidance note to institutions on cyber security.

5. Emerging ICT Risks due to new/emerging technologies

• NPS Regulations 2014 guidance on Outsourcing by PSPs (third party providers)

6. Money Laundering and Financing of Terrorism threats

• Integrated Population Registration System (IPRS)

• M-Pesa transaction daily/monthly limits• POCAMLA Laws - FRC

Consumer Protection

Mobile Money Transfer Platforms/Operators are required to;

Resolve all complaints within thirty days of being filed within laid out procedures in the NPS Regulations 2014.

Disclose of all fees to the sender and to the recipient.

Information on any system upgrades and accompanying downtime

Enable refund and cancellation of transactions in case of error. (Refunds only possible if money not cashed out.)

11

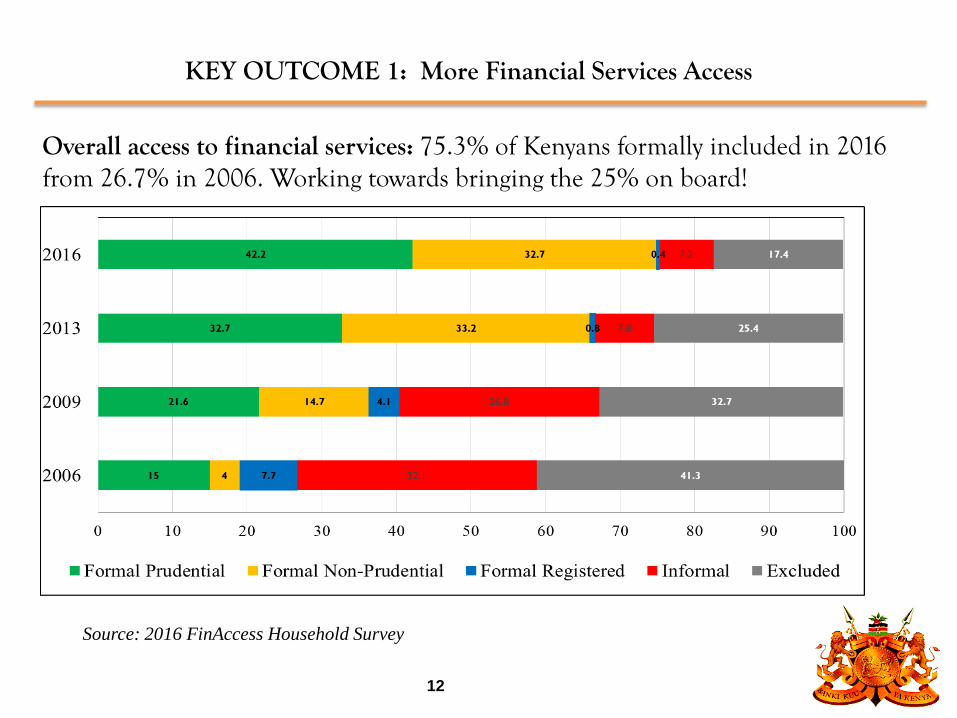

Overall access to financial services: 75.3% of Kenyans formally included in 2016 from 26.7% in 2006. Working towards bringing the 25% on board!

Source: 2016 FinAccess Household Survey

KEY OUTCOME 1: More Financial Services Access

12

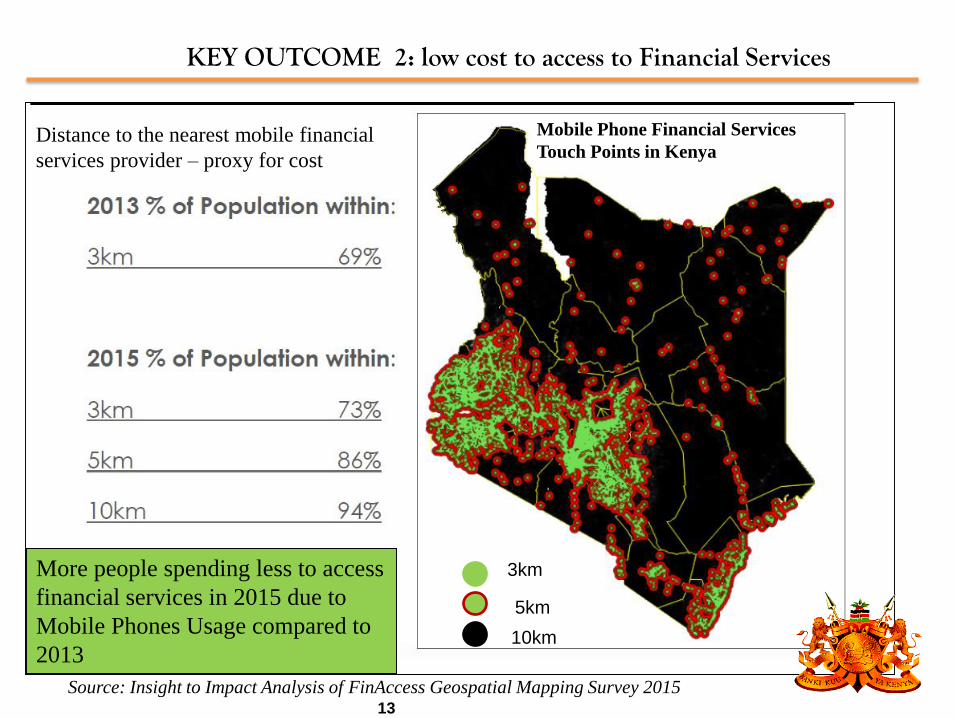

KEY OUTCOME 2: low cost to access to Financial Services

Source: Insight to Impact Analysis of FinAccess Geospatial Mapping Survey 2015

More people spending less to access

financial services in 2015 due to

Mobile Phones Usage compared to

2013

3km

5km

10km

Mobile Phone Financial Services

Touch Points in KenyaDistance to the nearest mobile financial

services provider – proxy for cost

13

Low cost of financial services access

Cost to Population to the nearest Financial Service Access Point: 2013 Vs. 2016 (%)

82,1

11,16.2

0,6

89,9

4,3 5.10,7

0

10

20

30

40

50

60

70

80

90

100

Less than KSh 50 KSh 51-100 Between KSh 101

and KSh 500

Above KSh 500

PE

RC

EN

TA

GE

2013 2016

• About 94% of Kenyans pay less than USD 1.00 to Access Financial Services

14

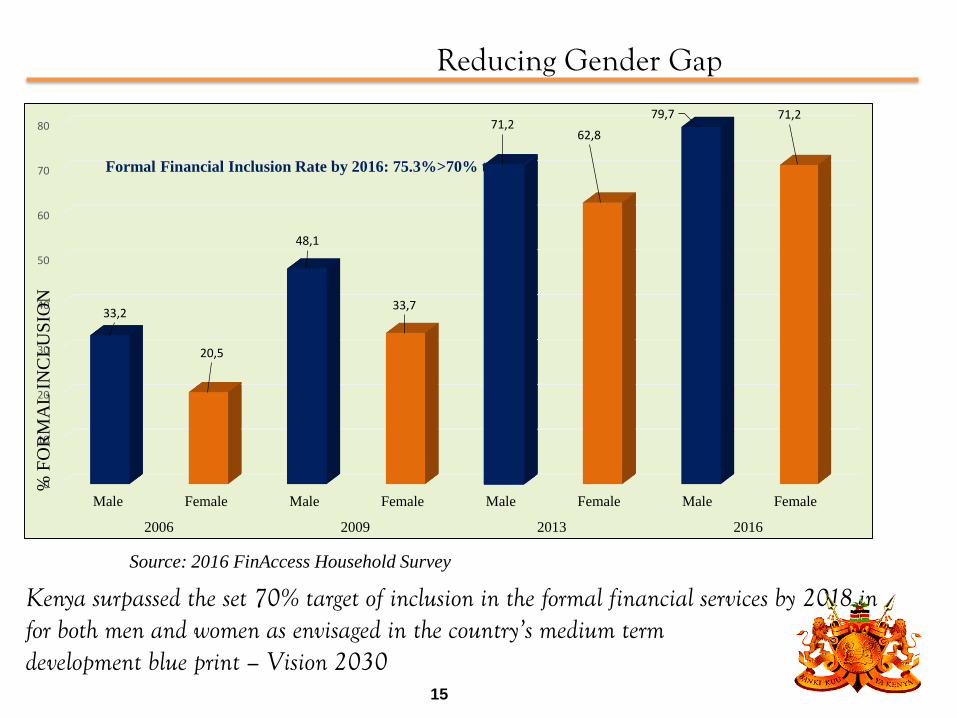

Reducing Gender Gap

0

10

20

30

40

50

60

70

80

Male Female Male Female Male Female Male Female

2006 2009 2013 2016

33,2

20,5

48,1

33,7

71,262,8

79,7 71,2

% F

OR

MA

L I

NC

LU

SIO

N

Kenya surpassed the set 70% target of inclusion in the formal financial services by 2018 in for both men and women as envisaged in the country’s medium term development blue print – Vision 2030

Source: 2016 FinAccess Household Survey

Formal Financial Inclusion Rate by 2016: 75.3%>70% target

15

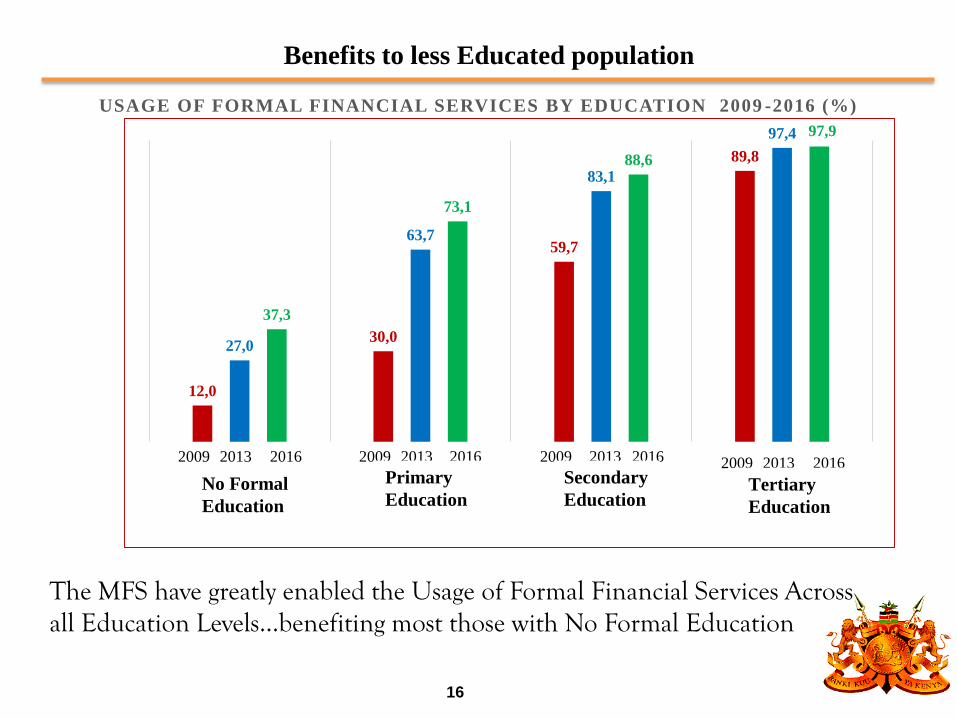

Benefits to less Educated population

The MFS have greatly enabled the Usage of Formal Financial Services Across all Education Levels…benefiting most those with No Formal Education

12,0

30,0

59,7

89,8

27,0

63,7

83,1

97,4

37,3

73,1

88,6

97,9

2009 2009200920092013 2013201320132016 201620162016

Secondary

EducationTertiary

Education

Primary

EducationNo Formal

Education

USAGE OF FORMAL FINANCIAL SERVICES BY EDUCATION 2009 -2016 (%)

16

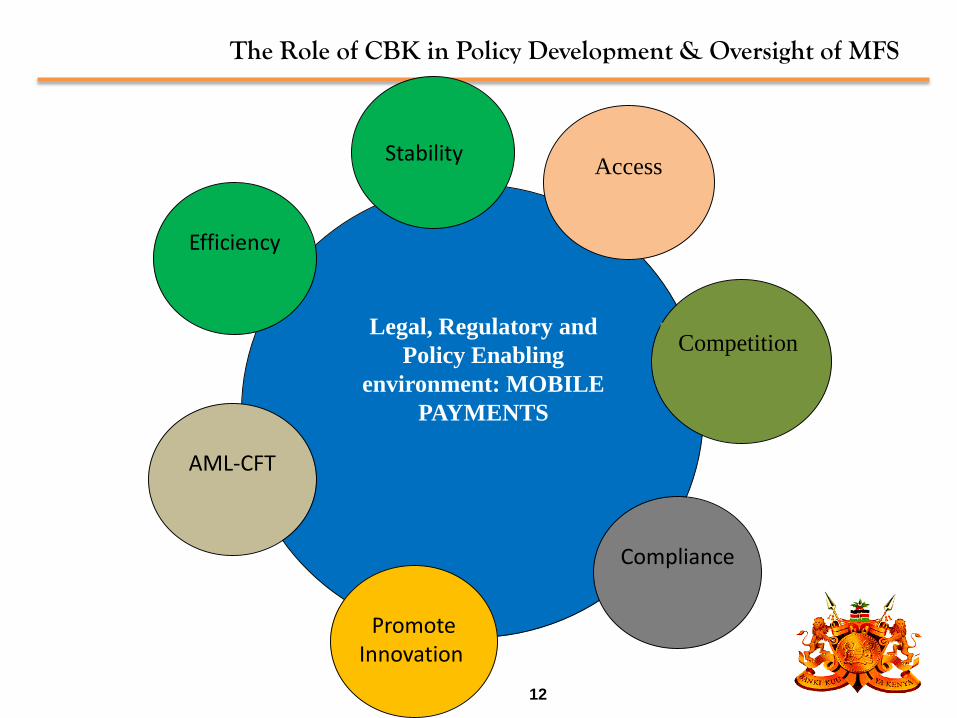

The Role of CBK in Policy Development & Oversight of MFS

Efficiency

AML-CFT

Promote Innovation

Compliance

Competition

Access

Legal, Regulatory and

Policy Enabling

environment: MOBILE

PAYMENTS

Stability

12

Lessons Learnt

• Regulatory objectives remain the same; enhance market confidence and safeguard stability of the financial system. However, we must balance stability and inclusion goals to support innovation.

• As regulators we should work alongside innovators so as to understand and facilitate these innovations

• Regulatory frameworks should be robust and balanced, dynamic across time and space, to support the provision of sustainable digital financial services to users and to guarantee the stability of the overall financial system.

17

Lessons Learnt Cont….

• Continuous application of the ‘‘Test and learn’’ model to keep up with the rapidly changing environment to ensure:

– Establishment of resilient and viable business models and ecosystems

– Enhanced corporate governance practices– Improved transparency– Management of emerging technology and emerging inherent

risks.

• Consumer protection in the face of innovations must be given attention deservedly

18

19

Q&A

THANK YOU